Austria Mobile Virtual Network Operator (MVNO) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

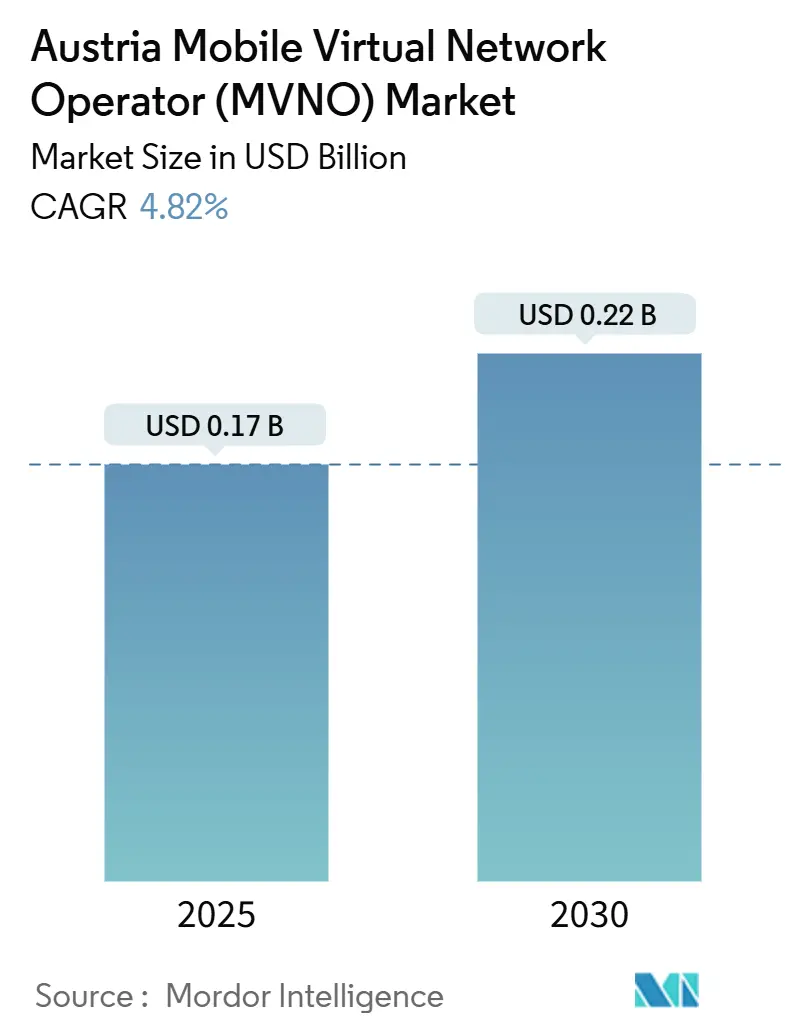

| Market Size (2025) | USD 0.17 Billion |

| Market Size (2030) | USD 0.22 Billion |

| Growth Rate (2025 - 2030) | 4.82% CAGR |

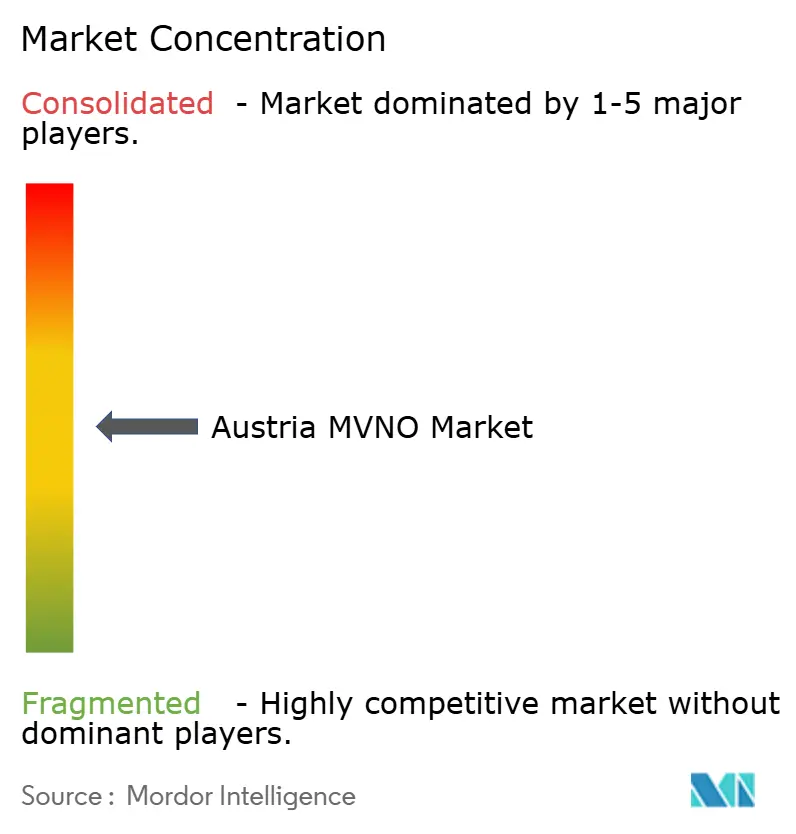

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Austria Mobile Virtual Network Operator (MVNO) Market Analysis by Mordor Intelligence

The Austria MVNO Market size is estimated at USD 0.17 billion in 2025, and is expected to reach USD 0.22 billion by 2030, at a CAGR of 4.82% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 1.17 million subscribers in 2025 to 1.39 million subscribers by 2030, at a CAGR of 3.54% during the forecast period (2025-2030). Measured expansion mirrors a mature cellular landscape in which favorable wholesale‐access regulation supports competition while subscriber saturation tempers headline growth. Continuous infrastructure upgrades by host operators A1, Magenta, and Drei keep network quality among Europe’s best, enabling virtual brands to guarantee service parity with facilities-based rivals. Cloud-native enablement, accelerating eSIM uptake and demand for enterprise private networks, underpins revenue diversification opportunities, whereas wholesale fee structures, limited direct spectrum control, and near-saturated penetration restrict margin expansion. Competitive strategies gravitate toward digital-only distribution, price transparency, and verticalized IoT solutions that elevate average revenue per user without network ownership.

Key Report Takeaways

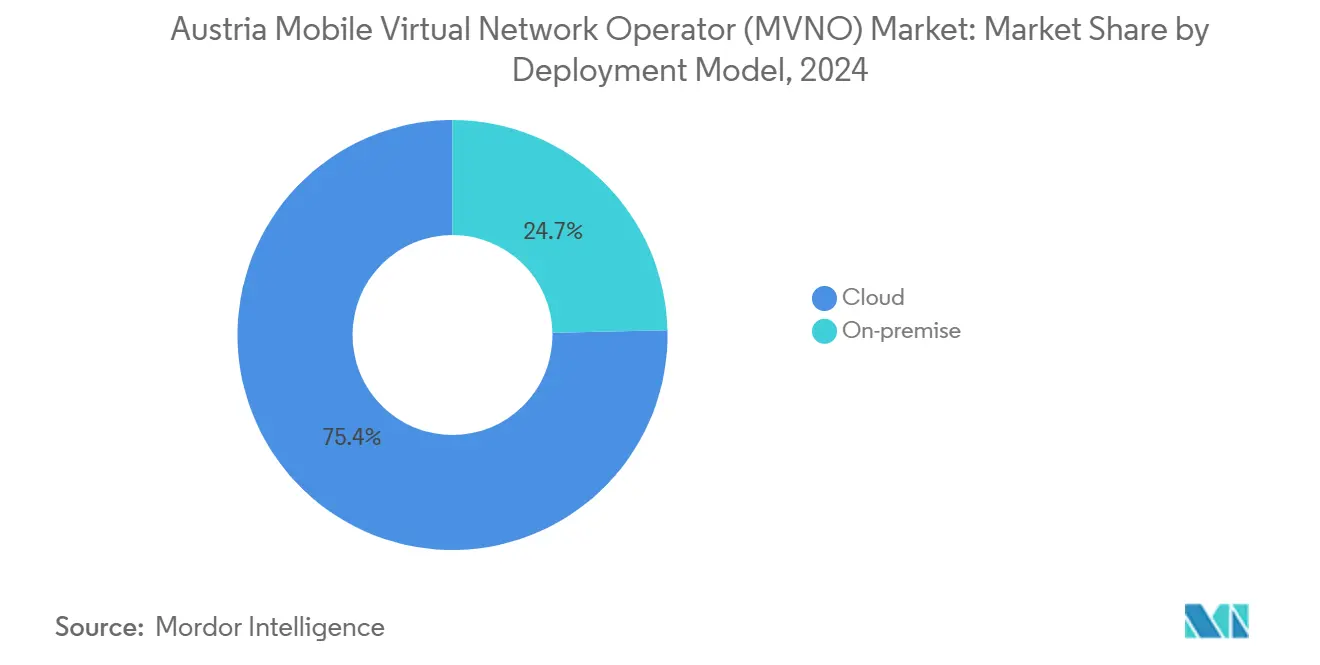

- By deployment model, cloud infrastructure led with a 75.35% revenue share in 2024, and is projected to expand at a 7.97% CAGR through 2030.

- By operational mode, reseller/light/brand MVNOs held 59.66% of the Austria MVNO market share in 2024, whereas full MVNOs post the fastest 21.14% CAGR to 2030.

- By subscriber type, consumer services accounted for an 81.74% share in 2024, while IoT-specific subscriptions rose at a 22.59% CAGR to 2030.

- By application, the other application segment captured 40.31% of the Austria MVNO market size in 2024; cellular M2M lines advance at an 18.49% CAGR between 2025-2030.

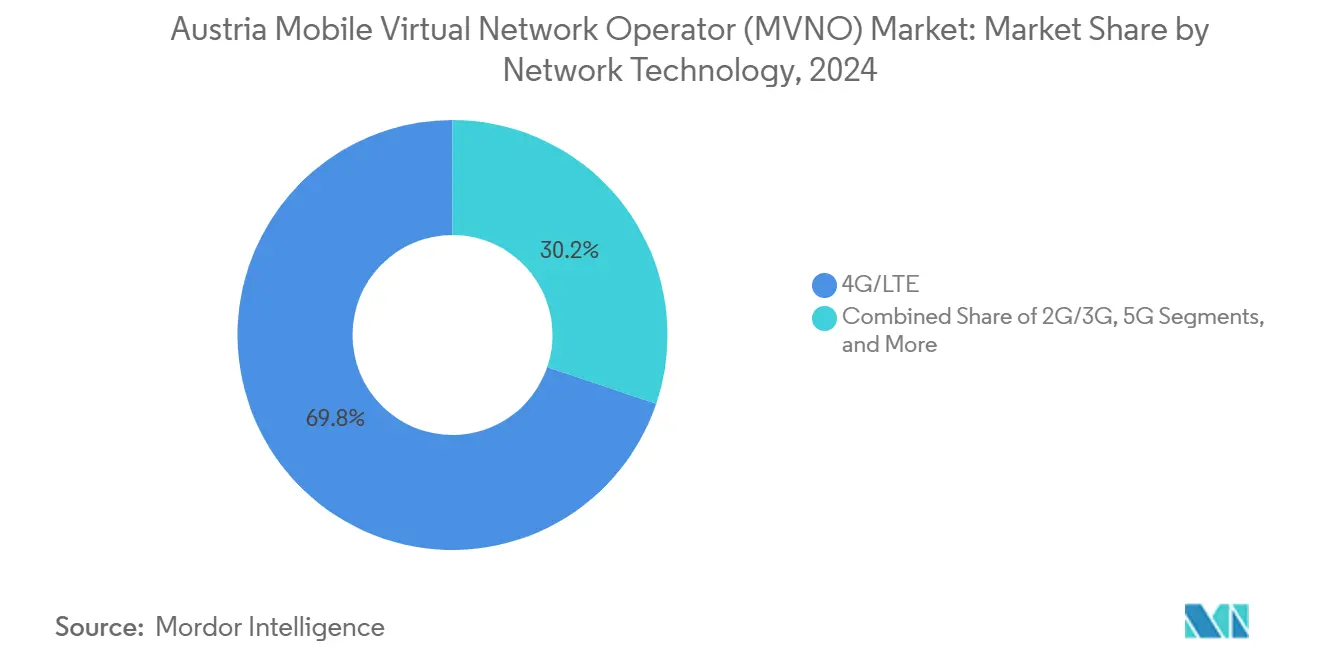

- By network technology, 4G/LTE connections dominated with 69.81% share in 2024, yet Satellite/NTN exhibits a breakout 99.54% CAGR on a nascent base.

- By distribution channel, online/digital-only sales represented 60.48% of 2024 revenue, and the same channel is set to log a 7.95% CAGR through 2030.

Austria Mobile Virtual Network Operator (MVNO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating eSIM adoption enabling friction-less onboarding | +0.8% | Austria and wider DACH region | Short term (≤ 2 years) |

| Intensifying price sensitivity amid inflationary pressure | +0.6% | Urban Austria | Medium term (2-4 years) |

| EU-driven wholesale access regulations (EECC) | +0.5% | Austria under EU mandate | Long term (≥ 4 years) |

| 5G SA wholesale deals allowing premium MVNO services | +0.9% | Vienna and Graz first-wave areas | Medium term (2-4 years) |

| Digital-first retail brands seeking loyalty adjacencies | +0.4% | E-commerce hubs across Austria | Short term (≤ 2 years) |

| Private-network and IoT slice demand from enterprises | +1.2% | Industrial regions and smart-city zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating eSIM Adoption Enabling Friction-less Onboarding

eSIM eliminates physical SIM logistics, letting Austrian MVNOs activate service in minutes through digital channels [1]Rundfunk und Telekom Regulierungs-GmbH, “Onlinesicherheit – RTR,” rtr.at. Fast activation resonates with digital-native consumers and frequent travelers who prioritize instant connectivity. Lower fulfilment cost widens gross margin headroom even under fixed wholesale fees. The technology also simplifies international expansion because the same remote-SIM-provisioning platform can localize plans in multiple markets. Regulatory identity-verification requirements remain unchanged, ensuring compliance consistency. Early movers Spusu and HoT report higher digital-channel conversions after introducing eSIM downloads; this is expected to accelerate overall Austria MVNO market penetration in the short term.

Intensifying Price Sensitivity Amid Inflationary Pressure

Inflation has nudged Austrian households toward a lower total cost of ownership when selecting mobile service [2]Die Presse Redaktion, “Weniger Wettbewerb bei Handy-Tarifen?” diepresse.com. Transparent tariff structures and contract-free offers, typical for virtual brands, align well with this sentiment. Host-network quality parity means consumers sacrifice little in perceived performance when shifting to value MVNOs. MNOs respond through promotions, yet their higher cost bases limit their ability to match discount levels sustainably. The heightened comparison shopping raises churn in premium brands, funneling incremental share toward the Austria MVNO market. Over 2025-2027, price elasticity will likely remain elevated, benefiting operators that optimize digital sales funnels and self-care apps.

EU-driven Wholesale Access Regulations (EECC)

The EECC obliges national regulators to ensure fair, transparent, and non-discriminatory wholesale access, which strengthens MVNO negotiating power with host networks. Austrian enforcement now extends to quality-of-service and 5G standalone features, protecting MVNO parity as networks evolve. Improved contractual certainty attracts foreign virtual brands considering Austrian entry and supports local MVNO scalability. Over the long term, better access terms translate into incremental margin recovery that can be reinvested in marketing and service innovation. The framework also provides a template for Austrian operators expanding into other EU states, reducing regulatory friction.

5G Stand-Alone Wholesale Deals Allowing Premium MVNO Services

Standalone 5G permits network slicing, ultra-low-latency performance, and IoT mass connectivity that previously required infrastructure ownership. Drei’s LoRaWAN partnership illustrates how MNOs open specialized wholesale products targeting industrial and municipal IoT needs [3]Kurrant Media, “Drei and Actility Enhance Austria’s IoT,” kurrant.com . MVNOs can now bundle premium enterprise connectivity or gaming-grade latency offerings, lifting ARPU beyond traditional discount positioning. Early availability in Vienna and Graz establishes proof-of-concept for nationwide rollouts. Host operators benefit from incremental traffic monetization without channel conflict, reinforcing collaborative dynamics. Over the medium term, this driver adds 0.9 percentage points to the Austria MVNO market CAGR as service diversity widens addressable revenue.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| MNO wholesale fee structures squeezing MVNO margins | -1.1% | Nationwide | Medium term (2-4 years) |

| Limited direct spectrum control curbing service innovation | -0.7% | Especially for premium services | Long term (≥ 4 years) |

| Near-saturation of Austria’s mobile subscriber base | -0.9% | Dense urban markets | Short term (≤ 2 years) |

| MVNO consolidation risk amid rising cost of scale | -0.6% | Smaller Austrian operators | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

MNO Wholesale Fee Structures Squeezing MVNO Margins

Host operators must recoup 5G and fiber backhaul investments, and wholesale tariffs remain their primary recovery mechanism. Current fee schedules compress gross margins by an estimated 5-6 percentage points versus 2022 levels, challenging small MVNO sustainability. Operators must therefore scale subscriber bases, optimize cloud BSS/OSS, and automate support to avoid negative operating leverage. Fee rigidity also restricts the ability to launch loss-leader tariffs, giving MNO sub-brands a relative pricing advantage. Without additional regulatory intervention or innovative revenue-share models, this restraint will shave almost one percentage point off the Austria MVNO market growth over 2025-2028.

Limited Direct Spectrum Control Curbing Service Innovation

Because virtual operators do not hold licensed spectrum, they rely on MNOs for network feature prioritization. This dependence limits the capacity to guarantee ultra-reliable low-latency service or deterministic quality for mission-critical IoT. Premium enterprise tenders often favor facilities-based carriers or private-network integrators able to commit service-level agreements at the physical layer. Although EU rules mandate access to advanced features, real-time resource orchestration remains inherently constrained. Consequently, MVNOs focus on operational excellence, brand experience, and application-layer value rather than deep network differentiation. The innovation ceiling reduces upside opportunity in high-margin segments, dragging long-term Austria MVNO market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Infrastructure Drives Scalability

Cloud platforms powered 75.35% of 2024 revenue, underscoring their role as the mainstay delivery architecture for the Austria MVNO market size. Migration continued at a 7.97% CAGR to 2030 as operators shed on-premise hardware in favor of pay-as-you-grow models. Virtualized core networks let entrants launch within weeks, using shared orchestration and OSS/BSS to minimize capital exposure. Lower upfront cost also attracts B2B specialist MVNOs targeting private network or IoT niches. Furthermore, cloud hosting enables rapid geographic expansion, evidenced by spusu’s rollout in Switzerland and Italy using the same multitenant stack.

On-premise deployments persist among certain healthcare and government clients prioritizing data sovereignty, yet their share is projected to decline below 20% by 2030. Hybrid topologies are emerging, where policy control and subscriber data reside in sovereign clouds while non-sensitive workloads operate on public IaaS hosts. Performance benchmarks show negligible latency differences in metro Vienna locations, supporting continued pivot to cloud. Funding rounds such as MAVOCO’s USD 12 million (EUR 11 million) Series A signal venture confidence in cloud-centric enablement, accelerating tooling maturity, and lowering total cost of ownership. The migration maintains the operational agility essential for Austria MVNO market competitiveness.

By Operational Mode: Full MVNOs Emerge Despite Reseller Dominance

Reseller/light/brand configurations held 59.66% share of the Austria MVNO market revenue in 2024 due to their lower complexity and swift time-to-market. However, full MVNOs are forecast to grow 21.14% annually through 2030, capitalizing on expanded control across core network elements that unlock service innovation and cost optimization. The Austria MVNO market share commanded by full operators is predicted to breach 30% by 2028 as turnkey platform vendors reduce technical barriers.

Service-operator hybrids, occupying the middle ground, appeal to brands needing limited control over IMS or messaging features but unwilling to manage complete cores. CompaxDigital’s acquisition of i-new unified mobile solutions exemplifies consolidation that equips emerging MVNOs with carrier-grade full-stack capabilities. Growth of IoT verticals and roaming hubs necessitates local breakout and multi-IMSI architectures, feasible mainly under full MVNO licenses. Consequently, operational-mode migration will be a decisive factor in capturing high-value enterprise contracts within the Austria MVNO market.

By Subscriber Type: IoT Services Accelerate Beyond Consumer Base

Consumer subscriptions remained dominant at 81.74% of 2024 SIMs, sustained by prepaid voice-plus-data bundles and family packages. Yet the IoT-specific category posts a robust 22.59% CAGR, reflecting factory automation, smart agriculture, and municipal sensor projects funded under Austria’s digitalization agenda. Enterprise macro-contracts, though smaller in SIM count, deliver higher ARPU than consumer lines due to managed services overlays.

IoT specialists leverage eUICC and LPWAN wholesale frameworks to furnish low-power deployments across several thousand endpoints. Healthcare exemplifies momentum: private 5G campus networks in Burgenland hospitals require segmented SIM profiles for medical devices, pushing incremental demand toward the Austria MVNO market size. Diversifying subscriber mix cushions MVNOs against churn in saturated consumer cohorts while elevating gross margins.

By Application: Cellular M2M Growth Outpaces Traditional Segments

The other application segment, comprising data-only SIMs, multi-service family packs, and tourism passes, commanded 40.31% revenue in 2024. Meanwhile, cellular M2M solutions grow 18.49% annually as manufacturing and logistics firms digitize asset tracking [4]LORIOT AG, “LORIOT and Microtronics Partner,” loriot.io . Discount voice plans continue to attract price-sensitive users, but margin dilution curbs their strategic appeal. Business applications face stable, although slower expansion, anchored by predictable enterprise contracts.

Edge analytics bundled with connectivity differentiates M2M propositions, allowing MVNOs to monetize platform fees instead of traffic alone. Partnerships between LORIOT and Microtronics showcase end-to-end industrial monitoring that combines LoRaWAN, LTE-M, and data-visualization layers. Such value-stacking uplifts average revenue per device and positions cellular M2M as the fastest profit pool in the Austria MVNO market.

By Network Technology: Satellite/NTN Emergence Amid 5G Maturation

Terrestrial 4G/LTE accounted for 69.81% of active lines in 2024, underpinning mainstream smartphone usage. Nationwide 5G coverage already exceeds 90% of the population, yet devices remain in the early replacement cycle. Satellite/NTN connections, although representing under 1% of SIMs, expand at an extraordinary 99.54% CAGR as low-earth-orbit constellations secure European market access.

Hybrid terrestrial-satellite bundles appeal to logistics, maritime, and alpine tourism sectors where a continuous footprint is mandatory. MVNOs can broker non-terrestrial capacity through wholesale aggregators without investing in gateway infrastructure, lowering entry thresholds. Gradual phase-out of 2G/3G refarming compresses legacy traffic, freeing spectrum for 5G NR expansion. Integrating carrier aggregation and slicing capabilities will be critical to sustain Austria's MVNO market competitiveness as service expectations escalate.

By Distribution Channel: Digital-Only Channels Lead Market Evolution

Digital-only channels delivered 60.48% of 2024 subscriptions and will grow 7.95% per year, catalyzed by eSIM uptake and app-centric account management. In-app onboarding costs average 70% lower than physical SIM distribution, directly enhancing EBITDA. Retail stores remain relevant for device bundling and elderly user support, but macro-trend momentum favors online acquisition.

Carrier sub-brand stores function as experiential showrooms, bridging brand accessibility with digital self-care. Third-party electronics retailers serve impulse SIM purchases and tourist packages, yet face commission compression. Long term, chatbots and AI-driven personalization are expected to push conversion rates above 30%, reinforcing digital dominance. Efficient distribution will therefore be central to sustaining profit in the Austria MVNO market, where wholesale cost is largely fixed.

Geography Analysis

Austria’s compact geography and high network quality minimize regional service disparities, yet urban corridors such as Vienna-Graz-Linz host the densest MVNO adoption owing to younger demographics and stronger price competition. Rural alpine regions show moderate MVNO penetration, constrained by perceived reliability and lower digital-channel literacy. Comprehensive 5G coverage underpins a uniform experience nationwide, enabling brands to market single national tariffs without coverage disclaimers.

Regional economic clusters influence enterprise IoT demand: automotive supply chains around Styria prioritize low-latency 5G slices, while tourism hotspots in Tyrol value satellite-integrated roaming packages. Such localized use cases allow MVNOs to price differentiated solutions despite national wholesale agreements. Austria MVNO market participants benefit from the European Union roaming regulation that abolishes intra-EU surcharges, letting them assemble multi-country propositions attractive to cross-border commuters.

Finally, geographic scale facilitates centralized customer-support operations in Vienna, keeping overhead low compared with larger multi-country markets. Domestic saturation pushes leading brands to leverage Austrian operational hubs for outward expansion across the DACH region, exporting process efficiencies while repatriating scale economies. Geographic agility thereby becomes an indirect driver of the Austria MVNO market growth trajectory.

Competitive Landscape

The Austria MVNO market features moderate concentration: the top five virtual brands control a significant share of active SIMs, with Spusu, HoT, Bob, yesss! and T-Mobile’s leading volume segments. Spusu emphasizes international diversification and network-quality marketing, while HoT leverages supermarket distribution and loyalty integration with food-retail giant Hofer. Bob remains A1’s budget flank, preserving share through aggressive prepaid bundles and app-first support.

Strategic differentiation gravitates toward frictionless digital journeys, flexible no-lock-in tariffs, and tailored add-ons such as day-pass roaming. Full-stack enablers (CompaxDigital, MAVOCO) provide turnkey cores and orchestration, lowering barriers for niche entrants and fomenting competition. Host operators balance defensive wholesale revenue with internal sub-brand positioning, ensuring virtual partners do not erode core postpaid bases.

Network-quality parity diminishes technical gaps; hence, customer experience KPIs, NPS, onboarding time, and e-care resolution become decisive. Regulatory actions such as anti-spoofing measures standardize security expectations, spurring competitive investments in fraud analytics. Overall, rivalry intensity remains high, favoring players with scale, diversified subscriber mixes, and multi-market ambitions.

Austria Mobile Virtual Network Operator (MVNO) Industry Leaders

Spusu Ltd.

HoT Telekom and Service GmbH (Hofer Telekom)

Yesss! (A1 Telekom Austria AG)

bob (A1 Telekom Austria AG)

eety Telekom (Hutchison Drei Austria GmbH)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Gesundheit Burgenland completed Austria’s first private 5G hospital networks across multiple sites, implemented by Magenta Telekom and CANCOM Austria.

- February 2025: MAVOCO secured EUR 11 million (USD 12 million) Series A funding led by 3TS Capital Partners and red-stars.com.

- September 2024: RTR enforced anti-spoofing regulations obliging mobile operators to block fraudulent use of Austrian caller IDs.

- January 2024: CompaxDigital completed its acquisition of i-new Unified Mobile Solutions, expanding full-stack MVNO enablement capabilities.

Austria Mobile Virtual Network Operator (MVNO) Market Report Scope

| Cloud |

| On-premise |

| Reseller / Light / Brand MVNO |

| Service Operator |

| Full MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online / Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party / Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller / Light / Brand MVNO |

| Service Operator | |

| Full MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online / Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party / Wholesale |

Key Questions Answered in the Report

What is the current value of the Austria MVNO market?

It is valued at USD 0.17 billion in 2025 and is projected to reach USD 0.22 billion by 2030.

Which deployment model controls most MVNO revenue in Austria?

Cloud-based deployment accounts for 75.35% of 2024 revenue, reflecting strong preference for scalable virtual cores.

Which subscriber group is growing fastest?

IoT-specific SIMs are expanding at a 22.59% CAGR owing to enterprise digitalization and smart-city projects.

How fast is Satellite/NTN connectivity expanding?

Satellite/NTN lines show a 99.54% CAGR, the highest among network technologies even though they start from a small base.

Which restraint most limits MVNO profitability?

High wholesale fees charged by host MNOs reduce gross margins by over 5 percentage points versus 2022 levels.

How will EECC regulations influence Austrian MVNOs?

EECC enforcement ensures fair wholesale access, improving long-term margins and supporting service innovation for virtual brands.

Page last updated on: