Hematology Analyzers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

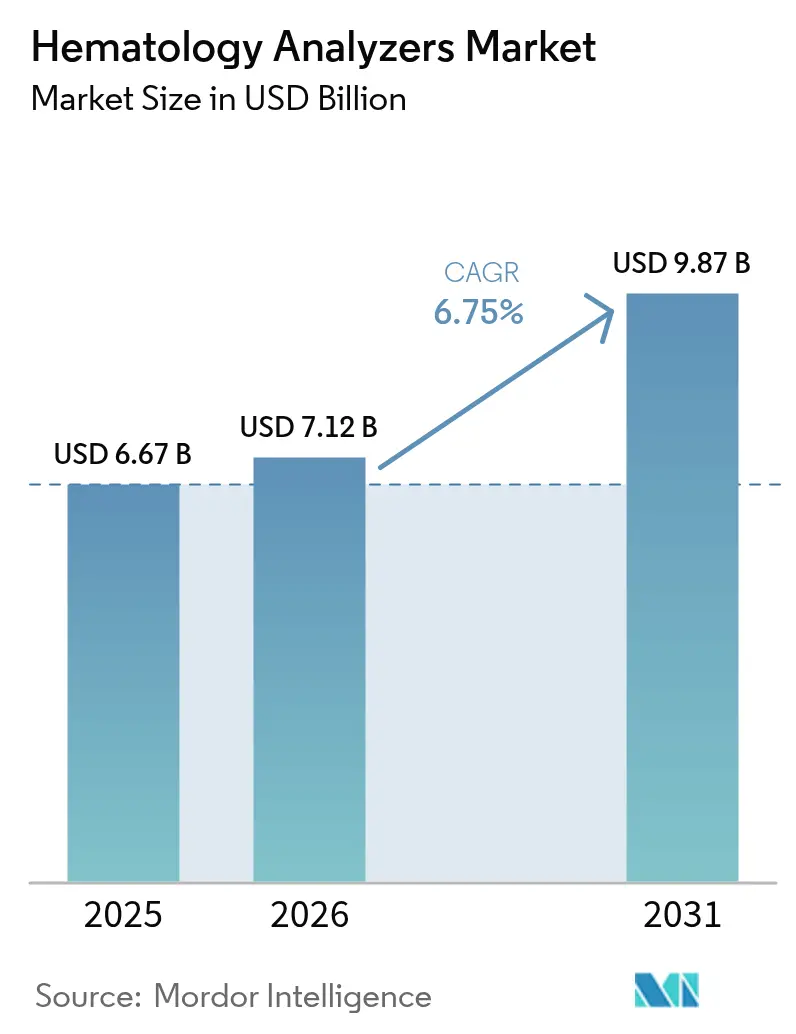

| Market Size (2026) | USD 7.12 Billion |

| Market Size (2031) | USD 9.87 Billion |

| Growth Rate (2026 - 2031) | 6.75% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

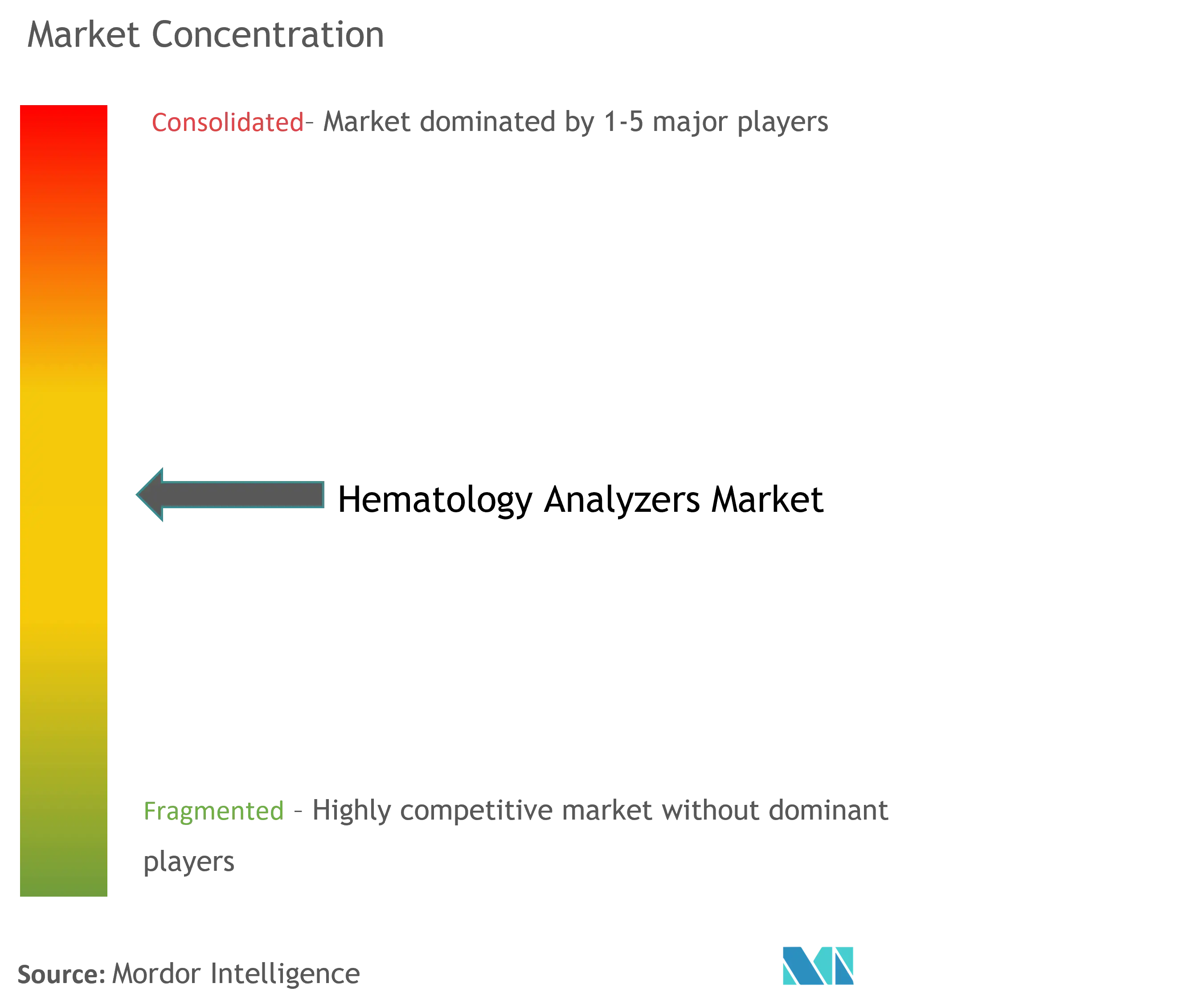

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hematology Analyzers Market Analysis by Mordor Intelligence

Hematology analyzers market size in 2026 is estimated at USD 7.12 billion, growing from 2025 value of USD 6.67 billion with 2031 projections showing USD 9.87 billion, growing at 6.75% CAGR over 2026-2031. Continued growth rests on three structural shifts: rapid migration from 3-part to 5- and 6-part differential systems across middle-income nations, public-sector screening mandates for neonatal and geriatric disorders, and steady integration of artificial-intelligence tools that merge morphology, flow cytometry, and chemistry data into a single workcell. Upstream, reagent consumption accelerates because advanced differentials require proprietary diluents, surfactants, and calibrators, locking laboratories into long-term supply contracts. Downstream, hospital consolidation and the rise of centralized mega-labs intensify demand for high-throughput automation that can clear two-hour turnaround targets while maintaining traceability across multi-site networks. Finally, AI-powered pre-classification slashes manual smear review times, mitigating technologist shortages and lifting analyzer utilization rates, a trend most pronounced in North America and increasingly visible across top-tier Chinese and Indian reference labs.

Key Report Takeaways

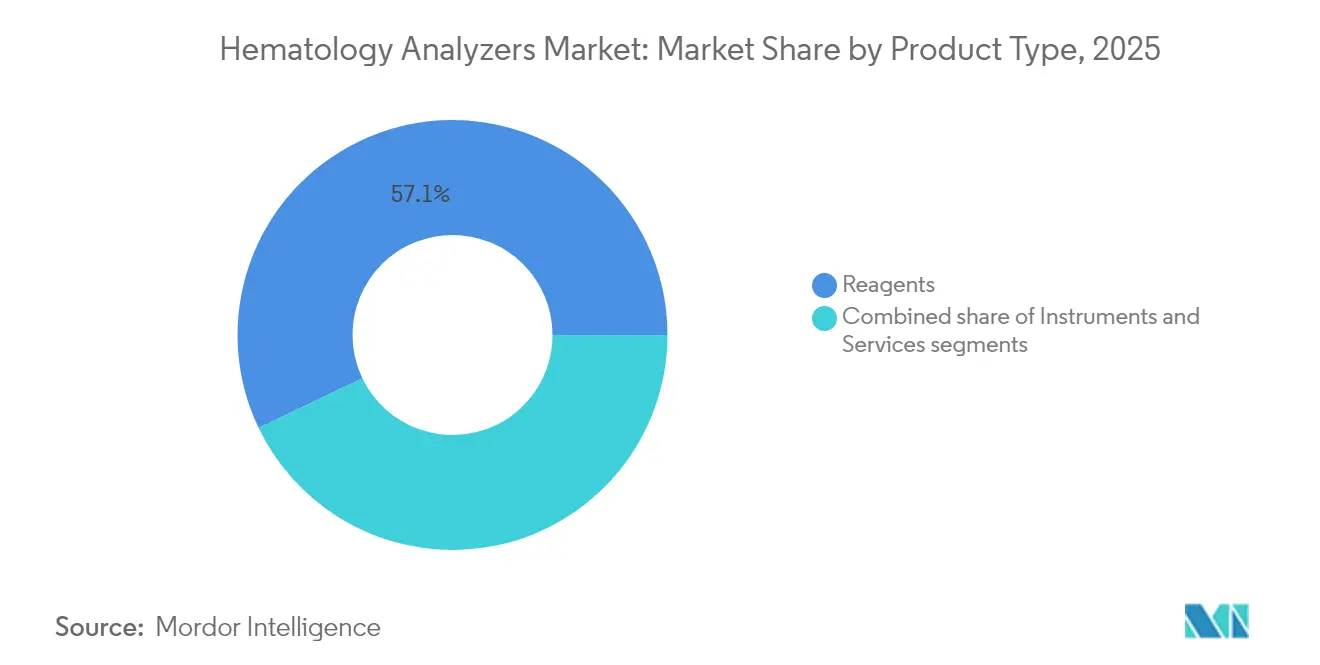

- By product type, reagents captured 57.12% of global revenue in 2025 and are projected to expand at an 8.15% CAGR through 2031.

- By modality, fully automated systems remained the dominant platform in 2024, processing the highest daily sample volumes; semi-automated models showed lower uptake and no separate growth figure was reported.

- By end user, hospital laboratories commanded the greatest share of test volumes in 2024, while commercial reference providers represented the quickest-expanding customer group even though a specific CAGR was not disclosed.

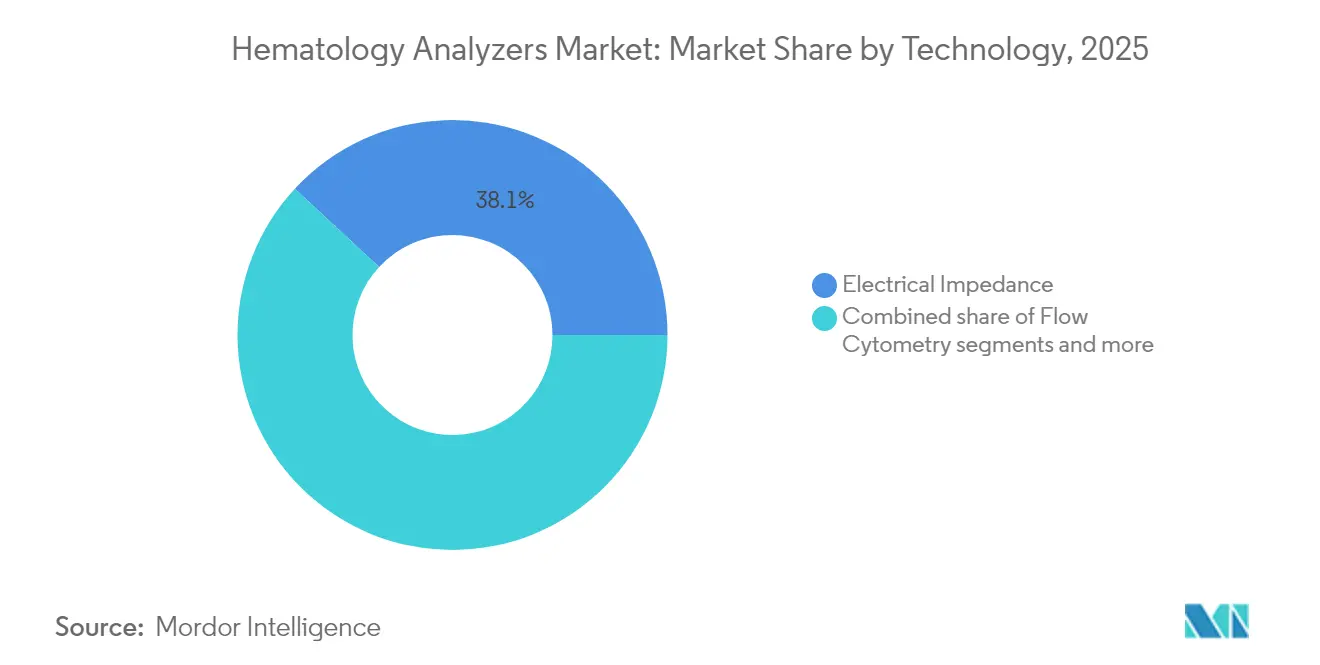

- By technology, electrical impedance led with 38.10% revenue share in 2025; flow cytometry platforms posted the fastest adoption pace, although a quantified CAGR was not provided.

- By application, anemia testing accounted for 37.45% of 2025 sales, whereas blood-cancer diagnostics is projected to expand at a 7.55% CAGR to 2031.

- By geography, North America held 39.85% of global revenue in 2025, while Asia-Pacific is forecast to register a 6.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hematology Analyzers Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of hematologic disorders | +1.8% | North America, Europe | Long term (≥ 4 years) |

| Adoption of 5- & 6-part analyzers in mid-income nations | +1.2% | Asia-Pacific, Latin America, MEA | Medium term (2-4 years) |

| Consolidation of central-lab networks | +0.9% | North America, EU | Medium term (2-4 years) |

| Shift toward integrated hematology-chemistry workcells | +0.7% | Global | Long term (≥ 4 years) |

| AI-driven pre-classification | +1.1% | Developed markets | Short term (≤ 2 years) |

| Government neonatal screening mandates | +0.8% | Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Hematologic Disorders

Escalating prevalence of leukemias, lymphomas, and myelomas fuels sustained demand for advanced differential analysis. Cancer registries in high-income countries recorded another uptick in non-Hodgkin lymphoma cases during 2024 despite plateaued mortality, underscoring the need for sensitive cell-flagging algorithms that standard 3-part instruments cannot deliver. Aging populations compound testing volume; Medicare beneficiaries exhibited a 2.68% blood-cancer diagnosis rate versus 0.31% among employer-insured cohorts in 2024, demonstrating how demographic load alone steers analyzer upgrades. Laboratories therefore prioritize platforms that integrate high-resolution optical pathways, AI classifiers, and digital reporting to reduce false negatives and accelerate therapeutic decisions.

Growing Adoption of 5- & 6-Part Differential Analyzers in Mid-Income Countries

Governments in China, India, Brazil, and Egypt accelerate infrastructure modernization programs that replace legacy 3-part devices with five-class or six-class leukocyte systems. Economic modeling shows point-of-care HbA1c screening via advanced analyzers to be cost-effective across urban and rural health centers in China, creating parallels for hematology rollouts. Vendors capitalize by bundling multi-year reagent contracts and remote-service packages, establishing recurring revenue streams within these high-growth territories.

Consolidation of Central-Lab Networks in the U.S. & EU

Hospital mergers and private-equity roll-ups shrink the overall count of independent clinical labs but sharply raise average daily test volume per site. Large networks demand high-throughput analyzers able to auto-route samples, auto-verify results, and deliver consistent performance across geographically dispersed draw centers. Labcorp’s continental workflow demonstrates the scale benefit: standardized platforms lower per-test costs and reinforce purchasing power when negotiating reagent supply agreements.

AI-Driven Pre-Classification Reducing Review Time

Artificial-intelligence modules now achieve 91% sensitivity for myeloblasts and 88% for atypical lymphocytes in routine smears, cutting manual review time by more than half in early adopter labs. This capability counters persistent shortages of medical technologists and reduces overtime bills. Early installations also show a measurable drop in slide retries, boosting analyzer uptime and throughput.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital budget freezes at sub-200-bed hospitals | -1.4% | Global, with highest impact in rural and community hospitals | Medium term (2-4 years) |

| Re-use of refurbished analyzers in South America | -0.6% | South America core, with spillover to other emerging markets | Medium term (2-4 years) |

| Shortage of qualified hematopathologists slowing test menu expansion | -0.8% | Global, with acute shortages in developing regions | Long term (≥ 4 years) |

| Supply-chain fragility for semiconductor flow cells | -0.5% | Global, with highest impact during geopolitical tensions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Capital Budget Freezes at Sub-200-Bed Hospitals

Community hospitals confront rising labor expenses and declining reimbursements, pushing capital projects to the back burner. Vacancy surveys reveal double-digit staffing gaps across laboratory departments, making it difficult for boards to justify million-dollar analyzer replacements. Smaller facilities therefore stretch service contracts on aging devices, increasing downtime risk and limiting access to advanced diagnostics for rural populations.

Shortage of Qualified Hematopathologists Slowing Test Menu Expansion

An estimated deficit of 20,000–25,000 U.S. lab technologists constrains the rollout of complex abnormal-cell assays even when new analyzers are installed. Attrition has only deepened the talent shortfall, leaving many labs unable to exploit extended test menus that differentiate next-generation platforms. Continued workforce pressure threatens to mute near-term revenue upside from premium analyzers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Reagents Sustain Recurring Revenue Momentum

Reagents generated 57.12% of the hematology analyzers market size in 2025, driven by test-volume growth and proprietary formulations that tie customers to a single vendor. Their predictable replacement cycle underpins an 8.15% CAGR through 2031, outpacing hardware additions as central labs maximize instrument utilization before purchasing new units. Advanced surfactant mixes, nucleic-acid dyes, and stabilization buffers tailored to AI-based morphology further lift average selling prices and margin profile.

Instrument revenues trail reagent contribution yet remain pivotal to platform penetration, particularly as mid-income buyers leapfrog to 5-part systems that promise lower per-test reagent consumption over time. Point-of-care analyzers carve a niche in trauma bays and oncology infusion centers, offering 60-second turnaround albeit at premium reagent costs. Services, though the smallest slice, gain strategic weight because algorithm updates and remote-performance monitoring are now mission-critical for sustaining AI classifier accuracy.

By Modality: Fully Automated Systems Command Laboratory Workflows

Automated instruments accounted for the dominant value share in 2024 as central labs chased consistency, barcode-driven traceability, and 98% first-pass accuracy benchmarks. The hematology analyzers market share for automated units is set to widen further as “dark-lab” concepts move from pilot to production, leveraging robotics that load racks 24/7 without human intervention. Semi-automated models retain relevance inside satellite clinics and blood banks with unpredictable workflows or tight capital budgets.

AI-infused autotesting pushes error-rate curves downward, freeing technologists for manual differentials on flagged samples. In parallel, vendors bundle cloud dashboards that benchmark analyzer utilization across sites, enabling multi-hospital groups to redeploy under-used units rather than approve new purchases. This asset-optimization logic locks customers further into vendor ecosystems, reinforcing lifetime value of each hardware install.

By End User: Hospital Laboratories Anchor Testing Volume

Hospital labs handle the bulk of inpatient and outpatient CBCs, creating scale economics that justify high-end analyzers with integrated slide makers. Their procurement committees increasingly adopt enterprise-wide refresh cycles that synchronize hematology, chemistry, and immunoassay platforms every eight years, a cadence favored by service-agreement pricing models. Commercial reference providers grow faster in percentage terms, outsourcing coagulation and advanced flow panels for smaller hospitals and physician offices lacking subspecialty personnel.

Academic and research centers demand open-tube sampling ports, advanced flagging, and raw-data export for clinical-trial protocols, making them early adopters of digital-imaging enhancements. Blood banks favor analyzers certified for donor screening with low carryover coefficients and high red-cell impedance resolution. Collectively, these distinct requirements push vendors to maintain multi-form-factor portfolios that cover bedside cartridges through 500-sample-per-hour automation lines.

By Technology: Electrical Impedance Retains Leadership Amid Hybrid Innovation

Electrical impedance contributed 38.10% revenue in 2025 because of its low cost per test and rugged design suited to high-volume environments. Flow cytometry, although more expensive, climbs fastest as immunophenotyping becomes core to oncology pathways. Portable magnetic flow cytometry prototypes now promise CD4 counts at the point of care, signaling future opportunities in primary-care clinics.

Laser scattering and fluorescence occupy specialty niches such as body-fluid cell counts, while digital imaging bridges gap by pairing high-resolution slide scans with AI morphology. Imaging flow cytometry blends the best of both worlds, capturing quantitative fluorescence signals alongside cell photographs, enabling single-cell analytics at throughputs close to classical impedance counters. Vendors therefore pursue hybrid pipelines that embed multiple detection channels within a single chassis, widening addressable menus without multiplying footprint.

By Application: Anemia Dominates, Oncology Drives Incremental Growth

Anemia panels produced 37.45% of global revenue in 2025 thanks to universal reliance on CBCs across inpatient, outpatient, and preventive-care settings. Their absolute volume secures reagent pull-through even in low-incidence geographies. Conversely, blood cancer diagnostics, posting a 7.55% CAGR, adds high-margin incremental tests that demand advanced immunophenotyping and digital imaging capabilities.

Hemorrhagic-condition monitoring remains a steady revenue contributor, particularly within surgical centers deploying platelet mapping and viscoelastic testing. Genetic disorder panels expand as hereditary anemia and thalassemia screening programs mature; India’s multicenter sickle-cell cohort alone will screen multiple million newborns annually by 2027. Infection detection benefits from sepsis-alert algorithms that track left-shift patterns and immature granulocytes, further lifting analyzer usage during emergency-department surges.

Geography Analysis

North America held 39.85% of global sales in 2025 and continues to prioritize integrated workcells that link hematology, chemistry, and molecular assays through unified middleware. Medicare reimbursement reforms, including new DRGs for gene therapies, indirectly bolster demand for precision CBC parameters used in eligibility and toxicity monitoring. Canada and Mexico add incremental growth as provincial modernization funds and private-sector expansions replace aging 3-part counters with AI-ready instruments.

Asia-Pacific, expanding at a 6.95% CAGR, gains momentum from demographic weight and public-health mandates. China’s 8.95% thalassemia carrier prevalence pushes provincial funding for mass-screening networks equipped with mid-tier analyzers that can process 120 samples per hour while maintaining cost discipline. India’s national sickle-cell elimination mission uses a hub-and-spoke model where high-throughput systems in district hospitals receive dried blood-spot cards from rural clinics, a workflow reliant on reagent stability and robust remote diagnostics. Japan and South Korea deploy mature automation suites yet continue to upgrade to AI morphology for workforce efficiency.

Europe demonstrates steady replacement demand complicated by In-Vitro Diagnostic Medical Device Regulation (IVDR) timelines. The 2024/1860 extension gives laboratories breathing room but nudges procurement toward CE-certified platforms supported by rigorous post-market surveillance, advantaging incumbents with deep regulatory expertise. Germany illustrates the automation imperative; MVZ’s adoption of ABB robots boosts sample throughput by 25% and sets a precedent for other high-wage economies.

Competitive Landscape

Industry concentration remains moderate anchored by large installed bases and reagent exclusivity. Sysmex leverages its alliance with CellaVision to secure roughly 85% slice of the U.S. hematology analyzers market, bundling digital-morphology scanners with XN-series counters under unified QC software. Beckman Coulter, Siemens Healthineers, and Abbott Laboratories differentiate via chemistry-hematology integration, enabling single-tube reflex testing for anemia etiologies or oncology protocols.

Strategic M&A reshapes supply dynamics: Advanced Instruments’ USD 2.2 billion takeover of Nova Biomedical extends the buyer into electrolyte and glucose testing, forming a one-stop consumables platform that competes head-to-head with established reagent franchises. Roche deepens vertical integration by committing EUR 600 million to a German reagent megaplant that will internalize 450 core raw materials by 2028, improving supply certainty for its cobas hematology line.

Partnerships with AI specialists accelerate product refresh cycles without heavy R&D spend. Siemens Healthineers’ pact with Scopio Labs embeds full-field digital morphology inside Atellica 2200 units, streamlining smear review and reducing external slide scanners. BD teams with Biosero to integrate robotic liquid handlers onto FACS analyzers, targeting pharma clients who need high-content screening for cell-therapy pipelines. Start-ups exploit white-space by focusing on single-cell analytics or micro-fluidic platforms tuned to decentralized oncology centers, winning Series-A funding on the back of workforce-efficiency metrics.

Hematology Analyzers Industry Leaders

Abbott Laboratories

HORIBA Ltd

Siemens Healthineers

Sysmex Corporation

Danaher Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Scopio Labs introduced an AI-driven platform that fully automates blood-smear morphology, cutting review time by 60%.

- December 2024: Roche broke ground on a EUR 600 million diagnostics production center in Penzberg, Germany, to secure reagent supply across hematology and other disciplines

Global Hematology Analyzers Market Report Scope

As per the scope of this report, hematology analyzers are the equipment used to run tests on blood samples, and they are used in the medical field to determine white blood cell counts, complete blood counts, reticulocyte analysis, and coagulation tests. The Hematology Analyzers market is Segmented by Product (Instruments, Reagents, and Services), End Users (Hospitals, Clinical Laboratories, Research Institutes, and Others), and Geography (North America, Europe, Asia Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Drug-in-adhesive |

| Reservoir |

| Matrix |

| Microneedle-assisted |

| Others |

| Smoking Cessation |

| Hormone Replacement Therapy |

| Pain Management |

| Neurological Disorders |

| Cardiovascular Disorders |

| Contraception |

| Others |

| Acrylate Adhesives |

| Silicone Adhesives |

| Hydrogel Adhesives |

| Other Adhesives |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Release Technology (Value) | Drug-in-adhesive | |

| Reservoir | ||

| Matrix | ||

| Microneedle-assisted | ||

| Others | ||

| By Therapeutic Area (Value) | Smoking Cessation | |

| Hormone Replacement Therapy | ||

| Pain Management | ||

| Neurological Disorders | ||

| Cardiovascular Disorders | ||

| Contraception | ||

| Others | ||

| By Adhesive Technology (Value) | Acrylate Adhesives | |

| Silicone Adhesives | ||

| Hydrogel Adhesives | ||

| Other Adhesives | ||

| By Distribution Channel (Value) | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| Others | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the hematology analyzers market in 2026?

The hematology analyzers market size reached USD 7.12 billion in 2026 and is projected to rise to USD 9.87 billion by 2031.

What annual growth rate is expected for hematology analyzers through 2031?

Global revenue is forecast to grow at a 6.75% CAGR over the 2026-2031 period.

Which product segment generates the highest revenue?

Reagents contribute the largest share, accounting for 57.12% of 2025 sales and expanding at an 8.15% CAGR.

Which geographic region is expanding fastest?

Asia-Pacific leads growth with a projected 6.95% CAGR, supported by national screening mandates and infrastructure upgrades.

How is artificial intelligence changing hematology workflows?

AI-enabled pre-classification flags abnormal cells with 91% sensitivity, cutting manual review time and mitigating technologist shortages.

What recent merger reshaped competitive dynamics?

Advanced Instruments USD 2.2 billion acquisition of Nova Biomedical in 2025 created a diversified platform spanning instruments and consumables.

Page last updated on: