Pharmaceutical Packaging Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

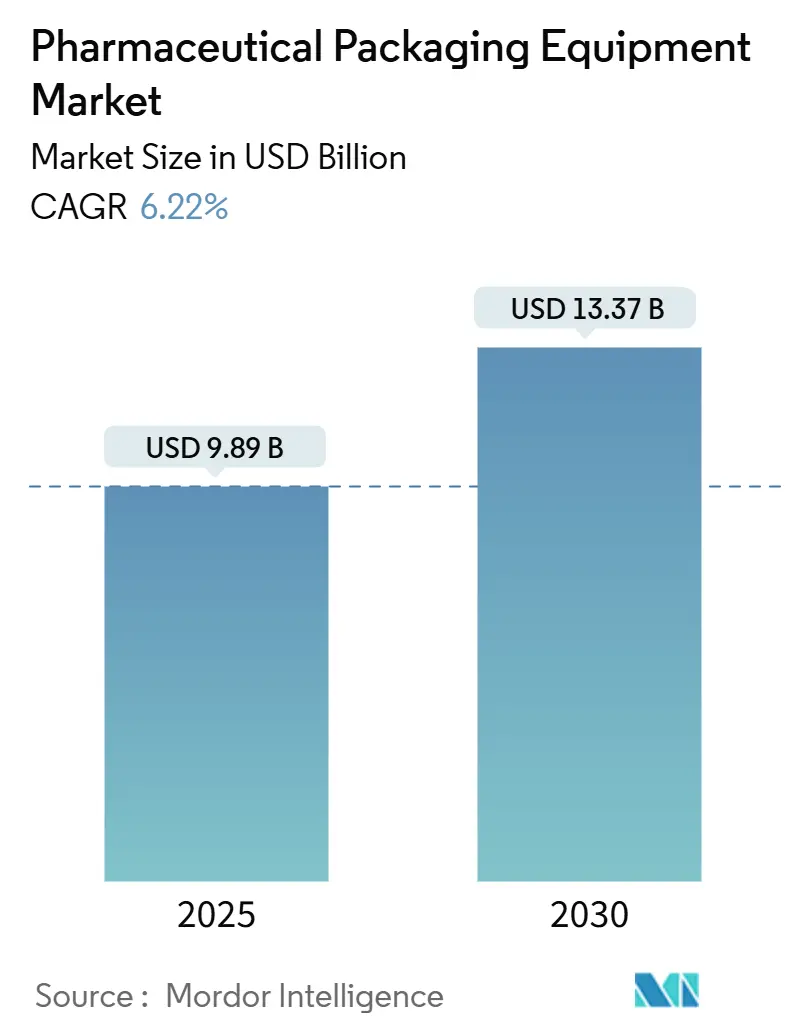

| Market Size (2025) | USD 9.89 Billion |

| Market Size (2030) | USD 13.37 Billion |

| Growth Rate (2025 - 2030) | 6.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmaceutical Packaging Equipment Market Analysis by Mordor Intelligence

The pharmaceutical packaging equipment market reached USD 9.89 billion in 2025 and is forecast to expand at a 6.22% CAGR, reaching USD 13.37 billion by 2030. Strong demand originates from mandatory unit-level serialization rules taking effect in the United States and Europe, rapid vaccine fill-finish capacity expansions, and the industry’s shift toward recyclable mono-material formats, which necessitate equipment retrofits. Asia-Pacific maintains clear volume leadership, yet North America and Europe dictate global compliance standards that shape technology roadmaps. Investments in artificial-intelligence-enabled predictive maintenance, modular micro-factories for personalized medicines, and robotics for end-of-line automation sharpen the competitive edge of equipment suppliers.[1]Heidi Vanheerswynghels, “Keeping Pace With Pharma Packaging,” Pharma Manufacturing, pharmamanufacturing.com

Key Report Takeaways

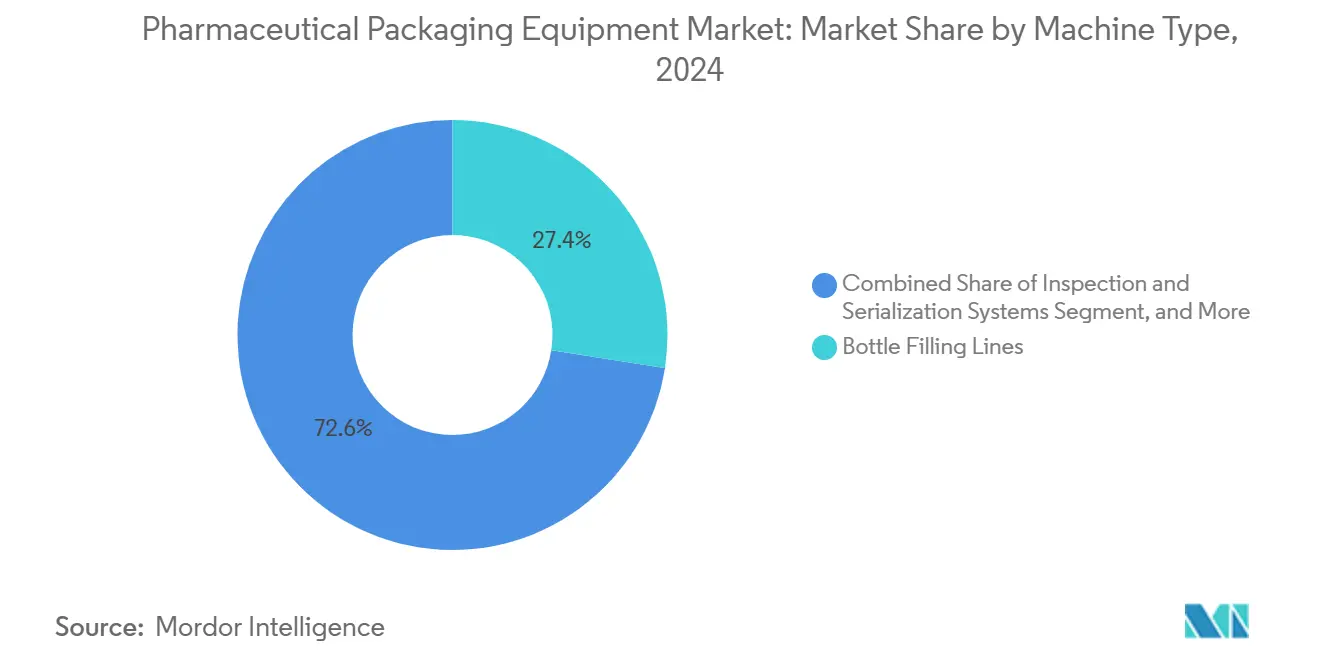

- By machine type, the pharmaceutical packaging equipment market size for inspection and serialization systems is projected to grow at a 7.88% CAGR between 2025-2030.

- By packaging tier, primary equipment captured 40.81% of the pharmaceutical packaging equipment market share in 2024.

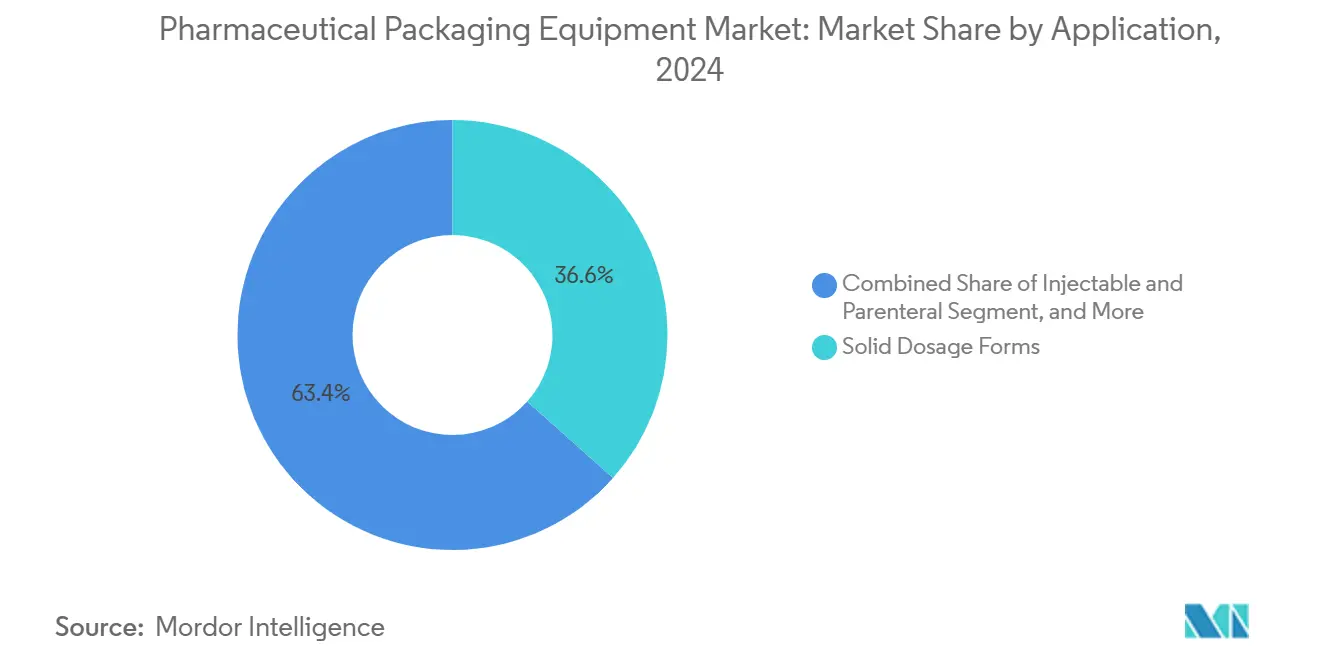

- By application, the pharmaceutical packaging equipment market size for injectable formats is projected to grow at an 8.29% CAGR between 2025-2030, outpacing the solid and liquid dosage segments.

- By end user, pharmaceutical manufacturers captured 51.25% of the pharmaceutical packaging equipment market share in 2024.

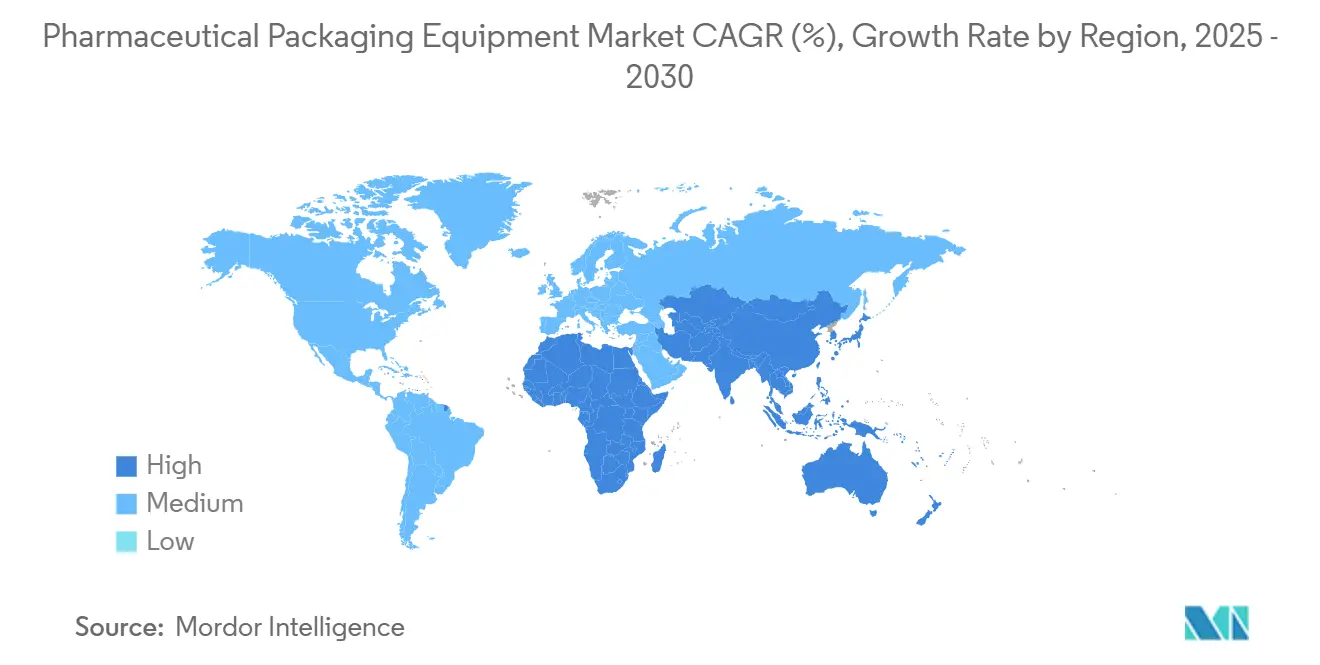

- By geography, the pharmaceutical packaging equipment market size for Asia-Pacific is projected to grow at a 7.19% CAGR between 2025-2030, marking the fastest regional growth.

Global Pharmaceutical Packaging Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing generic drug production volumes | +1.8% | Global - strongest in Asia-Pacific and North America | Medium term (2-4 years) |

| Stringent serialization regulations in the United States and Europe | +2.1% | North America and Europe, spreading worldwide | Short term (≤ 2 years) |

| Accelerated vaccine fill-finish capacity build-outs post-COVID-19 | +1.2% | Global - focus on North America and Europe | Medium term (2-4 years) |

| Shift toward sustainable packaging materials requiring retrofits | +0.9% | Europe and North America, growing in Asia-Pacific | Long term (≥ 4 years) |

| AI-driven predictive maintenance lowering total cost of ownership | +0.7% | Global - led by developed markets | Long term (≥ 4 years) |

| Modular “plug-and-play” micro-factories for personalized medicines | +0.5% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Generic Drug Production Volumes

Expansion programs by multinational and domestic manufacturers are reshaping throughput requirements at high-volume plants. Investments such as Piramal Pharma’s USD 80 million upgrade in Michigan and PCI Pharma Services’ USD 365 million global capacity boost underscore the procurement of faster bottle filling lines, high-speed cartoners, and flexible blister equipment. Equipment like Marchesini’s MA 360 cartoner, rated at 400 cartons per minute, illustrates the emphasis on cost-per-unit efficiency over SKU flexibility. As generic portfolios expand, rapid changeover capability becomes essential, driving demand for vision-guided robotics and recipe-driven control systems within the pharmaceutical packaging equipment market.

Stringent Serialization Regulations in the United States and Europe

Mandatory serialization under the U.S. Drug Supply Chain Security Act, fully enforced from November 2024, and the European Falsified Medicines Directive compel both greenfield and retrofit spending on vision-based coding, tamper-evident labeling, and data aggregation software. Over 6,000 pharmaceutical crime incidents were recorded in 2022, amplifying the global urgency. Antares Vision Group’s blow-fill-seal inspection platform tests 100 containers per minute while embedding 2D code verification.[2]Press Release, “At Achema, Antares Vision Group to Debut Automatic Inspection Machine for Blow-Fill-Seal Containers,” packagingconnections.com These compliance mandates accelerate the adoption of integrated line solutions, ensuring that inspection and serialization systems remain the fastest-growing slice of the pharmaceutical packaging equipment market.

Accelerated Vaccine Fill-Finish Capacity Build-Outs Post-COVID-19

Governments and manufacturers continue to build biologics infrastructure even after the pandemic supply shocks have receded. Canada’s National Research Council has laid out plans for new mRNA plants, while Novo Nordisk is investing USD 4.1 billion in North Carolina to expand its injectable output. Syntegon’s MLD Advanced fills 400 pre-sterilized syringes per minute, illustrating the premium on sterility assurance, containment isolators, and 100% in-line inspection technology. Correspondingly, aseptic blow-fill-seal, barrier isolators, and nested-format fixtures command higher margins within the pharmaceutical packaging equipment market.

Shift Toward Sustainable Packaging Materials Requiring Retrofits

European Union regulations on packaging waste push drugmakers toward mono-material films and weight-reduced glass. SCHOTT’s lightweight nest reduces glass weight by 30%, necessitating recalibrated pick-and-place and conveyance settings; similar adjustments are required when replacing PVC/PVDC blister films with recyclable alternatives. Pharmaworks validates heat-seal parameters for these materials, highlighting retrofit opportunities where servo temperature control and PID tuning enable sustainability without compromising seal integrity. These shifts fuel after-market revenue streams for suppliers able to update installed bases across the pharmaceutical packaging equipment industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure for state-of-the-art aseptic lines | -1.4% | Global - acute in emerging markets | Medium term (2-4 years) |

| Supply chain disruptions for precision components | -0.8% | Global - sharpest in Asia-Pacific | Short term (≤ 2 years) |

| Skilled labor shortages in equipment installation and validation | -0.6% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Cyber-security vulnerabilities in connected machinery | -0.4% | Global - stronger in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure for State-of-the-Art Aseptic Lines

Isolator-grade fill-finish lines can cost USD 10-50 million each, with isolator enclosures alone adding USD 2-5 million per project.[3]Featured Companies, “Marchesini Group at Achema 2024: Celebrating 50 Years of Innovation,” manufacturingchemist.com Payback periods often exceed five years, placing significant stress on mid-tier manufacturers’ balance sheets. Although modular skids and operating-lease models cushion upfront spending, limited availability restricts uptake and slows equipment turnover inside the pharmaceutical packaging equipment market.

Supply Chain Disruptions for Precision Components

Ongoing semiconductor and optics shortages prolong lead times for serialization and vision systems from 12-18 months to as long as 30 months. Bottlenecks in servo drives, depth-sensing cameras, and programmable logic controllers challenge smaller suppliers lacking purchasing leverage, constraining timely delivery of advanced units across the pharmaceutical packaging equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Inspection Systems Drive Technology Evolution

Inspection and serialization solutions are expected to introduce the fastest 7.88% CAGR to 2030, as compliance penalties outweigh capital outlays. At the same time, bottle filling lines maintained a 27.45% share of the pharmaceutical packaging equipment market in 2024, underpinned by high volumes of generic liquid dosage production. Modern plastic bottle lines now produce up to 600 bottles per minute, utilizing servo cappers and magnetic flowmeters to achieve ±0.5% accuracy. Blister equipment remains vital for solid doses, whereas cartoners and pouch fillers meet secondary and niche presentations, respectively. The interplay of high-speed container handling and synchronous data capture defines purchasing criteria, ensuring steady replacement cycles that lift the pharmaceutical packaging equipment market size for key machine groups.

Emergent digital features further differentiate machine classes. Optical character recognition on the fly, auto-splice film reels, and remote troubleshooting portals reduce downtime and elevate overall equipment effectiveness. Suppliers bundling these technologies into turnkey cells gain an advantage, as drug makers consolidate vendors to simplify validation.

By Packaging Type: Tertiary Automation Accelerates

Primary systems maintained a 40.81% market share because they directly interact with the drug product, thereby incurring the highest regulatory burden. Yet tertiary solutions grow at the fastest rate, with a 8.61% trajectory, as robotic case packers and palletizers shrink labor footprints. Case erectors, which lift throughput to 25 cases per minute, replace manual operations, improve ergonomic safety, and integrate seamlessly with warehouse management software. Connectivity through OPC UA or MQTT protocols enables real-time quality and asset tracking. This surge elevates the pharmaceutical packaging equipment market size for tertiary units beyond historical maintenance-level spending while reinforcing integration opportunities for single-source suppliers.

Secondary units, such as track-and-trace-ready labelers, bridge the gap between primary and tertiary systems. Tight synchronization with upstream blister or bottle lines, as well as downstream palletizing, is mandatory to meet DSCSA aggregation requirements. Suppliers who can supply integrated layers retain add-on revenue and lock in repeat service contracts.

By Application: Injectable Formats Reshape Equipment Demand

Solid dosage held 36.59% of the 2024 volume, but the injectable sub-segment is projected to grow at an 8.29% CAGR, driven by biologics, vaccines, and complex combination therapies. Prefilled syringes, cartridges, and autoinjectors dominate pipeline launches; consequently, isolator-contained filling, plunger insertion, and visual inspection units attract outsized capital budgets. Syntegon’s modular lines, which fill and assemble 400 ready-to-use syringes per minute, illustrate the premium placed on sterility and speed. Sustained ordering drives the pharmaceutical packaging equipment market size in injectable applications, fueling demand for end-to-end validation support, including media-fill studies and container-closure integrity testing.

Liquid oral and topical formulations require stable run-rate volumes, necessitating flexible, quick-clean bottle lines. Powder inhalation and transdermal patches carve niche demand pockets demanding thermoform-fill-seal systems with humidity control modules.

By End-User Industry: Contract Organizations Gain Momentum

In 2024, pharmaceutical manufacturers accounted for 51.25% of installations, while CMOs displayed the highest 7.91% CAGR. Outsourcing continues due to capacity bottlenecks, speed-to-market imperatives, and the capital-intensive nature of aseptic assets. PCI Pharma Services’ USD 365 million global upgrade cycle exemplifies this wave. CMOs prioritize multi-format flexibility and line clearance efficiency to cater to multiple sponsors, thereby enhancing pull-through for innovations such as auto-adjusting infeed rails and recipe-based torque settings. Consequently, the pharmaceutical packaging equipment market increasingly banks on project-based orders from CMOs that convert swiftly to service contracts.

Research laboratories and clinical manufacturing centers procure small-batch, modular skids, while nutraceutical producers gradually adopt pharmaceutical standards, broadening the buyer universe without fundamentally shifting volume distribution.

Geography Analysis

Asia-Pacific’s 30.79% share in 2024 derived from China’s and India’s prolific output of generics and active ingredients. Roche earmarked CNY 3 billion (USD 420 million) to amplify its Suzhou fill-finish site, showcasing multinational confidence in Chinese capabilities. Harmonization through PIC/S and the evolving Chinese GMP has spurred the adoption of Western inspection standards, lifting per-line investment values. India’s export-oriented suppliers focus on high-speed blister and bottle platforms to maintain competitiveness against patent expiries. Collectively, these dynamics justify the region’s 7.19% CAGR, the quickest within the pharmaceutical packaging equipment market.

North America ranks second, propelled by DSCSA enforcement that mandates unit-level serialization by 2024. Simultaneously, biologics expansion persists: Novo Nordisk is spending USD 4.1 billion, and the National Research Council of Canada is backing the development of new mRNA facilities. Such projects demand aseptic filling, barrier isolators, and 100% visual inspection lines, expanding regional order books. Mexico emerges as a near-shore beneficiary under the USMCA, attracting capital for blister, pouch, and serialization.

Europe anchors technology leadership. German clusters, centered around Uhlmann, Körber, and OPTIMA, export integrated lines worldwide, while Italian networks, led by Marchesini, combine specialized optics and robotics. EU regulations on falsified medicines and recyclable packaging accelerate retrofit cycles across the bloc, ensuring a steady revenue baseline despite slower macro growth. Eastern European plants, supplied by Western OEMs, offer cost-efficient production for multinationals, deepening intra-European trade of machinery and service contracts that sustain the pharmaceutical packaging equipment market.

Competitive Landscape

The market remains moderately fragmented. Five leading groups, IMA, Uhlmann, Marchesini, Syntegon, and OPTIMA, collectively capture close to 35% of the global revenue, aided by broad portfolios and extensive installed-base service capabilities. Consolidation is accelerating: Uhlmann has purchased Goldfuß Engineering to strengthen its end-of-line robotics, and Syntegon has acquired Telstar for sterile containment technology. Marchesini partnered with SEA Vision to integrate AI-first vision modules across its entire range, reinforcing its full-line integration capabilities.

Competitive vectors pivot on sustainability retrofits, digital twins for rapid FAT/SAT, and predictive maintenance dashboards that lower the total cost of ownership. Asian challengers ACG, Chutian Technology, and Tofflon win domestic orders through cost advantages and increasingly match Western software sophistication. Nevertheless, global pharmaceutical companies still favor Western suppliers for initial installations when launching high-value biologics due to their established compliance track records.

Service economics is growing pivotal as average maintenance agreements now span five years and incorporate performance-based KPIs. Suppliers offering 24-hour remote diagnostics, parts stock guarantees, and cyber-security hardening gain renewal advantages, fortifying their foothold in the pharmaceutical packaging equipment market.

Pharmaceutical Packaging Equipment Industry Leaders

IMA S.p.A.

Uhlmann Pac-Systeme GmbH and Co. KG

Körber Medipak Systems GmbH

Marchesini Group S.p.A.

Romaco Holding GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Uhlmann Group posted EUR 504 million (USD 569.5 million) revenue for FY 2024-25, a 9% rise, while acquiring Goldfuß Engineering and enlarging its Singapore hub.

- December 2024: Syntegon Technology finalized its purchase of Telstar, broadening sterile processing know-how for biologics lines.

- November 2024: IMA Life invested USD 30 million in a New York production center dedicated to freeze-drying equipment.

- September 2024: Marchesini Group directed EUR 7 million (USD 7.9 million) toward CORIMA expansion, unveiling AI-enabled inspection systems.

Global Pharmaceutical Packaging Equipment Market Report Scope

| Blister Packaging Equipment |

| Bottle Filling Lines |

| Pouching and Sachet Machines |

| Cartoning Machines |

| Labeling and Coding Systems |

| Inspection and Serialization Systems |

| Other Machine Types |

| Primary Packaging Equipment |

| Secondary Packaging Equipment |

| Tertiary Packaging Equipment |

| Solid Dosage Forms |

| Liquid Dosage Forms |

| Injectable and Parenteral |

| Other Applications |

| Pharmaceutical Manufacturing Companies |

| Contract Manufacturing Organizations |

| Research and Development Laboratories |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Machine Type | Blister Packaging Equipment | ||

| Bottle Filling Lines | |||

| Pouching and Sachet Machines | |||

| Cartoning Machines | |||

| Labeling and Coding Systems | |||

| Inspection and Serialization Systems | |||

| Other Machine Types | |||

| By Packaging Type | Primary Packaging Equipment | ||

| Secondary Packaging Equipment | |||

| Tertiary Packaging Equipment | |||

| By Application | Solid Dosage Forms | ||

| Liquid Dosage Forms | |||

| Injectable and Parenteral | |||

| Other Applications | |||

| By End-User Industry | Pharmaceutical Manufacturing Companies | ||

| Contract Manufacturing Organizations | |||

| Research and Development Laboratories | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the pharmaceutical packaging equipment market?

The market is valued at USD 9.89 billion in 2025.

How fast is demand for inspection and serialization machinery growing?

Inspection and serialization systems are projected to expand at a 7.88% CAGR through 2030.

Which region is expanding the quickest for new equipment installations?

Asia-Pacific is pacing the field with a 7.19% CAGR to 2030.

Why are tertiary packaging solutions gaining attention?

Robotic case-packing and palletizing deliver labor savings and throughput boosts, supporting an 8.61% CAGR in tertiary equipment.

How do serialization mandates influence capital spending?

Full enforcement of DSCSA in November 2024 and EU rules are driving immediate retrofits and new line investments focused on unit-level tracking.

What factors limit adoption of advanced aseptic lines?

High capital costs of USD 10–50 million per line and prolonged payback periods restrict smaller firms from investing.

Page last updated on: