Corrugated Box Packaging Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

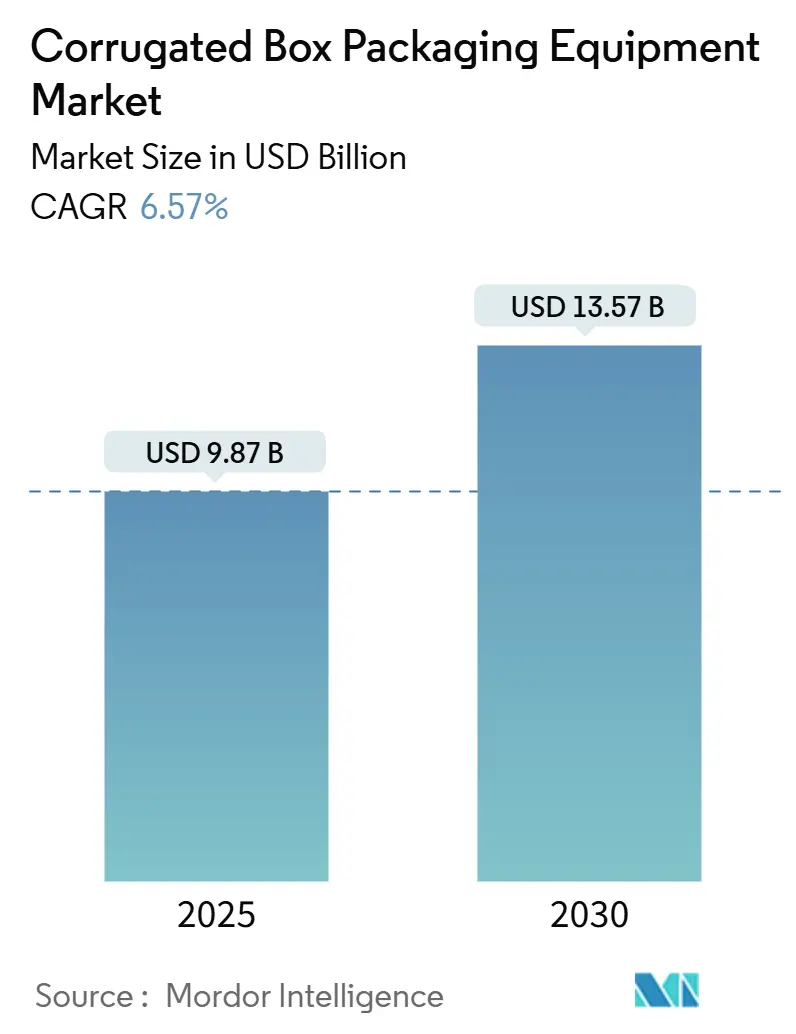

| Market Size (2025) | USD 9.87 Billion |

| Market Size (2030) | USD 13.57 Billion |

| Growth Rate (2025 - 2030) | 6.57% CAGR |

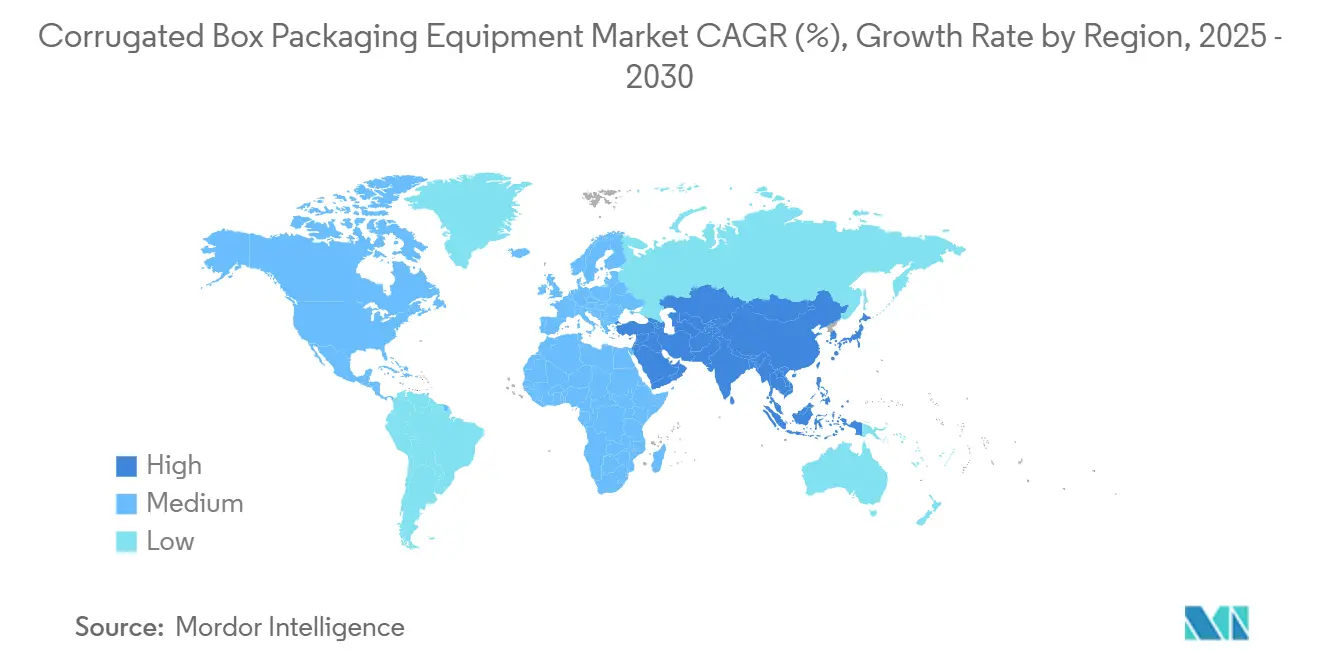

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Corrugated Box Packaging Equipment Market Analysis by Mordor Intelligence

The corrugated box packaging equipment market size stood at USD 9.87 billion in 2025 and is on track to reach USD 13.57 billion in 2030, registering a 6.57% CAGR. Momentum stems from the sustained e-commerce boom, corporate sustainability commitments, and manufacturers’ rapid pivot toward high-throughput, fully automatic lines. Vendors that combine servo-driven mechanics with cloud-based analytics are overcoming chronic labor shortages while lifting overall equipment effectiveness. Rapid machinery upgrades across Asia-Pacific, large sustainability-linked projects in Europe, and reshoring trends in North America jointly reinforce a healthy demand pipeline for the corrugated box packaging equipment market. Competitive intensity is rising as Chinese suppliers narrow quality gaps and as specialized automation firms capture white-space niches such as on-demand box making and vision-guided quality control.

Key Report Takeaways

- By machine type, flexo folder-gluer equipment held 38.21% of the corrugated box packaging equipment market share in 2024 while on-demand lines are projected to expand at a 14.83% CAGR through 2030.

- By automation level, fully automatic systems captured 47.01% of 2024 revenue; semi-automatic lines lag but still post a 12.48% CAGR to 2030.

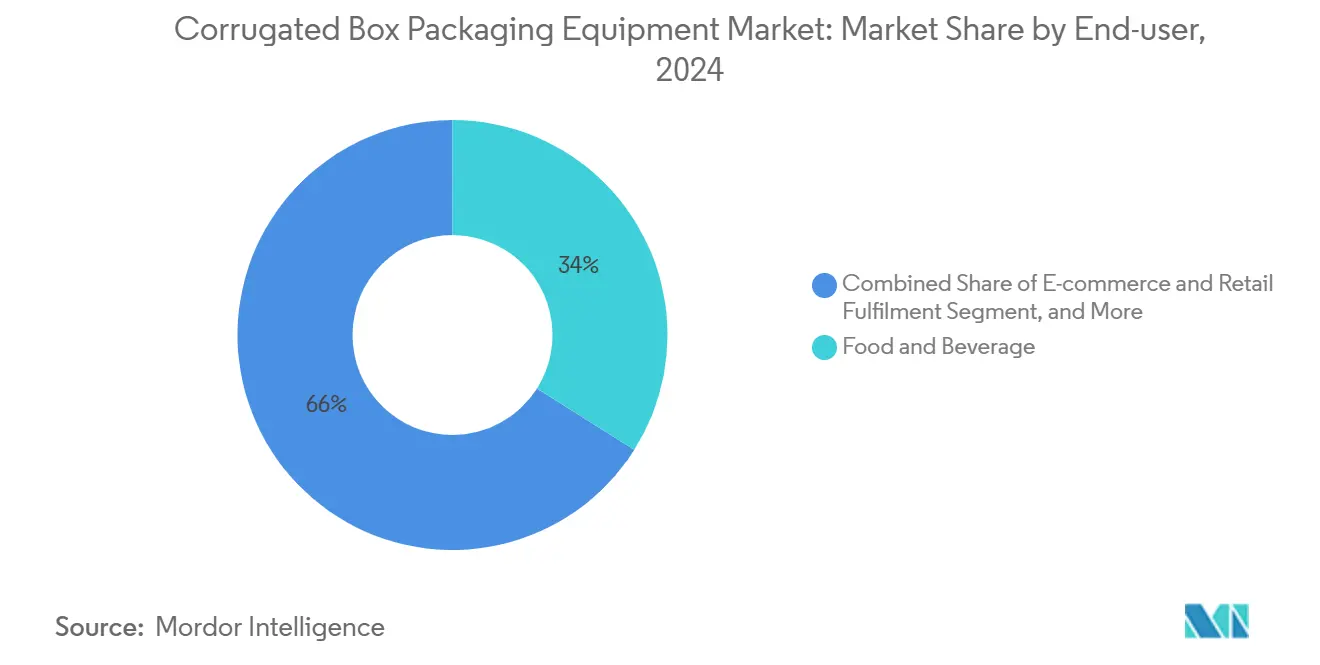

- By end-user industry, food and beverage applications led with 33.97% revenue share in 2024, whereas e-commerce and retail fulfillment is advancing at a 16.23% CAGR through 2030.

- By production capacity, 10-50 tons per hour installations commanded 41.04% of the corrugated box packaging equipment market size in 2024, while sub-10 tons per hour lines exhibit the fastest 13.13% CAGR to 2030.

- By geography, Asia-Pacific dominated with 52.21% revenue share in 2024 and is forecast to compound at an 8.71% CAGR through 2030.

Global Corrugated Box Packaging Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce Parcel Volume Surge | +2.1% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Sustainability-Linked Capex Incentives | +1.8% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Industry 4.0 Retrofits Slashing Downtime | +1.4% | Global, led by developed markets | Medium term (2-4 years) |

| Fit-To-Product Automated Lines for Void-Reduction | +1.2% | North America and Europe, early Asia-Pacific adoption | Short term (≤ 2 years) |

| Reshoring and Near-Shoring of Box Plants | +0.9% | North America and Europe | Long term (≥ 4 years) |

| High-Speed Vision QA Lowering QA Labor Need | +0.7% | Global, fastest adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Parcel Volume Surge

Expanding parcel streams compel fulfillment centers to adopt variable-size box makers that produce right-fit packaging on demand. The technology unlocks a USD 2.8 billion equipment opportunity as operators seek to curb dimensional-weight charges and void-fill costs. Mitsubishi Heavy Industries’ COMPOX system exemplifies this shift by marrying three-dimensional sizing with 600-box-per-hour throughput, enabling converters to trim material waste by up to 30% and monetize customized packaging services.[1]Mitsubishi Heavy Industries, “COMPOX Variable-Size Box-Making Machine,” mhi.com

Sustainability-Linked Capex Incentives

Corporate net-zero roadmaps and Extended Producer Responsibility rules accelerate fleet renewal toward energy-frugal machinery. DS Smith’s EUR 10 million (USD 10.8 million) purchase of a Bahmuller-Goepfert combination line underscores how decarbonization goals now shape equipment shortlists. Converters cite energy savings of 40-70% and larger recycled-content windows as decisive purchase triggers, reinforcing a replacement cycle that benefits vendors offering measurable eco-performance.[2]STI Group, “STI Group Invests EUR 8 million in Pioneering Laminating Technology,” sti-group.com

Industry 4.0 Retrofits Slashing Downtime

IoT sensors and machine-learning analytics cut unplanned stoppages from 15-20% to below 5%, materially lifting plant productivity. Closed-loop moisture control and vision-guided inspection protect print integrity and structural strength, while predictive maintenance prolongs asset life. Valmet, Bobst, and other OEMs bundle data dashboards and remote diagnostics, reducing dependence on scarce technicians and shortening troubleshooting cycles.[3]Bobst Group, “Annual Report 2024,” bobst.com

Fit-To-Product Automated Lines for Void-Reduction

On-demand systems that auto-adjust box dimensions appeal to logistics firms confronting Empty Space Ratio mandates. CMC Packaging Automation and Antalis launched a Scandinavian program that pairs right-sized packaging with labor-saving robotics, shrinking warehouse footprints and freight costs. AI-driven box DIM algorithms further optimize carton geometry over time, boosting warehouse turns and enhancing customer unboxing experiences. [4]CMC Packaging Automation, “Strategic Partnership with Antalis,” cmcsolutions.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Ticket Price for Fully-Automatic Lines | -1.6% | Global, most pronounced in emerging markets | Medium term (2-4 years) |

| Skilled Operator Shortage for Servo-Driven Machines | -1.2% | Developed markets, expanding globally | Long term (≥ 4 years) |

| Paper and Linerboard Price Volatility | -0.8% | Global, acute in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Fragmented Aftermarket-Service Networks in Emerging Markets | -0.5% | Africa and Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Ticket Price for Fully-Automatic Lines

State-of-the-art installations require USD 3-8 million, a jump that can delay projects among midsize converters lacking low-cost financing. Ancillary infrastructure-electrical upgrades, pits, and climate controls-adds 20-30% to budgets, making payback math daunting in volatile currency environments. Leasing and refurbished-equipment markets partly bridge the gap but often at the expense of digital-readiness and energy efficiency.

Skilled Operator Shortage for Servo-Driven Machines

Servo-based controls demand hybrid electro-mechanical expertise that remains scarce. Proficiency programs stretch 6-12 months, during which reduced line speeds and higher scrap rates erode ROI. OEMs are simplifying HMIs and embedding remote support, yet many converters still run redundant staffing or extended ramp-up schedules, limiting the immediate productivity gains promised by automation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: On-Demand Systems Drive Innovation

Flexo folder-gluers accounted for 38.21% of corrugated box packaging equipment market share in 2024, anchored by their versatility across standard board grades. However, fit-to-product lines are scaling fastest at a 14.83% CAGR, buoyed by direct-to-consumer retailers that want packaging tailored to each order. On-demand solutions shrink waste, trim freight charges, and position converters for premium service contracts, steering new CAPEX into smaller yet smarter machinery.

Mid-cycle upgrades center on rotary die-cutters for high-graphics retail displays and wet-end corrugators that boost speed without compromising board quality. Ancillary modules-stackers, palletizers, and in-line QA cameras-enhance through-line automation, meeting buyers’ demand for turnkey ecosystems rather than single-function units. Artificial-intelligence overlays predict blade wear, schedule tool changes, and benchmark output against peer lines, reinforcing a digital-first purchase mindset.

By Automation Level: Lights-Out Operations Gain Traction

Fully automatic equipment captured 47.01% of 2024 revenue and is projected to post a 12.48% CAGR as converters chase 24/7 uptime. Labor scarcity, rising wages, and workplace safety mandates reshape cost-benefit equations in favor of servo-driven lines that require minimal human intervention. Energy-regeneration drives and vacuum-controlled feeding further sharpen ROI calculations.

Semi-automatic installations persist where credit is tighter and labor remains plentiful, yet the performance delta is widening. Vendors bundle modular upgrades that let buyers migrate from manual to semi-automatic and eventually to lights-out operations, easing CapEx sticker shock. Predictive diagnostics embedded in PLCs alert plant managers before faults escalate, preserving throughput and safeguarding operator confidence in automation rollouts.

By End-User Industry: E-Commerce Reshapes Demand Patterns

Food and beverage converters led with a 33.97% stake in 2024, leveraging long production runs and steady SKU mixes. Still, e-commerce and retail fulfillment is the breakout vertical, advancing at 16.23% CAGR as marketplaces demand variable-size, logo-ready cartons. Electronics and appliance producers add further momentum by specifying shock-absorbing corrugated inserts tailored to fragile goods, nudging equipment makers to enhance creasing precision and board caliper flexibility.

Pharmaceutical shippers require tight dimensional tolerances and traceability, pushing machinery to integrate barcode verification and GMP-compliant cleaning regimes. Automotive and industrial customers prioritize double-wall, triple-flute strength, rewarding equipment that processes heavy-basis-weight papers without throttling speed. Across categories, recycled-content mandates spur demand for lines capable of handling higher OCC inputs while maintaining burst strength.

By Production Capacity: Mid-Range Systems Dominate

Installations rated 10-50 tons per hour delivered 41.04% of 2024 revenue, marrying adequate throughput with manageable CapEx. Such lines anchor plants that juggle multiple SKUs yet still crave batch flexibility. The sub-10 tons per hour cohort, however, is sprinting ahead at 13.13% CAGR, propelled by on-demand and micro-fulfillment models where right-size packaging trumps maximum volume.

In contrast, >100 tons per hour behemoths serve commodity board producers in China and the United States that chase unit-cost leadership. They rely on high-speed splicers, dual-lane stackers, and inline QA vision to sustain efficiency. Yet even megaplants now earmark floor space for smaller agile cells that tackle rush orders and specialty runs, underscoring a bimodal capacity strategy across the corrugated box packaging equipment market.

Geography Analysis

Asia-Pacific retained 52.21% revenue share in 2024, underpinned by China’s vast board output and India’s consumer-goods ascent. Regional equipment buyers favor full-line turnkey projects that couple wet-end corrugators with smart palletizers, ensuring rapid scale-up while sidestepping labor constraints. Government incentives for domestic machinery production further compress lead times and lower capital outlays. Japan remains a technology beacon, exporting precision robotics for folder-gluer retrofits and nurturing local demand for lights-out plants focused on high-mix, low-volume orders.

North America enjoys tailwinds from reshoring and its deep e-commerce ecosystem. Fulfillment-center proliferation and parcel-shipper contracts inject steady orders for on-demand lines, especially among third-party logistics providers adopting right-size packaging to meet newly enacted dimensional-weight surcharges. Sustainability regulations, including Extended Producer Responsibility laws, spur replacements of legacy steam-heated corrugators with energy-smart units featuring closed-loop heat recovery.

Europe treads a mixed path. Strict Packaging and Packaging Waste Regulation targets oblige converters to raise recycled-content thresholds, prompting investments in equipment that maintains board integrity with higher OCC inputs. Yet economic uncertainty and elevated interest rates temper spending, so plant managers prioritize machinery that pairs ecological compliance with measurable cost savings. Germany maintains pole position in precision die-cutting systems, while Southern Europe leans on mid-range folding-gluing units that balance affordability and feature sets.

The Middle East and Africa present early-stage expansion prospects. Import-substitution programs in Saudi Arabia and South Africa seed greenfield corrugator installations, though financing hurdles and service-network gaps elongate sales cycles. Latin America’s outlook brightens on near-shoring, with Mexico winning incremental investment as North American OEMs seek cross-border supply resilience.

Competitive Landscape

The corrugated box packaging equipment market displays moderate fragmentation. Top European houses such as Bobst Group and BHS Corrugated preserve technology leadership through continuous R&D, but Chinese entrants have narrowed quality differentials and gained share via aggressive pricing. Japanese suppliers like Mitsubishi Heavy Industries emphasize servo-controlled innovations, while niche automation firms target AI-driven vision inspection and predictive maintenance.

Strategic focus is shifting from pure speed metrics to digital ecosystems that entwine machinery, software, and services. Bobst’s 2024 results showcased rising subscription revenue from its Helpline Plus remote-support platform, underscoring how lifecycle contracts nurture sticky customer ties. Packsize and CMC occupy the high-growth on-demand niche, combining cloud-based box-dimensioning with compact forming units. Meanwhile, regional integrators partner with sensor and robotics providers to retrofit legacy lines, stretching plant lifespans and delaying wholesale replacements.

Sustainability remains a central battleground. OEMs tout energy-regeneration drives, lightweight blade materials, and glue-optimization algorithms to trim operating costs and CO₂ footprints. Equipment resale platforms are gaining traction as converters monetize used assets to fund next-gen purchases, intensifying cyclical upgrade patterns. Competitive parity now hinges on bundled offerings that merge mechanical reliability with data-rich dashboards, field-service responsiveness, and credible decarbonization narratives.

Corrugated Box Packaging Equipment Industry Leaders

Bobst Group SA

BW Papersystems (Barry-Wehmiller)

Mitsubishi Heavy Industries Printing and Packaging

BHS Corrugated Maschinen- und Anlagenbau GmbH

Dongfang Precision Science and Technology (Fosber)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: BW Papersystems delivered its 100th SheetWizard Dual Rotary Sheeter to Sylvamo do Brasil, featuring automatic pallet change and 1,100 ft-per-minute precision cutting.

- November 2024: DS Smith unveiled a multi-million USD investment in new heavy-duty corrugated machinery, broadening its portfolio for bulky goods packaging.

- October 2024: Mitsubishi Heavy Industries installed the first MPF-MII Prefeeder in North America, advancing automated feeding solutions for high-speed lines.

- October 2024: Mondi agreed to acquire seven Schumacher Packaging corrugated plants and two mega-box facilities in Germany for EUR 634 million (USD 685 million).

Global Corrugated Box Packaging Equipment Market Report Scope

The Corrugated Box Packaging Equipment Market Report is Segmented by Machine Type (Flexo Folder-Gluer, Rotary Die-Cutter, Single-Facer/Corrugator Wet-End, Finishing/Folder-Gluer Post-Print, Ancillary), Automation Level (Manual, Semi-Automatic, Fully Automatic/Lights-Out), End-User Industry (Food and Beverage, E-commerce and Retail Fulfilment, Electronics and Appliances, Pharmaceuticals and Healthcare, Industrial and Automotive), Production Capacity (<10, 10-50, 51-100, >100 Tons/hr), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Flexo Folder-Gluer (FFG) |

| Rotary Die-Cutter |

| Single-Facer / Corrugator Wet-End |

| Finishing / Folder-Gluer Post-Print |

| Ancillary (Stackers, QA, Palletizers) |

| Manual |

| Semi-Automatic |

| Fully Automatic / Lights-Out |

| Food and Beverage |

| E-commerce and Retail Fulfilment |

| Electronics and Appliances |

| Pharmaceuticals and Healthcare |

| Industrial and Automotive |

| Less than 10 Tons/Hr |

| 10 - 50 Tons/Hr |

| 51 - 100 Tons/Hr |

| Above 100 Tons/Hr |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Machine Type | Flexo Folder-Gluer (FFG) | ||

| Rotary Die-Cutter | |||

| Single-Facer / Corrugator Wet-End | |||

| Finishing / Folder-Gluer Post-Print | |||

| Ancillary (Stackers, QA, Palletizers) | |||

| By Automation Level | Manual | ||

| Semi-Automatic | |||

| Fully Automatic / Lights-Out | |||

| By End-User Industry | Food and Beverage | ||

| E-commerce and Retail Fulfilment | |||

| Electronics and Appliances | |||

| Pharmaceuticals and Healthcare | |||

| Industrial and Automotive | |||

| By Production Capacity | Less than 10 Tons/Hr | ||

| 10 - 50 Tons/Hr | |||

| 51 - 100 Tons/Hr | |||

| Above 100 Tons/Hr | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the corrugated box packaging equipment market in 2025?

The corrugated box packaging equipment market size reached USD 9.87 billion in 2025 and is projected to hit USD 13.57 billion by 2030.

Which equipment segment is growing the fastest?

Fit-to-product on-demand lines post the highest 14.83% CAGR through 2030, driven by e-commerce demand for variable-size cartons.

Why are fully automatic systems gaining popularity?

They reduce labor dependence, improve quality consistency, and enable 24/7 output, helping converters offset skilled-operator shortages.

Which region leads global demand?

Asia-Pacific commands 52.21% revenue share and maintains the strongest 8.71% CAGR thanks to China’s scale and India’s consumer-goods expansion.

What is the main restraint on equipment adoption?

High upfront costs for fully automatic lines, ranging from USD 3-8 million, limit uptake among midsize converters, especially in emerging markets.

Page last updated on: