Secondary Packaging Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

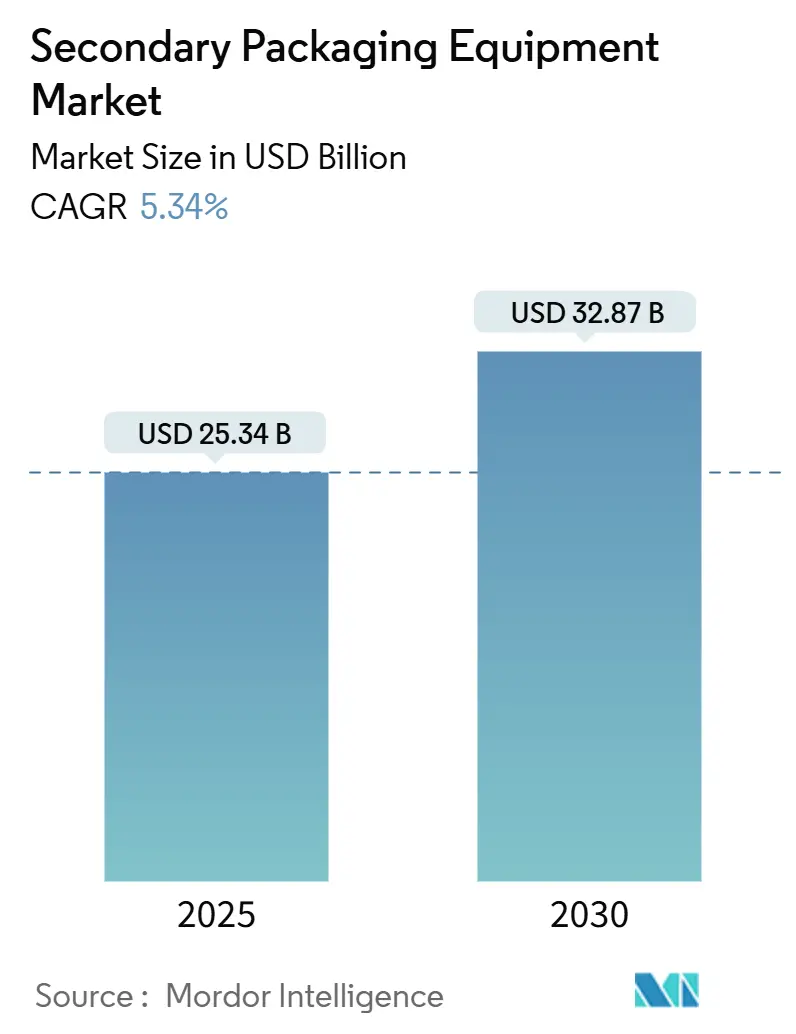

| Market Size (2025) | USD 25.34 Billion |

| Market Size (2030) | USD 32.87 Billion |

| Growth Rate (2025 - 2030) | 5.34% CAGR |

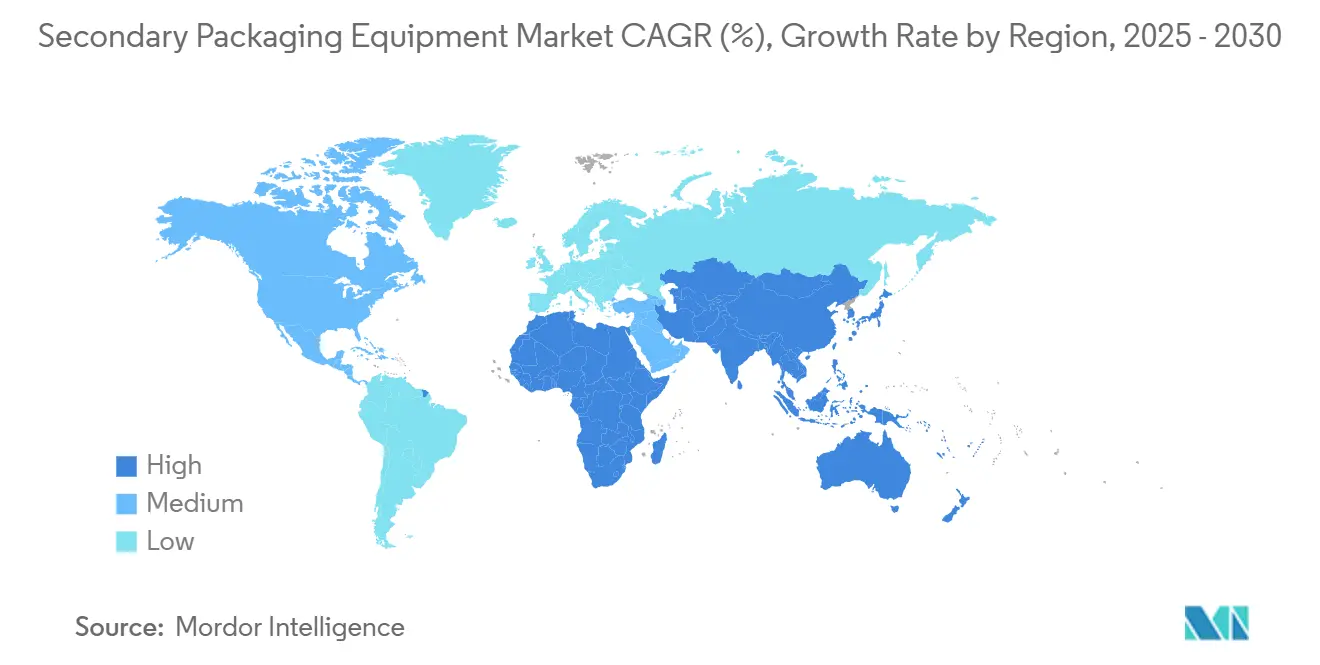

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Secondary Packaging Equipment Market Analysis by Mordor Intelligence

The secondary packaging equipment market size reached USD 25.34 billion in 2025 and is projected to increase to USD 32.87 billion by 2030, growing at a 5.34% CAGR. The growth reflects rising demand for automated, sustainable, and e-commerce-ready solutions that improve line efficiency while lowering total packaging material use. Global brand owners are accelerating capital expenditures on modular case packers, cartoners, palletizers, and wrapping systems to keep pace with the proliferation of SKUs, labor shortages, and stricter recycling mandates. Investment momentum is strongest across food and beverage, pharmaceutical, and personal care plants, where rapid changeovers and integrated inspection sensors deliver measurable throughput and quality gains.

Key Report Takeaways

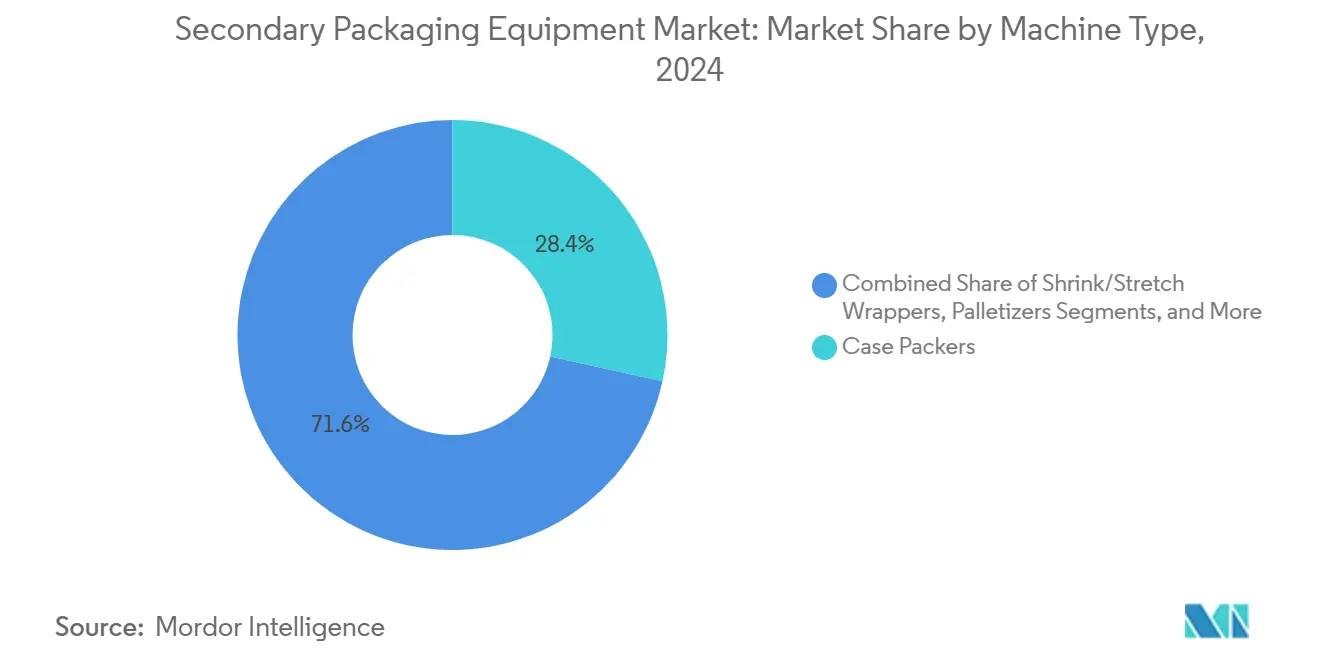

- By machine type, the case packers segment captured 28.45% of the secondary packaging equipment market share in 2024.

- By automation level, the secondary packaging equipment market size for automated systems is projected to grow at a 7.48% CAGR between 2025–2030.

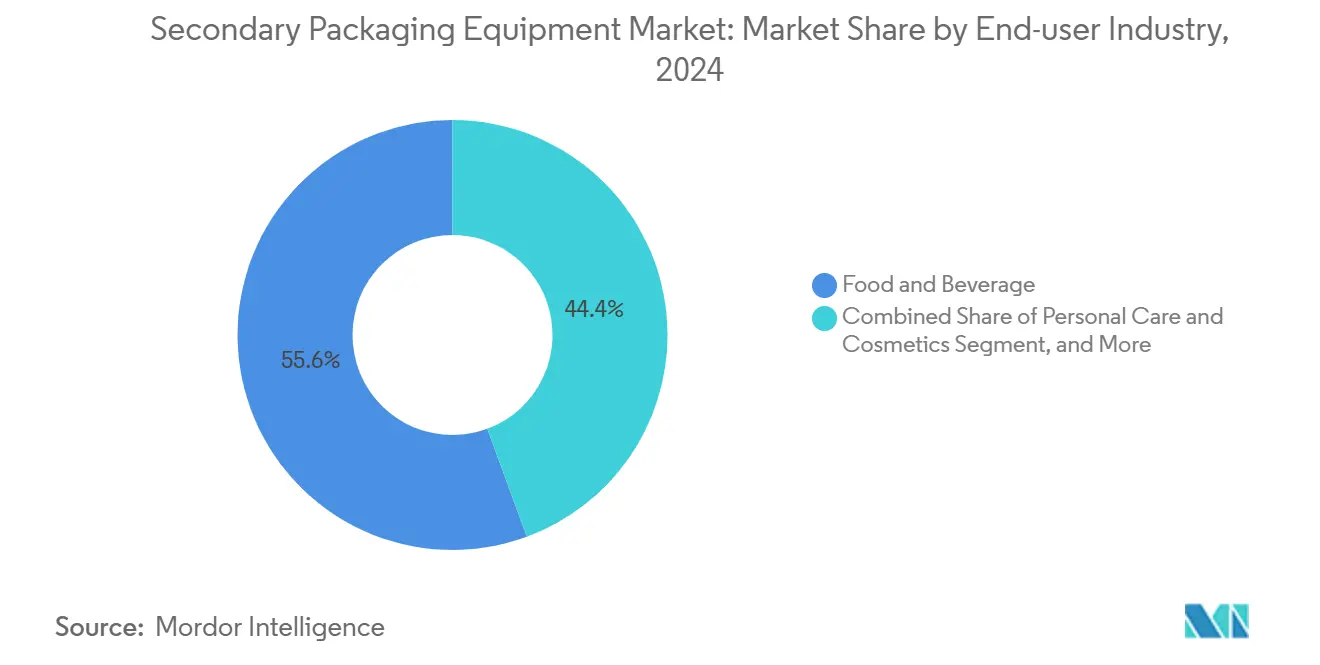

- By end-user industry, the food and beverage segment captured 55.63% of the secondary packaging equipment market share in 2024.

- By geography, the Asia-Pacific region captured the leading position in 2024 and is forecast to grow at an 8.83% CAGR between 2025–2030.

Global Secondary Packaging Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in demand for single-serve, on-the-go formats | +0.8% | Global highest in North America and Asia-Pacific | Medium term (2–4 years) |

| Shift of CPG brands to monomaterial flexible packs for recyclability | +0.9% | Europe and North America, expanding to the Asia-Pacific | Long term (≥ 4 years) |

| Expansion of e-commerce grocery fulfillment networks | +1.2% | Global highest in North America and Europe | Short term (≤ 2 years) |

| Food safety-driven adoption of high-barrier pouch machinery in emerging markets | +0.7% | Asia-Pacific, South America, the Middle East, and Africa | Medium term (2–4 years) |

| Integration of smart inspection sensors lowers downtime by <2% | +0.6% | Global early adoption in developed markets | Short term (≤ 2 years) |

| OEM financing programs for mid-tier converters in Latin America | +0.4% | South America spillover to other emerging markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Surge in Demand for Single-Serve, On-the-Go Formats

Single-serve SKUs accounted for more than 35% of new food and beverage launches in 2024, prompting manufacturers to adopt secondary packaging equipment that can handle smaller case counts at higher speeds. Amazon earmarked EUR 700 million (USD 791 million) for fulfillment technology optimized for single-portion products, underscoring the scale of infrastructure upgrades underway. Modular case packers equipped with servo-driven changeover kits now switch between package dimensions in minutes, rather than hours, while computer-vision systems ensure precise placement, limiting damage to over 250 packs per minute.

Shift of CPG Brands to Monomaterial Flexible Packs for Recyclability

Global brands have pledged to use all-recyclable packaging by 2030, fueling demand for secondary packaging lines that are compatible with monomaterial films. Coveris introduced MonoFlex barrier film in 2024, which operates on existing wrapping equipment without requiring retrofits.[1]Coveris Launches MonoFlex Recyclable Barrier Film,” Packaging World, packworld.com Equipment suppliers are integrating lower-temperature sealing jaws and film tension controls that preserve line uptime while cutting energy use by 12-15%. EU legislation requiring 65% recyclable packaging is pushing converters to switch from multilayer structures to PE or PP monomaterial webs, extending the replacement cycle well beyond 2030.

Expansion of E-commerce Grocery Fulfillment Networks

E-grocery penetration jumped to 12.3% in 2024, prompting retailers and 3PLs to redesign secondary packaging lines around mixed-SKU, batch-of-one workflows. FedEx rolled out AI-directed robotics in 15 distribution centers, tripling pick rates and compressing order-to-ship windows to under two hours. Case erectors now build custom-sized corrugated formats on demand, while automatic sealers integrate with label printers and track-and-trace software for last-mile visibility.

Food Safety-Driven Adoption of High-Barrier Pouch Machinery in Emerging Markets

Regulators across Brazil, India and Southeast Asia tightened microbial limits on ready-to-eat foods, elevating demand for high-barrier pouch equipment that delivers commercial sterility without refrigeration. Brazil’s ANVISA 2024 rules require enhanced oxygen barriers, spurring processors to invest in multi-lane stand-up pouch formers with nitrogen flushing modules GOV.BR. Equipment manufacturers bundle operator training and remote diagnostics to address labor shortages while increasing first-time-right rates to above 98%.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-intensive nature limits SME adoption | -0.7% | Global highest in emerging markets | Long term (≥ 4 years) |

| Skilled operator shortage raising OPEX ≥15% | -0.9% | North America and Europe, spreading worldwide | Medium term (2–4 years) |

| Volatility in multilayer film prices disrupting ROI models | -0.5% | Global variable by region | Short term (≤ 2 years) |

| Stricter EU machinery safety directives adding compliance costs | -0.4% | Europe spillover to export markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Capital-Intensive Nature Limits SME Adoption

Automated secondary packaging lines cost USD 500,000-2.5 million, a barrier for small converters that generate limited free cash. Total ownership escalates 25-30% when installation, training, and long-term service contracts are factored in. Brazil’s BNDES Finame facility offers loans up to R$150 million (USD 30 million) at subsidized rates, but similar programs are scarce elsewhere. Many SMEs defer upgrades, stretching payback periods to six years and slowing penetration of the secondary packaging equipment market.

Skilled Operator Shortage Raising OPEX ≥15%

Operator vacancies remain open for 4-6 months, and wages for certified technicians increase by 15-20% annually. Siemens reported that automation projects are slipping by a quarter due to labor gaps, which are inflating commissioning costs and delaying revenue realization. OEMs respond with intuitive HMIs, remote monitoring, and augmented-reality repair guides that cut on-site support visits by 40%, yet talent shortages continue to cap throughput in mature economies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Case Packers Lead Through Versatility

Case packers captured the largest slice of 2024 revenue at 28.45%, confirming their cross-industry adaptability. This dominance is supported by quick-change gripper heads that shift between glass jars, pouches, and cans with minimal downtime, making them a cornerstone of the secondary packaging equipment market. In contrast, shrink and stretch wrappers are posting the highest 7.73% CAGR as e-commerce merchants streamline material usage via ultra-thin films that still secure loads against scuffing during parcel sortation. The secondary packaging equipment market size tied to wrapping machines is projected to expand at a faster rate than any other sub-category through 2030, with demand concentrated in fulfillment hubs across North America and Europe.

Integrated systems are blurring the traditional boundaries of machines. Pacteon’s robotic case erector-palletizer fusion trims floor-space requirements by 30% while upping OEE, a sign that customers prefer single-vendor solutions to ease maintenance complexity.[2]Pacteon Collaborative Case Erector-Palletizer at PACK EXPO 2024,” Packaging World, packworld.com Cartoners remain essential in the pharmaceutical industry because serialization modules authenticate every carton, thereby reducing the risk of counterfeits. Palletizers, although capital-intensive, utilize AI-driven algorithms that refine stack patterns in real-time, reducing stretch film usage by 8-10% and enhancing downstream stability.

By Automation Level: Automatic Systems Drive Efficiency

Automatic lines held a 43.69% share in 2024 and posted a 7.48% CAGR to 2030, illustrating how labor scarcity is pushing companies toward lights-out production. These platforms integrate vision-guided robotics and predictive maintenance dashboards, which help push unplanned downtime below 2%. The secondary packaging equipment market share for semi-automatic units remains stable in niche applications, particularly in runs where tactile assessment safeguards fragile packs, such as cosmetics gift sets.

Manual lines persist mainly among low-volume artisanal processors, yet even here, entry-level cobots priced under USD 35,000 are eroding the cost advantage of hand-packing. FLtècnics’ AutoSplicer Pro, for instance, swaps film rolls without stopping the line, lifting OEE by up to 12% while lowering operator fatigue. Automation upgrades also simplify future compliance with ISO 13849 safety audits, which now favor predictable robotic motions over variable human tasks.

By End-user Industry: Food and Beverage Dominance with Personal Care Acceleration

The food and beverage sector accounted for 55.63% of 2024 revenue, reflecting continuous SKU refreshes and enhanced hygiene standards. Equipment suppliers tailor IP65-rated stainless frames and tool-less changeovers to cut allergen cross-contact risks. In parallel, the personal care and cosmetics segment’s 7.62% CAGR is driven by consumers upgrading to premium skin treatments. China’s skincare spend is on track to rise from 420 billion CNY (USD 59.2 billion) in 2024 to 530 billion CNY (USD 74.6 billion) by 2029, pulling in localized packaging capacity.

Pharmaceutical producers adopt track-and-trace compliant cartoners and case labelers that serialize each secondary pack, ensuring traceability across the supply chain. Industrial and consumer goods lines are incorporating rugged robotics capable of handling heavier loads, while sustainability commitments are nudging all verticals toward recycled corrugated board and thinner overwraps.

Geography Analysis

The Asia-Pacific region captured 34.68% of global revenue in 2024 and is forecasted to grow at an 8.83% CAGR through 2030, maintaining its leading position in the secondary packaging equipment market. China leads with grants that subsidize high-speed case packers for food exporters, whereas India’s Production Linked Incentive scheme offsets 10% of capital outlays for pharmaceutical packaging plants.[3]China’s Skincare Market Growth Drives Packaging Innovation,” Reuters, reuters.com The region’s midsize converters gravitate toward modular systems that scale with demand, cushioning initial cash outflows.

North America ranks second by value, driven by e-commerce order complexity and chronic labor shortages that justify the rapid adoption of fully automatic palletizers. Here, the secondary packaging equipment market size for AI-enhanced robotics is expected to double by 2029 as DC operators chase same-day shipping promises. The United States also pilots advanced sensor suites that feed real-time OEE dashboards, enabling remote line optimization across multi-site networks. Europe emphasizes circularity, with the EU’s 2030 recyclability mandate propelling conversions to monomaterial wrapping films. Consequently, the secondary packaging equipment market share belonging to retrofitted wrappers is climbing ahead of new-build machines, reflecting a preference for refurbishments that limit carbon footprints.

Compliance with updated machinery safety directives adds 8-12% to acquisition budgets, yet also grants CE-marked systems a premium in export destinations. Brazil’s Finame loans remove part of the barrier, accounting for over one-third of secondary packaging line purchases in 2024. The Middle East and Africa continue to import turnkey lines to secure food and pharmaceutical supply chains, but OEMs are increasingly basing service engineers in Gulf hubs to reduce downtime for regional customers.

Competitive Landscape

The secondary packaging equipment market is moderately consolidated, with the ten largest vendors controlling approximately 45-50% of the 2024 revenue. Krones AG strengthened end-to-end PET capabilities by acquiring Netstal for CHF 220 million (USD 248 million), integrating injection molding with downstream case packing. Syntegon Technology merged with Telstar, combining freeze-dryer expertise with sterile filling and secondary cartoning capabilities optimized for high-potency drugs. Coesia expanded its North American footprint through a USD 85 million acquisition that includes e-commerce-ready case packers.

Competitive advantage hinges on changeover agility, energy efficiency, and digital service layers that predict component wear. Leading OEMs embed IIoT gateways delivering cloud analytics under subscription contracts, turning one-time equipment sales into annuity streams. Niche players carve out territory in all-paper overwrap or license eco-film patents to differentiate themselves. Collaboration with robot specialists expands every supplier’s addressable market, as buyers increasingly prefer integrated cells over piecemeal retrofits.

Rising compliance costs create a barrier for entrants lacking certification expertise, while growing demand in emerging markets rewards vendors that bundle financing and operator training. Top suppliers are forecast to sustain R&D outlays near 6-7% of revenue through 2027, funding AI-driven path planning and lightweight gripper materials that further shrink the carbon footprint of secondary packaging lines.

Secondary Packaging Equipment Industry Leaders

-

Syntegon Technology GmbH

-

Coesia S.p.A.

-

IMA Group

-

Barry-Wehmiller Companies Inc.

-

Pro Mach, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Krones AG completed the Netstal acquisition for CHF 220 million (USD 248 million), adding PET preform injection molding to its integrated portfolio.

- September 2024: Amazon committed EUR 700 million (USD 791 million) to European fulfillment center automation, prioritizing mixed-SKU secondary packaging lines.

- August 2024: FedEx partnered with Nimble Robotics to deploy automated systems across 15 distribution centers, achieving 3× faster order processing.

- June 2024: Coesia S.p.A. bought a North American equipment maker for USD 85 million to enhance e-commerce-oriented case packing solutions.

Global Secondary Packaging Equipment Market Report Scope

| Case Packers |

| Cartoners |

| Case Erectors and Sealers |

| Shrink / Stretch Wrappers |

| Palletizers |

| Food and Beverage |

| Pharmaceuticals and Healthcare |

| Personal Care and Cosmetics |

| Consumer Goods |

| E-commerce |

| Other End-user Industries |

| Automatic |

| Semi-Automatic |

| Manual |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Machine Type | Case Packers | ||

| Cartoners | |||

| Case Erectors and Sealers | |||

| Shrink / Stretch Wrappers | |||

| Palletizers | |||

| By End-Use Industry | Food and Beverage | ||

| Pharmaceuticals and Healthcare | |||

| Personal Care and Cosmetics | |||

| Consumer Goods | |||

| E-commerce | |||

| Other End-user Industries | |||

| By Automation Level | Automatic | ||

| Semi-Automatic | |||

| Manual | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What was the global value of the secondary packaging equipment market in 2025?

It reached USD 25.34 billion in 2025.

How fast is demand for automatic secondary packaging equipment growing?

Automatic systems are expanding at a 7.48% CAGR between 2025 and 2030.

Which region is the largest buyer of secondary packaging machinery?

Asia-Pacific leads with a 34.68% share of 2024 revenue and the fastest 8.83% CAGR outlook.

Why are shrink and stretch wrappers the fastest-growing type of machine?

E-commerce requires lighter, secure loads, driving wrapper demand at a 7.73% CAGR through 2030.

What factors limit adoption among small packaging converters?

High capital costs and lengthy payback periods constrain SMEs despite financing programs.

Which industry segment is accelerating the most after 2024?

Personal care and cosmetics are projected to grow at a 7.62% CAGR through 2030, driven by premium skincare demand.

Page last updated on: