Platelet Rich Plasma Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

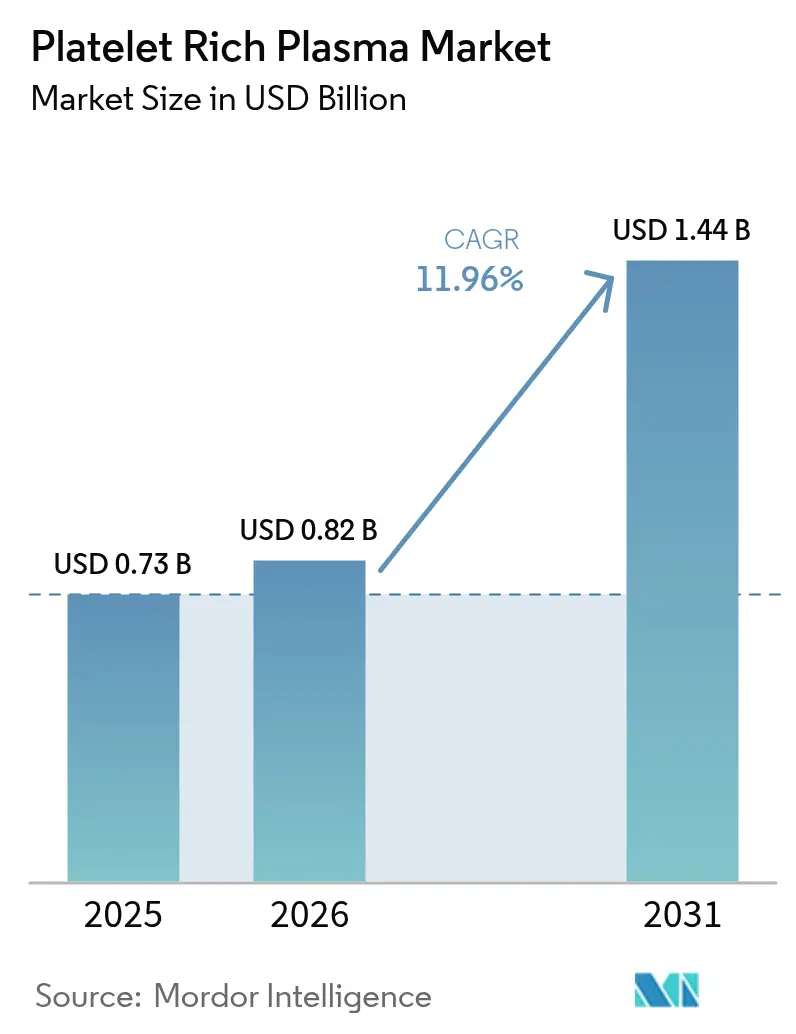

| Market Size (2026) | USD 0.82 Billion |

| Market Size (2031) | USD 1.44 Billion |

| Growth Rate (2026 - 2031) | 11.96% CAGR |

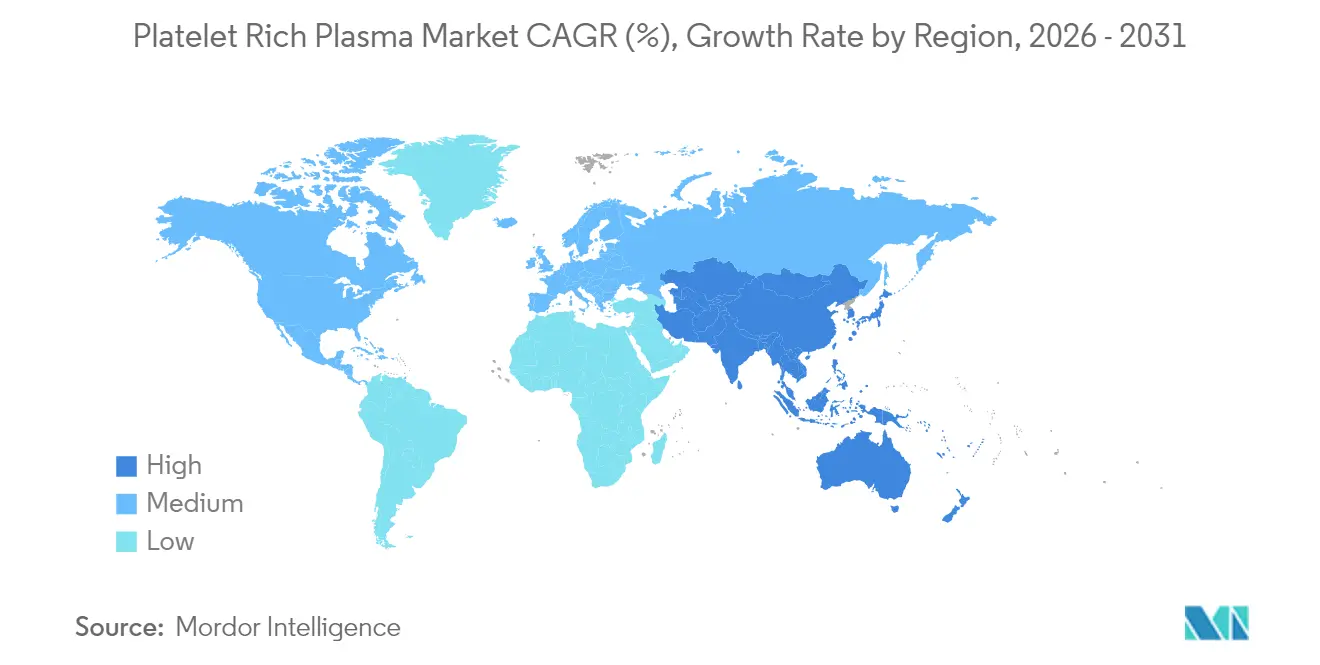

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Platelet Rich Plasma Market Analysis by Mordor Intelligence

The platelet rich plasma market size was valued at USD 0.73 billion in 2025 and estimated to grow from USD 0.82 billion in 2026 to reach USD 1.44 billion by 2031, at a CAGR of 11.96% during the forecast period (2026-2031). Demand accelerates as hospitals migrate regenerative therapies into office settings, automated preparation systems eliminate operator variability, and clinical evidence broadens across orthopedic, aesthetic, and dental indications. Orthopedic sports medicine keeps the widest clinical footprint, yet facial rejuvenation, hair restoration, and other cosmetic uses now set the growth pace. Companies differentiate by pairing microfluidic centrifuges with AI-guided separation algorithms, while regulatory clarity around autologous protocols sustains provider confidence. Asia-Pacific’s medical tourism boom and rising disposable income amplify global momentum, even as standardization gaps and reimbursement limits temper uptake in cost-sensitive markets.

Key Report Takeaways

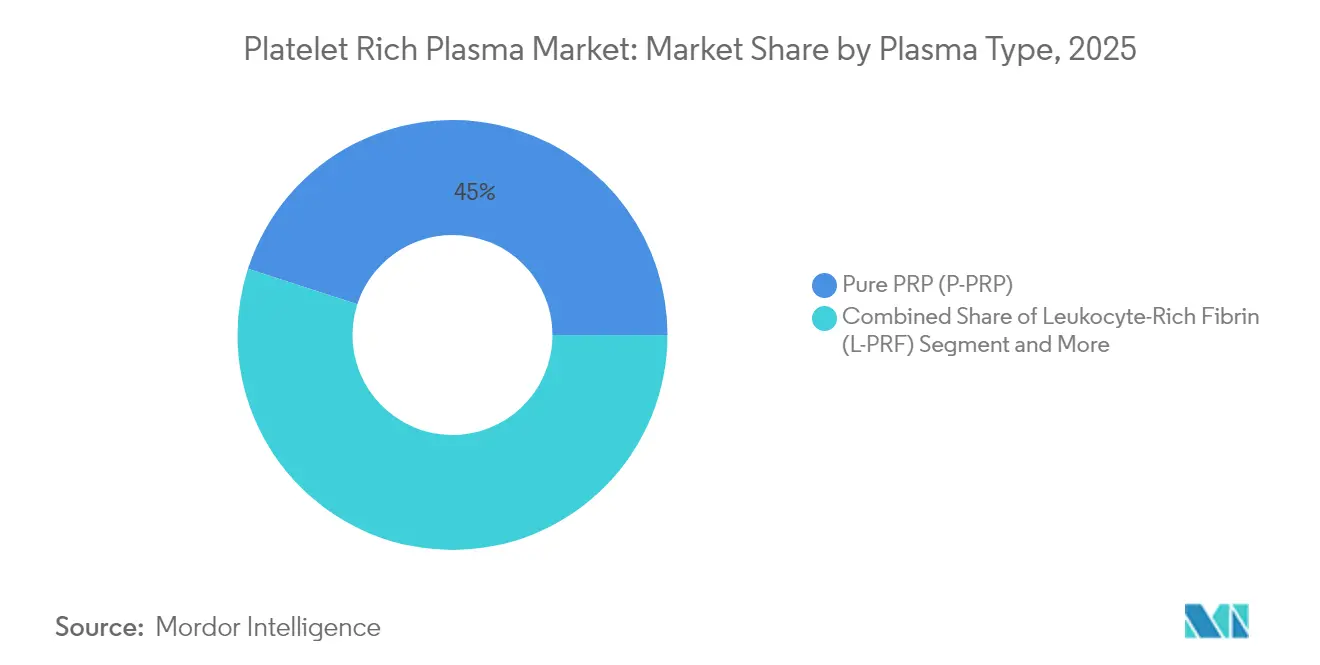

- By plasma type, Pure PRP led with 45.02% revenue share in 2025, whereas Leukocyte-Rich Fibrin is poised for the fastest expansion at an 17.92% CAGR through 2031.

- By application, sports medicine dominated with 40.01% of platelet rich plasma market share in 2025, while cosmetic and dermatological procedures are projected to escalate at a 17.52% CAGR to 2031.

- By end user, hospital settings controlled 47.02% of the platelet rich plasma market size in 2025, but specialty and ambulatory clinics are advancing the quickest at 16.54% CAGR.

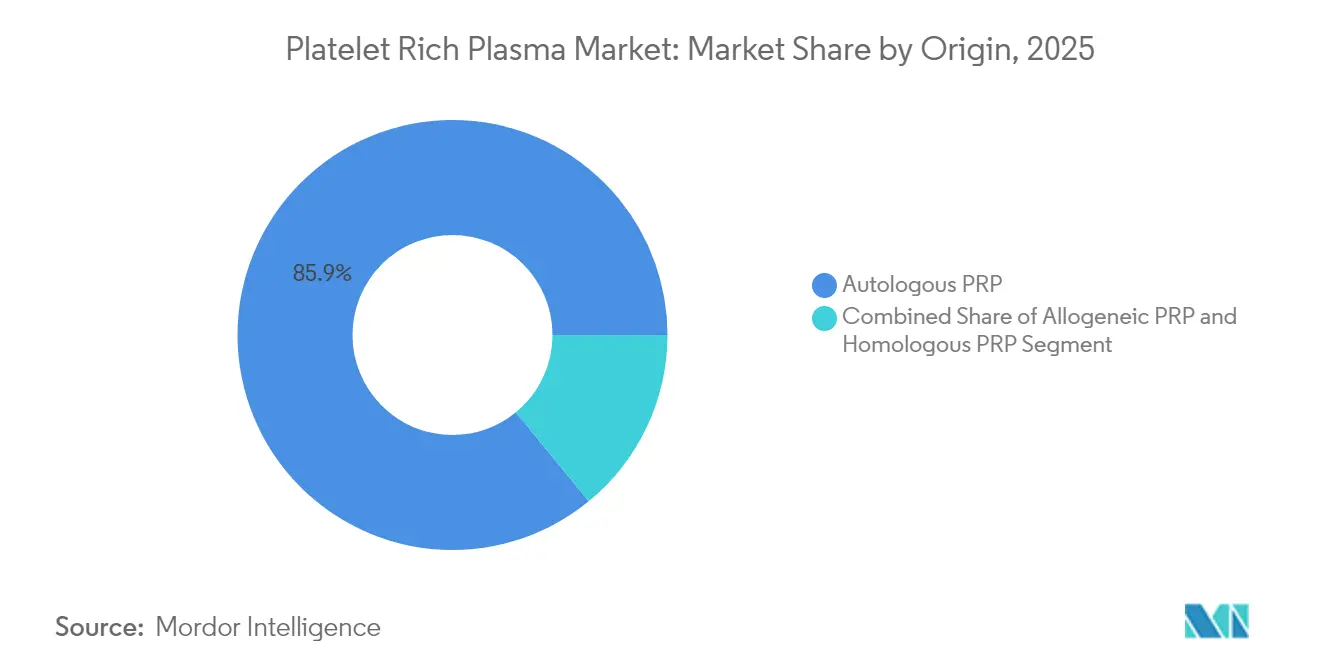

- By origin, autologous products represented 85.92% of 2025 revenue, yet allogeneic offerings are registering an impressive 15.38% CAGR as standardized donor protocols mature.

- By geography, North America held 39.21% share in 2025, although Asia-Pacific is forecast to generate the highest 15.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Platelet Rich Plasma Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of sports injuries & orthopedic disorders | +2.8% | North America, Europe, global spread | Medium term (2-4 years) |

| Growing cosmetic & aesthetic procedures volume | +3.2% | Asia-Pacific, North America | Short term (≤ 2 years) |

| Technological advances in PRP preparation systems | +2.1% | Early adoption in developed markets | Long term (≥ 4 years) |

| Aging population driving chronic musculoskeletal cases | +2.5% | Developed economies worldwide | Long term (≥ 4 years) |

| Surge in PRP + adjunct combo protocols | +1.4% | North America, Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Hospital shift to in-office autologous regenerative care | +1.8% | North America leading | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Sports Injuries & Orthopedic Disorders

Elite and amateur athletes increasingly select PRP as a first-line intervention for tendon and ligament trauma, with National Football League data showing a 15% uptick in regenerative therapy usage over traditional surgery in 2024[1]“Player Health and Safety Report 2024,” NFL Players Association, nflpa.com. Standard protocols involve three injections across six weeks, yielding faster return-to-play timelines and lower reinjury risk compared with lengthy physical therapy. Sports governing bodies continue to approve PRP while banning synthetic growth factors, preserving competitive integrity and steering demand toward autologous options. Weekend athletes mirror this shift, pursuing minimally invasive relief for chronic overuse injuries. Together, these trends enlarge the platelet rich plasma market by funneling a wider patient spectrum into orthopedic clinics that now view biologics as cost-effective adjuncts to conventional care.

Growing Cosmetic & Aesthetic Procedures Volume

Aesthetic medicine has embedded PRP into microneedling, laser resurfacing, and “vampire facial” protocols, with the American Society of Plastic Surgeons reporting a 47% surge in PRP-based cosmetic sessions in 2024[2]“2024 Plastic Surgery Statistics Report,” American Society of Plastic Surgeons, plasticsurgery.org. Younger consumers opt for preventive skin rejuvenation, while hair-restoration seekers embrace autologous options over synthetic implants. Social media and celebrity endorsements have scaled consumer awareness, enabling medical spas to expand beyond metropolitan hubs. Premium pricing remains acceptable because PRP avoids foreign fillers and provides a “natural” outcome narrative. Regulatory oversight, however, varies across markets, signaling future harmonization needs to safeguard treatment consistency and practitioner accreditation.

Technological Advances in PRP Preparation Systems

Automated microfluidic centrifuges deliver standardized platelet concentrations in under 15 minutes, shrinking chair time and boosting patient throughput. Terumo BCT’s AI-enabled platforms adjust spin parameters to each patient’s hematocrit, securing reproducible dosing and better outcomes. Integrated leukocyte filters allow clinicians to tailor inflammatory profiles per indication, for example selecting leukocyte-poor PRP for tendon healing and leukocyte-rich PRF for wound care. These advances address historical skepticism about biologic variability and support greater insurer confidence. Equipment vendors now bundle disposables, software, and training into subscription models that lower upfront costs, further expanding the platelet rich plasma market into small clinics.

Aging Population Driving Chronic Musculoskeletal Cases

Populations in Japan, the United States, and Western Europe are aging, and degenerative joint disease prevalence rises in parallel. Seniors prefer biologic injections to postpone or avoid joint replacement surgery, creating recurring treatment revenue and broadening payer discussions on cost offsets. Longevity trends also boost elective procedures such as anti-aging skin therapies, extending PRP demand outside orthopedic walls. Healthcare systems view PRP as a pathway to mitigate high surgical costs and rehab stays for older adults, positioning the therapy within value-based care initiatives that reward improved function and reduced hospitalization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of standardized preparation protocols | -1.8% | Higher in emerging markets | Medium term (2-4 years) |

| High out-of-pocket cost & weak reimbursement | -2.4% | Global, acute in developing economies | Short term (≤ 2 years) |

| Growing evidence-based scrutiny of PRP clinics | -1.2% | North America & Europe | Medium term (2-4 years) |

| Competing cell-free biologics cannibalizing demand | -0.9% | Developed markets first | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lack of Standardized Preparation Protocols

Systematic reviews have cataloged more than 40 preparation methods, each producing different platelet counts and growth-factor profiles, undercutting reproducibility and payer acceptance. Equipment disparities, staff training gaps, and inconsistent leukocyte filtration compound variability, especially in smaller or resource-constrained clinics. The FDA and international societies promote harmonized guidelines, yet global implementation trails regulatory intent. Until protocols converge, insurers label many PRP applications investigational, and peer-reviewed studies struggle to aggregate comparable outcome data. This ambiguity dampens referral confidence and slows broad clinical adoption, restraining the platelet rich plasma market in several regions.

High Out-of-Pocket Cost & Weak Reimbursement

Typical PRP injections cost USD 500–2,000 per session, and most insurers classify treatments outside a few orthopedic indications as elective, shifting payment responsibility to patients[3]“Economic Impact of Regenerative Medicine Treatments,” American Academy of Orthopaedic Surgeons, aaos.org. Multiple sessions amplify financial burden, limiting repeat uptake among middle-income populations. Some European health systems reimburse partially, while several Asian markets depend entirely on self-pay models. Providers experiment with financing plans and bundle pricing, but affordability remains a hurdle in emerging economies. Unless evidence drives policy change, reimbursement gaps will cap market penetration despite demonstrated clinical advantages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Plasma Type: Advanced Variants Drive Innovation

In 2025, Pure PRP captured 45.02% of the platelet rich plasma market, translating to USD 0.33 billion. However, the platelet rich plasma market size for Leukocyte-Rich Fibrin is projected to expand at an 17.92% CAGR between 2026 and 2031 as clinicians leverage its dense fibrin matrix for sustained growth-factor release. Orthopedic specialists favor leukocyte-poor formulations to minimize inflammation, whereas oral surgeons adopt L-PRF to bolster bone graft stability. Equipment makers respond with programmable centrifuges that toggle white-cell content on demand, encouraging precision medicine protocols. Emerging alternatives like advanced PRF and injectable-PRF fit niche applications, enhancing segment depth and fueling incremental revenue for system suppliers.

Across hospitals and dental offices, comparative studies from the International Association of Oral and Maxillofacial Surgeons document higher bone-to-implant contact rates using L-PRF than conventional graft material. The data prompt insurers in select European markets to pilot partial reimbursement, signalling mainstream acceptance. Meanwhile, autologous platelet lysate and plasma gel derivatives reach dermatology and wound-care niches, diversifying clinician toolkits. Collectively, the plasma-type spectrum broadens therapeutic flexibility and keeps innovation pipelines active, thus underpinning sustained growth in the platelet rich plasma market.

By Application: Cosmetics Disrupts Traditional Hierarchy

Orthopedic sports medicine held 40.01% of platelet rich plasma market share in 2025, equal to USD 0.29 billion. Yet cosmetic and dermatological interventions are accelerating at a 17.52% CAGR to 2031, supported by medical-spa proliferation and consumer appetite for minimally invasive anti-aging options. The platelet rich plasma market size for aesthetic procedures is expected to double by 2031 as younger demographics seek preventive skin quality improvements and hair-loss solutions. Dental and oral-maxillofacial indications follow, driven by PRP’s role in implant osseointegration and periodontal regeneration.

In ophthalmology, autologous PRP eye drops gain traction for severe dry-eye syndrome and corneal surface repair, receiving clinical-practice endorsement from the American Academy of Ophthalmology. Wound-care teams employ PRP dressings to accelerate postsurgical healing and chronic ulcer closure, expanding payer discussions around hospital cost avoidance. Neurology and spine specialties remain exploratory yet promising, with early trials assessing PRP injections for discogenic pain. Application diversity cushions revenue streams and shields the platelet rich plasma market from specialty-specific slowdowns.

By End User: Specialty Clinics Challenge Hospital Dominance

Hospitals accounted for 47.02% of platelet rich plasma market size in 2025, but ambulatory and specialty clinics are tracking a 16.54% CAGR as patients opt for shorter wait times and transparent pricing. Portable systems free providers from centralized labs, enabling procedure rooms to deliver same-day treatments. The Veterans Health Administration logged 40% year-on-year growth in outpatient regenerative therapies in 2024, underscoring institutional confidence. Clinics leverage social-media marketing and subscription models that bundle multiple injections, cultivating repeat business and community referral loops.

Academic research centers, though smaller in revenue, propel evidence generation and protocol refinement. Hospital networks respond by redesigning orthopedic and sports-medicine units into clinic-style suites, preserving referral traffic and capturing self-pay revenue. Equipment vendors facilitate the shift by offering lease programs responsive to variable outpatient volumes, ensuring continuous capital formation for the platelet rich plasma market.

By Origin: Allogeneic Solutions Gain Momentum

Autologous PRP commanded 85.92% revenue share in 2025, reflecting established safety and regulatory preference. Nevertheless, the platelet rich plasma market size for allogeneic products is anticipated to grow at a 15.38% CAGR as clear FDA guidance in 2024 catalyzes investment in donor screening and pathogen testing. Off-the-shelf solutions cut preparation time, a crucial advantage in emergency departments and trauma units where immediate intervention is vital. Quality-assured donor batches also promise reproducibility, addressing current variability critiques.

Pilot programs in U.S. academic hospitals evaluate allogeneic PRP for acute fracture care, while European biotech firms scale manufacturing to clinical-grade volumes. Cost reductions from centralized production could unlock payer willingness to reimburse standardized biologics, potentially redefining competitive dynamics. Homologous autologous composites remain niche due to regulatory hurdles, yet they exemplify ongoing exploration in origin-based differentiation that sustains innovation within the platelet rich plasma market.

Geography Analysis

North America generated USD 0.29 billion in platelet rich plasma market revenue in 2025 and preserved a 39.21% lead by leveraging robust clinical research networks, payer familiarity with biologics, and early FDA guidance. United States providers bundle PRP with arthroscopic procedures, advancing insurer acceptance, while Canada’s single-payer system selectively covers knee-osteoarthritis injections. Mexico’s cross-border clinics attract global patients seeking lower-cost packages that combine sports-injury repair and cosmetic enhancements, illustrating medical tourism’s effect on regional demand.

Asia-Pacific’s platelet rich plasma market is forecast to grow at 15.55% CAGR, the fastest worldwide. China’s 2024-2030 regenerative-medicine roadmap earmarks funding for PRP research centers, accelerating technology transfer and local device manufacturing. Japan’s super-aged society embraces PRP to delay hip and knee replacements, aligning with government efforts to contain elder-care expenditures. South Korea’s aesthetics sector integrates PRP into popular K-beauty regimens, while India’s multispecialty hospitals bundle orthopedic PRP packages for inbound medical tourists, strengthening foreign-exchange revenue and driving domestic adoption.

Europe maintains steady momentum, benefiting from harmonized EMA guidelines and multiple large-scale randomized controlled trials led by German and U.K. centers. Partial reimbursement for specific orthopedic and dental indications in Germany and Italy improves affordability. France and Spain record heightened cosmetic uptake, supported by stringent practitioner training mandates that enhance consumer trust. Middle East & Africa remain nascent yet attractive; Gulf Cooperation Council hospitals import premium centrifuges to capitalize on rising wellness tourism, and South Africa’s private clinics pilot PRP protocols in sports-injury rehabilitation.

Competitive Landscape

Market concentration is moderate, with orthopedic giants Stryker and Zimmer Biomet bundling PRP systems alongside implants to cross-sell into existing accounts. Terumo BCT and Arthrex fortify positions through automated centrifuges featuring AI-based platelet optimization, targeting hospitals that demand repeatable outcomes. Specialty firms such as Harvest Technologies and EmCyte innovate around closed-loop cartridges and micro-volume kits ideal for aesthetic clinics, creating entry barriers grounded in intellectual property.

White-space opportunities lie in standardized allogeneic products, combination regimens that marry PRP with hyaluronic acid or stem-cell exosomes, and specialty niches like ophthalmology. Patent filings on microfluidic channels and optical platelet-count sensors surged 18% year-on-year in 2024, reflecting investment in precision devices. Strategic collaborations emerge: device makers partner with academic hospitals to produce high-quality trial data, while pharma companies explore topical PRP gels that complement wound-healing drug portfolios. Competitive success pivots on regulatory compliance, evidence generation, and service models that blend capital equipment, disposables, and clinical training.

Platelet Rich Plasma Industry Leaders

EmCyte Corporation

Johnson & Johnson (DePuy Synthes)

Arthrex Inc.

Zimmer Biomet

Terumo Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Smith+Nephew introduced the CENTRIO Platelet-Rich-Plasma System, a biodynamic hematogel that supports moist wound environments.

- December 2024: Illuminate PRP gained FDA clearance for a point-of-care device that prepares autologous PRP for clinical use.

Global Platelet Rich Plasma Market Report Scope

As per the report's scope, platelet-rich plasma is defined as autologous blood with concentrations of platelets above baseline levels (which contains at least seven growth factors). Platelet-rich plasma therapy employs injections of the patient's concentrated platelets to accelerate the healing of injured tendons, ligaments, muscles, and joints.

The platelet rich plasma market segmentation includes type, application, end user, and geography. By type, the market is segmented into pure PRP, leukocyte-rich PRP, leukocyte-rich fibrin, and other types. By application, the market is segmented into orthopedics, cosmetic surgery and dermatology, neurology, cardiology, ophthalmology, and other applications. By end user, the market is segmented into hospitals and clinics, and research institutes. By geography, the global market is segmented into North America (United States, Canada, Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, Rest of Asia-Pacific), Middle East and Africa (GCC, South Africa, Rest of Middle East and Africa), and South America (Brazil, Argentina, Rest of South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market value (in USD billion) for the above segments. By Type Pure PRP Leukocyte-Rich PRP Leukocyte-Rich Fibrin Other Types By Application Orthopedics Cosmetic Surgery and Dermatology Neurology Cardiology Ophthalmology Other Applications By End User Hospitals & Clinics Research Institutes By Geography North America United States Canada Mexico Europe Germany United Kingdom France Italy Spain Rest of Europe Asia Pacific China Japan India Australia South Korea Rest of Asia Pacific Middle East and Africa GCC South Africa Rest of Middle East and Africa South America Brazil Argentina Rest of South America

| Pure PRP (P-PRP) |

| Leukocyte-Rich PRP (L-PRP) |

| Pure Platelet-Rich Fibrin (P-PRF) |

| Leukocyte-Rich Fibrin (L-PRF) |

| Other / Advanced Variants (A-PRF, i-PRF) |

| Orthopedics & Sports Medicine |

| Cosmetic Surgery & Dermatology |

| Dentistry & Oral-Maxillofacial |

| Neurology & Spine |

| Cardiology |

| Ophthalmology |

| Wound Care & Others |

| Hospitals |

| Specialty & Ambulatory Clinics |

| Research Institutes |

| Autologous PRP |

| Allogeneic PRP |

| Homologous PRP |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Plasma Type | Pure PRP (P-PRP) | |

| Leukocyte-Rich PRP (L-PRP) | ||

| Pure Platelet-Rich Fibrin (P-PRF) | ||

| Leukocyte-Rich Fibrin (L-PRF) | ||

| Other / Advanced Variants (A-PRF, i-PRF) | ||

| By Application | Orthopedics & Sports Medicine | |

| Cosmetic Surgery & Dermatology | ||

| Dentistry & Oral-Maxillofacial | ||

| Neurology & Spine | ||

| Cardiology | ||

| Ophthalmology | ||

| Wound Care & Others | ||

| By End User | Hospitals | |

| Specialty & Ambulatory Clinics | ||

| Research Institutes | ||

| By Origin | Autologous PRP | |

| Allogeneic PRP | ||

| Homologous PRP | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current global value of the platelet rich plasma market?

The market stands at USD 0.82 billion in 2026 and is projected to grow to USD 1.44 billion by 2031.

Which segment is expanding the quickest?

Cosmetic and dermatological applications are rising at a 17.52% CAGR through 2031.

How dominant are autologous products?

Autologous formulations represented 85.92% of 2025 revenue, although allogeneic options are gaining ground.

Which region offers the highest growth potential?

Asia-Pacific is forecast to register the fastest 15.55% CAGR between 2026 and 2031.

How are preparation technologies evolving?

AI-guided microfluidic centrifuges now deliver standardized platelet concentrations in under 15 minutes, boosting clinical confidence.

What limits wider adoption today?

High out-of-pocket costs and inconsistent preparation protocols remain the chief barriers to broader uptake.

Page last updated on: