Household And Personal Care Packaging Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

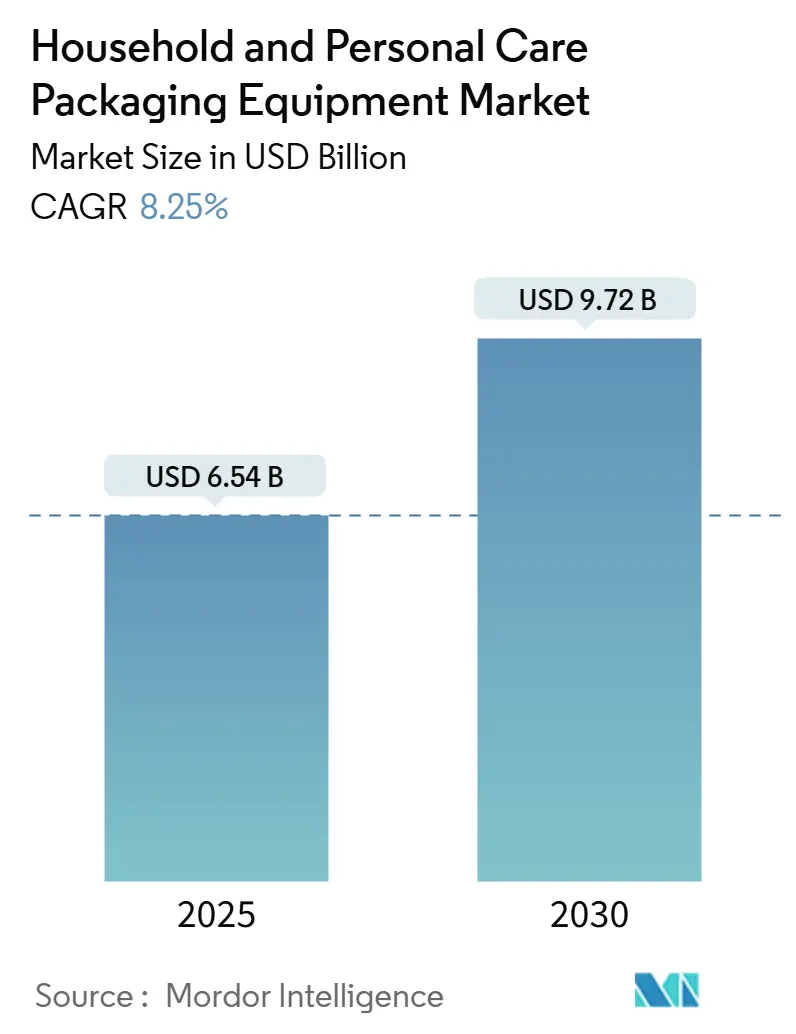

| Market Size (2025) | USD 6.54 Billion |

| Market Size (2030) | USD 9.72 Billion |

| Growth Rate (2025 - 2030) | 8.25% CAGR |

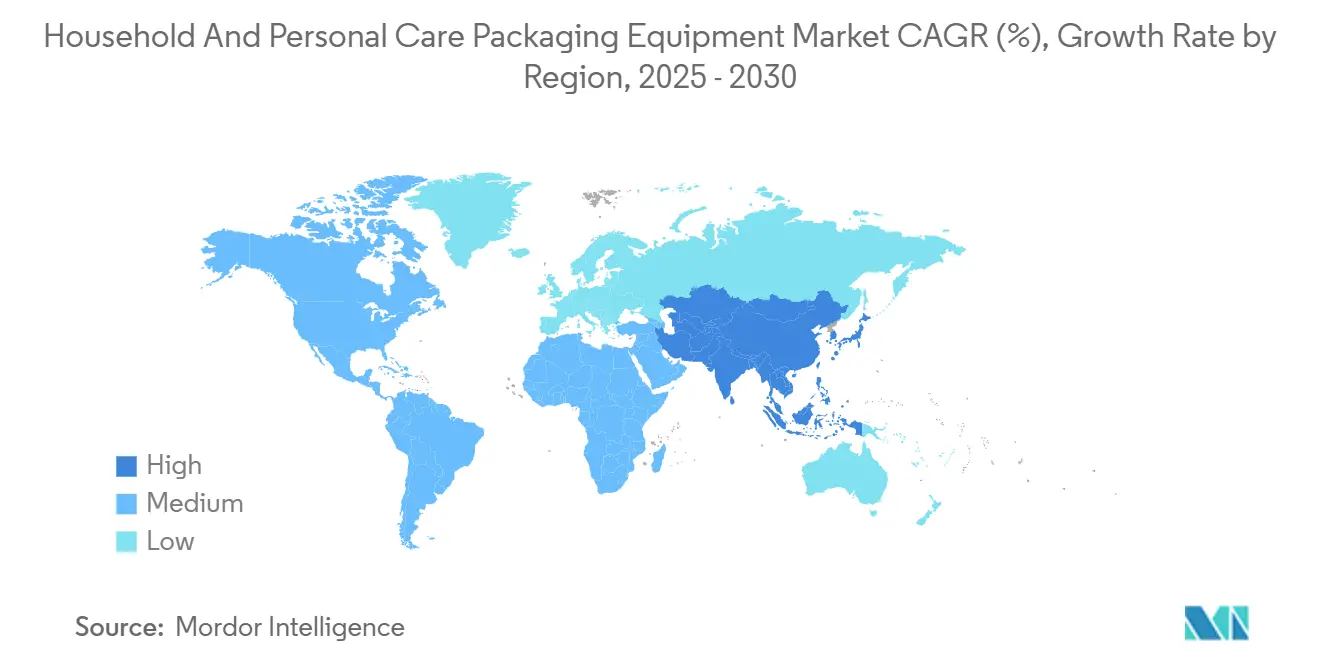

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Household And Personal Care Packaging Equipment Market Analysis by Mordor Intelligence

The Household and Personal Care Packaging Equipment market size is USD 6.54 billion in 2025 and is forecast to reach USD 9.72 billion by 2030, expanding at an 8.25% CAGR. Strong growth rests on five pillars: rapid SKU proliferation that makes agile changeovers indispensable, automation that eases labor shortages, sustainability regulations that favor post-consumer recyclate designs, e-commerce packaging that requires tamper-evident solutions, and smart-factory retrofits that cut energy use. Asia-Pacific is advancing quickest as China and India ramp up production, whereas North America commands the largest share by coupling advanced robotics with strict regulatory compliance. Competitive intensity is climbing because European specialists and cost-competitive Asian vendors are racing to build platform ecosystems that fuse machinery, software, and services. Each of these factors reinforces capital outlays, drives innovation, and accelerates technology partnerships across the market.

Key Report Takeaways

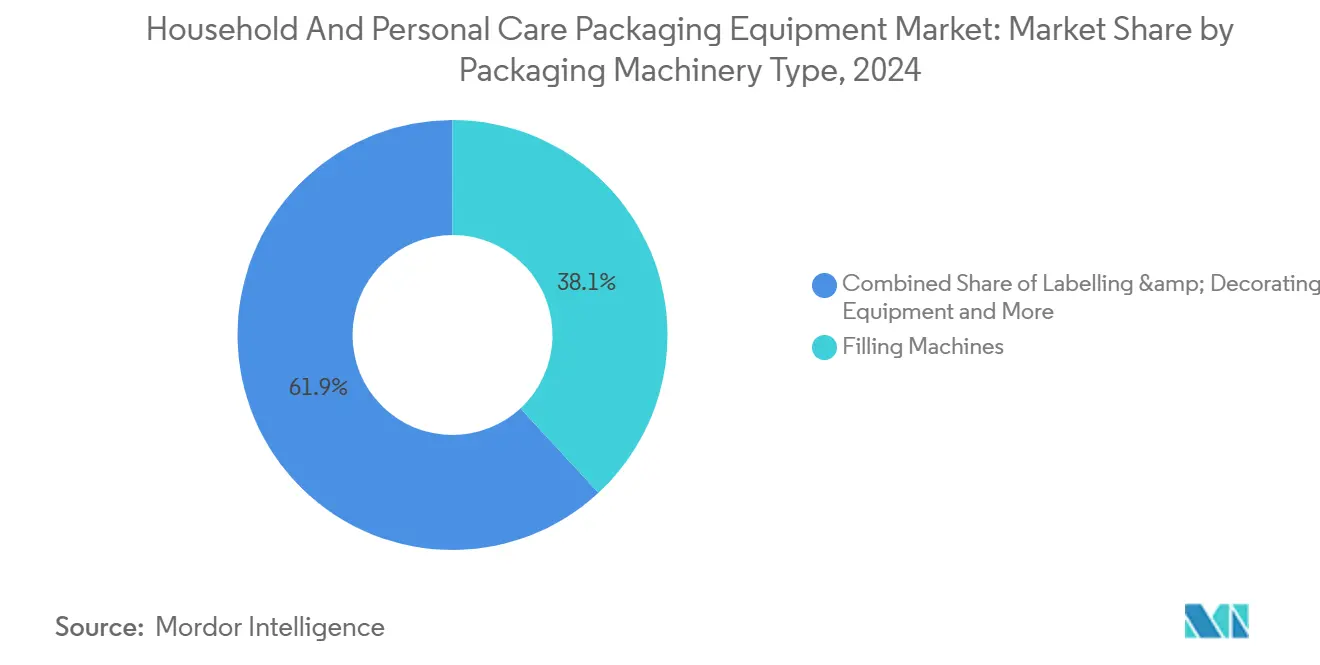

- By packaging machinery type, filling systems led with 38.12% revenue share in 2024, while labelling and decorating equipment is projected to grow at a 9.81% CAGR through 2030.

- By packaging type, bottles and jars controlled 34.52% of the Household and Personal Care Packaging Equipment market share in 2024, whereas pouches and sachets are forecast to register an 11.18% CAGR by 2030.

- By operation, primary packaging accounted for 52.13% of the Household and Personal Care Packaging Equipment market size in 2024, while tertiary systems are advancing at a 10.47% CAGR through 2030.

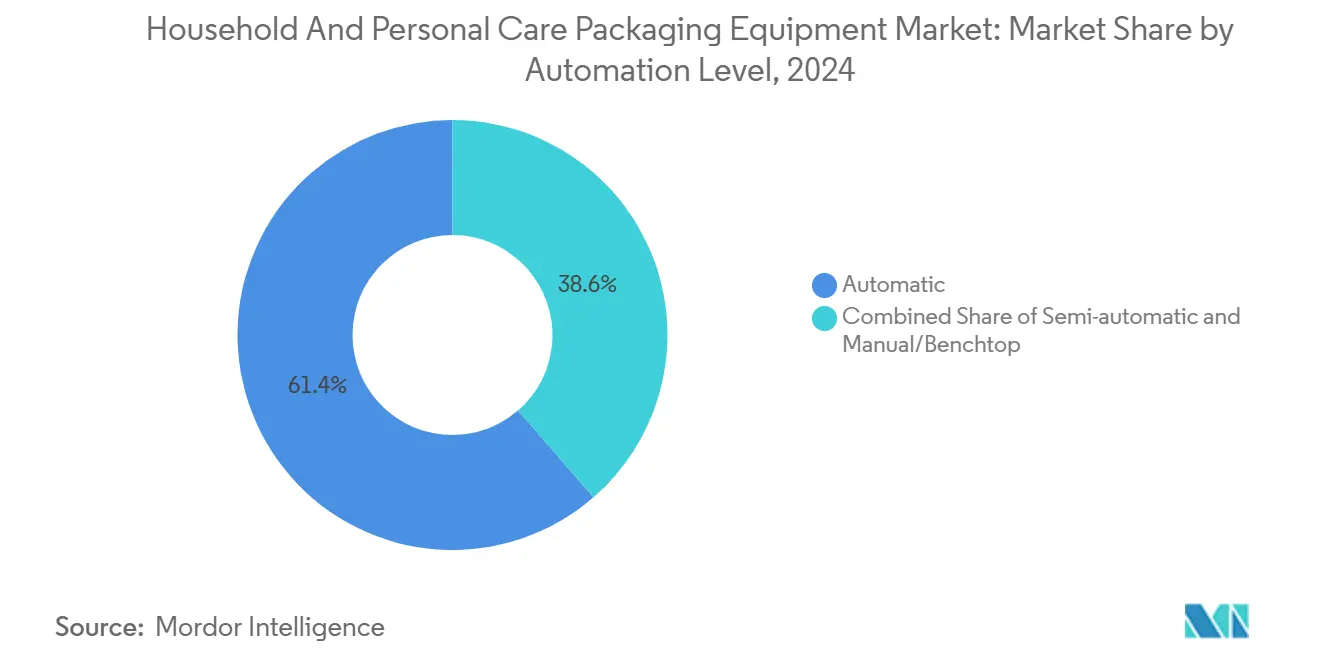

- By automation level, automatic systems captured 61.38% revenue share in 2024 and are projected to record the fastest 12.37% CAGR to 2030.

- By end-user application, skincare products dominated with 29.67% share in 2024 and fragrances and deodorants are expected to post the highest 10.08% CAGR through 2030.

Global Household And Personal Care Packaging Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated SKU Proliferation Driving Flexible Packaging Lines | 2.1% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Growing Demand for Post-consumer Recyclate-Ready Equipment | 1.8% | Europe and North America core, expanding to APAC | Long term (≥ 4 years) |

| Rising Automation to Mitigate Labor Shortages | 2.3% | North America and Europe primary, APAC emerging | Short term (≤ 2 years) |

| E-commerce-Ready Packaging Formats | 1.6% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Smart Factory Retro-fits | 0.9% | Advanced manufacturing regions globally | Long term (≥ 4 years) |

| Refillable and Re-use Models Requiring Modular Machinery | 0.7% | Europe leading, North America following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated SKU Proliferation Driving Flexible Packaging Lines

Beauty and personal care brands introduced 40% more variants in 2024 than in pre-2024 years, forcing plants to handle multiple formats without extended downtime. Orders for flexible lines at a leading supplier rose 35% during 2024 as converters prioritized agile systems. [1]Krones AG, “Sustainability Report 2024,” KRONES.COM Servo-driven modules now reset in under 15 minutes, whereas legacy mechanical drives took up to three hours. Fast changeovers enable economical micro-batches that support personalization and seasonal launches. As SKU variety continues rising, flexible machinery becomes a strategic hedge against obsolescence. Consequently, agile equipment is now a baseline requirement rather than a premium option across the market.

Growing Demand for Post-consumer Recyclate-Ready Equipment

The EU directive mandating 30% recycled content by 2030 accelerates upgrades that manage variable melt flow and contamination. A German producer invested EUR 45 million (USD 48.2 million) in 2024 to engineer PCR-compatible fillers and sealers.[2]Syntegon Technology, “Annual Report 2024,” SYNTEGON.COM New lines include in-line vision for contaminant detection, self-cleaning screw feeds, and predictive analytics that adjust torque to material viscosity. These features add 15-20% to capital cost yet assure compliance and protect brand equity. Early adopters in Europe and North America report smoother certification audits and fewer line stoppages, strengthening business cases for recyclate-ready machinery. Market penetration is widening to Asia-Pacific as exporters align with European sustainability benchmarks.

Rising Automation to Mitigate Labor Shortages

The United States recorded 380,000 unfilled manufacturing jobs in 2024, a gap that lifted robotics demand. Integrated pick-and-place cells can remove up to 60% of manual tasks, cutting injury risk and extending weekend capacity.[3]IMA Group, “Strategic Acquisitions and Market Expansion,” IMA.IT Payback periods for robotic case packers have fallen from four years to 18–24 months, inviting mid-tier firms to automate earlier than planned. Sensors now feed cloud dashboards that recommend maintenance windows, translating into 5–7% OEE gains. Workforce upskilling programs also benefit as operators transition from repetitive handling to machine-supervision roles, improving long-term retention.

E-commerce-Ready Packaging Formats

E-commerce claimed 18% of global beauty and household sales in 2024, so packages must endure parcel environments rather than retail shelves. One U.S. vendor posted 45% growth in equipment orders that embed tamper-evident seals, automated drop-test checks, and serialized QR codes.[4]ProMach Inc., “E-commerce Packaging Solutions Growth Report,” PROMACHINC.COM Secondary packers now cradle products in corrugate cut exactly to size, trimming void fill and reducing breakage. Software links scanners to logistics platforms so each parcel gains end-to-end visibility. As direct-to-consumer volumes climb, brand owners view e-commerce-capable lines as critical infrastructure, ensuring the market maintains double-digit momentum.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Capex and Long ROI Cycle | -1.4% | Global, particularly affecting emerging markets | Short term (≤ 2 years) |

| Volatility in Raw-Material Prices Affecting OEM Margins | -1.1% | Global, with acute impact in steel-dependent regions | Medium term (2-4 years) |

| Regulatory Uncertainty Around Plastic Taxes | -0.8% | Europe and North America primarily | Medium term (2-4 years) |

| High Energy Consumption Pressure | -0.6% | Europe and regions with high energy costs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Capex and Long ROI Cycle

Installing an advanced liquid-filling and palletizing line costs USD 2–5 million, and added sustainability modules lift outlays by 25% versus 2024 baselines. Financing remains tight in emerging economies, stretching ROI to six years even where demand is strong. Multilateral banks offer concessional loans, yet approvals can lag procurement schedules, causing project delays. Suppliers now propose subscription models covering machinery, software, and maintenance for monthly fees, but adoption is nascent. Unless creative financing scales, capex barriers will temper near-term expansion in price-sensitive tiers of the market.

Volatility in Raw-material Prices Affecting OEM Margins

Steel and aluminum account for almost 40% of machinery cost, and price spikes trimmed OEM margins by 3–4 percentage points after 2024. Frequent quotation revisions complicate buyer budgeting and push some projects into hold status. Servo-motor shortages lengthen lead times, forcing expanded inventories that soak up working capital. Suppliers resort to hedging and dual sourcing yet must still pass surcharges downstream, eroding cost predictability. Such volatility disincentivizes risk-averse buyers, softening order pipelines, especially for discretionary upgrades within the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Machinery Type: Filling Systems Lead Automation Drive

Filling systems generated 38.12% of 2024 revenue, underscoring their pivotal role in dose accuracy, contamination control, and regulatory compliance. Demand for servo-controlled pistons, mass-flow meters, and CIP loops remains high as formulators add suspended actives, microbeads, and viscous gels. The Household and Personal Care Packaging Equipment market size for labelling and decorating lines is scaling faster, projected at a 9.81% CAGR through 2030 due to digital inkjet modules that allow short runs and direct-to-shape printing. Inline cameras verify color registration and flag skew angles, reducing waste and ensuring shelf appeal. Palletizing robots now feature AI vision that auto-teaches new SKU patterns in minutes, giving converters full end-to-end automation.

Second-level systems such as capping machines gain from tougher tamper-evidence norms, while inspection equipment sells briskly because serial-number legislation spreads beyond pharmaceuticals. Suppliers integrate bar-code readers and laser coders so traceability begins at the filler and extends to the pallet. This holistic approach positions the Household and Personal Care Packaging Equipment market as a cornerstone of smart manufacturing strategies.

By Packaging Type: Bottles Dominate While Pouches Surge

Bottles and jars commanded 34.52% of 2024 revenue, favored for aesthetics, controlled dispensing, and premium cues in skincare and shampoos. Lightweight neck finishes and tethered caps cut resin use and improve recyclability. Conversely, pouches and sachets are on an 11.18% CAGR run because they trim material 70% compared with rigid bottles and suit e-commerce shipping. High-speed stand-up pouch fillers combine ultrasonic sealing and nitrogen flushing to guard sensitive serums. The Household and Personal Care Packaging Equipment market share for aerosol lines remains stable, buoyed by dry-shampoo and disinfectant sprays. Carton applicators ride concentrated refills that reduce shipping weight, aligning with retailer sustainability scorecards. Flexibility to switch among PET bottles, laminated pouches, and carton sleeves is now table stakes for new line tenders.

By Operation: Primary Packaging Leads Tertiary Growth

Primary steps retained 52.13% revenue share in 2024, driven by tight microbial specs and dosing precision. Smart contact-less fillers reduce shear to protect probiotic actives in toothpaste and creams. Still, tertiary systems are advancing at a 10.47% CAGR through 2030. Palletizers deploy cobots that coexist with staff in constrained footprints, while stretch-wrappers incorporate film-thickness sensors that cut consumption 12%. The Household and Personal Care Packaging Equipment market size for secondary packers expands too, as omnichannel brands ship shelf-ready trays to bricks-and-mortar and e-commerce shippers simultaneously. Unified line controllers now harmonize OEE from filler through pallet, giving managers single-screen visibility.

By Automation Level: Full Automation Accelerates

Automatic platforms captured 61.38% share in 2024 and are projected to grow 12.37% annually, reflecting the push for lights-out operations and traceable quality. Multi-axis robots stack irregular bottle shapes without change parts, while digital twins simulate 12-month wear in hours, trimming commissioning time. Semi-automatic rigs remain useful in artisan cosmetics where batch sizes are below 5,000 units, but falling robot prices shorten the justification gap. The Household and Personal Care Packaging Equipment market share for manual stations is shrinking as integrators release plug-and-play cells that drop into existing conveyors and scale gradually.

By End-User Application: Skincare Leads Fragrance Growth

Skincare retained 29.67% share in 2024 because active-rich serums demand nitrogen-blanketed fillers and UV-blocking labels. The Household and Personal Care Packaging Equipment market size for fragrances and deodorants is climbing fastest, predicted at a 10.08% CAGR through 2030 as personalized scent capsules and alcohol-free sprays emerge. Vacuum-sealed fillers cut headspace oxygen, preserving volatile note. House-cleaning line upgrades center on corrosion-resistant valves and closed-loop pH monitors, while oral-care producers adopt servo brushes that apply multi-stripe pastes without color bleed. Equipment makers thus tailor micro-features to each application niche, broadening product portfolios.

Geography Analysis

North America holds the largest slice of global revenue thanks to world-leading automation density, mature beauty brands, and strict FDA packaging guidelines. United States plants deploy line-side analytics that slash unplanned downtime by 10%, while Canada’s natural-ingredient labels invest in small-batch flex fillers. Mexico leverages near-shoring trends, fitting mid-speed lines that serve private labels for U.S. retailers. The Household and Personal Care Packaging Equipment market continues stable growth as existing facilities replace decade-old machinery with sensor-rich versions.

Europe’s competitive edge is sustainability leadership. Germany’s engineering houses deliver digital platforms that track energy kilowatt-hours per pack, aiding carbon disclosures. France’s luxury players demand flawless finish quality, pushing decorators into high-resolution inkjets, while Italy excels in small-footprint cartoners aligned with boutique fragrances. Strong regulatory clarity under the Packaging and Packaging Waste Regulation supports predictable equipment cycles.

Asia-Pacific is the growth engine. China’s investments in smart plants surge as rising wages lift the ROI for robots. India’s hygiene-product producers add pouch lines to tap urban demand, and government incentives under the Production Linked Incentive Scheme lower effective capital cost. Japan and South Korea adopt AI-driven inspection for high-margin K-beauty serums. The Household and Personal Care Packaging Equipment market thus benefits from both scale and sophistication, although local talent shortages in advanced mechatronics remain a challenge.

Competitive Landscape

The Household and Personal Care Packaging Equipment market shows moderate concentration but rising consolidation. European leaders bundle hardware, software, and lifecycle services to lock in customers, while Asian entrants compete on cost and localized support. A U.S. group invested USD 150 million in 2024 to expand e-commerce equipment lines validated with digital twins that prove throughput before shipping. Strategic acquisitions of robotics firms and software start-ups accelerate platform building, and pay-per-use contracts lower client capex. Suppliers also open regional tech centers offering simulation labs, which shorten decision cycles for brand owners and embed vendor solutions deeply.

Start-ups target niche advantages such as refill station modules and AI vision plug-ins that retrofit legacy fillers. Established players respond by forming partnerships with recycling technology firms to integrate PCR handling. As customers migrate to single-dashboard line control, suppliers without software stacks risk marginalization. The competitive story is therefore shifting from standalone machines to integrated ecosystem offerings, setting the stage for further mergers that will reshape market share rankings.

Household And Personal Care Packaging Equipment Industry Leaders

Krones AG

Syntegon Technology GmbH

Tetra Pak International S.A.

ProMach Inc.

IMA Group (Industria Macchine Automatiche S.p.A.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Sidel Group completed a EUR 80 million (USD 85.7 million) program aimed at lightweight equipment for concentrated cleaners.

- September 2024: Krones AG initiated a EUR 120 million (USD 128.6 million) R and D spend on energy-efficient lines for PCR packaging.

- August 2024: Tetra Pak International acquired TechniBlend for USD 85 million, enhancing smart-factory capability in liquid household segments.

- July 2024: Syntegon Technology unveiled a filling platform optimized for 30% PCR content in beauty packs.

Global Household And Personal Care Packaging Equipment Market Report Scope

The Household and Personal Care Packaging Equipment Market Report is Segmented by Packaging Machinery Type (Filling Machines, Capping and Sealing Machines, Labelling and Decorating Equipment, Wrapping and Bundling Equipment, Palletizing and Depalletizing Systems, Others), Packaging Type (Bottles and Jars, Tubes, Pouches and Sachets, Aerosol Cans, Cartons and Boxes, Others), Operation (Primary Packaging, Secondary Packaging, Tertiary Packaging), Automation Level (Automatic, Semi-automatic, Manual/Benchtop), End-User Application (Skin Care Products, Hair Care Products, Oral Care Products, Household Cleaning Products, Fragrances and Deodorants, Others), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Filling Machines |

| Capping and Sealing Machines |

| Labelling and Decorating Equipment |

| Wrapping and Bundling Equipment |

| Palletizing and Depalletizing Systems |

| Other Packaging Machinery Types (Inspection, Coding) |

| Bottles and Jars |

| Tubes |

| Pouches and Sachets |

| Aerosol Cans |

| Cartons and Boxes |

| Other Packaging Types (Blisters, Stick Packs) |

| Primary Packaging |

| Secondary Packaging |

| Tertiary Packaging |

| Automatic |

| Semi-automatic |

| Manual/Benchtop |

| Skin Care Products |

| Hair Care Products |

| Oral Care Products |

| Household Cleaning Products |

| Fragrances and Deodorants |

| Other End-User Applications |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Packaging Machinery Type | Filling Machines | ||

| Capping and Sealing Machines | |||

| Labelling and Decorating Equipment | |||

| Wrapping and Bundling Equipment | |||

| Palletizing and Depalletizing Systems | |||

| Other Packaging Machinery Types (Inspection, Coding) | |||

| By Packaging Type | Bottles and Jars | ||

| Tubes | |||

| Pouches and Sachets | |||

| Aerosol Cans | |||

| Cartons and Boxes | |||

| Other Packaging Types (Blisters, Stick Packs) | |||

| By Operation | Primary Packaging | ||

| Secondary Packaging | |||

| Tertiary Packaging | |||

| By Automation Level | Automatic | ||

| Semi-automatic | |||

| Manual/Benchtop | |||

| By End-User Application | Skin Care Products | ||

| Hair Care Products | |||

| Oral Care Products | |||

| Household Cleaning Products | |||

| Fragrances and Deodorants | |||

| Other End-User Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What factors are accelerating investment in automated packaging lines for household and personal care goods?

Rising SKU complexity, labor shortages, and sustainability mandates shorten payback periods, making fully automatic equipment essential for flexible, efficient operations.

Which packaging format is growing fastest in beauty and cleaning products?

Pouches and sachets are projected to grow at an 11.18% CAGR through 2030, helped by lightweight materials and e-commerce suitability.

Why does Asia-Pacific post the highest growth in equipment sales?

Capacity expansions in China and India, government incentives for smart factories, and rising consumer demand for personal care products lift regional adoption.

How are machinery vendors supporting recycled-content initiatives?

Suppliers offer PCR-ready fillers and sealers with advanced contaminant detection and self-cleaning features to maintain package integrity at 30% recycled content thresholds.

What is the usual capital outlay for a complete automated packaging line?

A turnkey high-speed system costs between USD 2 million and USD 5 million, with enhanced sustainability and robotics features accounting for recent 25% cost increases.

Which end-use segment is forecast to grow fastest up to 2030?

Fragrances and deodorants are expected to expand at a 10.08% CAGR, propelled by personalized scents and aerosol innovations that require specialized filling systems.

Page last updated on: