High-throughput Screening Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

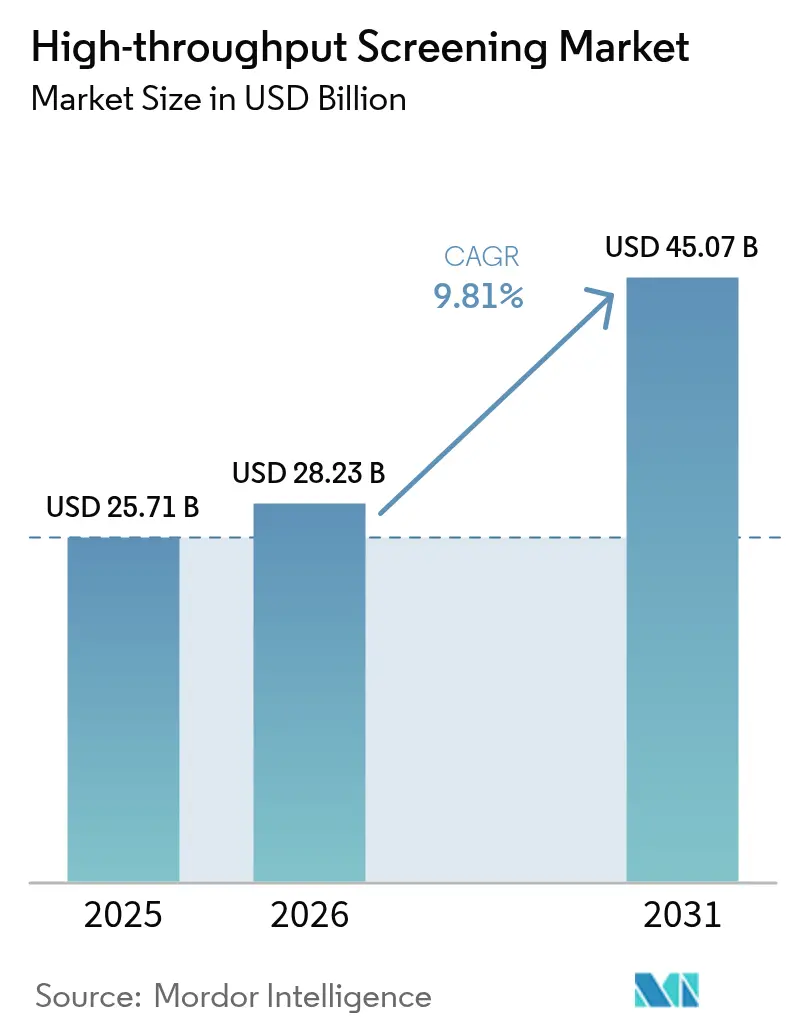

| Market Size (2026) | USD 28.23 Billion |

| Market Size (2031) | USD 45.07 Billion |

| Growth Rate (2026 - 2031) | 9.81% CAGR |

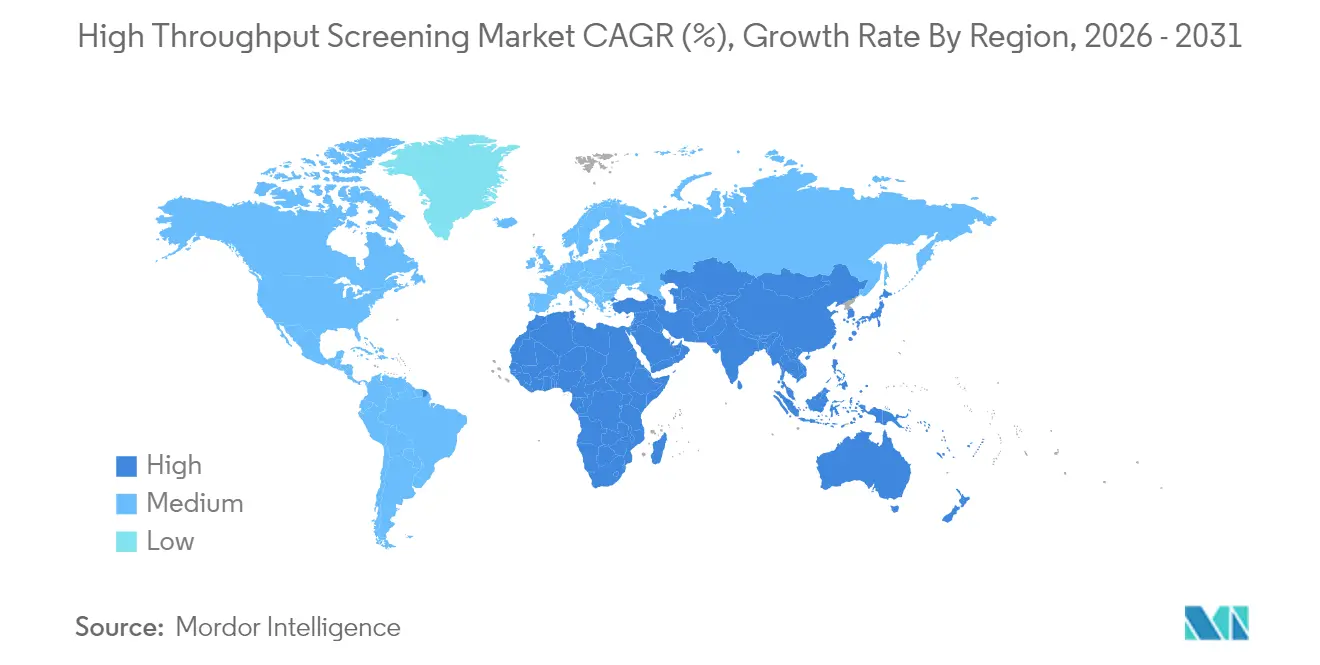

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High-throughput Screening Market Analysis by Mordor Intelligence

High-throughput Screening market size in 2026 is estimated at USD 28.23 billion, growing from 2025 value of USD 25.71 billion with 2031 projections showing USD 45.07 billion, growing at 9.81% CAGR over 2026-2031.

This expansion is anchored in widespread adoption of AI-enabled automation that compresses drug-discovery timelines and trims per-assay costs by 40%. Growing demand for physiologically relevant 3-D assays, rising R&D budgets focused on precision medicine, and strategic outsourcing to contract development and manufacturing organizations (CDMOs) reinforce the upward trajectory. Intensifying competition among integrated platform providers fosters rapid technology refresh cycles, while venture investment in microfluidic ultra-high-throughput screening (uHTS) platforms fuels product innovation. Regulatory encouragement of non-animal testing and sustainable laboratory practices adds momentum by redirecting capital toward advanced cell-based systems.

Key Report Takeaways

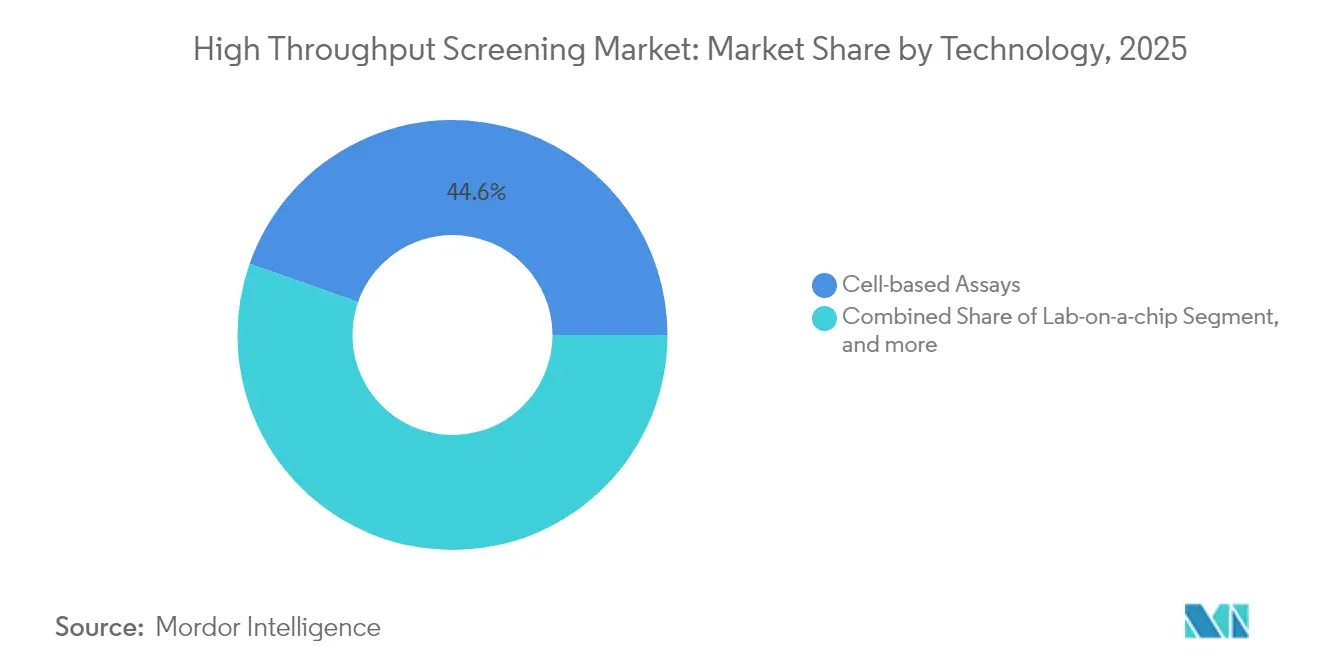

- By technology, cell-based assays led with 44.63% of high throughput screening market share in 2025; lab-on-a-chip and microfluidic platforms are projected to grow at a 10.54% CAGR to 2031.

- By application, primary and secondary screening accounted for 52.98% of the high throughput screening market size in 2025, while toxicology and ADME applications are set to expand at a 13.41% CAGR through 2031.

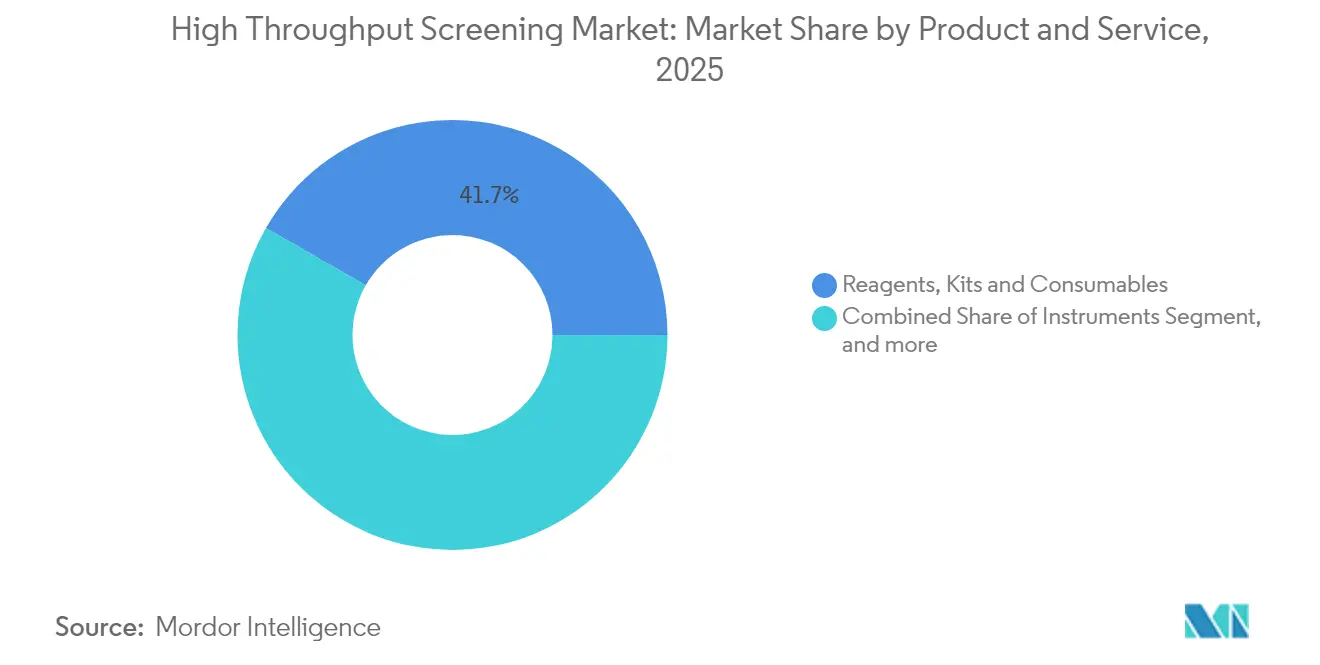

- By product & service, reagents, kits, and consumables commanded 41.72% revenue share in 2025; services are advancing at a 15.02% CAGR through 2031.

- By end-user, pharmaceutical and biotech companies held 48.35% high throughput screening market share in 2025; CDMOs are the fastest growing, registering a 11.78% CAGR to 2031.

- By geography, North America retained 39.22% revenue share in 2025, whereas Asia-Pacific is forecast to progress at a 13.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global High-throughput Screening Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advances in robotic liquid-handling & imaging systems | +2.1% | Global, North America & EU lead adoption | Medium term (2-4 years) |

| Rising pharma/biotech R&D spending & pipeline growth | +1.8% | Global, concentrated in major pharma hubs | Long term (≥ 4 years) |

| Adoption of physiologically relevant cell-based & 3-D assays | +1.5% | North America & EU core, expanding to APAC | Medium term (2-4 years) |

| AI/ML in-silico triage shrinking wet-lab library size | +1.3% | Global, Silicon Valley & Boston clusters lead | Short term (≤ 2 years) |

| Venture-Backed Microfluidic uHTS Platforms | +0.9% | North America & EU, emerging in APAC | Medium term (2-4 years) |

| Rising CDMOs Bundling HTS In Integrated Discovery Contracts | +1.2% | Global, with Asia-Pacific showing fastest adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Advances in Robotic Liquid-Handling & Imaging Systems

Breakthroughs in adaptive robotics are elevating throughput and reproducibility across the high throughput screening market. Computer-vision modules now guide pipetting accuracy in real time, cutting experimental variability by 85% compared with manual workflows.[1]arXiv preprint, “Real-Time Vision-Guided Pipetting,” arxiv.org Integrated AI detection algorithms process more than 80 slides per hour, lifting the ceiling for high-content imaging throughput.[2]Evident Scientific, “High-Content Imaging Productivity,” evidentscientific.com Dual-interface programming lets chemists configure complex workflows without specialist coding, broadening user access. Capital investments exceeding USD 2 million per workcell remain justified as return-on-investment profiles improve with volumes above 100,000 compounds annually. The result is a self-reinforcing cycle of platform upgrades that propels the high throughput screening market toward greater scale, speed, and data quality.

Rising Pharma/Biotech R&D Spending & Pipeline Growth

Expanded R&D budgets dedicated to precision medicine funnel capital into screening platforms that integrate computational biology with automated experimentation. AI-powered discovery has shortened candidate identification from six years to under 18 months, attracting venture flows to companies such as Recursion Pharmaceuticals, which progressed two AI-discovered oncology drugs to clinical trials in early 2025.[3]Recursion Pharmaceuticals, “Advancement of AI-Discovered Oncology Drugs,” recursion.com The multiplier effect between rising budgets and algorithmic efficiency positions early-stage screening as a strategic lever for risk mitigation and timeline compression. Oncology and rare-disease pipelines especially benefit, as rapid compound triage supports combination-therapy exploration and personalized regimens.

Adoption of Physiologically Relevant Cell-Based & 3-D Assays

Commercial 3-D organoid and organ-on-chip systems increasingly replicate human tissue physiology, boosting predictive accuracy and lowering late-stage attrition. Organ-on-chip devices model drug-metabolism pathways that standard 2-D cultures cannot capture, addressing the 90% clinical-trial failure rate linked to inadequate preclinical models. Advanced bioreactors optimize nutrient delivery, while microfluidic chips create physiological microenvironments that assess transport across biological barriers. AI-guided stem-cell manufacturing scales production of induced pluripotent stem cells, opening new windows for disease modeling and regenerative toxicology screens. These developments converge to strengthen the high throughput screening market’s value proposition in translational research.

AI/ML In-Silico Triage Shrinking Wet-Lab Library Size

Virtual screening powered by hypergraph neural networks now predicts drug–target interactions with experimental-level fidelity, shrinking wet-lab libraries by up to 80%. Generative models suggest novel chemotypes that satisfy multi-parameter optimization, widening accessible chemical space while cutting reagent costs. Language models trained on reaction data increasingly outperform human experts in retrosynthetic planning. Computational triage concentrates physical screening on top-ranked hits, improving cost efficiency and throughput, and reinforcing the appeal of integrated AI-HTS platforms to pharma and CDMO partners.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure for fully automated HTS workcells | -1.4% | Global, smaller biotech firms most affected | Medium term (2-4 years) |

| Shortage of skilled assay-automation specialists | -0.8% | North America & EU, emerging pressure in APAC | Long term (≥ 4 years) |

| Data-quality & reproducibility issues across labs | -0.6% | Global, standards vary by region | Short term (≤ 2 years) |

| Sustainability push against single-use 1,536-well plastics | -0.4% | EU spearheads; North America & APAC follow | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure for Fully Automated HTS Workcells

Initial outlays near USD 5 million, including software, validation, and training, create financial friction for smaller firms. Annual maintenance and licensing inflate operating budgets by 15-20%. Although total cost of ownership favors high-volume users, capital intensity delays adoption in cash-constrained organizations and sustains demand for outsourced services. Equipment-leasing and shared-facility models partially offset the barrier, yet the pace of technology obsolescence remains an enduring hurdle to rapid market penetration.

Shortage of Skilled Assay-Automation Specialists

Interdisciplinary expertise in biology, chemistry, robotics, and data science is scarce. Academic programs have lagged, prompting companies to establish internal training pipelines and partner with technical institutes. Talent shortfalls inflate wages and slow deployment timelines in the high throughput screening industry benchmark facilities. Remote diagnostics and AI-assisted troubleshooting extend expert reach, but on-site assay optimization still requires specialized staff, tempering near-term scaling ambitions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Cell-Based Platforms Drive Physiological Relevance

Cell-based assays held 44.63% high throughput screening market share in 2025, reflecting their capability to model complex signaling pathways and predict human efficacy more accurately than biochemical alternatives. The segment benefits from continual advances in fluorescent reporters, 3-D culture scaffolds, and label-free impedance technologies that capture subtle phenotypic shifts. The high throughput screening market size associated with lab-on-a-chip and microfluidic platforms is set to expand rapidly as 10.54% CAGR growth unlocks reagent savings and heightens assay sensitivity. Demand for ultra-high-throughput platforms remains steady among large pharmaceutical libraries, whereas label-free approaches attract safety-toxicology workflows seeking minimal assay interference.

The fusion of high-content imaging with AI-driven analytics magnifies data depth per screen, enabling phenotypic discovery that surfaces unexpected mechanisms of action. Organoid-based screening further differentiates compound responses by tissue microarchitecture, aiding oncology programs that require tumor-microenvironment fidelity. Together, these innovations fortify the cell-based segment’s leading revenue position and catalyze a pipeline of next-generation systems that sustain the high throughput screening market’s long-term expansion.

By Application: Primary Screening Dominance Masks Toxicology Surge

Primary and secondary screening applications contributed 52.98% of the high throughput screening market size in 2025, underscoring their foundational role in hit identification. Automated assay miniaturization and AI triage have accelerated sample throughput, aligning with discovery teams’ need for rapid lead selection. In contrast, toxicology and ADME workflows are poised for 13.41% CAGR through 2031 as global regulators press for non-animal safety data. The shift reflects an economic calculus wherein early safety interrogation minimizes late-stage attrition costs, a prime consideration for venture-backed programs operating on compressed timelines.

In vitro toxicology platforms now incorporate human-derived cell lines, organ-on-chip devices, and predictive AI models, offering 360-degree safety profiling that informs candidate prioritization. CRISPR-enabled target validation accelerates disease-gene linkage studies, while multiplexed biomarker readouts sharpen translational relevance. Collectively, these dynamics diversify revenue streams by balancing legacy high-volume screens with safety-centric assays that draw premium pricing, reinforcing stability across the high throughput screening market.

By Product & Service: Services Growth Signals Industry Transformation

Reagents, kits, and consumables maintained 41.72% revenue share in 2025, yet service-oriented offerings are forecast to outpace all other categories at a 15.02% CAGR. Pharmaceutical sponsors increasingly outsource early discovery to CDMOs that bundle screening, hit-to-lead optimization, and preclinical services in integrated contracts. Flexible engagement models appeal to asset-light strategies, enabling sponsors to align expenditure with milestone achievement and diversify program portfolios.

Instruments continue to drive replacement cycles as vendors embed AI analytics and cloud connectivity, but incremental hardware sales lag the rapid expansion of managed services. Software platforms deliver differentiating value through data harmonization and visualization, facilitating cross-site reproducibility and audit readiness. The synergistic effect of informatics and services elevates switching costs, deepening vendor–client partnerships and anchoring recurring revenue streams that uphold growth momentum in the high throughput screening market.

By End-User: CDMO Acceleration Reshapes Discovery Economics

Pharmaceutical and biotech companies controlled 48.35% high throughput screening market share in 2025, leveraging established infrastructure and compound libraries. However, CDMOs are expanding at 11.78% CAGR as they capitalize on economies of scale and consolidated expertise. Outsourcing mitigates fixed-cost burdens for sponsors and grants smaller firms access to high-capacity platforms without heavy capital commitments. Academic institutes provide foundational research and novel assay concepts yet command limited revenue influence relative to commercial actors.

Asia-Pacific CDMOs gain additional traction by coupling lower operating expenses with proximity to burgeoning biotech clusters. The acquisition of China’s Fengli Group by Barentz typifies strategic moves to bolster regional capabilities and integrate local talent pools. These developments collectively tilt discovery economics toward external providers, cementing CDMOs as pivotal growth engines within the high throughput screening market.

Geography Analysis

North America generated 39.22% revenue in 2025, sustained by mature pharmaceutical ecosystems, high adoption of AI-enabled automation, and robust venture capital participation. Expansive compound libraries and favorable reimbursement landscapes accelerate platform upgrades, anchoring region-wide demand. The high throughput screening market size in the United States benefits from strategic National Institutes of Health (NIH) grants that incentivize translational research partnerships between academia and industry.

Europe maintains steady growth through stringent quality standards and supportive regulatory frameworks that encourage 3-D cell culture adoption. Clusters in Germany, the Netherlands, and the Scandinavian countries champion sustainable laboratory initiatives, spurring investments in reusable microfluidic cartridges that dovetail with continental environmental goals. The regional market also attracts Horizon-Europe funding earmarked for next-generation toxicology.

Asia-Pacific is forecast to advance at a 13.74% CAGR, outpacing Western counterparts as China’s biotech sector experiences renewed capital inflows and supportive policy measures. A 60% biotech stock rally in 2025 outperformed AI sector indices, channeling investor confidence toward drug-discovery infrastructure. Licensing deals between Western majors and Asian biotech firms establish screening hubs that leverage competitive operating costs while adhering to international compliance standards. Rapid adoption of organ-on-chip and microfluidic technologies positions Asia to leapfrog legacy modalities, expanding the high throughput screening market’s geographic diversification.

Emerging markets in South America and the Middle East & Africa exhibit untapped potential. Brazil and the United Arab Emirates spearhead national innovation agendas that fund shared HTS facilities within biotechnology parks. Infrastructure limitations and regulatory variability presently temper adoption rates, yet global CDMO expansion into these regions sets the stage for technology transfer and local capacity building, offering a future lift to worldwide high throughput screening market penetration.

Competitive Landscape

The high throughput screening market demonstrates moderate consolidation, with leading vendors integrating instrumentation, software, and services into unified platforms that heighten switching costs. Top players differentiate through proprietary AI algorithms that dissect multiparametric imaging and biochemical data, furnishing clients with actionable insights. Strategic acquisitions of niche software startups and microfluidic innovators reinforce end-to-end capability, exemplified by Applied Industrial Technologies’ purchase of IRIS Factory Automation to extend material-handling proficiency.

Competitive intensity rises as venture-backed disruptors commercialize organ-on-chip and sustainable screening consumables. These challengers target white-space opportunities in regulatory-compliant plastics alternatives and spatial-biology integrations. Established vendors respond by forming ecosystem partnerships, sharing application program interfaces (APIs) that permit third-party analytics while retaining instrument lock-in.

Platform convergence is a defining strategic vector. Vendors embed cloud LIMS, digital twins, and augmented-reality maintenance support to deliver comprehensive laboratory operating systems. This breadth curtails price competition and secures multi-year service contracts, safeguarding revenue visibility in the high throughput screening market. Sustainability credentials and data-governance assurances increasingly influence procurement decisions, prompting incumbents to publish transparent environmental and cybersecurity benchmarks to preserve market leadership.

High-throughput Screening Industry Leaders

Bio-Rad Laboratories Inc.

PerkinElmer Inc.

Thermo Fisher Scientific Inc.

Merck KGaA

Agilent Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity is emerging where high-throughput screening overlaps with transcriptomics, as vendors extend gene-expression readouts into 1,536-well plate workflows. In June 2026, Alithea Genomics opened early access for MERCURIUS 1536 DRUG-seq, framing transcriptomic profiling as a practical layer for compound response characterization at screening scale. This also creates whitespace for labs and CDMOs that can run sequencing-compatible HTS workflows, such as sample prep automation, barcoding, and downstream informatics, alongside traditional phenotypic and biochemical screens.

A second opportunity is the commercialization of standardized experimental datasets and pipelines that reduce friction between discovery automation and AI model development. July 2026 saw A-Alpha Bio launch Atlas as a data ecosystem built on AlphaSeq binding-affinity measurements, while optical pooled screening efforts reported workflow compression, including an automated genome-wide cell painting screen completed in eight days with sampling above 5 million cells. These signals point to demand for offerings that bundle high-throughput wet-lab generation, reproducible computational analysis, and data products that can be reused across sites. Public-access screening infrastructure adds another pull factor, with June 2026 seeing KRICT launch the DEL CoreBank Platform for DNA-encoded library screening and validation, lowering barriers for academic and mid-sized biotech users and widening downstream demand for instruments, reagents, and specialist services.

Recent Industry Developments

- June 2026: Thermo Fisher Scientific introduced three new Orbitrap mass spectrometry platforms at ASMS, including the Orbitrap Exploris EFOX Mass Detector and the TSQ Altis Plus EFOX positioned for high-throughput quantitation. The launches broaden the toolkit for high-throughput screening-adjacent workflows such as fast ADME and toxicology readouts, reinforcing instrument upgrade cycles tied to higher-throughput, higher-confidence decision making.

- October 2025: Merck KGaA partnered with Promega Corporation to co-develop 3D cell culture (organoid) assays aimed at advancing drug discovery screening. The collaboration supports physiologically relevant models within automated screening stacks and aligns with the market shift from 2D assays toward higher-predictivity cell-based formats.

- July 2024: Bio-Rad Laboratories expanded its Pioneer Antibody Discovery Platform services with SpyLock technology to enable rapid prototyping and high-throughput screening of bispecific antibodies. The expansion strengthens service-led screening options for biologics discovery programs and supports demand for scalable assay and analytics workflows beyond small-molecule libraries.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the high-throughput screening market is defined as the annual revenue generated from tools and services used to run automated, parallel testing of large compound or sample sets for drug discovery and related life-science research.

Scope exclusions: We exclude contract research revenues from full pre-clinical packages where screening is only one workflow among many.

Segmentation Overview

- By Technology

- Ultra-high-throughput Screening (uHTS)

- Cell-based Assays

- Lab-on-a-chip / Microfluidics

- Label-free Technologies

- High-content Screening

- By Application

- Target Identification / Validation

- Primary & Secondary Screening

- Toxicology & ADME

- By Product & Service

- Instruments

- Reagents, Kits & Consumables

- Software & Informatics

- Services

- By End-user

- Pharma & Biotech Firms

- Contract Research / CDMOs

- Academic & Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with a clean list of what gets counted as screening revenue, then mapping demand signals that explain where spending changes year to year. We relied on public and official sources such as the US FDA drug development activity database for activity signals, NIH and other national grant portals for research funding direction, OECD health and R&D statistics for macro context, and the World Bank for currency and broad economic indicators.

To keep the model tied to real buying behavior, we also reviewed public company filings, annual reports, investor presentations, conference abstracts, association websites, and reputable press coverage that discusses lab automation rollouts and screening throughput needs. Where needed, we used paid subscriptions for company financials and intelligence, patent databases to gauge technology intensity, and shipment-level trade data to sanity-check import and export patterns for relevant lab instruments. This list is not exhaustive, and additional public and paid sources were used for collection, validation, and clarification as the model was built.

Primary Interviews and Surveys

Primary work was used to pressure-test desk assumptions around what labs buy together, how pricing shifts across instrument types, and when software and service revenue is bundled versus sold separately. We spoke with a mix of instrument and reagent ecosystem participants, lab automation users, and channel-side experts across major regions so that volume logic, adoption timing, and currency effects could be checked before finalizing totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 13% | APAC: 39% |

| Mid tier: 51% | Functional/Unit leaders: 39% | EMEA: 34% |

| Smaller Players: 14% | Managers: 48% | Americas: 27% |

Market-Sizing & Forecasting

Sizing begins with a top-down build where overall life-science research and drug discovery activity is translated into an addressable screening spend pool, and then split across instruments, reagents and consumables, software, and specialist services using usage intensity and purchasing patterns seen in the field. Totals were also checked with selective bottom-up approximations, such as a sampled roll-up of supplier revenues, and a reasonableness check using installed base, average utilization, and typical replacement cycles.

Inputs used in the model include indicators like pharmaceutical and biotech R&D spend direction, growth in screening library sizes, adoption of automation and liquid-handling systems, assay mix shifts (cell-based versus biochemical), and the pace of drug pipeline progression that changes screening demand. Pricing was handled through simple ASP progression logic, refreshed using interview feedback on discounting, service attach rates, and software subscription behavior. When a bottom-up datapoint was missing for a small cohort or geography, gaps were handled through proxy ratios tied to research spend and lab density, then normalized back to the top-down total.

For forecasting, we applied scenario analysis with a base case supported by expert views on funding cycles, automation penetration, and instrument replacement timing, followed by sensitivity checks for slower R&D budgets or faster adoption of miniaturized assays. The output is a repeatable set of steps that can be traced back to the defined demand pool and a limited set of explainable drivers.

Data Validation & Update Cycle

Validation is done through triangulation across desk signals, interview feedback, and independent market metrics such as R&D budgets, research funding direction, and broad instrument trade movement where relevant. Outliers are flagged when growth appears disconnected from observable demand signals. After that, assumptions are revisited, and if needed, a re-contact is triggered with the relevant respondents.

Before sign-off, the model goes through a multi-step analyst review where calculations, unit logic, and currency conversions are checked, followed by a consistency review across regions and product group behavior. Reports are refreshed annually, and interim updates are made when material events occur that can shift spend patterns. Right before delivery, a final pass is completed so clients receive the latest updated view based on the most recent inputs available.

Mordor Intelligence's High Throughput Screening Market Estimate Compared With Other Published Estimates

Published market sizes for high-throughput screening can differ even when the market name is the same, because the counting boundary is not always aligned across tools, consumables, software, and service revenue. Differences also come from how analysts treat bundled lab automation deals, what they assume for pricing progression, and how frequently the base-year model is refreshed.

The key gap drivers we typically see are whether broader pre-clinical service packages are included, whether adjacent lab automation spending gets pulled into screening, and how aggressively adoption is projected in fast-growing research hubs. Currency timing also matters because this market is global, and the conversion month and inflation treatment can move a USD result even when local demand is unchanged.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 25.71 B (2025) | |

| Industry Research Publisher A | USD 25.55 B (2025) | A slightly tighter 2025 value can happen when software and specialist services are treated mainly as add-ons and when ASP escalation is kept conservative across instrument categories. |

| Industry Research Publisher B | USD 29.60 B (2025) | A higher number is typically linked to folding broader pre-clinical or lab automation spending into screening, and then applying higher attach rates for services and data software across end users. |

The table shows a visible spread around the 2025 value. In Mordor Intelligence's model, the market is limited to HTS-enabling instruments, reagents and consumables, software, and specialist services, while excluding full pre-clinical package revenues where screening is only one step. Once that scope line is kept consistent, the remaining difference usually comes from practical choices like service attach assumptions, ASP progression, and how quickly adoption is ramped in the forecast.

Key Questions Answered in the Report

What is the current value of the high throughput screening market?

The market is valued at USD 28.23 billion in 2026 and is forecast to reach USD 45.07 billion by 2031, growing at a 9.81% CAGR.

Which technology segment dominates the high throughput screening market?

Cell-based assays lead with 44.63% market share in 2025 because of their superior ability to mimic human biology.

Why are CDMOs growing faster than pharmaceutical companies in high throughput screening?

CDMOs grow at a 11.78% CAGR by offering integrated discovery services that let sponsors avoid heavy capital investment and accelerate timelines.

Which region is expected to grow the fastest?

Asia-Pacific is projected to expand at a 13.74% CAGR to 2031, propelled by strong biotech investment and favorable regulatory support.

What is driving adoption of microfluidic and lab-on-a-chip platforms?

These platforms provide physiologically relevant microenvironments, reduce reagent costs, and support sustainable laboratory practices, driving a 10.54% CAGR.

How are AI tools changing high throughput screening?

AI enables in-silico triage that cuts wet-lab library size by up to 80%, improves hit rates, and shortens drug-discovery timelines to under 18 months.

Page last updated on: