Market Overview

| Study Period | 2022 - 2031 |

|---|---|

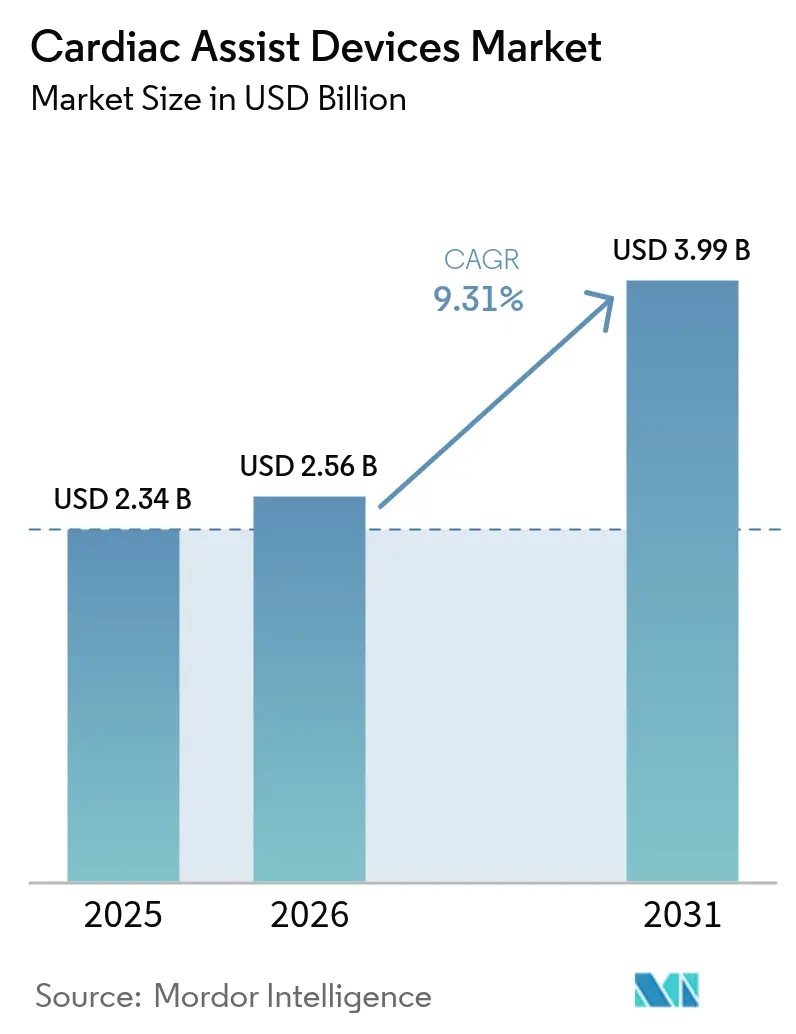

| Market Size (2026) | USD 2.56 Billion |

| Market Size (2031) | USD 3.99 Billion |

| Growth Rate (2026 - 2031) | 9.31% CAGR |

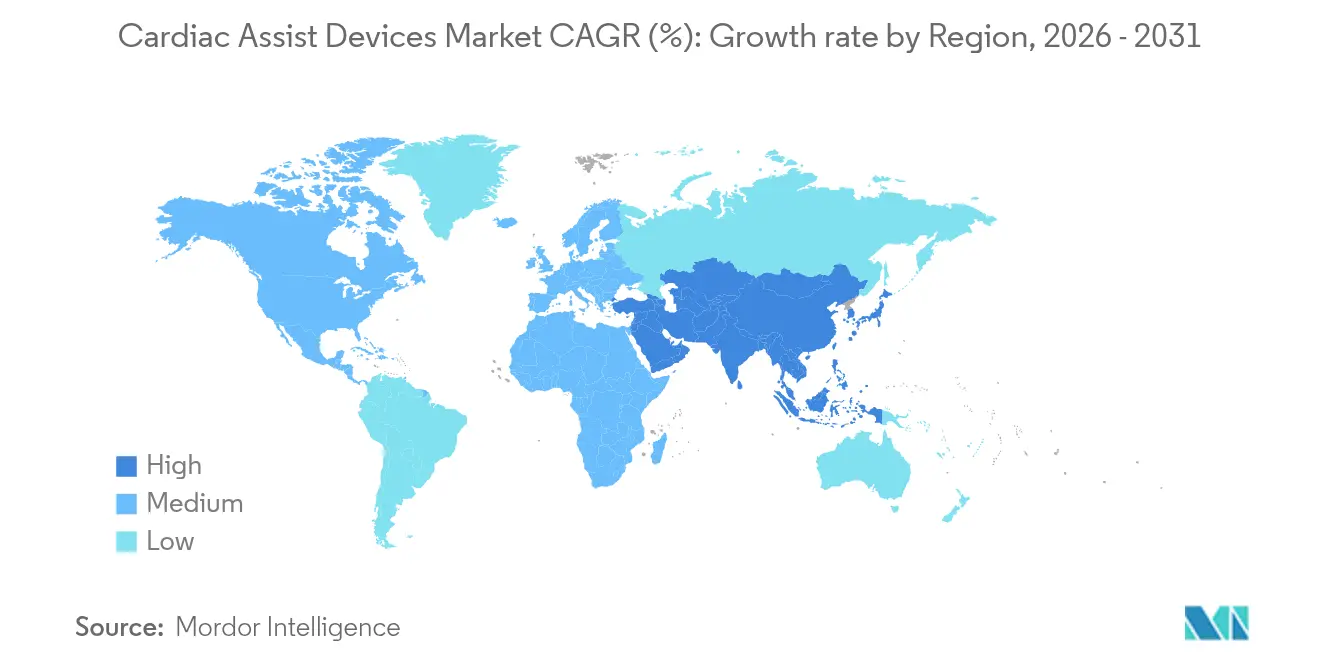

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cardiac Assist Devices Market Analysis by Mordor Intelligence

The cardiac assist devices market size is expected to grow from USD 2.34 billion in 2025 to USD 2.56 billion in 2026 and is forecast to reach USD 3.99 billion by 2031 at 9.31% CAGR over 2026-2031. The cardiac assist devices market is expanding as hospitals confront rising end-stage heart failure prevalence, donor-heart shortages, and growing confidence in continuous-flow technology. Breakthroughs in magnetically levitated pumps, percutaneous micro-pumps, and pediatric indications are enabling earlier intervention, while reimbursement expansion in Asia-Pacific is widening access. Regulatory momentum, exemplified by FDA approvals for pediatric Impella 5.5 and Impella CP, is encouraging destination-therapy uptake earlier in the disease course[1]Source: U.S. Food and Drug Administration, “Pediatric Indication Expansion for Impella,” fda.gov . Simultaneously, safety recalls—such as the HeartMate 3 EOGO event—are intensifying post-market surveillance and prompting iterative design improvements. Sustained venture investment in total artificial hearts and ambulatory counterpulsation systems signals that the cardiac assist devices market will remain a fertile arena for engineering innovation and business growth.

Key Report Takeaways

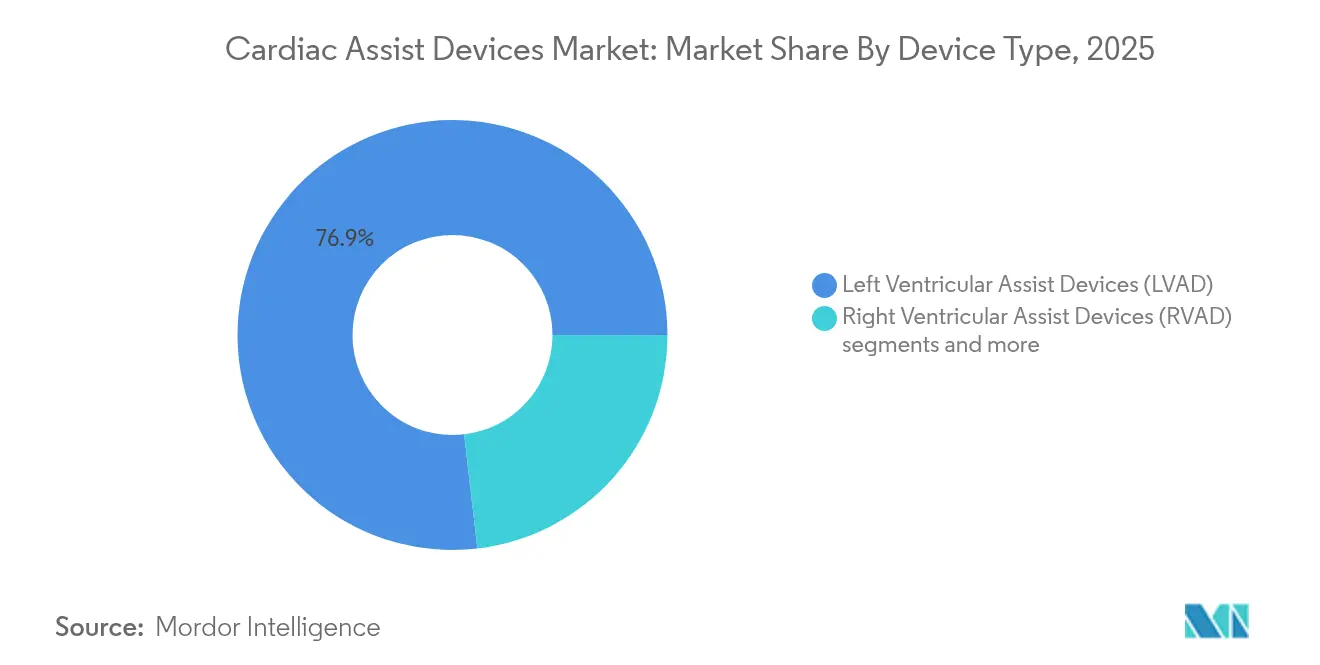

- By device type, left ventricular assist devices held 76.85% of cardiac assist devices market share in 2025, while total artificial hearts are advancing at a 10.07% CAGR to 2031.

- By application, bridge-to-transplant commanded 38.21% share of the cardiac assist devices market size in 2025; destination therapy is forecast to grow at 11.35% CAGR to 2031.

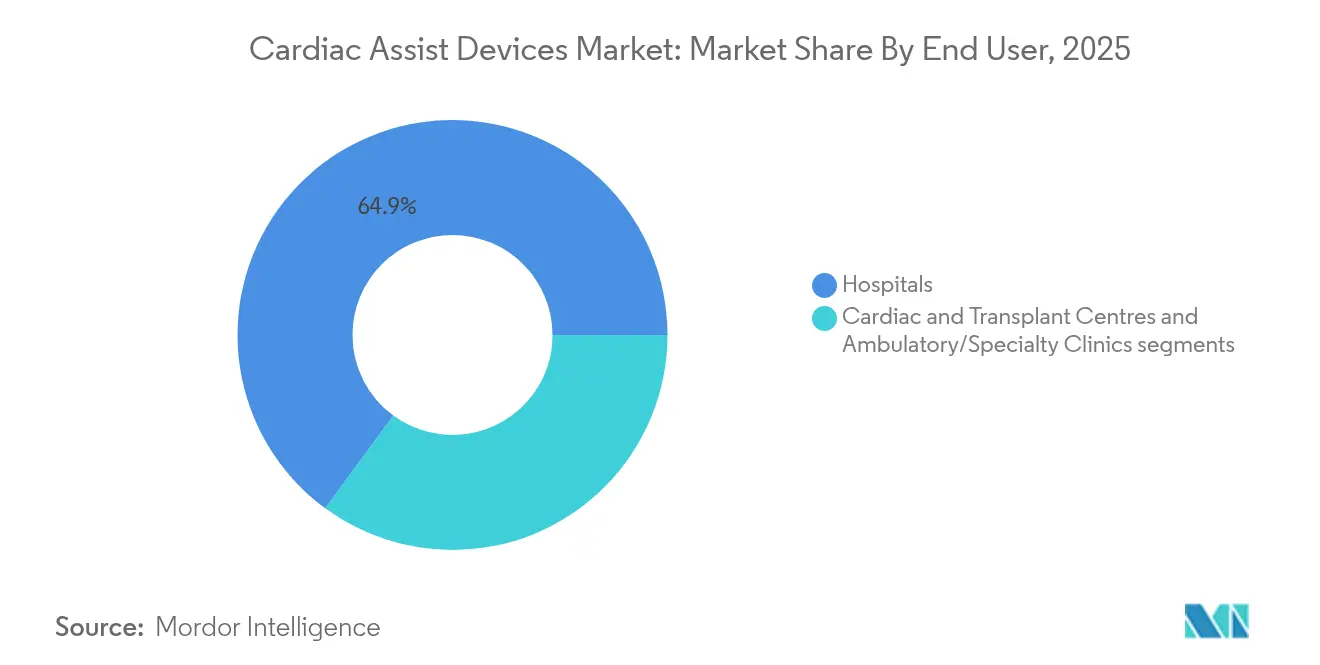

- By end-user, hospitals accounted for 64.92% of the cardiac assist devices market in 2025, whereas ambulatory/specialty clinics are expanding at a 10.18% CAGR through 2031.

- By geography, North America led with 41.08% revenue share in 2025; Asia-Pacific is projected to rise at a 11.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cardiac Assist Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Donor-heart shortage intensifying reliance on LVAD & TAH | +2.1% | Global, with acute impact in North America & Europe | Long term (≥ 4 years) |

| Continuous-flow LVADs lowering rehospitalisation versus pulsatile pumps | +1.8% | Global, led by North America & Europe adoption | Medium term (2-4 years) |

| Expanded indications for TAVR/MCS in moderate HF (FDA & EMA) | +1.5% | North America & Europe, spillover to APAC | Medium term (2-4 years) |

| Reimbursement expansion in Japan & South Korea for destination therapy | +0.9% | Asia-Pacific core, spillover to MEA | Short term (≤ 2 years) |

| Magnetically-levitated micro-pumps enabling full out-of-hospital support | +1.2% | Global, early gains in North America & Europe | Long term (≥ 4 years) |

| Surge in China's domestic VAD clinical trials after 2024 tender reforms | +0.7% | China national, with early gains in Beijing, Shanghai, Guangzhou | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Donor-Heart Shortage Intensifying Reliance on Mechanical Circulatory Support

Fewer than 100 pediatric heart transplants occur annually in China despite 40,000 children hospitalised for heart failure each year. The cardiac assist devices market therefore sees healthcare systems adopting mechanical circulatory support as first-line therapy rather than bridge solutions. Destination-therapy programmes now use devices such as the Aeson artificial heart, which has supported 30 bridge-to-transplant cases with median 156 days of assistance. Newly approved pediatric Impella systems extend percutaneous support to children weighing ≥30 kg, broadening the candidate pool. Survival outcomes with HeartMate 3 exceed five years, rivaling transplant benchmarks. This sustained efficacy repositions mechanical circulatory support as a definitive modality and underpins long-term growth of the cardiac assist devices market.

Continuous-Flow and Percutaneous Devices Lowering Complications Versus Legacy Systems

Full MagLev technology in HeartMate 3 eliminates mechanical wear points, while Impella’s axial-flow design reduces vascular trauma. The ARIES-HM3 study showed patients off aspirin experienced 40% fewer bleeding events, and the DanGer Shock trial reported a 12.7% absolute mortality reduction with Impella CP in STEMI cardiogenic shock jnjmedtech.com. Same-day discharge protocols and subclavian access enable outpatient recovery, lowering inpatient costs and enlarging the cardiac assist devices market. Reduced complication rates, combined with portability, make these systems attractive for both bridge-to-transplant and destination therapy pathways.

Expanded Indications for TAVR/MCS and Percutaneous Support in Moderate HF

In December 2024, the FDA cleared Impella 5.5 and Impella CP for pediatric heart failure, complementing adult cardiogenic shock and high-risk PCI applications. European CE Mark expansions for Aeson and Impella further democratise access across the continent carmatsa.com. Earlier-stage heart-failure patients can now benefit from percutaneous or durable mechanical support, shifting treatment algorithms away from medical therapy alone. This regulatory tailwind lifts adoption across all modalities and drives continued cardiac assist devices market expansion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Class-I recalls (HeartMate 3 EOGO, Medtronic HVAD withdrawal) | -1.4% | Global, acute impact in North America & Europe | Short term (≤ 2 years) |

| Anticoagulation-related bleeding & stroke risk still >20% | -0.8% | Global | Medium term (2-4 years) |

| Limited paediatric-sized fully implantable pumps (capacity bottleneck) | -0.6% | Global, acute impact in North America & Europe, emerging in APAC | Long term (≥ 4 years) |

| Supply-chain dependence on rare-earth magnets for MagLev rotors | -0.4% | Global, with acute impact in China supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Reimbursement Expansion in Japan & South Korea for Destination Therapy

Japan and South Korea now reimburse destination-therapy implantation costs, acknowledging durable VADs’ cost-effectiveness versus repeated hospitalisation. These decisions reduce out-of-pocket expenses and stimulate hospital investment in specialised programmes. With continuous-flow devices achieving longer durability and lower stroke rates, payers foresee improved quality-adjusted life years. Early reimbursement momentum in Asia-Pacific underpins the region’s double-digit CAGR within the cardiac assist devices market.

Class-I Recalls and Safety Concerns Across Device Categories

The April 2024 HeartMate 3 EOGO recall affected 13,883 devices, causing 273 injuries and 14 deaths due to graft obstruction[2]Source: U.S. Food and Drug Administration, “HeartMate 3 EOGO Recall,” fda.gov. Abiomed’s Impella recall over perforation risk led to 129 injuries and 49 deaths fda.gov. These events prompted tougher FDA post-market surveillance, causing some centres to pause VAD and percutaneous pump programmes. Heightened vigilance increases compliance costs and may temporarily temper growth in the cardiac assist devices market.

Anticoagulation-Related Bleeding & Stroke Risk Still >20% for Implantable Devices

Bleeding and stroke remain frequent, with stroke incidence near 13% post-implantation and 31% 30-day mortality. Acquired von Willebrand syndrome exacerbates gastrointestinal bleeding, while tight anticoagulation targets challenge outpatient management annalscts.com. Although aspirin-free HeartMate 3 regimens cut bleeding by 40%, overall risk still constrains patient eligibility, moderating cardiac assist devices market penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: LVADs Lead, Percutaneous Systems Expand

Left ventricular assist devices captured 76.85% of cardiac assist devices market share in 2025, reflecting robust evidence and broad surgical familiarity. The cardiac assist devices market size attributed to LVADs is forecast to grow alongside destination-therapy uptake, buoyed by HeartMate 3’s five-year survival benchmark. Total artificial hearts, such as BiVACOR’s titanium unit, are projected to advance at 10.07% CAGR, offering biventricular support for complex cases. Percutaneous Impella systems complement durable devices by treating acute cardiogenic shock and high-risk PCI, with more than 330,000 patients treated to date jnjmedtech.com. Right ventricular and biventricular assist devices fulfil niche needs, while intra-aortic balloon pumps retain relevance for short-term hemodynamic stabilisation. Collectively these modalities diversify the cardiac assist devices market and mitigate clinical risk across patient cohorts.

Continuous-flow engineering, miniaturisation, and magnetic levitation underpin most next-generation platforms. BrioVAD’s fully levitated rotor aims for quieter operation and reduced hemolysis, whereas magnetically levitated percutaneous micro-pumps promise lower vascular trauma. FDA breakthrough designations accelerate timelines, enabling competitive parity between emerging firms and incumbents. Successful early-feasibility implants validate performance and strengthen investor confidence, sustaining R&D momentum within the cardiac assist devices industry.

By Application: Bridge-to-Transplant Dominates, Acute Support Grows

Bridge-to-transplant indications garnered 38.21% of the cardiac assist devices market in 2025 as donor scarcity prolongs wait times. Destination therapy is projected to rise at 11.35% CAGR, driven by improving durability and payer recognition in Japan and South Korea. The cardiac assist devices market size for destination therapy is expected to expand sharply as clinical results show comparable survival to transplantation. Acute support using percutaneous pumps is gaining momentum after the DanGer Shock data set, which highlighted mortality reductions in STEMI shock, reinforcing guideline updates.

Bridge-to-recovery scenarios benefit from temporary support in myocarditis or post-cardiotomy shock, allowing myocardial rest and potential explant. High-risk PCI support broadens Impella utilisation, and bridge-to-candidacy pathways offer therapy during transplant work-ups. As evidence grows, clinicians integrate mechanical support earlier, converting ad-hoc salvage use into planned therapy lines, thereby enlarging the cardiac assist devices market.

By End-User: Hospitals Lead, Specialised Centres Emerge

Hospitals retained 64.92% of the cardiac assist devices market in 2025 due to surgical infrastructure and intensive monitoring requirements. Academic medical centres pilot new protocols, such as the INNOVATE trial comparing BrioVAD with HeartMate 3. Ambulatory and specialty clinics represent the fastest-growing venue at 10.18% CAGR, empowered by tele-monitoring and subclavian pump access that reduce inpatient length of stay. The cardiac assist devices market size attributable to ambulatory care is poised to widen as wireless sensors facilitate remote supervision.

Catheter labs inside hospitals remain critical for percutaneous deployments, whereas transplant centres anchor volume for durable implants. Emerging community-based heart recovery programmes will widen geographic reach, improving equity of access. Training initiatives and shared-care agreements between tertiary centres and local clinics will support patient transitions, fostering a multisetting ecosystem within the cardiac assist devices industry.

Geography Analysis

North America contributed 41.08% of global revenue in 2025, supported by early FDA approvals, specialised surgical capacity, and robust private-payer coverage. Leading institutions such as the Texas Heart Institute propel first-in-human trials for total artificial hearts, keeping the cardiac assist devices market at the forefront of innovation. Canada and Mexico add incremental demand through cross-border referrals and public-payer programmes.

Europe holds the second-largest share, with Germany, France, and the United Kingdom spearheading adoption through CE-harmonised approvals and integrated transplant programmes. The cardiac assist devices market benefits from universal health coverage, stable reimbursement, and mature surgical training pipelines. Southern European nations leverage medical tourism, while Nordic countries adopt outpatient LVAD pathways, further enhancing utilisation.

Asia-Pacific is the fastest-growing region at 11.74% CAGR, catalysed by China’s post-2024 reforms that incentivise domestic innovation, resulting in the world’s smallest 45-gram artificial heart implant. Japan’s and South Korea’s reimbursement expansions for destination therapy create fertile ground for continuous-flow devices, whereas India and Australia expand catheter-based pump programmes. Regional public-health investment and accelerating cardiovascular disease prevalence sustain long-term growth for the cardiac assist devices market.

Competitive Landscape

The cardiac assist devices market features moderate consolidation, with Abbott’s HeartMate 3 dominating durable VAD placements and Johnson & Johnson MedTech’s Abiomed unit leading percutaneous pumps jnjmedtech.com. BiVACOR, CARMAT, and BrioHealth Solutions are injecting disruption via magnetically levitated total artificial hearts and fully implantable mini-pumps. FDA breakthrough designations and venture funding exceeding USD 300 million since 2024 underpin their advance.

Strategic moves include Abbott’s aspirin-free regimen approval, BiVACOR’s early-feasibility implants, and Johnson & Johnson’s USD 16.6 billion acquisition of Abiomed that bolsters percutaneous dominance. Partnerships integrating remote monitoring and anticoagulation management—such as Abbott’s pact with Cadrenal Therapeutics—aim to differentiate care pathways. Geographic collaboration agreements with Chinese centers allow Western firms to tap fast-growing APAC demand. Meanwhile, indigenous Chinese manufacturers accelerate clinical trials, potentially introducing cost-competitive devices that could pressure established pricing dynamics.

Value-chain participants are prioritising AI-enabled diagnostics, portable power systems, and polymer-free pump housings to mitigate infection risk. Intellectual-property portfolios around magnetic levitation and bearing-less rotors are becoming pivotal. In response to recalls, companies invest in redundant sensor arrays and self-diagnosing firmware to pre-empt device failures, reinforcing trust in the cardiac assist devices industry.

Cardiac Assist Devices Industry Leaders

Abbott Laboratories

BiVACOR Inc.

Getinge AB

Medtronic PLC

Teleflex Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: FineHeart secured ANSM approval for a first-in-human study of its fully implantable Flowmaker LVAD.

- May 2025: BiVACOR received FDA breakthrough device designation for its titanium total artificial heart

- March 2025: Cadrenal Therapeutics partnered with Abbott for the TECH-LVAD trial evaluating tecarfarin with HeartMate 3

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study counts every newly manufactured mechanical pump, whether implantable or percutaneous, that temporarily or permanently supplements a failing heart, including left, right, and bi-ventricular assist devices, intra-aortic balloon pumps, and total artificial hearts. Blood oxygenation systems and extracorporeal membrane oxygenation units remain outside the scope.

Scope exclusion: Stand-alone cardiac rhythm management products and disposable cannula sets are not sized here.

Segmentation Overview

- By Device Type (Value)

- Left Ventricular Assist Devices (LVAD)

- Right Ventricular Assist Devices (RVAD)

- Bi-ventricular Assist Devices (BiVAD)

- Intra-aortic Balloon Pump (IABP)

- Total Artificial Heart (TAH)

- Other Circulatory Support Devices

- By Application (Value)

- Bridge-to-Transplant

- Destination Therapy

- Bridge-to-Recovery

- Other Applications

- By End-User (Value)

- Hospitals

- Cardiac & Transplant Centres

- Ambulatory / Specialty Clinics

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed cardiothoracic surgeons, procurement heads at transplant centers, and regional distributors across North America, Europe, and Asia-Pacific. Discussions validated implant volumes, average device prices, and reimbursement timelines, while short surveys of biomedical engineers helped benchmark failure and replacement rates that are rarely disclosed publicly.

Desk Research

We started with device shipment and therapy utilization files from regulators such as the FDA and EMA, complemented by hospital discharge records published by the CDC and Eurostat. Trade association briefs from the Advanced Medical Technology Association, transplant wait-list statistics from UNOS, and patent families retrieved through Questel enriched the view. Company 10-Ks, investor decks, and selected articles in Circulation provided cost, revision, and survival inputs. These sources are illustrative; many additional references were consulted for cross-checks and clarifications.

A second desk review pass leveraged paid databases, D&B Hoovers for manufacturer revenue splits and Dow Jones Factiva for deal flow, to ground estimates on verifiable financial signals.

Market-Sizing & Forecasting

We applied a top-down reconstruction that begins with advanced heart-failure prevalence, narrows to transplant-ineligible cohorts, and then layers in device penetration rates derived from hospital procedure logs. Results were cross-checked through selective supplier roll-ups and priced using region-specific average selling prices. Key variables like prevalence of NYHA class III/IV heart failure, organ-donor shortages, regulatory approvals, reimbursement tariff shifts, and average device dwell time drive the model. Multivariate regression anchors the five-year forecast, with scenario analysis adjusting for macroeconomic swings and technology adoption curves. Data gaps in bottom-up samples were filled by applying median values from matched facilities before re-triangulation.

Data Validation & Update Cycle

Outputs pass two analyst reviews, variance tests versus historic implant counts, and anomaly flags triggered by quarterly earnings calls. Reports refresh annually; interim updates occur if recalls, reimbursement changes, or landmark clinical results materially alter demand.

Why Mordor's Cardiac Assist Devices Baseline Commands Confidence

Published figures often diverge because firms pick different device baskets, price points, and refresh cadences. We highlight below how those choices influence today's market value.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.34 B | Mordor Intelligence | - |

| USD 3.38 B | Global Consultancy A | Bundles extracorporeal membrane oxygenation systems and balloons used only in cath-lab emergencies |

| USD 1.66 B | Regional Consultancy B | Uses selling prices net of distributor margins and models only implantable ventricular devices |

| USD 0.95 B | Industry Database C | Relies on customs codes that miss hospital-to-hospital transfers and refurbished pumps |

Differences stem mainly from scope width, discount assumptions, and how often numbers are refreshed. By selecting a clinically consistent device set, validating prices with end users, and revisiting models every year, Mordor delivers a balanced, transparent baseline that decision-makers can track and reproduce with confidence.

Key Questions Answered in the Report

What is the projected growth rate of the cardiac assist devices market through 2031?

The ventricular assist devices core segment is forecast to expand at a 9.31% CAGR, lifting the broader market’s value trajectory toward 2031.

Which device category currently dominates global revenues?

Left ventricular assist devices account for 76.85% of 2025 segment sales, reflecting mature clinical evidence and wide surgical familiarity.

How long do patients typically survive with the HeartMate 3 system?

The MOMENTUM 3 study reports median survival exceeding five years, positioning the device as a durable long-term therapy option.

What recent regulatory shifts have widened pediatric access?

In December 2024, the FDA cleared Impella 5.5 and Impella CP for children weighing ≥30 kg and ≥52 kg respectively, opening a new treatment cohort.

Why is Asia-Pacific the fastest-growing regional market?

Ch ina’s post-2024 procurement reforms, plus reimbursement expansion for destination therapy in Japan and South Korea, are propelling a 11.74% regional CAGR. Which safety risks should executives monitor most closely? • Class I recalls tied to graft obstruction or perforation and anticoagulation-related bleeding and stroke—still affecting more than 20% of implant recipients—remain the primary concerns. . . . . . . . New Research Ask me anything...

Page last updated on: