Hemostasis Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

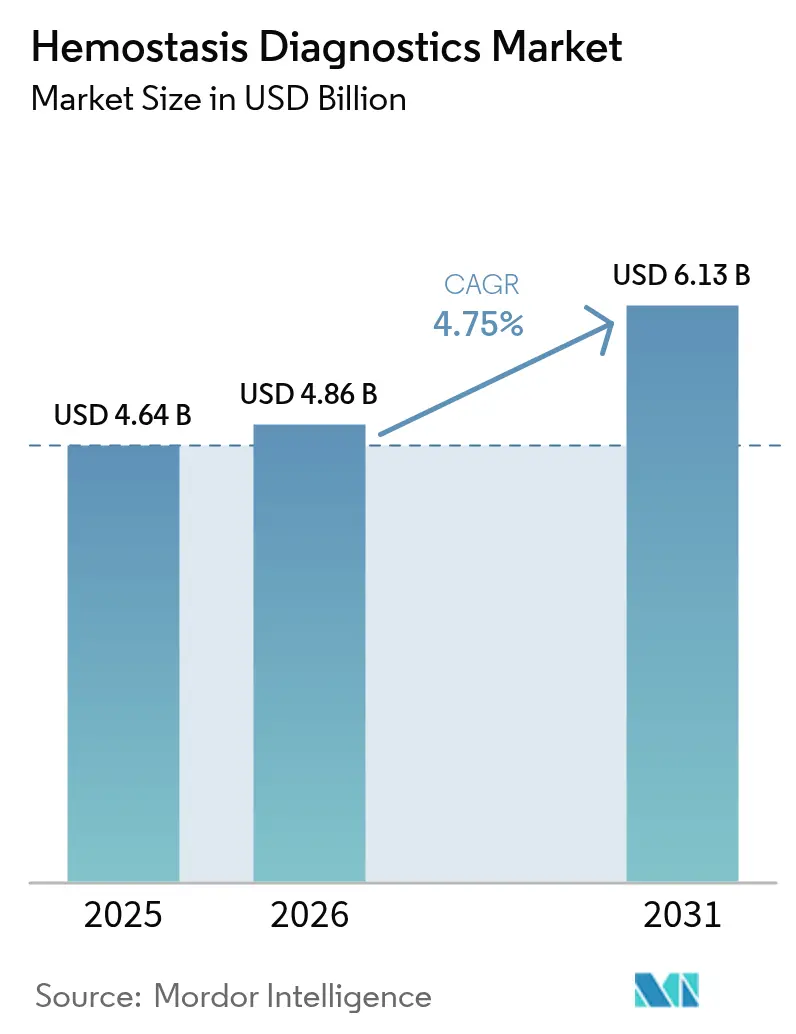

| Market Size (2026) | USD 4.86 Billion |

| Market Size (2031) | USD 6.13 Billion |

| Growth Rate (2026 - 2031) | 4.75% CAGR |

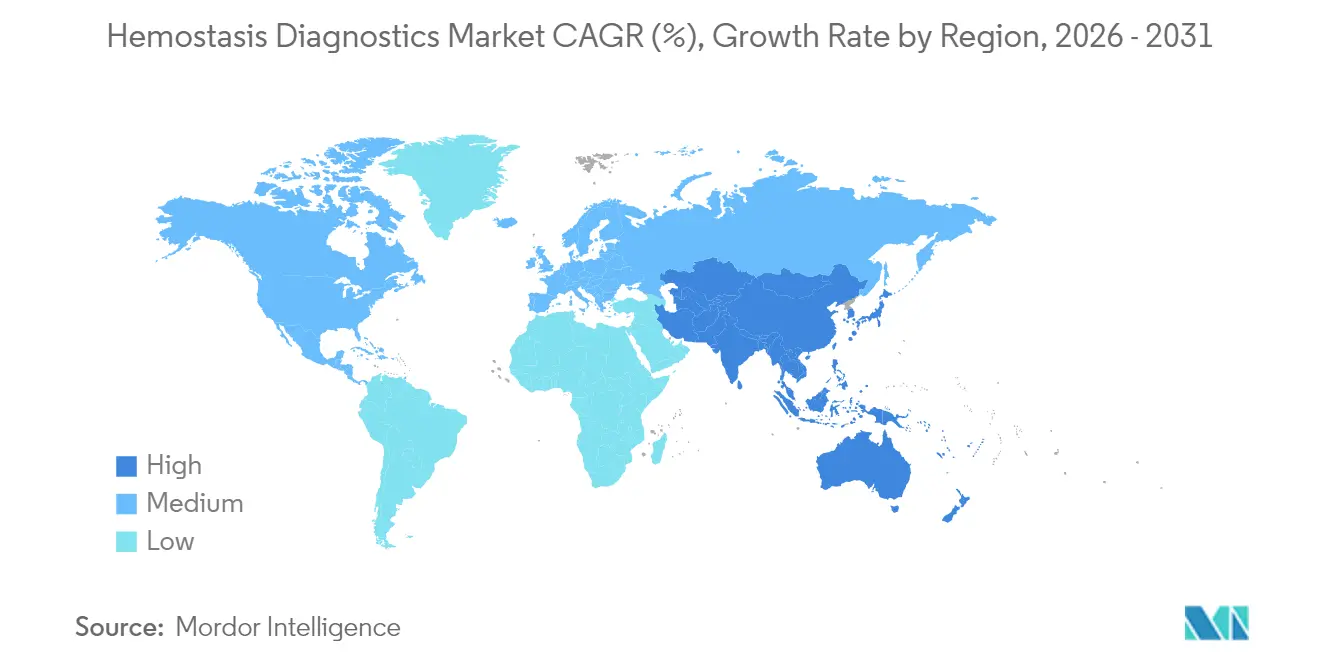

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

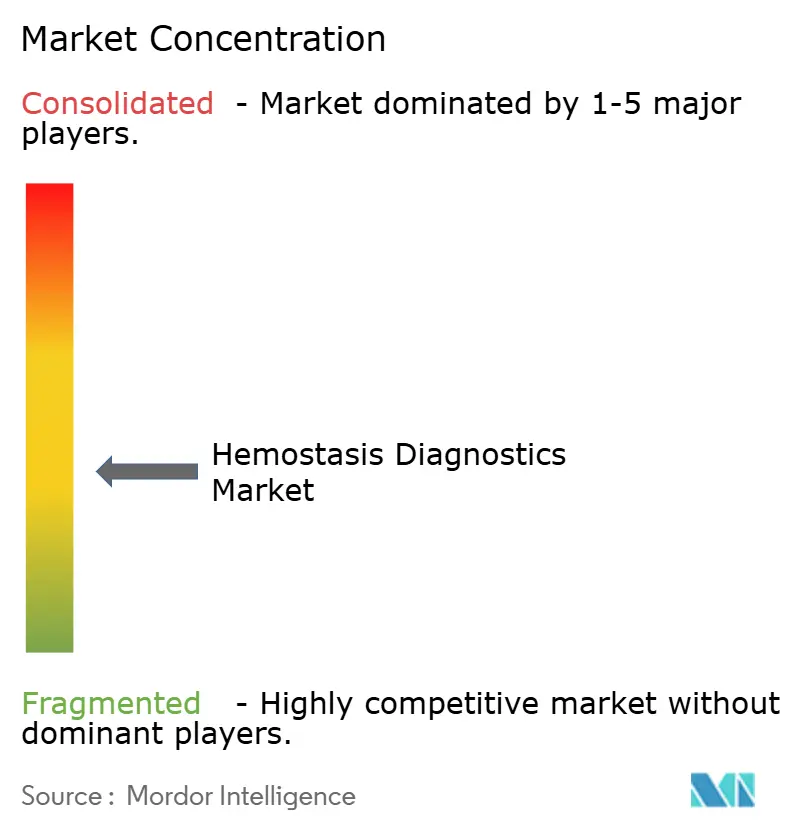

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hemostasis Diagnostics Market Analysis by Mordor Intelligence

The hemostasis diagnostics market size was valued at USD 4.64 billion in 2025 and estimated to grow from USD 4.86 billion in 2026 to reach USD 6.13 billion by 2031, at a CAGR of 4.75% during the forecast period (2026-2031). Demand is buoyed by the rising prevalence of bleeding disorders, rapid uptake of viscoelastic testing platforms, and hospitals’ shift from centralized laboratories to point-of-care coagulation assessments. Automation, microfluidics, and artificial intelligence now underpin new analyzers that deliver reliable results from very small specimen volumes, a feature valued in neonatal, ECMO, and trauma settings. Regulatory tailwinds—including the FDA’s 2025 reclassification of viscoelastic systems into Class II—shorten market-entry timelines, while reimbursement headwinds and interoperability gaps temper the pace of adoption. Competitive intensity increases as suppliers integrate vertically, expand reagent portfolios, and bundle hardware with data-management solutions to secure multiyear laboratory contracts.

Key Report Takeaways

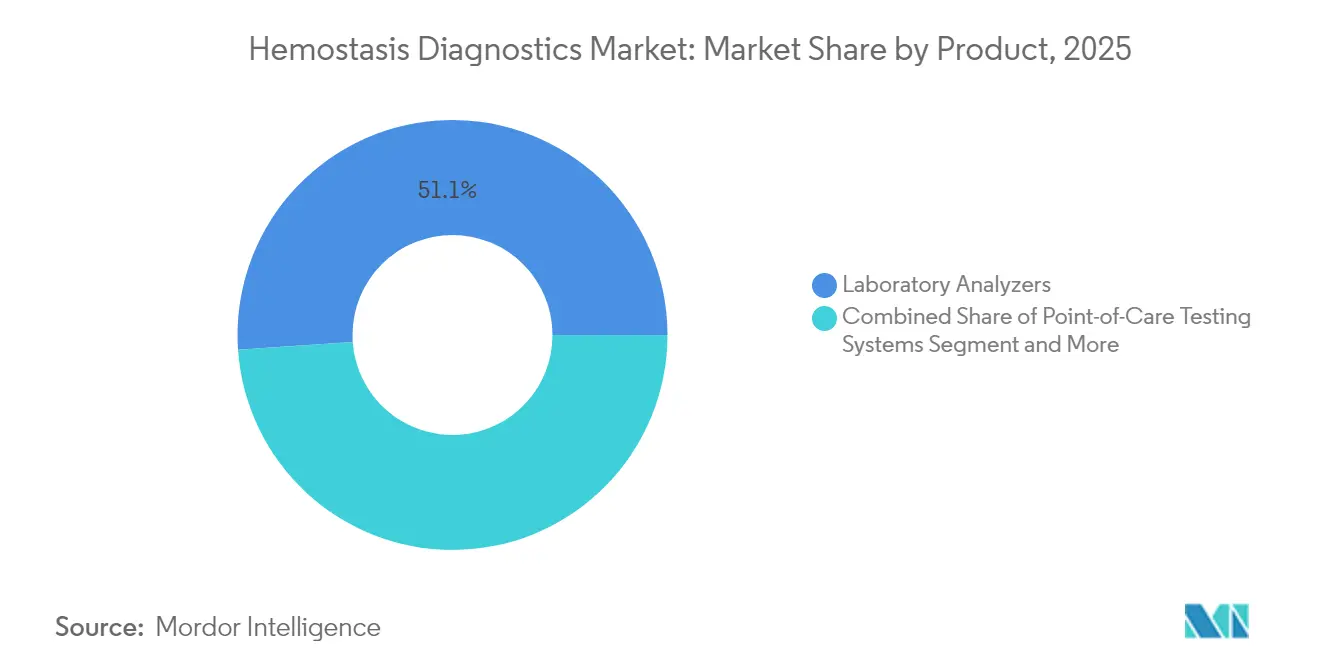

- By product, laboratory analyzers led with 51.10% of the hemostasis diagnostics market share in 2025; point-of-care systems are projected to grow at an 7.95% CAGR to 2031.

- By test, PT/INR dominated with 26.20% revenue share in 2025, while viscoelastic assays are forecast to advance at a 9.85% CAGR.

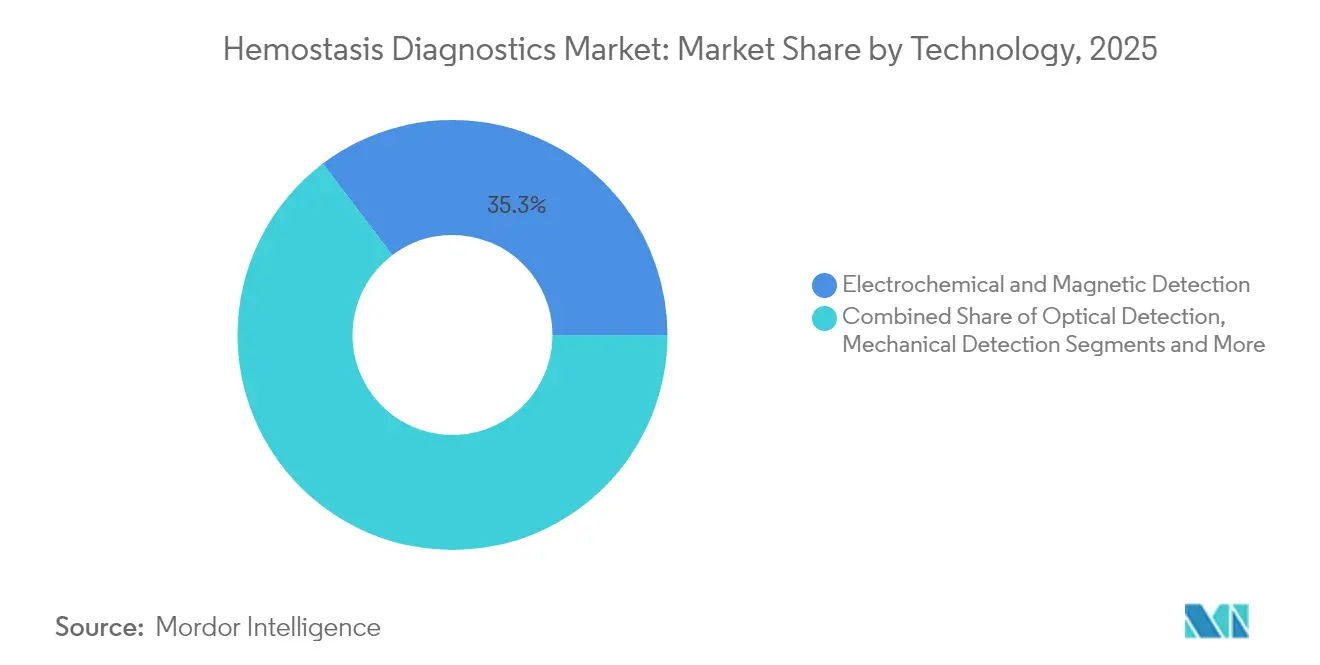

- By technology, electrochemical and magnetic detection commanded 35.30% of the hemostasis diagnostics market size in 2025; microfluidics is expanding at a 10.10% CAGR through 2031.

- By end user, hospitals accounted for 61.30% of 2025 revenue, whereas outpatient clinics are poised for 8.95% CAGR growth.

- By geography, North America held 37.40% of 2025 revenue; Asia-Pacific is the fastest-growing region with an 8.00% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hemostasis Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidences Of Bleeding Disorders | +1.2% | Global, with higher impact in developed markets | Long term (≥ 4 years) |

| Technological Advancements In Coagulation Testing | +0.9% | North America & EU leading, APAC adoption accelerating | Medium term (2-4 years) |

| Rising Adoption Of Automated Hemostasis Equipment | +0.8% | Global, concentrated in high-volume laboratories | Medium term (2-4 years) |

| Adoption Of Viscoelastic Testing (TEG/ROTEM) For Transfusion Management | +0.7% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Microfluidic Point-Of-Care (POC) Assays Enabling Decentralized Testing | +0.6% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Low-Volume Monitoring Demand In ECMO & Critical Care | +0.4% | Global, concentrated in tertiary care centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Incidences of Bleeding Disorders

Global hemophilia prevalence is now believed to be nearly triple earlier estimates, creating a substantial diagnostic gap that hospitals are eager to close[1]Centers for Disease Control and Prevention, “Data and Statistics on Hemophilia,” cdc.gov. The World Federation of Hemophilia records 20,000 new cases each year, yet more than 500,000 people remain undiagnosed worldwide, driving sustained demand for early-screening assays. Precise factor monitoring is essential because prophylactic regimens cut intracranial hemorrhage risk sharply and can lower annual treatment costs that today range between USD 213,874 and USD 869,940 per patient. Governments and payers therefore push for broader access to coagulation panels and point-of-care devices that facilitate routine monitoring outside tertiary centers. As population aging and surgical volumes climb, hospitals increasingly regard the hemostasis diagnostics market as indispensable rather than discretionary.

Technological Advancements in Coagulation Testing

Viscoelastic platforms such as Haemonetics’ FDA-cleared TEG 6s cartridge provide real-time, whole-blood clot dynamics that routine PT or aPTT cannot capture[2]Haemonetics Corporation, “Haemonetics Receives FDA Clearance for New TEG® 6s Global Hemostasis-HN Cartridge,” haemonetics.com. Clinical studies show protocol-guided transfusions cut blood-product use by up to 79% without raising bleeding risk, translating to sizeable cost savings for trauma and transplant centers. Parallel advances in microfluidics, exemplified by Nova Biomedical’s Stat Profile Prime Plus requiring only 90 μL of capillary blood, blur the line between laboratory and bedside testing. Artificial-intelligence-enabled platelet imaging from the University of Tokyo underscores a broader shift toward automated pattern recognition that could soon personalize antiplatelet regimens. These breakthroughs collectively raise throughput, lower sample-volume requirements, and improve clinical decision-making speed within the hemostasis diagnostics market.

Rising Adoption of Automated Hemostasis Equipment

Automation tackles two laboratory pain points—staff shortages and stringent quality control. Sysmex reported 14% sales growth in coagulation products in fiscal-Q2 2025 after scaling production in India to meet demand from high-volume labs. Siemens Healthineers has added more than 60 IVDR-ready assays to its reagents line, ensuring continuity for customers migrating to automated workcells. Roche’s cobas t 711 delivers 390 tests per hour with <3% coefficient of variation, a throughput level that smaller manual systems cannot match. Updated CLIA rules that tighten hematocrit and hemoglobin error limits drive laboratories to replace legacy instruments with high-precision analyzers. Consequently, automated platforms now form the backbone of the hemostasis diagnostics market in reference labs and integrated health systems alike.

Adoption of Viscoelastic Testing (TEG/ROTEM) for Transfusion Management

Combat-care studies reveal a 57% mortality reduction when trauma teams switch from conventional coagulation panels to viscoelastic-guided resuscitation. In liver transplantation, ROTEM pinpoints hyper- or hypocoagulability faster than classical tests, supporting judicious use of cryoprecipitate and platelet concentrates. Quantra’s QPlus cartridge recently earned FDA de novo clearance by demonstrating 72–98% accuracy versus reference ROTEM measurements, widening clinician choice for point-of-care viscoelastic assays. Postpartum hemorrhage protocols that integrate velocity-derived TEG parameters further solidify viscoelastic testing as a versatile tool across care settings. As evidence builds, hospitals incorporate viscoelastic devices into massive-transfusion kits, embedding them firmly within the hemostasis diagnostics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack Of Awareness In Developing Economies | -0.6% | Africa, parts of Asia-Pacific, Latin America | Long term (≥ 4 years) |

| Stringent Regulatory Approval Processes | -0.4% | Global, with varying intensity by region | Medium term (2-4 years) |

| Reimbursement Gaps For Advanced POC Devices | -0.3% | Global, particularly in emerging markets | Medium term (2-4 years) |

| Data-Interoperability Issues With LIS / HIS Integration | -0.2% | Global, concentrated in complex healthcare systems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lack of Awareness in Developing Economies

Under-recognition of bleeding disorders in many low-income regions keeps diagnostic volumes low despite rising surgical rates. The World Federation of Hemophilia notes large gaps in patient registries, complicating resource allocation. Many clinicians still rely solely on PT/INR because advanced coagulation panels are unavailable or unaffordable at district hospitals. Limited public-health funding competes with higher-profile disease priorities, delaying investment in analyzer platforms. Cultural reliance on traditional therapies further slows uptake of modern diagnostics. Still, localized manufacturing—such as Indian-based facilities that meet international quality standards—demonstrates a viable path to broaden access and lift the hemostasis diagnostics market over the long term.

Stringent Regulatory Approval Processes

Differing global regulations push development costs higher and lengthen launch timelines for innovators. Europe’s IVDR now classifies more than 80% of specialized hematology tests as in-house, obliging labs to conduct extensive validation and vigilance tracking. In the United States, recent FDA warning letters illustrate persistent scrutiny that can halt production and delay upgrades. For smaller firms lacking extensive clinical datasets, the cost of multi-jurisdiction trials is prohibitive, stifling product diversity in the hemostasis diagnostics market. Harmonization efforts are advancing, but until realized they will continue to constrain rapid diffusion of cutting-edge coagulation technologies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Laboratory Analyzers Dominate, but POC Systems Accelerate

Laboratory analyzers generated 51.10% of 2025 revenue, anchoring the hemostasis diagnostics market with high-throughput capabilities and broad test menus. Automation, advanced reagent stability, and middleware connectivity help large core labs clear staffing bottlenecks while meeting tighter quality-control targets. Point-of-care (POC) systems, although a smaller base, are advancing at an 7.95% CAGR as emergency departments, catheterization labs, and ambulatory surgery centers seek rapid clotting profiles at the bedside. This trend reflects a deeper structural pivot toward decentralized care and value-based reimbursement, which rewards shorter length of stay and lower transfusion cost. The reagents and consumables stream linked to laboratory analyzers remains a resilient profit pool because kits require continual replacement to keep instruments compliant with IVDR and CLIA standards. Miniaturization is blurring category lines, with fingertip micro-sampling and cartridge-based assays allowing analyzers to migrate closer to patients without sacrificing throughput.

In parallel, the hemostasis diagnostics industry is witnessing a surge in hybrid workstations able to toggle between high-volume central-lab mode and stat-testing mode during peak OR hours. Suppliers are bundling instruments with closed-loop reagent contracts, laboratory information system connectivity, and on-site training to secure multiyear deals. Hospitals struggling with skilled-technologist vacancies lean heavily toward platforms that deliver automated calibration, real-time QC, and predictive maintenance alerts. These integrated offerings solidify vendor lock-in and extend the lifecycle of laboratory analyzers, even as POC systems rise.

By Test: PT/INR Still Leads, Viscoelastic Assays Gain Ground

PT/INR retained 26.20% share of the hemostasis diagnostics market in 2025 because warfarin monitoring and surgical screening remain near-universal. Coumadin clinics and pre-op pathways rely on quick PT/INR readouts to adjust anticoagulant dosing and verify readiness for procedures. However, viscoelastic assays are sprinting ahead with a 9.85% CAGR. Surgeons and intensivists value whole-blood clot kinetics for targeted transfusion, a benefit conventional plasma-based tests cannot provide. D-dimer keeps its foothold in pulmonary embolism and deep-vein thrombosis workups, while fibrinogen tests gain traction for obstetric hemorrhage and trauma-induced coagulopathy risk stratification.

New test combinations, such as GFAP plus D-dimer for stroke triage, hint at multiplexed assay panels that could compress workups into a single sample. Even so, traditional aPTT remains indispensable for unfractionated heparin monitoring, preserving its place in the broader portfolio. As evidence mounts that viscoelastic-guided protocols save blood products and reduce ICU stays, tertiary centers add these assays to point-of-care carts, reshaping test-mix revenue within the hemostasis diagnostics market.

By Technology: Electrochemical Platforms Lead While Microfluidics Takes Off

Electrochemical and magnetic detection technologies captured 35.30% market share in 2025, favored for robust signal-to-noise ratios, adaptability to automation, and cost efficiency at scale. Optical detection retains wide use because legacy instruments are deeply embedded, yet faces gradual displacement as labs modernize. Microfluidics, posting a 10.10% CAGR, opens new frontiers by delivering comprehensive clotting profiles from microliter samples-a critical advance for neonates, ECMO patients, and field triage units. These lab-on-a-chip devices shorten analysis time to minutes without the need for centrifugation, aligning with emergency medicine workflows.

Mechanical detection remains relevant where direct clot-formation measurement is paramount, such as orthopedic surgery units monitoring antifibrinolytic therapy. Convergence is evident: next-generation analyzers fuse optical, mechanical, and electrochemical sensors with AI algorithms that flag aberrant patterns automatically. This integration reduces technician intervention and supports remote-monitoring models, strengthening the technology moat that established vendors hold in the hemostasis diagnostics market.

By End User: Hospitals Remain Core, Outpatient Facilities Surge

Hospitals commanded 61.30% of 2025 revenue because complex surgeries, trauma services, and intensive care units rely on broad coagulation menus under one roof. In-house laboratories favor analyzer platforms that link directly with electronic medical records, safeguarding rapid clinician access to results. Yet outpatient clinics and ambulatory surgery centers form the fastest-growing channel at 8.95% CAGR as procedural care migrates away from inpatient facilities. Point-of-care devices-handheld or benchtop-let clinicians clear same-day cases without the delays of central lab routing.

Reference laboratories continue to service esoteric factor assays and rare platelet-function tests, while blood banks depend on coagulation screening for donor safety and component quality. Digital connectivity now connects all end-users to centralized data lakes, enabling benchmarking of transfusion ratios and reagent utilization across networks. Consequently, vendors tailor service contracts to each segment’s workflow, enlarging their total addressable footprint within the hemostasis diagnostics market.

Geography Analysis

North America led with 37.40% of 2025 revenue thanks to sophisticated hospital networks, early adoption of automated analyzers, and stable reimbursement for advanced diagnostics. The United States’ dense trauma centers and transplant programs generate a steady stream of viscoelastic test demand, while the FDA’s 2025 Class II ruling eases new-device onboarding. Canada mirrors U.S. trends but places greater emphasis on provincial bulk-purchase contracts that favor multi-analyte platforms. Mexico’s ongoing health-system reform drives centralized laboratory buildouts, opening incremental sales channels for mid-tier analyzers.

Asia-Pacific is the fastest-growing geography, advancing at an 8.00% CAGR. China’s volume-based procurement pressures pricing for reagents, yet massive procedure volumes sustain absolute growth. Japan’s aging demographic fuels demand for chronic anticoagulation monitoring, while its technologically adept hospitals rapidly integrate AI-enabled platelet imaging. India’s expansion of indigenous manufacturing-seen in Sysmex’s new facilities-lowers acquisition costs for public hospitals, broadening access to automated hemostasis panels. South Korea and Australia, each with robust trauma and cardiac-surgery programs, continue to install viscoelastic analyzers alongside existing laboratory workstations. These combined forces elevate Asia-Pacific’s share of the hemostasis diagnostics market year by year.

Europe maintains steady mid-single-digit gains amid stringent IVDR compliance. Germany and France adopt microfluidic cartridges swiftly in high-acuity centers, whereas the United Kingdom accelerates point-of-care deployment through National Health Service modernization funds. Southern European nations invest selectively, prioritizing transfusion-sparing technologies to curb blood-product expenditures. The Middle East and Africa trail but show pockets of momentum in Gulf Cooperation Council states where new tertiary hospitals specify centralized coagulation labs from day one. Latin America’s growth rests largely on Brazil and Argentina, which are expanding trauma-care infrastructure and adopting viscoelastic testing in private hospital groups. Collectively, these regional narratives underscore varied but converging trajectories that keep the hemostasis diagnostics market on a positive global slope.

Regulatory Landscape

In the United States, hemostasis diagnostics are regulated as IVD medical devices under FDA frameworks, including device classification in 21 CFR Part 864 for coagulation and hemostasis-related tests. A key tailwind has been the FDA's 2025 reclassification of viscoelastic systems into Class II, which supports clearer predicates and shorter market-entry cycles for cartridge-based viscoelastic platforms used in trauma, cardiac surgery, and transplant pathways.

Quality and oversight requirements are also tightening in ways that influence product design controls and lab compliance. The FDA's Quality Management System Regulation (QMSR), effective February 2026, aligns US device quality requirements more closely with ISO 13485:2016, shaping how manufacturers manage software changes, traceability, and postmarket activities across global supply chains. Separately, the FDA's May 2024 final rule to phase out general enforcement discretion for laboratory developed tests (LDTs) over a multi-year period increases regulatory obligations for laboratories that develop in-house coagulation assays, adding documentation and validation burdens that can shift testing back toward cleared kits and automated analyzers. In Europe, the IVDR continues to raise evidence and lifecycle expectations for IVDs, while amended transitional provisions (Regulation (EU) 2024/1860) include deadlines such as the May 2026 milestone for certain legacy devices to have a Notified Body application lodged to maintain EU market access.

Competitive Landscape

The hemostasis diagnostics market remains moderately fragmented, with leading suppliers pursuing vertical integration and platform consolidation to defend share. Abbott, Danaher, Roche, Sysmex, Siemens Healthineers, and Werfen deploy multi-year R&D pipelines, emphasizing automation, microfluidics, and digital connectivity. Thermo Fisher’s USD 2 billion U.S. innovation program underscores scale advantages that furnish smaller firms with OEM reagents while reinforcing its own production security. Werfen’s unification of subsidiaries streamlines brand architecture, reinforcing its focus on specialized coagulation and point-of-care lines.

Strategic acquisitions intensify. Werfen’s prior purchase of Accriva Diagnostics bolstered its POC catalog, while Merit Medical’s 2025 acquisition of Biolife extended into hemostatic wound-management adjuncts, bridging devices and diagnostics. bioMérieux’s USD 141.8 million buyout of SpinChip adds a 10-minute whole-blood immunoassay platform, signaling convergence between coagulation and infectious-disease testing in near-patient settings. Siemens Healthineers’ OEM pact with Sysmex extends a 25-year partnership, blending extensive reagent lines with next-generation hardware to counter newcomer microfluidic entrants.

Technology differentiation revolves around throughput, sample-volume efficiency, and informatics. Vendors now embed middleware that pushes QC alerts directly to mobile dashboards, shrinking downtime. Cloud-ready analyzers furnish anonymized datasets for algorithm training, an emergent value proposition for customers seeking predictive transfusion analytics. Start-ups working on nanoengineered biosensors or AI-driven imaging target white-space segments such as ultra-rapid thrombosis prediction and non-invasive clot visualization, forcing incumbents to accelerate their own digital roadmaps. As procurement moves to total-cost-of-ownership evaluations rather than instrument price alone, bundled reagent-service contracts and guaranteed uptime become decisive differentiators, shaping competitive contours within the hemostasis diagnostics market.

Hemostasis Diagnostics Industry Leaders

Thermo Fisher Scientific, Inc.

F. Hoffmann-La Roche Ltd

Nihon Kohden Corporation

Abbott Laboratories

Siemens Healthineers

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Point-of-care and near-patient coagulation pathways offer clear whitespace where clinical protocols require rapid, actionable results and low sample volumes, particularly in obstetric hemorrhage, emergency surgery, and critical care. A concrete proof point is the FDA's September 2025 510(k) clearance expanding HemoSonics Quantra Hemostasis System use with the QStat cartridge into peripartum obstetric procedures, reinforcing investment in viscoelastic and cartridge-based testing beyond trauma and cardiac ORs. Roche's October 2025 FDA 510(k) clearance for the CoaguChek XS Plus System similarly points to continued demand for decentralized PT/INR monitoring and workflows that reduce reliance on centralized lab routing.

Opportunity also extends to the overlap between companion diagnostics and specialized coagulation assays that support newer hemophilia care models and risk stratification. Siemens Healthineers' March 2025 FDA clearance of the Innovance Antithrombin assay as a companion diagnostic for Sanofi's Qfitlia (fitusiran) shows how therapy-linked testing can pull advanced hemostasis assays into routine pathways at hospitals and specialty clinics. On the laboratory operations side, CLSI updates (H21:2024 and the April 2025 H21QG quick guide) reinforce standardized specimen handling expectations for coagulation testing, which supports automation, connectivity, and repeatable performance in high-throughput settings. As informatics becomes more central to procurement, interoperability and cybersecurity requirements referenced in FDA processes create room for vendors that bundle analyzers and POC devices with middleware, LIS/HIS integration, and software validation support to reduce implementation friction for multi-site health systems.

Recent Industry Developments

- May 2026: Roche entered a definitive agreement to acquire PathAI for USD 750 million upfront plus USD 300 million in milestones, expanding its AI capabilities for diagnostic workflows. The transaction supports the move toward algorithm-enabled interpretation and digital decision support that can complement coagulation and hemostasis testing in integrated hospital labs.

- June 2025: Nihon Kohden signed a 3-year supply deal with Noul to distribute AI-powered blood analysis systems in Latin America. The agreement broadens access to AI-assisted hematology and related diagnostic workflows, supporting demand for connected, automated testing systems used alongside coagulation diagnostics in hospital laboratories.

- July 2024: Roche completed the acquisition of LumiraDx's point-of-care technology to expand decentralized testing across clinical chemistry, immunochemistry, and coagulation. Adding an established POC technology base strengthens Roche's position in near-patient hemostasis testing models where speed, cartridge logistics, and connectivity influence purchasing decisions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers diagnostic products and tests used to evaluate blood clotting and related pathways in clinical care, including laboratory coagulation analyzers, point-of-care coagulation devices, and the associated reagents and consumables that enable routine testing.

Scope exclusions: We exclude therapeutic topical hemostats, surgical sealants, and general hematology counters from this market sizing.

Segmentation Overview

- By Product

- Laboratory Analyzers

- Automated Systems

- Semi-automated Systems

- Manual Systems

- Point-of-Care Testing Systems

- Reagents & Consumables

- Laboratory Analyzers

- By Test

- Activated Partial Thromboplastin Time (aPTT)

- Prothrombin Time (PT/INR)

- D-Dimer

- Fibrinogen

- Thrombin Time & Clotting-Factor Assays

- Viscoelastic Tests (TEG, ROTEM)

- By Technology

- Optical Detection

- Mechanical Detection

- Electrochemical & Magnetic Detection

- Microfluidics & Lab-on-Chip

- By End User

- Hospitals

- Diagnostic Laboratories

- Outpatient Clinics & Ambulatory Surgery Centers

- Blood Banks

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to build the demand and supply context for coagulation testing and to set practical boundaries for what counts as hemostasis diagnostics revenue. Public sources such as the US FDA device database, the US CDC, the World Health Organization, and the World Bank help us track disease burden signals, procedure intensity, and country level healthcare capacity that influences test volumes.

We also refer to sources such as OECD health statistics, peer reviewed clinical journals on coagulation testing utilization, and customs trade releases where they help clarify import intensity for analyzers and reagents. Company annual reports, investor presentations, and reputable press coverage are used to map product portfolios and regional exposure. We then cross-check using paid subscriptions for company financials and patent databases where needed. The sources listed here are illustrative only, and many other public and paid references were used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focuses on validating what is actually purchased and used, and then confirming pricing, replacement cycles, and the mix between routine assays and specialty tests, including viscoelastic testing where relevant. We interview a spread of stakeholders such as hospital lab leads, diagnostic lab managers, procurement teams, and product specialists across major regions, so gaps from desk research can be closed and assumptions aligned to real buying behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 16% | APAC: 44% |

| Mid tier: 46% | Functional/Unit leaders: 41% | EMEA: 35% |

| Smaller Players: 19% | Managers: 43% | Americas: 21% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where clinical testing demand is reconstructed from the expected pool of coagulation tests performed, which is then translated into revenue using realistic pricing and product mix. The model is organized so each step can be traced, beginning with indicators such as hospital and diagnostic lab activity, anticoagulant monitoring intensity, procedure volumes that trigger coagulation screening, and the share of testing done on point-of-care systems versus central lab analyzers.

To keep totals grounded, we corroborate results using selective bottom-up approximations, such as sampled analyzer placements by country, estimated reagent pull-through per instrument, and a price band check for key assays like PT/INR, aPTT, D-dimer, and fibrinogen. Where country level data is thin, gaps are handled through regional benchmarks that are adjusted by healthcare spend, lab infrastructure, and observed adoption patterns shared by interviewees. For forecasting, scenario analysis is used to reflect how guideline shifts, anticoagulant therapy mix, and procurement cycles can move demand. We then review assumptions with experts to settle on the most likely path.

Data Validation & Update Cycle

Validation is done through structured triangulation so the final value makes sense against multiple independent signals, not just one data stream. Our analysts run variance checks across countries and regions, review outliers against known reimbursement or procurement changes, and re-contact sources when price or volume assumptions look inconsistent.

Before sign-off, outputs are reviewed in more than one internal step, including a logic check on scope boundaries and a consistency check between growth drivers and the forecast curve. Reports are refreshed annually, with interim updates when a material event changes pricing, demand, or supply availability. Right before delivery, a fresh pass is completed so clients receive the most current view that can be supported by the latest public updates and expert checks.

Mordor Intelligence's Hemostasis Diagnostics Market Size Measured Against Other Published Estimates

Published market sizes for hemostasis diagnostics often do not match because teams choose different revenue boundaries and different timing for price inputs and currency conversion. Differences also show up when one model leans more on device shipments while another is driven by testing demand and reagent pull-through.

In our work, the biggest gap drivers usually come from how consumables are treated versus instruments, whether point-of-care systems are fully counted, and how fast average selling prices are assumed to move over the forecast window. When pricing is refreshed with recent tenders and distributor feedback, and currency timing is kept consistent for the same calendar year, Mordor Intelligence reduces noise in the total that can otherwise come from old price lists and mixed exchange rate assumptions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.86 B (2026) | |

| Industry Publisher A | USD 4.90 B (2025) | Uses an earlier base year and a longer forecast window, and the page-level scope is not clear on how analyzer versus reagent revenue is split, which can shift the total when consumables pull-through is assumed differently. |

| Global Consultancy B | USD 2.74 B (2025) | Appears to apply a narrower definition and may undercount recurring reagent revenue or exclude parts of routine coagulation testing in some settings, which typically leads to a lower starting value. |

The spread in published values is largely explained by scope boundaries and by how pricing and currency timing are handled from one year to the next. By keeping the market definition tight to hemostasis testing systems plus their consumables, and by checking the model against real world testing and procurement signals, the result stays easier to trace and repeat across countries.

Key Questions Answered in the Report

What is the current size of the hemostasis diagnostics market?

The market generated USD 4.86 billion in 2026 and is expected to grow to USD 6.13 billion by 2031 at a 4.75% CAGR.

Which region is growing fastest?

Asia-Pacific is expanding at an 8.00% CAGR thanks to rising surgical volumes, broader healthcare access, and accelerating technology adoption.

Why are viscoelastic assays gaining popularity?

They provide real-time, whole-blood clot kinetics that guide targeted transfusion, reducing blood-product use and improving outcomes in trauma, cardiac surgery, and transplantation.

How are regulatory changes affecting the market?

The FDA’s 2025 Class II reclassification streamlines U.S. approvals, while Europe’s IVDR imposes stricter validation burdens, collectively shaping product launch timelines.

What role does automation play in market growth?

Automated analyzers boost throughput, reduce human error, and help labs meet tightened quality-control targets, making them indispensable amid workforce shortages.

Which product segment is expected to grow fastest?

Point-of-care testing systems are projected to rise at an 7.95% CAGR as care pathways shift toward outpatient and emergency settings requiring immediate coagulation results.

Page last updated on: