Spa And Salon Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

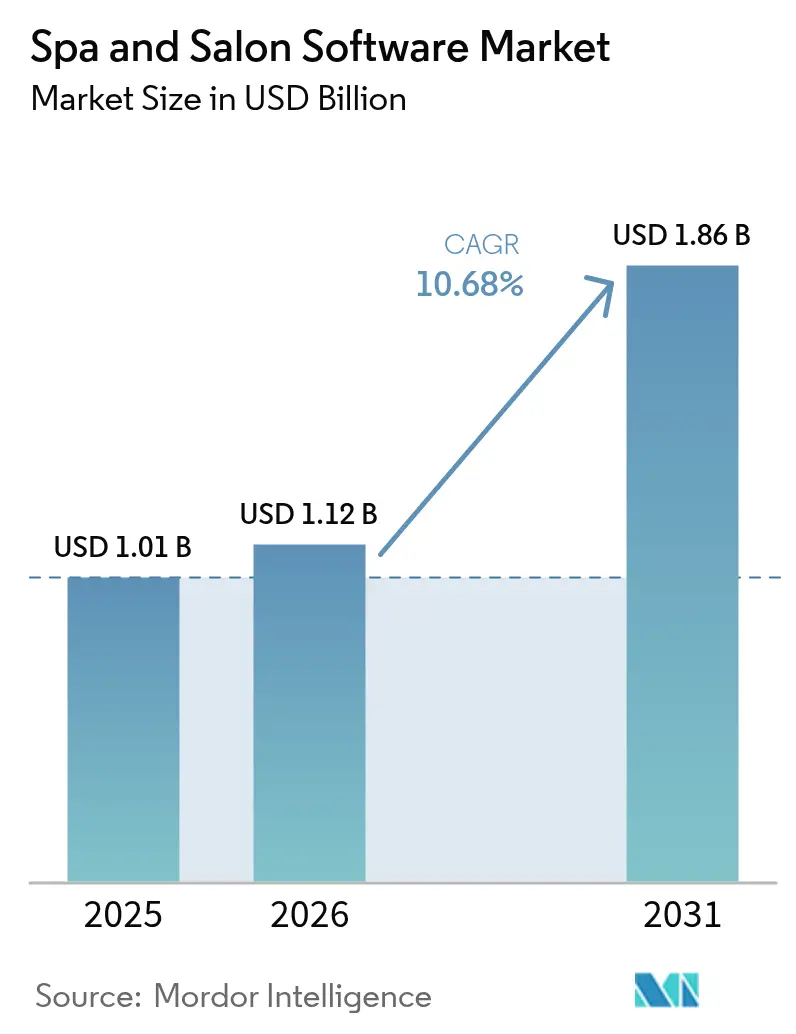

| Market Size (2026) | USD 1.12 Billion |

| Market Size (2031) | USD 1.86 Billion |

| Growth Rate (2026 - 2031) | 10.68% CAGR |

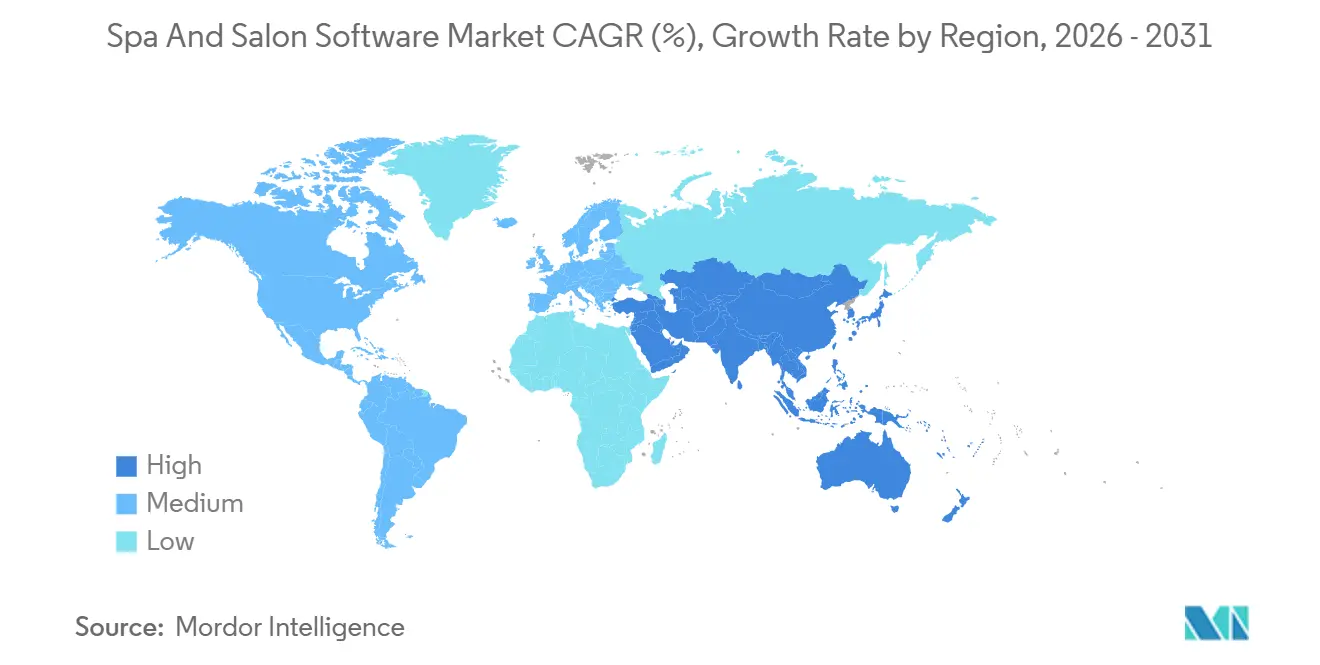

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

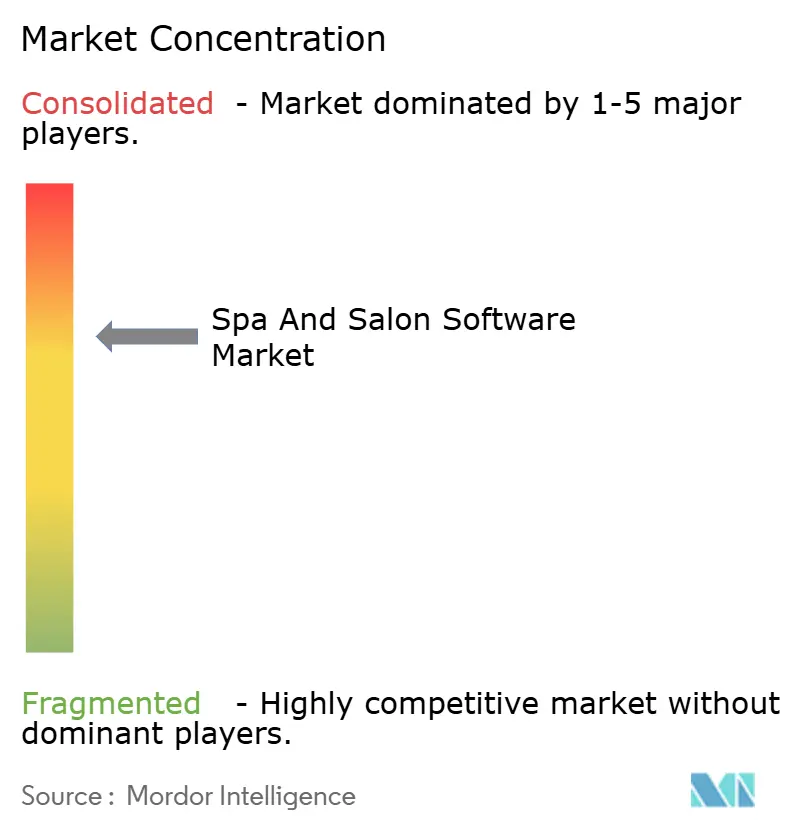

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spa And Salon Software Market Analysis by Mordor Intelligence

The spa and salon software market size was valued at USD 1.01 billion in 2025 and is estimated to grow from USD 1.12 billion in 2026 to reach USD 1.86 billion by 2031, at a CAGR of 10.68% during 2026-2031. Rapid migration from fragmented point solutions to unified cloud platforms, the embedding of payments and instant-payout finance, and the integration of AI-driven personalization are the principal structural forces accelerating demand. Small and individual professionals remained the largest customer cohort in 2025, yet multi-location chains are adopting centralized dashboards and cross-location data synchronization tools to scale efficiently. Cloud deployment, already dominant, continues to displace on-premises systems because subscription SaaS eliminates costly servers and enables real-time updates across dispersed sites. Marketplace integrations such as Square Go are raising client-acquisition efficiency, signalling that discovery, booking, and payment will converge on a single platform experience.

Key Report Takeaways

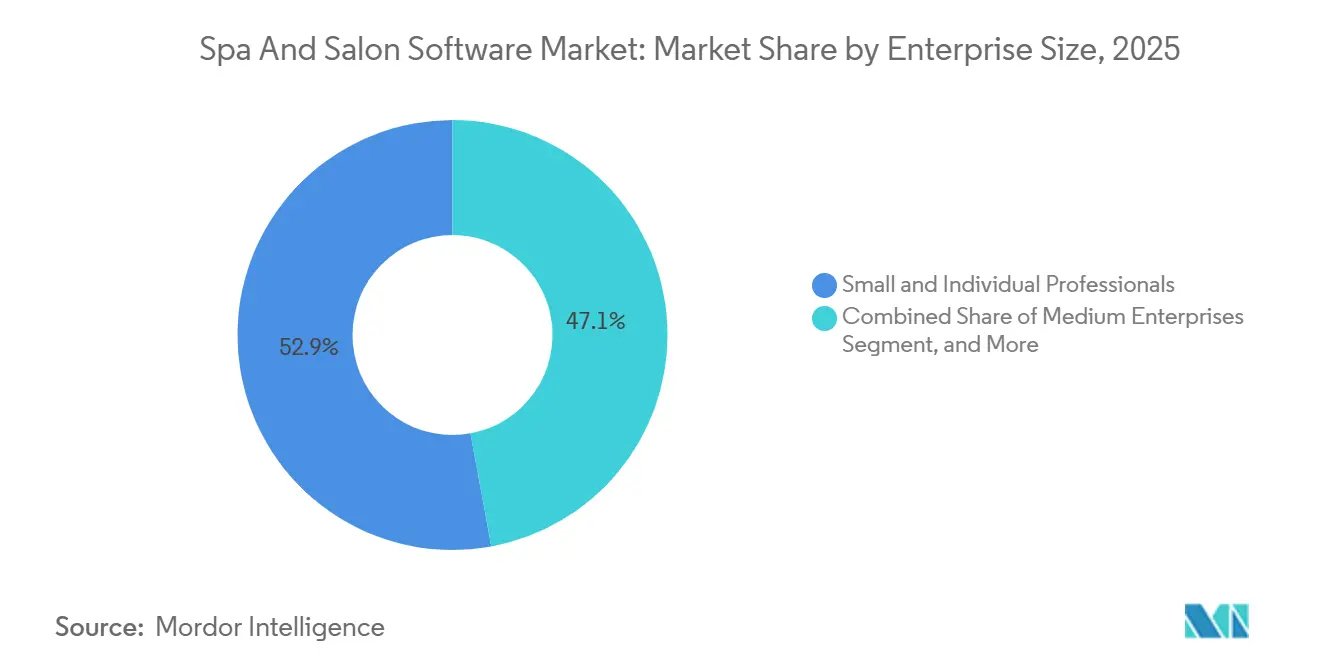

- By enterprise size, small and individual professionals commanded 52.89% of the spa and salon software market share in 2025, while medium enterprises are projected to grow at a 11.23% CAGR through 2031.

- By deployment model, cloud held 71.36% of the spa and salon software market in 2025 and is forecast to expand at a 11.27% CAGR between 2026-2031.

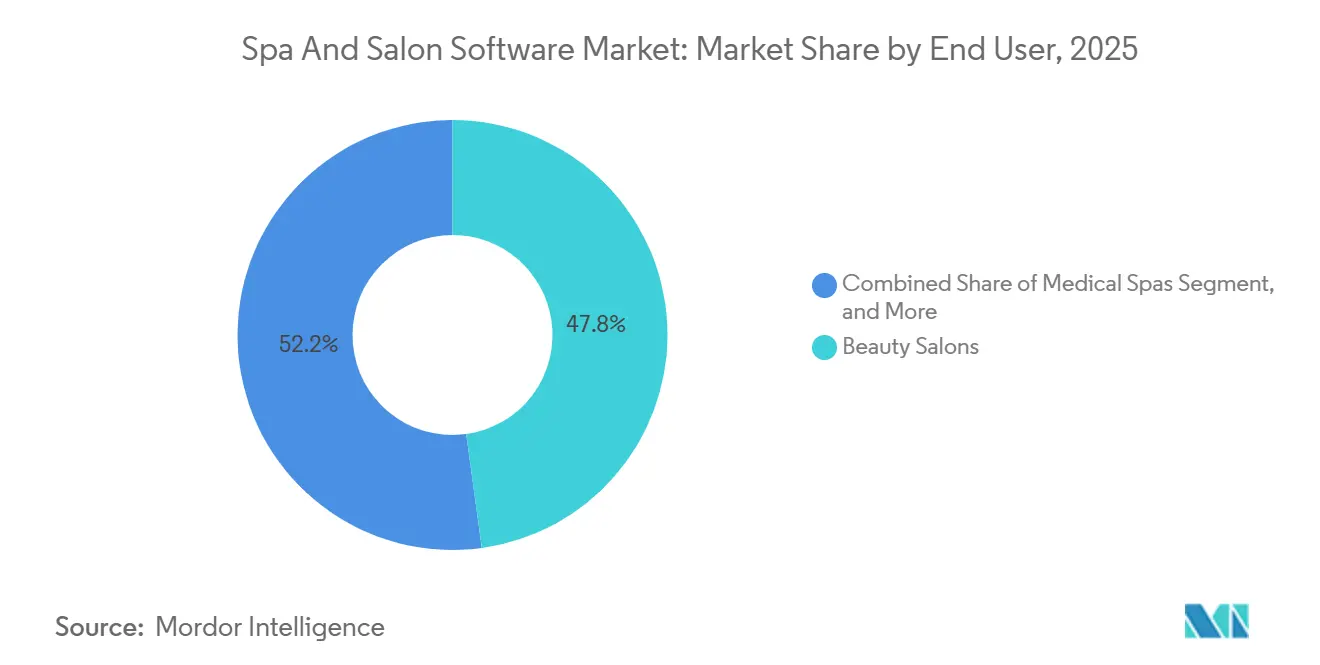

- By end user, beauty salons led with 47.82% revenue share in 2025; medical spas are set to grow at the fastest 11.89% CAGR to 2031.

- By functional module, appointment and CRM captured 36.46% of the spa and salon software market in 2025, while business intelligence and reporting is the fastest-growing module at a 11.64% CAGR.

- By geography, North America accounted for a 39.22% share of the spa and salon software market in 2025, whereas Asia-Pacific is the quickest-expanding region at an 11.69% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Spa And Salon Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Powered Hyper-Personalisation of Client Journeys | +2.3% | Global, with early adoption in North America, South Korea, and China | Medium term (2-4 years) |

| Rising Adoption of Cloud-Native SaaS by Multi-Location Chains | +2.1% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Marketplace Integrations Driving Client Acquisition and Upsell | +1.8% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Embedded Finance and Instant Payouts Improving Cash-Flow | +1.6% | Global, with rapid uptake in United States, United Kingdom, Australia, Canada | Short term (≤ 2 years) |

| Expansion of Membership-Based Revenue Models | +1.4% | Global, led by North America and Europe | Medium term (2-4 years) |

| Post-COVID Wellness Surge Among Gen-Z and Men | +1.2% | Global, with pronounced growth in Asia-Pacific and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Powered Hyper-Personalization of Client Journeys

South Korean beauty chains installed AI skin-analysis kiosks that completed more than 160,000 consumer scans by late 2025, lifting average ticket values as shoppers accepted algorithm-generated treatment recommendations.[1]Pulse by Maeil Business News Korea, “AI-Driven Skin Diagnostics,” mk.co.kr U.S. platforms such as GlossGenius now bundle a marketing assistant that drafts SMS and email campaigns in a stylist’s own brand voice, cutting manual promotion time to minutes. Reviva’s AI Treatment Builder pulls from past visit data, allergies, and service menus to automatically create step-by-step protocols that staff can follow without additional training. Operators report higher rebooking because guests experience tailored recommendations that feel clinically precise, yet the tools run in the background with no added labor. As more vendors bake predictive engines into core workflows, personalization shifts from a premium upcharge to a baseline expectation.

Rising Adoption of Cloud-Native SaaS by Multi-Location Chains

Zenoti found that salons that activated its multi-location toolkit earned an additional USD 163,000 in six months by using nearby-availability prompts and real-time waitlists to fill idle slots.[2]Zenoti, “Multi-Location Capability Revenue Impact,” zenoti.com Indian franchise leader Lakme Salon scaled past 500 outlets across 215 cities, a footprint that would be impossible to monitor without cloud dashboards that synchronize pricing, permissions, and KPIs each night. Cloud systems eliminate local servers, reducing capital expenses and enabling franchisors to push updates instantly to every location. The model also simplifies compliance by centralizing security patch management and audit logs. Chains expanding into new regions therefore view SaaS as a non-negotiable utility rather than an optional upgrade.

Marketplace Integrations Driving Client Acquisition and Upsell

Square Go links 250,000 beauty professionals with 300,000 monthly shoppers, and the company reports that marketplace clients rebook 38% more often than standard customers.[3]Square, “Square Go: The Free Marketplace App for Client Bookings,” squareup.com Mindbody studios that listed classes on ClassPass saw reservation volume jump roughly 30%, converting unused capacity into incremental revenue with no extra ad spend. Visibility inside a consumer marketplace eliminates the need for solo salons to master digital advertising or loyalty apps. Because idle appointment slots perish every hour, automated discovery channels have become a growth lever as powerful as price increases. Vendors without a built-in marketplace risk churn to platforms that bundle awareness, booking, and payment into a single loop.

Embedded Finance and Instant Payouts Improving Cash Flow

Fresha Capital advanced more than USD 5.5 million in revenue-based loans across seven countries within weeks of its February 2026 launch, and 80% of borrowers returned for a second round, showing high satisfaction with the model. Vagaro Capital moved nearly USD 3 million to 200 salons during its first month, depositing funds within hours and automatically deducting repayments from daily card sales. Instant access to USD 500-50,000 lets owners cover payroll or buy lasers without lengthy bank approvals, reducing cash-flow anxiety in a business where revenue fluctuates by day of the week. Platforms earn new fee streams and deepen loyalty because merchants depend on the software for both bookings and liquidity. As more vendors embed payout rails, access to on-dashboard capital is set to become a standard item on prospective buyers' checklists.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Switching and Implementation Costs for Legacy Users | -1.4% | Global, particularly North America and Europe with high legacy system penetration | Short term (≤ 2 years) |

| Growing Threat of Horizontal POS/Booking Platforms | -1.1% | Global, with highest intensity in North America, Europe, and Asia-Pacific urban markets | Medium term (2-4 years) |

| Fragmented Regulatory Data-Privacy Landscape | -0.9% | Europe (GDPR), North America (CCPA), Asia-Pacific (emerging frameworks) | Medium term (2-4 years) |

| Talent Shortage in IT Support for SMBs | -0.7% | Global, with acute impact in emerging markets and rural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Switching and Implementation Costs for Legacy Users

Square’s migration guide warns that owners often face 12-18 months of parallel running while staff learn the new dashboard and historical data is ported from aging servers. Zenoti highlights that fragmented tool stacks force salons to juggle spreadsheets and manual imports, making the risk of downtime feel greater than the promise of efficiency gains. Independent operators with no IT staff struggle most because contract exit penalties, training hours, and data-cleanup tasks hit cash and morale simultaneously. Even with vendor-led onboarding, owners still absorb lost billable time while calendars and retail SKUs reconcile. These hidden costs delay many upgrade decisions despite clear long-term benefits.

Fragmented Regulatory Data-Privacy Landscape

Medical spas in the United States must encrypt charts, vitals, and images under HIPAA rules, while European facilities juggle GDPR consent screens and breach-notification timelines that differ from California’s CCPA mandates. Vagaro holds ISO 27001, SOC 2, and HIPAA certifications, yet acknowledges that auditing and renewing these attestations can be costly. Smaller regional vendors often lack the resources to track shifting rules, which can limit cross-border rollouts for their clients. Franchise brands planning to expand from London to Dubai pause until their software proves compliance in both jurisdictions. The inconsistent patchwork, therefore, serves as both a moat for market leaders and a drag on overall adoption speed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Enterprise Size: Medium Enterprises Gain Speed From Franchise Digitalization

Small and individual professionals captured 52.89% of the spa and salon software market share in 2025, reflecting a vast base of booth renters and single-location salons that prize affordability and mobile usability. Within the overall spa and salon software market, the medium-enterprise cohort is projected to expand at a 11.23% CAGR between 2026-2031 as chain owners demand centralized dashboards, multi-location client files, and corporate reporting. Boulevard processes nearly USD 5 billion in annual payments for more than 5,000 U.S. businesses, evidence that mid-tier brands migrate once manual coordination breaks down.

Franchise expansion underpins this growth. Lakme Salon’s 500-unit network across 215 Indian cities relies on cloud dashboards that synchronize pricing and permissions nightly, ensuring brand standards are maintained despite distance. MyTime’s checklist for scalable franchises stresses multi-location hierarchy, intelligent scheduling, and open APIs, all features that convert rising complexity into repeatable playbooks. As more midsize chains cross the ten-location threshold, vendors with proven enterprise controls and white-glove onboarding are positioned for disproportionate share gains.

By Deployment Model: Cloud Extends Unassailable Lead

Cloud solutions accounted for 71.36% of the spa and salon software market share in 2025, and the spa and salon software market size tied to cloud is forecast to grow at a 11.27% CAGR through 2031. SaaS eliminates on-premises servers, provides automatic backups, and lets owners log in from anywhere; the benefits of on-premises systems cannot match without costly IT staff. Zenoti reports that multi-location clients using its cloud toolkit gained an extra USD 163,000 in six months by filling cancellations with real-time waitlists.

Hybrid installs persist as a bridge for operators phasing out old hardware, yet vendors are sunsetting hybrid support in favor of pure SaaS, shrinking the on-premises niche each quarter. Embedded finance underscores the shift, because loan underwriters such as Fresha Capital require live sales feeds that only cloud data lakes provide. As license renewals arrive, most owners find that the total cost of on-premises, including servers, manual patches, and downtime, exceeds the predictable monthly subscription cost, cementing the cloud’s lead.

By End User: Beauty Salons Still Dominate While Medical Spas Surge

Beauty salons commanded 47.82% of the spa and salon software market share in 2025, anchored by hair, nail, and full-service centers that require straightforward appointment books and mobile POS. The spa and salon software market size tied to medical spas, however, is forecast to advance at an 11.89% CAGR to 2031, as injectables, IV therapy, and laser services require HIPAA-compliant charting and encrypted image storage. Boulevard captured 15% of the U.S. medspa vertical within three years by embedding nested consent forms and practitioner license checks.

Day and resort spas emphasize shared bookings and sequential thermal rituals, driving demand for capacity management and package linkage in the scheduler. Barbershops and grooming studios require walk-in queue boards and rapid tip tracking to serve high-frequency male clientele, a segment rising sharply in Asia and North America. Nail and lash bars need minute-accurate blocks plus inventory deductions for each gel polish or lash tray, pushing vendors to refine vertical templates. The widening gap between compliance rules and workflow nuances fuels specialization, with platforms tailoring language, consent, and resource logic to each end-user niche.

By Functional Module: Analytics Rises From Back-Office To Profit Engine

The Appointment and CRM modules held 36.46% of the spa and salon software market in 2025, confirming their status as operational bedrock. Yet the analytics stack is the fastest-growing; business-intelligence tools are set to post a 11.64% CAGR over 2026-2031 as owners demand real-time dashboards on service mix, staff utilization, and retail performance. Phorest benchmarks each stylist against local peers and flags rebooking gaps, letting managers nudge under-performers with targeted goals.

Payments and POS modules integrate buy-now-pay-later, which Square data show lifts average ticket size by 2.6 times compared with standard cards. Inventory systems now automatically deduct back-bar product usage, triggering restock orders that free cash that would otherwise be stuck on the shelf. Staff-management engines forecast labor needs using AI, aligning rosters with demand curves, and reducing overtime. The convergence of these once-separate modules into unified suites reduces double entry and error rates, turning data visibility into a daily decision tool rather than a month-end report.

Geography Analysis

North America accounted for 39.22% of the spa and salon software market share in 2025, as large franchise chains and independent specialists already rely on vertical SaaS for scheduling, payments, and embedded finance. Vendors continue to upsell AI assistants, revenue-based lending, and business-intelligence dashboards instead of pursuing first-time conversions, so average revenue per user in the region is the highest globally. The United States also leads pilot programs for instant-payout rails because Fintech charters enable platforms to settle card proceeds within minutes rather than days.

Asia-Pacific is the fastest-growing geography, projected to grow at a 11.69% CAGR from 2026-2031, as salon owners in China and India shift from notebooks to mobile apps that bundle discovery and payments. South Korea accelerates demand with AI skin-diagnostic kiosks that push clinics toward data-rich cloud systems, while Gangnam Unni’s 8 million-user marketplace funnels international tourists into local aesthetic centers. As these countries digitize, the incremental spa and salon software market size from Asia-Pacific often matches North America’s annual growth rate, despite a lower base.

Europe grows more moderately because GDPR forces vendors to engineer jurisdiction-specific consent flows and breach-notification logs, stretching development roadmaps. Consolidation helps offset the compliance drag: the Treatwell-Uala merger created a 45,000-salon network that can negotiate payment rates and API access at scale. South America, led by Brazil, and the Middle East and Africa remain in early adoption stages where localized payment gateways such as Mada or Pix determine vendor selection, yet government e-invoicing mandates are nudging owners toward compliant cloud platforms. Overall, regional differences in privacy law, digital payment norms, and tourism flows shape feature priorities, but unified cloud stacks allow global players to roll out localized templates quickly.

Competitive Landscape

The market is moderately concentrated: the top five platforms, Vagaro, Booksy, Mindbody, Styleseat, and Fresha, collectively accounted for roughly 76% of online booking traffic in 2025, yet no single firm holds a dominant market share across every segment. Vendors primarily compete by incorporating financial services into their offerings, integrating artificial intelligence (AI) assistants to enhance functionality, and managing consumer marketplaces effectively to minimize the costs associated with merchant acquisition.

Scale advantages intensified in January 2026 when Playlist, parent of Mindbody and ClassPass, agreed to merge with EGYM, forming a USD 7.5 billion entity boasting USD 800 million net revenue in 2025. Square, meanwhile, leverages its broader merchant ecosystem to cross-sell scheduling, banking, and point-of-sale, reaching 600,000 monthly active beauty and wellness sellers and undercutting vertical players on payment fees. Boulevard differentiates itself as up-market by offering enterprise controls such as single sign-on and role-based permissions, securing 15% of the U.S. medspa vertical less than 3 years after entering the niche.

White-space persists in HIPAA-driven medical spas, male-grooming walk-ins, and cross-border tourism hubs that require multilingual and multi-currency billing. AI-native upstarts like RhinoAgents promise 25% efficiency gains with virtual front-desk bots, putting pressure on incumbents to release conversational tools quickly. All major platforms now field embedded-finance arms Fresha Capital, Vagaro Capital, Mindbody Capital, and AuraPay Capital, creating a commoditized lending layer where approval speed, flexible repayment, and transparent flat fees become key differentiators. Competitive intensity is likely to heighten as private-equity-backed rollups chase the remaining independent vendors, aiming to amass data scale large enough to train proprietary AI models and lock in merchant loyalty.

Spa And Salon Software Industry Leaders

Mindbody, Inc.

Vagaro, Inc.

DaySmart Software, LLC

Boulevard Labs Inc.

GlossGenius, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Adyen and Fresha announced that Fresha Capital surpassed USD 5.5 million in capital issued after expanding to seven markets.

- January 2026: Playlist (Mindbody, ClassPass) and EGYM agreed to merge, backed by USD 785 million new equity, creating a USD 7.5 billion entity.

- October 2026: Square partnered with SalonCentric and released new App Marketplace integrations to extend beauty-specific functionality.

- August 2025: Boulevard secured USD 80 million Series D funding to accelerate AI research and enterprise features.

Global Spa And Salon Software Market Report Scope

The Spa and Salon Software Market Report is Segmented by Enterprise Size (Small and Individual Professionals, Medium Enterprises, Large Enterprises), Deployment Model (Cloud, On-Premises, Hybrid), End User (Beauty Salons, Day and Resort Spas, Medical Spas, Barbershops and Grooming Studios, Nail and Lash Studios, Other End Users), Functional Module (Appointment and CRM, POS and Payments, Inventory and Supply-Chain, Staff and Resource Management, Business Intelligence and Reporting), and Geography (North America, South America, Europe, Asia Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Small and Individual Professionals |

| Medium Enterprises |

| Large Enterprises |

| Cloud |

| On-Premises |

| Hybrid |

| Beauty Salons |

| Day and Resort Spas |

| Medical Spas |

| Barbershops and Grooming Studios |

| Nail and Lash Studios |

| Other End Users |

| Appointment and CRM |

| POS and Payments |

| Inventory and Supply-Chain |

| Staff and Resource Management |

| Business Intelligence and Reporting |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Enterprise Size | Small and Individual Professionals | ||

| Medium Enterprises | |||

| Large Enterprises | |||

| By Deployment Model | Cloud | ||

| On-Premises | |||

| Hybrid | |||

| By End User | Beauty Salons | ||

| Day and Resort Spas | |||

| Medical Spas | |||

| Barbershops and Grooming Studios | |||

| Nail and Lash Studios | |||

| Other End Users | |||

| By Functional Module | Appointment and CRM | ||

| POS and Payments | |||

| Inventory and Supply-Chain | |||

| Staff and Resource Management | |||

| Business Intelligence and Reporting | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will the spa and salon software market be by 2031?

It is forecast to reach USD 1.86 billion by 2031, growing at a 10.68% CAGR from 2026.

Which region is growing fastest for spa technology vendors?

Asia-Pacific is projected to expand at an 11.69% CAGR, fueled by digitization in China and India plus AI skin-diagnostics adoption in South Korea.

Why are medical spas adopting new software faster than beauty salons?

Medical spas need HIPAA-compliant charting, consent management, and multi-resource booking that legacy salon systems cannot deliver, driving an 11.89% CAGR for this segment.

What makes cloud deployment so dominant?

Cloud eliminates servers, provides live updates, and enables embedded finance that relies on real-time data, giving it 71.36% share in 2025 and continued double-digit growth.

How do embedded finance products benefit salon owners?

Revenue-based advances like Fresha Capital fund payroll or equipment within hours, with repayment tied to daily sales, improving cash flow without traditional loan paperwork.

Which functional module is gaining the most traction?

Business intelligence and reporting is the fastest-growing module at an 11.64% CAGR as owners seek predictive insights on service mix and staff utilization.

Page last updated on: