Product Design And Development Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

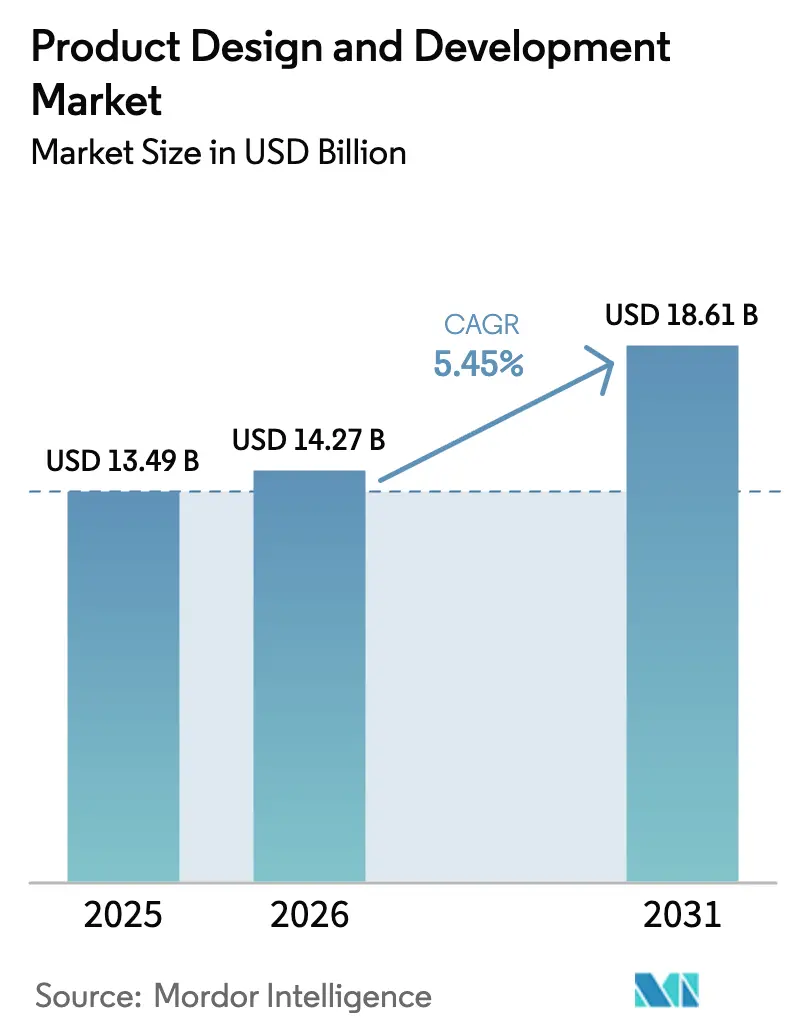

| Market Size (2026) | USD 14.27 Billion |

| Market Size (2031) | USD 18.61 Billion |

| Growth Rate (2026 - 2031) | 5.45% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Product Design And Development Market Analysis by Mordor Intelligence

The Product Design And Development Market size is expected to increase from USD 13.49 billion in 2025 to USD 14.27 billion in 2026 and reach USD 18.61 billion by 2031, growing at a CAGR of 5.45% over 2026-2031.

Momentum stems from original-equipment manufacturers (OEMs) that shift toward asset-light strategies, outsourcing engineering to specialist partners able to absorb ISO 13485 compliance overheads, AI-based simulation licenses, and growing cybersecurity validation costs. Generative design platforms shorten concept-to-prototype cycles, while miniaturized implants and wearable patches require multidisciplinary systems engineering that few in-house teams can fund sustainably. Private-equity owners press mid-tier OEMs to redeploy capital into clinical evidence and market access, reinforcing demand for variable-cost external design talent. Regionally, Asia-Pacific accelerates on sovereign manufacturing incentives, yet North America retains the largest installed client base for high-complexity projects. Competitive intensity is moderate; the top 10 design houses hold 40% of global revenue, leaving ample scope for niche specialists in single-use surgical tools and software-as-a-medical-device applications.

Key Report Takeaways

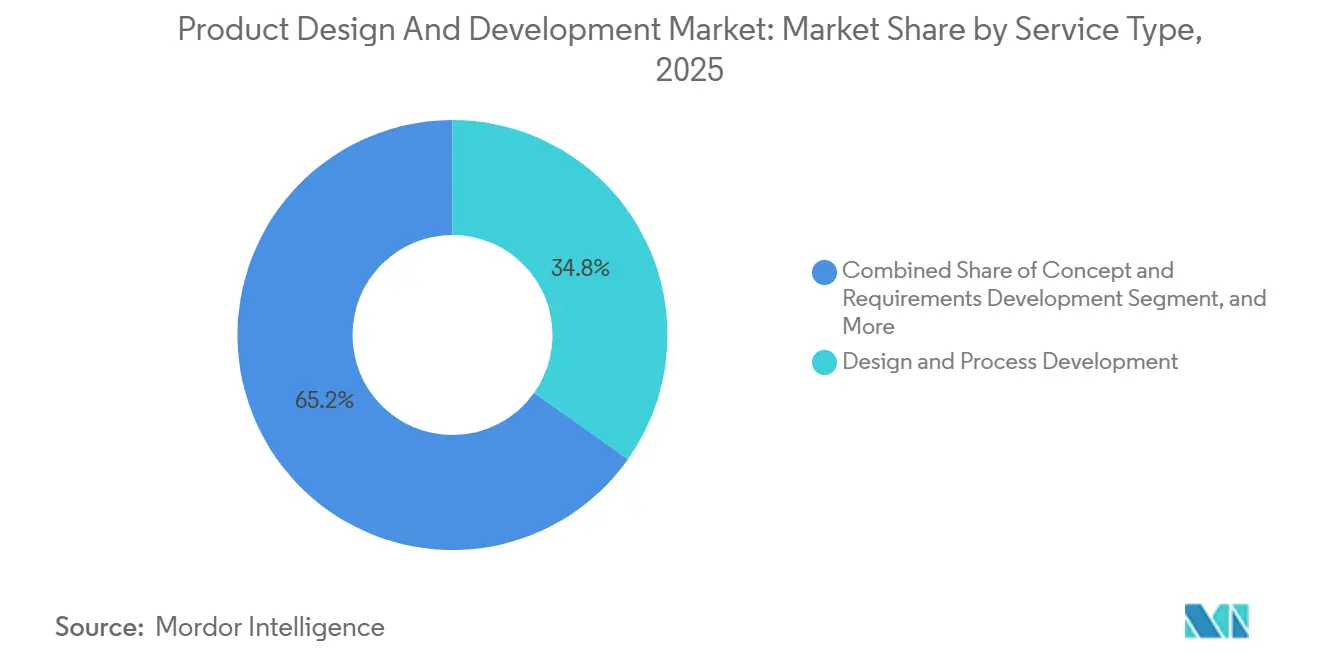

- By service type, design & process development led with 34.81% revenue share in 2025; design & process verification is projected to expand at a 6.96% CAGR to 2031.

- By application, diagnostic equipment accounted for 29.37% of the product design and development market in 2025, while therapeutic equipment is projected to grow at a 7.41% CAGR through 2031.

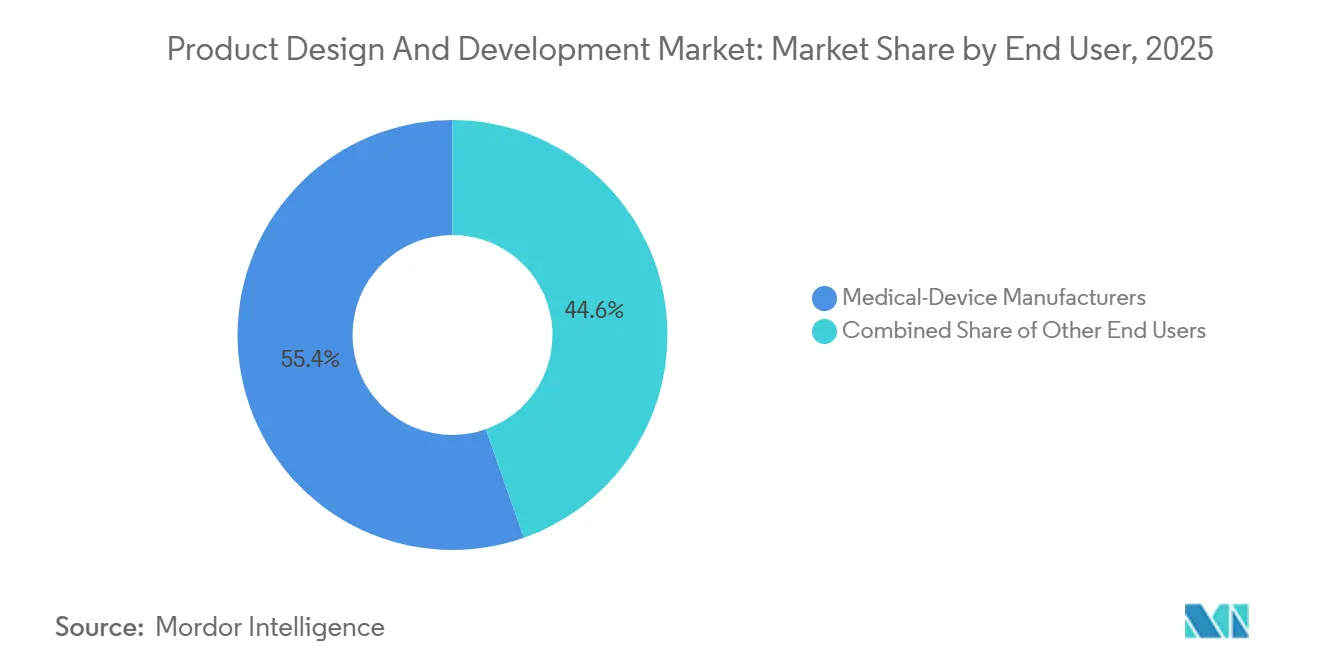

- By end user, medical-device manufacturers held 55.38% of the product design and development market share in 2025, whereas contract research and manufacturing organisations recorded the fastest 6.08% CAGR through 2031.

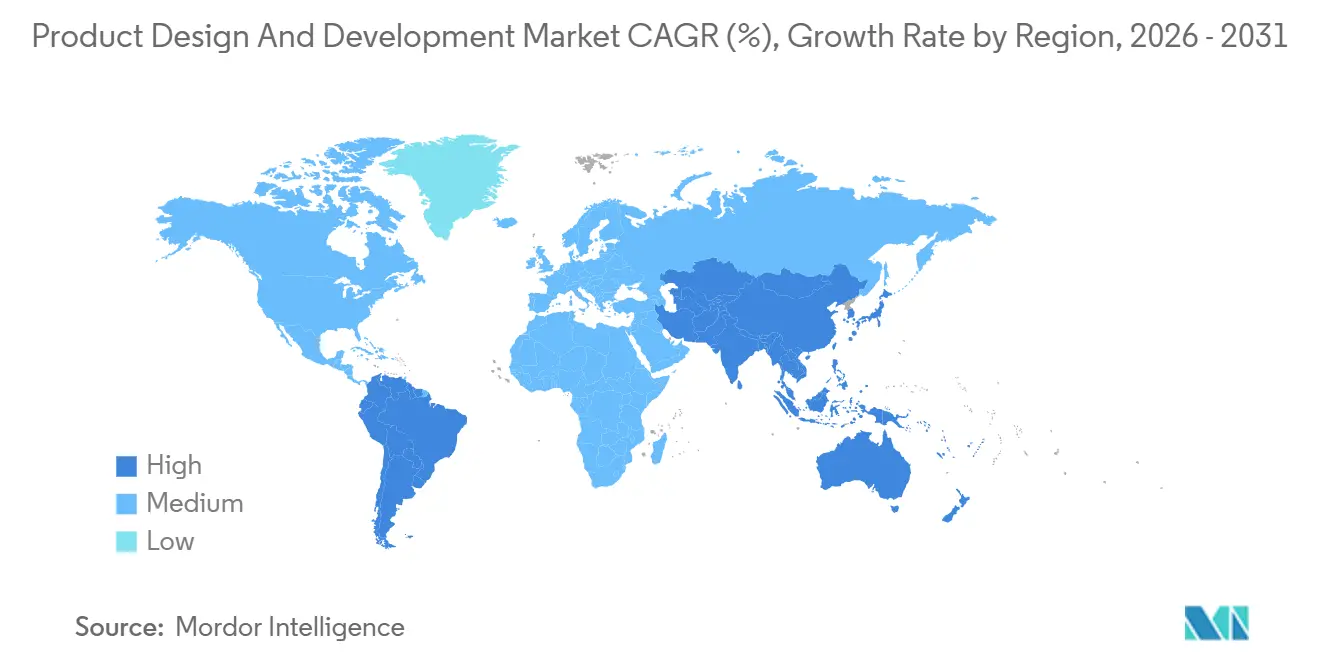

- By geography, North America commanded a 39.24% share in 2025, and the Asia-Pacific region is forecast to register an 8.73% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Product Design And Development Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Enabled Design-Automation Platforms Reduce Concept-To-Prototype Cycle-Time | +1.2% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Miniaturisation of Implantable & Wearable Devices Demands Advanced Systems-Engineering | +0.9% | Global, APAC manufacturing hubs accelerating | Long term (≥ 4 years) |

| Med-Tech VC Funding Surge in Robotics & Cardiovascular Devices | +0.8% | North America & EU core, spill-over to APAC | Short term (≤ 2 years) |

| OEM Pivot to Asset-Light Models Outsourcing Design to Control R&D Burn | +1.3% | Global, particularly North America & EU mid-tier OEMs | Medium term (2-4 years) |

| Regulatory Harmonisation Favours Specialist Design Partners | +0.7% | EU & APAC regulatory convergence zones | Long term (≥ 4 years) |

| Sustainability Mandates Push Eco-Design & Circular-Economy Services | +0.6% | EU leading, North America & APAC following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Enabled Design-Automation Platforms Reduce Concept-to-Prototype Cycle Time

Generative algorithms iterate thousands of geometries in hours, optimizing for strength, biocompatibility, and manufacturability that once required weeks of manual CAD effort.[1]Siemens Healthineers, “Annual Report 2025,” siemens-healthineers.com Hospitals seeking faster 510(k) clearances favor suppliers who slash first-article lead times by up to 35%. Smaller startups are now entering the product design and development market with cloud simulations rather than establishing whole internal engineering departments. The approach also cuts material waste by more than 20% and supports early verification under ISO 14971 risk management. Regulators have yet to codify how AI-generated design rationale must be documented, adding uncertainty to Design History File requirements.

Miniaturization of Implantable & Wearable Devices Demands Advanced Systems Engineering

Continuous glucose monitors, loop recorders, and neurostimulators now package multisensor arrays, antennas, and rechargeable batteries into sub-10 g footprints.[2]Abbott Laboratories, “FreeStyle Libre 3 Product Overview,” abbott.com Precision micro-assembly combines semiconductor techniques with medical-grade encapsulation, prompting design houses to recruit RF engineers, materials scientists, and human factors specialists. Demand is amplified by patch-based biosensors that support remote patient monitoring reimbursement models. ISO 14708 active-implant standards add electromagnetic compatibility and battery safety layers that most OEMs prefer to outsource. As payers reimburse earlier interventions, wearable volumes expand, fortifying a long-term tailwind for the product design and development market.

Med-Tech Venture Capital Funding Surge in Robotics & Cardiovascular Devices

Cardio-robotic startups attracted USD 8.2 billion in 2025, a 28% annual increase that fuels prototype, verification, and first-in-human programs. Modular robotic arms and haptic feedback systems require deep mechatronics, sterile-interface materials, and accelerated fatigue testing—all core competencies of specialist design partners. Cardiovascular innovators focus on transcatheter valves and bioresorbable stents, demanding iterative finite-element analysis that pushes projects to external labs. Design houses often accept equity stakes, aligning incentives yet introducing revenue volatility that sophisticated firms offset by portfolio diversification across therapeutic franchises.

OEM Pivot to Asset-Light Models Outsourcing Design to Control R&D Burn

Private-equity-owned OEMs reduce fixed engineering headcount, shifting USD 42 million toward external partners in 2025 alone.[3]Stryker Corporation, “Form 10-K 2025,” stryker.com Variable project fees protect EBITDA during regulatory delays and allow capital redeployment into commercialization. Multi-year master-service agreements guarantee minimum volumes for design firms, improving revenue visibility. The trend is particularly strong in single-use surgical instruments and consumables, which have three-to-five-year refresh cycles, generating recurring redesign work that stabilizes earnings and strengthens supplier relationships across the product design and development market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Cybersecurity Liability Drives Reluctance to Share Design IP | -0.8% | Global, acute in North America & EU | Short term (≤ 2 years) |

| Talent Deficit in ISO 13485 Systems-Engineers Inflates Project Cost | -0.6% | Global, most severe in North America & EU | Medium term (2-4 years) |

| Fragmented Data Interoperability Standards Slow Software-Heavy Device Programmes | -0.5% | Global, particularly impacting digital health segments | Medium term (2-4 years) |

| Inflationary Metals & Electronics Pricing Erodes Design-To-Value Gains | -0.7% | Global, with acute pressure in APAC manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Cybersecurity Liability Drives Reluctance to Share Design IP

Health-sector ransomware attacks increased by 19% year-over-year in 2025, with several incidents attributed to vulnerabilities in third-party firmware. OEMs now require air-gapped development environments and prohibit contractors from retaining code, which adds weeks to each iteration. Liability insurance premiums for design houses have increased by 30–40%, and underwriters now require ISO 27001 certification, as well as annual penetration testing. Compliance costs strain small consultancies and delay collaborations, tempering growth in the product design and development market. Draft FDA guidance mandates a software bill of materials and vulnerability disclosure protocols, heightening documentation overhead for all parties.

Talent Deficit in ISO 13485 Systems Engineers Inflates Project Cost

A 2025 consortium survey found that 62% of design firms ranked skilled labor shortages as their top bottleneck. Median time-to-fill for senior systems engineers exceeds five months, and salaries rose 12% in North America. To compensate, design houses increased hourly rates by 8–10%, inflating client budgets. Offshore centers in India and Eastern Europe offer relief but introduce time-zone friction that can elongate project schedules by up to 20%. Some firms invest in six-month internal academies co-run with notified bodies, delaying billable productivity yet building a sustainable pipeline for the medical device product design and development industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Verification Momentum Outpaces Front-End Development

The service-mix continues to pivot toward verification as regulators intensify scrutiny of usability, software validation, and real-world evidence. Design & process verification is projected to grow at a 6.96% CAGR through 2031. FDA human-factors guidance now mandates formative and summative studies with representative users, adding USD 150,000–USD 300,000 to typical verification budgets. In parallel, the design community embeds AI-driven test automation, lowering per-iteration costs while increasing the number of iterations within fixed timelines. The product design and development market size for verification services is therefore set to expand as software-heavy devices require continuous risk monitoring even after commercial launch.

The design & process verification segment accounted for 34.81% of revenue in 2025, reflecting robust demand for early-stage ideation, feasibility, and initial architecture definition. However, OEMs often postpone large-scale concept programs until financing is secured, introducing revenue lumpiness that design houses offset by engaging in post-launch lifecycle optimization. Jabil, for example, reported that lifecycle services accounted for 18% of its medical device revenue in 2025. Pilot-to-volume manufacturing transfer remains crucial when clients shift production to low-cost regions; process validation under ISO 14644 cleanroom standards commands premium fees. As regulatory expectations intensify, service providers with integrated quality management systems can close verification and transfer loops more efficiently, thereby strengthening their competitive position within the product design and development market.

By Application: Therapeutic Equipment Surges on Robotics and Cardiovascular Innovation

Diagnostic equipment maintained a 29.37% share in 2025, driven by point-of-care analyzers and AI-enhanced imaging systems that compress time-to-diagnosis in outpatient settings. Portable ultrasound devices and handheld analyzers benefit from declining CMOS sensor costs, enabling decentralized diagnostics. Yet the fastest growth is in therapeutic equipment, forecast to expand at a 7.41% CAGR through 2031, driven by surgical robotics, transcatheter valves, and neurostimulators that integrate real-time software and haptic feedback. Robotics programs often involve five-year co-development pipelines, providing high-margin recurring work for design specialists.

Consumables & disposables generate steady revenue because OEMs regularly re-engineer form factors to reduce material intensity and comply with sustainability mandates. Clinical Laboratory Equipment projects focus on high-throughput automation platforms subject to ISO 15189 accreditation, while Surgical Equipment design centers on single-use end effectors that must tolerate repeated sterilization or support cost-effective disposability. Digital & Connected Health Solutions add demand for cybersecurity hardening and interoperable data architectures. As Medicare expanded coverage for remote patient monitoring in 2024, volumes of wearable patches surged, reinforcing growth prospects for the product design and development market size across application lines.

By End User: CMOs Gain Share as Pharma Deepens Device Involvement

Medical-device manufacturers retained 55.38% of 2025 revenue, but growth is tempered as they offload design complexity to focus on commercialization. Contract research & manufacturing organisations (CMOs) are projected to grow at a 6.08% CAGR, buoyed by pharmaceutical firms that lack internal device expertise but seek delivery platforms for biologics and combination products. The FDA guidance now permits a single submission for drug-device hybrids when the primary mode of action is pharmaceutical, thereby reducing redundant testing.

Pharmaceutical firms are increasingly sourcing connected auto-injectors and smart inhalers, thereby elevating demand for ISO 13485-compliant design partners that understand pharmaceutical filling, sterilization, and cold-chain logistics. CMOs offering integrated design-to-fill-finish services therefore expand wallet share within the product design and development market. For device OEMs, design transfer projects surge when production migrates from high-cost geographies to Malaysia, Mexico, or Eastern Europe, necessitating process capability studies and supplier requalification. Digital therapeutics further blur lines between software and hardware, prompting end users across all categories to tap software-as-a-medical-device specialists.

Geography Analysis

North America accounted for 39.24% of 2025 revenue, supported by a dense ecosystem of OEM headquarters, venture funding, and a transparent FDA path that design partners navigate efficiently. Clients prize local design support for high-complexity implants and Class III robotics, leading to average project values 25% above global norms. The product design and development market size in the United States also benefits from Medicare reimbursement that accelerates adoption of remote-monitoring devices and stimulates design refresh projects directed at home use.

Asia-Pacific is projected to grow at 8.73% CAGR through 2031, the highest regional pace. China’s regulator approved 87 innovative Class III devices in 2025, aided by expedited pathways for domestic intellectual property. India’s Production-Linked Incentive scheme offers 5% rebates on incremental sales, prompting multinationals to establish engineering hubs in Bangalore and Hyderabad. South Korea’s fast-track review program for AI-driven diagnostics further boosts regional demand. Design firms with ISO 13485 certificates across multiple APAC sites gain a structural edge as clients seek simultaneous U.S., EU, and China submissions without redundant documentation.

Europe faces growth headwinds from Medical Device Regulation (MDR) and In-Vitro Diagnostic Regulation (IVDR) bottlenecks. Notified-body queues stretched CE-marking lead times to 24 months in 2025, causing some OEMs to prioritize U.S. or APAC launches. Nevertheless, specialist consultancies with pre-certified quality management systems win share by navigating MDR rigor efficiently. In the Middle East & Africa and South America, hospital capacity expansion drives modest demand for diagnostic and surgical instrumentation. Brazil’s ANVISA alignment with FDA and EU standards simplifies dossier reuse, fostering cross-border design engagements. GCC countries fund medical-device industrial zones that reward local-content design partnerships, broadening the long-term addressable base for the product design and development market.

Competitive Landscape

The competitive arena remains moderately fragmented. Integer Holdings, Jabil, Flex, and Plexus deliver vertically integrated offerings that span concept, prototyping, tooling, and volume manufacturing, attracting OEMs seeking one-stop solutions. Their global factory networks and multi-site ISO 13485 certifications enable synchronized product launches in the United States, Europe, and China, justifying fee premiums of 15–20%. Cambridge Consultants, TTP, and Exponent differentiate themselves through deep domain expertise, such as neurostimulation algorithms, microfluidics, and cybersecurity validation, which commands premium hourly rates that smaller clients accept to mitigate technical risk.

Design houses increasingly deploy digital threads that link CAD, PLM, manufacturing execution, and post-market surveillance databases, enabling closed-loop improvements based on field data. AI-native platforms promise to compress early-stage engineering by up to 40%, potentially disrupting fee structures centered on billable hours. Meanwhile, patent filings in medical robotics increased by 22% in 2025, underscoring an innovation race that fuels recurring demand for high-value design services. Providers that bundle design with post-market analytics lock in multi-year revenue through continuous improvement mandates.

White-space niches persist in software-as-a-medical-device, eco-design for circular economy compliance, and human factors engineering for home-use devices. Barriers to entry escalate in cybersecurity, where ISO 27001 certification and dedicated penetration testing teams become necessary credentials. The top 10 firms capture roughly 40% of revenue, implying moderate concentration that leaves space for regional and therapeutic specialists to thrive within the product design and development market.

Product Design And Development Industry Leaders

Jabil Inc.

Sterling Medical Devices

Flex Ltd.

DeviceLab Inc.

Ximedica (Veranex)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Exponent Inc. expanded its medical-device cybersecurity practice by hiring 12 specialists in penetration testing and threat modeling.

- May 2025: IIT Delhi launched a Healthcare Product Development Programme to bridge academic research and industry commercialization.

- March 2025: Siemens and Accenture created a dedicated business group aimed at scaling software-defined products and factories.

- January 2024: Integer Holdings completed the acquisition of Pulse Technologies for USD 285 million, adding advanced cardiac rhythm management and neuromodulation design capabilities.

Global Product Design And Development Market Report Scope

As per the scope of the report, the process of conceiving, producing, and iterating products that solve users' issues or satisfy specific medical needs is known as product design, and product development refers to the entire process of creating new products and bringing them to market, from conception to deployment. Various companies offer product design and development services to medical device manufacturing companies and other end-users.

The product design and development market is segmented by service type (research, strategy, and concept generation, concept and requirements development, design and process development, design and process verification, and other service types), application (clinical laboratory equipment, therapeutics equipment, diagnostic equipment, surgical equipment, consumables, and others), end-user (medical devices companies, pharmaceutical and biopharmaceutical companies, and other end-users) and geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across the major regions globally. The report offers the value (in USD million) for all the above segments.

| Research, Strategy & Concept Generation |

| Concept & Requirements Development |

| Design & Process Development |

| Design & Process Verification |

| Pilot-to-Volume Manufacturing Transfer |

| Post-Launch Lifecycle Optimisation |

| Diagnostic Equipment |

| Therapeutic Equipment |

| Clinical Laboratory Equipment |

| Surgical Equipment |

| Consumables & Disposables |

| Digital & Connected Health Solutions |

| Medical-Device Manufacturer |

| Pharmaceutical & Biopharmaceutical Firms |

| Contract Research & Manufacturing Organisations |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Research, Strategy & Concept Generation | |

| Concept & Requirements Development | ||

| Design & Process Development | ||

| Design & Process Verification | ||

| Pilot-to-Volume Manufacturing Transfer | ||

| Post-Launch Lifecycle Optimisation | ||

| By Application | Diagnostic Equipment | |

| Therapeutic Equipment | ||

| Clinical Laboratory Equipment | ||

| Surgical Equipment | ||

| Consumables & Disposables | ||

| Digital & Connected Health Solutions | ||

| By End User | Medical-Device Manufacturer | |

| Pharmaceutical & Biopharmaceutical Firms | ||

| Contract Research & Manufacturing Organisations | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the product design and development market?

The market is valued at USD 14.27 billion in 2026 and is projected to reach USD 18.61 billion by 2031.

Which service category is expanding the fastest?

Design & Process Verification is the fastest-growing service, advancing at a 6.96% CAGR through 2031.

Which application area offers the highest growth potential?

Therapeutic Equipment, particularly surgical robotics and cardiovascular devices, is forecast to grow at 7.41% CAGR.

Why are CMOs gaining traction among pharmaceutical companies?

Pharma firms increasingly require integrated device expertise for combination products and therefore partner with CMOs that provide end-to-end design-to-fill-finish solutions.

Which region will grow most rapidly through 2031?

Asia-Pacific is projected to expand at an 8.73% CAGR, driven by manufacturing incentives and streamlined regulatory pathways.

Page last updated on: