Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

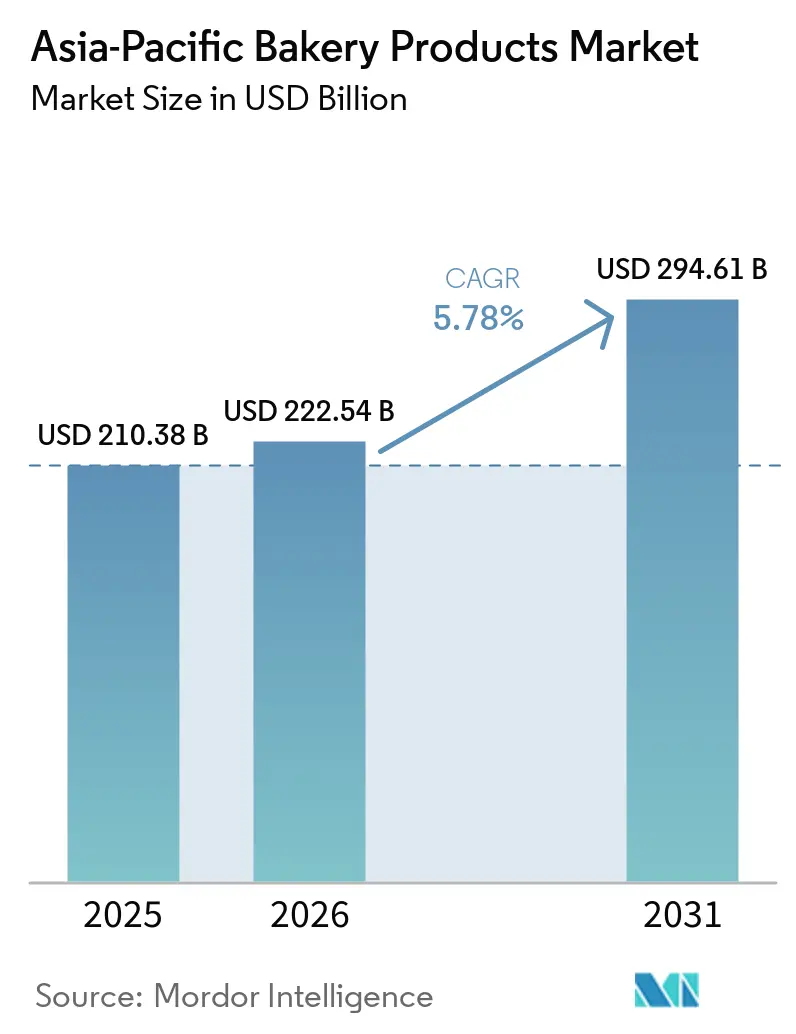

| Base Year Market Size (2025) | USD 210.38 Billion |

| Market Size (2026) | USD 222.54 Billion |

| Market Size (2031) | USD 294.61 Billion |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Bakery Products Market Analysis by Mordor Intelligence

The Asia Pacific bakery products market size was valued at USD 210.38 billion in 2025 and estimated to grow from USD 222.54 billion in 2026 to reach USD 294.61 billion by 2031, at a CAGR of 5.78% during the forecast period (2026-2031). Urban consumers, with rising disposable incomes and broader retail access, are increasingly gravitating towards convenient foods that resonate with their cultural tastes. This shift is driven by the growing demand for time-saving meal options that do not compromise on familiarity or quality. As busy lifestyles compress meal prep times, ready-to-eat items like breads, cakes, and pastries are seeing a surge in popularity, catering to both convenience and taste preferences. The trend of premiumization is also noteworthy; consumers are drawn to brands that marry indulgence with health-conscious choices, such as whole grains and reduced sugar, reflecting a balance between luxury and wellness. While multinational companies are driving innovation in the category through strategic local acquisitions to better understand and cater to regional preferences, domestic players are holding their ground by spotlighting regional flavors and ensuring neighborhood distribution to maintain their competitive edge. Enhancements in cold-chain infrastructure, a surge in digital commerce, and evolving packaging regulations are collectively expanding the market reach for products across all tiers, enabling producers to cater to a wider and more diverse consumer base.

Key Report Takeaways

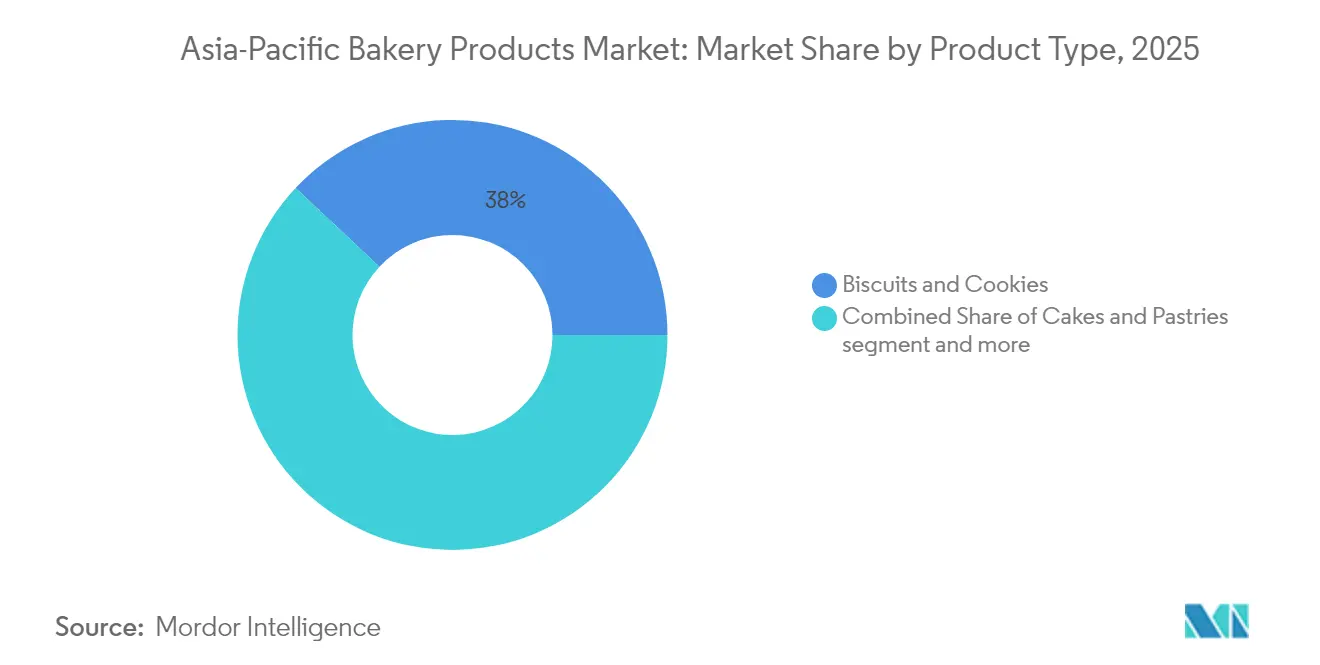

- By product type, biscuits and cookies led with 38.02% revenue share in 2025; cakes and pastries are forecast to expand at a 6.53% CAGR to 2031.

- By category, conventional lines accounted for 92.74% of 2025 sales; free-from alternatives are set to record a 7.41% CAGR through 2031.

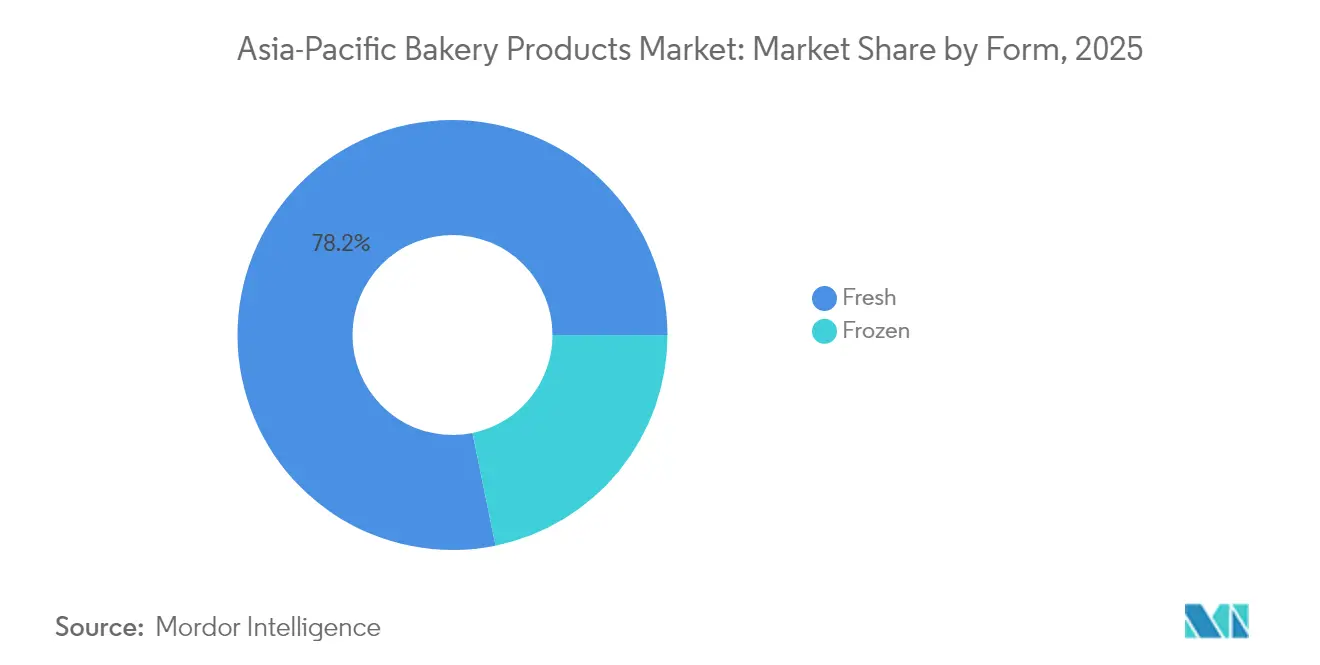

- By form, fresh offerings captured 78.21% share in 2025; frozen products are anticipated to grow at a 6.4% CAGR over the same period.

- By distribution channel, off-trade outlets held an 82.97% share in 2025; on-trade venues are expected to rise at a 6.69% CAGR by 2031.

- By geography, China commanded 29.05% of 2025 revenues; India is projected to achieve a 6.95% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Bakery Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Convenience-driven snacking boom | +1.2% | Urban China, Japan, South Korea | Medium term (2-4 years) |

| E-commerce acceleration for baked goods | +0.8% | China, India, Southeast Asia | Short term (≤ 2 years) |

| Health-oriented product reformulation | +0.9% | India, Indonesia, Malaysia | Long term (≥ 4 years) |

| Expansion of in-store supermarket bakeries | +0.7% | China, Japan, Australia | Medium term (2-4 years) |

| Functional-fiber fortification initiatives | +0.6% | Japan, Australia, premium China | Long term (≥ 4 years) |

| Sustainable packaging mandates | +0.5% | Australia, Japan, Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Convenience-driven snacking boom

In bustling megacities, the demand for portable bakery items has surged, with many now serving as convenient meal replacements. With commuters often dedicating over 90 minutes daily to transit, there's a growing preference for on-the-go options like single-serve cakes, filled buns, and nutrient-rich breads that are easy to consume while traveling. Japan boasts a vast network of over 56,000 convenience stores, each rotating freshly baked goods multiple times a day to ensure optimal softness and aroma, catering to the fast-paced lifestyle of urban consumers. Meanwhile, in China, store operators have introduced on-site ovens, catering to shoppers' desires for warm, freshly baked items at any time of the day or night, enhancing the overall shopping experience. Recognizing the preferences of female professionals aged 26-40, brands are adopting portion-controlled packaging that balances calorie management with flavor diversity, addressing both health-conscious and taste-driven needs. Furthermore, to enhance energy sustenance and meet the nutritional demands of busy consumers, brands are infusing their offerings with slow-release carbohydrates and plant proteins, ensuring each serving provides long-lasting energy and satiety.

E-commerce acceleration for baked goods

Contributing a quarter of the world's digitally deliverable services, the region has developed platforms capable of managing temperature-sensitive orders, enabling the seamless delivery of perishable goods. Insulated "last-mile" carriers ensure that artisanal sourdough loaves, gluten-free muffins, and exclusive pastries arrive fresh at distant homes, maintaining product quality and customer satisfaction[1]Source: Asian Development Bank," E-COMMERCE EVOLUTION IN ASIA AND THE PACIFIC", www.dpworld.com. Subscription models for weekly bread baskets not only generate recurring revenue but also enhance demand forecasting by providing businesses with consistent data on consumer preferences and purchasing patterns. Through cross-border channels, Taiwanese pineapple cakes and Japanese chiffon rolls are gaining popularity among fans in Malaysia, all without the need for physical storefronts, thereby reducing overhead costs and expanding their market reach. AI-driven search tools, by recommending products based on previous purchases, are boosting basket values and personalizing the shopping experience for consumers. However, achieving profitable scaling hinges on the presence of dense urban clusters, where the costs of same-day delivery remain feasible, ensuring operational efficiency and cost-effectiveness.

Health-oriented product reformulation

India's regulatory body has set a cap of 2% on industrial trans-fats, pushing manufacturers to pivot towards non-hydrogenated oils to comply with the new standards. Concurrently, sugar-reduction initiatives in Indonesia and Malaysia are prompting swift recipe modifications to align with evolving health guidelines. Major bakers are now substituting sucrose with stevia blends, a natural sweetener known for its low-calorie benefits, and are opting for multi-grains rich in β-glucan, which is associated with improved heart health, over refined wheat. In three years, Britannia achieved a 3.3% reduction in sugar content and a notable 75.8% increase in whole-grain usage, reflecting a significant shift toward healthier product offerings. Research published in peer-reviewed journals indicates that incorporating hull-less barley flour boosts the antioxidant capacity of sandwich bread, enhancing its nutritional profile while maintaining a texture that consumers favor. While reformulating recipes can elevate costs due to the use of premium ingredients and additional research and development efforts, consumers are inclined to pay a premium for products flaunting "better-for-you" seals on their packaging, which signify healthier choices.

Expansion of in-store supermarket bakeries

Retailers leverage freshly baked goods to boost overall basket values. Japanese grocers use compact deck ovens to churn out baguettes, Danish pastries, and savory rolls hourly, ensuring the enticing aroma wafts through the aisles and enhances the shopping experience. Australian chains highlight “baked today” crusty loaves, aiming to create a unique selling point that sets them apart from online grocery rivals while appealing to consumers seeking freshness and quality. In China, live preparation counters let shoppers witness dough proofing and golden browning, offering a sensory experience that emphasizes transparency, craftsmanship, and trust in product quality. Automation, through tools like spiral mixers, divider-rounders, and programmable proofers, lessens the reliance on skilled labor, streamlines production processes, and makes the model feasible even in smaller urban settings where space and resources are limited. Collaborating with local pastry chefs expands offerings, introducing diverse and artisanal options to attract a broader customer base without inflating capital costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile wheat and dairy input prices | -0.4% | Import-dependent markets | Short term (≤ 2 years) |

| Sugar-tax ripple effects in ASEAN | -0.3% | Southeast Asia | Medium term (2-4 years) |

| Stricter trans-fat regulations | -0.8% | India, Malaysia | Medium term (2-4 years) |

| Supply-chain bottlenecks for frozen logistics | -0.6% | Infrastructure-constrained areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile wheat and dairy input prices

Throughout 2024, wholesale wheat prices remained steady between INR 31,500 and 34,300 per tonne, squeezing the gross margins of branded breads and cookies. Concurrent surges in milk powder and butter prices have driven up costs for laminated dough. This situation has left producers with two choices: either raise list prices, which could risk losing price-sensitive customers, or reduce product weights, potentially impacting consumer perception of value. Economies reliant on imports, like Indonesia, face heightened vulnerabilities, sourcing over half of their wheat from abroad and consequently feeling the brunt of freight and currency fluctuations. These challenges are further exacerbated by global supply chain disruptions and geopolitical tensions, which add to the unpredictability of costs. To mitigate risks, larger buyers often turn to annual contracts, locking in prices to avoid volatility, or explore alternative grains, such as sorghum, to diversify their supply base. In contrast, smaller bakeries, without the leverage of scale, are either putting a hold on low-margin SKUs or postponing their innovation efforts, waiting for a return to stability in raw material prices. This delay in innovation could hinder their ability to compete in an already challenging market environment.

Stricter trans-fat regulations

Local producers of crackers and wafers, accustomed to using partially hydrogenated oils for achieving crisp textures and extending shelf life, now face significant formulation hurdles due to mandatory trans-fat ceilings. These regulations aim to reduce health risks associated with trans-fat consumption, but they have introduced operational challenges for manufacturers. Two years post-enactment of the rule, research from India's food authority reveals that compliance in the informal sector remains below 40%, highlighting a substantial gap in adherence. While substitutes like interesterified palm fractions, shea stearin, and high-oleic sunflower oil can be used, they often lead to double-digit increases in input costs. Additionally, these alternatives may alter the product's mouthfeel if not meticulously balanced, potentially impacting consumer acceptance. To address these challenges, technical service teams from multinational ingredient suppliers are conducting on-site trials for regional firms, offering tailored solutions and guidance. However, despite these efforts, the adoption rate remains sluggish, putting these firms at risk of enforcement penalties, product withdrawals, and potential market share losses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Premium Cakes and Pastries Outpace Staples

In 2025, biscuits and cookies dominated the Asia Pacific bakery products market, capturing 38.02% of total sales. Their leading position stems from their long shelf life, convenience, and widespread flavor appeal among diverse consumers. Moreover, aggressive promotional pricing by both regional and international brands has bolstered their accessibility, particularly in cost-sensitive markets. Rural consumers, drawn to the affordability of multipack formats, have shown a consistent preference for traditional sweet biscuits, benefiting from their deep penetration in general trade channels. This category's resilience spans both premium and value ranges, granting it an edge over other bakery formats. Consequently, biscuits and cookies have solidified their status as a household staple, retaining significance in contemporary retail settings.

Conversely, cakes and pastries are set to experience the swiftest growth, boasting an impressive CAGR of 6.53% during the forecast period. Younger consumers increasingly perceive dessert-style bakery items as social symbols, especially during holidays, café visits, and celebrations, driving premium demand. In China, the cake segment alone exceeded USD 3 billion, with specialty shops proudly displaying hand-decorated sponges and creamy rolls, underscoring the artistry involved. Coastal cities, witnessing a shift in traditional breakfast habits due to an evolving café culture, have embraced Western delights like croissants and cruffins. This artisan approach fuels revenue, with patisserie houses marketing limited-batch entremets at prices two to three times higher than packaged counterparts. Beyond mere indulgence, the surge in digital food tutorials is encouraging home cooks to experiment with layered desserts, subsequently driving demand for essential ingredients like flour, butter, and yeast. This blend of experiential value, premium branding, and youthful enthusiasm positions the category for swift growth throughout the Asia Pacific region.

By Category: Free-From Lines Close the Gap

In 2025, conventional bakery SKUs commanded a dominant 92.74% share of the total turnover in the Asia Pacific market. Their widespread appeal, rooted in wheat-based, sweetened formulations, resonates with mass-market preferences. This not only underscores their popularity but also enables manufacturers to harness economies of scale. The enduring success of these products can be attributed to their familiarity, affordability, and efficient distribution channels, spanning both modern and traditional retail outlets. For consumers, whether in rural areas or mainstream urban centers, conventional baked goods are a staple, woven into the fabric of daily life. This strong foothold not only ensures consistent volume but also provides stability to companies, even amidst fluctuations in premium or niche formats. While health-focused alternatives are on the rise, conventional bakery items continue to thrive, serving the region's largest consumer base.

Free-from bakery goods, including gluten-free, sugar-free, and allergen-light varieties, are poised for the most significant growth, with a projected CAGR of 7.41%. Urban consumers, becoming increasingly discerning, are driving this demand, often seeking specific claims such as “no maltodextrin” and “zero lactose.” Supermarkets, responding to this heightened interest, are dedicating more shelf and end-cap space to these specialized items. Countries like Australia and Singapore are seeing particularly strong traction, driven by increased awareness of celiac disease and broader wellness initiatives. In response, manufacturers are investing in allergen-segregated production lines, ensuring food safety and capitalizing on premium pricing that often exceeds conventional offerings by over 30%. Research into functional ingredient substitutions, such as apple puree, inulin, and stevia, allows manufacturers to cut sugar content while preserving sensory qualities, though these formulation challenges demand substantial research and development investment. Ingredient suppliers play a crucial role, introducing innovations like resistant starches, inulin, and natural sweeteners, ensuring health claims don't compromise texture and taste. Industry moves, like Grupo Bimbo’s acquisition of a gluten-free specialty baker, highlight the segment's long-term promise, supported by a loyal consumer base that views these "free-from" options as essential health solutions rather than mere indulgences.

By Form: Frozen Innovation Gains Traction

In 2025, the Asia Pacific market saw fresh bakery products commanding a significant 78.21% share, underscoring the region's deep-rooted cultural ties to daily bread and steamed bun purchases. Consumers, accustomed to integrating fresh-baked goods into their meals and snacks, treat these items as staples. Distribution channels, primarily local bakeries, neighborhood shops, and street vendors, ensure these goods remain accessible, catering to consistent demand in both urban and rural settings. This preference for freshness not only underscores perceptions of quality and authenticity but also drives repeat purchases. Even in bustling modern cities, the allure of freshly baked bread and buns often overshadows packaged alternatives. Consequently, the fresh bakery segment stands as the largest and most resilient pillar of the regional bakery industry.

While fresh bakery products dominate the scene, the frozen bakery segment is rapidly gaining momentum, projected to grow at an impressive CAGR of 6.4%. This surge is largely attributed to advancements in cold-chain logistics throughout Southeast Asia, which are not only broadening distribution but also upholding quality standards. Central kitchens are increasingly turning to flash-frozen par-baked croissants and similar items. This strategy allows establishments like hotels, cafés, and quick-service restaurants to bake on demand, significantly curbing waste and minimizing labor needs. Additionally, frozen pizza bases are riding the wave of popularity, thanks to the burgeoning fast-food chains and cloud kitchens that prioritize consistent product performance. Yet, geographical disparities exist: while freezer penetration soars past 95% in South Korea, it stagnates at a mere 15% in Indonesia, leading to varied household adoption rates. To bridge these gaps, there's a notable uptick in investments towards refrigerated transport fleets and multi-temperature distribution centers, bolstering supply chain efficiency and food safety compliance. Brands are also ramping up consumer education efforts, emphasizing taste parity and touting marketing claims like “oven-fresh aroma” to assuage first-time buyer hesitations, setting the stage for continued category growth.

By Distribution Channel: Foodservice Recovery Lifts On-Trade

In 2025, off-trade retail channels, including hypermarkets, supermarkets, convenience stores, and e-commerce, commanded a dominant 82.97% share of bakery product sales in the Asia Pacific. This stronghold stems from the convenience, affordability, and diverse assortments these outlets offer, positioning them as primary shopping hubs for many households. Supermarkets, in particular, not only provide packaged staples but also feature in-store bakery counters, enhancing freshness and variety, which in turn bolsters shopper loyalty. E-commerce has swiftly carved a niche in the premium segment, especially excelling during gifting occasions, where items like macaron assortments and celebration cakes command higher packaging margins. Traditional wet markets still play a vital role in countries such as Indonesia and the Philippines, where consumers prioritize daily freshness and flexible pricing for everyday bread purchases. The varied and accessible nature of off-trade formats solidifies their status as the backbone of bakery distribution, catering to both budget-conscious and premium-seeking consumers.

While off-trade channels dominate, on-trade venues are set to experience the fastest growth, with a projected CAGR of 6.69% through 2031, fueled by a resurgence in dine-in culture. Cafés, restaurants, and hotel bakeries are becoming increasingly favored by younger demographics, who perceive these venues as social hubs for indulgence and lifestyle expression. Major chains are broadening their regional presence, exemplified by Japanese café operator Doutor's recent announcement of 60 new stores in Vietnam and Thailand, each showcasing localized treats like matcha chiffon slices and fusion sandwiches. Supermarkets are venturing into in-house café concepts, luring shoppers to dine on-site and enhancing profits through bakery and coffee pairings. Online food aggregators are amplifying this growth by featuring patisserie menus alongside savory takeout, granting artisanal and dark-kitchen bakers a platform to reach expansive urban audiences. As consumers increasingly seek experiential dining and as bakery formats integrate into full-service offerings, the on-trade segment is emerging as a vibrant growth engine for the market.

Geography Analysis

China commands a dominant 29.05% share of the Asia Pacific bakery products market. By 2025, national retail bakery sales neared USD 53 billion, driven by the urban middle class's embrace of Western eating habits and a surge in hobbyist home baking kits. With per-capita consumption at a modest 7.2 kg, there's ample room for growth as incomes rise. Cakes account for 41% of the local turnover, while pastries, buoyed by social media's spotlight on trendy flavors like matcha red-bean crêpe cakes, are witnessing the fastest growth at a 10.5% CAGR. Retailers are enhancing in-store ovens to produce soft, milky loaves that cater to Asian tastes.

India leads with a robust 6.95% CAGR, bolstered by its favorable demographics and a widening reach into rural areas. Biscuit behemoth Parle ensures its products are a staple in over six million mom-and-pop stores, making multi-serve packs easily accessible. The FSSAI's push for front-of-pack nutrition labeling is steering recipes towards reduced sugar and increased whole grains. Organized retail is gaining momentum; in 2024, modern grocery spaces expanded by 9%, creating stronger shelf presence for premium bakery offerings, including croissants, cupcakes, and products within the growing India cake segment.

Japan emphasizes premium quality through meticulous craftsmanship and stringent product safety. Supermarkets offer fresh loaves baked every four hours, while convenience stores promote soft whipped-cream buns, perfect for on-the-go snacking. Australia pioneers sustainability in the sector, enforcing a mandate for recyclable or compostable bakery packaging by 2028. South Korea's burgeoning café culture is elevating the popularity of intricate viennoiserie, a trend amplified by an online community that celebrates visually appealing desserts. In Southeast Asia, while Indonesia, Vietnam, and the Philippines experience rapid growth, they grapple with logistical hurdles. Here, frozen bread and cake mixes are in demand, especially in institutions where fresh supply chains falter. The Regional Comprehensive Economic Partnership is streamlining import duties on wheat gluten and bakery machinery, easing cost constraints for plant expansions.

Competitive Landscape

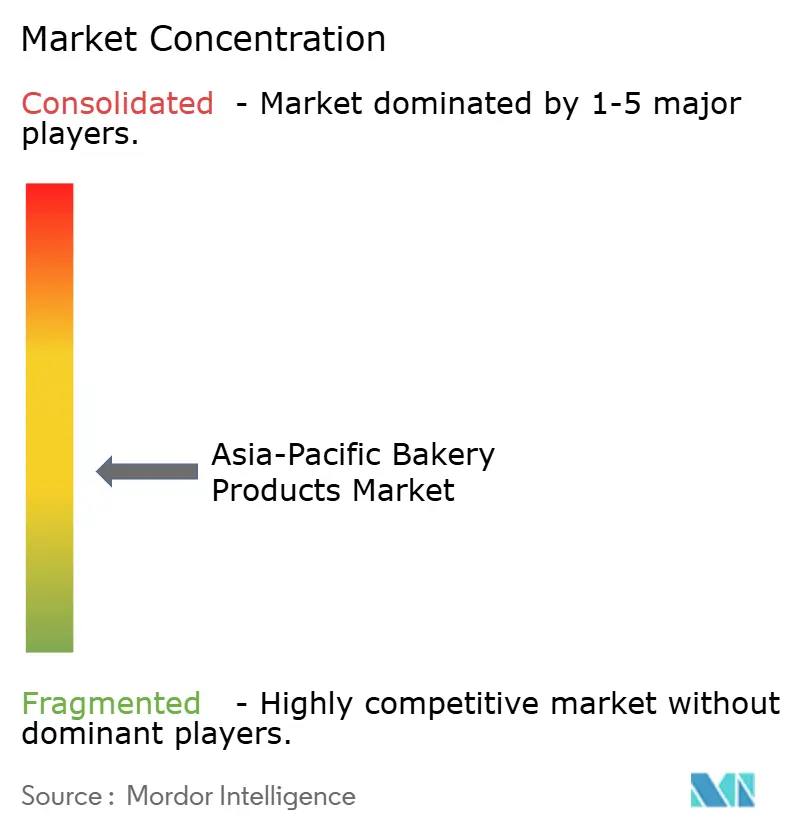

The competitive arena is moderately fragmented, with national champions coexisting alongside global multinationals. Only a handful of companies command more than a 5% individual market share, allowing regional artisans to flourish by catering to localized flavor profiles. Leading international groups are making strategic moves: Mondelēz International has taken a controlling stake in Evirth, a Chinese cake specialist, positioning itself firmly in the premium segment. In a collaborative effort, Lotus Bakeries teamed up with Mondelēz to craft biscuits filled with flavors tailored to Indian palates, utilizing Oreo’s extensive distribution network. Grupo Bimbo’s introduction of gluten-free products signals a strategic shift towards lucrative wellness trends.

Investments in automation are redefining cost leadership in the industry. Japanese factories have adopted continuous fermentation lines, significantly reducing proofing time while maintaining a consistent crumb texture. In Australia, producers are turning to solar-powered ovens, not only to cut energy costs but also to meet retailer emission standards. Mastery in digital commerce is becoming a key differentiator; companies that harness granular consumer data to feed AI recommendation engines are witnessing enhanced online conversion rates. In response, smaller bakers are emphasizing their farm-to-flour stories and community ties, turning authenticity into customer loyalty.

Hedging against raw material price fluctuations and prioritizing packaging stewardship are top of mind for companies. To shield against price shocks, firms are locking in wheat futures or branching out into regional grain variants. Forward-thinking companies are experimenting with biodegradable wheat-bran trays, staying ahead of impending bans on single-use plastics. With regulators tightening limits on saturated fat and sodium, research and development partnerships between enzyme suppliers and shortening manufacturers are becoming more pronounced, offering well-capitalized players a strategic advantage.

Asia-Pacific Bakery Products Industry Leaders

-

Mondelēz International, Inc.

-

Britannia Industries Limited

-

Wilmar International Limited (Goodman Fielder)

-

Grupo Bimbo SAB de CV

-

Yamazaki Baking Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Lotte India debuted its biscuit snack range, Pepero, offering both original and crunchy flavors. This launch marked the company's entry into the premium biscuit snack segment, aiming to cater to evolving consumer preferences for innovative and indulgent snack options.

- April 2025: Britannia introduced a new milled bread, boasting a zero-maida claim, and incorporating millets like ragi, jowar, bajra, and oats in its formulation. This product aligns with the growing demand for healthier alternatives in the bakery market, targeting health-conscious consumers seeking nutrient-rich options.

- January 2025: Mondelez International's Oreo brand rolled out limited-edition Pokémon cookies in India, featuring 16 distinct Pokémon-inspired designs. This launch was part of a strategic initiative to engage younger audiences and capitalize on the popularity of the Pokémon franchise, creating a unique and collectible product experience.

- November 2024: Britannia revamped its biscuit line with "Pure Magic Choco Stars," star-shaped biscuits filled with chocolate cream. This product reinvention aimed to enhance the brand's premium biscuit portfolio, offering a playful yet indulgent treat for consumers of all age groups.

Asia-Pacific Bakery Products Market Report Scope

Bakery products, which include bread, rolls, cookies, pies, pastries, and muffins, are usually prepared from flour or meal derived from some form of grain. The Asia-Pacific bakery products market is segmented by product type, distribution channel, and country. By product type, the market is segmented into cakes and pastries, biscuits and cookies, bread, morning goods, and other product types. By distribution channel, the market is segmented into supermarkets and hypermarkets, convenience stores, specialty stores, online retail stores, and other distribution channels. Also, the study analyzes the bakery products market in emerging and established markets across the Asia-Pacific region, including China, Japan, India, Australia, and the Rest of Asia-Pacific. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Product Type

| Bread |

| Cakes and Pastries |

| Biscuits and Cookies |

| Morning Goods (Muffins, Doughnuts, Croissants) |

| Others |

Category

| Conventional |

| Free From |

Form

| Fresh |

| Frozen |

Distribution Channel

| Foodservice/HORECA | |

| Retail\Off Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Specialist Bakeries | |

| Online Retail Retails | |

| Others |

By Geography

| China |

| Japan |

| India |

| Australia |

| South Korea |

| Indonesia |

| Thailand |

| Malaysia |

| Philippines |

| Vietnam |

| Rest of Asia-Pacific |

| By Product Type | Bread | |

| Cakes and Pastries | ||

| Biscuits and Cookies | ||

| Morning Goods (Muffins, Doughnuts, Croissants) | ||

| Others | ||

| Category | Conventional | |

| Free From | ||

| Form | Fresh | |

| Frozen | ||

| Distribution Channel | Foodservice/HORECA | |

| Retail\Off Trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Specialist Bakeries | ||

| Online Retail Retails | ||

| Others | ||

| By Geography | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Malaysia | ||

| Philippines | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What is the current value of the Asia Pacific bakery products market?

The Asia Pacific bakery products market is valued at USD 222.54 billion in 2026 and is forecast to reach USD 294.61 billion by 2031.

Which product category is growing fastest in Asia Pacific baked goods?

Cakes and pastries show the highest growth, registering a 6.53% CAGR between 2026 and 2031.

How large is China’s share of bakery sales in the region?

China accounts for 29.05% of total regional bakery revenue as of 2025

Which channel will grow fastest for bakery distribution?

On-trade venues such as cafés and restaurants are set to expand at a 6.69% CAGR as foodservice rebounds and new store formats proliferate.

Page last updated on: