End-Of-Line Packaging Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

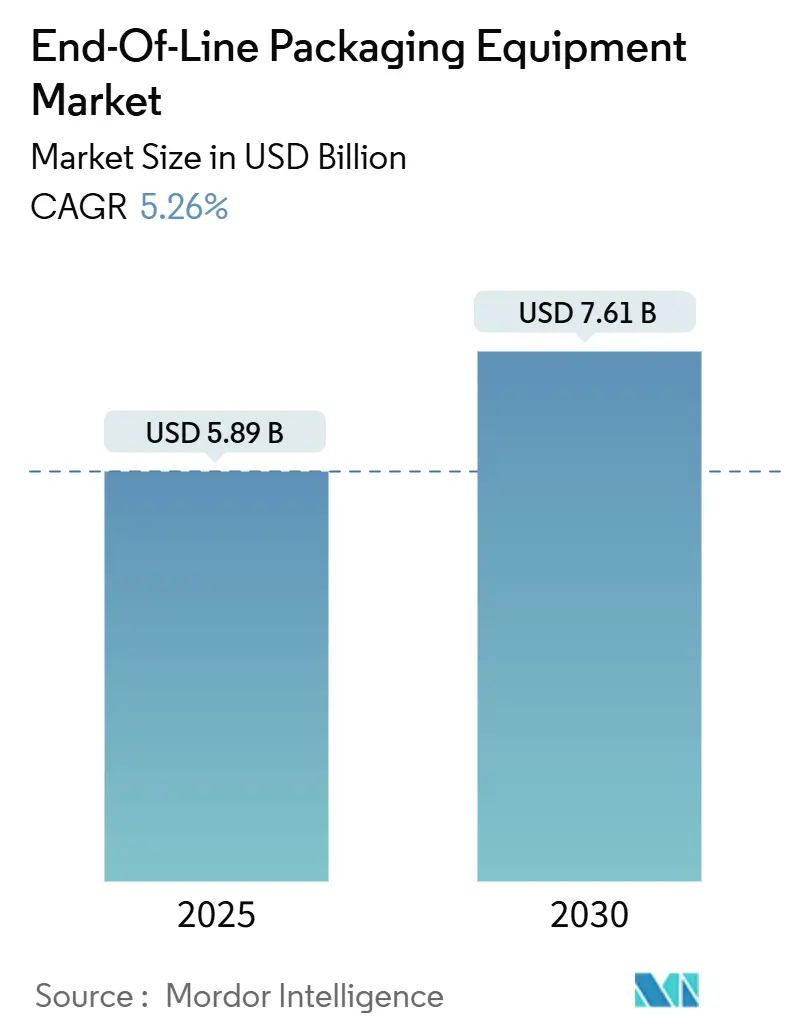

| Market Size (2025) | USD 5.89 Billion |

| Market Size (2030) | USD 7.61 Billion |

| Growth Rate (2025 - 2030) | 5.26% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

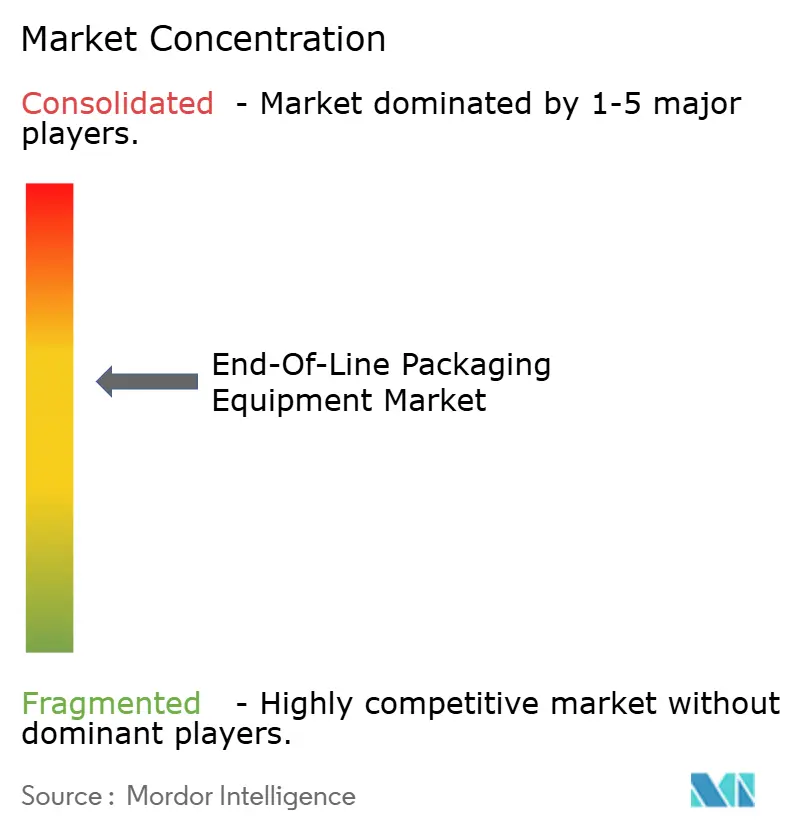

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

End-Of-Line Packaging Equipment Market Analysis by Mordor Intelligence

The end-of-line packaging equipment market size stands at USD 5.89 billion in 2025 and is forecast to reach USD 7.61 billion by 2030, reflecting a 5.26% CAGR over the period. The market’s momentum rests on rising e-commerce parcel volumes, persistent labor shortages that force greater automation, and regulatory pressure to make packaging recyclable-ready. Digital twin platforms, predictive maintenance analytics, and modular designs have become mainstream as producers seek to balance capital spending with flexibility. E-commerce fulfillment hubs are reshaping case-packing and palletizing specifications, sustainability rules are pushing lightweight materials that stress legacy machinery, and shortages of skilled technicians are elevating equipment reliability as a decisive purchasing criterion. Incumbent vendors are therefore bundling hardware with remote diagnostics, while small and medium-size enterprises (SMEs) gravitate toward semi-automatic cells that can later scale to fully automatic operation.

Key Report Takeaways

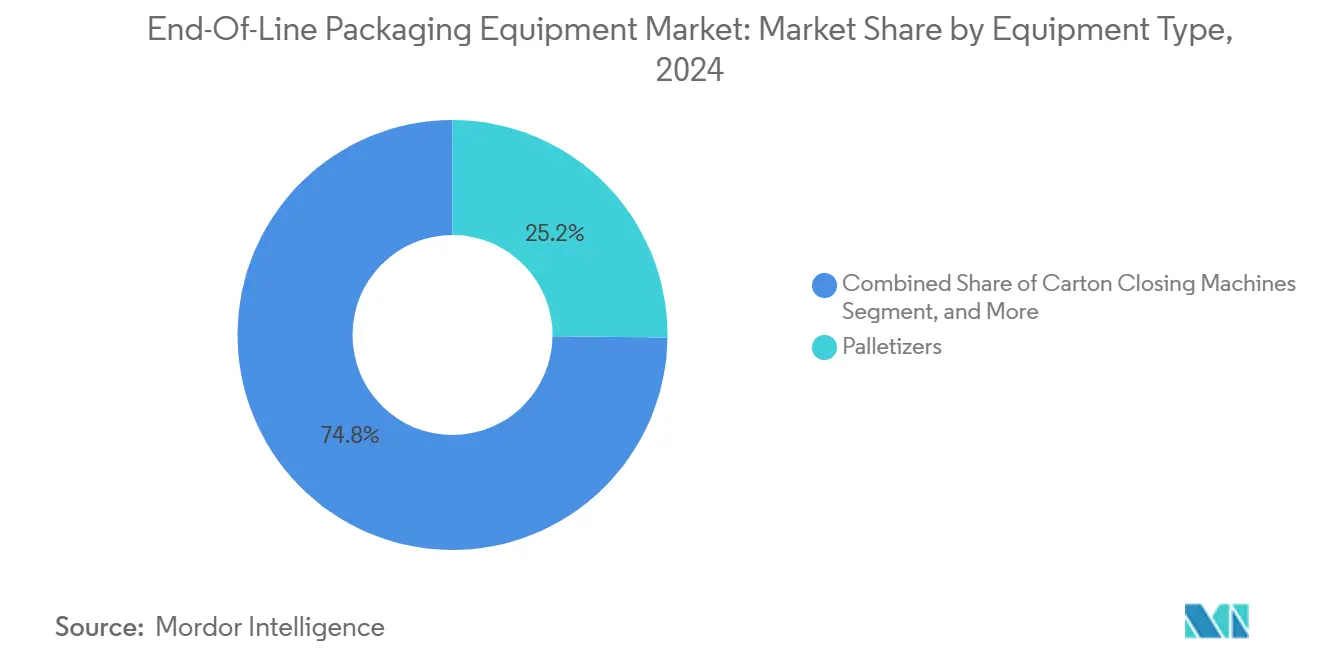

- By equipment type, palletizers captured 25.19% of the end-of-line packaging equipment market share in 2024.

- By function, the end-of-line packaging equipment market size for wrapping and sealing is projected to grow at a 5.89% CAGR between 2025-2030.

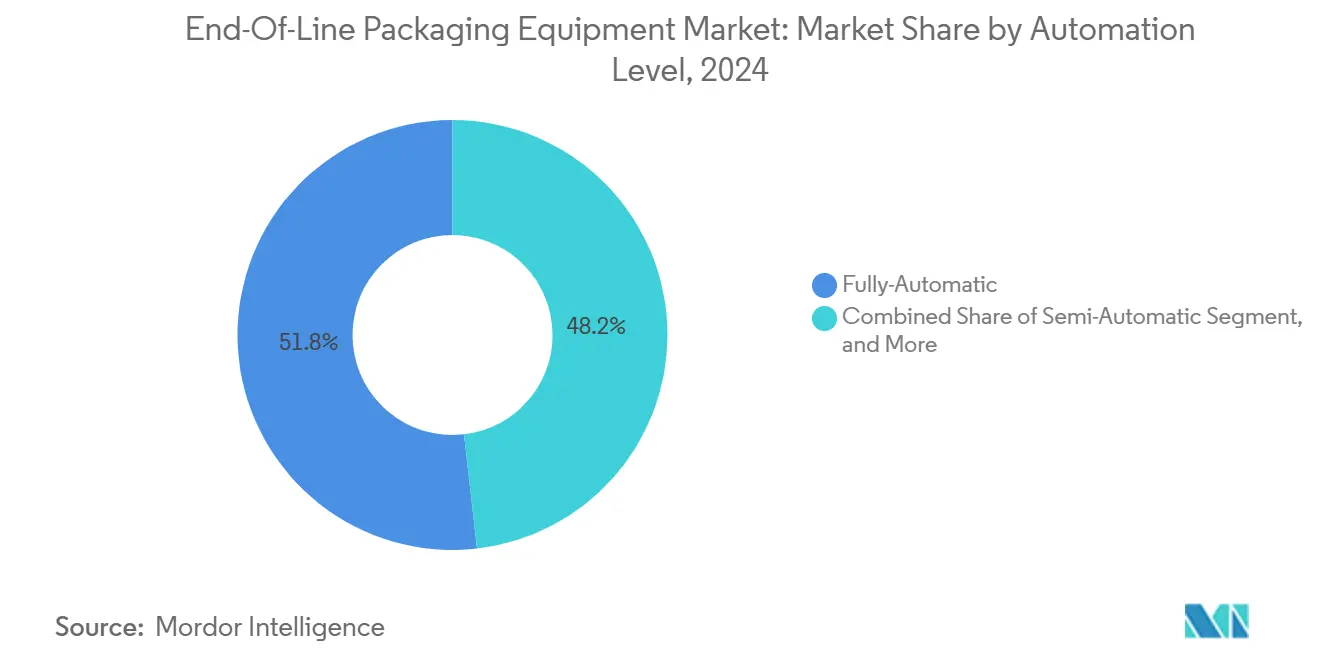

- By automation level, fully automatic systems captured 51.82% of the end-of-line packaging equipment market share in 2024.

- By end-user, the end-of-line packaging equipment market size for e-commerce fulfillment is projected to grow at a 6.19% CAGR between 2025-2030.

- By geography, North America captured 27.61% of the end-of-line packaging equipment market share in 2024.

Global End-Of-Line Packaging Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising e-commerce parcel volumes | +1.8% | Global with emphasis on North America and Europe | Medium term (2-4 years) |

| Digital twin-enabled line optimisation | +1.2% | North America and Europe, expanding into Asia-Pacific | Long term (≥ 4 years) |

| Labor shortage accelerating automation adoption | +1.5% | Global, strongest in developed markets | Short term (≤ 2 years) |

| Sustainability mandates driving recyclable-ready packaging | +0.9% | Europe and North America, spreading globally | Medium term (2-4 years) |

| Surge in SKUs requiring flexible equipment | +0.7% | Global consumer goods hubs | Medium term (2-4 years) |

| Government incentives for smart factories | +0.6% | Asia-Pacific, Europe, select North American regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising E-Commerce Parcel Volumes

Explosive parcel throughput is prompting fulfillment centers to replace manual case-packing islands with high-speed, SKU-agnostic equipment. Amazon opened 15 new North American hubs in 2024, each specified with advanced palletizing robots that handle mixed case profiles while maintaining throughput above 1,200 units per hour.[1]Amazon.com Inc., “Form 10-K 2024,” sec.gov Equipment capable of dynamic changeovers is essential because a single facility can now process thousands of distinct product dimensions daily. Stretch wrapper demand benefits as individual-shipment stability outweighs bulk pallet integrity, nudging buyers toward film-optimization software that reduces material usage without compromising containment. Vendors that pre-integrate barcode inspection, weigh-checks, and label verification are winning orders because fulfillment operators prefer turnkey packages that minimize commissioning time. The impact will extend into 2026 as omnichannel retail accelerates unit picks over traditional case shipments, further enlarging the addressable end-of-line packaging equipment market.

Digital Twin-Enabled Line Optimisation

Digital twins model entire packaging lines in real-time, allowing for the simulation of wear trajectories and micro-adjustments of servo profiles before faults propagate. Schneider Electric noted a 23% decline in unplanned downtime at customer sites after embedding twin-driven analytics in 2024. Data from edge devices migrates to cloud dashboards, where algorithms flag vibration anomalies and recommend bearing swaps during scheduled lulls rather than emergency stoppages. As European Union funds subsidize Industry 4.0 investments, adoption spreads beyond blue-chip multinationals to mid-tier converters that previously relied on reactive maintenance. Over the long term, twin technology will redefine service contracts, with vendors transitioning from transactional spare parts sales to performance-based uptime guarantees, thereby cementing recurring revenue streams while boosting the end-of-line packaging equipment market.

Labor Shortage Accelerating Automation Adoption

The U.S. manufacturing sector ended 2024 with 380,000 unfilled positions, turning labor scarcity into a strategic risk rather than an episodic inconvenience. Food and beverage producers that once depended on seasonal labor now fast-track end-of-line robotic cells that pick, inspect, and seal with minimal human oversight. Procurement teams report that equipment reliability and intuitive human-machine interfaces are more important than purchase price, as unplanned downtime directly erodes throughput margins. Compact collaborative robots are gaining traction where space limitations rule out conventional six-axis arms. In the short term, SMEs opt for semi-automatic stretch wrappers and cartoners to reduce labor needs without incurring the full capital outlay of hyperscale solutions, thereby expanding the mid-priced segment of the end-of-line packaging equipment market.

Sustainability Mandates Driving Recyclable-Ready Packaging

The European Union’s Packaging and Packaging Waste Regulation 2025/40 obliges brand owners to meet stringent recyclability targets, thereby forcing equipment retrofits to handle thinner films, mono-material cartons, and bio-based adhesives. Line engineers must recalibrate heat-seal bars and tension controls to avoid tearing lighter substrates, while vision systems now inspect for correct eco-label placement. Vendors that offer quick-change forming sets and lower-energy heater banks report surging order volumes as converters race to certify compliance. The ripple effect is expected to be felt in North America by 2027 as multinational firms standardize packaging specifications globally, driving sustainability-ready machines deeper into the end-of-line packaging equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX for SME converters | -0.8% | Global, strongest in emerging markets | Short term (≤ 2 years) |

| Limited interoperability across OEM control systems | -0.6% | Global, pronounced in fragmented production clusters | Medium term (2-4 years) |

| Supply chain volatility in servo motors and PLCs | -0.5% | Global, acute in Asia-Pacific | Short term (≤ 2 years) |

| Energy-intensity concerns amid green targets | -0.4% | Europe and North America, spreading worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX for SME Converters

Fully automatic palletizing islands priced between USD 200,000 and USD 500,000 stretch the working-capital limits of regional converters, many of whom still rely on bank overdrafts or leasing lines denominated in volatile local currencies.[2]European Investment Bank, “SME Access to Finance Survey 2024,” eib.org Leasing programs that bundle service, software, and spares are easing adoption, yet monthly payments remain daunting when order visibility is short. Modular cells that allow buyers to begin with a single robotic arm and add vision or wrap stations incrementally are mitigating the pinch, but widespread diffusion awaits lower component costs and expanded trade-credit facilities. Consequently, CAPEX aversion tempers the otherwise robust trajectory of the end-of-line packaging equipment market in cash-constrained geographies.

Limited Interoperability Across OEM Control Systems

Proprietary communication stacks often prevent seamless data exchange between palletizers, stretch wrappers, and case packers sourced from different brands, inflating integration budgets and elongating commissioning timelines.[3]International Society of Automation, “Industrial Control Systems Interoperability Technical Report 2024,” isa.org Custom middleware patches can account for up to 10% of the total project spend and introduce cybersecurity vulnerabilities. While open protocols, such as OPC UA for PackML, are gaining momentum, brownfield factories equipped with legacy PLCs and serial-link devices struggle to retrofit. Until common semantic models are enforced across the supplier base, plant engineers will either lock in single-vendor ecosystems or accept suboptimal runtime analytics, restraining the full digital potential of the end-of-line packaging equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Palletizers Anchor Automation Expansion

The palletizer segment represented 25.19% of 2024 revenue, underpinning the operational backbone of distribution-ready order fulfillment. As of 2025, the end-of-line packaging equipment market size for palletizers alone is approaching USD 1.48 billion, benefiting from continuous-motion designs that stack 100 cases per minute without causing product damage. Stretch wrappers recorded the sharpest momentum, charting a 6.18% CAGR to 2030 because omnichannel retailers demand secure single-parcel loads immune to conveyor shocks. The resulting investments elevate wrap automation beyond bulk pallets and into zone-based fulfillment cells that process diverse SKUs within a two-minute cycle time.

OEMs differentiate on gripper versatility, adopting vacuum-on-tool changeovers that cut idle seconds, while load-stability software calibrates film tension using dynamic weight feedback. Shrink bundlers maintain relevance in beverage multipacks, though their sub-5% share underscores a shift toward corrugated wraparound cases that simplify recycling. Case packers remain staples for legacy supermarket channels; however, machines that self-adjust to random-size cartons open new addressable niches. Cumulatively, product-agnostic operation, smaller footprints, and predictive spares positioning strengthen the link between agile logistics and the broader end-of-line packaging equipment market.

By Function: Palletizing Demand Remains Foundational

Palletizing functions captured 32.28% of global turnover during 2024 as manufacturers prioritize throughput stability amid volatile order volumes. The end-of-line packaging equipment market share coursed by palletizing systems reinforces their role as the final buffer before warehouse management systems take custody. Wrapping and sealing capabilities headline growth charts at 5.89% CAGR thanks to retail shifts toward direct-to-consumer shipping, which values corner protection and puncture resistance over cube optimization.

Integrated vision inspection modules within wrapping frames verify barcode readability and film overlap tolerances without halting line flow. Labeling and coding advance steadily because pharmaceutical serialization mandates escalate complexity, triggering demand for synchronized inkjet, laser, and RFID stations. Inspection stations widen their presence as food safety regulators tighten allergen-control audits, using hyperspectral cameras to spot contaminants at speeds topping 200 units per minute. Collectively, higher functional convergence shrinks physical footprints, allowing both greenfield and retrofit facilities to future-proof packaging assignments while enlarging the scope of the end-of-line packaging equipment market.

By Automation Level: Semi-Automatic Cells Bridge Budget Gaps

Fully automatic lines contributed 51.82% of 2024 revenue, a reflection of multinational producers that benchmark overall equipment effectiveness above 85%. The end-of-line packaging equipment market size tied to fully automatic configurations is projected to reach USD 4.2 billion by 2030; however, growth moderates as SMEs shift toward scalable semi-automatic alternatives. At a 5.66% CAGR, hybrid cells combine manual feed stations with robotic offloads, delivering 70% of the labor saving at 50% of the capital outlay.

Collaborative robots enable line Takt rates of 8-10 picks per minute while occupying less than 2 m², making them suitable for brownfield plants that lack sufficient floorspace for high-speed robotic gantries. Equipment vendors embed touchscreen wizards that guide changeovers in under 3 minutes, aligning with labor realities where training windows are compressed. Manual lines persist in low-volume artisanal production and certain emerging regions where wage differentials remain steep; yet, their proportional decline is built into the forecast as semiautomatic add-ons scale easily into fully automatic forms. Therefore, tiered automation options remain essential for capturing white-space opportunities within the end-of-line packaging equipment market.

By End-User Industry: E-Commerce Redefines Specification Hierarchies

Food and beverage enterprises accounted for 34.55% of end-user revenue in 2024; however, their absolute growth is plateauing as the installed bases mature. Conversely, the end-of-line packaging equipment market size attributable to e-commerce fulfillment is growing at a 6.19% CAGR, outpacing every legacy sector as operators redesign lines to accommodate random-length boxes, variable-weight parcels, and real-time carrier labeling. A typical e-commerce cell demands high-speed print-and-apply labelers that interface directly with warehouse management systems, a departure from batch-coded factory packaging.

Consumer packaged goods manufacturers focus spending on flexible palletizers to manage multi-SKU pallet patterns required by retailer-specific planograms, while pharmaceutical companies invest in inspection-heavy lines that comply with serialization audits. Industrial packaging, though niche, necessitates heavy-payload robots capable of handling 50 kg cases, with reinforced frames supporting long dwell heat-sealers for thick polyethylene liners. Across segments, data connectivity to enterprise resource planning (ERP) software has become non-negotiable, ensuring traceability and facilitating circular-economy reporting demanded by regulators and brand owners. Consequently, specification divergence enriches the technology mix feeding the end-of-line packaging equipment market.

Geography Analysis

North America retained 27.61% share in 2024, anchored by mature e-commerce ecosystems and manufacturers racing to mitigate labor gaps. The regional end-of-line packaging equipment market size is forecast at USD 2.22 billion by 2030, with U.S. factories integrating digital twin dashboards ahead of Europe. Canada’s food processing sector continues brownfield upgrades, while Mexican maquiladoras adopt semi-automatic palletizers to balance wage pressures.

Asia-Pacific posts the quickest 6.14% CAGR as China’s 14th Five-Year Plan subsidizes smart-factory grids and India’s production-linked incentive schemes stimulate packaging automation outlays. Japan and South Korea refine small-batch robotic cartoners for cosmetics exports, and Southeast Asian nations such as Vietnam capture contract-assembly footprints that mandate cost-efficient end-of-line cells. These dynamics collectively raise the region’s share within the end-of-line packaging equipment market.

Europe balances moderate growth with high specification complexity, stemming from strict green-packaging rules that favor machines capable of handling ultra-thin substrates. Germany’s equipment OEM cluster accelerates modular servo architectures, the United Kingdom simplifies validation procedures to comply with post-Brexit customs checks, and Italy’s beverage corridor upgrades shrink bundlers to handle tethered caps. As Eastern Europe draws automotive battery plants, demand for heavy-duty palletizers rises, sustaining continental relevance in the global end-of-line packaging equipment market.

Competitive Landscape

Market concentration remains moderate, with the top five suppliers controlling an estimated 42% of 2024 revenue. ABB aligns its robotics portfolio with proprietary vision stacks, Krones couples beverage fillers to palletizers via unified SCADA layers, and ProMach cross-sells multiplex brands through turnkey lifecycle contracts. These players leverage global service footprints and digital twin platforms to lock in multi-year equipment-as-a-service subscriptions.

Niche innovators penetrate white spaces by offering low-cost cobots packaged with no-code programming, appealing to SMEs that prefer rent-to-own arrangements. Sustainability compliance becomes a competitive lever, as vendors who certify bio-plastic compatibility command premium pricing. Software-defined motion control further blurs boundaries between hardware vendors and industrial-IoT integrators, intensifying partner ecosystems while raising switching costs for end users. Supply-chain localization, particularly in Asia-Pacific, also influences vendor decisions on where to situate final assembly plants, shaping the competitive geometry of the end-of-line packaging equipment market.

End-Of-Line Packaging Equipment Industry Leaders

ABB Ltd.

Krones AG

ProMach Inc.

Sidel Group

Schneider Electric SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: ABB announced a USD 150 million expansion of robotic packaging production in North America and Europe, adding flexible palletizing and case-handling capacity.

- August 2024: Krones completed the EUR 180 million (USD 195 million) acquisition of Ocme Srl, bolstering capabilities in pharmaceutical serialization and tamper-evident packaging.

- July 2024: ProMach launched a digital twin-enabled optimisation platform that reduces unplanned downtime by up to 30%.

- June 2024: Schneider Electric invested USD 200 million in a Singapore smart-manufacturing hub focused on packaging automation controls.

Global End-Of-Line Packaging Equipment Market Report Scope

| Palletizers |

| Case Packers |

| Carton Closing Machines |

| Stretch Wrappers |

| Shrink Bundlers |

| Other Equipment Types |

| Case Handling |

| Palletizing |

| Wrapping and Sealing |

| Labeling and Coding |

| Inspection |

| Manual |

| Semi-automatic |

| Fully-automatic |

| Food and Beverage |

| Consumer Packaged Goods |

| Pharmaceuticals |

| Industrial |

| E-commerce Fulfilment |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Equipment Type | Palletizers | ||

| Case Packers | |||

| Carton Closing Machines | |||

| Stretch Wrappers | |||

| Shrink Bundlers | |||

| Other Equipment Types | |||

| By Function | Case Handling | ||

| Palletizing | |||

| Wrapping and Sealing | |||

| Labeling and Coding | |||

| Inspection | |||

| By Automation Level | Manual | ||

| Semi-automatic | |||

| Fully-automatic | |||

| By End User Industry | Food and Beverage | ||

| Consumer Packaged Goods | |||

| Pharmaceuticals | |||

| Industrial | |||

| E-commerce Fulfilment | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the end-of-line packaging equipment market?

The market stands at USD 5.89 billion in 2025.

How fast is the market expected to grow?

It is projected to expand at a 5.26% CAGR from 2025 to 2030.

Which equipment type leads sector revenue?

Palletizers hold the largest share at 25.19% of 2024 revenue.

Which region will see the fastest growth?

Asia-Pacific shows the highest 6.14% CAGR through 2030.

Why are semi-automatic systems gaining popularity?

They deliver most automation benefits while requiring lower initial investment, appealing to SMEs facing tight capital budgets.

How are sustainability mandates influencing equipment design?

Regulations demand machines that run thinner, mono-material substrates and integrate recyclability features, reshaping R&D priorities.

Page last updated on: