Pompe Disease Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

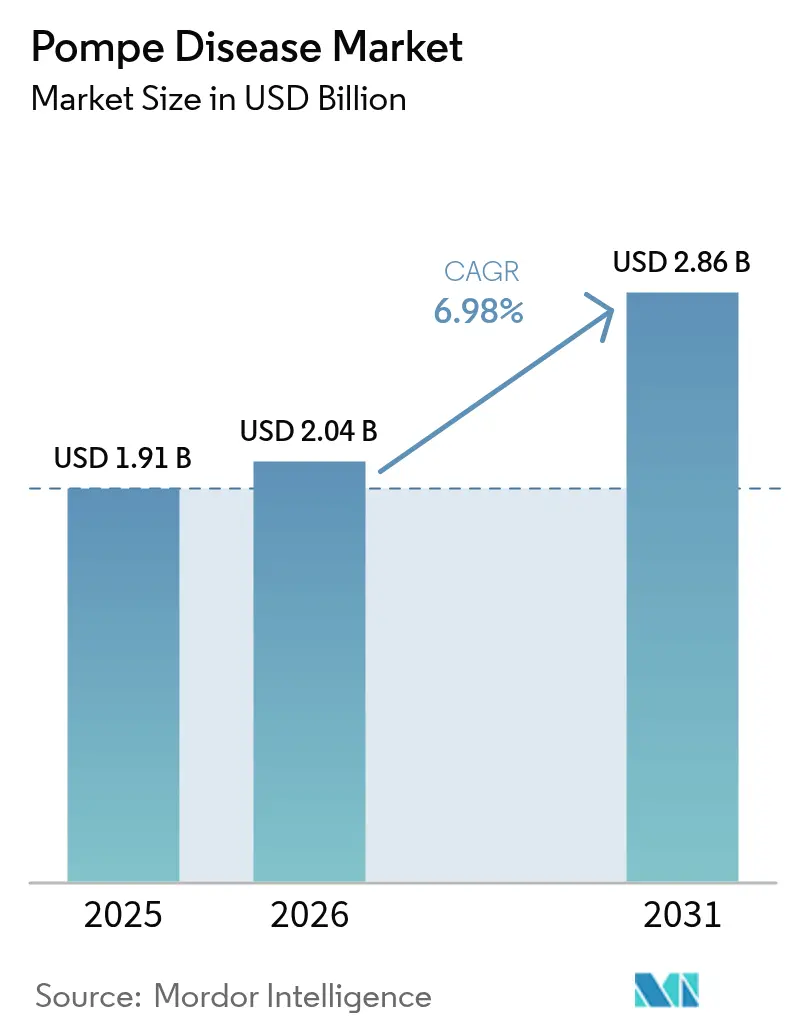

| Market Size (2026) | USD 2.04 Billion |

| Market Size (2031) | USD 2.86 Billion |

| Growth Rate (2026 - 2031) | 6.98% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pompe Disease Market Analysis by Mordor Intelligence

Pompe Disease Market size in 2026 is estimated at USD 2.04 billion, growing from 2025 value of USD 1.91 billion with 2031 projections showing USD 2.86 billion, growing at 6.98% CAGR over 2026-2031.

Uptake is shifting from single-agent enzyme replacement therapy (ERT) toward next-generation ERTs, combination regimens, and investigational gene and mRNA platforms, broadening therapeutic choice while sustaining double-digit revenue growth from new launches. Accelerating newborn screening mandates, especially in the Asia-Pacific region, have revealed disease prevalence far higher than earlier estimates, strengthening the commercial case for early intervention and lifelong therapy. Investment has intensified across the value chain, with sponsors committing hundreds of millions of dollars to secure manufacturing capacity for viral vectors and second-generation recombinant enzymes, ensuring supply resilience and de-risking launch timelines. At the same time, payers in the United States and Europe are tightening value-based reimbursement criteria, prompting developers to generate real-world evidence that links higher up-front prices to demonstrable functional gains and longer-term cost offsets. Competitive intensity is rising as Sanofi defends its incumbency while Amicus Therapeutics, Shionogi, and several gene-therapy specialists deploy capital to capture emerging opportunity niches across infantile-onset and late-onset disease segments.

Key Report Takeaways

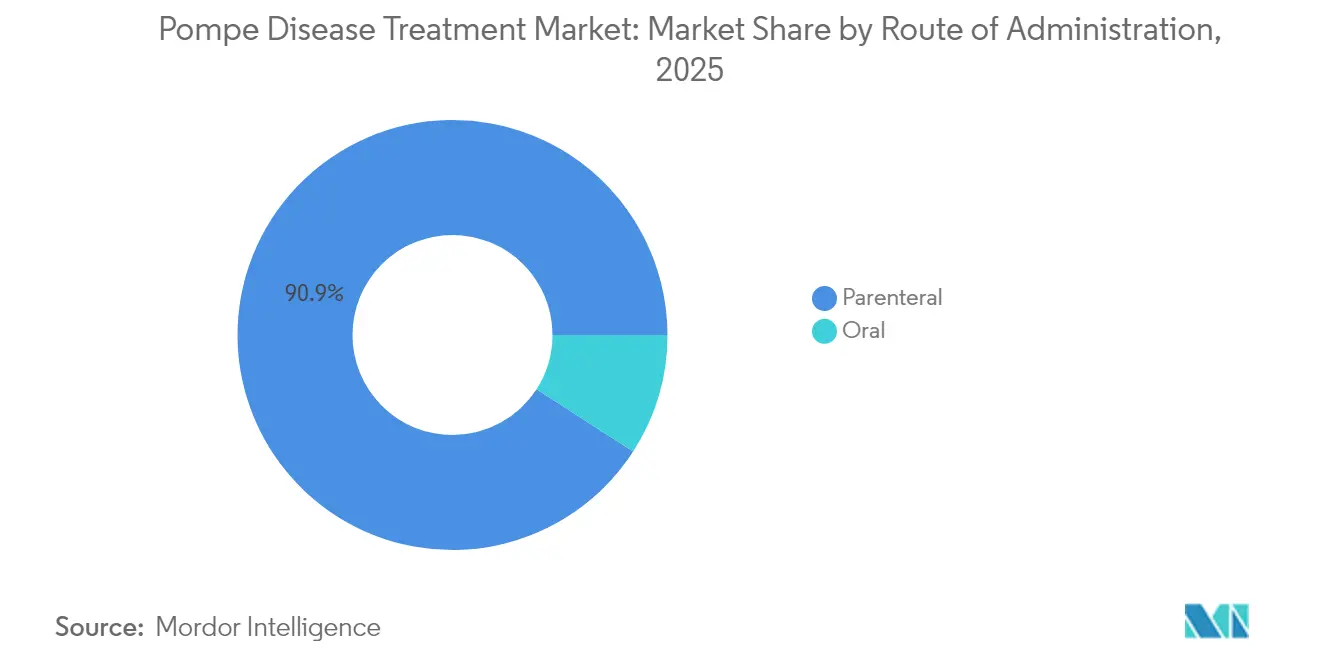

- By route of administration, parenteral products led with 90.88% of the pompe disease market share in 2025, while oral candidates are projected to post an 8.25% CAGR through 2031.

- By therapy type, enzyme replacement therapy retained 89.75% share of the pompe disease market size in 2025; combination therapy is forecast to grow at 8.55% CAGR to 2031.

- By disease onset, late-onset cases accounted for 68.22% of the pompe disease market size in 2025, whereas infantile-onset treatments are advancing at a 9.12% CAGR.

- By distribution channel, hospital pharmacies held 56.10% revenue share in 2025, yet online pharmacies show the fastest rise at 8.78% CAGR to 2031.

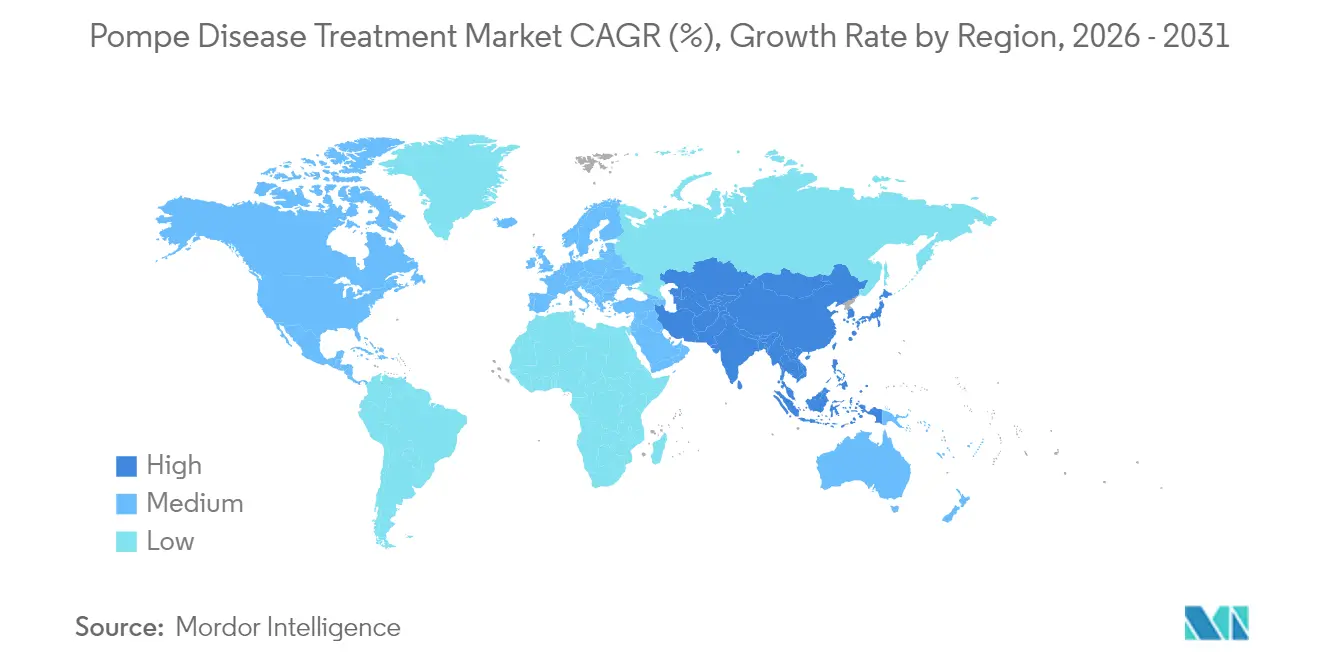

- Geographically, North America commanded 46.20% of pompe disease market share in 2025, while Asia-Pacific is expanding at a 9.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pompe Disease Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Launch of novel second-generation ERTs | +2.1% | Global; early uptake in North America & EU | Medium term (2-4 years) |

| Expanding newborn screening mandates | +1.8% | Global; rapid rollout in Asia-Pacific | Long term (≥ 4 years) |

| mRNA-based ERT platforms in trials | +1.2% | North America & EU | Long term (≥ 4 years) |

| China’s rare-disease reimbursement acceleration | +0.9% | Asia-Pacific core markets | Medium term (2-4 years) |

| Gene-therapy funding surge | +0.7% | Global; capital concentrated in developed markets | Long term (≥ 4 years) |

| Global orphan-drug incentives | +0.6% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Launch of Novel Second-Generation ERTs

Second-generation enzymes such as cipaglucosidase alfa, launched in combination with miglustat, improve mannose-6-phosphate tagging and cellular uptake, delivering greater glycogen clearance in skeletal muscle and demonstrating superior patient-reported outcomes versus legacy alglucosidase alfa. Europe’s early designation of the regimen as preferred therapy for adults with late-onset disease signals traction beyond the United States, while Amicus projects more than USD 1 billion in cumulative revenue by 2028. Market enthusiasm is reinforced by regulatory flexibility under orphan-drug frameworks that shorten review cycles and extend exclusivity, encouraging other sponsors to prioritise enhanced ERT constructs.

Expanding Newborn Screening Mandates

Genomics-first screening programmes in China, Japan, and several US states detect Pompe disease at markedly higher rates than enzyme-activity assays, with Chinese pilots reporting overall lysosomal prevalence of 1 in 1,512 births. Earlier identification drives pre-symptomatic treatment, especially for infantile-onset cases where rapid cardiac and respiratory decline can be prevented. Governments are embedding Pompe panels into national screening catalogues, extending reimbursement and stimulating sustained uptake that underpins long-run prescription volume growth.

mRNA-Based ERT Platforms in Clinical Trials

Proof-of-concept data for mRNA-3927 in propionic acidemia, showing a 70% reduction in metabolic crises, validate lipid-nanoparticle delivery of messenger RNA as a modality for endogenous enzyme production. Translational programmes for Pompe disease target hepatocytes to secrete functional acid alpha-glucosidase, potentially enabling once-monthly dosing or even self-administration. Manufacturing scalability mirrors COVID-19 vaccine platforms, suggesting meaningful cost-of-goods reductions relative to complex recombinant enzymes.

Gene-Therapy Funding Surge

More than USD 1.5 billion in venture and strategic capital flowed into Pompe AAV projects during 2024–2025 as developers move SPK-3006, AT845, and other candidates into registrational studies. Investments include Astellas’ USD 100 million vector facility in North Carolina to secure clinical and early commercial supply.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High therapy cost | −1.4% | Global; acute in emerging markets | Short term (≤ 2 years) |

| Delayed diagnosis & low awareness | −0.8% | Global; resource-limited settings | Medium term (2-4 years) |

| Viral-vector manufacturing bottlenecks | −0.6% | Developed markets | Medium term (2-4 years) |

| Value-based pricing pressure | −0.4% | North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Therapy Cost

Annual per-patient spending of EUR 483,907 in Germany positions Pompe as the costliest lysosomal disorder, with 98.5% attributable to drug acquisition.[1]H. K. Miebach, “Economic Burden of Lysosomal Storage Disorders in Germany,” Orphanet Journal of Rare Diseases, ojrd.biomedcentral.com Although orphan-drug policy supports premium pricing, payers now demand hard outcomes data before granting full reimbursement, prolonging negotiations and delaying broad launch roll-outs, particularly for combination and gene-therapy entrants.

Delayed Diagnosis & Low Awareness

Late-onset cases often mimic muscular dystrophy, extending diagnostic odysseys that postpone therapy for years and compress potential treatment windows. Artificial-intelligence algorithms applied to electronic health-record datasets show promise in flagging suspect phenotypes, but adoption outside academic centres remains limited, maintaining under-diagnosis in rural and low-income regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Route of Administration: Parenteral Dominance Drives Innovation

Parenteral products accounted for 90.88% of the Pompe disease market in 2025, resulting in a market size of USD 1.74 billion and a 6.25% CAGR, driven by the advancement of improved enzyme constructs into the clinic. Intravenous delivery benefits from decades of clinician familiarity, mature specialty-pharmacy logistics, and proven clinical benefit in stabilising respiratory and ambulatory function. Avalglucosidase alfa exemplifies formulation innovation, incorporating bis-phosphorylated mannose-6-phosphate tags that enhance muscle uptake and facilitate longer infusion intervals. Temperature-controlled distribution advances keep product wastage below 1% and maintain an on-time delivery rate of 98%, further solidifying the parenteral model.

Oral administration remains a nascent but strategically important approach. Maze Therapeutics’ MZE-001, an oral glycogen-synthase inhibitor, underpins Sanofi’s USD 750 million acquisition and Shionogi’s USD 150 million licensing pact, reflecting the conviction that a convenient daily pill can complement or even displace biweekly infusions. If Phase II data confirm glycogen-reduction biomarkers, the Pompe disease industry could see a bifurcated treatment algorithm, wherein patients transition from parenteral ERT to oral substrate-reduction maintenance, altering the revenue mix and logistical demands.

By Therapy Type: ERT Leadership Faces Combination Challenge

Enzyme replacement therapy generated 89.75% of 2025 revenue, equal to a Pompe disease market size of USD 1.71 billion, but its share is projected to decline modestly as combination regimens scale. Clinicians continue to rely on alglucosidase alfa and avalglucosidase alfa due to extensive long-term safety data and reimbursement familiarity. However, the FDA approval of cipaglucosidase alfa plus miglustat heralds a paradigm shift: Amicus reported 90% year-over-year revenue growth in Q1 2025 as treatment-experienced patients switched to the combination following improved six-minute-walk test scores.

Gene and mRNA therapies populate the “other” category and may compress the ERT window of dominance. A single-administration AAV vector or once-monthly mRNA injection could reshape adherence patterns, particularly for younger cohorts. Developers must nonetheless clear manufacturing and immunogenicity hurdles before large-scale commercialisation.

By Disease Onset Type: LOPD Dominance Masks IOPD Innovation

Late-onset Pompe disease (LOPD) contributed 68.22% of 2025 revenue, reflecting both higher prevalence and longer treatment duration. Although growth will persist, forecast models allocate a 9.12% CAGR to infantile-onset Pompe disease (IOPD) through 2031, lifting its revenue share as prenatal and newborn interventions scale. The PEARL trial’s in-utero ERT seeks to induce immune tolerance, potentially eliminating antibody-mediated reduction in drug efficacy. If successful, infant survival and neuro-motor outcomes could improve dramatically, prompting guideline changes and further enlarging the addressable patient pool.

For LOPD, data confirm that treatment initiation within two years of first symptom extends ventilator-free survival by more than five years relative to later starts. Consequently, payer policies increasingly reimburse genetic testing for adults with unexplained proximal muscle weakness, leading to higher diagnostic yield and steady patient flow into specialist centres.

By Distribution Channel: Hospital Pharmacies Lead Digital Transformation

Hospital pharmacies controlled 56.10% of 2025 sales, driven by infusion centre infrastructure, multidisciplinary care teams, and stringent quality control protocols that are essential for biologics with narrow stability ranges. Their share is expected to taper slightly as online pharmacies capture digitally savvy patient segments; however, absolute revenue from hospitals will rise in tandem with the overall Pompe disease market expansion. Large networks, such as Accredo, leverage predictive cold-chain analytics to achieve 99% dispensing accuracy, thereby reinforcing clinician trust.

E-pharmacy platforms are projected to record a 8.78% CAGR, supported by hybrid care models that bundle telehealth consultations, remote spirometry, and home delivery of infusion supplies. Retail giants are investing in dedicated rare-disease hubs, diversifying access points, and alleviating travel burdens on patients residing far from tertiary centres. Limited distribution agreements nevertheless confine volume to fewer than 10 accredited pharmacies, preserving stringent oversight and minimising counterfeit risk.

Geography Analysis

North America anchored 46.20% of 2025 sales, equivalent to USD 0.88 billion, reflecting robust payer coverage, active newborn screening across all US states, and early-adopter behaviour among neuromuscular specialists. The region also captures the majority of ongoing phase III gene-therapy trials, supported by deep capital markets and an experienced contract-manufacturing ecosystem. Policy shifts such as Inflation Reduction Act price negotiations inject uncertainty but are unlikely to undermine high clinical value assessments for life-threatening rare diseases.

Europe constitutes the second-largest regional block, characterised by a harmonised regulatory pathway through the European Medicines Agency yet fragmented reimbursement decision-making at the member-state level. Western European nations generally fund Pompe ERT within three months of marketing authorisation, whereas many Central and Eastern European markets lag by more than two years, creating intra-regional access disparities. Industrial commitments such as Roche’s EUR 90 million gene-therapy site in Germany and UCB’s EUR 200 million enzyme facility in Belgium reflect growing confidence that Europe will remain a profitable launch region despite rising health-technology-assessment scrutiny.

Asia-Pacific registers the fastest trajectory at 9.02% CAGR. China’s mandatory genomic newborn screening yielded incidence data that immediately expanded the diagnosed population and triggered policy moves to subsidise ERT. Japan’s Pharmaceuticals and Medical Devices Agency maintains an expedited 9-month median review cycle for orphan drugs, with seven years of exclusivity, incentivising sponsors to submit global dossiers early. Meanwhile, Australia and South Korea have added avalglucosidase alfa to national reimbursement schedules, signalling broader regional integration of next-generation therapies. Supply-chain investments, including local fill-finish capacity, mitigate import-related delays and lower landed costs, fostering sustainable volume growth.

Competitive Landscape

Market concentration remains high, with Sanofi, Amicus Therapeutics, and a handful of other companies collectively controlling majority of the global market revenue. Sanofi’s historical leadership is rooted in first- and second-generation ERT franchises producing stable annual cash flow. Amicus accelerated share capture by launching the first approved combination regimen and expects global availability in at least 20 countries by end-2025, supported by robust post-marketing data packages.

Strategic transactions underscore the premium placed on differentiated mechanisms. Sanofi outbid peers with a USD 750 million cash purchase of Maze Therapeutics’ oral glycogen-synthase programme, while Shionogi simultaneously secured worldwide rights for USD 150 million upfront plus milestones, effectively cornering parallel development paths for the same asset class.[3]Shionogi & Co. Ltd., “Global License for MZE-001 Glycogen Synthase Inhibitor,” shionogi.comSuch deals reveal intense competition for promising pipeline assets capable of offsetting pressure on mature ERT portfolios.

Distribution is concentrated as well. Fewer than 10 specialty pharmacies manage roughly 80% of infused Pompe therapies, granting them leverage in formulary negotiations and patient-support contracting. Yet this concentration expedites the diffusion of innovation; once a new product secures a limited-distribution agreement, nationwide hospital networks can switch patients within weeks, compressing the typical post-launch uptake curve.

Pompe Disease Industry Leaders

Amicus Therapeutics

Sanofi

Exerkine Corporation

Genethon

Maze Therapeutics, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Amicus Therapeutics reported Q1 2025 revenue of USD 125.2 million with 90% year-over-year growth for Pombiliti + Opfolda, guided to GAAP profitability in H2 2025 and confirmed launches in up to 10 new countries during 2025.

- May 2024: Shionogi licensed Maze Therapeutics’ MZE-001 oral substrate-reduction therapy for USD 150 million upfront; the FDA granted orphan-drug designation, expediting development.

- April 2024: Sanofi presented Mini-COMET study data showing avalglucosidase alfa improved ptosis in paediatric infantile-onset Pompe patients, reinforcing second-generation ERT benefits.

- September 2023: The FDA approved Pombiliti (cipaglucosidase alfa-atga) plus Opfolda (miglustat) for adults with late-onset Pompe disease inadequately controlled on standard ERT.

Global Pompe Disease Market Report Scope

As per the scope of the report, Pompe disease, also known as glycogen storage disease type II disorder, is an autosomal recessively inherited metabolic disorder caused by glycogen accumulation in the lysosome. Pompe disease is a rare (estimated at 1 in every 40,000 births), inherited, and often fatal condition that disables the heart and skeletal muscles. It is caused by mutations in a gene that makes an enzyme called acid alpha-glucosidase (GAA). The Pompe Disease Market is segmented by Route of Administration (Oral and Parenteral), Treatment Type (Substrate Reduction Therapy (SRT), Enzyme Replacement Therapy (ERT), and Others), End User (Hospitals, Ambulatory Surgery Centers, and Others), and Geography (North America, Europe, Asia Pacific, the Middle East and Africa, and South America). The report offers the value (in USD million) for the above segments. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report assigns a value of (USD million) to the aforementioned segments.

| Oral |

| Parenteral |

| Enzyme Replacement Therapy (ERT) |

| Combination Therapy |

| Other Therapies |

| Infantile-Onset Pompe Disease (IOPD) |

| Late-Onset Pompe Disease (LOPD) |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Route of Administration | Oral | |

| Parenteral | ||

| By Therapy Type | Enzyme Replacement Therapy (ERT) | |

| Combination Therapy | ||

| Other Therapies | ||

| By Disease Onset Type | Infantile-Onset Pompe Disease (IOPD) | |

| Late-Onset Pompe Disease (LOPD) | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and projected growth of the Pompe disease market?

The market reached USD 2.04 billion in 2026 and is expected to expand to USD 2.86 billion by 2031, delivering a 6.98% CAGR.

Which therapy type currently leads global revenue?

Enzyme replacement therapy (ERT) generated 89.75% of 2025 revenue, underlining its continuing dominance despite emerging combination and gene-therapy options.

Which geographic region shows the fastest growth?

Asia-Pacific posts the highest trajectory at a 9.02% CAGR through 2031, propelled by newborn genomic screening and wider rare-disease reimbursement.

How significant are therapy costs and related pricing pressures?

Average annual spending can reach EUR 483,907 (USD 523,000) per patient in Germany, prompting US and EU payers to intensify value-based pricing scrutiny.

Page last updated on: