Hungary Mobile Virtual Network Operator Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 91.64 Million |

| Market Size (2030) | USD 126.29 Million |

| Growth Rate (2025 - 2030) | 6.62% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hungary Mobile Virtual Network Operator Market Analysis by Mordor Intelligence

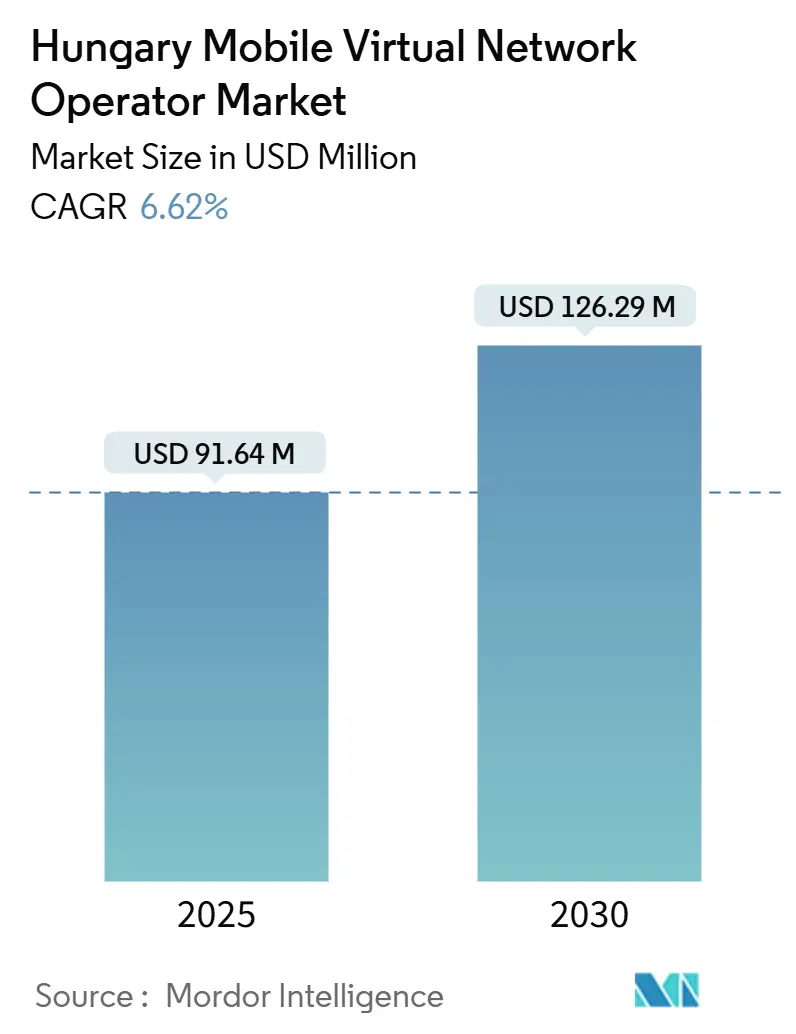

The Hungary Mobile Virtual Network Operator Market size is estimated at USD 91.64 million in 2025, and is expected to reach USD 126.29 million by 2030, at a CAGR of 6.62% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 286.92 thousand subscribers in 2025 to 380.95 thousand subscribers by 2030, at a CAGR of 5.83% during the forecast period (2025-2030).

Consistent household 5G coverage of 83.7%, the rapid spread of eSIM-enabled devices, and wholesale 4G/5G access mandates keep entry barriers manageable even as host-network consolidation lowers the number of MNOs to three. Digital-only onboarding trims acquisition costs, while EU “roam-like-at-home” rules ensure service-quality parity abroad, letting Hungarian providers address cross-border traffic without premium pricing. Specialized IoT connectivity, satellite partnerships, and private 5G campus networks widen addressable use cases across manufacturing, logistics, and agriculture. At the same time, near-universal SIM penetration and aggressive quad-play bundles force MVNOs to compete on differentiated service layers rather than headline tariffs.

Key Report Takeaways

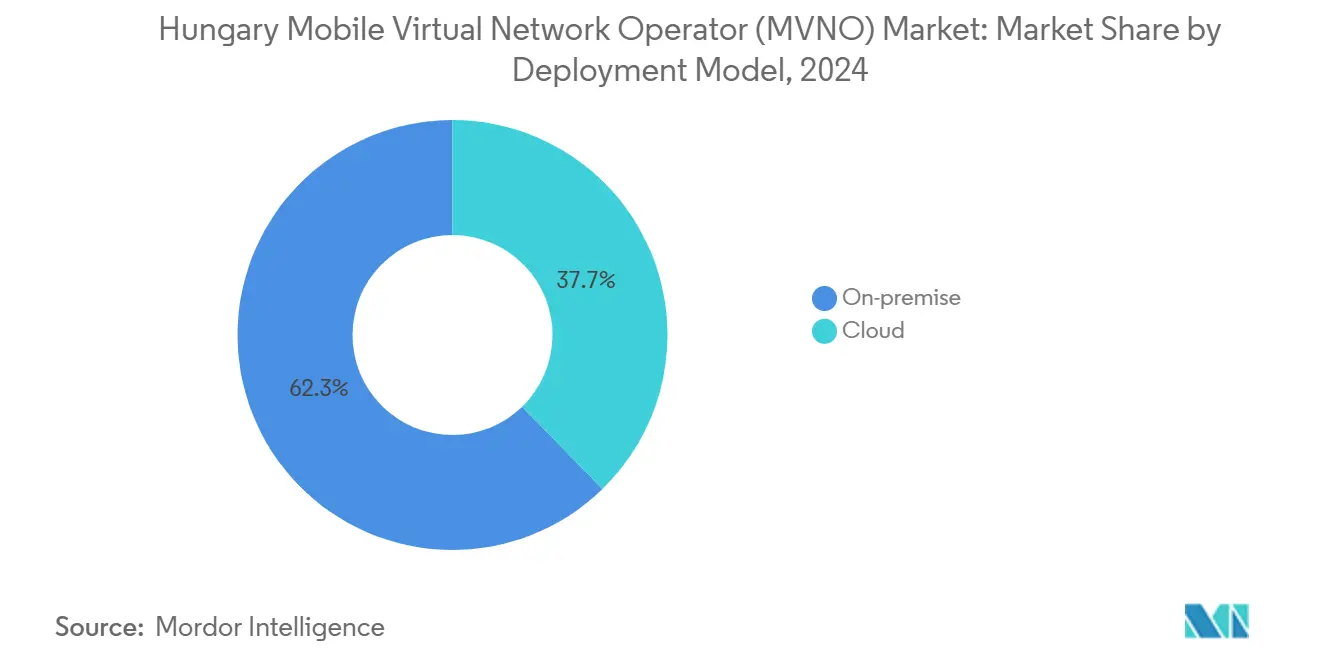

- By deployment model, on-premise platforms captured 62.28% share of the Hungary Mobile Virtual Network Operator (MVNO) market size in 2024, yet cloud-based solutions will grow at 19.56% CAGR during the forecast period.

- By operational mode, reseller/light/brand MVNOs led with 54.49% revenue share in 2024, whereas service operators are set to expand at a 13.77% CAGR to 2030.

- By subscriber type, consumer lines held 94.88% of the Hungary Mobile Virtual Network Operator (MVNO) market size in 2024, while IoT-specific services are advancing at a 17.44% CAGR through 2030.

- By application, discount plans dominated with a 43.25% share in 2024, while cellular M2M services are poised to rise at an 18.69% CAGR to 2030.

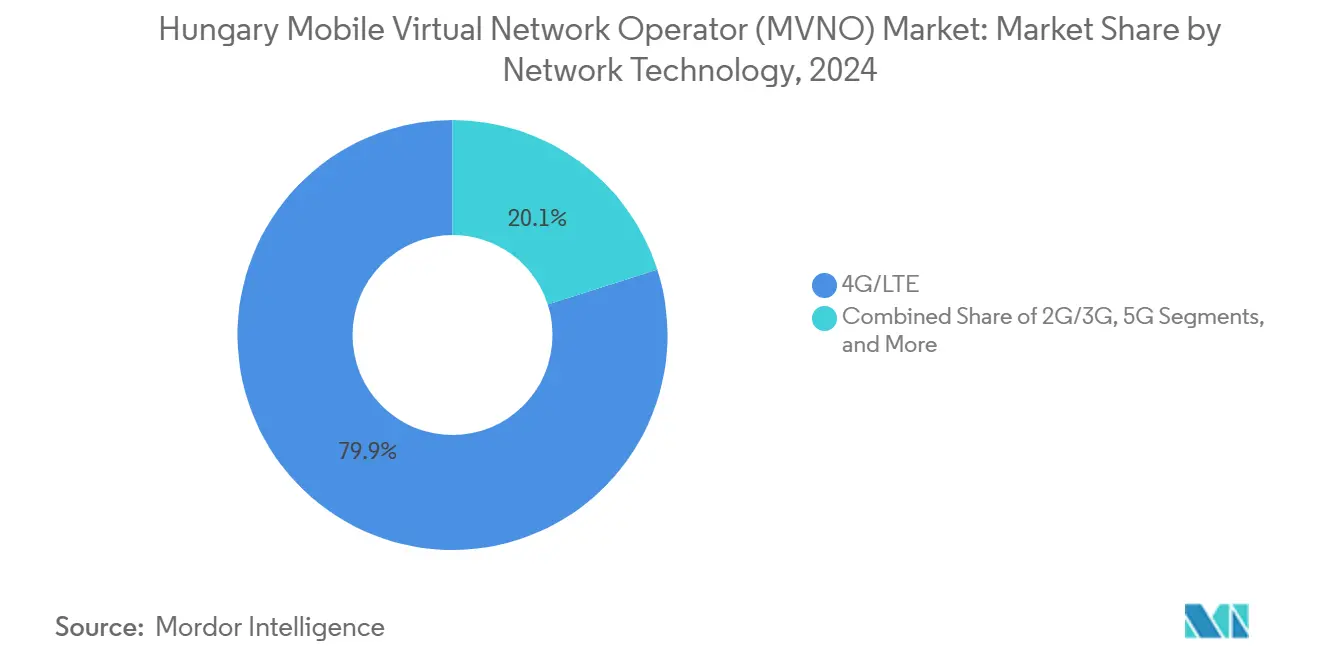

- By network technology, 4G/LTE commanded 79.93% of the Hungary MVNO market share in 2024, while satellite/NTN connections are forecast to surge at a 47.11% CAGR to 2030.

- By distribution channel, online and digital-only sales accounted for 47.94% of the Hungary Mobile Virtual Network Operator market market size in 2024 and will climb at a 12.12% CAGR to 2030.

Hungary Mobile Virtual Network Operator Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising price-sensitivity among Hungarian prepaid and hybrid subscribers | +1.2% | Budapest, Debrecen, Szeged metro zones | Short term (≤ 2 years) |

| EU “Roam-Like-at-Home” policy boosting cross-border MVNO traffic | +0.8% | Border counties with Austria, Slovakia, Romania | Medium term (2-4 years) |

| Accelerating eSIM and digital-only onboarding reducing customer acquisition cost | +1.5% | Urban centers, tech-savvy cohorts | Medium term (2-4 years) |

| Wholesale 4G/5G access mandates strengthening MVNO bargaining power | +0.9% | Nationwide | Long term (≥ 4 years) |

| Spectrum-sharing rules enabling niche 5G campus networks for industry 4.0 | +0.7% | Western and Central industrial belts | Long term (≥ 4 years) |

| Multi-IMSI connectivity needs of OEM-led automotive exports | +0.6% | Vehicle-manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Price-Sensitivity Among Prepaid and Hybrid Users

Average monthly prepaid costs range from HUF 739 to HUF 10,901, making low-price offers highly attractive to budget-conscious subscribers [1]National Media and Infocommunications Authority, “Average Monthly Cost of Prepaid Mobile Packages – April 2025,” nmhh.hu. Annual tariff indexation of 3.5-3.7% by major MNOs magnifies this sensitivity, pushing users toward discount MVNOs. Netfone Mobile’s 74.21% revenue jump in 2024 illustrates how lean, multi-network resellers monetized the trend through unlimited data plans. Competitive pricing remains an effective acquisition lever even in a saturated voice market, boosting migration from incumbent prepaid brands. Consequently, value-oriented propositions are likely to secure incremental share within the Hungary MVNO market.

Accelerating eSIM and Digital-Only Onboarding

Yettel’s Yepp service enables instant sign-up, remote identity verification, and domestic unlimited data via eSIM [2] Yettel Hungary, “Yepp Digital Subscription Launch,” yettel.hu. The model removes SIM-card logistics and shortens activation windows from days to minutes, cutting acquisition cost per user. International aggregators such as Airalo mirror the approach, marketing Hungary mobile virtual network operator (MVNO) market offers to inbound travelers. Dual-SIM phones let subscribers keep an existing number while adding a short-term MVNO plan, broadening addressable segments. Lower onboarding friction increases churn velocity but simultaneously expands overall SIM demand for secondary and tertiary use cases.

EU “Roam-Like-at-Home” Quality Parity

Since 2022, European rules obligate host networks to supply 4G/5G abroad at domestic retail prices, ending historic quality downgrades [3]European 5G Observatory, “June 2024 Biannual Report,” 5gobservatory.eu. Hungary’s seven land borders make cross-border commuters a sizeable base for MVNOs offering fixed-fee roaming. Wholesale parity reduces cost uncertainty, supporting sustainable margins even for smaller players. The regulation also reassures consumers that roaming performance will match domestic experience, a decisive factor for business travelers and freight drivers crossing the Schengen perimeter. Enhanced roaming, therefore, enlarges potential traffic volumes for the Hungary mobile virtual network operator market.

Wholesale 4G/5G Access Mandates

EU competition rules require nondiscriminatory wholesale terms, empowering MVNOs to negotiate capacity on reasonable rates. With 4,300 5G sites delivering 83.7% household reach, Hungary hosts adequate spectrum to support third-party services. The planned spin-off of Magyar Telekom’s towers into a neutral entity will reinforce passive-infrastructure openness. Stronger bargaining power enables MVNOs to lock in multi-year capacity, underpinning investment in niche propositions such as private 5G slices for factories. As a result, wholesale safeguards sustain supply diversity despite MNO consolidation.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Near-100% SIM penetration and falling ARPU depressing margin headroom | -1.8% | Entire country | Short term (≤ 2 years) |

| Aggressive quad-play bundles by MNOs raising switching costs | -1.1% | Fiber-rich urban corridors | Medium term (2-4 years) |

| Possible network-wholesale tightening after state-backed 4iG-Yettel tie-ups | -0.9% | Nationwide | Medium term (2-4 years) |

| Immature 5G-SA MVNE stack delaying IoT-centric MVNO launches | -0.7% | Industrial IoT regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Near-100% SIM Penetration and Falling ARPU

Hungary reports virtually universal mobile penetration, so providers must win users from rivals instead of tapping unsupplied demand. Market maturity drags blended ARPU to EUR 15.8 per month, leaving little headroom for MVNO mark-ups. Heavy price competition depresses gross margins and elongates payback periods on customer acquisition spend. While new use cases such as connected sensors raise line counts, the revenue per line for low-bandwidth IoT remains small. High penetration, therefore, tempers near-term growth for the Hungary MVNO market.

Aggressive Quad-Play Bundles by MNOs

Integrated operators bundle mobile with gigabit fiber, PayTV, and streaming to create sticky service portfolios. Discounts across access lines, content, and hardware installment plans boost switching costs for households. Standalone MVNOs struggle to replicate four-service packages without owning fixed assets, weakening value perception among bundle-seeking families. Although regulation bars tying practices, the convenience of single billing and unified customer care remains a competitive moat. Converged offers thus narrow the consumer pool open to MVNO migration, especially in big cities where fiber coverage is dense.

Segment Analysis

By Deployment Model: Cloud Adoption Accelerates Service Launches

On-premise deployments accounted for 62.28% of the Hungary mobile virtual network operator (MVNO) market size in 2024 as enterprises favored direct hardware control and data-sovereignty compliance. Large banks and utilities retain physical cores to meet internal security standards, stabilizing demand for on-site platforms. Even so, cloud solutions are growing fastest at 19.56% CAGR because they minimize capex and provide elastic scaling for seasonal traffic peaks. Vendor offerings with pre-integrated OSS/BSS stacks shorten roll-out cycles from months to weeks, enabling new entrants to test propositions with lower risk.

Cloud expansion also supports low-latency features via regional edge nodes, a prerequisite for factory automation and smart-port logistics. Hybrid topologies surface when firms mix on-premise policy engines with cloud packet gateways for field assets. The model lets industrial players apply granular control to production traffic while leveraging unified orchestration for remote assets. As hyperscalers open Hungarian availability zones, latency gaps versus on-premise shrink further, fueling wider adoption within the Hungary MVNO market.

By Operational Mode: Service Operators Outperform

Reseller/light/brand players held 54.49% of 2024 revenue due to minimal infrastructure outlays and quick time-to-market. Netfone’s multi-MNO approach showed how pooled coverage and aggressive pricing resonate with value seekers. Still, Service Operators are forecast to log a 13.77% CAGR by adding core network elements such as HLR/HSS and policy servers. Partial control lets them tailor quality of service tiers and enterprise-grade VPNs, unlocking higher ARPU verticals.

Full MVNOs remain capital-intensive, but secure independence over roaming, IMSI ranges, and service quality, a strategic asset for export-oriented IoT projects. The operational-mode mix illustrates a shift from cost-focused resale toward capability-rich service provisioning as specialized demand scales. Cross-border logistics firms, for example, prize guaranteed throughput during border hand-offs, while campus-network tenants value private slices. Depth of control, therefore, becomes a selling point within the Hungary mobile virtual network operator market.

By Subscriber Type: IoT Lines Gain Momentum

Consumer accounts still dominate at 94.88% in 2024, reflecting Hungary’s mature handset landscape. Prepaid youth and migrant communities form the bulk of churn-ready prospects, incentivizing simple, app-managed plans. Enterprise subscriptions, though a smaller base, show steady additions across fleet management, payment terminals, and CCTV backhaul.

The standout growth story involves IoT-specific lines, set to grow at a 17.44% CAGR. Private 5G at East-West Gate Terminal boosted container throughput 40% after adopting sensor-rich cranes, demonstrating near-term productivity gains. Such results spur manufacturers to embed connectivity from the design stage, driving multi-IMSI SIM orders for exported vehicles and machinery. As sensor density climbs, IoT will account for an outsized share of incremental SIM additions to the Hungary MVNO market.

By Application: Cellular M2M Leads Next-Wave Use Cases

Discount voice-and-data packages retained 43.25% of 2024 revenue, underpinned by price-sensitive prepaid cohorts. Business applications remain important to SMEs that need managed connectivity with predictable billing and customer support.

Cellular M2M shows the fastest 18.69% CAGR through 2030. Remote metering, predictive maintenance, and smart-agriculture sensors all rely on secure, low-latency links. Reported private-network deployments deliver 20-90% productivity lifts and up to 40% OPEX savings, aligning cost with rapid payback horizons. Other niche uses, such as travel eSIMs and ethnic-community bundles, round out service portfolios but lack the scale of industrial automation. The shift toward machine traffic underlines the deepening diversification of the Hungary mobile virtual network operator market.

By Network Technology: 4G Dominates but Satellite Surges

4G/LTE underpinned 79.93% of active lines in 2024 owing to near-ubiquitous coverage and affordable devices. Vodafone’s 3G sunset accelerates spectrum re-farming to LTE, boosting capacity and spectral efficiency. 5G adoption quickened after Yettel launched standalone mode in 2023, allowing network slicing for latency-critical workloads.

Satellite/NTN links, although embryonic, are set for a 47.11% CAGR. Low-Earth-orbit constellations extend coverage to remote oil fields, Danube shipping lanes, and mountain tourist zones. GSMA counts 91 operator-satellite tie-ups that collectively touch roughly 5 billion subscribers worldwide, underscoring collective confidence in direct-to-handset models. This momentum will gradually embed satellite fallback into enterprise SIM portfolios, broadening the Hungary MVNO market reach.

By Distribution Channel: Digital-Only Sales Take Center Stage

Online portals and app-based flows captured 47.94% of 2024 activations and will grow 12.12% CAGR as eKYC regulations mature. Yepp’s fully digital plan set a local benchmark by combining unlimited data, immediate eSIM download, and 24-hour chat support. Retail stores remain relevant for device bundling and elderly customers who prefer face-to-face service. Carrier sub-brands maintain premium experiences with curated handset ranges, while wholesale partners extend reach into electronics chains and e-commerce sites.

Identity-verification rules still require occasional in-person checks, but regulators are piloting remote biometric onboarding that could soon make the process end-to-end digital. Once adopted, paperless flows will further compress activation costs, letting MVNOs reinvest savings into targeted marketing. The channel transition, therefore, underpins future subscriber growth in the Hungary MVNO market.

Geography Analysis

The Hungary mobile virtual network operator (MVNO) market concentrates heavily in Budapest, which hosts more than one-third of mobile lines and enjoys 90% 5G outdoor coverage. Affluent consumers seek unlimited data, and enterprises demand managed IoT links for smart buildings, supporting premium MVNO sub-brands. Secondary cities such as Debrecen, Szeged, and Pecs show double-digit subscriber growth as younger users hunt for low-cost data options. Regional universities attract international students who favor travel eSIMs, further enlarging digital-only uptake.

Rural counties lag in disposable income, yet offer headroom for agriculture IoT. Farms employ soil-moisture sensors and livestock trackers that communicate via narrow-band LTE, creating incremental SIM demand. Government smart-village grants encourage local councils to pilot connected streetlighting and waste-collection solutions, drawing in M2M-centric MVNOs.

Border districts benefit most from roam-like-at-home parity. Daily commuters to Austria and Slovakia adopt dual-number plans that merge domestic allowances with cross-border voice. Freight carriers on the Budapest-Bucharest corridor prefer SIMs with bundled EU data to avoid bill shocks. As a landlocked hub with seven neighbors, Hungary thus leverages its geographic position to expand roaming traffic within the Hungary MVNO market.

Competitive Landscape

Industry consolidation reshaped host-network availability when 4iG merged Vodafone Hungary and DIGI into the One Hungary brand in 2025. The move shrank host choices from four to three but yielded a nationwide footprint spanning 135 retail outlets and 98 settlements. Magyar Telekom’s planned tower spin-off will inject more neutrality into the passive layer, partially offsetting wholesale leverage held by integrated carriers.

Netfone demonstrates that lean operations and multi-network access can still thrive. Its unlimited-data offers captured prepaid switchers and produced a five-fold jump in net profit during 2024. International eSIM players such as Soracom market Hungary MVNO market data packs via global apps, capturing tourists before arrival. Industrial specialists, including Intelliport, supply 450 MHz SIMs for utilities needing deep-indoor reach.

Competitive focus is turning to user experience and vertical integration rather than headline gigabyte pricing. Providers differentiate on self-care app design, real-time spend controls, and tailored enterprise APIs. Satellite partnerships and private 5G orchestration modules serve as further levers to secure niche segments. Overall, the Hungary MVNO market now balances three powerful host groups against a widening array of agile, digitally native MVNO brands.

Hungary Mobile Virtual Network Operator Industry Leaders

Netfone Telecom Ltd.

4iG Plc

Soracom, Inc.

Airalo Pte. Ltd.

Tarr Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: 4iG completed the operational merger of Vodafone Hungary and DIGI under One Hungary, creating the country’s largest converged operator.

- September 2024: 4iG signed an MoU with North Macedonia to explore telecom entry, extending its Western Balkans footprint.

- August 2024: Magyar Telekom transferred 2 × 5 MHz of 2100 MHz spectrum to Yettel Hungary, optimizing 4G/5G capacity for both parties.

- July 2024: 4iG acquired PR-Telecom, adding 3,400 km of fiber that passes 250,000 homes, strengthening fixed-line presence.

Hungary Mobile Virtual Network Operator Market Report Scope

| Cloud |

| On-premise |

| Reseller / Light / Brand MVNO |

| Service Operator |

| Full MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online / Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party / Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller / Light / Brand MVNO |

| Service Operator | |

| Full MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online / Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party / Wholesale |

Key Questions Answered in the Report

What is the 2025 value of the Hungary mobile virtual network operator (MVNO) market?

The Hungary mobile virtual network operator (MVNO) market size stands at USD 91.64 million in 2025.

How fast is the Hungary MVNO market expected to grow?

It is forecast to register a 6.62% CAGR between 2025 and 2030.

Which subscriber type is growing the quickest?

IoT-specific lines are projected to expand at a 17.44% CAGR through 2030, reflecting demand from Industry 4.0 projects.

Why are digital-only plans important in Hungary?

ESIM-based, app-managed offers cut activation costs and attract tech-savvy users, supporting rapid line additions.

How will host-network consolidation affect MVNOs?

Fewer MNOs may tighten wholesale terms, yet infrastructure spin-offs and EU access mandates preserve bargaining power for MVNOs.

Which technology segment shows the highest growth potential?

Satellite/NTN connectivity is forecast to rise at a 47.11% CAGR, extending coverage to remote and maritime applications.

Page last updated on: