Autism Spectrum Disorders Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

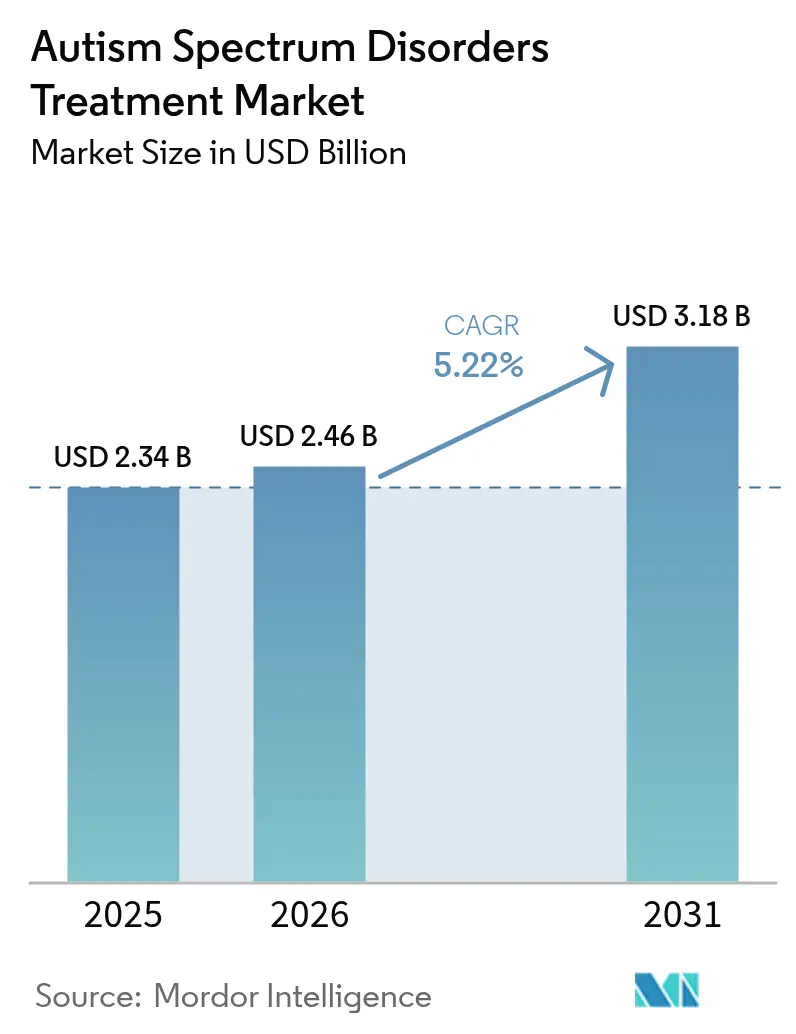

| Market Size (2026) | USD 2.46 Billion |

| Market Size (2031) | USD 3.18 Billion |

| Growth Rate (2026 - 2031) | 5.22% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

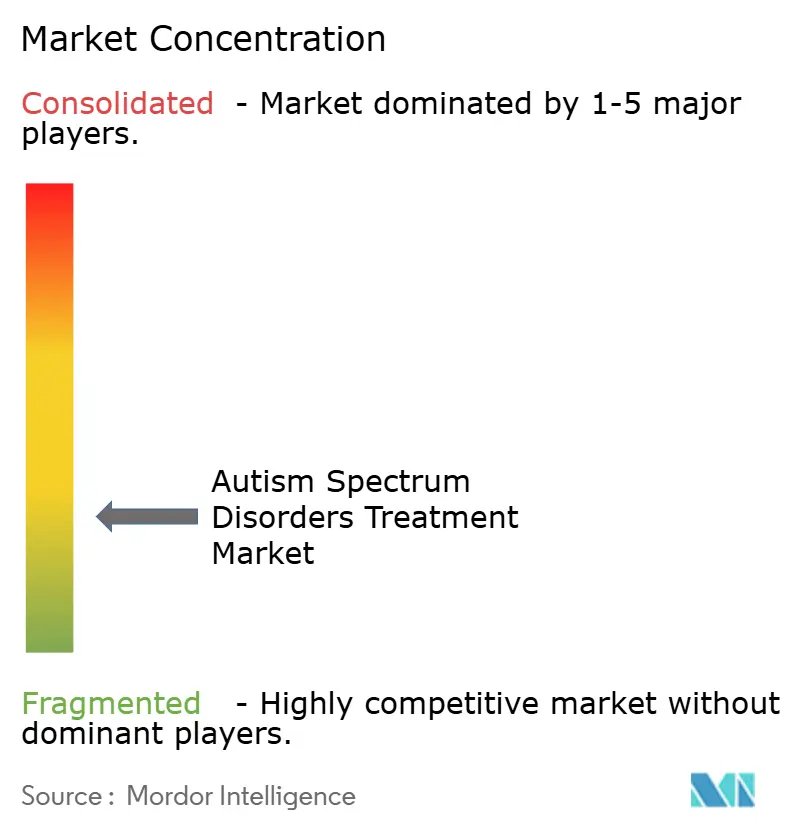

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Autism Spectrum Disorders Treatment Market Analysis by Mordor Intelligence

The Autism Spectrum Disorders Treatment market size is expected to grow from USD 2.34 billion in 2025 to USD 2.46 billion in 2026 and is forecast to reach USD 3.18 billion by 2031 at 5.22% CAGR over 2026-2031. Rapid uptake of cannabinoid-based medicines, growing use of FDA-cleared digital diagnostics and broader reimbursement for software-as-a-medical-device tools are redirecting investment from symptomatic control toward mechanism-based intervention. Precision medicine strategies built on biomarker discovery now complement genetic testing services, expanding the addressable patient base while improving therapy-matching accuracy. In parallel, regulators in Japan and China are opening expedited pathways for botanical drugs, shifting growth momentum eastward. Competitive dynamics remain fragmented because smaller innovators leverage microbiome, endocannabinoid and neuropeptide science to sidestep incumbent antipsychotic positions, yet incumbents still anchor hospital-based prescribing patterns through deep payer relationships.

Key Report Takeaways

- By drug class, antipsychotic medicines led with 41.10% Autism Spectrum Disorder treatment market share in 2025, while cannabinoid therapies are forecast to compound at 8.38% through 2031.

- By ASD type, Autistic Disorder accounted for 53.20% share in 2025, while Rett Syndrome treatments are set to rise at an 7.88% CAGR to 2031.

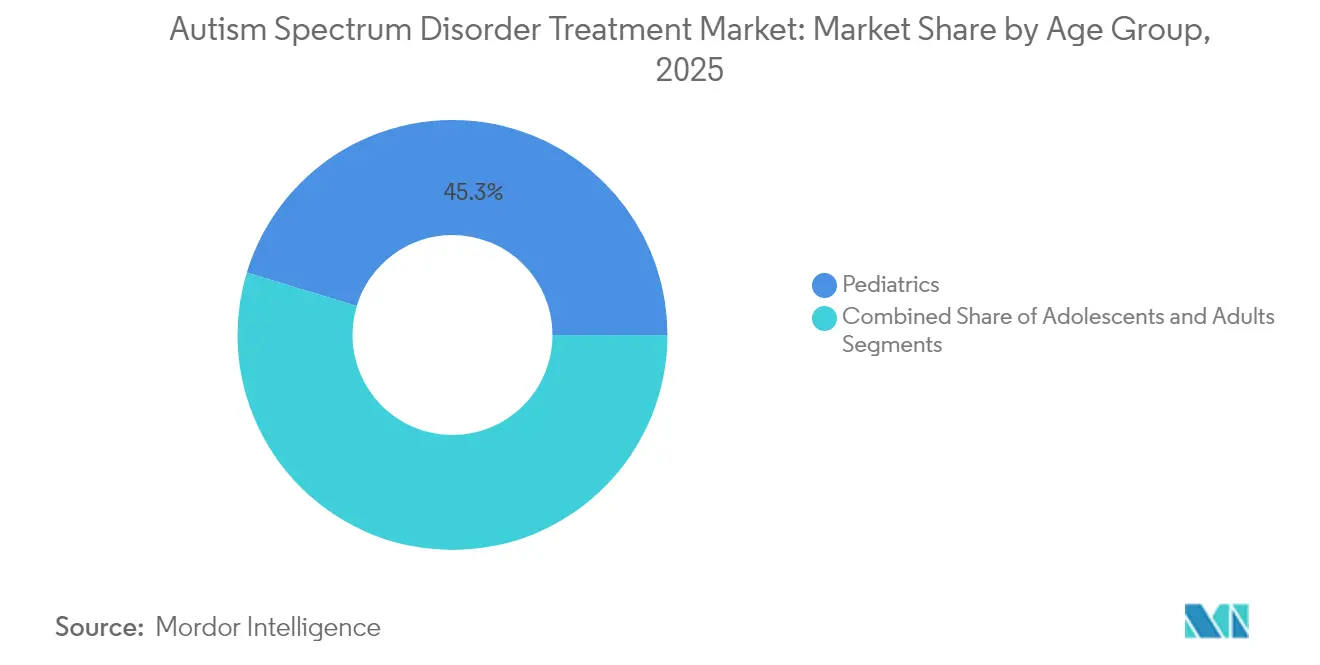

- By age group, the pediatric segment held 45.30% share of the Autism Spectrum Disorder treatment market size in 2025; adult therapies are expanding at an 8.55% CAGR to 2031.

- By distribution channel, hospital pharmacies captured 59.95% of the Autism Spectrum Disorder treatment market size in 2025; online pharmacies are advancing at a 8.62% CAGR through 2031.

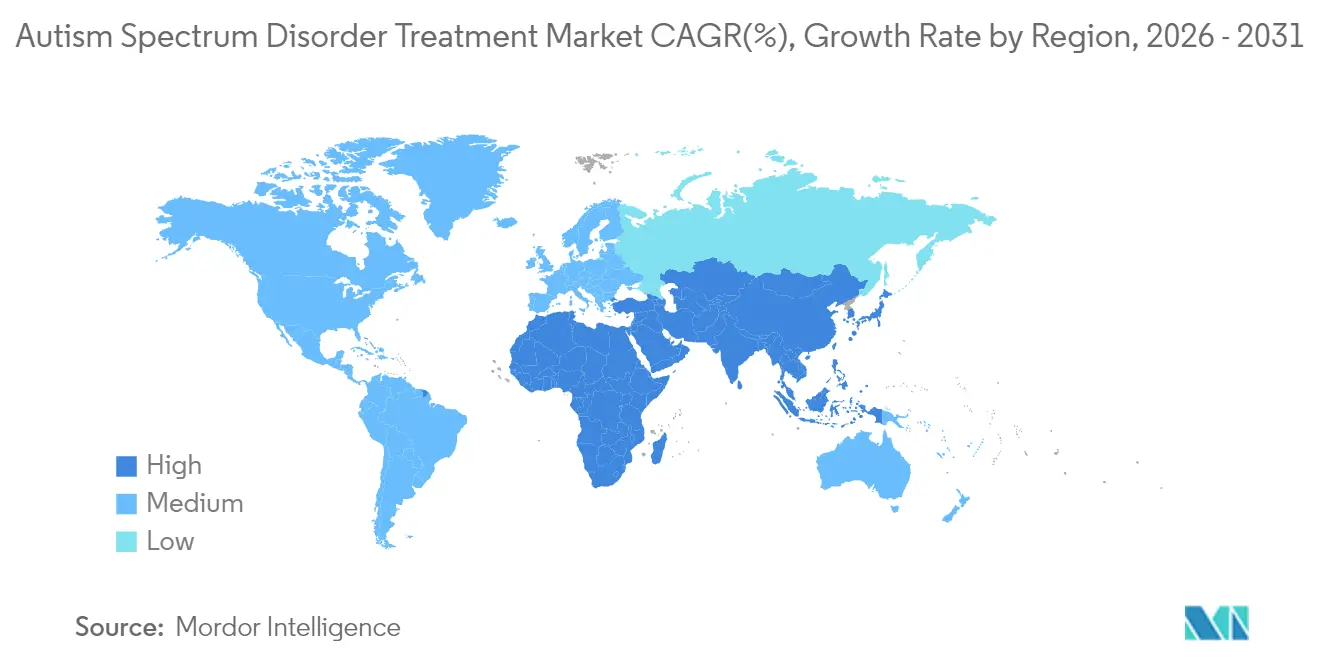

- By geography, North America commanded 45.70% revenue in 2025, whereas Asia-Pacific is projected to post a 7.55% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Autism Spectrum Disorders Treatment Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High burden of Autism Spectrum Disorders | +1.2% | Global; highest in North America and Europe | Long term (≥ 4 years) |

| Growing awareness & early diagnosis programs | +1.0% | Global; accelerated gains in APAC and emerging markets | Medium term (2-4 years) |

| Expanding reimbursement for ASD therapies | +0.8% | North America & EU core; spill-over to APAC | Short term (≤ 2 years) |

| Robust late-stage pipeline of novel drugs | +1.1% | Global; regulatory leadership in US and EU | Medium term (2-4 years) |

| Advances in diagnostic tools & digital apps | +0.6% | North America & EU; early adoption in urban APAC | Short term (≤ 2 years) |

| Private-sector funding for rare ASD sub-types | +0.4% | Global; concentrated in biotech hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Burden of Autism Spectrum Disorders (ASD)

Escalating prevalence—now 1 in 36 children—adds load to health systems that still rely on labor-intensive behavioral care, prompting families to seek pharmacologic relief when aggression threatens safety.[1]Frontiers in Integrative Neuroscience, “Unlocking autism's complexity: the Move Initiative's path,” frontiersin.org Lifetime economic burden has been pegged at USD 7 trillion by 2029, reflecting medical costs plus lost productivity. Pharma pipelines still focus on pediatric needs, yet rising diagnoses among young adults are widening the untreated population, validating the adult segment’s 8.92% CAGR outlook.[2]JAMA Network Open, “Attention-Deficit/Hyperactivity Disorder in Medicaid-Enrolled Autistic Adults,” jamanetwork.com Medication remains common; two-thirds of autistic adolescents receive psychotropics, underscoring unmet demand for safer, more targeted drugs.

Growing Awareness & Early Diagnosis Initiatives Coupled with Government Funding

The NIMH allocates USD 47 billion for neuroscience, and HRSA adds USD 5 million for autism programs, reinforcing national priorities.[3]National Institute of Mental Health, “FY 2024 Budget – Congressional Justification,” nih.govMultistage screening networks are improving detection among underserved groups, while FDA-designated tools like StrandDx ASD promise prediction at birth with 80-90% accuracy. Earlier identification lengthens treatment horizons, supporting recurring revenue models for therapy developers.

Expanding Reimbursement Coverage for ASD Therapies

Highmark now reimburses Cognoa’s Canvas Dx without prior authorization, signaling payer openness to digital diagnostics. TRICARE’s Autism Care Demonstration covers Applied Behavior Analysis, and state Medicaid plan s integrate autism services into managed care, reducing emergency department use while attracting private-equity capital into scalable clinic chains. Coverage for cannabis-based drugs and software therapeutics shortens the commercialization runway for innovators.

Robust Late-stage Pipeline of Novel Therapeutics

Phase 2 success for Yamo’s L1-79 delivered a 7.94-point social-function gain, de-risking catecholamine modulation strategies. DeFloria’s multi-cannabinoid AJA001 secured IND clearance, opening FDA’s first botanical path in autism. Microbiome agent AB-2004 met Phase 2b endpoints, and vasopressin plus oxytocin analogs show functional gains, diversifying therapeutic targets and diluting development risk.[4]Nature Medicine, “Safety and target engagement of an oral small-molecule treatment for Autism Spectrum Disorder: A Phase 1b/2a clinical trial of AB-2004,” nature.com

Restraints Impact Analysis of Autism Spectrum Disorders Treatment Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of long-term pharmacologic care | -0.9% | Global; highest in emerging markets | Long term (≥ 4 years) |

| Stringent regulatory hurdles | -0.7% | Global; most intense in US and EU | Medium term (2-4 years) |

| Limited efficacy & side effects of current drugs | -0.6% | Global; strongly felt in pediatric settings | Medium term (2-4 years) |

| Data-privacy limits on pooled genomics | -0.3% | North America & EU core; spill-over to APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Long-term Pharmacologic Management

Lifelong drug regimens accumulate costs that deter uptake, especially where payer budgets remain tight. Metabolic monitoring for antipsychotics adds testing fees and clinician visits, and adherence gaps drive relapse episodes that require expensive interventions. Polypharmacy exposes patients to additive side-effect risks; roughly 30% of individuals take two or more agents, adding complexity and financial load.

Stringent Regulatory Hurdles & Limited Surrogate Endpoints

The FDA demands improvement in core social communication, not just irritability, thus elongating trials that depend on behavioral scales with subjective rater variability. Botanical candidates must show pharmaceutical-grade consistency, increasing manufacturing costs. Lack of international harmonization further multiplies approval timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Autism Spectrum Disorders Treatment Market Segment Analysis

By Drug Class:

Cannabinoids Challenge Antipsychotic DominanceAntipsychotics retained 41.10% Autism Spectrum Disorder treatment market share in 2025, anchored by risperidone and aripiprazole approvals for irritability. Their growth is moderating due to metabolic risks, while cannabinoid therapeutics record an 8.38% CAGR as FDA acceptance of botanical dossiers widens. Antidepressants and SSRIs remain stable for anxiety comorbidity, and stimulants such as methylphenidate gain favor for overlapping ADHD. Hormone-based approaches advance via oxytocin and vasopressin analogs, and microbiome modulators show Phase 2 success. Evolving evidence prompts neurologists to shift anticonvulsant use toward lower teratogenic agents.

The Autism Spectrum Disorder treatment market size for cannabinoid drugs could climb markedly if AJA001 and HOPE-1 secure approval, though rigorous lot consistency testing remains a gatekeeper. Antipsychotic incumbents are deploying long-acting injectables to defend share, yet patient and caregiver sentiment is gravitating toward therapies that treat social deficits, setting the stage for category disruption over the forecast window.

By ASD Type:

Rett Syndrome Drives Precision Medicine AdoptionAutistic Disorder stood at 53.20% of revenue in 2025, reflecting diagnostic prevalence. Rett Syndrome, a rare but well-defined genetic variant, is growing fastest at 7.88% CAGR, riding trofinetide’s first-in-class approval. Market access teams are educating clinicians on syndrome-specific eligibility, shifting perceptions from broad-spectrum prescriptions to genotype-guided options.

The Autism Spectrum Disorder treatment market size attached to Rett Syndrome therapies will expand further as Canada’s Priority Review and potential EU filings widen geographic reach. Success of DAYBUE also motivates investors to fund programs for Phelan McDermid and Fragile X, signaling momentum toward tailored molecules that can command premium pricing.

By Age Group:

Adult Market Emerges from Diagnostic ShadowAdults represented the fastest-growing cohort at 8.55% CAGR, even though pediatrics still holds 45.30% of revenue. Greater awareness and refined diagnostic criteria uncover cases in people aged 18+, while Medicaid prepares for rising service demand. Treatment protocols now integrate mood and attention comorbidity drugs, emphasizing holistic care.

The Autism Spectrum Disorder treatment market size attached to adult pharmacotherapy is expected to keep expanding as longitudinal studies show economic benefits from treating anxiety and ADHD in adulthood. Pharmaceutical marketers are reshaping outreach, using digital channels that resonate with self-advocating adult communities.

By Distribution Channel:

Digital Transformation Accelerates AccessHospital pharmacies controlled 59.95% of 2025 sales, owing to complex case management. Online outlets, however, enjoy a 8.62% CAGR, driven by telehealth integration and payer acceptance of mail-order fulfillment. Specialty pharmacies deliver value in cannabinoid temperature-controlled shipping and microbiome capsule counseling.

Knowledge gaps among community pharmacists highlight training needs; only 43.3% understand core autism symptoms, spurring niche platforms that bundle education with e-dispensing. Digital therapeutics such as Canvas Dx bypass traditional channels altogether, foreshadowing hybrid care models where apps and pills are co-prescribed.

Geography Analysis

North America Autism Spectrum Disorders Treatment Market

North America held 45.70% of 2025 revenue as FDA approvals, broad insurance coverage and early digital tool adoption support therapy demand. The US leads clinical-trial volume, and Canada’s fast-track processes for Rett Syndrome drugs indicate regulatory alignment. Mexico is climbing as diagnosis rates improve alongside private insurance penetration.

Europe Autism Spectrum Disorders Treatment Market

Europe exhibits stable expansion. EMA harmonization eases multi-country launches, and Germany’s Digital Health Applications pathway reimburses software therapeutics. France and Italy sustain antipsychotic volume, while the UK funds community autism hubs that incorporate pharmacologic and behavioral care.

APAC Autism Spectrum Disorders Treatment Market

Asia-Pacific posts the strongest growth at 7.55% CAGR. Japan is updating its Pharmaceuticals and Medical Devices Act to smooth botanical approvals, and China’s Hainan pilot zone permits conditional imports of unapproved drugs for urgent needs, accelerating cannabinoid access. India’s expanding telemedicine footprint supports online pharmacy uptake, although reimbursement lags.

South America and MEA Autism Spectrum Disorders Treatment Market

Middle East & Africa remains nascent but benefits from Gulf states’ employment of universal health-coverage programs that include pediatric neurodevelopmental services. South America records steady gains, with Brazil’s ANVISA fast-tracking certain cannabis formulations and Argentina increasing public funding for early screening.

Competitive Landscape

Competition is fragmented. No firm controls more than a low-double-digit share, and therapeutic diversity keeps switching costs low for clinicians. Incumbents such as Otsuka and Roche defend antipsychotic franchises yet invest in next-gen programs like balovaptan to address social communication. Smaller biotechs pursue differentiated paths: Axial targets the microbiome, DeFloria crafts botanical multi-cannabinoid blends, and MindMed explores R-(-)-MDMA, illustrating willingness to tackle previously stigmatized compounds.

Digital enablers also influence rivalry. Cognoa partners with payers to tie AI-based diagnosis directly to drug pathways, while LinusBio offers epigenetic tests that may inform dosing. Private-equity consolidation of clinic networks boosts purchasing clout, pressuring manufacturers on pricing but also offering large-scale data for real-world evidence generation.

Strategic collaborations grow: Yamo Pharmaceuticals pairs with contract research organizations to accelerate Phase 3, and Acadia teams with patient-advocacy groups to educate caregivers, supporting rapid uptake. The field’s low concentration leaves room for platform companies that can integrate genetic screening, digital monitoring and targeted pharmacology into unified care models.

Autism Spectrum Disorders Treatment Industry Leaders

PaxMedica

Otsuka Pharmaceutical Co., Ltd.

F. Hoffmann-La Roche Ltd

Jazz Pharma

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Autism Spectrum Disorders Treatment Market Companies Covered in this Report

- QIAGEN

- PaxMedica Inc.

- Yamo Pharmaceuticals LLC

- Otsuka

- Roche

- Curemark LLC

- Zynerba Pharmaceuticals Inc.

- Axial Therapeutics

- STALICLA SA

- Johnson & Johnson

- Jazz Pharma

- Eli Lilly and Company

- Pfizer

- NeuroNOS

- DeFloria, Inc.,

- Jaguar Gene Therapy

- Anavex Life Sciences Corp.

Read Analysis of Autism Spectrum Disorders Treatment Companies

Recent Industry Developments in Autism Spectrum Disorders Treatment Market

- May 2025: Yamo Pharmaceuticals announced positive Phase 2 results for L1-79 at the 2025 INSAR Annual Meeting.

- March 2025: NeuroNOS secured USD 2 million to progress a nitric oxide-modulating therapy for autism, with human trials slated for 2026.

- February 2025: DeFloria received IND clearance for AJA001, a multi-cannabinoid botanical drug, with Phase 2 trials planned for mid-2025.

- April 2024: Health Canada accepted trofinetide for Priority Review, potentially benefiting 600-900 Rett patients.

Autism Spectrum Disorders Treatment Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the autism spectrum disorders (ASD) treatment market as the total global spend on prescription medicines, including antipsychotics, selective serotonin reuptake inhibitors, stimulants, sleep regulators, and emerging cannabinoid agents, together with structured, evidence-based interventions such as Applied Behavior Analysis, speech, and occupational therapy sessions delivered in hospitals, clinics, and home settings by certified professionals.

Scope Exclusions: We exclude nutritional supplements, diagnostic screening tools, and informal alternative therapies that lack peer-reviewed efficacy.

Segments Covered in This Report

- By Drug Class

- Antipsychotic Drugs

- SSRIs / Antidepressants

- Stimulants

- Hormone Therapies

- Anticonvulsants

- Cannabinoid-based Therapies

- Microbiome Modulators

- Other Drug Classes

- By ASD Type

- Autistic Disorder

- Asperger Syndrome

- PDD-NOS

- Rett Syndrome

- Childhood Disintegrative Disorder

- Other Types

- By Age Group

- Pediatrics (2–12 yrs)

- Adolescents (13–17 yrs)

- Adults (18+ yrs)

- By Distribution Channel

- Hospital Pharmacies

- Retail & Drug Stores

- Specialty Pharmacies

- Online Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Next, we interviewed child psychiatrists, board-certified behavior analysts, major pharmacy buyers, and payer policy leads across North America, Europe, and Asia. These conversations validated therapy intensity norms, confirmed average selling prices, and clarified reimbursement inflection points before we locked our assumptions.

Desk Research

We began by mining open, reputable datasets, including the U.S. CDC autism prevalence tables, WHO Global Health Observatory, OECD health expenditure series, FDA drug sales dashboards, and association portals such as Autism Speaks, which were complemented by peer-reviewed clinical journals. Company filings, investor presentations, and press releases enriched recent launch uptake data, while paid repositories, including D&B Hoovers and Dow Jones Factiva, supplied revenue splits and pipeline timelines that we stitched into our baseline. This is where Mordor Intelligence analysts ensure consistency across geographies. The sources listed are illustrative only; many additional references informed data gathering, validation, and clarification.

Market-Sizing & Forecasting

We apply a top-down prevalence to treated cohort model that translates diagnosed ASD counts into demand pools, which are then aligned with payer coverage limits and average treatment intensity to yield gross spend by care pathway. Results are corroborated with selective bottom-up approximations; for example, sampled drug brand sales and large provider therapy hour disclosures allow adjustments where gaps emerge. Key variables include diagnosed prevalence ratios, annual therapy hours per patient, regimen adherence levels, reimbursement rate shifts, pipeline drug approval probabilities, and regional pricing bands. Multivariate regression with scenario analysis produces the forecast, and any missing micro-level inputs are bridged using expert agreed ratios that stay within documented ranges.

Data Validation & Update Cycle

We pass model outputs through variance scans against independent metrics, followed by peer review and senior analyst sign-off. Reports refresh annually, and interim updates follow material drug approvals, guideline changes, or reimbursement revisions. A fresh quality check precedes every client delivery so users receive our latest view.

How Mordor Intelligence's Autism Spectrum Disorders Treatment Market Size Compares to Other Published Estimates

We acknowledge that published estimates often diverge because firms choose differing scopes, patient funnels, and refresh cadences, which can puzzle decision-makers.

Key Gap Drivers include broader inclusion of allied services, use of unverified prevalence stretch factors, and single source price benchmarks in some external publications, whereas Mordor Intelligence narrows scope to evidence-based modalities, applies documented prevalence data, and updates exchange rates at every refresh.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.34 B (2025) | Mordor Intelligence | - |

| USD 7.96 B (2024) | Global Consultancy A | Counts caregiver training and wide behavioral service ecosystem |

| USD 34.10 B (2023) | Industry Journal B | Adds screening services and other neurodevelopmental disorders |

| USD 2.04 B (2022) | Regional Consultancy C | Relies on drug revenue only, omits therapy spend |

These contrasts show that our disciplined variable selection, multi-step validation, and annual refresh cycle deliver a balanced, transparent baseline that stakeholders can trace to clear inputs and repeatable steps.

Key Questions Answered in the Report

What is the current size of the Autism Spectrum Disorder market?

The Autism Spectrum Disorder market size stands at USD 2.46 billion in 2026 and is projected to grow to USD 3.18 billion by 2031 at a 5.22% CAGR.

Which region is the fastest-growing in Autism Spectrum Disorder therapies?

Asia-Pacific shows the highest growth, with a projected 7.55% CAGR through 2031 as China and Japan streamline approvals for novel treatments.

Which drug class is expanding most rapidly?

Cannabinoid-based therapies are advancing at an 8.38% CAGR, challenging antipsychotic dominance as botanical regulatory frameworks mature.

Why is the adult segment gaining prominence?

Delayed diagnoses and better awareness are uncovering unmet needs among adults, driving an 8.55% CAGR for therapies focused on individuals aged 18 and older.

How are digital tools affecting autism care?

FDA-cleared diagnostics like Canvas Dx shorten time to diagnosis, while AI-enabled monitoring apps guide medication adjustments, improving treatment precision.

What drives investment into rare autism sub-types?

Successful approval of trofinetide for Rett Syndrome proves that genotype-specific drugs can secure premium pricing and fast regulatory review, attracting private-sector funding for similar precision-medicine programs.

Page last updated on: