Global Continuous Bioprocessing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

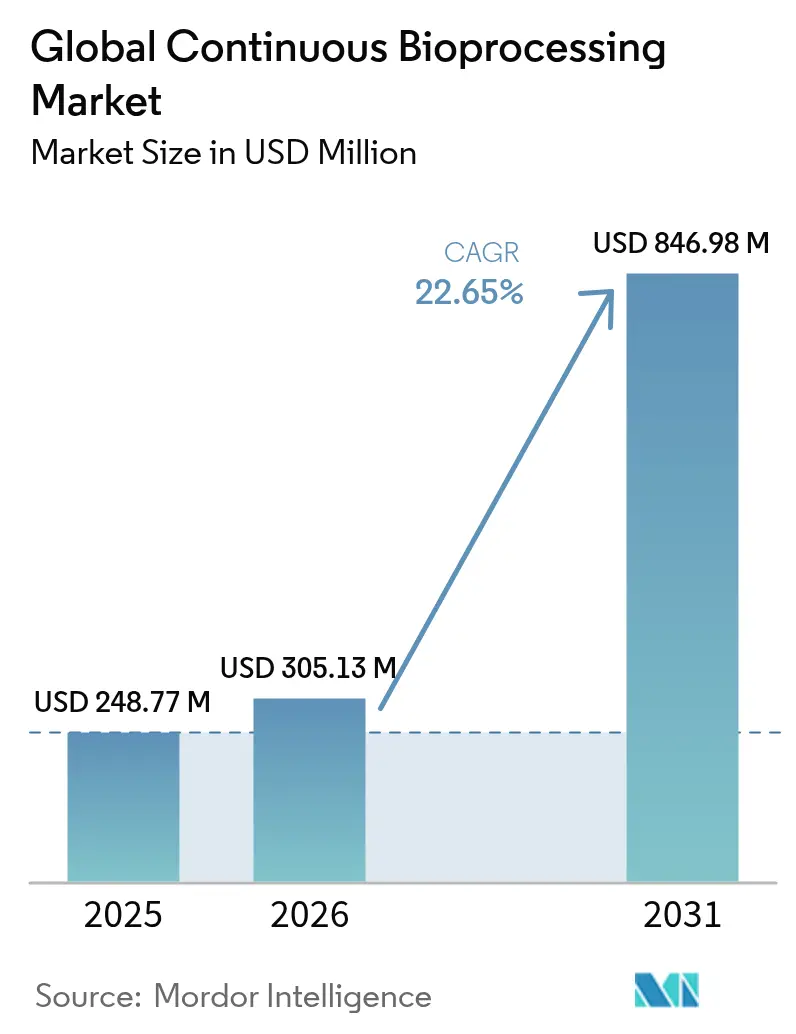

| Market Size (2026) | USD 305.13 Million |

| Market Size (2031) | USD 846.98 Million |

| Growth Rate (2026 - 2031) | 22.65% CAGR |

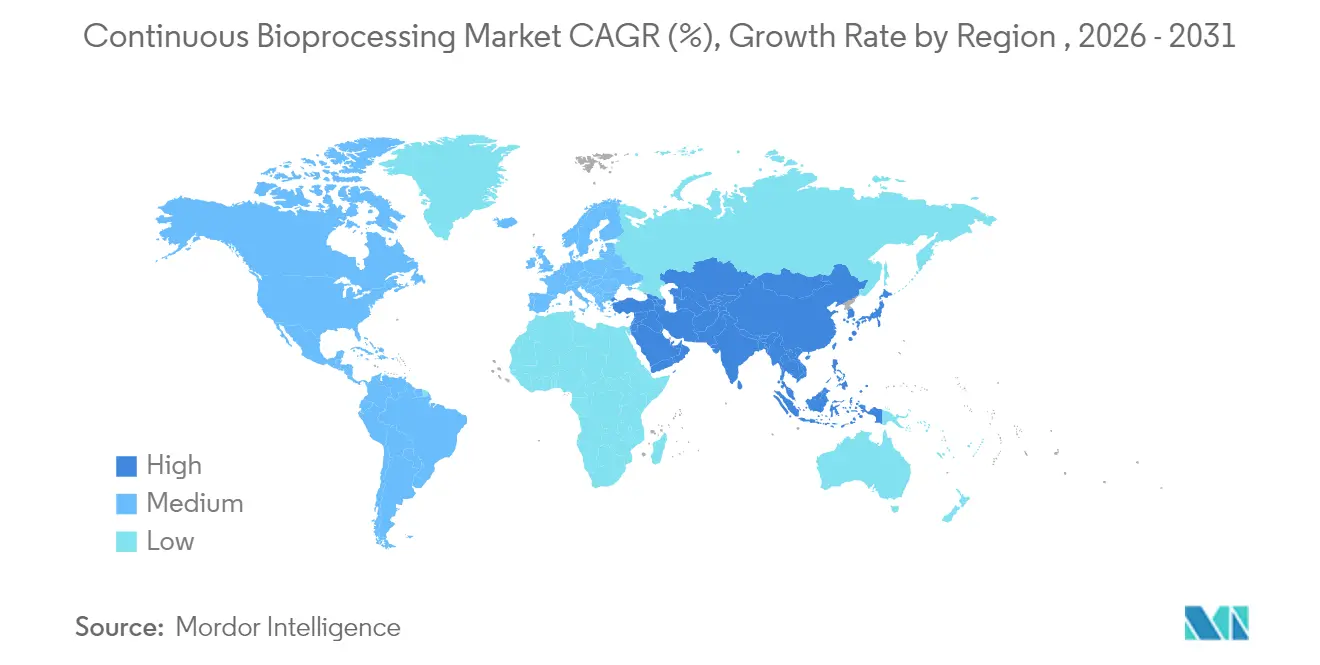

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Continuous Bioprocessing Market Analysis by Mordor Intelligence

continuous bioprocessing market size in 2026 is estimated at USD 305.13 million, growing from 2025 value of USD 248.77 million with 2031 projections showing USD 846.98 million, growing at 22.65% CAGR over 2026-2031. Rapid transition from batch to integrated continuous platforms underpins this growth, as drug makers pursue shorter production cycles, higher volumetric productivity and smaller facility footprints to sustain competitiveness. Demand is reinforced by the expanding biologics pipeline, looming patent expirations on blockbuster drugs and the need to deliver cost-effective biosimilars at scale. Vendors are responding with modular, single-use systems that simplify installation and accelerate changeovers, while digital twins and artificial-intelligence-driven analytics enable real-time process control. Regional momentum remains strongest in North America, yet Asia-Pacific’s capital inflows and policy incentives are narrowing the gap, creating a multipolar growth map for the continuous bioprocessing market.

Key Report Takeaways

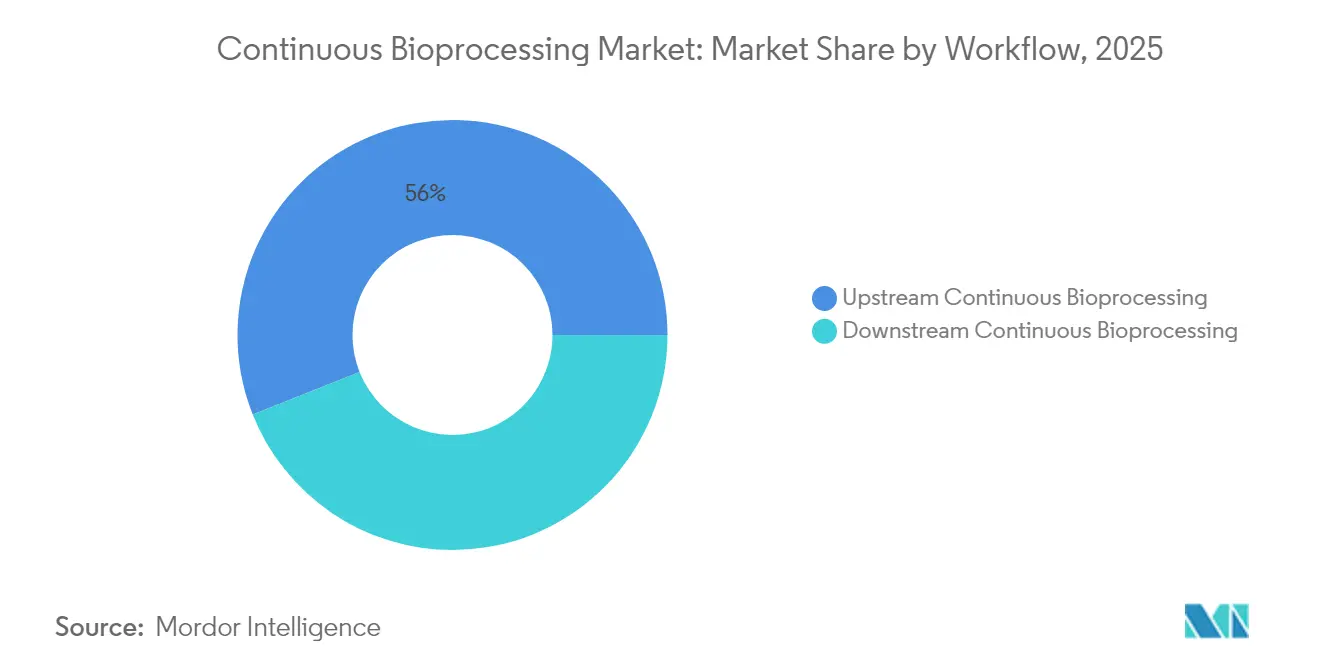

- By workflow, upstream operations led with 56.02% revenue share in 2025; downstream is projected to expand at a 24.01% CAGR through 2031.

- By product, bioreactors accounted for 60.74% of the continuous bioprocessing market size in 2025; tangential-flow filtration is forecast to record a 24.31% CAGR to 2031.

- By application, monoclonal antibodies held 46.08% share of the continuous bioprocessing market size in 2025, while cell & gene therapies are advancing at a 24.45% CAGR to 2031.

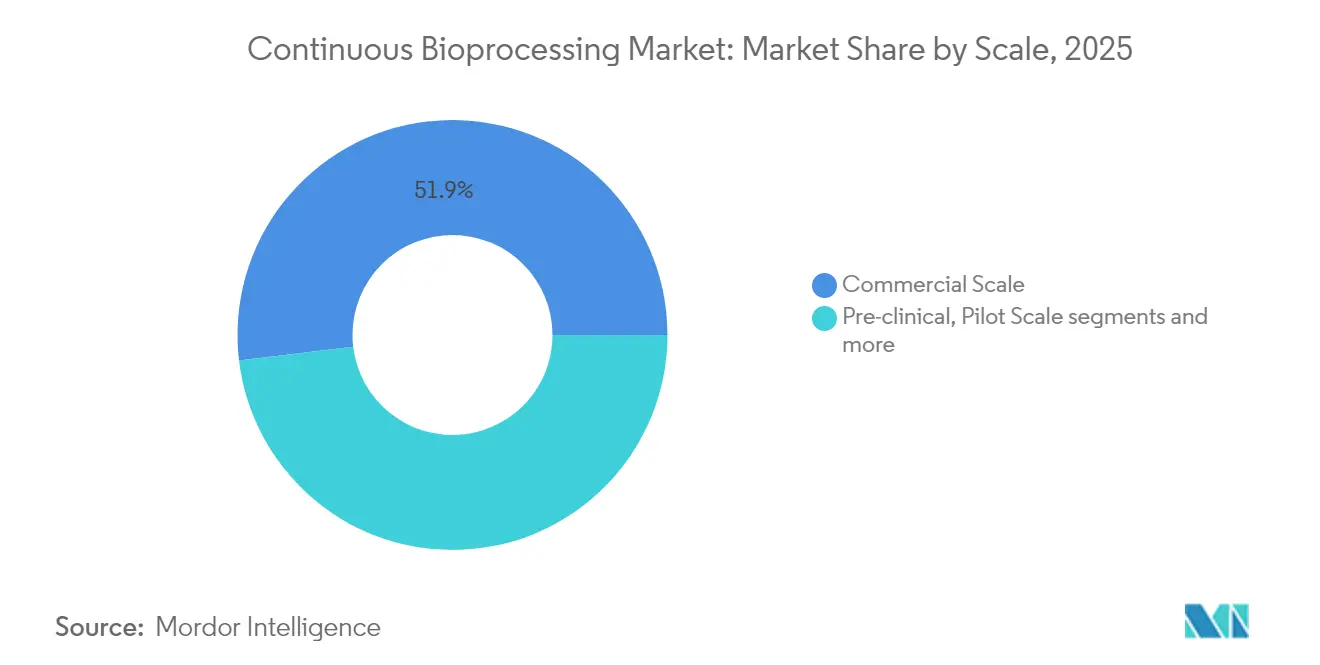

- By scale, commercial operations captured 51.89% of continuous bioprocessing market share in 2025; clinical scale is poised for a 26.72% CAGR through 2031.

- By end user, biotechnology companies commanded 68.93% revenue share in 2025; CDMOs show the highest projected CAGR at 25.38% over 2026-2031.

- By geography, North America led with 42.28% share in 2025; Asia-Pacific is forecast as the fastest-growing region at 24.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Global Continuous Bioprocessing Market*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for biologics & biosimilars | 5.80% | Global, with strongest impact in North America & Europe | Medium term (2-4 years) |

| Need to reduce manufacturing cost & footprint | 5.20% | Global, particularly acute in Asia-Pacific emerging markets | Long term (≥ 4 years) |

| Accelerated product changeover & flexibility | 3.80% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Regulatory encouragement for continuous manufacturing | 3.40% | North America & EU regulatory jurisdictions | Medium term (2-4 years) |

| Integration of PAT with AI-driven real-time release analytics | 2.60% | Global, led by North America & developed APAC markets | Long term (≥ 4 years) |

| Adoption of perfusion-compatible single-use sensors in emerging markets | 2.10% | APAC core, spill-over to MEA and Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Biologics & Biosimilars

More than 1,200 cell and gene therapy trials were active in 2024 versus just 37 US-approved products, underscoring a supply-demand gap that continuous platforms can close by elevating volumetric productivity and enabling rapid line changeovers. Samsung Biologics won contracts worth over USD 3.3 billion in 2024 and scaled to 784,000 L capacity using continuous technology, illustrating how large-volume biologics producers are embracing intensive, steady-state operations. Biosimilar developers likewise pursue continuous bioprocessing to contain costs amid aggressive price competition, especially in Europe. The modality’s steady output and smaller footprint alleviate capacity bottlenecks that have historically delayed market entry for high-demand therapies. Collectively, these trends push the continuous bioprocessing market toward mainstream adoption in both pioneer and fast-follower regions.

Need to Reduce Manufacturing Cost & Footprint

Digital process design and intensified continuous operations can trim biomanufacturing costs by up to 70%, translating to USD 1.25 billion annual savings for a typical blockbuster biologic. Government support mirrors industry priorities: China earmarked USD 4.17 billion for new biomanufacturing capacity in 2024, with policymakers citing the strategic importance of cost-competitive biologics production Continuous bioprocessing eliminates the need for several large-scale stainless-steel units, enabling smaller, modular facilities that reduce capital intensity and operating overhead. Higher titer outputs shorten downstream campaigns, cut buffer volumes and reduce energy demands, further lowering cost-per-gram benchmarks. These structural savings position the continuous bioprocessing market as a preferred route for greenfield plants in both developed and emerging economies.

Accelerated Product Changeover & Flexibility

Personalized medicine demands smaller, more frequent batches, and continuous systems permit changeovers in hours instead of days, thereby maximizing asset utilization bioprocessintl.com. Multiproduct facilities incorporate single-use modules that remove cleaning validation, a regulatory pinch point in batch facilities. The FDA emphasizes robust risk assessments for multiproduct operations, signaling confidence in flexible, continuous architectures fda.gov. Adoption of single-use sensors adapted for perfusion further boosts turnaround efficiency in Asia-Pacific’s new facilities, where speed to market differentiates local innovators. As clinicians request rapid access to clinical-grade material for small patient cohorts, manufacturers increasingly rely on continuous setups to meet timelines without sacrificing quality.

Regulatory Encouragement for Continuous Manufacturing

The FDA’s January 2025 draft cGMP guidance explicitly names continuous manufacturing as a recommended advanced approach, encouraging firms to embed process models in commercial control strategies. Concurrent guidance on artificial-intelligence credibility establishes a risk-based framework for AI models that underpin real-time release analytics, validating digital tools central to continuous bioprocessing [1]Source: U.S. Food and Drug Administration, “FDA Proposes Framework to Advance Credibility of AI Models Used for Drug and Biological Product Submissions,” fda.gov . European authorities are preparing the EU Biotech Act, scheduled for implementation in 2026, to harmonize technology-neutral rules that facilitate continuous production across member states. Regulatory convergence reduces duplication of validation efforts for multinational plants, accelerating global scale-outs. This policy momentum de-risks capital allocation and cements the continuous bioprocessing market’s forward trajectory.

Restraints Impact Analysis of Global Continuous Bioprocessing Market*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX & retrofitting challenges | -4.80% | Global, particularly acute in cost-sensitive emerging markets | Short term (≤ 2 years) |

| Limited proven downstream continuous solutions | -3.20% | Global, with strongest impact in complex biologics manufacturing | Medium term (2-4 years) |

| Regulatory validation complexities for multi-product facilities | -2.70% | Global, with heightened impact in highly regulated markets | Medium term (2-4 years) |

| Scarcity of skilled workforce for hybrid control architectures | -2.10% | Global, most acute in rapidly expanding APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX & Retrofitting Challenges

Converting a legacy batch plant to continuous can cost 50-70% more than greenfield builds because utilities, clean-room layouts and validation protocols must be overhauled. Smaller biotech firms face liquidity constraints, delaying investment despite medium-term paybacks of 3-5 years. Suppliers now offer equipment-as-a-service and lease-to-own agreements to spread cash requirements, but balance-sheet impact still slows uptake in price-sensitive regions. Capital risk is amplified by immature second-hand markets for continuous gear, limiting fallback options if pipelines shift. Consequently, CAPEX intensity remains a notable drag on the continuous bioprocessing market’s near-term penetration outside top-tier sponsors.

Limited Proven Downstream Continuous Solutions

While perfusion bioreactors routinely achieve multi-month steady states, downstream operations such as chromatography and virus filtration lack fully validated, plug-and-play continuous counterparts for every molecule class. Periodic counter-current chromatography is narrowing the gap, yet published data for low-titer enzymes and complex glycoproteins remain sparse [2]Source: Springer, “Design and optimization of a continuous purification process using ion-exchange periodic counter-current chromatography for a low-titer enzyme,” springer.com. Validation frameworks must adapt from lot-based to time-based release logic, requiring regulator-approved statistical models that few firms have yet mastered. Until end-to-end solutions mature, hybrid approaches dominate, tempering the growth pace of the continuous bioprocessing market in highly variable product portfolios.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Global Continuous Bioprocessing Market Segment Analysis

By Workflow:

Upstream Dominance Drives Market EvolutionUpstream continuous bioprocessing held 56.02% of continuous bioprocessing market share in 2025, thanks to high-cell-density perfusion and intensified seed trains that raise titers three- to five-fold over fed-batch alternatives. This leadership translates into larger installed perfusion bioreactor fleets, robust supply chains for single-use consumables and accumulated know-how that lowers technical barriers for new entrants. Downstream still represents a smaller slice of continuous bioprocessing market size but is forecast to grow at 24.01% CAGR to 2031 as chromatography skid vendors standardize multicolumn systems and continuous ultrafiltration deployments expand.

Innovations such as high-density cell banking enable direct inoculation into production vessels, cutting overall production timelines by four to five days and aligning well with tight clinical supply windows bioprocessintl.com. Simultaneously, advanced PAT sensors embedded in upstream lines deliver real-time metabolite data that feed AI-driven controllers for on-the-fly parameter adjustments. Collectively, these refinements reinforce the upstream segment’s pivotal role in guiding end-to-end continuous adoption, cementing its contribution to continuous bioprocessing market momentum across monoclonal antibody, vaccine and emerging cell therapy workflows.

By Product:

Bioreactors Lead Technology IntegrationBioreactors constituted 60.74% of continuous bioprocessing market size in 2025, confirming their status as the central integration node for upstream intensification. The footprint includes alternating-tangential-flow perfusion devices and vertical-wheel impeller designs that support sensitive cells at scale. Tangential-flow filtration modules follow as the fastest-growing product line, advancing at 24.31% CAGR through 2031 as end-users seek closed, steady-state clarification and concentration solutions.

Emerging designs allow 1 L to 5,000 L scalability with consistent shear profiles, simplifying tech transfer from process development to GMP suites pbsbiotech.com. Continuous chromatographic skids now integrate UV, conductivity and pool-volume feedback to ensure column loading consistency, while single-use flow-paths curb cross-contamination risk and eliminate costly cleaning cycles. Collectively, these product innovations fortify supplier ecosystems and expand addressable applications, deepening the installed base that sustains the continuous bioprocessing market.

By Application:

Cell & Gene Therapies Drive InnovationMonoclonal antibodies retained 46.08% revenue share in 2025, reflecting well-established process templates that encourage steady-state, perfusion-based production lines. Yet cell & gene therapies are projected at a 24.45% CAGR, the fastest in the portfolio, as allogeneic CAR-T and viral-vector manufacturers pivot from labor-intensive batch cultures to automated, closed systems. Microfluidic bioreactors shorten expansion cycles, while real-time analytics safeguard critical quality attributes, reinforcing the segment’s pull on continuous innovation.

The continuous bioprocessing market responds with modular, scalable units that fit within hospital-adjacent suites or centralized commercial plants, offering flexible throughput for personalized regimens. Parallel advances in mRNA vaccines, recombinant proteins and viral-like-particle platforms further diversify demand, prompting vendors to tailor continuous hardware and software to molecule-specific kinetics and stability profiles.

By Scale:

Commercial Operations Lead Market MaturityCommercial installations captured 51.89% continuous bioprocessing market share in 2025, exemplified by Samsung Biologics’ 180,000-L Plant 5 that leverages continuous lines to serve global clients. Large-volume facilities benefit from economies of scale, where operating expenditure reductions compound over multi-ton annual outputs. Clinical-scale setups, however, maintain the strongest growth trajectory at 26.72% CAGR, as sponsors embed continuous architectures early to avoid disruptive technology switches upon scale-up.

Digital twins and mechanistic models bridge bench-scale characterization with pilot and commercial suites, de-risking first-in-human timelines and facilitating regulatory discussions. Pre-clinical intensification laboratories use identical single-use flow-paths as commercial systems, ensuring data integrity and comparability. Consequently, the scale spectrum forms a seamless continuum that elevates confidence in continuous workflows and undergirds the continuous bioprocessing market’s expansion into new therapeutic modalities.

By End User:

Biotechnology Companies Drive AdoptionBiotechnology firms accounted for 68.93% of 2025 revenue, reflecting their innovation focus and agility in adopting novel manufacturing paradigms ahead of larger incumbents. CDMOs, while presently smaller, are growing at 25.38% CAGR because sponsors outsource to partners that can offer turnkey, continuous capacity without investing in brick-and-mortar assets themselves..

Modern CDMOs differentiate through multi-client suites equipped with modular continuous skids that scale rapidly with demand surges. Meanwhile, academic centers advance proof-of-concept studies and develop talent pipelines, mitigating the skilled-labor deficit that once slowed implementation. This collaborative ecosystem accelerates technology diffusion and reinforces diversified growth channels across the continuous bioprocessing market.

Geography Analysis

North America Continuous Bioprocessing Market

North America led with 42.28% revenue share in 2025, underpinned by mature biomanufacturing hubs, supportive regulatory frameworks and a robust venture-capital environment. Fujifilm committed USD 1.2 billion to expand capacity in North Carolina, while Lonza acquired Genentech’s 330,000-L Vacaville plant for USD 1.2 billion, reinforcing the region’s long-term capacity outlook. The cluster’s academic-industry consortia foster rapid scale-up of emerging modalities such as allogeneic CAR-T cells, cementing the region’s leadership in high-complexity therapeutics.

APAC Continuous Bioprocessing Market

Asia-Pacific is the fastest-growing region, forecast at 24.86% CAGR, driven by China’s USD 4.17 billion biomanufacturing stimulus and South Korea’s parallel capacity surge, where Lotte Biologics is building a USD 3.3 billion site pharmamanufacturing.com. Cost-competitive labor, streamlined regulatory reforms and government tax incentives lure multinational sponsors to locate new continuous lines in the region. Local biotech champions likewise adopt continuous workflows to compete on quality and speed with Western peers, pushing supply-chain localization for single-use consumables and advanced sensors.

Europe Continuous Bioprocessing Market

Europe maintains steady expansion as sustainability mandates align with continuous processing advantages. Adoption accelerates further once the EU Biotech Act takes effect in 2026, harmonizing standards for real-time release and digital records. European vendors lead innovation in multicolumn chromatography, closing the downstream gap and positioning the bloc as a competence hub for continuous purification technologies. Collectively, regional dynamics ensure that the continuous bioprocessing market evolves across multiple centers of excellence, reducing systemic risk and fostering healthy competitive tension.

Competitive Landscape

The continuous bioprocessing market is moderately fragmented. Danaher integrated Pall’s filtration portfolio into Cytiva in a USD 7.5 billion transaction, creating a vertically aligned giant spanning cell-culture media to chromatography . Sartorius complements its bioreactors with PAT software, while Thermo Fisher pairs hardware with analytical testing services, signaling a race to deliver end-to-end ecosystems. Samsung Biologics combines CDMO services with proprietary continuous platforms, translating operational expertise into market-ready capacity for global clients.

Specialists exploit white-space opportunities in downstream integration and AI-enabled control. Repligen’s alternating-tangential-flow devices boost perfusion efficiencies, while start-ups refine optical metabolism sensors that retrofit into disposable flow-paths repligen.com. AI vendors supply digital twins for predictive quality assurance, capitalizing on new FDA guidance that clarifies model validation expectations. Joint ventures and partnership models proliferate as incumbents acquire software stacks or minority stakes to bolster portfolios.

Competitive intensity is amplified by client expectations for validation support and regulatory navigation. Vendors increasingly bundle equipment leases with on-site training, data-management platforms and GMP documentation templates. This service-rich approach raises switching costs and cultivates long-term relationships that stabilize revenue streams. At the same time, the moderate fragmentation leaves room for nimble entrants to capture niche segments, particularly in continuous viral-vector purification and AI-driven downstream scheduling, sustaining innovation across the continuous bioprocessing market.

Global Continuous Bioprocessing Industry Leaders

3M

Thermo Fisher Scientific

Merck KGaA

Sartorius AG

Eppendorf SE

- *Disclaimer: Major Players sorted in no particular order

Global Continuous Bioprocessing Market Companies Covered in this Report

- Sartorius

- Thermo Fisher Scientific

- Danaher Corporation (Cytiva & Pall)

- Merck KGaA (MilliporeSigma)

- 3M

- Repligen

- Eppendorf

- Getinge AB (Applikon)

- ABEC

- Novasep Holding SAS

- Entegris Inc.

- Asahi Kasei

- Meissner Filtration Products

- PBS Biotech Inc.

- Lonza Group

- AGC Biologics

- Samsung Group

- Wuxi Biologics

- ThermoGenesis Holdings Inc.

- Kuhner Shaker AG

Recent Industry Developments in Global Continuous Bioprocessing Market

- Jan 2025: FDA released final guidance on artificial-intelligence applications in drug development, establishing a risk-based framework for model credibility that supports real-time release analytics in continuous bioprocessing.

- October 2024: Lonza completed its USD 1.2 billion acquisition of Genentech’s Vacaville site, adding 330,000 L capacity for continuous biologics productio.

- October 2024: Samsung Biologics secured a USD 1.24 billion manufacturing contract with an Asian partner, underscoring global demand for large-volume continuous capacity.

Global Continuous Bioprocessing Market Report Scope and Research Methodology

Market Definition and Coverage

According to Mordor Intelligence, we define the continuous bioprocessing market as the global revenue earned from equipment, single-use assemblies, and enabling software that operate in truly continuous or perfusion-based upstream and downstream steps within biopharmaceutical manufacturing lines. The study captures new sales plus replacement disposables at the original equipment manufacturer selling price.

Scope exclusion: Pilot-scale teaching rigs and hybrid batch lines that cannot sustain uninterrupted flow for a full production run are outside our count.

Segments Covered in This Report

- By Workflow

- Upstream Continuous Bioprocessing

- Downstream Continuous Bioprocessing

- By Product

- Continuous Bioreactors

- Tangential Flow Filtration (TFF) Systems

- Continuous Chromatography Systems

- Consumables & Single-Use Components

- Process Control & Monitoring Software

- By Application

- Monoclonal Antibodies

- Vaccines

- Cell & Gene Therapies

- Recombinant Proteins

- Others (Biosimilars, Blood Factors)

- By Scale

- Pre-clinical & Pilot Scale

- Clinical Scale

- Commercial Scale

- By End User

- Biopharmaceutical & Biotechnology Companies

- Contract Manufacturing & Development Organizations (CMOs/CDMOs)

- Academic & Research Institutes

- By Region

- North America

- United States

- Canada

- Mexico

- Europe

- South America

- Germany

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed bioprocess engineers at contract manufacturers, procurement leads in biotech firms across North America, Europe, and Asia, and regulatory consultants. These discussions validated throughput assumptions, typical selling prices, and regional readiness levels that secondary material alone could not resolve.

Desk Research

Our team first built a fact base from open-access regulators and trade bodies such as the US FDA Biologics License Application files, EMA marketing authorizations, UN Comtrade shipment codes for bioprocess hardware, OECD R&D statistics, and annual capacity tables released by the Biotechnology Innovation Organization. We complemented these with company 10-Ks, investor decks, scientific conference proceedings, and paid access to D&B Hoovers for supplier revenues, Dow Jones Factiva for deal flow, and Questel patent analytics that signal technology adoption curves. The sources listed illustrate the breadth; many additional datasets were mined to cross-check figures and clarify trends.

Market-Sizing & Forecasting

We applied a top-down build. Starting with global biologics output and average titers, we translated volumes into the continuous bioreactor capacity and associated filtration or chromatography stations required. Select bottom-up checks, supplier roll-ups and channel ASP × volume probes, refined totals. Key model variables include installed perfusion reactor count, cycle time reduction factors, monoclonal antibody clinical pipeline size, regional manufacturing expenditure, and regulator guidance releases. A multivariate regression combined with scenario analysis underpins the 2025-2030 outlook.

Data Validation & Update Cycle

Outputs pass multi-layer analyst reviews; anomalies trigger fresh source calls before sign-off. The model refreshes every twelve months, with interim updates if facility expansions, major policy shifts, or supply disruptions materially alter assumptions.

How Mordor Intelligence's Global Continuous Bioprocessing Market Size Compares to Other Published Estimates

Published figures vary because firms differ on what qualifies as continuous operation, the pace of adoption, and whether consumables revenue is folded in.

Our disciplined scope selection, variable transparency, and annual refresh narrow these gaps for decision-makers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 248.77 M (2025) | Mordor Intelligence | - |

| USD 304.52 M (2024) | Regional Consultancy A | Treats all single-use batch hardware as continuous, inflating totals |

| USD 207.60 M (2023) | Global Consultancy B | Omits downstream continuous steps, leading to undercount |

| USD 218 M (2023) | Trade Journal C | Uses linear reactor price erosion and uniform global uptake assumptions |

These comparisons show that when scope, variables, and refresh cadence align with on-the-ground realities, Mordor Intelligence delivers a balanced, traceable baseline that clients can rely on.

Key Questions Answered in the Report

How big is the Global Continuous Bioprocessing Market?

The Global Continuous Bioprocessing Market size is expected to reach USD 305.13 million in 2026 and grow at a CAGR of 22.65% to reach USD 846.98 million by 2031.

What is the current Global Continuous Bioprocessing Market size?

In 2026, the Global Continuous Bioprocessing Market size is expected to reach USD 305.13 million.

Who are the key players in Global Continuous Bioprocessing Market?

3M, Thermo Fisher Scientific, Merck KGaA, Sartorius AG and Eppendorf SE are the major companies operating in the Global Continuous Bioprocessing Market.

Which is the fastest growing region in Global Continuous Bioprocessing Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Global Continuous Bioprocessing Market?

In 2025, the North America accounts for the largest market share in Global Continuous Bioprocessing Market.

What years does this Global Continuous Bioprocessing Market cover, and what was the market size in 2025?

In 2025, the Global Continuous Bioprocessing Market size was estimated at USD 305.13 million. The report covers the Global Continuous Bioprocessing Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Global Continuous Bioprocessing Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: