Healthcare Smart Card Reader Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

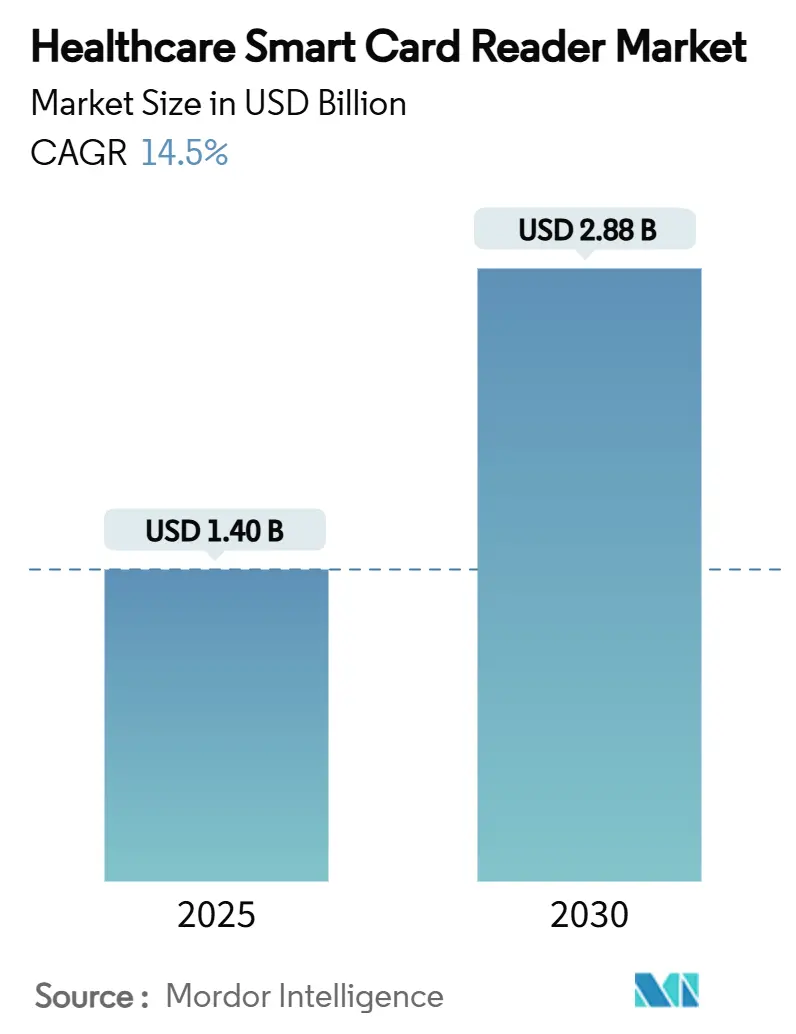

| Market Size (2025) | USD 1.40 Billion |

| Market Size (2030) | USD 2.88 Billion |

| Growth Rate (2025 - 2030) | 14.50% CAGR |

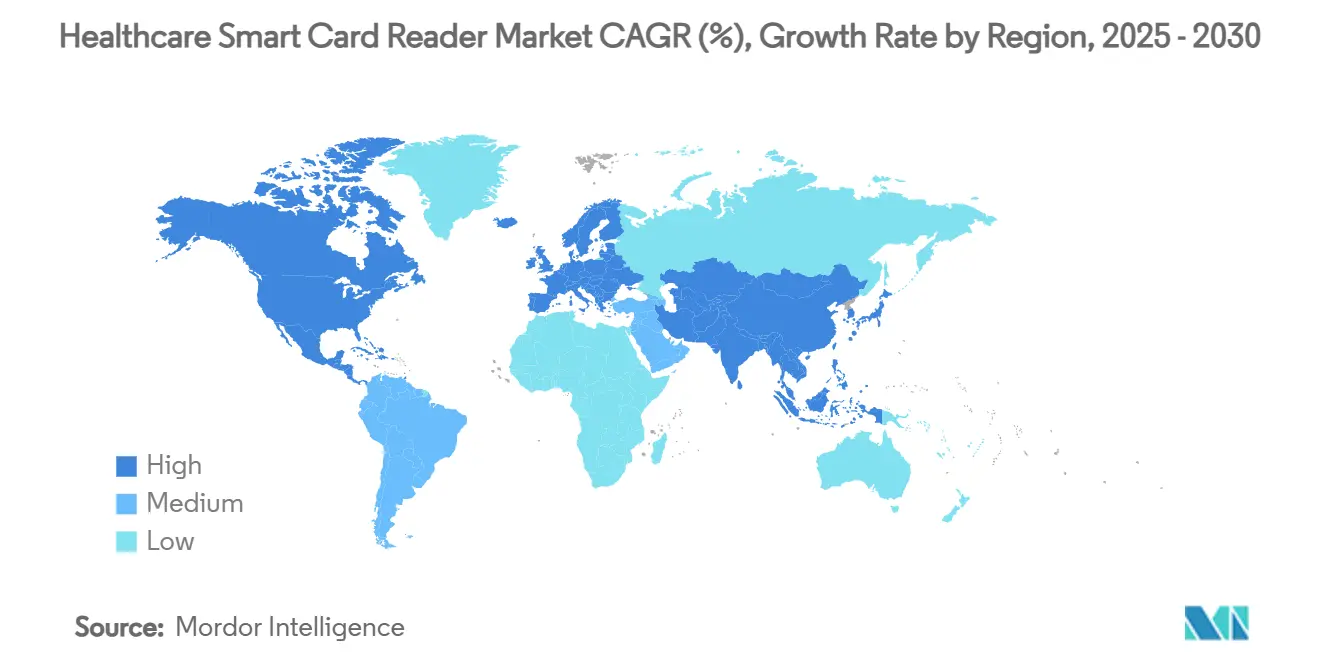

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Smart Card Reader Market Analysis by Mordor Intelligence

The global healthcare smart card reader market size stands at USD 1.40 billion in 2025 and is projected to reach USD 2.88 billion by 2030, advancing at a 14.50% CAGR over the forecast period. Mandatory eHealth card roll-outs, rising data-breach penalties, and enduring post-COVID hygiene standards collectively underpin this double-digit trajectory. North America holds the largest regional foothold because HIPAA compliance and mature health IT ecosystems have normalised multi-factor authentication. Contactless technology leads the product mix as hospitals hard-wire infection-control safeguards into procurement policies, while dual-interface readers scale quickly on the promise of hybrid deployment flexibility. Application momentum is shifting toward asset and inventory tracking as administrators quantify efficiency gains from RFID-enabled workflows. Consolidation among reader vendors and identity-management specialists is accelerating, reflecting a strategic pivot toward end-to-end solutions that span hardware, middleware, and compliance support.

Key Report Takeaways

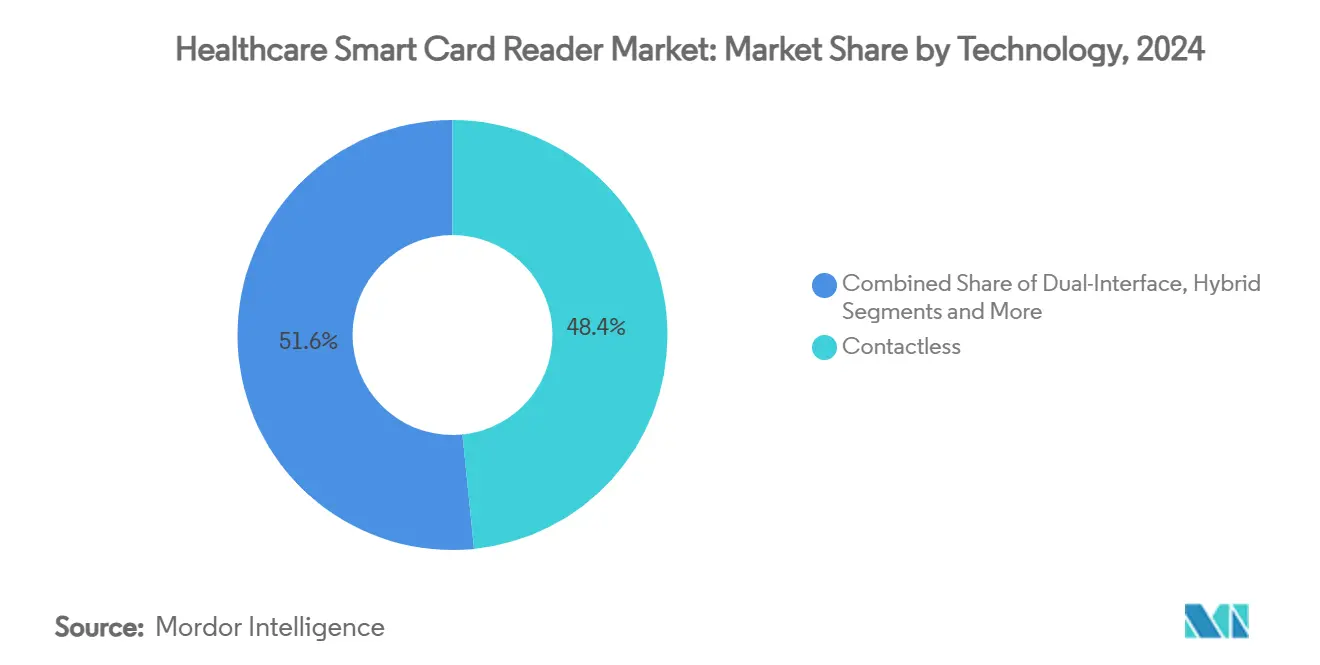

- By technology, contactless readers commanded 48.4% revenue share in 2024, whereas dual-interface units are forecast to post the fastest 13.40% CAGR through 2030.

- By application, patient identification and authentication led with 51.6% share in 2024; asset and inventory tracking is on course for an 18.20% CAGR to 2030.

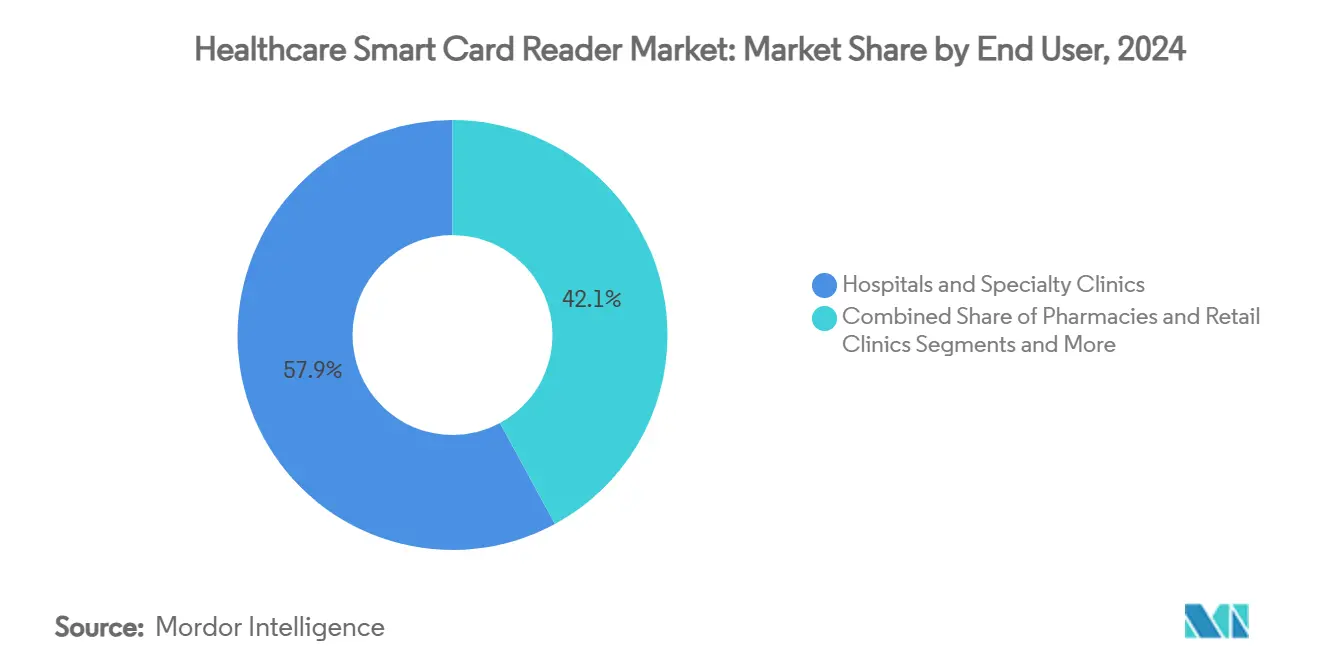

- By end user, hospitals and specialty clinics represented 57.9% of the healthcare smart card reader market size in 2024, while ambulatory surgical centers are expected to record the strongest 14.70% CAGR over the outlook period.

- By region, North America held 37.8% healthcare smart card reader market share in 2024; Asia-Pacific is projected to expand at a 12.60% CAGR to 2030.

Global Healthcare Smart Card Reader Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory eHealth smart-card roll-outs | +3.20% | EU, Japan, Canada; spreading globally | Medium term (2-4 years) |

| Spike in data-breach fines | +2.80% | North America, EU; spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Post-COVID hygiene push for contactless tech | +2.10% | Global | Short term (≤ 2 years) |

| EHR & SSO integrations | +2.40% | North America core; EU and Asia-Pacific gaining | Medium term (2-4 years) |

| Hybrid NFC/smart-card asset tracking | +1.90% | Asia-Pacific core; Middle East & Africa emerging | Long term (≥ 4 years) |

| Reader miniaturisation for wearables | +1.10% | Global; early uptake in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory eHealth Smart-Card Rollouts

National ID-linked health-card schemes are reshaping authentication infrastructure, locking in predictable multi-year demand cycles. Germany’s elektronische Gesundheitskarte now supports more than 80 million patient interactions annually.[1]Bundesministerium für Gesundheit, “Die elektronische Gesundheitskarte (eGK),” bundesgesundheitsministerium.deJapan made the linkage of My Number Card to insurance obligatory in December 2024, which instantly enlarged the addressable installed base for compatible readers. Secondary demand is spreading to pharmacies and emergency care units that must interface with government telematics networks. Healthcare providers adopting readers early position themselves to comply with future mandates in emerging economies where similar frameworks are taking shape. Vendor roadmaps, therefore, prioritize certification against evolving sovereign standards to secure cross-border revenue continuity.

Spike in Data-Breach Fines

Average breach costs in healthcare touched USD 10 million in 2024, magnifying the ROI of strong authentication. The Dutch Data Protection Authority levied a EUR 750,000 (USD 863,475) fine for improper biometric handling, underscoring regulators’ intent to penalize gaps in identity management. Smart card readers satisfy HIPAA and GDPR multi-factor requirements without locally storing sensitive data. Hospitals with large patient databases model the comparative cost of breach remediation versus reader roll-outs and find the latter compelling. Demand therefore leans toward readers embedded with cryptographic processors that future-proof against tighter privacy statutes.

Post-COVID Hygiene Push

Contactless cards comprised 92% of all payment-card shipments in 2024, a behavioural shift spilling into healthcare access systems. Infection-control committees now rank touchless authentication as a baseline specification for new devices. NFC-enabled readers let clinicians badge in without touching surfaces, reducing contamination risk in sterile zones. Dual-interface models that toggle between contact and contactless modes gain extra traction because they future-proof infrastructure choices. Reader suppliers differentiate on proximity-sensing range, firmware upgradability, and easy-wipe housings that withstand disinfectant chemicals.

EHR & SSO Integrations

More than 2,300 US facilities have implemented single sign-on tied to smart cards, cutting daily login events that previously exceeded 70 per clinician.[2]Sage Journals, “Leveraging Identity and Access Management,” journals.sagepub.comInteroperability between smart pumps and EHRs delivered USD 370,000 in extra revenue a year at a regional hospital through better charge capture. These quantified gains make a strong boardroom case for reader capital expenditure. API-first EHR architectures widen integration lanes, enabling auto-population of audit trails and reducing documentation lag.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High integration & compliance cost | -2.10% | Global; most acute in emerging markets | Short term (≤ 2 years) |

| Biometrics cannibalizing card budgets | -1.80% | North America, EU; Asia-Pacific gathering pace | Medium term (2-4 years) |

| Secure MCU chip shortages | -1.40% | Global; Asian manufacturing hubs heavily exposed | Short term (≤ 2 years) |

| Infection-control rules limiting contact | -1.20% | Global; strictest in North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Integration & Compliance Cost

Full-scale reader deployment can cost between USD 150,000 and USD 250,000, a burden that smaller clinics struggle to absorb. Legacy practice-management software often needs middleware connectors, inflating project budgets and training hours. HIPAA documentation and recurring audits layer further expense. Some providers opt for bar-code medication administration systems that cost USD 40,000 per bed over five years, sacrificing advanced features to stay within capital limits.[3]American Journal of Managed Care, “Cost of Implementing Bar Code Medication Administration,” ajmc.com These budget dynamics slow the universal penetration of premium reader technology.

Biometrics Cannibalizing Budget

Fingerprint or facial recognition negates card loss or sharing risk and operates contactlessly, aligning neatly with infection-control norms. Embedded sensors in medical workstations sidestep the need for separate reader hardware. Yet privacy statutes in Illinois, Texas, and Europe remain stringent, pushing some hospitals back toward smart cards for legal comfort. This tug-of-war fuels R&D into biometric-card hybrids that offer dual assurance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Contactless Readers Cement Leadership

Contactless readers held a 48.4% share of the Healthcare Smart Card Reader market in 2024. Hospitals perceive them as the safest option for sterile workflows in wards, pharmacies, and labs. Dual-interface units are the fastest climbers, riding a 13.40% CAGR because they allow gradual migration from contact to touchless ecosystems without stranding existing card stock. Contact-based models persist in high-assurance areas such as controlled drug safes, where a physical insertion step doubles as a deliberate-action safeguard. NFC-compatible designs now dominate vendor portfolios, underpinning future convergence with smartphone-based credentials and equipment tags.

Rapid firmware updates enabling ISO/IEC 11073 compliance keep installed bases current, an attribute coveted by health-system CIOs wary of frequent rip-and-replace cycles. The combined healthcare smart card reader market size for contactless and dual-interface products is forecast to top USD 2 billion by 2030, reflecting the entrenched bias toward hygienic authentication environments. Technology vendors now differentiate less on raw read speed and more on API richness that simplifies linkage to identity-and-access-management platforms. As a result, middleware ecosystems around leading EHR suites have blossomed, further entrenching contactless modalities.

By Application: Inventory Tracking Outpaces Core Authentication

Patient identification maintained a 51.6% share in 2024, anchoring the traditional use case for smart card readers. However, asset and inventory tracking is surging at an 18.20% CAGR as hospitals pivot toward data-driven utilization models. Real-time location analytics tied to smart card check-ins dramatically cut equipment hunt time and improve auditability. The Healthcare Smart Card Reader market size for asset-tracking deployments is projected to climb sharply as administrators fold RFID and NFC functions into single infrastructure footprints, validating the “do more with less hardware” narrative.

E-prescription and billing workflows gain traction where pharmacy systems merge insurance eligibility, dispensing, and authentication into one badge-tap event. Claims and insurance management applications, though nascent, promise to automate policy validation, reducing manual errors and fraud. As integration hurdles fall, cross-department adoption accelerates, pushing reader functionality beyond isolated single-sign-on contexts and into enterprise-wide logistics chains. This expansion cements readers’ status as cross-functional nodes rather than siloed peripherals, positioning them well against standalone biometric devices that lack asset-tracking hooks.

By End User: Ambulatory Surgical Centers (ASCs) Gain Momentum

Hospitals and specialty clinics controlled 57.9% of market revenue in 2024, leveraging scale economics and robust IT teams to execute complex implementations. These institutions drive vendor roadmaps through enterprise-wide RFPs that bundle authentication, medication cabinet access, and device integrations. Yet ASCs chart the steepest growth curve at a 14.70% CAGR, propelled by procedure volume shifting out of inpatient settings. ASCs prize quick patient turnover and therefore favour contactless or dual-interface readers, which shave seconds off each authentication event.

Retail pharmacies and minute clinics install low-profile readers at prescription counters to expedite e-script validation under stricter controlled-substance rules. Health insurers deploy readers in branch offices for on-the-spot identity verification, a strategy that trims fraud and accelerates claims adjudication. Academic research facilities also adopt readers for secure database access tied to clinical-trial participation, highlighting the technology’s utility beyond direct patient-care arenas. These varied deployments ensure the Healthcare Smart Card Reader industry maintains diversified revenue streams, insulating it somewhat from cyclical procurement patterns in any single provider category.

Geography Analysis

North America’s 37.8% share in 2024 stems from HIPAA-motivated demand for robust multi-factor authentication and an installed base exceeding 2,300 single-sign-on-enabled facilities. Average breach costs touching USD 10 million underscore the financial logic behind reader investments. The United States dominates regional revenue owing to its scale and complex regulatory overlay, while Canada advances national eHealth card programs and Mexico’s private hospital groups modernise IT suites. The Healthcare Smart Card Reader market share concentration in advanced U.S. health systems pushes vendors to develop premium, integration-heavy offerings that command higher average selling prices.

Europe benefits from GDPR enforcement and nationally mandated eHealth initiatives. Germany’s eGK program alone services more than 80 million citizens, ensuring a massive, predictable replacement cycle for compliant readers. Regulatory precedent, such as the Dutch EUR 750,000 biometric fine, nudges buyers toward smart card solutions viewed as legally safer. Eastern European markets display latent potential as EU funding accelerates health-IT catch-up, while supply-chain sovereignty concerns fuel appetite for domestically manufactured readers like those shipped from IDEMIA’s new French plant.

Asia-Pacific delivers the fastest 12.60% CAGR through 2030, keyed by Japan’s December 2024 mandate tying My Number IDs to health insurance. China’s scale, India’s national digital-health mission, and expanding private insurance in Southeast Asia combine to create diverse demand tiers, from high-spec readers in urban super specialty hospitals to cost-sensitive models in rural clinics. In parallel, Middle East & Africa health-system modernization underpins green-field deployments, especially across GCC states where public spending remains high. South America’s trajectory is slower but positive as Brazil and Argentina adopt stricter patient-data regulations, partially harmonizing with GDPR frameworks and thereby guiding requirements toward smart card-based authentication.

Competitive Landscape

The competitive set is moderately fragmented, featuring multinational identity-management brands alongside niche healthcare integrators. 2024 saw a spike in mergers: TOPPAN Holdings grabbed HID’s Citizen Identity Solutions to broaden geographic reach, while Vitaprotech paid USD 145 million for Identiv’s reader operations, folding 700 engineers into a unified physical-access platform. Competition centres on ease of EHR integration, dual-interface capability, and infection-control-ready housings. HID Global, Thales, and Identiv sustain differentiation through certified encryption modules, but newer entrants focus on AI-aided user-behaviour analytics.

White-space opportunities exist where readers fuse authentication with inventory oversight, especially in surgical theatres needing traceability of implants and instruments. Patent filings highlight biometric-card hybrids such as Infineon’s SECORA Pay Bio, which embeds fingerprint sensors into cards compliant with current reader slots, a tactic designed to leverage the existing infrastructure while countering pure biometric encroachment. Supply-chain sovereignty has risen to strategic priority, pushing European buyers toward local manufacturing options, evidenced by IDEMIA’s new 100 million card facility in France.

Reader vendors are also partnering with device OEMs to embed modules directly into infusion pumps and medication cabinets. Identiv joined forces with Novanta to streamline RFID adoption in smart medical devices. Similarly, Zebra Technologies and Merck KGaA launched an integrated cyber-physical trust platform for pharmaceutical traceability, signaling cross-industry fertilization. Competitive intensity is therefore shifting from stand-alone readers to vertically integrated ecosystems.

Healthcare Smart Card Reader Industry Leaders

HID Global (ASSA ABLOY AB)

Identiv Inc.

rf IDEAS Inc.

Thales Group (Gemalto)

NXP Semiconductors N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: TOPPAN Security completed its acquisition of Dzcard Group, doubling banking-card manufacturing capacity and enlarging personalization centres across Thailand, the Philippines, and India.

- March 2025: Zebra Technologies and Merck KGaA introduced the M-Trust platform, combining mobile scanners with advanced cryptography for product verification in pharma supply chains.

- February 2025: Identiv partnered with Novanta to bundle RFID inlays and reader tech for healthcare OEMs, simplifying compliance in smart devices.

- October 2024: IDEMIA opened a new French plant, setting up a 100% European value chain capable of producing 100 million banking cards annually, a move resonating with healthcare buyers seeking supply-chain sovereignty.

Global Healthcare Smart Card Reader Market Report Scope

| Contact |

| Contactless |

| Dual-Interface |

| Hybrid |

| Patient ID & Authentication |

| E-Prescription & Billing |

| Access Control to Restricted Areas & Devices |

| Asset & Inventory Tracking |

| Claims & Insurance Management |

| Hospitals & Specialty Clinics |

| Ambulatory Surgical Centers |

| Pharmacies & Retail Clinics |

| Health-Insurance Payers |

| Research & Academic Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Contact | |

| Contactless | ||

| Dual-Interface | ||

| Hybrid | ||

| By Application | Patient ID & Authentication | |

| E-Prescription & Billing | ||

| Access Control to Restricted Areas & Devices | ||

| Asset & Inventory Tracking | ||

| Claims & Insurance Management | ||

| By End User | Hospitals & Specialty Clinics | |

| Ambulatory Surgical Centers | ||

| Pharmacies & Retail Clinics | ||

| Health-Insurance Payers | ||

| Research & Academic Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast value of the Healthcare Smart Card Reader market by 2030?

The market is projected to reach USD 2.88 billion by 2030 at a 14.50% CAGR.

Which technology segment leads current deployments?

Contactless smart card readers hold 48.4% share owing to infection-control priorities.

Which region is growing the fastest?

Asia-Pacific is expected to register a 12.60% CAGR through 2030 on the back of national eHealth mandates.

Why are ambulatory surgical centers adopting readers rapidly?

ASCs value the workflow speed and data security gains that dual-interface readers deliver, supporting a 14.70% CAGR.

How do smart card readers support asset management?

NFC-enabled readers double as RFID interrogators, linking equipment usage data to authenticated staff for tighter compliance and efficiency.

What competitive moves shaped the market recently?

TOPPAN’s and Vitaprotech’s acquisitions in 2024–2025 signalled accelerated consolidation aimed at delivering end-to-end identity solutions.

Page last updated on: