Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

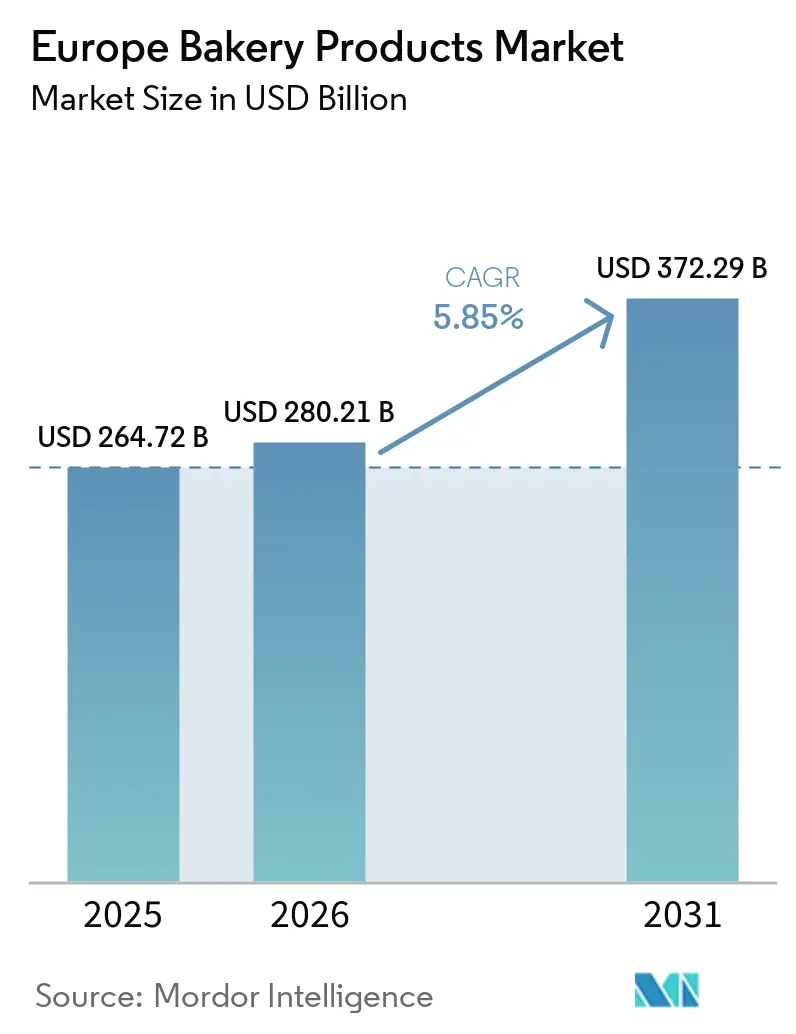

| Base Year Market Size (2025) | USD 264.72 Billion |

| Market Size (2026) | USD 280.21 Billion |

| Market Size (2031) | USD 372.29 Billion |

| Growth Rate (2026 - 2031) | 5.85% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Bakery Products Market Analysis by Mordor Intelligence

The European bakery products market size was valued at USD 264.72 billion in 2025 and estimated to grow from USD 280.21 billion in 2026 to reach USD 372.29 billion by 2031, at a CAGR of 5.85% during the forecast period (2026-2031). This upward trajectory highlights the market's resilience as consumers increasingly gravitate towards healthier, sustainable, and convenient baked goods. For example, data from the Department for Environment, Food and Rural Affairs reveals that in 2022/23, UK consumers favored unfrozen cakes and pastries, averaging 105 grams per person weekly. Buns, scones, and teacakes followed closely at 59 grams[1]Source: Department for Environment, Food and Rural Affairs, "Family food datasets", gov.uk. The market is buoyed by a rising demand for clean-label products, a digital retail transformation, and an increasing preference for frozen items. These trends are expanding the market's reach for both major manufacturers and niche specialists. Furthermore, the market is witnessing a premiumization trend, allowing companies to elevate average prices without dampening demand, even amidst volatile commodity costs. To counter regulatory challenges and maintain both margins and credibility, firms are channeling investments into automation, traceability, and eco-friendly packaging.

Key Report Takeaways

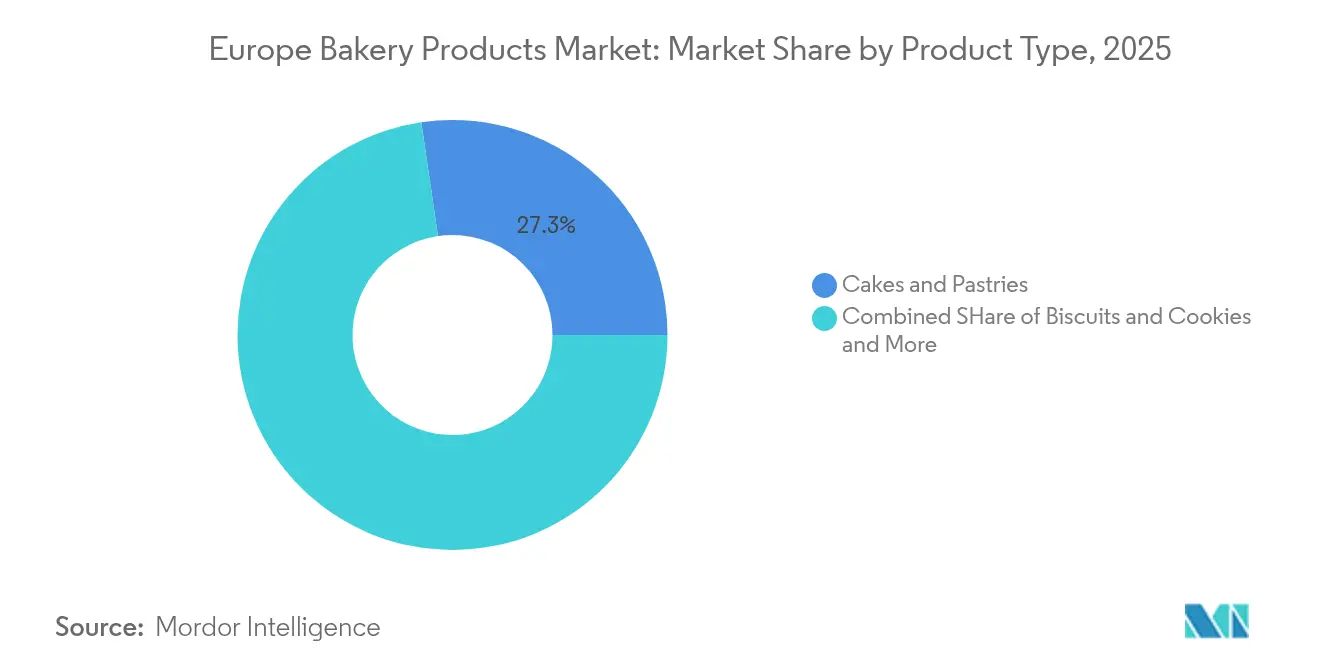

- By product type, cakes and pastries led with 27.32% of the European bakery products market share in 2025, while biscuits and cookies are projected to expand at a 6.03% CAGR through 2031.

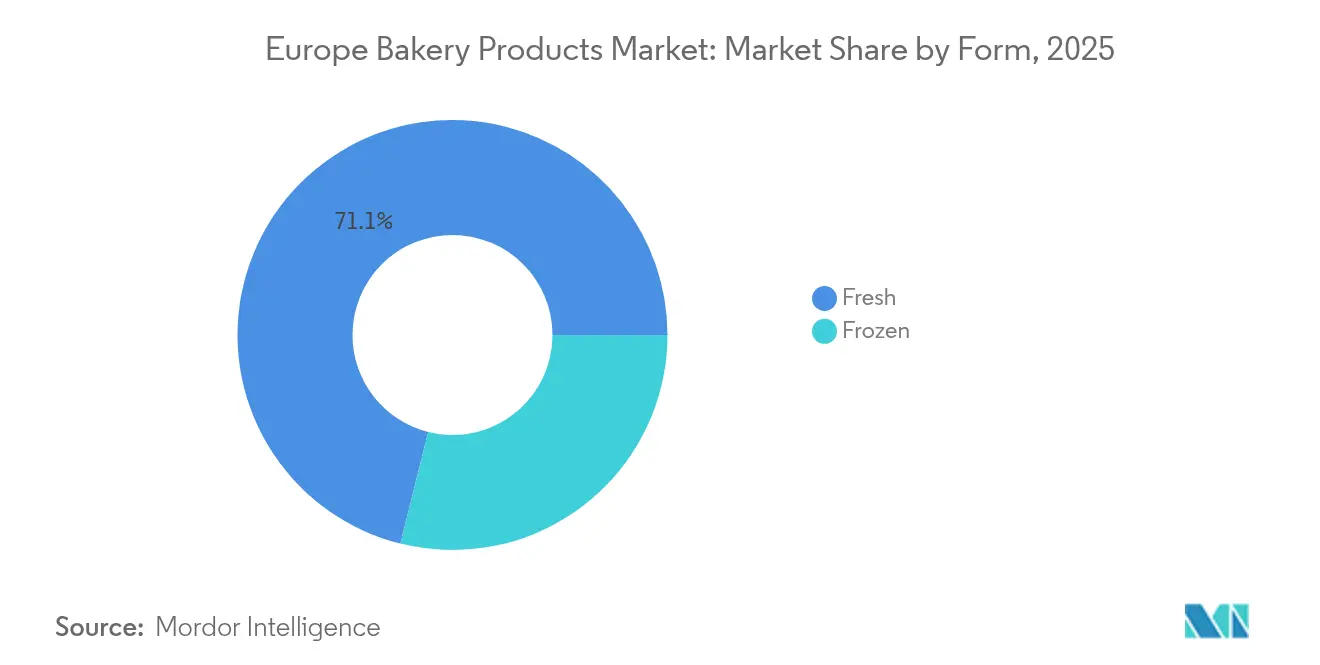

- By form, fresh items accounted for 71.10% share of the European bakery products market size in 2025, and frozen products are advancing at a 6.12% CAGR through 2031.

- By category, conventional goods held a 41.09% share of the European bakery products market size in 2025, and organic/clean-label items are growing at a 6.44% CAGR to 2031.

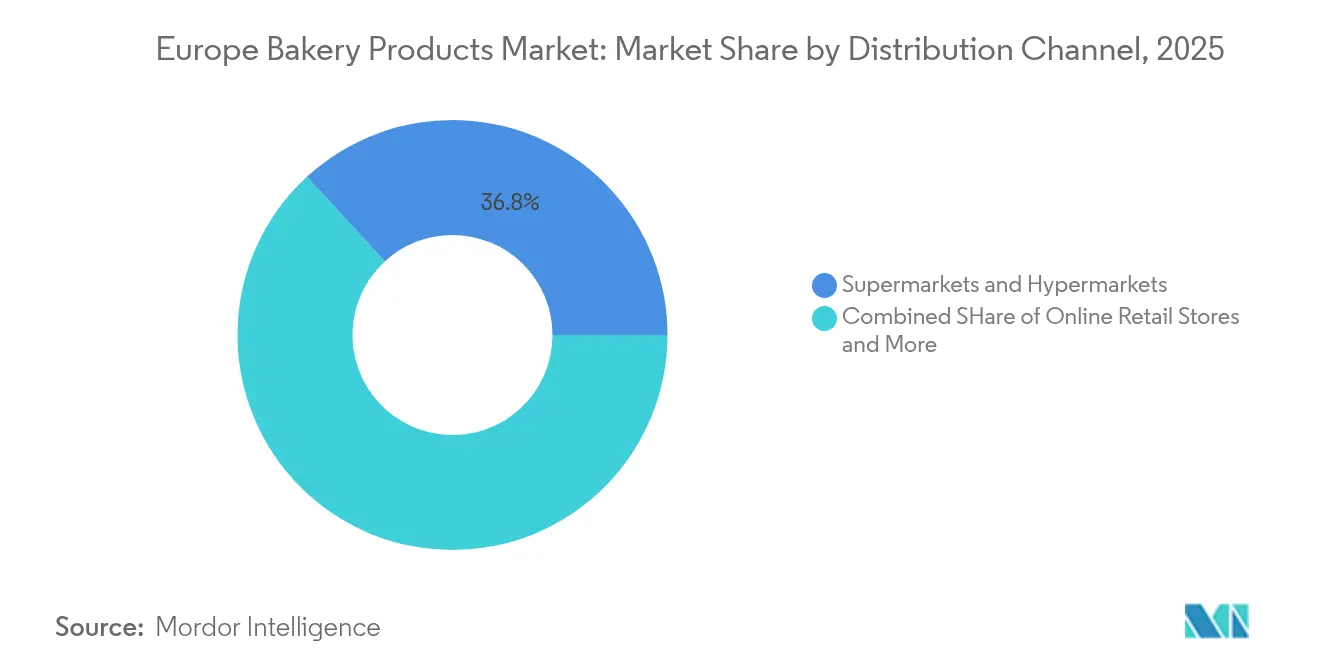

- By distribution channel, supermarkets and hypermarkets captured 36.84% revenue share in 2025, while online retail is the fastest-growing path to market with a 6.88% CAGR to 2031.

- By country, the United Kingdom commanded 29.01% of the European bakery products market share in 2025, Germany records the highest projected CAGR at 6.01% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Bakery Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health and wellness trends | +1.2% | Global, with the strongest influence in Germany, the Netherlands, and Sweden | Medium term (2-4 years) |

| Product innovation and premiumization | +0.9% | Western Europe's core markets, expanding to Eastern Europe | Long term (≥ 4 years) |

| Growing demand for clean label and natural ingredients | +1.1% | Europe-wide, particularly strong in organic-focused markets | Medium term (2-4 years) |

| Sustainability and packaging innovation | +0.7% | Europe-wide compliance-driven, early adoption in Nordic countries | Long term (≥ 4 years) |

| Consumer desire for freshness and shelf-life extension | +0.8% | Global, with emphasis on urban markets across major Europe cities | Short term (≤ 2 years) |

| Growth in out-of-home and on-the-go consumption | +1.0% | Urban centers across the United Kingdom, Germany, and France, with spillover to smaller cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Health and Wellness Trends

European consumers are increasingly favoring functional and nutritionally enhanced bakery products, with protein-enriched and fiber-fortified options gaining traction. In Germany, demand for high-protein snacks and gut-friendly bakery items is rising, while plant-based and flexitarian preferences are reshaping formulations across Europe. According to the German Frozen Food Institute, in 2024, food retailers sold 114,684 tons of frozen cakes, and out-of-home markets sold 91,136 tons[2]Source: German Frozen Food Institute, "Sales statistics 2024", tiefkuehlkost.de. Manufacturers like CSM Ingredients are innovating with technologies such as SlimBake, which reduces fat content by up to 30% without compromising taste or texture. Generation Z is driving demand for personalized nutrition and snack alternatives, while Italian consumers are seeking sustainable bakery goods with health benefits. EFSA's updated guidance on novel foods is enabling the use of innovative ingredients like fermented green lentils as egg replacers, reducing production costs by 30% and meeting clean-label standards.

Product Innovation and Premiumization

European bakers are racing to innovate, pouring resources into automation and unique products to tap into premium markets. Take Grupo Bimbo: in July 2025, the company funneled a whopping USD 2 billion into automation and sustainability across its European branches, underscoring the industry's push for tech-savvy and efficient operations. Sourdough isn't just for traditional loaves anymore; it's set to make waves in various baked goods, thanks to a surge in consumer interest. And as social media and tech fuel flavor experimentation, culinary fusion concepts are on the rise. French bakeries, blending age-old techniques with today's demand for convenience and quality, are leading a renaissance in the artisanal segment, showcasing the evident premiumization trend. On another front, the embrace of Industry 4.0 technologies, from robotics to blockchain traceability, is not only transforming production but also meeting the modern consumer's call for transparency and quality assurance.

Growing Demand for Clean Label and Natural Ingredients

Driven by consumer skepticism towards artificial additives, bakery product formulations are undergoing a fundamental shift. Manufacturers are increasingly adopting clean-label strategies to align with evolving market expectations. Health-conscious consumers are fueling robust growth in the European natural food additives market. There's a rising demand for dual-functional ingredients that cater to both nutritional and preservation needs. Corbion's launch of natural mold inhibition solutions marks a significant leap in extending the shelf life of bakery products, all while upholding a clean-label stance. Regulatory frameworks are bolstering the trend towards organic and "free from" products, favoring natural alternatives over their synthetic counterparts. Notably, EU regulations are tightening the reins on certain chemical preservatives and colorings in food. Highlighting the vigilance in the market, the Bundesamt für Verbraucherschutz und Lebensmittelsicherheit reported 269 food product warnings in Germany as of May 2023[3]Source: Bundesamt für Verbraucherschutz und Lebensmittelsicherheit, "Number of published warnings about food products", bvl.bund.de. Meanwhile, the European Food Safety Authority's refreshed guidance on novel foods is streamlining the approval process for innovative natural ingredients. This includes plant-based and fermented solutions that not only boost nutritional profiles and shelf stability but also adhere to clean-label standards.

Sustainability and Packaging Innovation

EU Regulation 2025/40 on packaging and packaging waste is spurring groundbreaking innovations in sustainable packaging within Europe's bakery sector. The regulation stipulates that all packaging must be recyclable by 2030. It sets specific targets: 30% recycled content in PET food packaging by 2030, escalating to 50% by 2040. In a notable industry response, Mondelez International has teamed up with Saica Group to craft recyclable paper-based packaging for its multipack confectionery and biscuits. Mondelez is also aiming for a 25% cut in virgin plastic packaging materials by 2025. Similarly, the regulation's ban on PFAS in food-contact packaging by August 2026 is prompting the industry to invest heavily in alternative barrier technologies. Addressing Europe's annual bread waste, Polish startup Rebread is converting bread waste into multifunctional ingredients, buoyed by consumer surveys showing a robust appetite for upcycled products. The push for sustainability isn't limited to packaging; companies are overhauling their entire supply chains. They're pouring investments into energy-efficient production technologies and strategies to shrink their carbon footprints, all in pursuit of the EU's ambitious climate neutrality targets set for 2050.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from artisanal and specialty bakeries | -0.8% | Western Europe, particularly France, Germany, and Italy | Medium term (2-4 years) |

| Consumer skepticism and label scrutiny | -0.6% | Europe-wide, strongest in health-conscious markets | Short term (≤ 2 years) |

| Environmental and sustainability demands | -0.9% | Europe-wide regulatory compliance, early impact in Nordic countries | Long term (≥ 4 years) |

| Ingredient costs and supply chain disruptions | -1.2% | Global impact, particularly affecting Eastern European supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Competition from Artisanal and Specialty Bakeries

Across Europe, the rise of artisanal and specialty bakeries is putting intense pressure on industrial bakery producers, especially in premium segments where consumers prioritize authenticity and craftsmanship. In France, artisan bakeries are witnessing a revival, with a resurgence in traditional bakeries after years of decline. This comeback is bolstered by innovations that seamlessly merge age-old techniques with contemporary conveniences. Furthermore, the Real Bread Campaign's triumph over major UK supermarkets, challenging their "freshly baked" claims, underscores a heightened consumer awareness. This awareness leans heavily towards authentic bakery products, distancing from mass-produced options. Artisanal bakeries, with their inherent flexibility, are quick to adapt to local tastes and dietary trends, often rolling out innovative products months ahead of their industrial counterparts. Highlighting the industry's sentiment, the German Baker's Confederation, which represents over 9,200 bakeries, underscores the dual focus on skilled craftsmanship and energy-efficient technologies as key competitive advantages over mass-market producers. In response to this evolving landscape, industrial producers are channeling significant investments into product differentiation and premium positioning, all while striving to retain their foothold in value-centric market segments.

Ingredient Costs and Supply Chain Disruptions

In the European bakery goods market, rising ingredient costs and frequent supply-chain disruptions have become major growth impediments. These challenges are squeezing margins, prompting reformulations, delaying product roll-outs, and shifting investments from innovation to resilience. Key staples like wheat, sugar, cocoa, vegetable oils, yeast, and specialty ingredients have seen input prices surge, driven by heightened imports, rising commodity prices, and tighter global markets. Concurrently, sustained volatility in European energy prices has pushed up milling, refrigeration, and baking costs. This dual challenge is compressing manufacturer margins, elevating retail prices, and dampening demand for premium or innovation-led products. For instance, the Agriculture and Horticulture Development Board reported that in 2023/24, UK wheat imports rose to approximately 2.4 million tonnes, up from 1.3 million tonnes the previous year. Additionally, logistics and input bottlenecks, including seasonal crop variability, transport delays, and evolving sustainability and regulatory requirements, are increasing working capital needs. As a result, manufacturers are prioritizing supply-security measures like longer contracts, dual sourcing, and local sourcing strategies. While these measures enhance security, they also inflate short-term unit costs and decelerate the pace of new product development (NPD). In response, industry bodies and coalitions have taken explicit actions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cakes and Pastries Drive Premium Growth

In 2025, cakes and pastries dominate the market with a 27.32% share, underscoring European consumers' penchant for these indulgent treats, whether for daily enjoyment or special occasions. Meanwhile, sweet biscuits in Europe and cookies are on the rise, boasting a projected CAGR of 6.03% through 2031, thanks to their convenience and health-oriented adaptations. Bread, a staple in traditional diets, is grappling with shifting dietary trends and stiff competition from alternative carbs. Urban markets are witnessing a surge in demand for 'morning goods', as busy consumers hunt for nutritious yet portable breakfast options.

Mondelez International's keen interest in the global cakes and pastries arena, highlighted by its acquisition of Chipita Global SA, underscores the segment's robust growth potential, especially in Central and Eastern Europe. Retailers are increasingly adopting in-store bakery models that employ freeze-and-thaw techniques for cakes and pastries, a move that's slashing labor costs and waste while upholding product quality. As Europe's demographics diversify, there's a rising appetite for specialty and ethnic bakery products, with consumers eager for genuine international flavors. Furthermore, the infusion of functional ingredients across product lines is not only setting manufacturers apart but also catering to the health-conscious demand for enhanced nutritional value.

By Form: Fresh Dominates While Frozen Accelerates

In 2025, fresh bakery products dominate the market with a 71.10% share, underscoring consumer preferences for the quality, taste, and texture of freshly baked goods. Meanwhile, the frozen segment, though currently smaller, is on a growth trajectory, boasting a 6.12% CAGR through 2031. This surge is attributed to benefits like supply chain efficiency, extended shelf life, and advanced freezing technologies that uphold product quality. Such growth signals the sector's alignment with modern retail demands and a consumer shift towards convenience without sacrificing taste.

Technological advancements in blast freezing and packaging bolster the frozen segment's growth, ensuring product integrity during storage and distribution. This not only broadens manufacturers' geographic reach but also curtails food waste. European retailers are increasingly turning to frozen bakery solutions, streamlining inventory management and cutting down labor costs tied to in-store baking. While fresh products enjoy premium pricing and steadfast consumer loyalty, especially in artisanal and specialty segments where immediate consumption is key, the market sees a clear segmentation. Fresh goods dominate planned purchases and special occasions, whereas frozen options cater to impulse buys and convenience, highlighting the coexistence of both segments.

By Category: Organic Clean Label Emerges as Growth Engine

In 2025, conventional bakery products command a dominant 41.09% market share, underscoring entrenched consumer habits and price sensitivity across Europe's diverse markets. Yet, the organic/clean label segment is on an impressive trajectory, boasting a 6.44% CAGR through 2031. This surge signals a pivotal shift in consumer focus towards ingredient transparency and health-centric choices. Highlighting this trend, the Federal Ministry of Food and Agriculture (Bundesministerium für Ernährung und Landwirtschaft) reported that by December 2024, Germany had 109,567 products proudly flaunting organic labels. Meanwhile, the protein/functional segment, though currently modest in size, is swiftly adapting to cater to the nutritional and lifestyle aspirations of health-conscious consumers.

As consumers become more discerning, clean label positioning gains prominence. Shoppers now meticulously examine ingredient lists, favoring products devoid of artificial additives, preservatives, and synthetic chemicals. The protein/functional segment is riding the wave of heightened nutritional awareness and active lifestyle trends. Products in this category are increasingly featuring plant-based proteins, enhanced fiber, and other functional ingredients that offer distinct health advantages. Moreover, Europe's inclination towards plant-based diets and holistic health is spurring innovations in bakery formulations, merging indulgence with nutritional benefits. The steadfastness of the conventional segment can be attributed to price-sensitive consumers who prioritize value, especially during economic downturns when discretionary spending tightens.

By Distribution Channel: Online Retail Transforms Market Access

In 2025, supermarkets and hypermarkets command a dominant 36.84% market share, thanks to their vast geographic reach, competitive pricing, and the allure of one-stop shopping for mainstream European consumers. Meanwhile, online retail stores are the rising stars, boasting a robust 6.88% CAGR through 2031. This surge mirrors the broader digital transformation and shifts in consumer shopping habits, a trend notably accelerated by post-pandemic lifestyle changes. Urbanization and a fast-paced lifestyle bolster the growth of convenience stores, while bakeries and specialty shops carve out their niche with artisanal offerings and tailored customer experiences.

In Germany, online food sales are rising, with bakery products leveraging subscription services, direct-to-consumer models, and marketplace platforms. Convenience channels grow with hybrid work trends and demand for quick meals, especially in the UK’s food-to-go segment. Discount retailers and cash-and-carry operations attract price-sensitive consumers with value and bulk options. Manufacturers must adopt channel-specific strategies to optimize assortments, pricing, and promotions while ensuring brand consistency. Digital integration is essential for inventory management, customer engagement, and data-driven decisions in a complex retail landscape.

Geography Analysis

The United Kingdom led the European bakery products market with 29.01% revenue share in 2025, supported by an advanced retail network and high per-capita consumption. Germany shows top growth momentum at a 6.01% CAGR as eco-minded shoppers lean toward plant-based and functional bakery lines. France sustains its artisanal heritage, with renewed consumer interest in region-specific breads bolstering local firms.

Italy’s focus on sustainability sees the majority of buyers evaluating environmental impact when selecting bakery goods, with private labels capturing a prominent volume. Spain benefits from tourism and Mediterranean preferences that favor diverse pastry assortments. Nordic markets, though smaller, set benchmarks for recyclable packaging and carbon-neutral baking. Eastern European countries such as Poland witness rapid modernization, aided by acquisitions like Grupo Bimbo’s Vel Pitar purchase in Romania. Belgium and the Netherlands support cross-border flows thanks to their logistical hubs. Regulators apply common EU rules, yet local tastes keep innovation pipelines busy. Consolidation, illustrated by Valeo Foods’ purchase of Italy’s Dal Colle, underscores the search for scale and brand depth across the European bakery products market.

Competitive Landscape

The European bakery products market is highly competitive and moderately fragmented, with multinational corporations, regional specialists, and artisanal producers competing for market share through strategies like portfolio diversification, innovation, sustainability, and acquisitions. Global leaders such as Grupo Bimbo, Associated British Foods Plc (ABF), and Mondelēz International dominate mainstream retail channels by leveraging their scale and automation while adapting to local preferences. For instance, Grupo Bimbo expanded its presence in Southern Europe by acquiring the Slovenian-based bakery group Don Don in November 2024 and further entered Croatia, Montenegro, and Serbia in 2025 through acquisitions like Your 5 minutes and Lulu Bakery, strengthening its position in the Balkan region.

Mid-tier and niche companies are capitalizing on health and wellness trends by focusing on specific market attributes. Dr. Schär AG/SPA, for example, has prioritized gluten-free and specialized nutrition products, achieving significant growth with an 11% increase in global turnover in 2024. Similarly, Vandemoortele has emphasized strategic acquisitions and sustainability, acquiring the Italian frozen bakery specialist Lizzi s.r.l. in February 2025 and Dolciaria Acquaviva in June 2024, solidifying its position in the Italian market. In September 2025, Vandemoortele secured EUR 100 million in financing to support further expansion and acquisitions, reinforcing its presence in the frozen bakery and plant-based food sectors.

Other players, such as Lantmännen Unibake, are focusing on product innovation to meet consumer demand for healthier options. In May 2024, Lantmännen Unibake Germany launched its "Better Buns," featuring improved nutritional values and a lower CO2 footprint. This emphasis on innovation and sustainability has become a key growth strategy across all segments of the European bakery products market, enabling companies to align with evolving consumer preferences and regulatory requirements.

Europe Bakery Products Industry Leaders

-

Grupo Bimbo, S.A.B. de C.V.

-

Associated British Foods Plc

-

Mondelēz International, Inc.

-

Yıldız Holding

-

Ferrero International SpA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Doughlicious launched its first range of ambient (non-frozen), soft-baked single-serve cookies, produced in their West London factory using British oats. These cookies were launched in four flavors: Double Chocolate Chip, Salted Caramel Cookie, Chocolate Chip, and Banana Good Granola. Additionally, the cookies are vegan, gluten-free, and free from artificial additives, preservatives, flavors, or colors.

- July 2024: McVitie launched its ‘Signature’ range of biscuits, which featured premium ingredients, richer flavors, and elevated textures, aiming at consumers seeking luxury biscuit experiences, according to the company. The range included sophisticated recipes that blend tradition with innovation to meet evolving tastes toward indulgence and premiumization in Europe’s biscuit market.

- April 2024: Wildfarmed launched its regenerative bread range, which emphasized regenerative agriculture practices, focusing on sustainable farming methods that restore soil health and biodiversity. The bread range was asserted to appeal to environmentally conscious consumers looking for bakery products that go beyond organic claims by promoting active ecological restoration.

- July 2023: Dr Schär invested EUR 12m (USD 13.2 million) in biscuit production at its manufacturing facility in Dreihausen, Germany. The company aimed to increase biscuit production, and the deal was intended to see the company add new machines for measuring biscuit cream, which would improve the dosing of the ingredients and reduce waste.

Europe Bakery Products Market Report Scope

Bakery products include baked products such as bread, cookies, rolls, pies, and muffins that are prepared from dough batter.

The European bakery products market can be broadly segmented into three major segments, such as by product type, distribution channel, and geography. Based on product type, the market is classified into cakes and pastries, biscuits, bread, morning goods, and other product types. Based on the distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, speciality stores, online retail stores, and other distribution channels. Also, the study provides an analysis of the bakery products market in the emerging and established markets across the region, including the United Kingdom, Germany, France, Russia, Italy, Spain, and the Rest of Europe.

For each segment, the market sizing and forecasts have been done based on value (in USD million).

By Product Type

| Bread |

| Cakes and Pastries |

| Biscuits and Cookies |

| Morning Goods |

| Other Bakery Products |

By Form

| Fresh |

| Frozen |

By Category

| Conventional |

| Organic/Clean Label |

| Protein/Functional |

By Distribution Channel

| Supermarkets and Hypermarkets |

| Convenience Stores |

| Bakeries/Specialty Stores |

| Online Retail Stores |

| Other Retail Channels |

By Geography

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Russia |

| Sweden |

| Belgium |

| Poland |

| Netherlands |

| Rest of Europe |

| By Product Type | Bread |

| Cakes and Pastries | |

| Biscuits and Cookies | |

| Morning Goods | |

| Other Bakery Products | |

| By Form | Fresh |

| Frozen | |

| By Category | Conventional |

| Organic/Clean Label | |

| Protein/Functional | |

| By Distribution Channel | Supermarkets and Hypermarkets |

| Convenience Stores | |

| Bakeries/Specialty Stores | |

| Online Retail Stores | |

| Other Retail Channels | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe bakery products market today?

The Europe bakery products market size reached USD 280.21 billion in 2026 and is projected to climb to USD 372.29 billion by 2031 at a 5.85% CAGR.

Which product type leads the category?

Cakes and pastries hold the largest share at 27.32% of 2025 sales, with biscuits and cookies showing the fastest projected growth.

What role does online retail play?

Online platforms are the fastest-expanding channel with a 6.88% CAGR, supported by home delivery and subscription services.

Which country is growing the quickest?

Germany is forecast to register the highest growth at a 6.01% CAGR through 2031 as consumers favor clean-label and sustainable options.

How are companies addressing sustainability rules?

Firms invest in recyclable and recycled-content packaging, energy-efficient baking lines, and upcycling initiatives to meet EU targets for 2030.

What is driving demand for clean-label baked goods?

Shoppers scrutinize ingredient lists and seek natural preservatives and plant-based components, spurring 6.44% CAGR growth in organic and clean-label items.

Page last updated on: