Tourette Syndrome Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

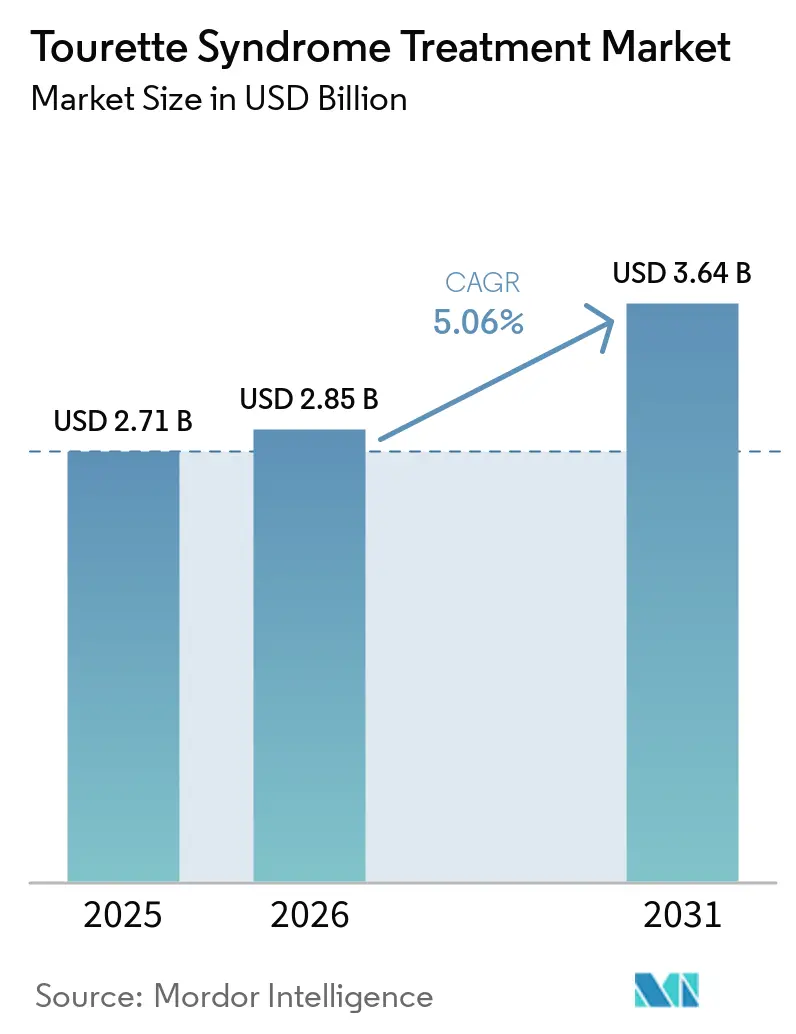

| Market Size (2026) | USD 2.85 Billion |

| Market Size (2031) | USD 3.64 Billion |

| Growth Rate (2026 - 2031) | 5.06% CAGR |

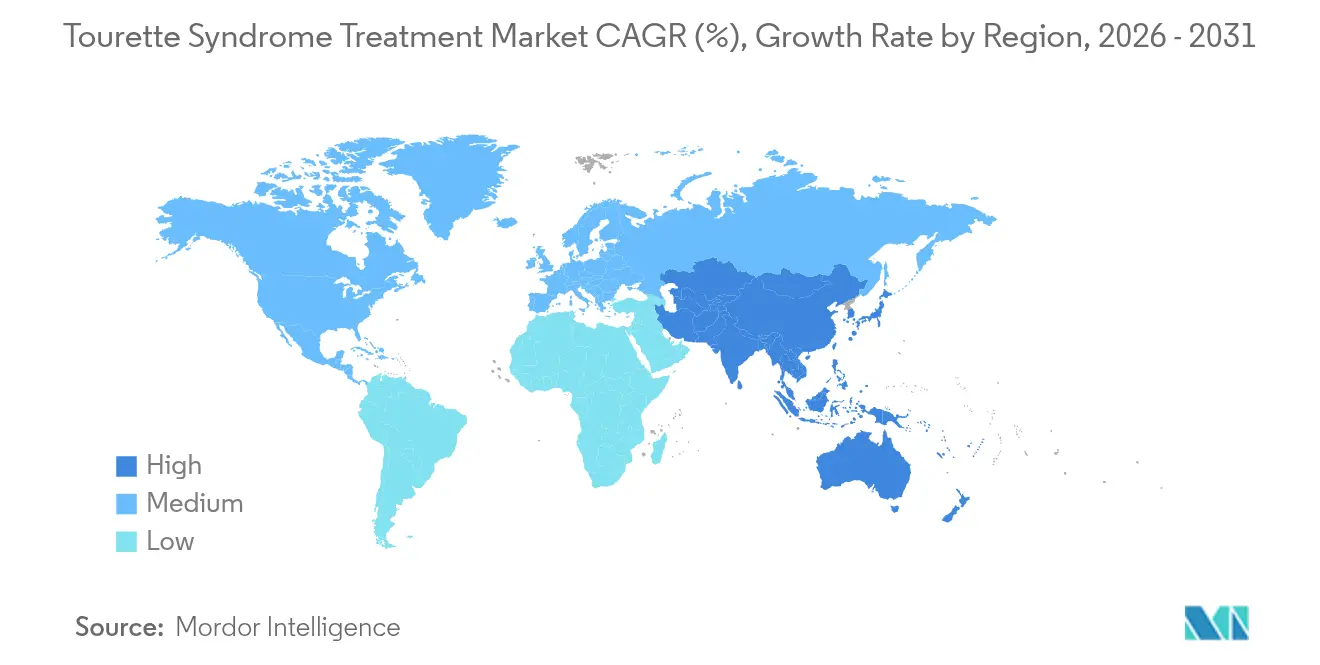

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

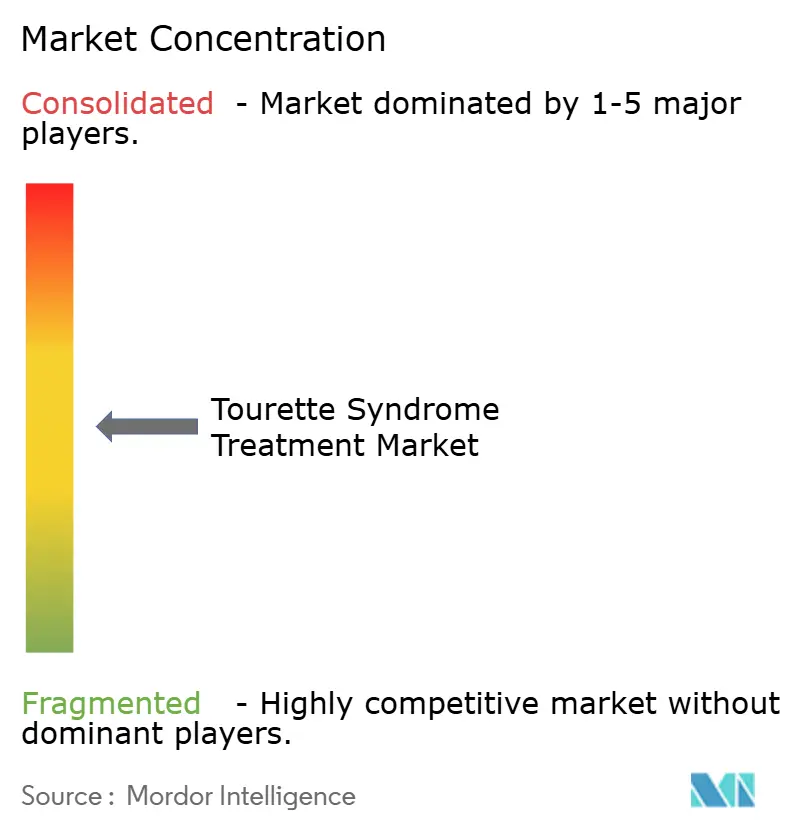

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tourette Syndrome Treatment Market Analysis by Mordor Intelligence

Tourette syndrome treatment market size in 2026 is estimated at USD 2.85 billion, growing from 2025 value of USD 2.71 billion with 2031 projections showing USD 3.64 billion, growing at 5.06% CAGR over 2026-2031. Growth is sustained by earlier diagnosis, rapid clinical adoption of VMAT-2 inhibitors, and expanding payer coverage for behavioral therapy. Parallel progress in digital dispensing channels, particularly online pharmacies, is lowering access frictions. Precision-medicine pipelines, reinforced by orphan-drug incentives, are redefining therapeutic classes while gene- and cell-based candidates incubate in late-stage laboratories. Nevertheless, high out-of-pocket costs and lingering safety concerns surrounding dopamine-blocking drugs temper full-scale uptake.

Key Report Takeaways

- By drug class, antipsychotics led with 57.94% of the Tourette syndrome treatment market share in 2025; VMAT-2 inhibitors are poised for the fastest 7.02% CAGR through 2031.

- By treatment modality, pharmacological options captured 80.64% revenue share in 2025, while deep-brain stimulation is projected to advance at a 7.20% CAGR to 2031.

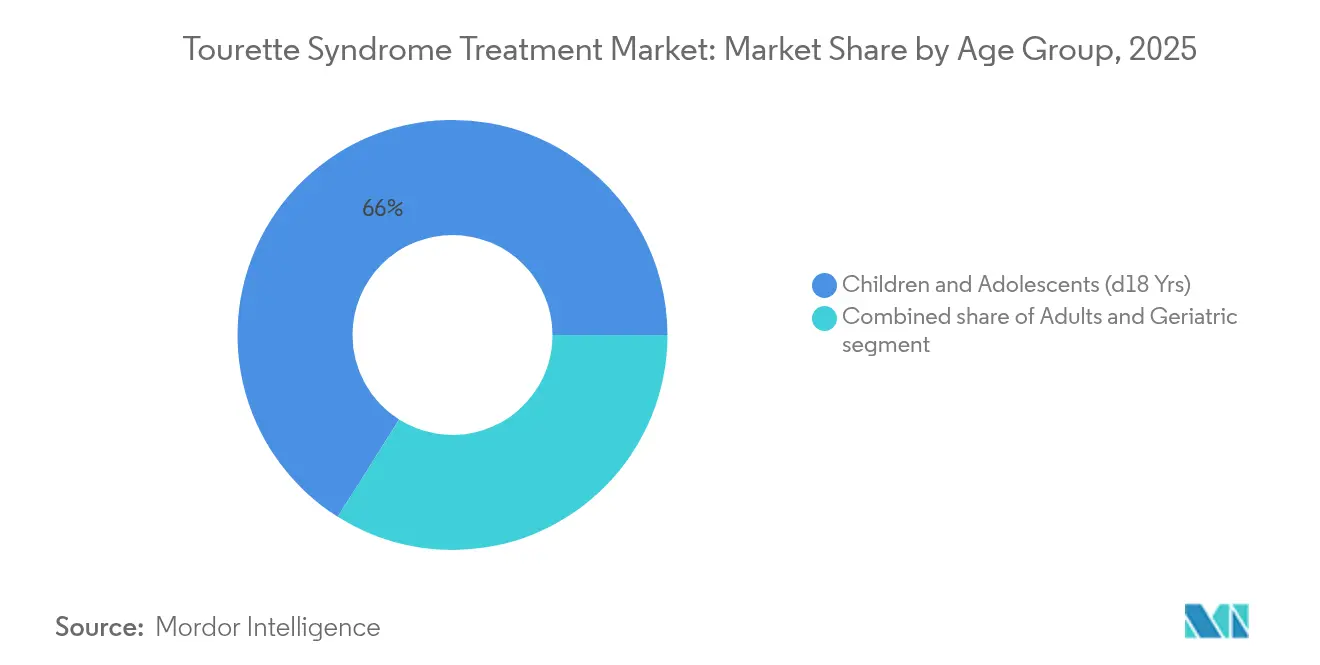

- By age group, the pediatric cohort held 66.04% of the Tourette syndrome treatment market size in 2025; the adult cohort records the highest 7.78% CAGR through 2031.

- By distribution channel, hospital pharmacies controlled 44.20% revenue share in 2025, whereas online pharmacies expand at an 8.05% CAGR to 2031.

- By geography, North America retained 42.10% share in 2025; Asia-Pacific is forecast to grow at 6.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Tourette Syndrome Treatment Market*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence and earlier diagnosis of Tourette syndrome | +1.2% | Global (North America & Europe core) | Medium term (2-4 years) |

| Advancements in neuropsychiatric drug development pipelines | +1.8% | North America & EU; spill-over to APAC | Long term (≥ 4 years) |

| Favorable regulatory incentives for rare neurological disorders | +0.9% | United States & European Union | Short term (≤ 2 years) |

| Expansion of healthcare reimbursement and insurance coverage | +0.7% | North America & Europe; emerging APAC | Medium term (2-4 years) |

| Increasing investments in neurodevelopmental research collaborations | +0.5% | Global academic–industry hubs | Long term (≥ 4 years) |

| Technological progress in behavioral and device-based therapies | +0.6% | North America, Europe, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence and Earlier Diagnosis

Enhanced screening protocols now uncover adults whose tics were once misclassified, adding thousands of patients to registries each year. Biomarker discoveries detailing cortical interneuron deficits provide objective confirmation tools that move beyond subjective rating scales. Teleconsultations funnel specialist expertise into rural regions, reducing wait-times for neurological evaluation. Comorbidity-focused assessments capture overlapping ADHD and OCD symptoms, expanding therapeutic demand. Early intervention improves behavioral-therapy responsiveness, strengthening long-term adherence trajectories.

Advancements in Neuropsychiatric Drug Development Pipelines

Breakthroughs in VMAT-2 inhibition illustrate the move from broad dopamine blockade toward precision modulation. Emalex Biosciences’ Phase 3 success introduces the first novel Tourette class in five decades, inspiring record venture inflows. Second-generation compounds under Neurocrine stewardship refine benefit-risk ratios after first-wave challenges. Cannabinoid research, showcased in the CANNA-TICS trial, delivers symptomatic relief where legacy regimens fail[1]PubMed, “Nabiximols for Treatment-Resistant Tourette Syndrome,” pubmed.ncbi.nlm.nih.gov. Combined, these innovations elevate clinician confidence in pharmacologic renewal cycles.

Favorable Regulatory Incentives for Rare Neurological Disorders

FDA orphan-drug designations grant seven-year exclusivity, tax credits, and user-fee waivers, accelerating dossier submissions. Adaptive-trial frameworks accommodate tic variability, shrinking sample-size burdens for smaller firms. The Orphan Products Grants Program subsidizes natural-history studies, sharpening endpoint selection. Recent patent-term extensions for neurological molecules signal continuing policy support. Collectively, incentives mitigate commercial-risk perceptions and widen entrant diversity.

Expansion of Healthcare Reimbursement and Insurance Coverage

UnitedHealthcare’s special-needs pilots demonstrate that tailored benefit packages raise medication adherence and therapy utilization. CBIT is now covered in multiple U.S. states after sustained evidence generation, marking a pivotal reimbursement shift[2]CDC, “Comprehensive Behavioral Intervention for Tics,” cdc.gov. Cigna’s updated guidelines endorse deep-brain stimulation for refractory cases, albeit under strict documentation rules. Telehealth parity laws extend payment to virtual consults, democratizing access for mobility-constrained adults. Wider payer engagement helps convert latent diagnoses into active prescriptions.

Restraints Impact Analysis of Tourette Syndrome Treatment Market*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High treatment costs and affordability challenges in emerging markets | –1.4% | APAC, Latin America, MEA; rural North America | Long term (≥ 4 years) |

| Adverse side-effect profiles of existing pharmacological therapies | –0.8% | Global (pediatric focus) | Medium term (2-4 years) |

| Limited awareness and social stigma around tic disorders | –0.6% | Emerging markets; rural regions worldwide | Medium term (2-4 years) |

| Stringent regulatory and clinical-trial requirements for novel therapies | –0.5% | United States, European Union, Japan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Treatment Costs and Affordability Challenges in Emerging Markets

Comprehensive Tourette management can surpass USD 15,000 annually, eclipsing median incomes across much of APAC and South America. Deep-brain stimulation implantation crosses USD 100,000 when device maintenance is included. Premium pricing for VMAT-2 agents reflects rare-disease R&D expense yet curtails uptake in price-sensitive health systems. While generic antipsychotics offer lower sticker prices, downstream costs from metabolic side effects erode savings. Limited public insurance penetration keeps out-of-pocket shares elevated, challenging sustained therapy adherence.

Adverse Side-Effect Profiles of Existing Pharmacological Therapies

Typical antipsychotics carry metabolic and extrapyramidal liabilities that deter long-term use in children. The VMAT-2 pioneer INGREZZA missed key Tourette efficacy targets, illustrating development intricacies. Patients often weigh tic suppression against weight gain, sedation, and cognitive blunting. Behavioral methods like CBIT avoid pharmacologic toxicity but demand specialist time and patient commitment[3]Tourette Association of America, “CBIT Training Gaps,” tourette.org. Cannabinoid alternatives promise gentler profiles, yet regulatory variability and dosage standardization remain unresolved.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Tourette Syndrome Treatment Market Segment Analysis

By Drug Class:

Antipsychotics Face VMAT-2 ChallengeAntipsychotics held 57.94% of the Tourette syndrome treatment market share in 2025, underscoring their entrenched status as first-line pharmacotherapy. Yet demand momentum is shifting as VMAT-2 inhibitors outpace at a 7.02% CAGR, reflecting clinicians’ appetite for narrower dopamine modulation with fewer metabolic penalties. Atypical formulations surpass typical compounds because of reduced extrapyramidal adverse events. Still, weight-gain risk propels search for leaner profiles. Alpha-2 agonists preserve a valued niche for dual tic-and-ADHD presentations, while benzodiazepines serve episodic crises rather than chronic regimens.

VMAT-2 uptake accelerates despite higher acquisition costs because patients tolerate them better and adhere longer, offsetting pharmacy budgets via lower adverse-event management. Cannabinoid candidates, inspired by CANNA-TICS data, trail in regulatory limbo yet attract compassionate-use prescriptions in severe cases. Dopamine-modulating agents with receptor-selective architectures line late-stage pipelines, aiming to balance efficacy with cardiometabolic safety. Overall, therapeutic substitution threatens antipsychotic volume even as those legacy agents remain indispensable in many public systems because of generic availability. The evolving class mix highlights competitive fluidity inside the Tourette syndrome treatment market.

By Treatment Modality:

Behavioral Therapy Gains GroundPharmacological approaches accounted for 80.64% of the Tourette syndrome treatment market size in 2025, reflecting clinician comfort with medication-based symptom control. Deep-brain stimulation, though still niche, records the fastest 7.20% CAGR, supported by responsive-stimulation research that optimizes electrode output for tic severity fluctuations. Insurance willingness to cover refractory cases widens patient funnels. Concurrently, CBIT earns guideline endorsement and payer reimbursement, moving from experimental to mainstream practice.

Gene and cell therapies reside in early-phase inquiry yet benefit from Mayo Clinic findings that map cortical interneuron deficits as future vector targets. Telemedicine integrates seamlessly with behavioral regimens, enabling weekly CBIT sessions without geographic limits and boosting completion rates. Pharmacologic dominance therefore coexists with maturing device and behavioral segments, creating multimodal pathways that personalize care journeys throughout the Tourette syndrome treatment market.

By Age Group:

Adult Recognition AcceleratesThe pediatric cohort commanded 66.04% of the Tourette syndrome treatment market size in 2025, anchored in the disorder’s childhood onset. However, the adult cohort is expanding at an 7.78% CAGR as heightened awareness corrects decades of misdiagnosis. Employers increasingly recognize tic accommodations under disability frameworks, pushing demand for therapies that preserve job productivity. Adult-onset identification underscores lifelong management needs rather than spontaneous symptom resolution assumed in earlier eras.

Therapy selection diverges by age. Children often start with CBIT before medication layering, while adults tolerate VMAT-2 agents better than antipsychotics owing to metabolic risk accumulation. Geriatric patients, though a small base, necessitate careful polypharmacy checks to avoid cognitive compromise. Telehealth adoption resonates with working adults who require discreet, schedule-friendly consultations. As adult prevalence figures grow, guideline committees revise dosing algorithms to reflect differing metabolic profiles, cementing age as a decisive segmentation lens in the Tourette syndrome treatment market.

By Distribution Channel:

Digital Transformation AcceleratesHospital pharmacies retained 44.20% share of the Tourette syndrome treatment market size in 2025 thanks to their role in initiating VMAT-2 titration and deep-brain stimulation device programming. Yet online pharmacies exhibit an 8.05% CAGR, mirroring broader telehealth adoption. Discretion, home delivery, and automated refill reminders appeal to patients wary of public stigma. Retail chains remain vital for routine antipsychotic refills but morph into counseling hubs offering side-effect mitigation advice.

Integrated digital platforms now synchronize e-prescriptions with CBIT coaching apps, driving adherence through single sign-on ecosystems. Specialty pharmacies nested inside tertiary hospitals expand outreach programs, shipping cooled biologics and cannabinoid formulations under stringent chain-of-custody protocols. Pandemic-era flexibilities around controlled-substance e-scripts persist in many jurisdictions, bolstering sustained volume migration to digital channels across the Tourette syndrome treatment market.

Geography Analysis

North America Tourette Syndrome Treatment Market

North America accounted for 42.10% of the Tourette syndrome treatment market share in 2025, leveraging mature insurance systems and prolific clinical-trial networks. Mayo Clinic’s biomarker breakthrough cements the region’s research authority, while FDA orphan-drug pathways shorten time-to-market for innovators. Yet high co-pays on newer agents spark adherence drop-offs, prompting advocacy for copay-assistance programs. Cross-border telehealth agreements between the United States and Canada enable specialist consult pooling, widening patient reach.

Europe Tourette Syndrome Treatment Market

Europe delivers consistent, protocol-driven care anchored by national health systems. The multicenter CANNA-TICS study typifies the continent’s collaborative posture toward alternative therapeutics, spurring policy debate on wider cannabinoid access. Northern European reimbursement standards readily cover CBIT and, increasingly, responsive DBS, whereas Southern markets still ration device spending. Diverse payer policies encourage manufacturers to tailor price-volume agreements per member state, influencing launch sequencing strategies within the Tourette syndrome treatment market.

APAC Tourette Syndrome Treatment Market

Asia-Pacific posts a 6.29% CAGR through 2031 as diagnosis rates rise in China and India’s tier-two cities. Japan’s expert-consensus guidelines deliver some of the world’s most detailed dosing frameworks, accelerating clinician uptake of VMAT-2 inhibitors. Governments invest in neurology centers of excellence that couple genetic screening with tele-CBIT outreach to remote prefectures. Local production of generic antipsychotics lowers entry costs, though import dependency for novel agents persists until domestic licensing catches up. Cultural stigma remains a barrier, but social-media advocacy drives earlier care-seeking among urban millennials, enlarging the treated base.

Competitive Landscape

The tourette syndrome treatment industry displays moderate fragmentation as legacy multinationals and agile biotechs contest share. No single firm exceeds one-quarter revenue, positioning the field for partnership flux and licensing trades. Neurocrine continues iterative VMAT-2 research after mixed Tourette read-outs, banking on reformulated candidates with tighter receptor footprints. Emalex’s Phase 3 triumph underscores the disruptive potential of focused innovators securing orphan-drug protections and venture capital heft.

Digital-therapeutic entrants layer medication management with real-time tic-tracking algorithms, forming service bundles that appeal to payers seeking outcome-based contracts. Large pharma shops eye these platforms for companion-diagnostic deals that could elevate adherence data visibility. Consolidation trends surfaced when Lundbeck absorbed Longboard Pharmaceuticals, underscoring pipeline-diversification motives in neuroscience portfolios.

Gene-therapy pioneers monitor FDA’s KEBILIDI approval as regulatory precedent for neural vector delivery. Start-ups targeting interneuron restoration scout academic alliances at institutions like Mayo Clinic to secure biomarker validation. Meanwhile, cannabinoid formulators cultivate clinical-grade supply chains to satisfy growing European demand. Competitive intensity therefore rests on dual fronts: pharmacologic novelty and ecosystem-wide patient-engagement solutions within the Tourette syndrome treatment market.

Tourette Syndrome Treatment Industry Leaders

AstraZeneca Plc

Reviva Pharmaceuticals Inc.

Viatris Inc.

Otsuka Holdings Co. Ltd

Teva Pharmaceutical Industries Ltd

- *Disclaimer: Major Players sorted in no particular order

Tourette Syndrome Treatment Market Companies Covered in this Report

- AstraZeneca

- Viatris

- Otsuka

- Reviva Pharmaceuticals

- Teva Pharmaceutical Industries

- Catalyst Pharmaceuticals Inc.

- Neurocrine Biosciences

- Novartis

- Eli Lilly and Company

- Pfizer

- Johnson & Johnson

- Abbvie

- Lundbeck A/S

- Emalex Biosciences

- Sage Therapeutics

- Ipsen

- Aptinyx Inc.

- Psyadon Pharmaceuticals

- Amryt Pharma

- Zynerba Pharma

Recent Industry Developments in Tourette Syndrome Treatment Market

- June 2025: Mayo Clinic published evidence of cortical interneuron deficits as diagnostic biomarkers, opening precision-therapy avenues.

- March 2025: Neurocrine presented new INGREZZA data at leading neurology congresses, reinforcing sustained efficacy in tardive dyskinesia.

- February 2025: Relmada Therapeutics purchased Sepranolone rights from Asarina Pharma, broadening its neurology pipeline.

- February 2025: Emalex Biosciences completed Phase 3 trials for its novel Tourette therapy, setting the stage for an FDA submission.

- January 2025: Neurocrine Biosciences opened Phase 1 enrollment for NBI-1065890, a next-generation VMAT-2 inhibitor aimed at refined dopamine release modulation.

Tourette Syndrome Treatment Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the Tourette syndrome treatment market as all paid interventions, approved medicines, structured behavioral programs such as Comprehensive Behavioral Intervention for Tics, and surgical or device-based neuromodulation delivered to children, adolescents, and adults diagnosed with Tourette syndrome worldwide. According to Mordor Intelligence, values are expressed in constant 2025 US dollars at the point of patient expenditure or hospital procurement.

Scope Exclusion: Purely supportive mobile apps or self-help wearables that lack clinical validation sit outside this scope.

Segments Covered in This Report

- By Drug Class

- Typical Antipsychotics

- Atypical Antipsychotics

- VMAT-2 Inhibitors

- Alpha-2 Adrenergic Agonists

- Benzodiazepines

- Dopamine-Modulating Agents

- Cannabinoid-Based Therapies

- By Treatment Modality

- Pharmacological Therapies

- Behavioral Therapies (CBIT, HRT, Etc.)

- Deep-Brain Stimulation

- Emerging Gene & Cell Therapies

- By Age Group

- Children & Adolescents (<18 Yrs)

- Adults (19-59 Yrs)

- Geriatric (60 + Yrs)

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts held structured calls with pediatric neurologists, adult movement disorder specialists, behavioral therapists, and payer representatives across North America, Europe, and Asia Pacific. Interviews clarified treated patient shares, average therapy intensity, pricing corridors, and likely reimbursement shifts, which helped close data gaps spotted in secondary work.

Desk Research

We began with large public datasets such as CDC morbidity surveys, NIH clinical trials dashboards, Eurostat hospital discharge files, and UN population prospects, followed by association white papers from the Tourette Association of America and the European Society for the Study of Tourette Syndrome. Financial clues were gathered from company 10-Ks, patent libraries through Questel, and news flows in Dow Jones Factiva. D&B Hoovers supplied revenue splits for key drug makers. These are illustrative; many additional open and licensed sources fed our evidence base.

Market-Sizing & Forecasting

A top-down prevalence model estimates the pool of diagnosed Tourette cases in each country and then applies region-specific treatment seeking rates and average annual spend per therapy line. Supplier roll-ups of key antipsychotic and VMAT-2 inhibitor sales plus counts of deep brain stimulation implants validate and fine-tune the totals. Core variables include diagnosed prevalence, uptake of VMAT-2 inhibitors, growth in CBIT session volumes, DBS procedure counts, reimbursement coverage expansion, and median drug price inflation. Forecasts to 2030 use multivariate regression that links those drivers to historical spending trends, and results are stress tested with scenario analysis shared with our expert panel.

Data Validation & Update Cycle

Outputs pass two analyst reviews, anomaly checks against external health spend benchmarks, and variance reconciliation before sign-off. We refresh the entire model every twelve months, with interim revisions triggered by major drug approvals or pricing changes so clients always receive the latest view.

How Mordor Intelligence's Tourette Syndrome Treatment Market Size Compares to Other Published Estimates

Published market estimates often differ because firms pick dissimilar service mixes, patient pools, and refresh cadences.

Key gaps arise when other publishers restrict scope to drug sales, fold Tourette into broader tic disorders, or retain static prevalence ratios that miss the impact of earlier diagnosis and wider insurance cover now visible in 2025. Mordor's disciplined variable selection and annual update rhythm keep figures aligned with real world demand signals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.71 B (2025) | Mordor Intelligence | - |

| USD 2.07 B (2022) | Regional Consultancy A | Drugs only and static prevalence assumptions |

| USD 2.40 B (2023) | Global Consultancy B | Excludes behavioral and neuromodulation spends |

These comparisons show that our balanced mix of therapeutic modalities, live prevalence tracking, and yearly model refresh produces a dependable baseline that decision makers can trace back to clear, reproducible steps.

Key Questions Answered in the Report

What is the current size of the Tourette syndrome treatment market?

The Tourette syndrome treatment market size reached USD 2.85 billion in 2026 and is projected to grow to USD 3.64 billion by 2031.

Which drug class is expanding fastest?

VMAT-2 inhibitors are advancing at a 7.02% CAGR through 2031, outpacing all other pharmacologic segments.

How big is the pediatric segment?

Pediatric patients represented 66.04% of the Tourette syndrome treatment market size in 2025, reflecting the disorder’s childhood onset.

Which region will grow quickest?

Asia-Pacific is forecast to post a 6.29% CAGR to 2031, driven by expanding diagnosis rates and improving insurance coverage.

Are behavioral therapies covered by insurance?

Yes, major U.S. payers now reimburse CBIT after accumulating evidence of efficacy, reducing out-of-pocket costs for families.

What are the main cost barriers?

Annual comprehensive care can exceed USD 15,000, and deep-brain stimulation surpasses USD 100,000, limiting access in emerging markets without robust insurance support.

Page last updated on: