High Throughput Process Development Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 18.16 Billion |

| Market Size (2031) | USD 27.63 Billion |

| Growth Rate (2026 - 2031) | 8.78% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High Throughput Process Development Market Analysis by Mordor Intelligence

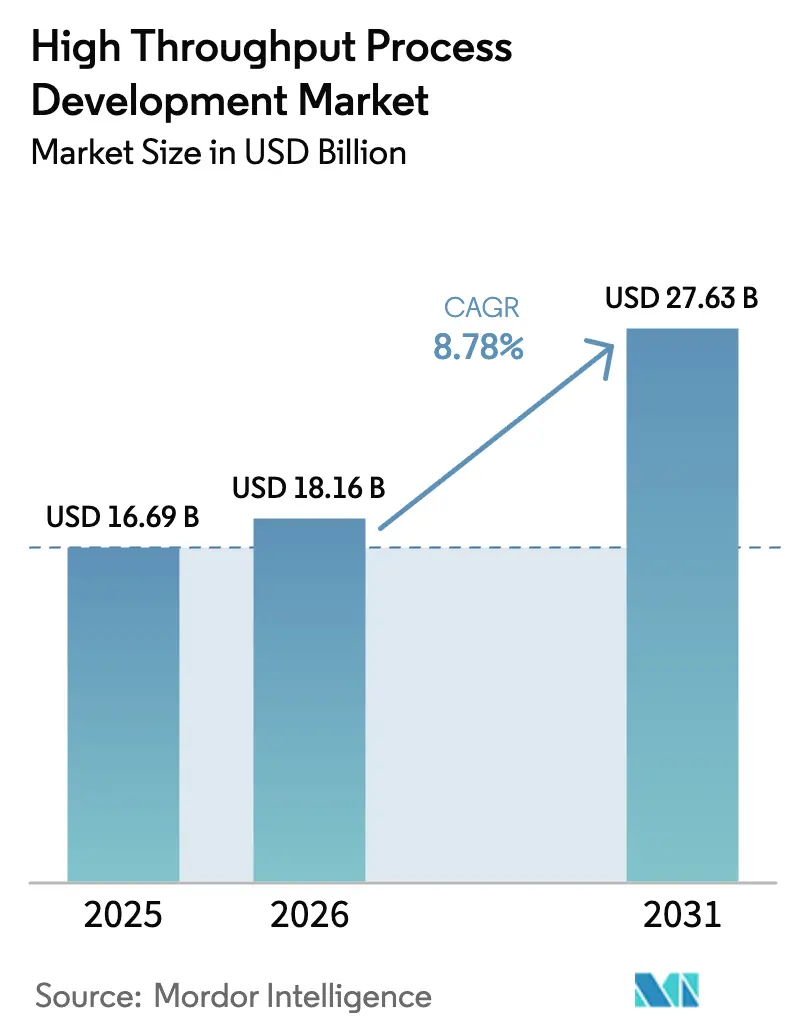

High Throughput Process Development market size in 2026 is estimated at USD 18.16 billion, growing from 2025 value of USD 16.69 billion with 2031 projections showing USD 27.63 billion, growing at 8.78% CAGR over 2026-2031.

Demand for miniaturized automated platforms, rising biologics approvals, and regulatory encouragement for advanced manufacturing are accelerating uptake across biopharma R&D and production settings. Chromatography innovations that support continuous downstream processing, wider adoption of predictive analytics, and an expanding contract development footprint are reshaping competitive strategies. The United States and Europe benefit from regulatory clarity and capital inflows, while Asia-Pacific is gaining momentum through large-scale public investment and improved local supply chains. Environmental scrutiny of single-use plastics and persistent shortages of digitally skilled staff remain the prime counterweights to growth.

Key Report Takeaways

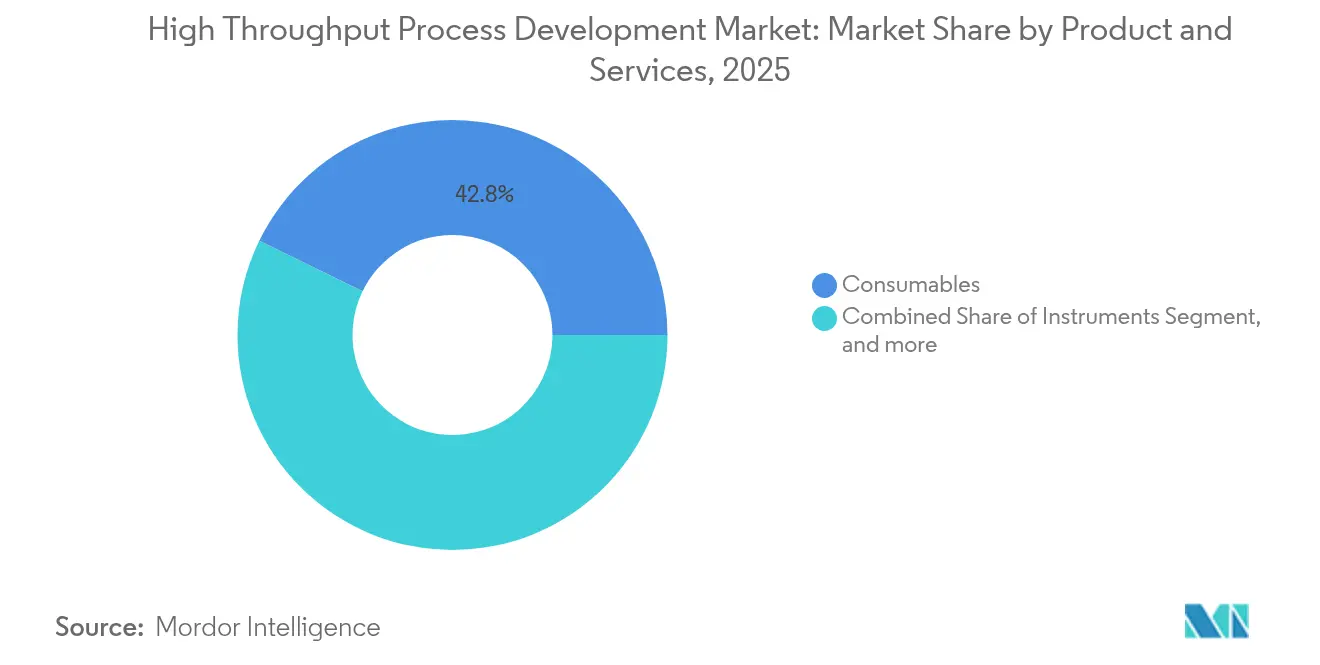

- By product & services type, consumables led with 42.78% of the high throughput process development market share in 2025; software solutions are forecast to expand at an 11.42% CAGR to 2031.

- By technology, chromatography commanded 51.12% share of the high throughput process development market size in 2025 and is advancing at a 9.19% CAGR through 2031.

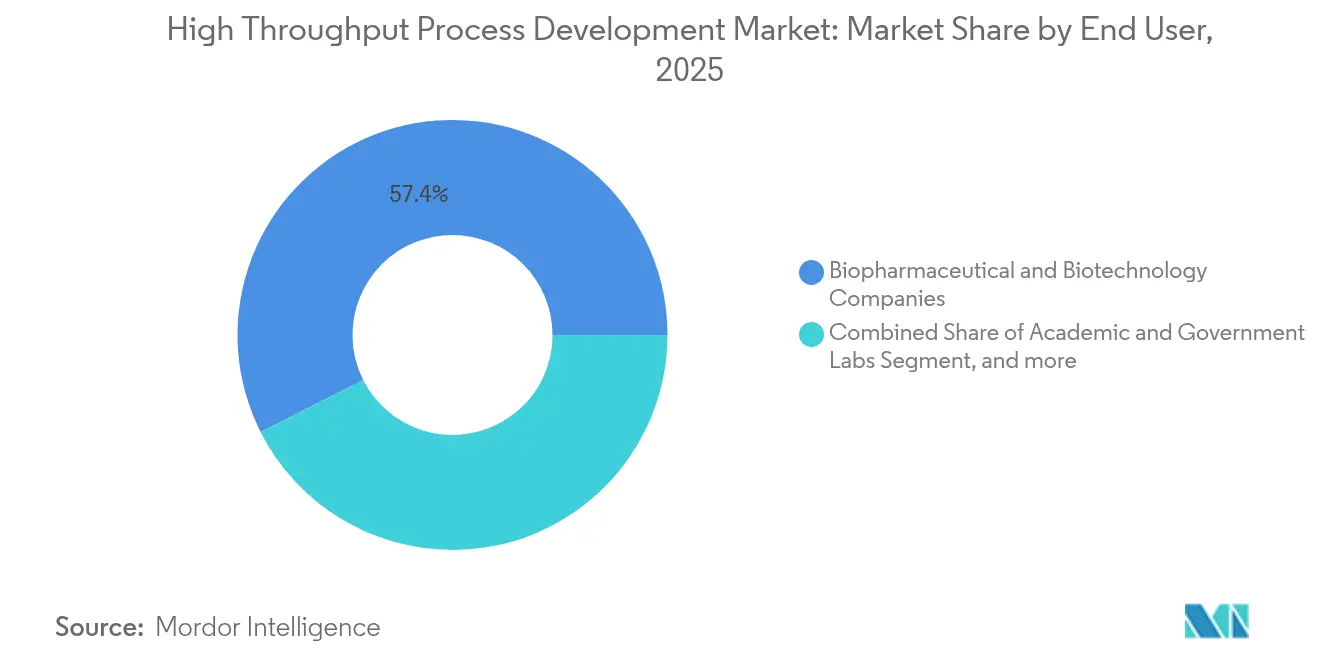

- By end user, biopharmaceutical and biotechnology companies held 57.44% revenue share in 2025, while contract research and manufacturing organizations are projected to grow at a 12.24% CAGR during 2026-2031.

- By geography, North America accounted for 39.12% share of the high throughput process development market in 2025; Asia-Pacific is set to register the highest regional CAGR at 10.67% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global High Throughput Process Development Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Demand for Next-Gen Biologics | +2.1% | Global, concentrated in North America & EU | Medium term (2-4 years) |

| Cost Pressure in Biomanufacturing | +1.8% | Global, particularly acute in Asia-Pacific | Short term (≤ 2 years) |

| Shift Toward Continuous and Intensified Processing | +1.6% | North America & EU lead, APAC adoption rising | Long term (≥ 4 years) |

| Miniaturized, Single-Use Technologies | +1.4% | Global, early uptake in North America | Medium term (2-4 years) |

| AI-Driven Analytics and Automation | +1.2% | North America & EU core, spill-over to APAC | Long term (≥ 4 years) |

| Near-Shoring and Supply Chain Resilience | +0.9% | North America & EU with regional hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Demand for Next-Gen Biologics

The FDA cleared 33 new biological products in 2024, including several gene and cell therapies, underscoring the rapid evolution of therapeutic pipelines.[1]Center for Biologics Evaluation and Research, “BLA Approvals 2024,” fda.govComplex modalities require smaller, configurable development platforms capable of parallel experimentation, which is expanding uptake of high-throughput bioreactor arrays. Flexible facilities let manufacturers pivot between low-volume personalized treatments and larger commercial runs without lengthy changeovers. Companies are building modular plants dedicated to next-generation antibodies, such as Kyowa Kirin’s USD 530 million site in North Carolina.[2]Kyowa Kirin Co. Ltd., “Kyowa Kirin to Build North Carolina Biologics Plant,” kyowakirin.com These investments shorten development cycles and reduce material waste, boosting adoption of micro-scale screening tools.

Cost Pressure in Biomanufacturing

Health-system price controls and intensifying biosimilar rivalry continue to squeeze margins, pushing firms toward process intensification and outsourcing. Continuous bioprocessing platforms decrease plant footprints and utility costs, while strategic offloading to Asian CDMOs lowers capital exposure. Firms such as WuXi and Samsung have added mammalian and antibody-drug conjugate suites to meet global demand, leveraging regional cost advantages. Artificial-intelligence engines embedded in supervisory control systems improve resource utilization by double-digit percentages, supporting real-time cost governance. Although single-use components carry higher material prices, they remove cleaning validation expenses and limit cross-contamination risk for multi-product lines.

Shift Toward Continuous and Intensified Processing

Regulators explicitly encourage continuous production; the FDA’s Advanced Manufacturing Technologies Designation Program fast-tracks novel hardware and analytical solutions. Perfusion bioreactors now reach cell densities above 100 million cells/mL, increasing volumetric productivity and curbing media consumption. Multicolumn continuous chromatography modules complement upstream gains, cutting buffer use and cycle times. North American sites adopt these systems to retrofit legacy plants, while Asian greenfield projects specify intensified flows from day one. Integrated upstream-downstream skids demonstrate processing time reductions near 60% and yield improvements above 30%, validating the economics of end-to-end continuous lines.

Rising Demand for Miniaturized, Single-Use Technologies

Micro-scale tools multiply experimental throughput and minimize reagent use. An MDPI study documented automated RNA-Seq preparation of 24 samples within 11.5 hours when coupled to parallel miniature bioreactors. Scalability from 15 mL to 250 mL supports early clone ranking and media optimization without compromising performance. Environmental concerns are steering suppliers toward recyclable polymers and lower-impact resins ahead of new USP requirements effective 2026. Microfluidic chips are emerging to manipulate picoliter volumes, allowing thousands of process variants to be screened daily and accelerating data generation for machine-learning models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Investment and Infrastructure Needs | -1.9% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Talent Shortage in Automation and Data Science | -1.5% | North America & EU core, spreading to APAC | Medium term (2-4 years) |

| Data Integration Challenges Across Scales | -0.8% | Global | Long term (≥ 4 years) |

| Environmental Concerns Over Single-Use Plastics | -0.6% | EU leading, North America following | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Investment and Infrastructure Needs

Setting up a full-scope high-throughput process development center can demand USD 50–100 million in equipment, cleanrooms, and analytics. Compliance with multiple regulatory regimes adds validation and documentation expenses. Modular plant concepts mitigate risk by breaking construction into discrete skids deployable in phases. Resilience allocated USD 225 million for a modular drug-product complex that can be reconfigured rapidly to different modalities. Cloud-based data environments lower on-premise information-technology costs, but cybersecurity and qualification overhead persist, limiting smaller entrants.

Talent Shortage in Automation and Data Science

Digital bioprocessing needs engineers fluent in control theory, coding, and biochemistry, yet the pipeline of qualified staff falls short. The National Institute for Bioprocessing Research and Training (NIBRT) reports rising demand for programming skills alongside classic upstream expertise.[3]National Institute for Bioprocessing Research and Training, “Talent Needs in Biopharma Manufacturing,” nibrt.ie Companies escalate internal academies and university partnerships to reskill operators on Python, R, and SQL. Automation partly offsets labor gaps but also raises the bar for technical proficiency, creating a self-reinforcing shortage cycle. Regions that combine government grants with academic curricula, such as Ireland and Singapore, are making incremental progress but capacity constraints continue to cap throughput expansions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product & Services Type: Software Drives Digital Transformation

The software category represents the fastest-expanding component of the high throughput process development market, growing at an 11.42% CAGR on rising demand for real-time analytics and digital twins. Consumables preserved a 42.78% share of the high throughput process development market in 2025 as single-use bags, filters, and prepacked columns remain indispensable for rapid setup. Instruments maintain steady momentum with automated liquid handlers and multicolumn chromatography skids supporting intensified workflows. Services are becoming more attractive as firms outsource specialized statistical modeling, chemometrics, and validation tasks to concentrate capital on core assets.

Digital platforms integrate disparate data sources, apply machine-learning models to optimize parameters, and enable remote collaboration among globally distributed teams. Regulatory guidance on software assurance clarifies expectations for algorithm transparency, reducing adoption hesitancy. The high throughput process development market size for software applications is projected to widen in tandem with continuous processing because control algorithms must reconcile upstream and downstream operations in near real time. Consumables growth remains tied to the transition toward flexible facilities, though suppliers are redesigning plastics to meet tightening environmental standards.

By Technology: Chromatography Maintains Dominance

Chromatography retained 51.12% share of the high throughput process development market size in 2025 growing at an 9.19% CAGR, underpinned by the ubiquity of Protein A affinity steps in monoclonal antibody production. Waters launched its BioResolve Protein A column with seven-fold sensitivity gains, enabling earlier detection of titer changes that inform feed strategies. Continuous multicolumn formats such as simulated moving bed, commercialized by KNAUER, cut buffer use and shorten process times. Ion-exchange and hydrophobic-interaction variants address emerging modalities like antibody-drug conjugates, while inline sensors measure product quality attributes to ensure regulatory compliance.

Upstream intensification amplifies the load entering purification trains, requiring higher-capacity resins and smarter scheduling algorithms. Chromatography vendors differentiate through ligand stability, lower elution volumes, and resin recyclability. Alternative separation technologies, including membrane adsorbers and precipitation, gain niche traction but have yet to match chromatography’s versatility. As continuous purification converges with perfusion culture, integration readiness keeps chromatography at the center of process development strategies within the high throughput process development market.

By End User: CRO/CMO Segment Accelerates

Biopharma and biotech companies controlled 57.44% of spending in 2025, driven by internal pipeline priorities and platform manufacturing strategies. Contract research and manufacturing organizations are the most dynamic end-user group, advancing at a 12.24% CAGR as sponsors adopt asset-light models to conserve capital. Large CDMOs build integrated suites that span cell-line development to commercial fill-finish, appealing to emerging firms lacking infrastructure. Academic and government laboratories remain critical for method innovation and standards development, providing open data that feed industry benchmarking efforts.

The high throughput process development market increasingly revolves around partnership ecosystems. Sponsors supply molecular blueprints and clinical insight, while CDMOs provide scale-up expertise and global regulatory interfaces. Automation enables CDMOs to run multiplexed projects concurrently, improving facility utilization. As regulatory submissions demand richer process understanding, CDMOs invest in advanced analytics to ensure each candidate meets evolving quality requirements. Talent shortages present a bottleneck; therefore, strategic alliances include staff secondment and joint training modules to secure skills pipelines.

Geography Analysis

North America led the high throughput process development market with a 39.12% revenue contribution in 2025, supported by sizeable capacity investments such as Lonza’s USD 1.2 billion Vacaville acquisition that added 330,000 L of mammalian capacity. The United States benefits from responsive regulatory pathways that endorse advanced manufacturing, spurring early adoption of continuous bioprocessing and AI-driven control software. Government grants and workforce initiatives further bolster the region’s competitiveness.

Europe sustains strong innovation in purification chemistry, analytics, and sustainability practices. Environmental directives accelerate the pivot toward recyclable single-use systems and carbon-efficient operations. The region also contributes to global harmonization of standards, which supports technology exports to emerging markets. Investment flows target both legacy hubs in Germany and Ireland and expanding clusters in Central and Eastern Europe that offer competitive cost structures.

Asia-Pacific delivers the fastest growth at a 10.67% CAGR through 2031, propelled by China’s USD 4.17 billion national biomanufacturing program and Japan’s biotech revitalization roadmap. Singapore and South Korea act as regional centers of excellence for cell and gene therapies. Local CDMOs secure global contracts, reinforced by advantageous cost bases and improving regulatory transparency. Despite expansion, shortages in experienced automation engineers temper project timelines. South America and the Middle East & Africa trail but show rising interest as governments seek domestic biologics production to lower import dependency and strengthen health security.

Competitive Landscape

The high throughput process development market is moderately fragmented, with established chromatography and bioreactor suppliers competing alongside digital-native entrants. Automation capability, data interoperability, and sustainability credentials weigh more heavily in purchasing decisions than legacy throughput metrics. Sartorius and Siemens announced plans to integrate supervisory control software with single-use bioreactors to deliver plug-and-play intensified production lines. Similar collaborations pair hardware innovators with algorithm specialists to accelerate product rollouts and reduce validation burdens.

Large suppliers leverage scale to bundle consumables, instruments, and software into unified platforms. Mid-size firms carve out niches in microfluidics, digital twins, or eco-designed plastics. The FDA’s Advanced Manufacturing Technologies Designation Program grants early engagement with reviewers, offering smaller innovators a route to credibility and market entry. Competitive positioning thus hinges on the ability to demonstrate regulatory-ready documentation and measurable sustainability gains. White-space opportunities persist in integrating continuous downstream operations, developing recyclable polymer alternatives, and linking laboratory data directly to enterprise resource planning for end-to-end traceability within the high throughput process development market.

High Throughput Process Development Industry Leaders

Agilent Technologies

Thermo Fischer Scientific

Danaher Corporation

Bio Rad Laboratories Inc.

GE Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Amgen announced a USD 900 million investment to expand its Ohio biomanufacturing facility, focusing on advanced biologics production capabilities and process intensification technologies to support growing demand for complex therapeutics.

- January 2025: Cytiva and Cellular Origins announced a strategic partnership to integrate automated cell and gene therapy manufacturing technologies, combining Cytiva's Sefia platform with Cellular Origins' Constellation robotic platform for scalable CGT production.

- September 2024: Serán BioScience secured over USD 200 million in strategic growth funding to build a commercial-scale manufacturing facility in Oregon, featuring advanced particle engineering solutions including spray drying and hot melt extrusion capabilities.

- June 2024: Kyowa Kirin approved up to USD 530 million investment to build its first North American biologics manufacturing facility in North Carolina, focusing on next-generation antibody production for rare diseases.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the high-throughput process development (HTPD) market as global revenue from instruments, single-use or reusable consumables, workflow software, and service contracts that let bioprocess teams run many miniature upstream or downstream experiments in parallel before pilot scale.

Scope exclusion: stand-alone high-throughput screening platforms used only for small-molecule library assays are not counted.

Segmentation Overview

- By Product & Services Type

- Consumables

- Instruments

- Automated Liquid Handlers

- Chromatography Systems

- Other Instruments

- Services

- Software

- By Technology

- Chromatography

- Affinity

- Ion-exchange

- Size-Exclusion & Membrane Chromatography

- UV-Visible Spectroscopy

- Other Technologies

- Chromatography

- By End User

- Biopharmaceutical & Biotechnology Companies

- Contract Research & Manufacturing Organization

- Academic & Government Labs

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed bioprocess engineers, CDMO sourcing heads, automation vendors, and regulators across North America, Europe, and Asia-Pacific. The talks validated unit counts, average selling prices, and new preferences such as single-use micro-columns, which fine-tuned regional adoption curves.

Desk Research

We drew on publicly available pillars such as US FDA Emerging Technology notes, EMA guidance on process analytics, BIO annual biologics output tables, Harmonized System trade codes for chromatography media, and patent sets accessed through Questel. Company 10-Ks, investor decks, and quality case studies mapped price lanes, while D&B Hoovers and Dow Jones Factiva clustered supplier revenues. These references illustrate the desk path, and many additional sources were reviewed to cross-check facts.

Market-Sizing & Forecasting

We anchored sales through a top-down rebuild of global biologics capacity and R&D spend, applied step-wise HTPD penetration ratios, and cross-checked totals with sampled supplier roll-ups. Key drivers include single-use bioreactor installations, monoclonal antibody pipeline size, chromatography resin pricing, median optimization cycles, and regional wage indices. Multivariate regression blended with scenario analysis projects demand, and channel checks close any bottom-up gaps.

Data Validation & Update Cycle

Outputs pass three-layer variance checks and senior review, and if any driver moves beyond five percent against fresh trade or regulatory data, the model is reopened. Reports refresh annually, with interim flashes for material events.

Why Mordor's High Throughput Process Development Baseline Earns Trust

Published estimates diverge because definitions, currency years, and optimism levels shift, yet our disciplined variables and yearly refresh narrow those spreads.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 16.69 B (2025) | Mordor Intelligence | - |

| USD 10.87 B (2024) | Global Consultancy A | Counts tools only and omits consumables |

| USD 20.20 B (2024) | Regional Consultancy B | Blends HTPD with high-throughput screening revenue |

| USD 15.30 B (2024) | Industry Journal C | Uses constant 2023 FX rates and infrequent updates |

These comparisons show that our balanced scope, dual-path modeling, and peer-validated inputs give decision-makers a dependable midpoint.

Key Questions Answered in the Report

What is driving demand in the high throughput process development market?

Rising approvals of complex biologics and regulatory support for continuous manufacturing are encouraging biopharma firms to adopt automated, miniaturized platforms that shorten development timelines.

Which product segment is growing the fastest?

Software solutions are expanding at an 11.42% CAGR through 2031 as companies integrate digital twins and predictive analytics into routine process development.

Why is Asia-Pacific considered the growth engine?

Government funding programs, cost advantages, and improving regulatory systems are propelling the region to a projected 10.67% CAGR, the highest worldwide.

How do continuous bioprocessing technologies cut costs?

Perfusion and multicolumn chromatography systems increase volumetric productivity, reduce buffer consumption, and shrink facility footprints, producing measurable operational savings.

What are the main obstacles to wider adoption?

High upfront capital needs and a shortage of personnel skilled in automation and data science impede rapid scale-out, though modular plants and targeted training are easing these constraints.

How intense is competition among suppliers?

The market remains moderately fragmented; differentiation now hinges on advanced automation, data integration, and sustainable materials rather than basic throughput specifications.

Page last updated on: