Premium Bakery Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

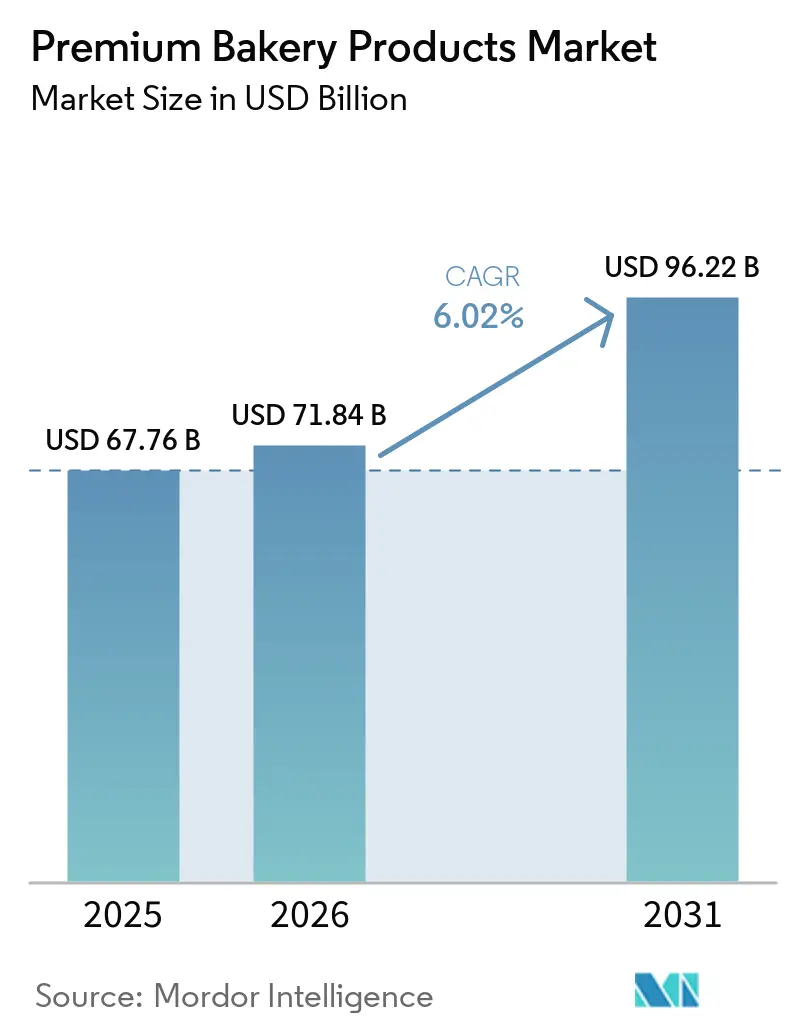

| Market Size (2026) | USD 71.84 Billion |

| Market Size (2031) | USD 96.22 Billion |

| Growth Rate (2026 - 2031) | 6.02% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Premium Bakery Products Market Analysis by Mordor Intelligence

The premium bakery market size is expected to grow from USD 67.76 billion in 2025 to USD 71.84 billion in 2026 and is forecast to reach USD 96.22 billion by 2031 at 6.02% CAGR over 2026-2031. The premium bakery market expansion results from consumer demand for artisanal products, clean-label ingredients, and convenience products suitable for urban consumers. Increased disposable incomes in emerging economies contribute to market growth, while enhanced freezing technologies facilitate expanded distribution networks for small-scale manufacturers. Despite food inflation, consumers continue to purchase premium bakery products that offer health benefits or authentic characteristics. Additionally, supply-chain disruptions and raw material cost variations present market challenges. However, organizations implementing diversified sourcing strategies and data analytics maintain operational efficiency. Besides, the bread and frozen segments exhibit substantial growth opportunities. Premium breads, including artisanal and specialty products, attract health-focused consumers who seek authentic flavors and natural ingredients. This market requirement drives product development, specifically in ancient grains and organic components. The frozen bakery segment grows through technological advancements that maintain product standards and enable increased distribution of premium products.

Key Report Takeaways

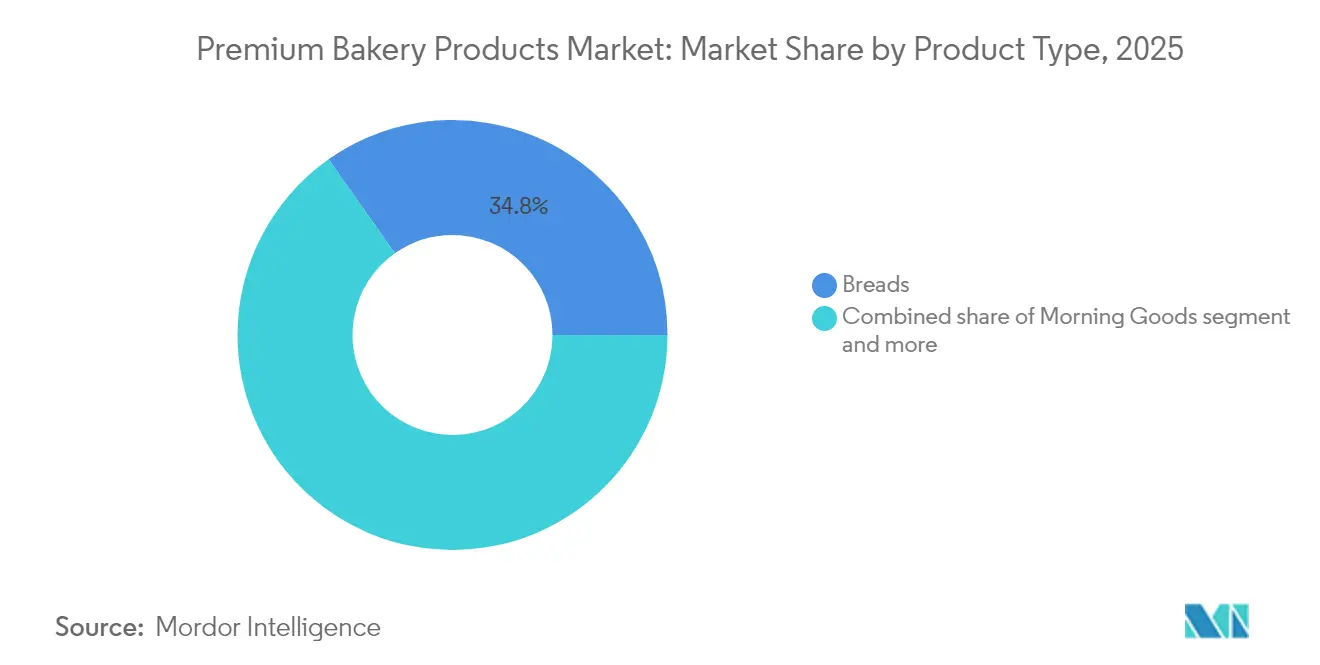

- By product type, breads captured 34.78% share of the premium bakery market in 2025, while cookies and biscuits are projected to expand at a 6.33% CAGR to 2031.

- By form, the fresh segment held 68.62% of the premium bakery market size in 2025, while the frozen products segment is forecast to grow at 5.18% through 2031.

- By category, the conventional segment retained a 71.58% share in 2025; the gluten-free segment is projected to expand at a 7.58% CAGR between 2026-2031.

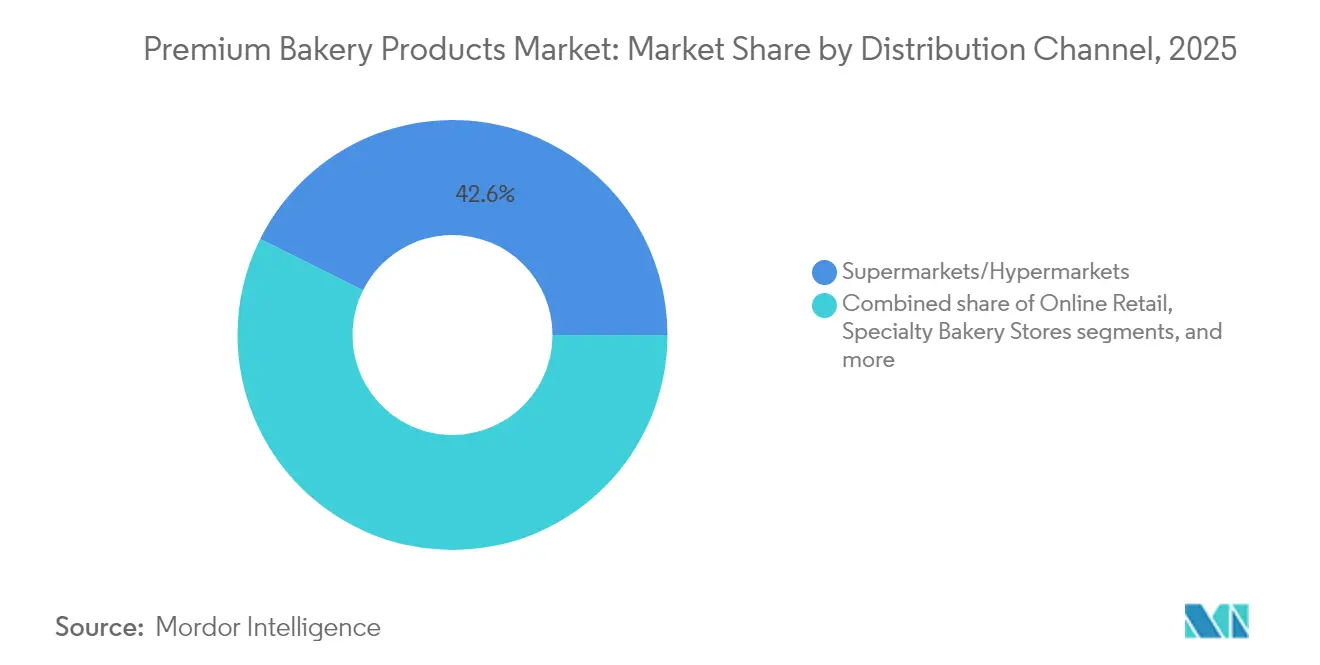

- By distribution channel, supermarkets/hypermarkets led with 42.63% premium bakery market share in 2025; online retail is set to rise at 7.42% CAGR through 2031.

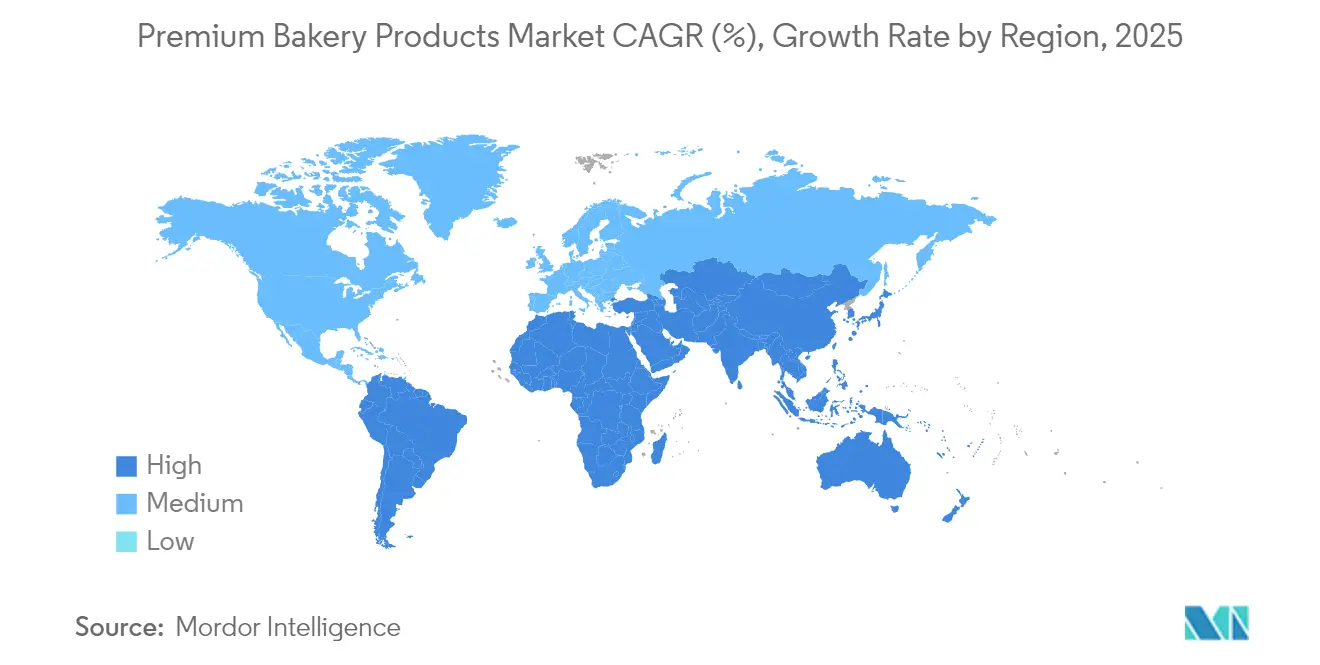

- By geography, Europe commanded 30.12% premium bakery market share in 2025, whereas Asia-Pacific is projected to record the fastest 6.51% CAGR over the period 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Premium Bakery Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising urban lifestyles increase demand for premium on-the-go bakery products | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Growing demand for clean-label and organic bakery products | +1.8% | North America and Europe primary, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Advanced freezing technologies extend premium product shelf life | +0.9% | Global, particularly benefiting emerging markets | Short term (≤ 2 years) |

| Increasing consumer preference for artisanal and gourmet bakery products | +1.5% | Europe and North America core, selective Asia-Pacific markets | Medium term (2-4 years) |

| Innovation in flavors and ingredients | +0.7% | Global, with regional flavor preferences | Short term (≤ 2 years) |

| Expansion of specialty diet products | +1.1% | North America and Europe primary, growing in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Urban Lifestyles Increase Demand for Premium On-the-Go Bakery Products

Urbanization is changing how people consume food, as city dwellers seek convenient, high-quality food options that fit their busy lifestyles. This shift has increased demand for premium grab-and-go products, transforming traditionally basic food categories into opportunities for upscale offerings. According to the Bureau of Labor Statistics, U.S. households spent an average of USD 574 on bakery products in 2023 [1]Source: Bureau of Labor Statistics, " Consumer expenditures in 2023," bls.gov . The Snack Food and Wholesale Bakery report indicates that center store breads were the second highest-selling bakery category in the U.S. in 2024, with unit sales of 3.3 billion units [2]Source: Snack Food & Wholesale Bakery, "State of the Industry 2024: Bakers continue to show resilience and creativity," snackandbakery.com . Individually wrapped premium products that maintain freshness while offering portability have gained significant market share. This trend is visible not only in developed markets but also in emerging economies, where rising disposable incomes and Western influence drive similar consumer preferences. Breakfast items like pastries and morning goods have adapted to this trend by incorporating refined flavors and natural ingredients in portable formats, expanding their consumption beyond traditional breakfast occasions.

Growing Demand for Clean-Label and Organic Bakery Products

Clean-label requirements are transforming ingredient sourcing and formulation strategies as consumers increasingly examine product compositions and demand transparency in manufacturing processes. According to the CBI Ministry of Foreign Affairs, clean-label products are expected to dominate the European food and beverage industry, making up over 70% of portfolios between 2025 and 2026, increasing from 52% in 2021. Additionally, 99% of European manufacturers consider clean-label products essential to their business strategy, with 87% already offering them in the market as of 2025 [3]Source: CBI Ministry of Foreign Affairs, "Which trends offer opportunities or pose a threat to the European natural food additives market?“, cbi.eu . This growth enables premium bakers to secure consistent organic inputs while maintaining price premiums that offset higher raw material costs. The clean-label movement extends beyond organic certification to include natural preservation methods, with innovations like cultured wheat and botanical extracts replacing traditional chemical preservatives. The rising demand for organic bakery products is further encouraging manufacturers to adopt transparent ingredient sourcing and sustainable production practices. Consumer willingness to pay higher prices for clean-label products creates competitive advantages for brands that invest in transparent supply chains and natural formulations. The trend particularly appeals to millennials and Gen Z consumers who prioritize health and environmental considerations, supporting market expansion as these demographics become primary purchasing decision-makers.

Advanced Freezing Technologies Extend Premium Product Shelf Life

Technological advancements in preservation and freezing systems are transforming the premium bakery market by enabling producers to expand their distribution networks while maintaining product quality. The introduction of MULTIVAC's Cooling@Packing system, which received the German Packaging Award in 2024, demonstrates this evolution. This system reduces products' temperature from 95°C to 30°C during the packaging process, minimizing contamination risks and extending shelf life [4]Source: MULTIVAC Group, "MULTIVAC wins the German Packaging Award with Cooling@Packing," multivac.com . Additionally, modern freezing methods, including cryogenic and ultra-low-temperature freezing, preserve the textures, flavors, and structural integrity of premium products such as artisan breads, pastries, and cakes by limiting ice crystal formation. These technological improvements enable premium bakery brands to distribute frozen-ready or bake-off products to remote markets while maintaining their artisanal quality. The advancements particularly benefit smaller producers by providing access to broader geographic markets, reducing product waste, and ensuring consumers receive bakery items at optimal quality. The integration of advanced preservation methods with premium product positioning creates expansion opportunities for artisanal and high-quality bakery brands, enabling them to increase production while maintaining their traditional craftsmanship standards.

Increasing Consumer Preference for Artisanal and Gourmet Bakery Products

Artisanal products combine traditional craftsmanship, authentic production methods, and quality ingredients to create meaningful food experiences beyond standard premium offerings. Social media platforms enhance the visibility of these visually appealing products, generating organic marketing that reduces acquisition costs for premium brands. Retail bakery companies now offer artisan-style packaged products that combine handcrafted quality with efficient distribution methods. These products address the growing consumer demand for authentic, indulgent, ready-to-eat baked goods that feature premium ingredients and traditional production methods. Companies are expanding their premium product lines in supermarkets by offering convenient formats with fresh-baked characteristics, reaching wider consumer segments while maintaining artisanal qualities. Also, Quality Bakery Products (QBP) exemplifies this trend with its new retail offerings in May 2025, including an artisan fruit cake featuring selected fruits and nuts, and retail pie shells designed for consumer convenience. These launches align with QBP's expansion of premium, artisanal-style products in the packaged bakery market. The continued popularity of sourdough, which increased during the pandemic, shows ongoing consumer interest in traditional fermentation and complex flavors that distinguish artisanal products from conventional alternatives. The gourmet segment has benefited from ingredients innovation, incorporating ancient grains and functional components that justify premium pricing while offering perceived health advantages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price point and affordability issues | -1.4% | Global, particularly pronounced in emerging markets | Medium term (2-4 years) |

| Fluctuations in raw material prices | -1.1% | Global, with varying regional impacts | Short term (≤ 2 years) |

| Fragmented artisanal channel limiting scale in emerging markets | -0.8% | Asia-Pacific and Latin America primarily | Long term (≥ 4 years) |

| Rising concerns about sugar and carbohydrate intake | -0.9% | North America and Europe primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Price Point and Affordability Issues

Premium positioning creates inherent accessibility barriers that limit market penetration, particularly as economic uncertainty pressures household budgets and forces consumers to prioritize value over quality. The bifurcation of consumer spending patterns, with economically stressed households gravitating toward value offerings while affluent segments embrace premium products, constrains overall market expansion potential. Organic wheat pricing significantly exceeds conventional alternatives, with price sensitivity affecting bakery adoption decisions despite consumer interest in organic products. This pricing pressure intensifies in emerging markets where premium bakery products compete against traditional alternatives and local artisanal offerings at substantially lower price points. The challenge becomes particularly acute during inflationary periods when raw material costs rise faster than consumer purchasing power, forcing brands to choose between margin compression and market share erosion. Strategic responses include value engineering, portion optimization, and tiered product portfolios that maintain premium positioning while offering accessible entry points for price-sensitive consumers.

Fluctuations in Raw Material Prices

Commodity volatility creates operational complexity and margin pressure that undermines predictable pricing strategies and long-term planning capabilities across the premium bakery value chain. For instance, according to the United States Department of Agriculture, baking ingredient costs surged 22% in 2022/23, with eggs experiencing 60% increases due to avian influenza outbreaks, while flour and butter prices rose approximately 20%. Wheat price volatility, driven by geopolitical tensions and weather disruptions, particularly affects premium bakers who rely on specialty flour varieties with limited supply alternatives. Premium bakers increasingly adopt just-in-case inventory strategies and diversified sourcing approaches to mitigate volatility impacts, though these measures increase working capital requirements and operational complexity. Raw material price fluctuations introduce uncertainty in product formulation and brand consistency, which are critical to maintaining premium positioning. Premium bakery brands, which often emphasize unique or high-quality ingredients, such as European-style cultured butter, organic flours, or free-range eggs, face narrower substitution options compared to mass-market producers. This limits their flexibility in adapting to price swings and puts pressure on either raising retail prices or absorbing margin losses, both of which threaten their competitive edge in a price-sensitive yet quality-driven consumer segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Breads Lead While Snacking Drives Innovation

Breads maintain market leadership with a 34.78% share in 2025, reflecting their foundational role in global diets and the successful premiumization of traditional staples through artisanal positioning and clean-label formulations. The segment benefits from sourdough popularity and ancient grain innovations that command premium pricing while delivering perceived health benefits. Cookies and biscuits emerge as the fastest-growing category with 6.33% CAGR through 2031, driven by snacking occasions and portable format preferences that align with urban lifestyle trends.

Morning goods capitalize on convenience trends and premium breakfast positioning, while cakes and pastries benefit from celebration market demand and individual portion innovations. The "others" category encompasses emerging formats like protein-enriched products and functional bakery items that blur traditional category boundaries. Better-for-you formulations across all product types reflect consumer health consciousness, with high-protein and low-carb variants gaining traction among fitness-focused demographics. Innovation in flavors and ingredients enables product differentiation within established categories, creating opportunities for premium positioning and margin expansion.

By Form: Fresh Dominance Challenged by Frozen Innovation

Fresh products command 68.62% market share in 2025, benefiting from consumer perceptions of quality and artisanal authenticity that drive premium positioning and impulse purchases. The fresh segment particularly thrives in perimeter bakery environments where visual appeal and aroma create sensory marketing advantages that frozen alternatives cannot replicate. However, frozen products advance at 5.18% CAGR through 2031, enabled by technological innovations that preserve quality while extending distribution reach and reducing waste.

Advanced freezing technologies and improved packaging solutions address historical quality concerns that limited frozen premium positioning, creating new market opportunities for artisanal brands seeking geographic expansion. The frozen segment benefits from convenience trends and extended shelf life requirements in emerging markets where cold chain infrastructure enables premium product access. Hybrid approaches, such as par-baked frozen products that finish in retail environments, combine convenience benefits with fresh presentation to capture both segments' advantages. The form segmentation increasingly reflects supply chain strategies rather than pure consumer preferences, with successful brands optimizing across both formats to maximize market reach and operational efficiency.

By Distribution Channel: Traditional Retail Evolves Amid Digital Disruption

Supermarkets/hypermarkets maintain a dominant 42.63% market share in 2025. These large-format retailers leverage their scale advantages and substantial investments in perimeter bakery departments, which create compelling fresh product showcases and generate significant impulse purchase opportunities. Their in-store bakery operations effectively combine convenience with perceived freshness, though they continue to face increasing challenges from private label competition and operational complexity in their daily operations. Online retail demonstrates substantial momentum, projected to grow at a 7.42% CAGR through 2031, establishing itself as the fastest-expanding distribution channel. This remarkable growth is primarily driven by direct-to-consumer artisanal brands and subscription-based models that bypass traditional retail markups.

Specialty bakery stores maintain their strong market position through meticulously curated product selections and engaging retail environments that effectively support premium pricing and sustained customer retention. Convenience stores and grocery outlets consistently serve immediate consumption needs with strategically designed grab-and-go formats. The Horeca and foodservice segment successfully capitalizes on experiential dining trends and premium restaurant offerings, while managing challenges from increasing labor costs and operational requirements. The expanding e-commerce channel enables artisanal brands to establish premium positioning through comprehensive customer engagement strategies, although their distribution reach and product selection remain constrained by fulfillment costs and delivery limitations.

By Category: Conventional Stability Meets Specialty Growth

Conventional products maintain 71.58% market share in 2025, demonstrating the sustained dominance of traditional formulations in the market. This market position stems from widespread consumer familiarity and established supply chains that enable competitive pricing across distribution channels. Gluten-free products emerge as the fastest-growing category with 7.58% CAGR through 2031, driven by increased celiac disease awareness and health-conscious consumer preferences in global markets.

The specialty diet segment growth reflects diverse dietary restrictions and lifestyle choices, creating distinct market opportunities for premium products across regions. Consumers with wheat and gluten sensitivities show increased willingness to pay for both gluten-free and organic products, indicating potential cross-category sales opportunities in retail channels. Clean-label formulations serve as a bridge between conventional and specialty categories by addressing health concerns without dietary restrictions, appealing to broader consumer segments. The market segmentation reflects increasing health awareness and the premium bakery sector's adaptation to diverse dietary requirements while maintaining product quality and taste standards.

Geography Analysis

Europe holds a 30.12% market share in 2025, driven by established artisanal traditions and mature consumer preferences for premium bakery products. The region's robust regulatory frameworks support clean-label and organic certifications, providing significant competitive advantages for premium brands. Europe maintains its market leadership due to its traditional baking expertise, consumer demand for organic and clean-label products, and strict quality standards. The region's focus on sourdough breads, specialty grains, and plant-based products continues to attract consumers.

Asia-Pacific shows the highest growth rate at 6.51% CAGR through 2031, supported by increasing disposable incomes and widespread Western lifestyle adoption. The region's younger, urban population demonstrates growing interest in premium food products and health-conscious choices, particularly clean-label and functional bakery items. The increased use of digital platforms and food delivery services in China and India improves access to premium bakery items. The expansion of e-commerce in Asia-Pacific enables premium brands to reach consumers directly, bypass traditional retail markups, and build customer relationships through storytelling and personalized offerings. International brands entering these markets often form strategic partnerships with local players to effectively address regulatory requirements and regional preferences in fragmented markets.

North America maintains consistent growth through health-focused consumer preferences and premium positioning in traditional bakery categories through better-for-you formulations and artisanal positioning. The region's developed distribution networks and e-commerce infrastructure support the expansion of direct-to-consumer premium brands to achieve scale. South America and Middle East and Africa present growth potential due to increasing urbanization and rising incomes, though market success requires products tailored to local preferences and price considerations.

Competitive Landscape

The premium bakery market demonstrates moderate fragmentation, with artisanal bakeries and multinational corporations competing through differentiated market positioning and distribution channels. This fragmentation reflects the market's diverse consumer preferences and the relatively low barriers to entry for specialized premium brands, though scale advantages in distribution and raw material procurement favor larger players during periods of commodity price volatility. The major players in the market include Grupo Bimbo SAB de CV, Mondelez International Inc., and Britannia Industries Ltd.

Strategic patterns emphasize vertical integration and direct-to-consumer capabilities, with successful companies investing in proprietary distribution networks and e-commerce platforms that bypass traditional retail markups while building direct customer relationships that support premium pricing. Artisanal brands establish their market presence through traditional recipes, locally sourced ingredients, and clean-label products, which appeal to health-conscious consumers, particularly younger demographics. These companies build customer loyalty through social media presence and influencer collaborations. In response, large corporations acquire premium bakery startups, invest in research and development for innovative ingredients, and expand their product portfolios to include gluten-free, plant-based, and reduced-sugar options.

Data analytics enables companies to customize their offerings based on regional preferences, dietary requirements, and consumption occasions, improving market targeting. Companies also implement co-branding strategies and release limited-edition products to maintain market interest and differentiate themselves in the competitive environment.

Premium Bakery Products Industry Leaders

-

Grupo Bimbo SAB de CV

-

Mondelez International Inc.

-

Britannia Industries Ltd.

-

Associated British Foods plc (Allied Bakeries & ABF Brands)

-

Finsbury Food Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Rich Products (Rich's) introduced the Christie Cookie Co. Celebration Cookie, which combined a premium sugar cookie base made with butter, vanilla, and birthday cake flavoring. The cookie included sprinkles, white chocolate, and marshmallows, delivering a fresh-baked product suitable for celebratory occasions.

- December 2024: ARYZTA constructed a new large-scale stone oven line at its German facility. The expansion addressed the growing demand for authentic, stone-baked artisan breads in retail and foodservice markets. This investment enhanced ARYZTA's premium bakery production capacity and supported its strategy of manufacturing high-quality, traditional baked goods for global distribution.

- May 2024: Bridor established a bread and pastry manufacturing facility in New Jersey to expand its North American operations. The facility addressed the increasing demand for European-style baked goods and enhanced production capacity for artisanal products using traditional methods at an industrial scale. This investment strengthened Bridor's presence in the U.S. market through local manufacturing capabilities.

- March 2024: InVivo's Episens established GOURMANCE, a French bakery brand for foodservice and bakery professionals in domestic and international markets. The brand offered breads, viennoiseries, pastries, and culinary aids to meet the growing demand for premium ready-to-use bakery products. GOURMANCE implemented traditional production methods, including long fermentation processes, and utilized French ingredients such as local wheat, free-range eggs, and butter.

Global Premium Bakery Products Market Report Scope

Bakery goods come in a vast variety and are made from flour or meal made from cereals. The quality of premium bakery goods is greater than average, yet they are frequently more expensive. The global premium bakery products market is segmented based on Product type, Distribution channel, and Geography. Based on product type, the market is segmented into bread, cookies and biscuits, morning goods, cakes and pastries, and others. Based on the distribution channel, the market is segmented into hypermarkets/ supermarkets, specialty stores, online retail stores, and other distribution channels. The study also covers the global level analysis of the major regions, such as North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done based on value (in USD million).

| Breads |

| Cookies and Biscuits |

| Morning Goods |

| Cakes and Pastries |

| Others |

| Fresh |

| Frozen |

| Conventional |

| Gluten-Free |

| Horeca/Foodservice | |

| Retail/Household | Supermarkets/Hypermarkets |

| Specialty Bakery Stores | |

| Convenience Stores/Grocery Stores | |

| Online Retail Stores | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Netherlands | |

| Italy | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Nigeria | |

| Saudi Arabia | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Breads | |

| Cookies and Biscuits | ||

| Morning Goods | ||

| Cakes and Pastries | ||

| Others | ||

| By Form | Fresh | |

| Frozen | ||

| By Category | Conventional | |

| Gluten-Free | ||

| By Distribution Channel | Horeca/Foodservice | |

| Retail/Household | Supermarkets/Hypermarkets | |

| Specialty Bakery Stores | ||

| Convenience Stores/Grocery Stores | ||

| Online Retail Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Netherlands | ||

| Italy | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Nigeria | ||

| Saudi Arabia | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the premium bakery market?

The premium bakery market was valued at USD 71.84 billion in 2026 and is projected to reach USD 96.22 billion by 2031.

Which region holds the largest premium bakery market share today?

Europe leads with 30.12% premium bakery market share in 2025, driven by entrenched artisanal traditions.

Which product segment is expanding the fastest?

Cookies and biscuits post the highest 6.33% CAGR through 2031 due to rising snacking occasions

How quickly is the online channel growing?

Online retail sales are forecast to climb at a 7.42% CAGR between 2026-2031 as direct-to-consumer models scale.

Page last updated on: