Systemic Lupus Erythematosus Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

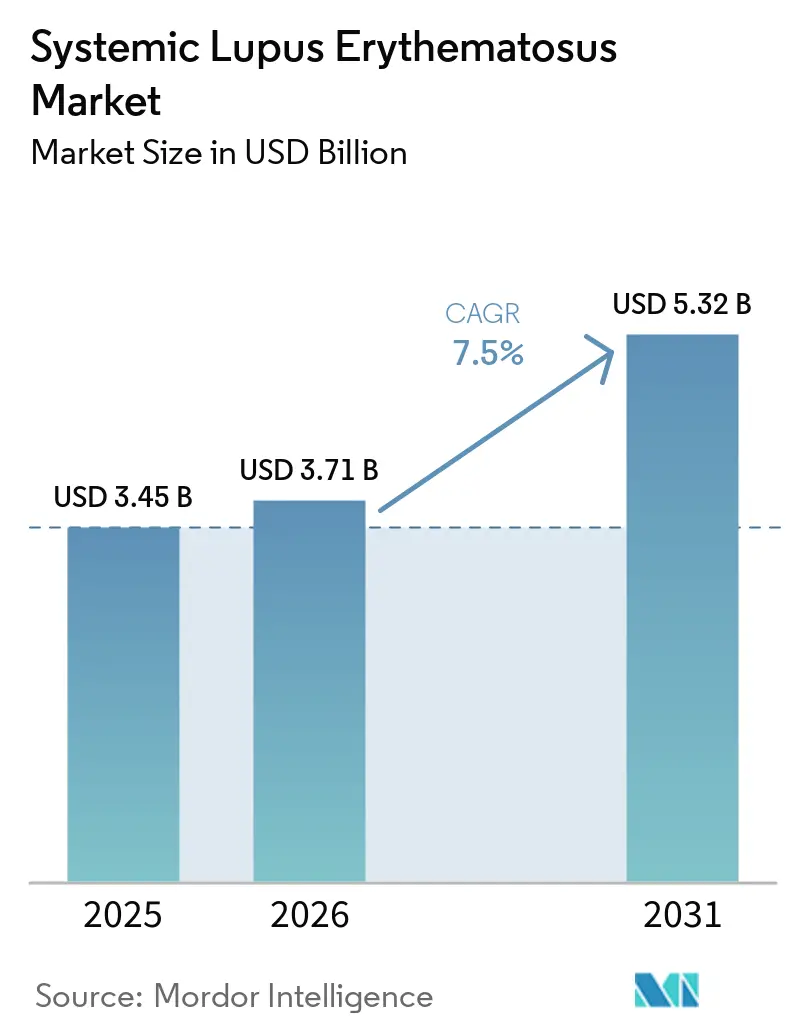

| Market Size (2026) | USD 3.71 Billion |

| Market Size (2031) | USD 5.32 Billion |

| Growth Rate (2026 - 2031) | 7.50% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Systemic Lupus Erythematosus Market Analysis by Mordor Intelligence

The Systemic Lupus Erythematosus Market size is expected to grow from USD 3.45 billion in 2025 to USD 3.71 billion in 2026 and is forecast to reach USD 5.32 billion by 2031 at 7.5% CAGR over 2026-2031.

Growth is fueled by the maturation of precision-medicine diagnostics, accelerated biologic approvals, and the first wave of cell-based therapeutics that directly modulate disease drivers. Regulatory agencies are expanding use of breakthrough and fast-track pathways, compressing development timelines and incentivizing early-stage investments. Venture capital inflows topped USD 500 million in 2024 for autoimmune platforms, while global manufacturing expansions exceeding USD 8 billion signal long-term confidence in complex biologics and cell therapies. Companion-diagnostic adoption is simultaneously expanding the eligible patient pool and refining treatment selection, reinforcing a virtuous cycle of value-based reimbursement.

Key Report Takeaways

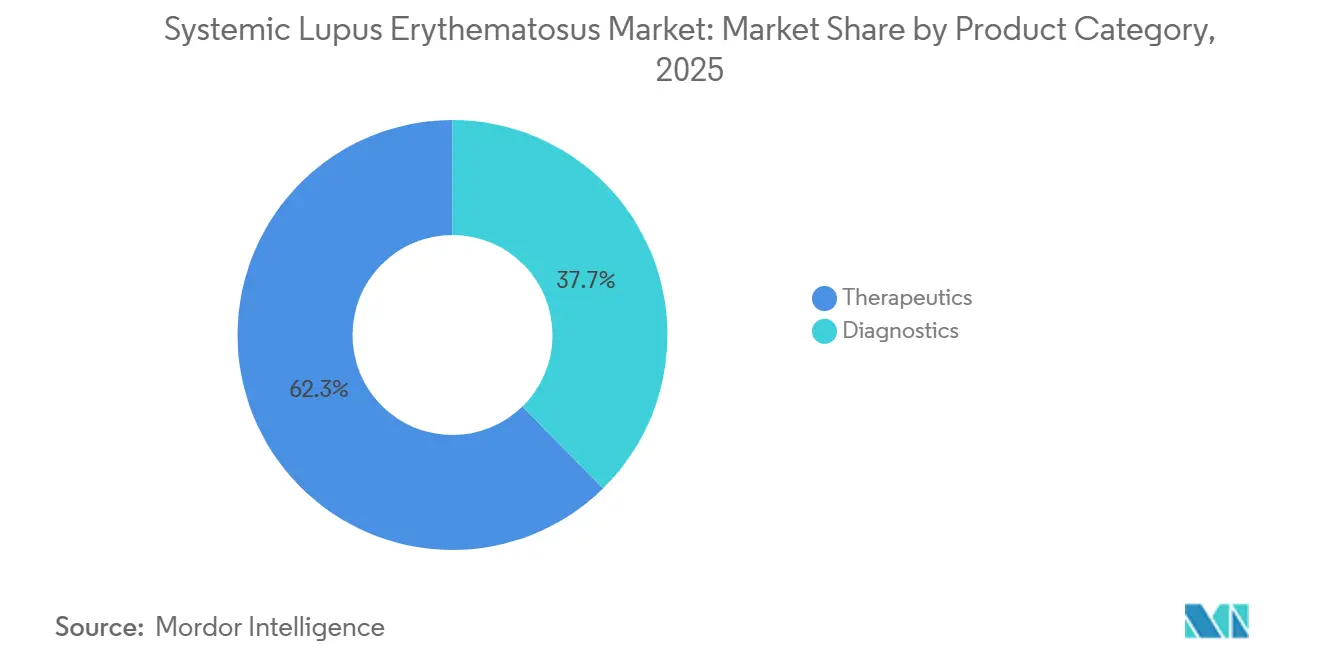

- By product category, diagnostics held 37.66% of systemic lupus erythematosus market share in 2025, while therapeutics trailed in growth; diagnostics are projected to expand at an 8.45% CAGR through 2031.

- By route of administration, the intravenous segment captured 51.43% of the systemic lupus erythematosus market size in 2025, but oral formulations are projected to grow at 8.60% CAGR through 2031.

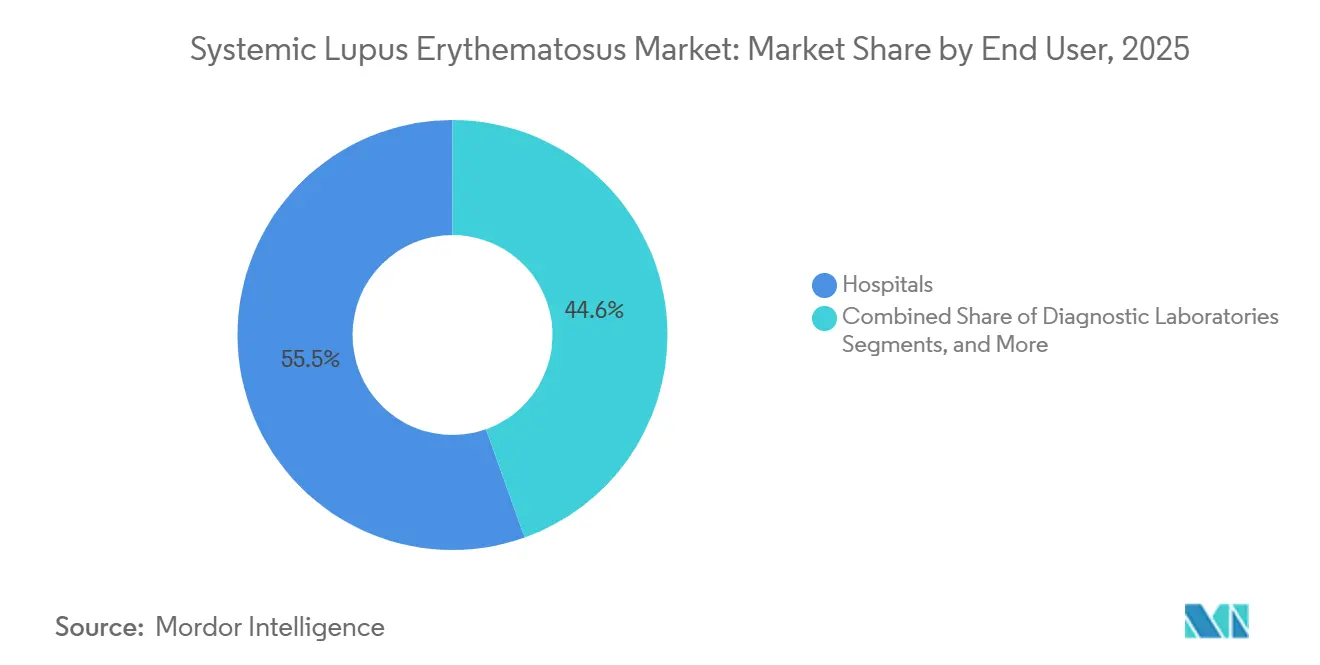

- By end user, hospitals accounted for a 55.45% share of the systemic lupus erythematosus market size in 2025; diagnostic is projected to grow at a 7.95% CAGR to 2031.

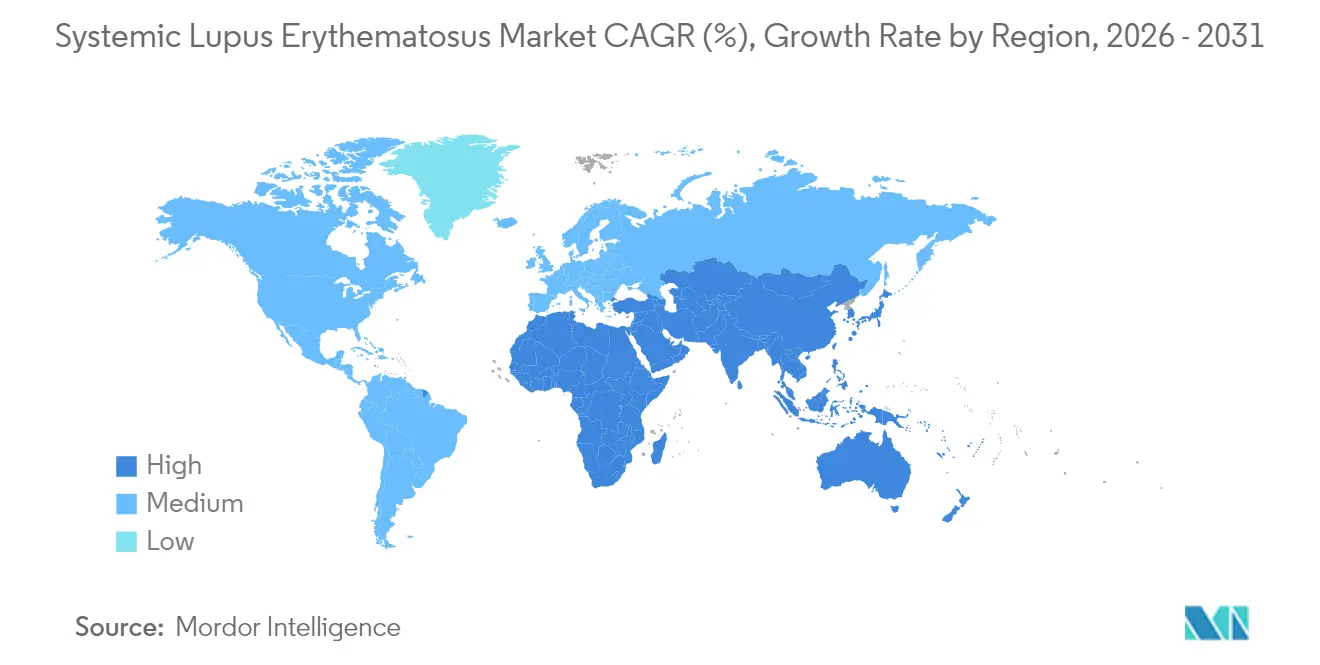

- By geography, North America led with 39.34% systemic lupus erythematosus market share in 2025, while Asia-Pacific is projected to grow at an 8.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Systemic Lupus Erythematosus Market*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising prevalence of SLE & earlier diagnosis | 1.5% | Global, with acute rises in Asia-Pacific and North America | Medium term (2-4 years) |

| FDA approvals of novel biologics | 1.2% | North America & Europe, spillover to APAC | Short term (≤ 2 years) |

| Adoption of advanced autoantibody panels | 0.9% | North America, Western Europe, urban APAC hubs | Medium term (2-4 years) |

| Growth in healthcare spending in emerging markets | 0.8% | APAC core (China, India), spill-over to MEA | Long term (≥ 4 years) |

| AI-driven multi-omics flare-prediction tools | 1.1% | North America, select EU centers, pilot sites in APAC | Long term (≥ 4 years) |

| Venture-backed tolerogenic cell therapies | 0.6% | North America, limited EU adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of SLE & Earlier Diagnosis

Recent data indicates prevalence rates of systemic lupus erythematosus (SLE) at 85.8 per 100,000 in Thailand, 92.3 per 100,000 in Catalonia, and 71.5 per 100,000 in Sweden.[1]Exagen Medical Policy Team, “AVISE Lupus Test Coverage,” Arkansas Blue Cross and Blue Shield, arkansasbluecross.com Increased adoption of anti-double-stranded DNA and anti-Smith testing in primary care settings has accelerated referrals, reducing delays between symptom onset and rheumatology confirmation. With payers requiring laboratory confirmation for first-line biologic approvals, test volumes are growing faster than population rates. In the United States, while the incidence has stabilized at 5.1 per 100,000 person-years, demographic shifts toward higher-risk ethnic groups are driving an increase in absolute case numbers. This steady rise in prevalence is expanding the SLE market by increasing the number of patients eligible for advanced treatments.

Rapid Approvals of Novel Biologics

In April 2026, the U.S. FDA approved subcutaneous anifrolumab, reducing per-dose administration costs by 22% and enabling home-based care. A supplemental biologics license application for obinutuzumab is targeting a decision by December 2026.[2]Jared Kaltwasser, “Obinutuzumab in Lupus Nephritis,” HCPLive, hcplive.com These approvals, combined with GlaxoSmithKline’s 2024 authorization of a pediatric belimumab autoinjector, highlight a regulatory focus on simplifying drug delivery rather than prioritizing first-in-class innovations. Simultaneous filings with the European Medicines Agency are shortening regional launch timelines, driving broader SLE market penetration within 18 months of initial U.S. approval.

Adoption of Advanced Autoantibody Panels

Exagen’s AVISE Lupus panel, which combines cell-bound complement activation products with traditional autoantibodies, has demonstrated 83% sensitivity and 78% specificity in multicenter studies.[3]Research Team, “Tele-rheumatology Outcomes,” Lupus Research Alliance, lupusresearch.org In 2025, Euroimmun and Thermo Fisher introduced recombinant antigen substrates to meet stricter FDA regulations on animal-sourced reagents. While these changes have increased per-test costs by up to 18%, they have significantly improved reproducibility. Health insurers in North America and Western Europe are increasingly mandating multi-marker confirmations before approving high-cost therapies. This shift has transformed previously elective tests into essential diagnostic steps, driving double-digit revenue growth for reference laboratories and expanding the market for precision-medicine solutions in SLE.

Growth in Healthcare Spending in Emerging Markets

In 2024, China’s National Healthcare Security Administration added belimumab to its reimbursement list, reducing annual patient out-of-pocket expenses from CNY 180,000 (USD 25,200) to CNY 36,000 (USD 5,040). In 2025, Saudi Arabia allocated USD 1.2 billion to enhance rheumatology infusion capacity, including the establishment of 12 new centers. Although 36.2% of lupus households in India continue to face catastrophic healthcare expenditures, rising middle-class purchasing power is driving private-sector sales. These policy initiatives and income growth are increasing the number of treated patients in the SLE market, even as per-capita spending in emerging markets remains lower than in developed economies.

Restraints Impact Analysis of Systemic Lupus Erythematosus Market*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High cost of biologics & limited reimbursement | -0.7% | Global, acute in emerging APAC and MEA | Short term (≤ 2 years) |

| Safety concerns over chronic immunosuppression | -0.5% | Global | Medium term (2-4 years) |

| Diagnostic heterogeneity; lack of gold-standard test | -0.4% | Global, pronounced in fragmented healthcare systems | Medium term (2-4 years) |

| Regulatory scrutiny on porcine-derived antigens | -0.3% | North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Costs of Biologics & Limited Reimbursement

In the U.S., belimumab is priced at nearly USD 35,000 annually, while anifrolumab approaches the USD 40,000 mark. Such pricing exceeds median household earnings in many emerging markets. In China, while reimbursements have reduced copayments, disparities across provinces leave rural communities facing significant financial burdens. European insurers require evidence of sustained remission for coverage beyond a year, delaying broader adoption. Additionally, biosimilar developers are hesitant to challenge established biologics, as many agents remain off-label for systemic lupus erythematosus (SLE), extending the exclusivity period for originators. This has resulted in a segmented treatment landscape where corticosteroids and hydroxychloroquine dominate, limiting short-term revenue potential for newer agents in the SLE market.

Safety Concerns with Chronic Immunosuppression

Serious infection rates under belimumab nearly double the baseline risk for lupus. Opportunistic infections associated with rituximab and high-dose cyclophosphamide have prompted regulators to enforce stricter Risk Evaluation and Mitigation Strategies. Physicians often rotate biologics to reduce cumulative exposure, but this practice complicates adherence tracking and increases the likelihood of flare-ups. Furthermore, mandatory annual screenings for tuberculosis or hepatitis B before refills introduce administrative delays, causing frustration among patients. These safety and compliance challenges, despite clear efficacy benefits, continue to constrain the rapid growth of the systemic lupus erythematosus market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Systemic Lupus Erythematosus Market Segment Analysis

By Product Category:

Diagnostics Capitalize on Precision FinancingIn 2025, diagnostics captured 37.66% of the systemic lupus erythematosus market share, as reference labs took on roles mandated by payers. Multi-marker panels, which assess complement activation and interferon signatures, now determine eligibility for premium biologics, forecasting an 8.45% CAGR through 2031. Revenue is predominantly driven by immunoassays utilizing enzyme-linked platforms, thanks to automated analyzers ensuring a 24-hour turnaround. Following closely are adjunct modalities like complement split-product testing, urinalysis for proteinuria, and imaging, all refining prognosis and detecting organ threats.

Financial incentives are on the rise: specialist clinics bundle testing with telehealth consultations, tapping into additional reimbursement streams. Meanwhile, large hospital networks are entering joint ventures with commercial labs to handle elevated sample volumes. As health systems synchronize biologic access with test-verified flare risks, diagnostics increasingly dominate the systemic lupus erythematosus market, even with only modest hikes in per-test prices.

By Route of Administration:

Patient-Managed Formats AccelerateIn 2025, the intravenous route held 51.43% of the systemic lupus erythematosus market share, but its dominance is waning. Tablet developments focusing on JAK pathways, alongside other small-molecule strategies, are projected to grow at an 8.60% CAGR through 2031, fueled by home-care delivery models. Subcutaneous formulations are gaining traction; anifrolumab secured at-home approval in 2026, and belimumab autoinjectors are now available for both adults and children.

Hospital infusion suites are adjusting their business models, as shorter chair times and fewer visits lead to reduced revenue. On the flip side, pay-by-performance contracts are emerging for self-injected biologics, linking net prices to flare-rate reductions. With remote monitoring tools capturing real-time adherence and biomarkers, oral and subcutaneous products are expanding the systemic lupus erythematosus market size by shifting costs from facility fees to drug margins.

By End User:

Labs and Clinics Share the Value ChainIn 2025, hospitals represented 55.45% of the systemic lupus erythematosus market size, thanks to their pivotal roles in acute care, organ biopsies, and inpatient biologic loading. However, diagnostic laboratories are on a rapid ascent, charting a 7.95% CAGR toward 2031, as payer mandates direct testing volumes to high-throughput facilities. Specialty rheumatology clinics are also reaping benefits, crafting bundled-payment pathways that integrate diagnostics, teleconsultation, and at-home dosing.

Lab consolidation is in full swing; national chains are acquiring regional centers to harness economies of scale in recombinant-antigen assays. Concurrently, rural infusion centers, bolstered by public-health grants, are expanding to serve underserved areas, where patients once traveled hours for therapy. These evolving care settings are diversifying revenue streams across the systemic lupus erythematosus market, reducing reliance on tertiary hospitals.

Geography Analysis

North America and APAC Systemic Lupus Erythematosus Market

In 2025, North America captured a significant 39.34% share of the systemic lupus erythematosus market, driven by Medicare support for high-cost biologics and the implementation of biomarker requirements. In the Asia-Pacific region, an 8.25% CAGR through 2031 is attributed to expanded provincial reimbursements in China and pediatric drug approvals in Japan. Although 36.2% of lupus families in India still face catastrophic healthcare expenses, increasing private insurance adoption and growing medical tourism are gradually improving access to treatments.

Europe, Middle East and South America Systemic Lupus Erythematosus Market

Europe presents a mixed outlook: centralized EMA approvals simplify processes for manufacturers, but national health-technology assessments impose budgetary restrictions, delaying drug formulary entries by up to 18 months. In the Middle East, governments are investing in domestic monoclonal-antibody production facilities to reduce import dependency, with the United Arab Emirates planning a new facility set to commence operations in 2027. In South America, Brazil and Argentina drive regional growth through private-sector coverage, even as public healthcare systems continue to ration access. These regional dynamics highlight areas of concentrated growth within the systemic lupus erythematosus market while emphasizing regions where unmet needs persist.

Competitive Landscape

GlaxoSmithKline's Benlysta and AstraZeneca's Saphnelo lead the systemic lupus erythematosus market, while the diagnostics segment remains fragmented with key players such as Exagen, Euroimmun, and Thermo Fisher. Established pharmaceutical companies are focusing on extending product lifecycles; AstraZeneca, for instance, has secured multiple device patents for anifrolumab between 2024 and 2026 to maintain subcutaneous exclusivity.

Mid-stage biotechnology firms are advancing curative approaches. Cabaletta Bio's CABA-201 CAR-T, currently in Phase 1/2 enrollment as of 2024, is designed to achieve durable remission with a single infusion. Similarly, Kyverna's KYV-101, expected to begin dosing in 2025, targets selective B-cell depletion. Meanwhile, digital health companies are integrating wearable data with multi-omics scores, aiming for reimbursement opportunities by mid-2027.

In diagnostics, competition centers on turnaround times and biomarker coverage. Exagen's AVISE test demonstrates 83% sensitivity but faces adoption challenges due to its dependence on flow-cytometry infrastructure. Conversely, Euroimmun's recombinant substrate kits reduce batch variability and qualify for CLIA-waiver eligibility, enabling access to primary-care markets. As reimbursement algorithms increasingly incorporate diagnostic testing, these assays are expected to play a more prominent role in the systemic lupus erythematosus market's competitive dynamics.

Systemic Lupus Erythematosus Industry Leaders

Eli Lilly and Company

Novartis AG

AstraZeneca plc

Bristol Myers Squibb Company

GSK Plc

- *Disclaimer: Major Players sorted in no particular order

Systemic Lupus Erythematosus Market Companies Covered in this Report

- Abbvie

- Amgen

- AstraZeneca

- Biogen

- Bristol-Myers Squibb

- Eli Lilly and Company

- Euroimmun Medizinische Labordiagnostika GmbH

- Exagen

- Roche

- GlaxoSmithKline

- Johnson & Johnson

- Merck

- Novartis

- PerkinElmer Inc. (Diagnostics)

- Pfizer

- Quest Diagnostics

- Sanofi

- Siemens Healthineers

- Thermo Fisher Scientific

- UCB

Recent Industry Developments in Systemic Lupus Erythematosus Market

- January 2026: The U.S. FDA approved subcutaneous anifrolumab, authorizing at-home use and slashing per-dose costs by 22%.

- April 2025: The FDA accepted Genentech’s supplemental BLA for obinutuzumab in moderate-to-severe SLE, setting a December 2026 decision target.

- February 2025: Adicet Bio received FDA Fast Track designation for ADI-001, an allogeneic gamma delta CAR-T cell therapy, for refractory systemic lupus erythematosus with extrarenal involvement, marking the second Fast Track designation for this investigational therapy.

Global Systemic Lupus Erythematosus Market Report Scope

As per the scope of the report, systemic lupus erythematosus (SLE) is an autoimmune inflammatory disease affecting multiple organs with various clinical manifestations. Joints, skin, kidneys, blood cells, brain, heart, and lungs are all impacted by SLE. SLE is triggered by a combination of genetic and environmental factors, such as medications, infections, and stress. The systemic lupus erythematosus market is segmented by product category, route of administration, end-user, and geography. By product category, the market includes diagnostics (immunoassays, complement tests, urinalysis, imaging, and others) and therapeutics (B-cell inhibitors, T-cell inhibitors, cytokine inhibitors, immunosuppressants, corticosteroids, and others). By route of administration, the market is segmented into oral, intravenous, and subcutaneous. By end-user, the market is categorized into hospitals, specialty clinics, diagnostic laboratories, and home-care settings. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

Segmentation Overview

| Diagnostics | Immunoassays |

| Complement Tests | |

| Urinalysis | |

| Imaging | |

| Others | |

| Therapeutics | B-Cell Inhibitors |

| T-Cell Inhibitors | |

| Cytokine Inhibitors | |

| Immunosuppressants | |

| Corticosteroids | |

| Others |

| Oral |

| Intravenous |

| Subcutaneous |

| Hospitals |

| Specialty Clinics |

| Diagnostic Laboratories |

| Home-care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Category | Diagnostics | Immunoassays |

| Complement Tests | ||

| Urinalysis | ||

| Imaging | ||

| Others | ||

| Therapeutics | B-Cell Inhibitors | |

| T-Cell Inhibitors | ||

| Cytokine Inhibitors | ||

| Immunosuppressants | ||

| Corticosteroids | ||

| Others | ||

| By Route of Administration | Oral | |

| Intravenous | ||

| Subcutaneous | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Diagnostic Laboratories | ||

| Home-care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the systemic lupus erythematosus market?

Mordor Intelligence reports USD 3.71 billion for 2026, with a forecast to USD 5.32 billion by 2031.

How fast is the systemic lupus erythematosus market expected to grow?

The market is projected to post a 7.5% CAGR from 2026 to 2031, according to Mordor Intelligence.

Which product segment is expanding quickest within systemic lupus erythematosus?

Diagnostics are forecast to rise at an 8.45% CAGR through 2031 as multi-marker panels become reimbursement prerequisites.

Why is Asia-Pacific viewed as the fastest growing geography?

Provincial reimbursement expansion in China and new pediatric approvals in Japan support an 8.25% CAGR for the region through 2031.

Which route of administration is gaining share in systemic lupus erythematosus therapy?

Oral and subcutaneous formats together outpace intravenous delivery, with tablets projected for an 8.60% CAGR to 2031.

Page last updated on: