Luxembourg Mobile Virtual Network Operator Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

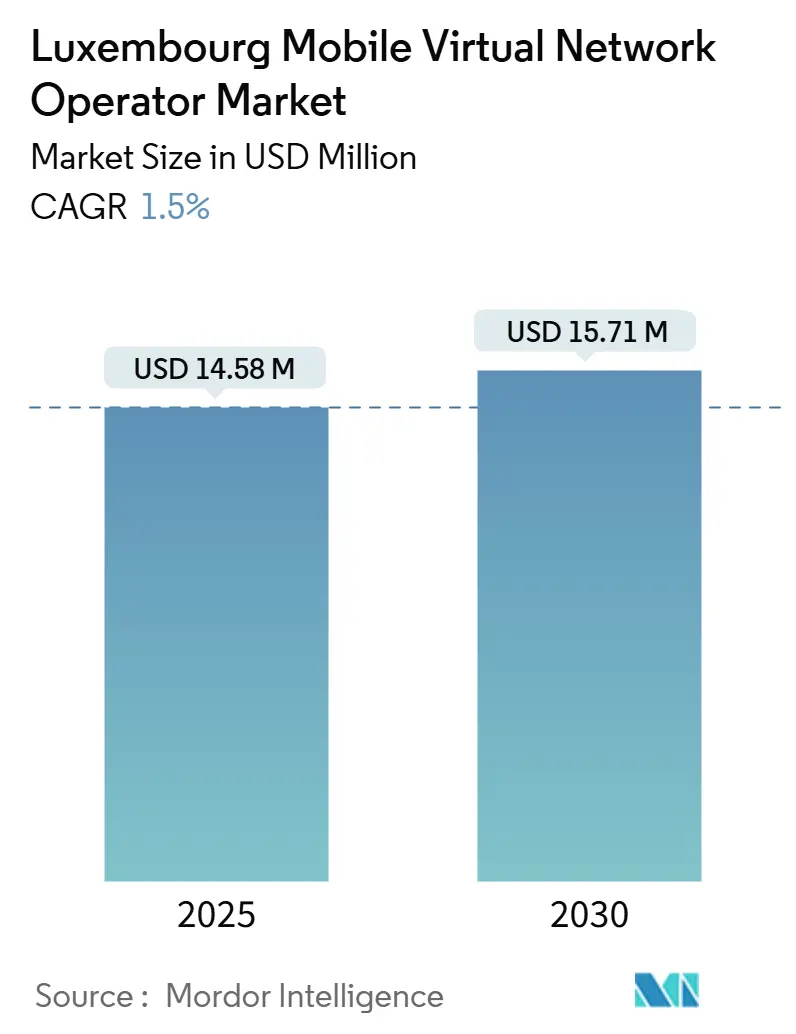

| Market Size (2025) | USD 14.58 Million |

| Market Size (2030) | USD 15.71 Million |

| Growth Rate (2025 - 2030) | 1.50% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Luxembourg Mobile Virtual Network Operator Market Analysis by Mordor Intelligence

The Luxembourg Mobile Virtual Network Operator Market size is estimated at USD 14.58 million in 2025, and is expected to reach USD 15.71 million by 2030, at a CAGR of 1.5% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 94.20 thousand subscribers in 2025 to 104 thousand subscribers by 2030, at a CAGR of 2% during the forecast period (2025-2030).

Luxembourg’s near-universal 5G household coverage, regulatory mandates that assure wholesale access, and a cross-border workforce exceeding 200,000 commuters anchor steady demand for virtual mobile services [1]European Commission, “Luxembourg 2024 Digital Decade Country Report,” digital-strategy.ec.europa.eu. Cloud-based deployments dominate because enterprises favor scalable, remotely managed platforms, while government-backed satellite initiatives signal the next wave of connectivity innovation that may bypass terrestrial bottlenecks. Specialized segments, chiefly enterprise M2M and IoT, are expanding much faster than legacy voice services as Luxembourg cements its role as a European financial center with stringent operational-resilience mandates under DORA. Competitive intensity is moderate; three infrastructure owners supply wholesale capacity, yet low notification fees and enforced number portability let niche MVNOs enter quickly and carve out profitable micro-segments.

Key Report Takeaways

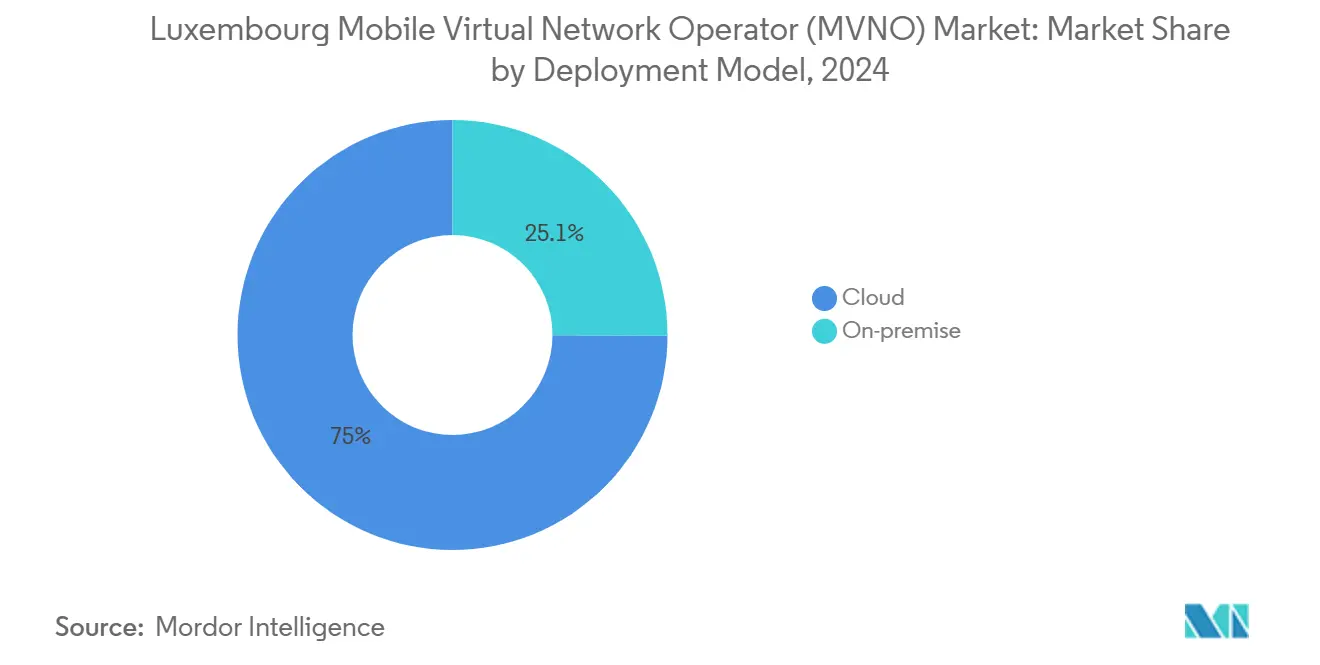

- By deployment model, cloud solutions held 74.95% revenue share in 2024, and it is projected to grow at a 5.03% CAGR through 2030.

- By operational mode, reseller/light/brand MVNOs captured 56.16% of the Luxembourg mobile virtual network operator market share in 2024, while full MVNOs are advancing at an 8.19% CAGR through 2030.

- By subscriber type, consumer connections led with 51.72% in 2024; IoT-specific subscriptions are expected to expand at a 12.33% CAGR to 2030.

- By application, discount plans accounted for 39.61% of the Luxembourg MVNO market size in 2024, and cellular M2M is rising at an 8.19% CAGR through 2030.

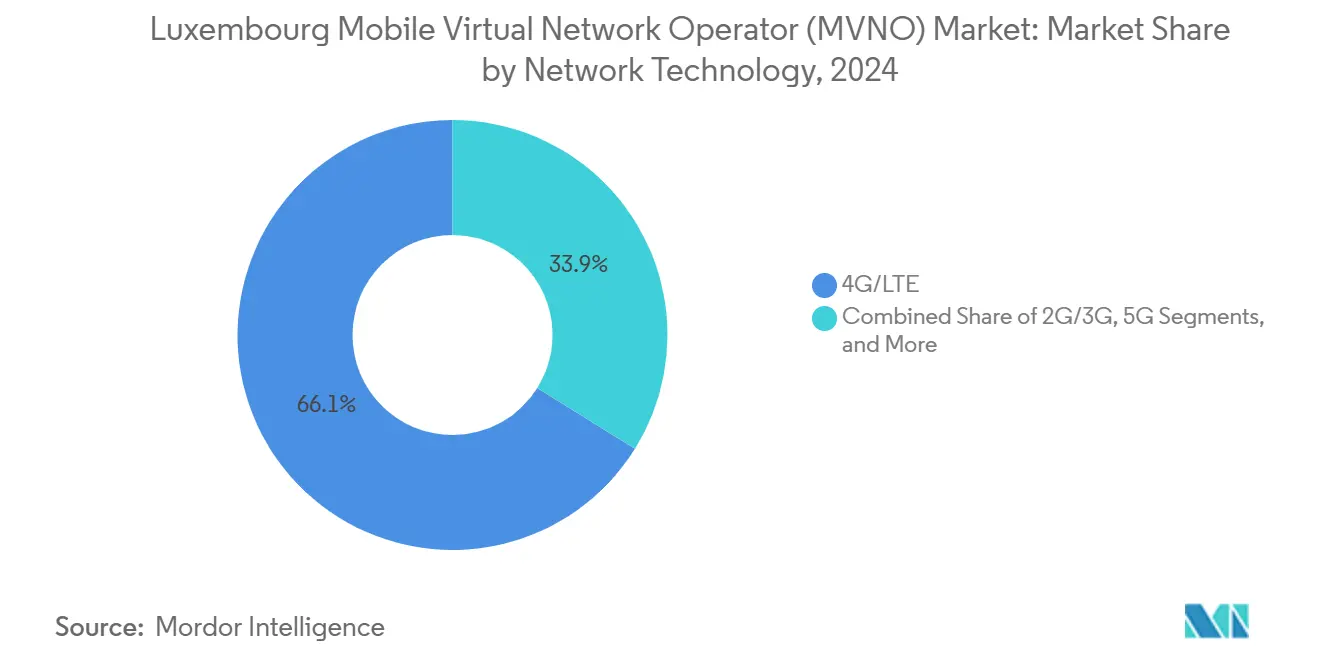

- By network technology, 4G/LTE dominated with 66.12% share in 2024; satellite/NTN solutions exhibit a 93.22% CAGR through 2030.

- By distribution channel, online and digital-only sales commanded a 61.96% share in 2024, widening further at a 4.75% CAGR on the back of eSIM-enabled onboarding.

Luxembourg Mobile Virtual Network Operator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-sensitive migrant workforce demanding low-price prepaid offers | +0.3% | National, with spillover to cross-border regions | Short term (≤ 2 years) |

| Enterprise M2M/IoT connectivity uptake in finance and logistics | +0.4% | National, concentrated in Luxembourg City financial district | Medium term (2-4 years) |

| ILR-mandated wholesale access and number portability | +0.2% | National | Long term (≥ 4 years) |

| eSIM-enabled digital onboarding lowering entry barriers | +0.3% | National | Medium term (2-4 years) |

| Government space-economy push spurring satellite-backed MVNO models | +0.2% | National, with EU cross-border applications | Long term (≥ 4 years) |

| EU cross-border commuting intensifying “roam-like-at-home” propositions | +0.1% | Cross-border regions (France, Belgium, Germany) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cost-Sensitive Migrant Workforce Demanding Low-Price Prepaid Offers

Cross-border employees represent 44% of Luxembourg’s labor force and sustain a recurring need for low-cost, flexible voice-and-data bundles that eliminate roaming surcharges [2]Government of the Grand Duchy of Luxembourg, “Cross-border public transportation gratuity,” luxembourg.public.lu. Their price sensitivity underpins prepaid growth and accelerates the adoption of MVNOs such as MTX Connect, which markets contract-free data eSIMs to frequent travelers. Labor-market studies show employers struggle with commuter integration, reinforcing demand for multilingual helplines and tailored billing cycles. The EU’s push for digital identity interoperability, evidenced by French citizens activating Luxembourg services via France Identité, eases onboarding and undercuts legacy SIM logistics. Accordingly, the Luxembourg mobile virtual network operator market gains incremental uplift from prepaid propositions that blend local usage with borderless allowances.

Enterprise M2M/IoT Connectivity Uptake in Finance and Logistics

Roughly 3 million devices already run on POST Telecom’s global IoT platform, illustrating the scale of machine connectivity rooted in Luxembourg’s finance and logistics sectors [3]POST Telecom, “Connectivité IoT mondiale – POST,” post.lu. Proximus NXT’s nationwide NB-IoT footprint lets financial institutions deploy tamper-proof metering and secure transaction terminals, a capability amplified by the Digital Operational Resilience Act from January 2025. MVNOs that package SIM-agnostic provisioning, granular SLAs, and compliance logging can command premium pricing in this segment. Public-sector digital-transformation funding worth EUR 302 million further bolsters enterprise adoption of cloud-centric mobile services.

ILR-Mandated Wholesale Access and Number Portability

The Institut Luxembourgeois de Regulation obliges host MNOs to provide non-discriminatory access, imposes a EUR 2,500 notification fee instead of a traditional license, and caps annual levies at 0.65% of turnover. The watchdog’s SmartCompare.lu portal launched in 2024, boosting consumer switching and transparency. MVNOs can therefore concentrate resources on differentiated value propositions instead of license compliance, enhancing long-run growth prospects for the Luxembourg MVNO market.

eSIM-Enabled Digital Onboarding Lowering Entry Barriers

POST Luxembourg’s QR-based eSIM launched at EUR 5 proves consumer readiness for fully digital activations. Because retail rents in Luxembourg City remain high and vacancies are limited, bypassing physical SIM distribution slashes operating expenditures for virtual operators. Moreover, 60.1% of residents possess at least basic digital skills, accelerating uptake of app-based identity checks and instant provisioning. The result is a structurally faster sign-up funnel, which in turn enlarges the addressable base for the Luxembourg mobile virtual network operator market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Small national subscriber base limiting scale efficiencies | -0.2% | National | Long term (≥ 4 years) |

| Elevated wholesale access fees compressing MVNO margins | -0.3% | National | Medium term (2-4 years) |

| GDPR + CSSF data-security compliance inflating OPEX | -0.1% | National, with EU regulatory alignment | Short term (≤ 2 years) |

| Scarce and costly retail space in Luxembourg City | -0.1% | Luxembourg City commercial districts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Small National Subscriber Base Limiting Scale Efficiencies

With only 672,000 residents, Luxembourg offers limited headroom for mass-market scaling, a challenge underscored by total mobile revenue of EUR 598.1 million in 2023. Retail-space constraints compound acquisition costs, driving MVNOs toward niche strategies or cross-border bundles to maintain viable customer-lifetime values.

Elevated Wholesale Access Fees Compressing MVNO Margins

Mobile CAPEX hit EUR 28.2 million in 2023, and infrastructure owners are recouping investment through higher wholesale tariffs that squeeze reseller margins. Proximus’s EUR 108 million tower sale illustrates the capital intensity underpinning these fees, making cost management critical for the Luxembourg MVNO industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Dominance Drives Digital Transformation

Cloud deployments accounted for 74.95% of the Luxembourg Mobile Virtual Network Operator Market share in 2024 and are advancing at a 5.03% CAGR through 2030. This segment benefits from Luxembourg’s resilient data-center ecosystem and the Digital Decade fund of EUR 302 million that prioritizes public-sector cloud adoption. The Luxembourg Mobile Virtual Network Operator (MVNO) Market size tied to on-premise solutions remains small, preserved mainly for highly regulated banking applications demanding local data residency under CSSF guidance.

Enterprises migrating toward API-driven service platforms derive operational agility and proactive SLA dashboards that mitigate downtime. Further convergence with eSIM orchestration reduces logistics overhead, lifting gross margins for MVNOs operating purely in the cloud. Meanwhile, the government’s nationwide fiber backbone and the LU-CIX 400 G upgrade strengthen backhaul resiliency, permitting higher-order virtualization workloads to flourish.

By Operational Mode: Full MVNO Growth Signals Market Maturation

Reseller models seized 56.16% revenue in 2024 due to their rapid time-to-market and minimal CAPEX requirements. However, the Luxembourg mobile virtual network operator market size accruing to full MVNO architectures is rising at an 8.19% CAGR as operators seek deeper control over billing, numbering, and core-network functions to differentiate beyond price.

Greater service autonomy allows full MVNOs to embed custom encryption modules and real-time analytics demanded by Luxembourg’s finance sector. The ILR’s straightforward authorization framework and mandatory number portability lessen friction in migrating to proprietary core networks. Consequently, infrastructure-light resellers are re-evaluating uplift paths toward service-operator or full-core status to safeguard long-term relevance within the Luxembourg mobile virtual network operator market.

By Subscriber Type: IoT Transformation Reshapes Revenue Streams

Consumer lines formed 51.72% of subscriptions in 2024, yet IoT-dedicated SIMs exhibit a 12.33% CAGR, reflecting a structural pivot toward automation and smart-city deployments. Enterprise connections hold stable demand for high-SLA services, underpinning blended ARPU levels well above EU averages.

The Luxembourg MVNO market size from IoT devices is propelled by ubiquitous NB-IoT coverage and forthcoming satellite-direct-to-device proofs, giving enterprises seamless fallback paths in latency-sensitive workflows. MVNOs that offer self-service onboarding portals and cross-border eSIM profiles stand to lock in long contracts, minimizing churn versus consumer segments.

By Application: Cellular M2M Drives Enterprise Innovation

Discount plans garnered 39.61% of 2024 revenue, yet cellular M2M solutions within the Luxembourg MVNO market are expanding at an 8.19% CAGR through 2030. Business-class bundles appeal to the headquarters of multinational firms requiring encrypted voice, priority data lanes, and multi-currency invoicing.

Satellite-enabled 5G IoT represents a breakthrough avenue as OQ Technology pursues a 30-satellite constellation that promises seamless device connectivity in rural worksites, shipping corridors, and financial disaster-recovery zones. This diversification mitigates dependence on price-sensitive discount offerings and elevates the strategic posture of the Luxembourg Mobile Virtual Network Operator market.

By Network Technology: Satellite/NTN Emergence Transforms Connectivity Paradigms

4G/LTE furnished 66.12% of traffic in 2024, but satellite/NTN links are clocking a 93.22% CAGR, the fastest of any segment in the Luxembourg MVNO market. 5G SA rollouts by Orange and Tango will widen outdoor coverage beyond 90% by late 2025, narrowing latency gaps versus fiber.

Government grants under LuxIMPULSE accelerate R&D for direct-to-phone satellite messaging, offering MVNOs redundancy and unique SLAs for critical-infrastructure customers. As terrestrial sunset plans phase out 2G/3G, handset refresh cycles provide opportune inflection points for MVNO migrations onto dual terrestrial-satellite profiles that ensure always-on service, vital for the finance sector’s operational-resilience mandates.

By Distribution Channel: Digital-First Strategies Dominate Market Access

Online storefronts produced 61.96% of 2024 gross additions and are expected to grow at a 4.75% CAGR to 2030, leveraging Luxembourg’s 60% digital-skills penetration and eSIM uptake for near-instant activation. Traditional retail persists for high-touch service demos but is constrained by a 14.3% vacancy rate in city centers that drives rental premiums.

Carrier sub-brands and wholesale channels increasingly serve migrant workers at transit hubs, offering multilingual SIM pick-ups. Digital onboarding, powered by eIDAS, streamlines KYC across borders, ensuring the Luxembourg MVNO market continues to tilt toward mobile apps, chatbots, and self-care dashboards.

Geography Analysis

Luxembourg’s domestic footprint forms the nucleus of revenue generation, underpinned by 99.6% 5G household coverage and some of Europe’s highest disposable-income levels. Dense fiber and plentiful data centers enable MVNOs to monetize premium connectivity and low-latency links essential for banking and fund-administration clients. Regulatory clarity, rapid number portability, and SmartCompare.lu enhance market liquidity, encouraging customer churn toward value-added propositions that sustain ARPU above EU medians.

Neighboring France, Belgium, and Germany collectively send around 200,000 workers daily into Luxembourg, expanding the effective addressable base beyond the resident population. MVNOs tailor plans that merge domestic allowances with seamless roaming to the commuters’ home networks under the EU’s roam-like-at-home regime. Multilingual support and SEPA-wide billing cement customer loyalty. Enterprises operating cross-border logistics chains also tap unified IoT SIM profiles, reducing complexity across customs checkpoints.

Broader EU expansion is within reach for Luxembourg-based full MVNOs that leverage the country’s regulatory credibility and satellite-innovation ecosystem. LuxIMPULSE-funded NTN research positions local operators to export hybrid terrestrial-satellite packages throughout European rural industries. The Luxembourg MVNO market thus serves as a proving ground for niche, high-margin propositions adaptable to other small yet affluent EU states.

Competitive Landscape

Three host networks, POST, Tango, and Orange, dominate wholesale supply, resulting in moderate concentration and creating bargaining leverage for specialized MVNO entrants. POST maintains a technological lead via its global IoT management platform and early eSIM rollout, giving partners enterprise-grade tooling. Tango rides Proximus’s NB-IoT network to service industrial automation, while Orange emphasizes 5G SA for consumer multimedia.

MTX Connect focuses on international data-only eSIMs, capturing traveler spend otherwise lost to Wi-Fi rentals. OQ Technology is using LuxIMPULSE grants and a EUR 30 million funding quest to stitch satellite backhaul into MVNO packages, offering coverage in maritime zones and construction sites beyond terrestrial reach. Tower monetization, illustrated by Proximus’s EUR 108 million sale to InfraRed Capital Partners, could spur neutral-host opportunities that further increase retail competition.

Sustainable differentiation hinges on bundling compliance features such as GDPR-ready data stores and DORA-aligned reporting. Firms that integrate chat-based support and AI-driven network analytics also gain customer-experience advantages difficult for price-led resellers to replicate. Consequently, the Luxembourg MVNO market favors operators able to balance niche focus with technology depth, rather than sheer subscriber scale.

Luxembourg Mobile Virtual Network Operator Industry Leaders

e-LUX Mobile Telecommunication S.A.

Soracom Inc.

Truphone (1GLOBAL Holdings B.V.)

Things Mobile S.R.L.

MTX Connect S.R.L.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Proximus Group closed the EUR 108 million divestment of Proximus Luxembourg Infrastructure to InfraRed Capital Partners, forming the country’s first independent TowerCo while retaining anchor-tenant rights.

- November 2024: ILR introduced SmartCompare.lu, a free online comparator covering all fixed and mobile offers to nurture transparent consumer choice.

- November 2024: OQ Technology began a EUR 30 million Series B raise to scale its 5G IoT satellite fleet to 30 spacecraft and widened its footprint to Greece, Saudi Arabia, and Rwanda.

- February 2024: OQ Technology and the European Space Agency signed MACSAT 2.0 to study direct-to-cell satellite voice and messaging under LuxIMPULSE funding.

Luxembourg Mobile Virtual Network Operator Market Report Scope

| Cloud |

| On-premise |

| Reseller / Light / Brand MVNO |

| Service Operator |

| Full MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online/Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party/Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller / Light / Brand MVNO |

| Service Operator | |

| Full MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online/Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party/Wholesale |

Key Questions Answered in the Report

How fast is the Luxembourg MVNO market expected to grow through 2030?

The Luxembourg MVNO market is projected to expand from USD 14.58 million in 2025 to USD 15.71 million in 2030, registering a 1.5% CAGR.

Which deployment model leads revenue today?

Cloud deployment holds 74.95% of 2024 revenue, reflecting Luxembourg’s well-developed data-center infrastructure.

What subscriber segment is growing the quickest?

IoT-specific SIMs are increasing at 12.33% CAGR, outpacing consumer and enterprise lines.

Why are satellite/NTN technologies important for Luxembourg?

Government-backed programs such as LuxIMPULSE fund projects that let MVNOs integrate direct-to-device satellite coverage, enabling ubiquitous connectivity where terrestrial 4G/5G is unavailable.

How do ILR rules benefit new MVNO entrants?

Operators need only a EUR 2,500 notification under Luxembourg’s general authorization and enjoy mandatory wholesale access plus capped annual fees, cutting entry barriers significantly.

What role does cross-border commuting play in market demand?

Roughly 200,000 daily commuters from France, Belgium, and Germany seek roaming-inclusive bundles, making specialized cross-border plans a core revenue niche for local MVNOs.

Page last updated on: