Tunisia Mobile Virtual Network Operator Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

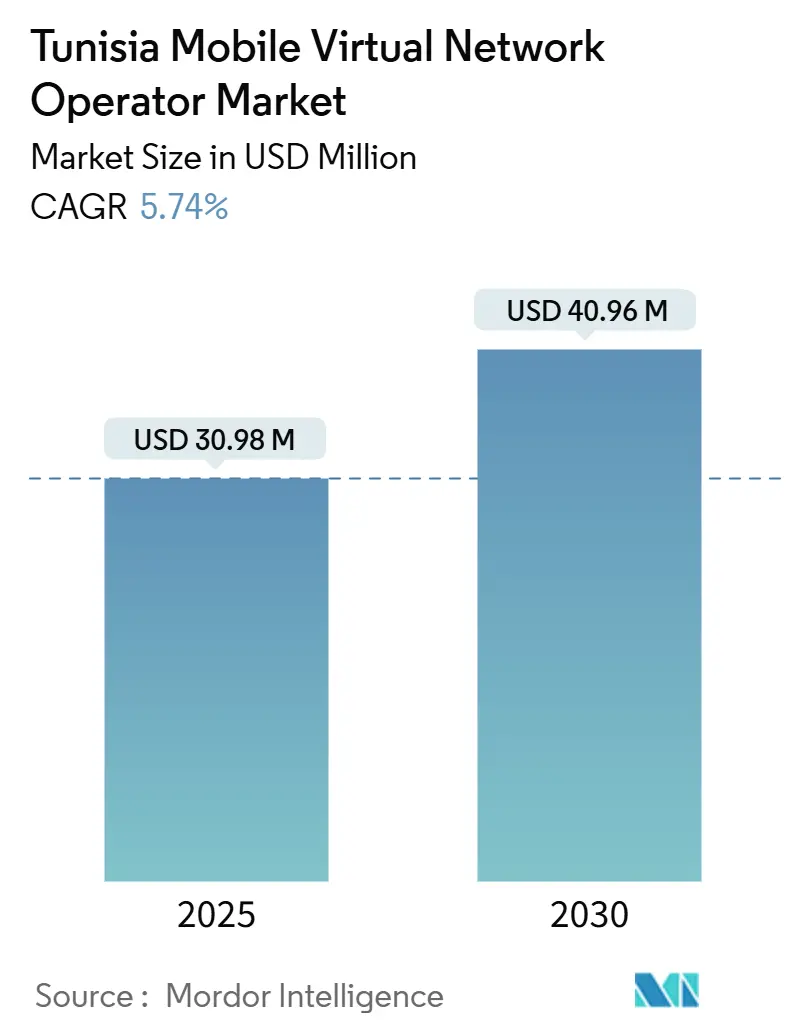

| Market Size (2025) | USD 30.98 Million |

| Market Size (2030) | USD 40.96 Million |

| Growth Rate (2025 - 2030) | 5.74% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tunisia Mobile Virtual Network Operator Market Analysis by Mordor Intelligence

The Tunisia Mobile Virtual Network Operator Market size is estimated at USD 30.98 million in 2025, and is expected to reach USD 40.96 million by 2030, at a CAGR of 5.74% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 435.46 thousand subscribers in 2025 to 538.69 thousand subscribers by 2030, at a CAGR of 4.35% during the forecast period (2025-2030).

The nation’s wholesale framework is tightly controlled by Tunisie Telecom, Ooredoo, and Orange, yet the April 2025 5G launch positions the Tunisia MVNO market for a structural step-change in service innovation. Elevated mobile penetration, strong diaspora links, and mounting demand for digital-first experiences underpin sustained subscriber additions. Cloud-native MVNE platforms, number portability, and neutral-host tower projects collectively trim entry costs, encouraging specialized entrants that address underserved consumer and IoT niches. At the same time, domestic-ownership rules and a three-operator oligopoly temper immediate scale gains, keeping the Tunisia mobile virtual network operator (MVNO) market relatively small but strategically significant within North Africa’s digital transformation agenda.

Key Report Takeaways

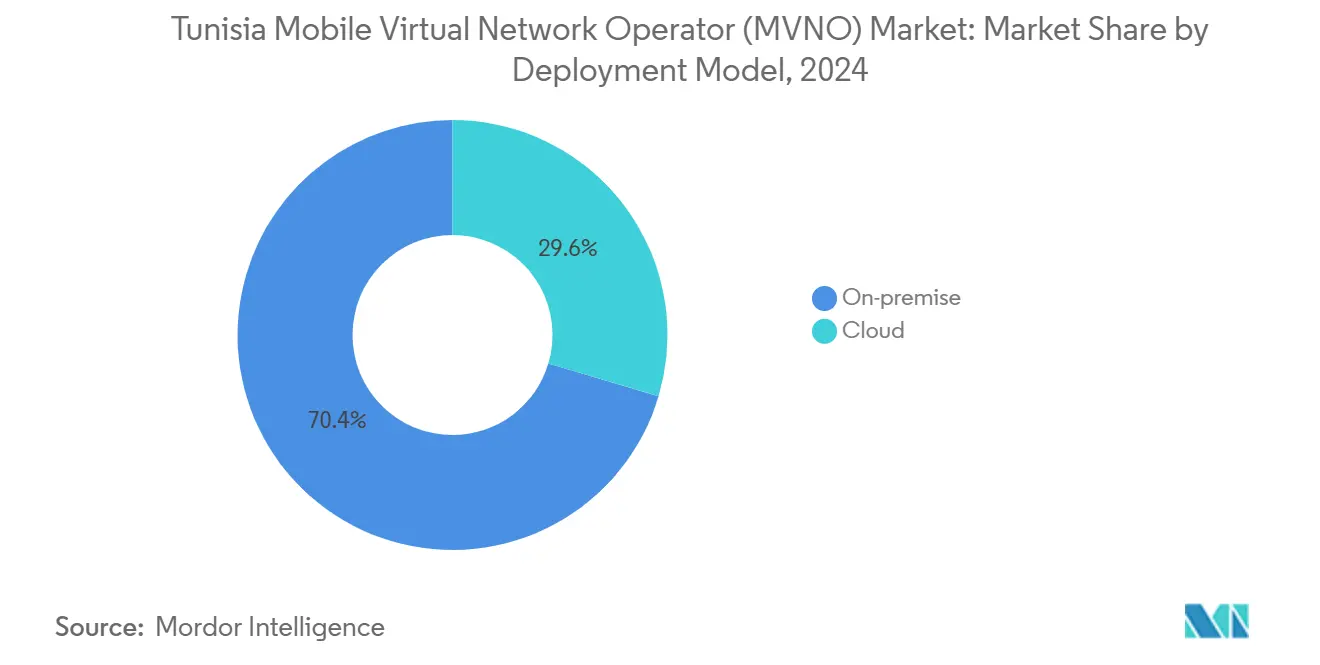

- By deployment model, on-premise solutions led with 70.41% of the Tunisia MVNO market share in 2024, while cloud deployment is projected to expand at a 22.63% CAGR through 2030.

- By operational mode, reseller and light MVNO formats commanded 72.54% of the market share in 2024, while full MVNOs are poised for 23.98% CAGR to 2030.

- By subscriber type, the consumer segment held 83.56% revenue share in 2024, while IoT-specific services are advancing at a 27.25% CAGR through 2030.

- By application, discount services captured 50.37% of the Tunisia mobile virtual network operator (MVNO) market size in 2024, and cellular M2M is pacing at a 21.31% CAGR to 2030.

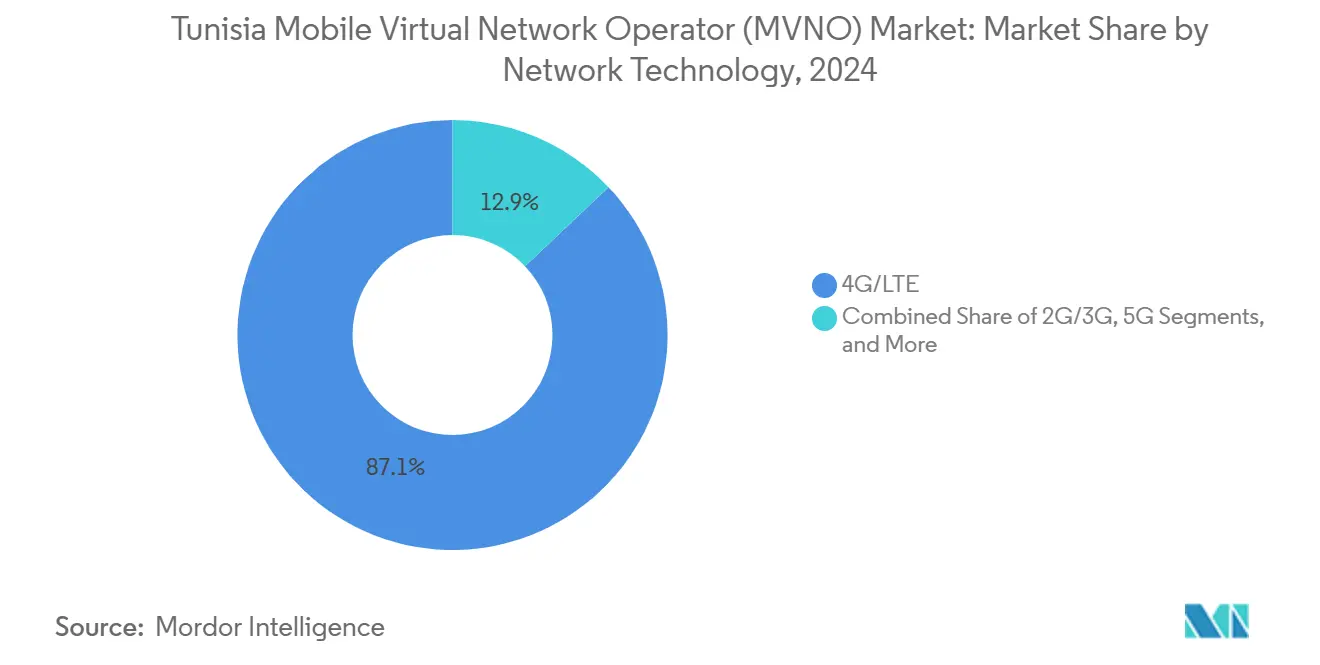

- By network technology, 4G/LTE accounted for 87.07% share of the Tunisia mobile virtual network operator market in 2024, while 5G is forecast to expand at a 57.72% CAGR to 2030.

- By distribution channel, the online/digital-only channel led with 42.35% of the Tunisia MVNO market share in 2024, and it is projected to expand at a 11.91% CAGR to 2030.

Tunisia Mobile Virtual Network Operator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imminent 5G-wholesale access licenses spur new MVNO entrants | +1.8% | Tunis-Sfax corridor | Medium term (2-4 years) |

| Cloud-native MVNE platforms slash time-to-market and CAPEX | +1.2% | National urban hubs | Short term (≤ 2 years) |

| Strong demand for low-cost international and diaspora calling plans | +0.9% | Diaspora-dense regions | Long term (≥ 4 years) |

| Mandatory mobile number portability unleashes switch-over churn | +0.7% | National | Medium term (2-4 years) |

| Youth-led fintech ecosystem seeks telco rails for super-apps | +0.6% | Urban and suburban | Medium term (2-4 years) |

| Neutral-host tower expansion cuts wholesale radio-access costs | +0.5% | Nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Imminent 5G-wholesale access licenses spur new MVNO entrants

The December 2024 5G spectrum award to all three network operators unlocked high-capacity wholesale pipes, and Tunisie Telecom activated the region’s first commercial 5G service in April 2025. Fifteen-year license tenure delivers regulatory certainty, encouraging virtual operators to invest in differentiated propositions such as ultra-low-latency enterprise links and massive IoT connectivity. Network slicing offers service-quality guarantees previously unattainable on 4G, while broader 700 MHz and 3.5 GHz allocations ease historical capacity bottlenecks. Although interconnect pricing is still brokered with the dominant trio, additional spectrum headroom reduces congestion risk, signaling a pivotal growth window for the Tunisia mobile virtual network operator (MVNO) market.

Cloud-native MVNE platforms slash time-to-market and CAPEX

Virtualized core stacks allow service launches within 6-12 months, a sharp reduction from the 18-plus-month cycles typical of legacy hardware architectures. Operators sidestep sizeable upfront network investments, reallocating capital toward marketing, analytics, and digital care tools in line with Tunisia’s “Tunisie Digital 2025” program [1]Global Affairs Canada, “Information and communications technologies (ICT) market in Tunisia,” tradecommissioner.gc.ca. Automated compliance reporting embedded in cloud platforms simplifies regulatory submissions, while elastic compute scales with subscriber acquisition, supporting the Tunisia MVNO market in reaching profitability faster.

Strong demand for low-cost international and diaspora calling plans

Remittances exceeded USD 2 billion in 2024, evidencing tight economic and social ties between Tunisian expatriates and their families. Lycamobile’s early success confirms the addressable base for competitively priced IDD bundles, and rising tourist inflows plus the uptake of eSIM travel products widen the pool of price-sensitive users seeking friction-free cross-border voice and data [2]Wise, “How to buy a prepaid SIM card for Tunisia?” wise.com . This durable demand propels the Tunisia mobile virtual network operator market toward segment-specific innovations such as bundled remittance credits or bilingual customer support, differentiating virtual operators from incumbent retail tariffs.

Mandatory mobile number portability unleashes switch-over churn

The 2016 portability mandate removed a historic loyalty barrier, enabling customers to retain numbers when changing providers. MVNOs leverage digital channels and simplified KYC flows to lure cost-conscious subscribers away from MNO prepaid packs. Uniform technical interfaces supervised by the National Telecommunications Authority lower integration effort, allowing newer entrants to focus resources on customer experience rather than back-office complexity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Wholesale rate negotiation remains dominated by three MNOs | -1.4% | Nationwide | Long term (≥ 4 years) |

| 51% Tunisian-ownership rule limits foreign capital inflows | -0.8% | National policy | Medium term (2-4 years) |

| Expensive national cybersecurity compliance for MVNO cores | -0.6% | Nationwide | Short term (≤ 2 years) |

| Low e-payment penetration inflates SIM-registration friction | -0.4% | Rural governorates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Wholesale rate negotiation remains dominated by three MNOs

Tunisie Telecom, Ooredoo, and Orange wield near-total control of essential radio-access and backhaul assets, giving them outsized influence over resale prices and traffic prioritization. Although the regulator enforces non-discrimination clauses, small-scale virtual operators lack the bargaining power seen in larger economies, constraining margin headroom and curbing aggressive retail discounting. The resulting cost structure tempers subscriber acquisition speed within the Tunisia MVNO market.

51% Tunisian-ownership rule limits foreign capital inflows

Telecommunications statutes cap non-resident equity at 49%, compelling global MVNO brands to forge local joint ventures that can elongate deal cycles and complicate governance [3]U.S. Department of State, “Tunisia: 2015 Investment Climate Statement,” state.gov. Capital-intensive full-MVNO ambitions often stall without majority control, narrowing the field to investors willing to cede operational influence. Consequently, the Tunisia MVNO industry attracts fewer big-ticket investments than peer North-African markets with liberalized ownership rules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: On-premise dominance amid cloud transition

On-premise architectures accounted for 70.41% of the Tunisia MVNO market share in 2024. A legacy preference for local data custody aligns with national cybersecurity norms, allowing MVNOs to demonstrate direct oversight of customer information. However, cloud solutions are climbing at a 22.63% CAGR, buoyed by cost flexibility and faster service iteration cycles. Tier-3 data centers built in Tunis and Sfax, together with sovereign cloud frameworks, further reduce perceived security risks. As MVNOs pivot to multi-tenant core functions, hybrid models blending on-premise signaling with cloud-hosted billing emerge as the dominant architecture by 2030.

Regulatory comfort with virtualized network functions dovetails with the government’s digitization targets, letting smaller players bypass capital-intensive switching facilities. The Tunisia mobile virtual network operator market size for cloud deployments is projected to touch USD 0.02 million by 2030, underpinned by SaaS-based BSS stacks and containerized IMS. While on-premise systems continue supporting compliance-heavy enterprise contracts, incremental migrations to public IaaS reduce total cost of ownership, enabling sharper retail pricing without eroding gross margins.

By Operational Mode: Reseller models lead full-MVNO growth

Reseller, light, and brand formats captured 72.54% of the Tunisia MVNO market size in 2024, reflecting easy entry pathways that rely on host-operator provisioning. Full MVNO agreements, though capital-heavy, are accelerating at a 23.98% CAGR through 2030 as regulatory templates mature. Operators graduating from reseller status invest in their own HLR/HSS and OSS stacks, enhancing control over SIM provisioning, quality of service, and roaming.

The Tunisia MVNO market rewards deeper technical integration with higher ARPU upsides from enterprise IoT bundles and value-added digital wallets. Yet, full MVNOs face intricate compliance audits covering lawful-intercept and data-retention rules, adding to fixed-cost overhead. Service-operator variants act as a halfway house, letting firms manage branding and CRM while outsourcing switching, a strategy resonating with fintech startups that prioritize user experience over bare-metal control.

By Subscriber Type: Consumer focus with IoT acceleration

Consumers delivered 83.56% of active lines in 2024, validating the market’s heritage of price-led voice and data propositions. Cross-SIM usage drives penetration above 128%, fomenting churn cycles that favor nimble MVNOs with digital onboarding. Enterprise segments remain comparatively modest, yet lucrative contracts surface in tourism, retail chains, and SME bundles that integrate payment rails with mobile connectivity.

IoT lines are racing ahead at a 27.25% CAGR, leveraging 5G’s massive machine-type connectivity and Tunisia’s smart-agriculture pilots in the Sahel and Cap Bon corridors. Several local device manufacturers now pre-bundle SIMs for cold-chain tracking and remote irrigation systems, signalling a meaningful uplift for the Tunisia MVNO market by 2030.

By Application: Discount services dominate M2M growth

Discount propositions held 50.37% of the Tunisia MVNO market share in 2024, anchored by diaspora IDD bundles and wallet-friendly prepaid packs. Business services supply steady margins but remain small in volume terms. Cellular M2M subscriptions, however, are forecast for a 21.31% CAGR, pushed by demand from logistics hubs around Radès Port and textile clusters near Monastir.

As device counts multiply, MVNOs with policy-based data throttling and self-service dashboards gain traction. Other niche applications, such as seasonal tourist eSIMs, make intermittent but high-margin contributions, particularly during seaside high season. The Tunisia MVNO market, therefore, pivots from blanket discounting toward segmented offers that embed advanced analytics and edge backhaul at scale.

By Network Technology: 4G dominance with 5G transformation

4G/LTE underwrote 87.07% of active MVNO traffic in 2024, benefiting from nationwide coverage and mature device ecosystems. Yet 5G is projected to grow at a 57.72% CAGR into 2030. Early adopters gravitate to enhanced mobile broadband speeds topping 500 Mbps in Tunis’s La Goulette district, and enterprises pilot URLLC use cases in Sousse’s industrial free zone.

2G/3G remains vital for legacy feature-phones in rural Jendouba and Kasserine governorates, while satellite/NTN fills coverage voids for maritime fishing fleets. Over the forecast horizon, the Tunisia MVNO market size linked to 5G is expected to outstrip 3G volumes, buoyed by affordable mid-tier handsets and declining backhaul tariffs as fiber rings extend inland.

By Distribution Channel: Digital transformation drives online growth

Online and app-only channels captured a 42.35% share in 2024 and maintain an 11.91% annual growth as eKYC modules synchronize with the national mobile ID program. Digital storefronts cut acquisition costs by roughly 30%, allowing operators to reinvest savings into promotional data top-ups. Traditional retail endures in secondary cities where cash preferences prevail; however, POS device rollouts and fintech tie-ins such as Asel Pay accelerate migration to card and wallet payments.

Carrier sub-brand kiosks inside MNO flagship stores offer physical touchpoints for warranty swaps and device financing, while third-party electronics chains provide omnichannel fulfillment. As 5G eSIM provisioning gains scale, the Tunisia MVNO market should see online activations exceed 60% of gross adds by 2029, mirroring smartphone-led digital commerce trajectories observed in peer Maghreb markets.

Geography Analysis

Urban hubs generate the bulk of Tunisia's MVNO market activity, with Tunis, Sfax, and Sousse together absorbing more than 65% of MVNO data traffic in 2024. Average downlink speeds exceed 42 Mbps in these metros, supporting high-definition video and cloud-gaming bundles. Coastal prosperity and better in-building coverage enable premium-tier data plans, while commuter belts around Ariana and Ben Arous display a rising appetite for budget post-paid offers tethered to bundled fintech wallets.

Interior governorates such as Kairouan and Siliana still confront patchy 4G reach, constraining MVNO uptake to voice-centric prepaid SKUs. Government-backed rural broadband subsidies aim to close the gap through neutral-host tower sharing, a development likely to expand the addressable base for discount-driven propositions. Cross-border transport corridors linking Algeria and Libya also hold latent potential for machine-to-machine fleet monitoring solutions once roaming wholesale rates normalize.

Internationally, Tunisia’s dense submarine cable nodes feeding Marseille and Palermo ensure latency under 60 ms to Western Europe, advantageous for diaspora voice quality and OTT content peering. Improved fiber backhaul to four land borders further strengthens redundancy, encouraging global MVNO brands exploring Maghreb expansion to regard the Tunisia MVNO market as a springboard for Francophone Africa.

Competitive Landscape

Lycamobile Tunisia exploits its worldwide IDD expertise to target the estimated 1.5 million Tunisians living abroad, bundling cross-border minutes with local data passes. Asel Mobile pursues a super-app roadmap, weaving Asel Pay transfers with zero-rating incentives that keep wallet balances on-net. Topnet Mobile leverages parent Tunisie Telecom’s wholesale terms and 570,000-plus existing ISP customers to cross-sell quad-play packages that include home fiber and IPTV.

New entrants eye opportunities in enterprise IoT, where service-level commitments and API-driven provisioning trump low-price competition. Cloud-native BSS suites, deployed via regional IaaS nodes, shorten innovation cycles, letting challengers iterate on roaming bundles or thin-slice 5G network capacity for events. Still, the Tunisia MVNO industry remains tethered to MNO goodwill on interconnect rates, maintaining a moderate concentration dynamic. In the future, liberalization of minority stakes could catalyze fresh capital and heighten rivalry, but no legislative timeline is confirmed.

Tunisia Mobile Virtual Network Operator Industry Leaders

Lycamobile Tunisia SARL

Asel Mobile SARL

Topnet Mobile SARL

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Tunisie Telecom activated North Africa’s first commercial 5G network in partnership with Ericsson, covering Tunis, Sfax, and Sousse.

- December 2024: Fintech firm Konnect secured new funding from Renew Capital to scale super-app services integrated with mobile connectivity.

- September 2024: Tunisia’s regulator issued 15-year 5G licenses to Tunisie Telecom, Ooredoo, and Orange via competitive tender.

Tunisia Mobile Virtual Network Operator Market Report Scope

| Cloud |

| On-premise |

| Reseller / Light / Brand MVNO |

| Service Operator |

| Full MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online / Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party / Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller / Light / Brand MVNO |

| Service Operator | |

| Full MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online / Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party / Wholesale |

Key Questions Answered in the Report

How large is the Tunisia MVNO market in 2025?

The market is valued at USD 0.03 million in 2025 with a 5.74% CAGR outlook to 2030.

Which technology will drive future MVNO growth in Tunisia?

5G is expected to post a 57.72% CAGR, underpinning enhanced broadband and IoT services.

What is the primary driver for new MVNO entrants?

Expanded 5G wholesale capacity and network slicing lower technical barriers and create new service niches.

How do domestic ownership rules affect foreign MVNO brands?

The 51% local equity requirement forces joint-venture structures, potentially slowing capital inflows.

Which subscriber category is growing fastest?

IoT-specific lines are advancing at a 27.25% CAGR as agriculture, logistics, and manufacturing digitize.

Are digital channels important for MVNO customer acquisition?

Yes, online and app-only sales already represent 42.35% of activations and continue to grow at 11.91% annually.

Page last updated on: