Autologous Cell Therapy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

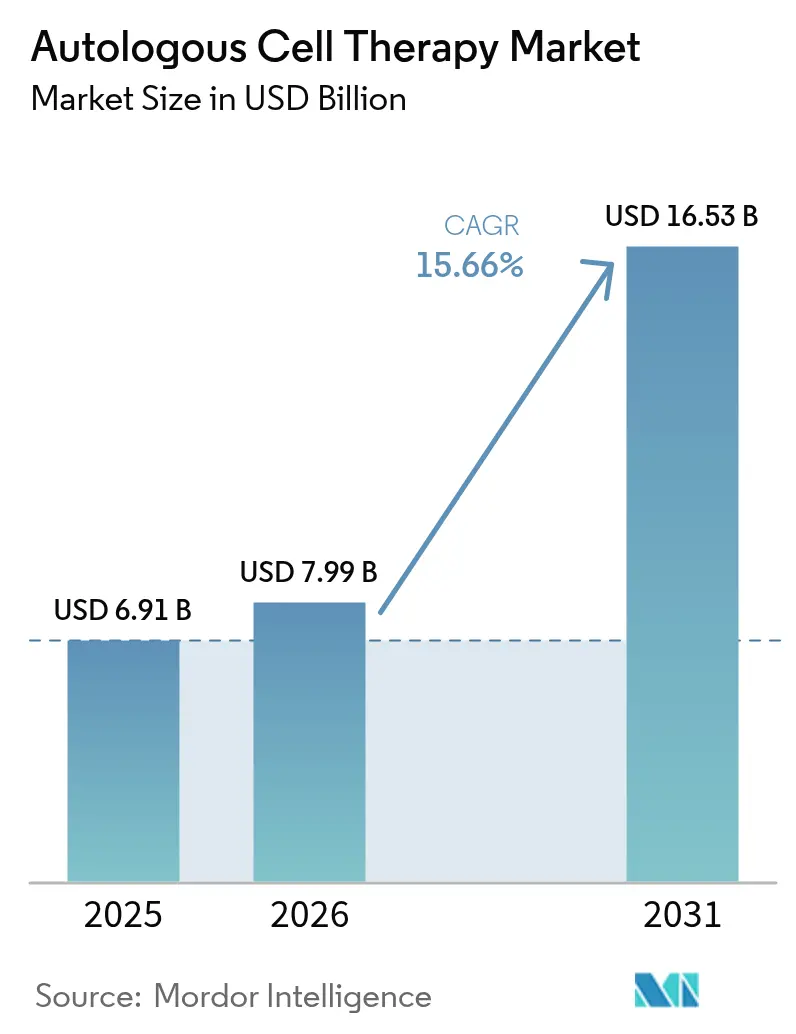

| Market Size (2026) | USD 7.99 Billion |

| Market Size (2031) | USD 16.53 Billion |

| Growth Rate (2026 - 2031) | 15.66% CAGR |

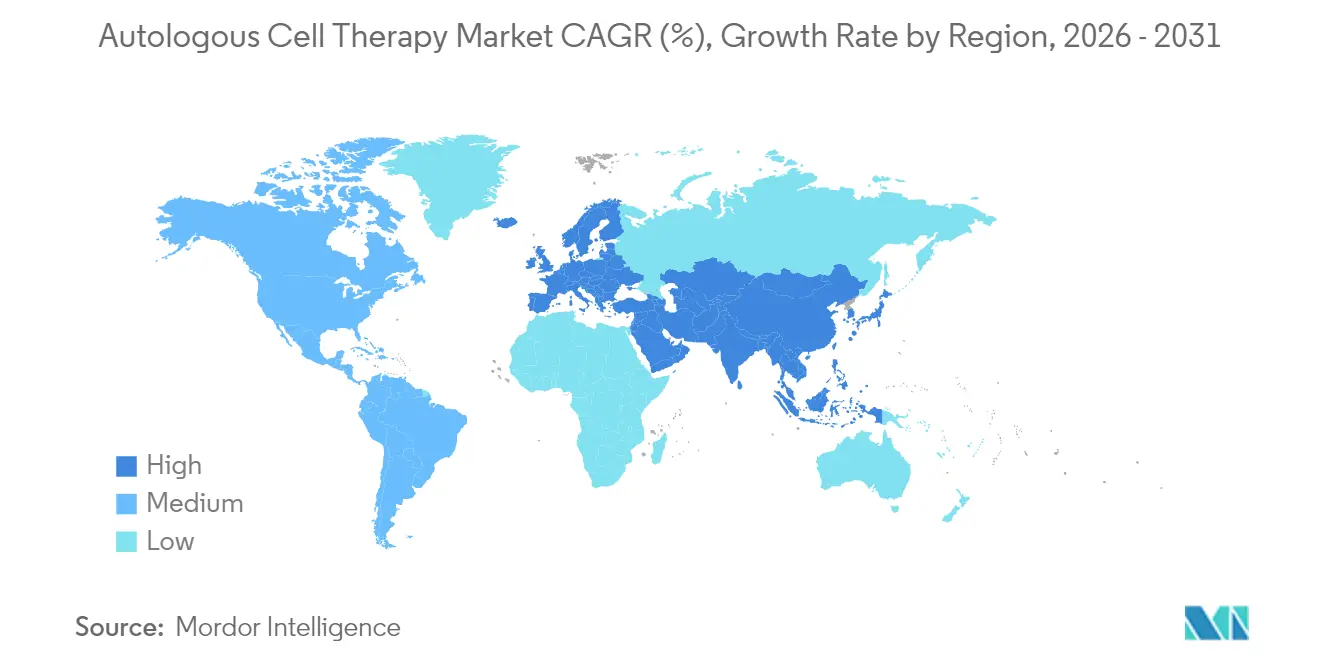

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

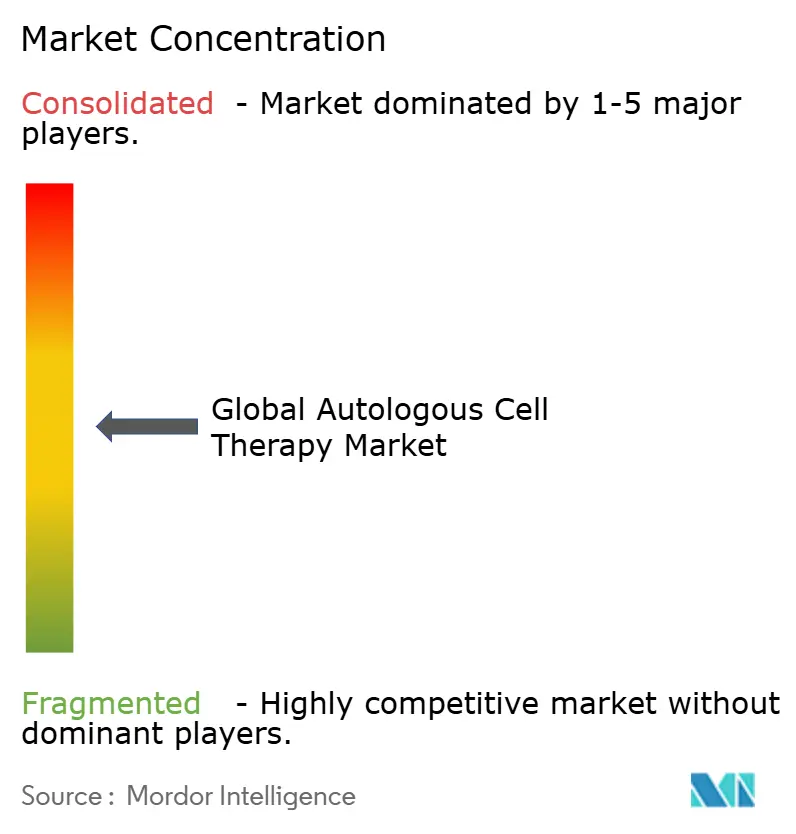

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Autologous Cell Therapy Market Analysis by Mordor Intelligence

The autologous cell therapy market size was valued at USD 6.91 billion in 2025 and estimated to grow from USD 7.99 billion in 2026 to reach USD 16.53 billion by 2031, at a CAGR of 15.66% during the forecast period (2026-2031). Heightened clinical adoption of patient-specific CAR-T products, rapid scale-up of point-of-care micro-factories, and United States FDA RMAT designations that cleared eight cell and gene therapies in 2024 underpin this acceleration[1]Source: U.S. Food and Drug Administration, “CAR-T Cell Products Guidance,” fda.gov. Competitive intensity has increased as pharmaceutical majors acquire automation assets to shorten vein-to-vein time from weeks to days, while outcomes-based contracts in Europe and Japan address payer concerns over single-administration costs exceeding USD 400,000 per patient. North America continues to command the largest regional position in the autologous cell therapy market at 53.34%, but Asia-Pacific is expanding the fastest at an 18.01% CAGR on the back of regulatory modernization and lower manufacturing overheads.

Key Report Takeaways

- By therapy modality, immune-cell products captured 43.12% of autologous cell therapy market share in 2025 while registering the highest CAGR of 16.98% through 2031.

- By application, oncology led with 35.26% revenue share in 2025; autoimmune disorders are forecast to expand at a 15.92% CAGR to 2031.

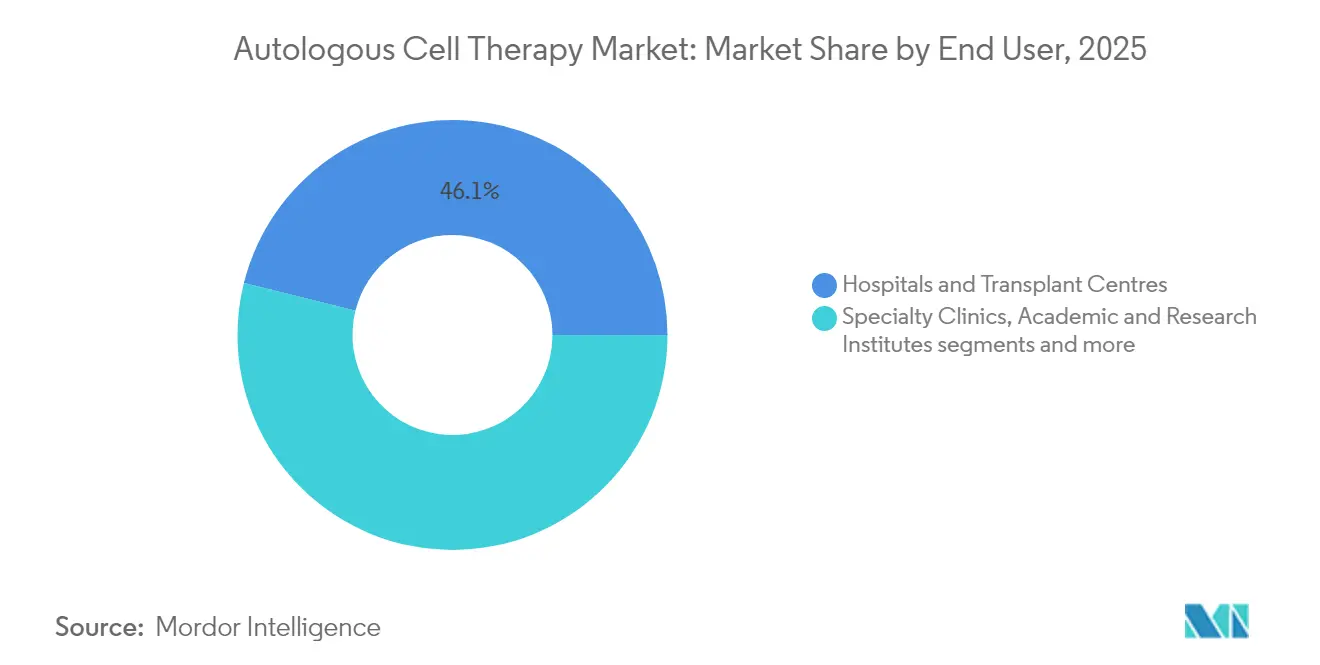

- By end user, hospitals and transplant centers accounted for 46.12% of the autologous cell therapy market size in 2025, whereas specialty clinics are poised for the fastest 16.1% CAGR.

- By geography, North America held 52.74% revenue share in 2025; Asia-Pacific is projected to grow at an 17.58% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Autologous Cell Therapy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-approval CAR-T therapy roll-outs worldwide | +2.80% | Global (North America & EU core) | Medium term (2-4 years) |

| Rapid adoption of closed-system point-of-care bioreactors | +2.10% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Expansion of cell-processing micro-factories inside transplant centres | +1.90% | Global, early uptake in major hospitals | Medium term (2-4 years) |

| Emergence of cryopreserved autologous starting-material banks | +1.40% | North America & EU core | Long term (≥ 4 years) |

| Outcomes-based reimbursement pilots in EU & Japan | +1.20% | EU & Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-approval CAR-T Therapy Roll-outs Worldwide

Global deployment of licensed CAR-T products is broadening beyond hematology to autoimmune and solid-tumor indications. Gilead’s anito-cel, positioned for a 2026 launch, targets multiple myeloma with the ambition to convert 20% of inpatient infusions to outpatient settings during pivotal trials. Bristol Myers Squibb’s CD19 NEX-T program applies optimized manufacturing to severe systemic lupus erythematosus, signalling a strategic pivot from oncology into immune reset therapies. A USD 200 million BioNTech–Autolus alliance underscores consolidation around shared production platforms able to support multi-asset pipelines Autolus Therapeutics. Real-world evidence from Kite Pharma confirms that Yescarta can be administered safely in outpatient oncology clinics, reducing bed occupancy and total care costs Kite Pharma. Together, these milestones widen patient access while improving the economic narrative that surrounds the autologous cell therapy market.

Rapid Adoption of Closed-system Point-of-care Bioreactors

Closed, automated bioreactors integrate cell isolation, transduction, and expansion inside a sealed cassette, trimming manual touch-points that previously drove batch failures. Ori Biotech’s IRO platform achieved 69% viral transduction versus 45% in legacy workflows while halving per-dose costs through 25% shorter production cycles[2]Source: Ori Biotech Ltd., “IRO Platform Unveiled at ISCT 2024,” oribiotech.com . Xcell Biosciences reports consistent T-cell outgrowth in its AVATAR Foundry across 50 mL to 1.5 L scale, enabling decentralized runs within hospital cleanrooms. These improvements strengthen supply resilience and create a virtuous feedback loop in the autologous cell therapy market, whereby faster turn-around amplifies clinical adoption.

Expansion of Cell-processing Micro-factories Inside Transplant Centres

Hospitals are commissioning compact, fully-enclosed suites that allow bedside collection, automated culture, and same-site reinfusion. Orgenesis’s OMPUL mobile unit demonstrates the ability to produce GMP-grade doses at a patient’s location, reducing inter-continental shipping costs that historically added USD 35,000 per lot Orgenesis. Spain’s public CAR-T program attained a 94% manufacturing success rate using on-site platforms, equal to commercial facilities but with shorter waitlists Frontiers in Immunology. Such micro-factory proliferation enhances geographic equity and accelerates growth of the autologous cell therapy market.

Emergence of Cryopreserved Autologous Starting-material Banks

Long-term storage below −120 °C safeguards cell potency, enabling multiple collections before scheduling manufacturing windows. Cytotherapy reports that dry-ice transport maintained 85% viability of mesenchymal stromal cells during COVID-19 air-cargo disruptions Cytotherapy. Stem Cells Translational Medicine identifies banking as especially valuable for heavily pre-treated oncology patients whose first apheresis often yields sub-therapeutic cell counts Stem Cells Translational Medicine. Building inventory bridges collection variability and de-risks batch scheduling across the autologous cell therapy market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost & limited economies of scale | −3.2% | Global, acute in emerging markets | Long term (≥ 4 years) |

| Complex vein-to-vein logistics & QC bottlenecks | −2.4% | Global, infrastructure dependent | Medium term (2-4 years) |

| Scarcity of viable cells in heavily pre-treated oncology patients | −1.8% | Global, advanced care settings | Short term (≤ 2 years) |

| Inter-patient cellular phenotype variability | −1.6% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost & Limited Economies of Scale

Per-patient manufacturing totals GBP 2,260–3,040 versus GBP 930–1,140 for allogeneic options due to donor-specific screening, unique batch records, and low equipment utilization BioPharm International. Mobilization procedures average USD 10,605, with merely 20% of candidates achieving optimal CD34+ cell yields without adverse events Nature Blood & Marrow Transplantation. Until automation neutralizes labor intensity, high cost tempers diffusion of the autologous cell therapy market.

Complex Vein-to-Vein Logistics & QC Bottlenecks

Therapies must remain below −120 °C; short-term excursions to −80 °C can drop viability by 30% according to Cytotherapy shipping audits Cytotherapy. Each patient batch undergoes full sterility and identity testing, extending release time by up to seven days PubMed. Delays adversely impact patients with rapidly progressing disease and constrain the autologous cell therapy market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Modality: Immune Cells Drive Market Evolution

Immune-cell products held 43.12% of autologous cell therapy market share in 2025, growing at a 16.98% CAGR as CAR-T, TCR-T, and tumor-infiltrating lymphocyte therapies validate curative potential beyond hematology. Breakthroughs such as next-generation CD19 constructs with shortened culture times underpin rising clinical confidence. Meanwhile, natural-killer cell programs trialed in refractory solid tumors promise broader immune coverage yet retain autologous compatibility advantages.

Stem-cell modalities remain integral through hematopoietic transplantation and mesenchymal stem cell (MSC) applications in inflammatory disorders. FDA clearance of remestemcel-L in 2025 gave MSC therapies their first pediatric GVHD label, revitalizing investor appetite. Induced pluripotent stem cell pipelines target ischemic cardiomyopathy but will require cost-of-goods below USD 80,000 per dose to compete with existing options. Gene-modified non-immune cells occupy niche regenerative segments, benefiting from CRISPR-Cas precision yet facing extensive release testing demands.

By Application: Oncology Leadership Faces Autoimmune Challenge

Oncology accounted for 35.26% of the autologous cell therapy market size in 2025, anchored by CAR-T success in large B-cell lymphomas. Durable remissions exceeding 50% at five years keep oncology at the revenue apex, though manufacturing failures in heavily pre-treated cohorts remain a headwind. Pipeline diversification into solid tumors—supported by micro-environment-targeted conditioning agents—is expected to fortify near-term growth.

Autoimmune disorders, however, project the fastest 15.92% CAGR as early phase data in systemic lupus erythematosus and multiple sclerosis demonstrate immune-reset potential with reduced relapse rates. If pivotal trials confirm durable efficacy, the autologous cell therapy market could see autoimmune indications eclipse oncology contributions beyond 2030. Cardiovascular, orthopedic, and neurological segments add steady incremental demand as cell-based tissue repair protocols mature.

By End User: Hospitals Anchor While Clinics Accelerate

Hospitals and transplant centers controlled 46.12% of autologous cell therapy market share in 2025, owing to embedded apheresis units, cryogenic storage, and intensive-care support for cytokine release syndrome management. Their dominance will persist as academic centers pioneer decentralized manufacturing models that integrate class C clean-rooms with automated bioreactors, compressing turnaround to five days for certain hematology protocols.

Specialty clinics are the fastest-growing channel amid improving outpatient safety profiles. Real-world Kite Pharma data verified that grade ≥3 adverse events in ambulatory settings mirror inpatient incidence, enabling payers to reimburse lower facility fees. Contract development and manufacturing organizations quietly underpin both channels by offering plug-and-play GMP suites that offload capital burdens from providers, further broadening the autologous cell therapy market footprint.

Geography Analysis

North America maintained 52.74% of autologous cell therapy market share in 2025, propelled by Medicare’s CGT Access Model that reimburses approved products contingent on registry data collection CMS. The region’s robust CDMO network shortens supply lines, and FDA’s Office of Therapeutic Products expects 10–20 annual approvals by 2025, sustaining leadership.

Asia-Pacific recorded the highest 17.58% CAGR owing to supportive regulation under Japan’s fast-track Sakigake program and China’s provincial insurance pilots that now cover select CAR-T therapies. Localized micro-factories dampen logistics costs by up to 40%, an essential factor in emerging economies. India leverages medical tourism, while Australia and South Korea invest in regional GMP hubs, further enlarging the autologous cell therapy market.

Europe grows steadily as managed entry agreements align multi-year payments with clinical benefit. Germany’s NUB reimbursement path grants temporary funding ahead of formal price negotiation, easing market access hurdles. Eastern Europe and Russia remain nascent but represent long-run whitespace as regulatory clarity improves.

Competitive Landscape

Competition is moderate; the five largest license holders command an estimated 55% combined revenue. Novartis expands Kymriah into follicular lymphoma, while Gilead/Kite advances anito-cel toward commercialization in multiple myeloma. Bristol Myers Squibb differentiates via autoimmune programs, securing pipeline depth outside crowded hematology spaces. BioNTech’s USD 200 million investment in Autolus exemplifies vertical integration to secure manufacturing capacity.

Strategic moves center on automation. Cellular Origins partnered with Cytiva to pair the Constellation robotic cluster with Sefia cell-processing hardware, targeting GMP deployment by late 2025 BioPharm International. Terumo BCT’s Quantum Flex system cuts harvest labor by 60%, appealing to hospital-owned facilities that lack extensive staff Pharmaceutical Manufacturer.

Emerging disruptors such as Ori Biotech and Orgenesis address cost and access constraints through modular platforms that can be deployed in underutilized hospital spaces. Lonza Group and Minaris scale out reserved suites for late-phase trials, de-risking capacity for mid-tier sponsors. Collectively, these dynamics accelerate clinical penetration and reinforce the growth trajectory of the autologous cell therapy market.

Autologous Cell Therapy Industry Leaders

Vericel Corporation

Pharmicell Co., Inc.

Holostem Terapie Avanzate S.r.l.

Opexa Therapeutics

Lineage Cell Therapeutics, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Kite Pharma presents real-world Yescarta outpatient data at ASCO 2025, confirming safety parity with inpatient care.

- May 2025: University of Colorado reveals ALA-CART next-generation CAR-T efficacy against resistant cancers, with clinical trials planned.

- April 2025: Throne Biotechnologies secures FDA RMAT for Stem Cell Educator therapy targeting Type 1 diabetes and Long COVID.

- January 2025: Cytiva partners with Cellular Origins to integrate Sefia with Constellation robotic cluster for CGT automation.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the autologous cell therapy market as all therapeutic products and related services in which a patient's own viable cells are harvested, expanded, or otherwise engineered outside the body and then reinfused to repair, replace, or regenerate diseased tissues. According to Mordor Intelligence, this market generated USD 6.91 billion in 2025.

We deliberately exclude allogeneic, xenogeneic, and acellular gene-editing therapies from scope.

Segmentation Overview

- By Therapy Modality (Value)

- Stem Cell Therapies

- Hematopoietic Stem Cells (HSC)

- Mesenchymal Stem Cells (MSC)

- Induced Pluripotent Stem Cells (iPSC)

- Immune Cell Therapies

- CAR-T Cells

- TCR-T Cells

- Tumour-Infiltrating Lymphocytes (TIL)

- Natural Killer (NK) Cells

- Gene-Modified Non-immune Cell Therapies

- Stem Cell Therapies

- By Application (Value)

- Oncology

- Cardiovascular Diseases

- Orthopaedic & Musculoskeletal Disorders

- Neurology

- Dermatology & Wound Healing

- Auto-immune Disorders

- Others

- By End User (Value)

- Hospitals & Transplant Centres

- Specialty Clinics

- Academic & Research Institutes

- Others

- By Geography (Value)

- North America

- United States

- Canada

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

During this stage, we conduct semi-structured interviews with transplant surgeons, cell-processing facility managers, payers, and technology vendors across North America, Europe, and Asia. Insights on treated patient counts, manufacturing yield, turnaround time, and average selling price enable Mordor analysts to refine desk-based assumptions and reconcile early model outputs.

Desk Research

We start with structured desk work that pulls annual transplant statistics from agencies such as the Center for International Blood and Marrow Transplant Research, regulatory approval logs from the US FDA, EMA, and PMDA, import-export records mined through Volza for critical reagents, and cost benchmarks reported in peer-reviewed journals like Cytotherapy.

We also review company 10-K filings, clinical-trial registries, Alliance for Regenerative Medicine updates, and subscription feeds from D&B Hoovers and Dow Jones Factiva to map commercial launches and revenue splits. We consider the sources listed as illustrative only; many additional open databases are consulted for data collection, validation, and clarification.

Market-Sizing & Forecasting

Our model employs a top-down patient-pool framework that begins with treated prevalence of key indications and marries it with therapy penetration rates and typical dose costs. Results are then balanced with selective bottom-up checks that use sampled batch volumes from licensed manufacturers to validate totals. Key variables include incidence of hematologic cancers, manufacturing yield loss, regulatory approval cadence, average selling price erosion after launch, and reimbursement expansion timelines. We project each driver through 2030 with multivariate regression, and scenario analysis tests policy shocks. Where facility-level data are thin, we impute calibrated industry averages, flag them, and review them in peer sessions.

Data Validation & Update Cycle

Outputs pass a two-layer review that screens for anomalies against historical transplant ratios, currency movements, and comparable therapy benchmarks. Our analysts revisit any variance before sign-off. Reports refresh annually, and a landmark approval or major safety alert triggers a mid-cycle update followed by a fresh validation pass.

Why Mordor's Autologous Cell Therapy Baseline Is Dependable

We acknowledge that published estimates often diverge because firms mix autologous and allogeneic revenue streams, apply dissimilar pricing, or work with outdated patient pools.

Mordor's disciplined scope, variable selection, and yearly refresh deliver a balanced midpoint clients can trust.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 6.91 B | Mordor Intelligence | - |

| 11.43 B | Global Consultancy A | Combines autologous revenue with ancillary processing kits and models uptake on announced capacity rather than realized throughput |

| 6.74 B | Industry Publication B | Uses transplant counts only and omits immune-cell oncology revenue outside accredited centers, yielding partial coverage |

In sum, Mordor's clearly bounded scope, transparent variable selection, and recurring validation create a reliable baseline that bridges overly optimistic and narrowly conservative figures, giving decision-makers a reproducible reference point.

Key Questions Answered in the Report

What is the global value of the autologous cell therapy market in 2026?

The market was valued at USD 7.99 billion in 2026 and is forecast to reach USD 16.53 billion by 2031.

Which therapy modality currently leads the autologous cell therapy market?

Immune-cell products, particularly CAR-T therapies, hold the lead with 43.12% revenue share.

Why is Asia-Pacific the fastest-growing region?

Regulatory reforms, expanding clinical infrastructure, and lower production costs drive an 17.58% CAGR in Asia-Pacific.

How are payers addressing high upfront costs of autologous therapies?

European and Japanese health systems use outcomes-based reimbursement, linking payments to long-term clinical success.

What manufacturing innovations are reducing costs?

Closed-system bioreactors and hospital-based micro-factories cut labor and logistics costs, lowering per-dose expenses by up to 50%.

Page last updated on: