Bioprocess Validation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

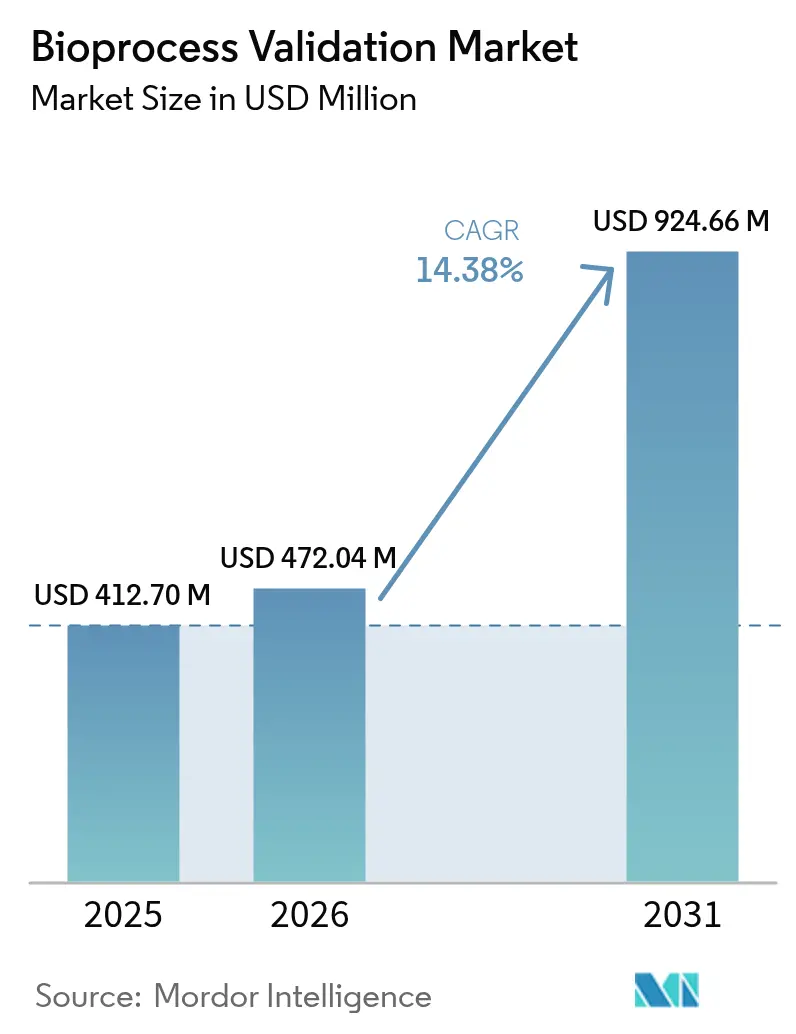

| Market Size (2026) | USD 472.04 Million |

| Market Size (2031) | USD 924.66 Million |

| Growth Rate (2026 - 2031) | 14.38% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bioprocess Validation Market Analysis by Mordor Intelligence

Bioprocess validation market size in 2026 is estimated at USD 472.04 million, growing from 2025 value of USD 412.70 million with 2031 projections showing USD 924.66 million, growing at 14.38% CAGR over 2026-2031. Growth is anchored in three inter-locking forces: stricter global regulatory guidance, greater volumes of commercial and clinical biologics, and the steady migration of validation work to contract development and manufacturing organizations (CDMOs). Demand has broadened as biologics account for around 50% of all drug candidates, which magnifies the number of facilities, processes, and analytical procedures that must be formally qualified. The United States Food and Drug Administration (FDA) and the European Medicines Agency (EMA) updated viral safety, analytical procedure, and contamination-control expectations in 2024, creating new compliance milestones that most producers must meet before batch release[1]U.S. Food and Drug Administration, “Q5A(R2) Viral Safety Evaluation of Biotechnology Products Derived From Cell Lines,” fda.gov. Digital validation frameworks—built around electronic batch records, data-integrity checkpoints, and audit-ready data trails—are now a major differentiator because they shorten inspection cycles and reduce the risk of compliance findings[2]Rapid Microbiology, “EMA Annex 1: Key Changes and Validation Implications,” rapidmicrobiology.com.

Key Report Takeaways

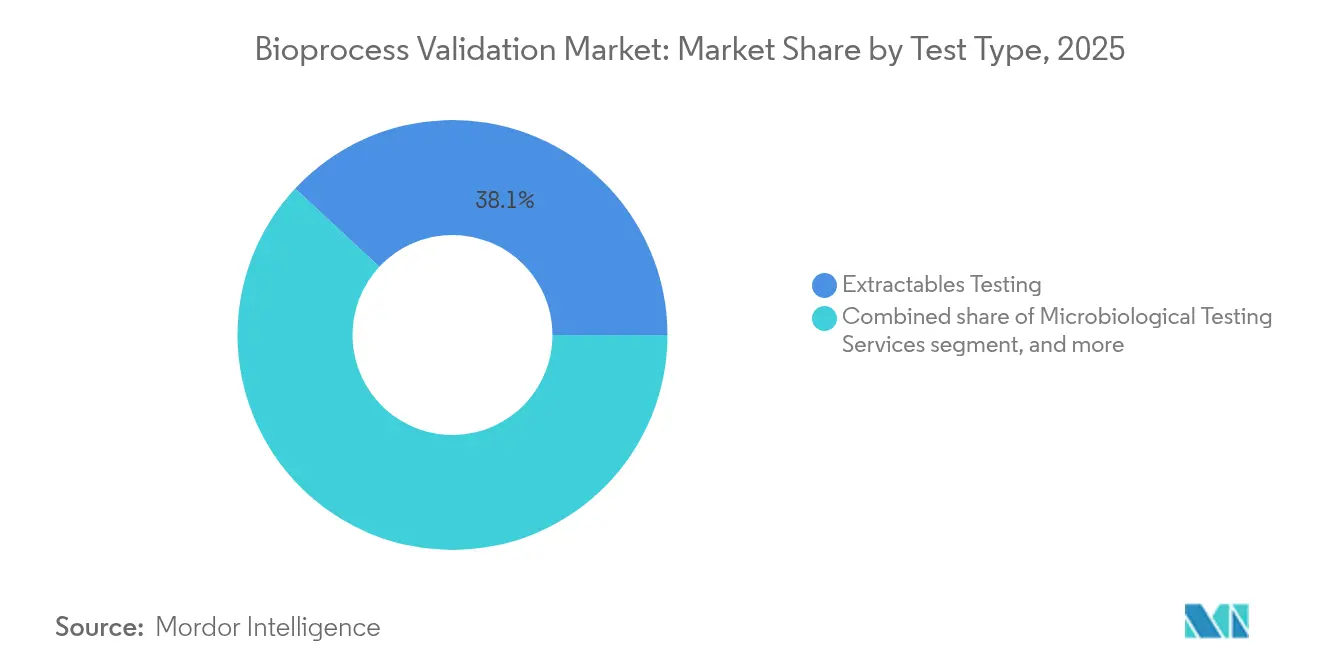

- By test type, extractables testing led with 38.07% of bioprocess validation market share in 2025, while integrity testing is forecast to expand at a 15.92% CAGR through 2031.

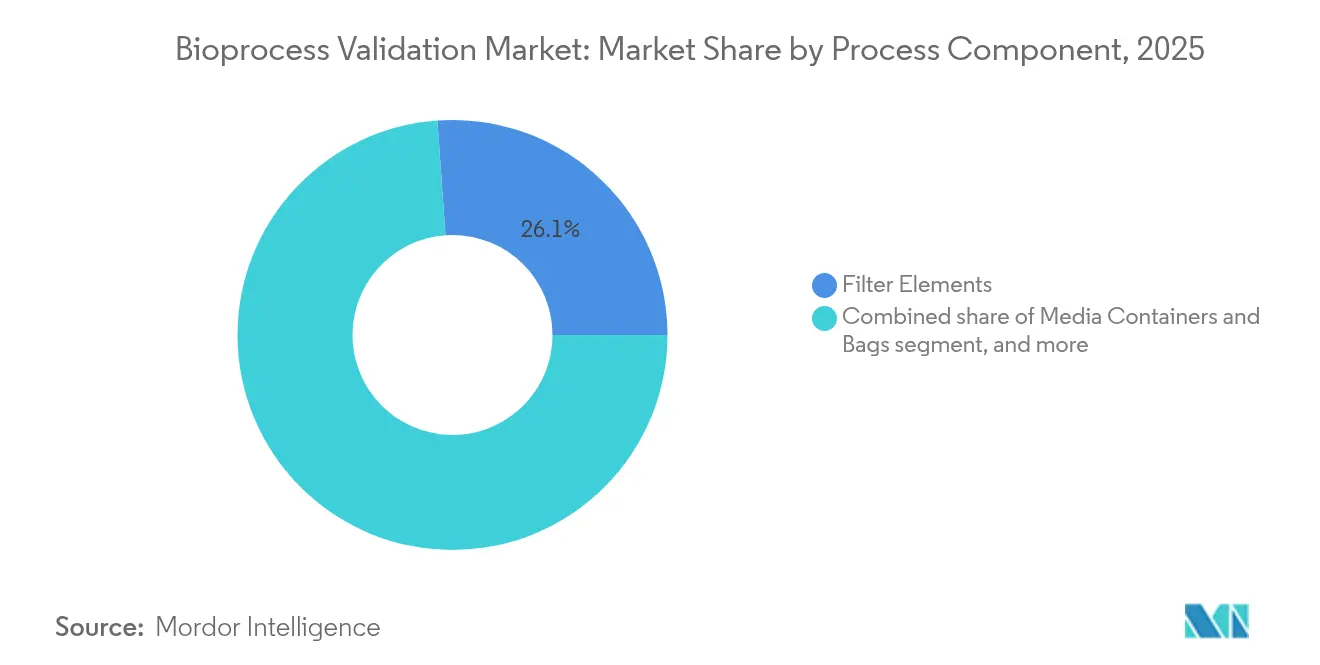

- By process component, filter elements accounted for 26.12% share of the bioprocess validation market size in 2025; bioreactors are projected to grow at a 13.98% CAGR between 2026-2031.

- By end user, pharmaceutical and biotechnology companies held 56.82% of the bioprocess validation market share in 2025, whereas CDMOs are advancing at a 16.88% CAGR through 2031.

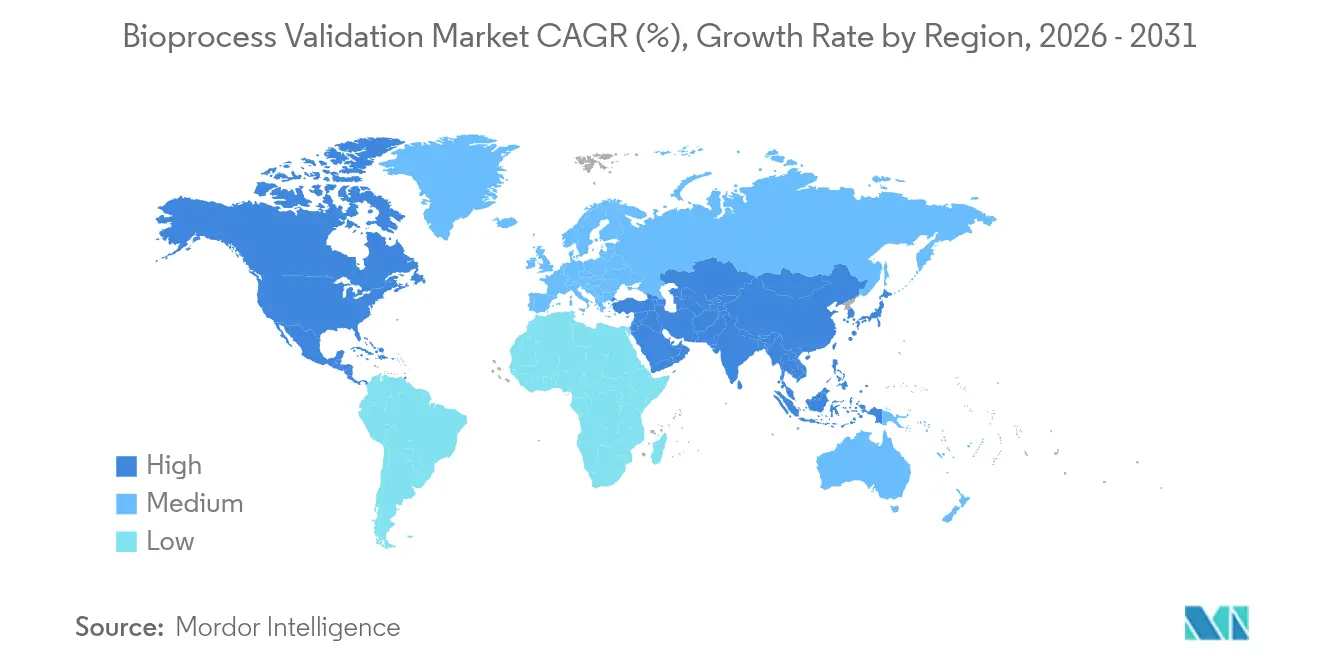

- By geography, North America captured 48.12% of the bioprocess validation market size in 2025; Asia-Pacific is the fastest-growing region at a 15.31% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bioprocess Validation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding global biopharmaceutical production volume | +3.2% | Global, concentrated in North America & EU | Medium term (2-4 years) |

| Stringent regulatory compliance requirements | +2.8% | Global, led by North America, EU, and Asia-Pacific | Short term (≤2 years) |

| Rising outsourcing of validation services to CDMOs | +2.1% | Global, with Asia-Pacific showing the highest growth | Medium term (2-4 years) |

| Adoption of advanced process analytical technology tools | +1.9% | North America & EU core, spill-over to Asia-Pacific | Long term (≥4 years) |

| Transition toward integrated continuous manufacturing lines | +1.6% | North America & EU early adopters, gaining traction in APAC | Long term (≥4 years) |

| Emergence of data-driven lifecycle validation frameworks | +1.3% | Global, strongest uptake in North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Global Biopharmaceutical Production Volume

Manufacturing scale-up fuels the bioprocess validation market as every new line, facility, and process change must be re-qualified. Lonza’s USD 1.2 billion purchase of Roche’s Vacaville plant in October 2024, which adds 330,000 L of bioreactor capacity, typifies large-scale expansions that generate multi-year validation programs. Continuous-manufacturing lines further elevate complexity because sensors, process-analytical-technology (PAT) modules, and real-time release strategies all need bespoke validation. Capacity utilization hovering near 85% in mature hubs tightens project timelines and nudges manufacturers to transfer part of the workload to specialty validation providers, especially for high-throughput extractables and microbiological studies.

Stringent Regulatory Compliance Requirements

The FDA’s Q5A(R2) viral-safety guide and Q2(R2) analytical-procedure guide set deeper expectations for viral-clearance validation and method robustness. In parallel, EMA’s revised Annex 1 compels continuous environmental monitoring in Grade A cleanrooms, adding routine pre-use and post-use filter-integrity tests. Data-integrity rules based on the ALCOA+ framework mean firms must deliver tamper-evident audit trails, pushing electronic batch records from nice-to-have to prerequisite. Harmonized guidelines reduce regional ambiguity yet accelerate compliance deadlines, prompting companies to front-load validation resources or risk marketing-authorization delays.

Rising Outsourcing of Validation Services to CDMOs

Roughly 72.6% of biomanufacturers now outsource some or all validation activities, citing cost control and access to specialized know-how. Eurofins Scientific reported EUR 3.419 billion BioPharma revenue in H1 2024, underpinned by validation demand that it absorbs across a global lab network. CDMOs bundle extractables, leachables, microbiological, and physical testing into turnkey packages, often priced below in-house alternatives once capital depreciation is considered. Cross-border footprints allow CDMOs to shift analytical workloads to lower-cost labs while maintaining quality-system parity, giving clients a double benefit of speed and price.

Adoption of Advanced Process Analytical Technology Tools

PAT instruments add continuous data feeds that compress the time between sampling and corrective action. Near-infrared, mid-infrared, and Raman spectroscopies deliver real-time concentration profiles that once took hours of off-line assays. Digital twins replicate process kinetics in silico, letting validation teams test control limits without touching hardware and thereby cutting re-qualification cycles. Machine-learning models now parse these data streams for deviation signatures, flagging potential losses before product attributes drift. Regulators view such tools favorably, seeing them as enablers of real-time release testing and reduced batch-record review.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and operational costs of validation testing | -1.8% | Global, with higher impact in emerging markets | Short term (≤2 years) |

| Limited availability of skilled validation workforce | -1.4% | Global, particularly acute in North America & EU | Medium term (2-4 years) |

| Complexity of extractables and leachables assessments | -1.2% | Global, most challenging for single-use heavy facilities | Medium term (2-4 years) |

| Data integrity and cybersecurity challenges in digital validation | -1.0% | Global, heightened in highly digitized plants | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Capital and Operational Costs of Validation Testing

Specialized equipment, controlled environments, and data-integrity platforms drive validation costs far above typical quality-control budgets. End-to-end extractables and leachables studies for a single biologic can top USD 500,000 when exhaustive analytical panels are required. Smaller biotechnology firms often lack the capital for dedicated validation suites, pushing them toward outsourcing, but even CDMO prices climb as materials, reference standards, and analytical talent become scarce. The cost burden is heavier in emerging economies where capital allocations must also cover basic facility upgrades to meet global Good Manufacturing Practice (GMP) expectations.

Limited Availability of Skilled Validation Workforce

About 38.5% of companies report difficulty hiring upstream process-development staff, while 37.2% struggle with downstream validation roles. Roles demand fluency in regulatory affairs, analytics, automation, and data security—a blend that traditional academic curricula rarely deliver. Salary premiums in mature hubs lure talent away from smaller centers, widening regional gaps. The move toward Industry 4.0 intensifies the crunch because validation engineers now need coding, statistical-modeling, and cybersecurity fundamentals on top of microbiology and chemistry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Extractables Testing Dominates Complex Validation Landscape

Extractables testing captured 38.07% of the bioprocess validation market in 2025, underlining the acute focus on material-derived impurities that could jeopardize drug safety. Regulatory expectations for single-use systems require full chemical profiling, with the FDA’s April 2024 draft on ANDA submissions laying out tightly scripted protocols. Suppliers and manufacturers jointly map polymer compositions, solvents, and potential leachables, then translate these findings into risk assessments before commercial batches can run. Integrity testing services, positioned to grow at a 15.92% CAGR through 2031, benefit from EMA mandates for pre-use/post-sterilization assessments. The shift toward closed processing gives integrity testing extra weight, because even minute filter compromise invites contamination.

Accelerating demand for rapid methods reshapes microbiological and physicochemical testing. Platforms such as the BACT/ALERT 3D system cut sterility timelines to six days, freeing warehouse space and cash that would otherwise sit in quarantine. Physicochemical assays remain essential for routine release, but automation upgrades deliver higher throughput with fewer analysts, mitigating the labor pinch. Compatibility studies for novel excipients, combination devices, and high-concentration formulations add fresh revenue pockets. Non-growth-based sterility testing—such as SCANRDI, which gives results in under four hours—emerges as a differentiator for producers chasing rapid release in competitive therapeutic classes.

By Process Component: Filter Elements Lead Amid Bioreactor Innovation

Filter elements controlled 26.12% of the bioprocess validation market size in 2025 and remain central to any contamination-control strategy. Regulators demand documented proof of retention, pressure endurance, and integrity across the life cycle of each filter, whether stainless steel or single-use. Annex 1 adds compulsory point-of-use integrity checks, swelling demand for high-accuracy test rigs and trained operators. Viral-clearance claims further multiply analytical runs because filters must prove log-reduction values under worst-case loads and flow rates.

Bioreactors, slated for a 13.98% CAGR, echo the broader movement toward intensified and continuous processing. Perfusion, single-use reactors, and automated feeding loops require validation plans that blend classical parameters (agitation, temperature, pH) with software validations for control logic. Lonza’s Vacaville purchase showcases how legacy stainless infrastructure and next-gen single-use modules coexist in mega-plants, each with unique validation dossiers. Media containers, bags, and mixing systems maintain steady mid-single-digit growth because closed processing pushes fluid handling into disposable formats that still demand chemical compatibility and extractables proof. Transfer systems ride a similar curve, propelled by multi-suite facilities that prefer modular skids and sterile connectors over hard-piped loops.

By End User: CDMOs Drive Outsourcing Transformation

Pharmaceutical and biotechnology firms supplied 56.82% of overall revenue in 2025 as they financed lot-specific tests, method transfers, and facility re-qualifications tied to pipeline progression. Internal quality groups still run core studies, but they increasingly ration their bandwidth to products in late-stage or commercial phases. CDMOs, posting a 16.88% CAGR through 2031, win the rest through bundled validation packages that span extractables, microbiology, viral clearance, and data-migration services. Eurofins’ multiyear track record—closing H1 2024 at EUR 3.419 billion BioPharma revenue—confirms the model’s global pull.

CDMOs also convert scale economies into favorable pricing, absorbing peak workloads during facility upgrades or expedited regulatory filings. Charles River Laboratories faced near-term revenue pressure in 2025 yet preserved its biotherapeutic-testing pipeline by reallocating resources to higher-margin cell and gene therapy programs. Academic centers, non-profit institutes, and government labs hold modest shares but remain critical for early-stage methods and regulatory science. Virtual biotech start-ups, often outsourcing 100% of CMC tasks, represent a consistent inflow of project-based validation business for CDMOs equipped with flexible capacity.

Geography Analysis

North America retained 48.12% of the bioprocess validation market in 2025, powered by the FDA’s leadership on global GMP norms and a dense cluster of commercial biologics producers. U.S. laboratories pioneer rapid-microbiology innovations, such as real-time viable-particle counters used in environmental monitoring, which translate into additional validation work for early adopters. SGS, for instance, achieved a zero-483 outcome in a 2024 FDA audit of its North American biologics center, underscoring the region’s high compliance bar. Canada expands through biologics corridor incentives in Québec and Ontario, whereas Mexico attracts fill-finish projects that channel validation fees into local service providers.

Asia-Pacific is set to outpace all regions at a 15.31% CAGR during 2026-2031. China’s five-year biotech roadmap funds capacity additions alongside domestic regulatory upgrades that increasingly mirror ICH standards. Surveys show 90% of Chinese plant managers aim for full global GMP alignment within ten years. India pushes forward through policy reforms that simplify import permits for reference standards and encourage third-party validation labs. Singapore partners with Charles River Laboratories to offer master cell-banking services that require CGMP-level validation, signalling a regional move toward advanced therapy production.

Europe commands mature demand shaped by the EMA’s Annex 1 and the continent’s strong biosimilar pipeline. Germany anchors the region with clusters in Bavaria and North Rhine-Westphalia running high-capacity stainless and single-use suites. France and Spain add modular facilities built for flexible campaigns, each calling for concurrent validation plans. Brexit generates dual-submission obligations for products sold in both the EU and United Kingdom, effectively doubling some validation documentation. The Middle East & Africa and South America lag in absolute size but gain from rising generic and biosimilar ambitions, notably in Brazil where ANVISA fortifies GMP inspections that elevate local demand for accredited validation labs.

Competitive Landscape

The bioprocess validation market shows moderate fragmentation. Merck KGaA, SGS, Eurofins Scientific, and Thermo Fisher Scientific field global networks that handle volume spikes and specialized assays. Thermo Fisher’s USD 4.1 billion purchase of Solventum’s purification and filtration arm in February 2025 deepens its downstream and validation bench strength, with management projecting USD 1 billion in incremental revenue from the deal. Danaher merged Cytiva and Pall into a USD 7.5 billion bioprocess unit that bundles filtration, chromatography, and single-use hardware, presenting customers with an integrated validation roadmap.

Technology leadership matters more each year. Firms investing in automated sample prep, cloud-native data lakes, and AI-driven trend analytics trim lot release time, making them preferred partners for speed-sensitive launches. Providers wielding six-day sterility tests capture share over labs that still rely on 14-day compendial methods. Smaller regional specialists carve profitable niches in extractables for novel polymers, cell and gene therapy assays, and digital-validation consulting. Market consolidation will likely continue as full-service players pick up niche labs to round out portfolios and secure local regulatory relationships.

Geographical white spaces persist, chiefly in fast-growing Asia-Pacific markets where validation capacity remains below projected manufacturing output. International firms use joint ventures and strategic site openings to close those gaps and lock in early customers. Competition also centers on workforce development; multinationals with in-house academies for validation science stand apart in hiring and retention, enabling them to sustain throughput even as project loads climb.

Bioprocess Validation Industry Leaders

Merck KGaA

Eurofins Scientific

SGS S.A.

Sartorius AG

Pall Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Thermo Fisher Scientific finalized the acquisition of Solventum’s purification and filtration business for USD 4.1 billion, broadening its bioproduction and validation service scope.

- October 2024: Lonza completed the USD 1.2 billion acquisition of Roche’s Vacaville, California biologics site, adding 330,000 L of capacity that requires extensive re-validation.

- October 2024: Lonza announced a new bioconjugation suite in Visp, Switzerland to support antibody-drug conjugate supply from 2027, with validation protocols tailored to highly potent compounds.

- September 2024: Eurofins Scientific acquired Infinity Laboratories, adding eight U.S. sites focused on microbiology, chemistry, and sterilization testing to strengthen its validation offering.

- September 2024: Lonza Walkersville began expanding its endotoxin-assay production facility to meet higher validation testing demand while embedding energy-efficient technologies.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the bioprocess validation market as all documented testing and qualification services or products that confirm a biopharmaceutical production line can repeatedly turn out safe, compliant batches, covering activities from filter integrity checks to viral clearance reports.

Scope exclusion: pilot-scale academic research runs and software-only quality-assurance tools sit outside our frame.

Segmentation Overview

- By Test Type

- Extractables Testing Services

- Microbiological Testing Services

- Physicochemical Testing Services

- Integrity Testing Services

- Compatibility Testing Services

- Other Testing Services

- By Process Component

- Filter Elements

- Media Containers & Bags

- Freezing & Thawing Process Bags

- Mixing Systems

- Bioreactors

- Transfer Systems

- Other Process Components

- By End User

- Pharmaceutical & Biotechnology Companies

- Contract Development & Manufacturing Organizations

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed validation managers at drug makers, CDMOs in North America, Europe, and Asia, plus regulators and single-use equipment suppliers. These calls clarified current pricing windows, batch failure frequencies, and likely regulatory tightening, allowing us to challenge secondary figures and tune model inputs.

Desk Research

We began with public rulebooks and guidance published by bodies such as the US FDA, EMA, and PMDA, which spell out mandatory validation tasks. Statistics from the World Health Organization, BioProcess International articles, and the Biotechnology Innovation Organization helped us size therapy pipelines and plant footprints. Company 10-K filings, investor decks, and customs shipment data enriched our cost and volume assumptions. Where granular revenue splits were needed, analysts tapped D&B Hoovers and Dow Jones Factiva for hard numbers. The sources named illustrate the mix; many more publications, portals, and datasets fed our evidence pool.

The desk sweep let us map regional capacity and typical spend per biologic while flagging gaps only insiders could close.

Market-Sizing & Forecasting

We built a top-down view anchored on 2024 biologic production volumes, regulatory inspection counts, and average validation spend per liter. Results were checked against selective bottom-up roll-ups of major service providers to fine-tune totals. Key variables included the number of commercial biologics, clinical pipeline size, single-use system penetration, share of manufacturing outsourced, and average filter integrity test fees. Forecasts to 2030 rely on multivariate regression that links those drivers to validation outlays, with scenario checks for policy shifts. Data gaps in bottom-up estimates were bridged with midpoint ranges agreed during expert calls.

Data Validation & Update Cycle

Outputs pass a two-stage analyst review, anomaly screens against independent market signals, and senior sign-off. We refresh each model at least once a year and trigger interim updates after material events, ensuring clients always receive a current baseline.

Why Mordor's Bioprocess Validation Baseline Earns Trust

Published estimates often differ because firms pick unique scopes, price corridors, or refresh cadences. By fixing a clear definition, validating every assumption with field interviews, and updating annually, Mordor delivers numbers that decision-makers can lean on.

Key gap drivers include competitors bundling digital analytics or excluding CDMOs, applying flat global ASPs, or using older base years, which inflate or depress totals relative to our 2025 view.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 412.7 M (2025) | Mordor Intelligence | - |

| USD 485.5 M (2024) | Global Consultancy A | Broader scope plus higher assumed test fees |

| USD 360.0 M (2024) | Trade Journal B | Omits CDMOs and most Asia-Pacific spend, uses 2019 currency factors |

Taken together, the comparison shows that Mordor's disciplined definition, mixed-method sizing, and brisk refresh cycle create a balanced, transparent reference point for strategic planning.

Key Questions Answered in the Report

What is the current value of the bioprocess validation market?

The market is valued at USD 472.04 million in 2026 and is forecast to grow to USD 924.66 million by 2031.

Which test type holds the largest share?

Extractables testing dominates with 38.07% of 2025 revenue, driven by single-use system adoption and regulatory focus on patient safety.

Why are CDMOs growing faster than other end users?

Pharmaceutical companies outsource validation to CDMOs for cost savings and specialized expertise, giving CDMOs a 16.88% projected CAGR through 2031.

Which region is expanding the fastest?

Asia-Pacific leads with a 15.31% CAGR thanks to capacity additions in China and India and closer alignment with global GMP standards.

How are new regulations affecting validation workloads?

Updated FDA and EMA guidance adds more stringent viral safety, analytical method, and contamination-control requirements, increasing the volume and complexity of validation studies.

What technologies are transforming validation practices?

Process analytical technology tools such as real-time spectroscopy, digital twins, and machine-learning models enable continuous monitoring and shorten release timelines.

Page last updated on: