Passport Reader Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

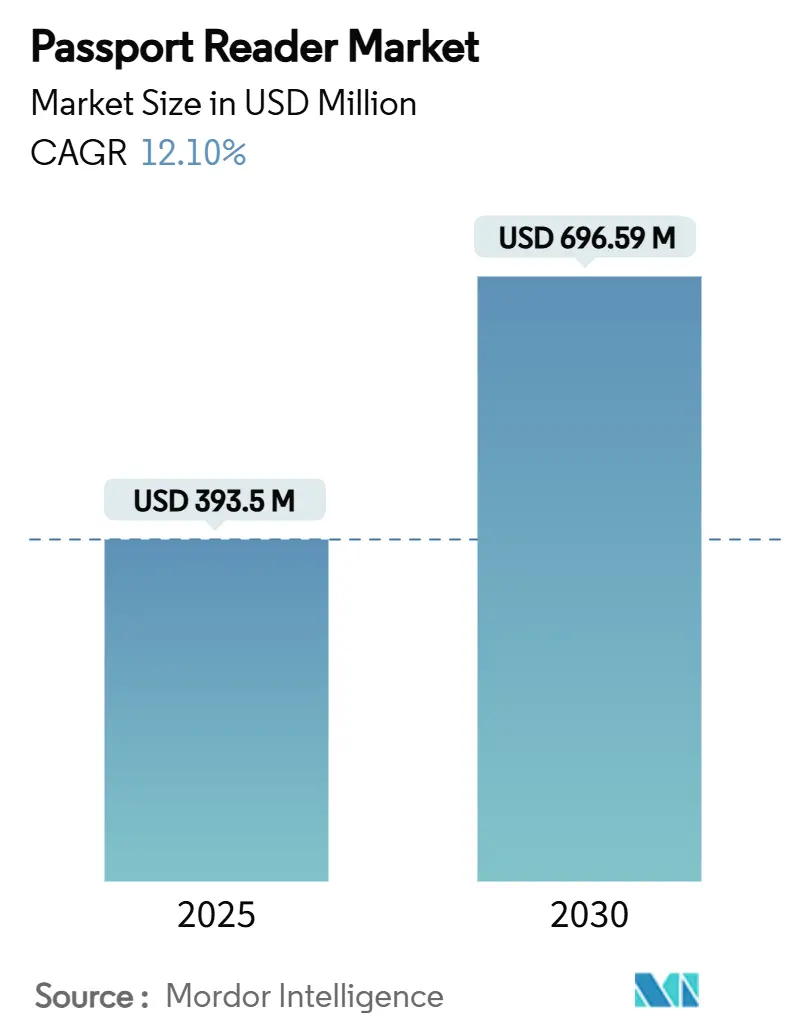

| Market Size (2025) | USD 393.5 Million |

| Market Size (2030) | USD 696.59 Million |

| Growth Rate (2025 - 2030) | 12.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Passport Reader Market Analysis by Mordor Intelligence

The passport reader market size is estimated at USD 393.50 million in 2025 and is forecast to reach USD 696.59 million by 2030, advancing at an annual 12.10% CAGR. Rising air-passenger volumes, the mandatory roll-out of ICAO-9303 e-passport standards, and the rapid adoption of self-service immigration kiosks collectively anchor this expansion. Airlines, airports, and border agencies view automated document verification as a way to reduce queues, curb fraud, and contain staffing costs while meeting strict security requirements. Component prices are moderating as shipment volumes climb, enabling smaller checkpoints to deploy RFID-ready systems that previously felt cost-prohibitive. Supply-side momentum is visible in semiconductor and optics investments that shorten lead times for BAC-compliant readers, while software vendors race to embed AI-based liveness checks that keep pace with emerging privacy rules. Altogether, the passport reader market continues to migrate from early adopter projects into core airport and border infrastructure worldwide.

Key Report Takeaways

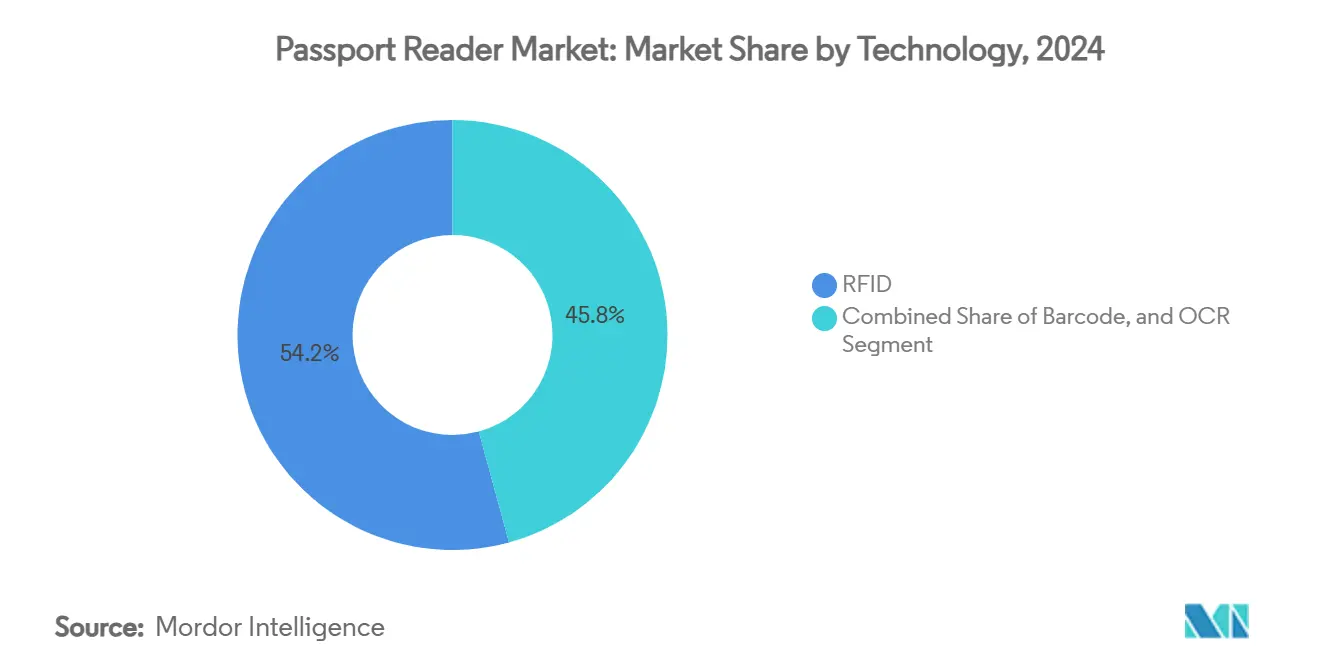

- By technology, RFID led with 54.23% of passport reader market share in 2024. OCR posted the highest technology growth at a 12.16% CAGR through 2030.

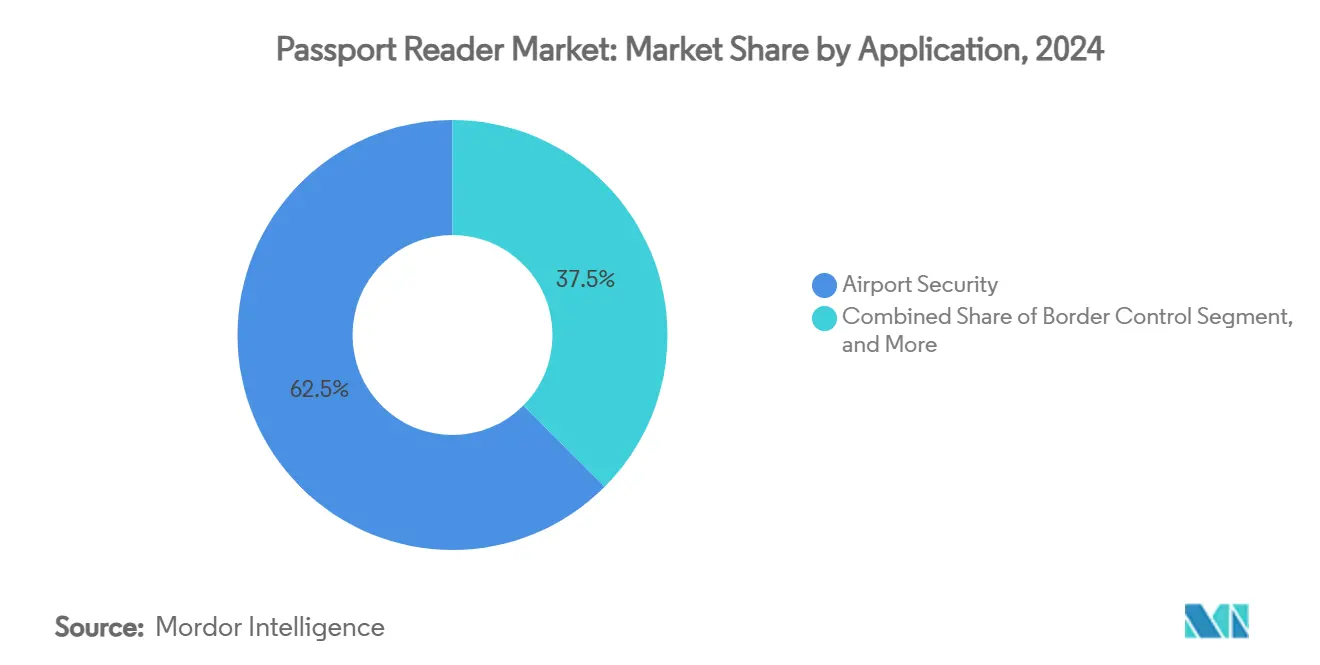

- By application, airport security held 62.52% of the passport reader market size in 2024, whereas border control records the fastest 12.59% CAGR.

- By type, self-service kiosks captured 37.27% of passport reader market size in 2024 and are expanding at 12.41% CAGR.

- By sector, the public sector accounted for 68.43% of passport reader market share in 2024, while private deployments rise 12.81% CAGR through 2030.

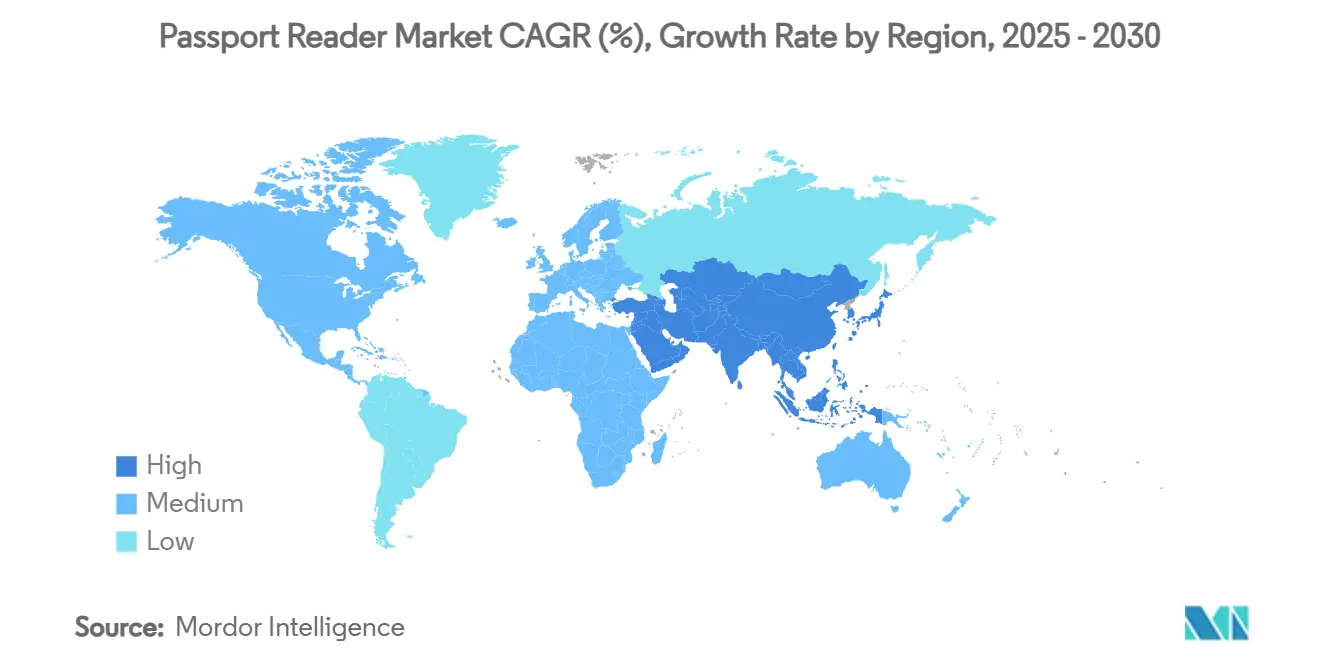

- By geography, North America dominated with 35.91% share in 2024; Asia-Pacific is forecast to log an 12.46% CAGR to 2030.

Global Passport Reader Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to ICAO-9303 e-passport standards | +2.1% | Global with Asia-Pacific and MEA acceleration | Medium term (2-4 years) |

| Escalating global air-passenger volumes | +1.8% | North America and Asia-Pacific hubs | Long term (≥ 4 years) |

| Heightened border-security funding post-COVID | +1.5% | North America and EU; spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Mandatory RFID/BAC upgrades at checkpoints | +1.3% | Schengen, US CBP and broader global roll-outs | Medium term (2-4 years) |

| API-based biometric-as-a-service integrations | +0.9% | North America and EU, urban Asia-Pacific | Long term (≥ 4 years) |

| Deployment in digital-nomad visa lounges | +0.4% | Worldwide visa hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid shift to ICAO-9303 e-passport standards

ICAO Document 9303 creates a universal blueprint for reading the 1 billion e-passports in global circulation, obliging vendors to bake multispectral imaging, BAC, and EAC cryptography into new devices. [1]ANSI, “Secure Biometrics: ICAO E-Passports,” ansi.org Poland’s 130-office rollout, powered by Neurotechnology’s SDK, shows how compliance slashes fingerprint match times and trims application queues. Early-moving governments now process passports in seconds, whereas laggards still face multi-minute checks that frustrate travelers and inflate labor needs. The next-wave Digital Travel Credential framework will rely on NFC hand-offs to smartphones, ensuring the passport reader market keeps shifting toward mobile-first verification.

Escalating global air-passenger volumes

Air travel rebounded sharply in 2025, and Chicago O’Hare’s automated passport kiosks cut average wait time by 33%, proving why airports see immediate ROI on self-service units. [2]Airport Improvement, “Self-Service Passport Readers Reduce Wait Times at O’Hare Int’l,” airportimprovement.com One kiosk clears passengers roughly five times faster than manual inspection, allowing terminals to meet peak-hour surges without expanding real estate. Istanbul New Airport’s 200 million-passenger blueprint showcases the same logic: passport readers tethered to video-conferencing support let a small team handle flows once requiring dozens of desks. As throughput tips past 2019 records, operators embed passport readers at bag-drop, boarding, and lounge access points, further enlarging the passport reader market.

Heightened border-security funding post-COVID

Washington, London, and Kuala Lumpur have redirected stimulus outlays to fully automated gates, iris capture, and biometric match-against-watchlist platforms. The UK Home Office earmarked GBP 195 million for its new Border Crossing and Helios suites, incorporating next-generation passport readers. [3]Find-Tender Service, “Home Office Crossing the Border Procurement 2024,” find-tender.service.gov.ukMalaysia’s MYR 617 million order for chips and polycarbonate pages secures multi-year reader demand that ripples across optics and RFID supply chains. Stable public budgets give manufacturers the confidence to finance R&D in quantum-safe encryption and contactless fingerprint capture—features expected to shape the passport reader market through 2030.

Mandatory adoption of RFID/BAC upgrades at checkpoints

EU rules requiring facial images and fingerprints on chip have set a hard replacement deadline for thousands of legacy readers. Ivory Coast’s 15-year concession with Zetes, projected to gross EUR 60 million, illustrates how mandates generate predictable revenue streams for suppliers. DERMALOG’s fast-gate deployment in the Maldives shows that once a country commits, it usually swaps the entire lane layout, lifting average deal sizes far above single-unit refreshes. Chip-reading complexity raises the moat for incumbents and reinforces the passport reader market’s moderate consolidation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex for full-page multispectral units | -1.4% | Smaller airports and remote borders worldwide | Short term (≤ 2 years) |

| Data-privacy and RFID-skimming concerns | -0.8% | EU and North America | Medium term (2-4 years) |

| Shortage of precision optical sensors | -1.1% | Semiconductor-dependent regions | Short term (≤ 2 years) |

| Reader incompatibility with decentralized ID | -0.6% | Early adoption markets in EU and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High capex for full-page and multispectral readers

State-of-the-art optics, infrared LEDs, and secure microcontrollers push unit prices beyond the budgets of many regional airports. Australia’s audit of passport procurement found limited competitive bidding, suggesting smaller agencies must accept premium prices and vendor lock-in. The DRC example, where citizens pay USD 185 for a biometric booklet while most proceeds go offshore, underscores how steep equipment costs cascade into end-user fees. This restraint slows replacement cycles and keeps a chunk of the passport reader market tied to older swipe models.

Data-privacy and RFID-skimming concerns

EU regulators insist that any chip-reading workflow protect personally identifiable information by default. Projects now add metallic shielding and stronger AES encryption, nudging hardware bills upward and lengthening certification timelines. Privacy advocates also push hotels to scan passports without storing scans, which forces vendors to invest in on-device cryptography and zero-knowledge proofs that still hit throughput targets. Although these upgrades ultimately enhance trust, they temporarily temper deployment speed in the passport reader market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: RFID consolidation amid OCR acceleration

RFID-enabled readers processed the majority of cross-border travelers in 2024, claiming 54.23% passport reader market share thanks to millisecond chip access and standards-aligned cryptography. IDEMIA’s ISO 18013-5 certification for its mIDReader shows suppliers merging mobile ID and chip reading in a single workflow, which future-proofs passenger checkpoints. OCR still posts a lively 12.16% CAGR, favored by banks and hotels that must read legacy documents issued pre-chip. Vendors now layer machine-learning OCR on top of contactless interfaces, delivering hybrid stations able to pivot between physical and digital travel credentials. That evolution helps sustain the passport reader market well past the chip transition phase.

In parallel, barcode scanners remain niche, particularly in issuing offices scanning provisional travel docs. Yet most governments view chip-first strategies as the core path, ensuring that mixed-technology readers will dominate the passport reader industry road map through 2030.

By Type: Self-service kiosks accelerate autonomous processing

Self-service kiosks represented 37.27% of passport reader market size in 2024 and show the fastest 12.41% CAGR through 2030. These eye-level booths fuse NFC antennas, full-page imaging cameras, and biometric facial match into one enclosure, enabling lean staffing models at airlines and immigration posts. Delhi Airport’s biometric kiosk installation cut per-passenger immigration clearance to under 30 seconds, illustrating the throughput gains fueling kiosk adoption. Meanwhile, swipe readers remain indispensable in embassy back-rooms that prioritize audit logging over high speed.

Ongoing upgrades add voice prompts, motorized camera height adjustment, and mobile boarding-pass NFC readers, letting one kiosk serve multiple flows from visa issuance to e-Gate enrollment. This versatility keeps self-service kiosks at the center of the passport reader market growth narrative.

By Application: Airport security maintains lead while border control surges

Airports consumed 62.52% of passport reader market size in 2024, reflecting decades of TSA PreCheck investment and airline boarding-gate integration. Yet border control facilities post the strongest 12.59% CAGR to 2030 as governments modernize land and sea crossings. DERMALOG’s Maldives deployment shows how remote islands adopt biometric e-gates to ease tourism flows while tightening watchlist screening. Ancillary uses in banking and hospitality gradually enlarge the total addressable passport reader market but remain secondary volume contributors.

Inter-agency data sharing increasingly links airport security and land-border programs, nudging vendors to design multi-protocol readers configurable by software update, rather than hardware replacement. That convergence protects customer capex and cements reader fleets as 10-year assets.

By Sector: Public procurement dominates, private momentum builds

Government agencies controlled 68.43% passport reader market share in 2024, buoyed by tender cycles and sovereign mandates. The private-sector channel, however, posts 12.81% CAGR, led by banks such as ASB that saw a fivefold drop in branch visits after rolling out NFC passport onboarding. Hotels accelerate too, installing compact readers at concierge desks to shrink check-in to under a minute. Insurance, telecom, and coworking operators follow suit, suggesting private use cases will account for an increasing slice of the passport reader market by 2030.

API-first architecture lets corporates plug passport validation into KYC workflows without storing any personal data, addressing privacy laws while expanding deployment beyond traditional security checkpoints.

Geography Analysis

North America retained 35.91% of passport reader market share in 2024 on the back of TSA PreCheck’s nationwide footprint and Clear Secure’s 147 airport lanes, which lifted the vendor’s revenue 40% year-over-year. The BEAGLE framework signed in May 2025 streamlines procurement across Department of Homeland Security branches, ensuring a steady five-year pipeline for compliant readers. Canada and Mexico synchronize tech specs for trusted-traveler schemes, ensuring interoperability and pushing vendor demand deeper into land crossings.

Asia-Pacific is the fastest-growing region at 12.46% CAGR, with Malaysia’s MYR 617 million biometric passport program, Indonesia’s Batam seaport facial recognition lanes, and Hong Kong’s QR-enabled corridors to Macao all reinforcing the growth trajectory. China, India, and Japan fuel volume via smart-airport buildouts that bundle readers, e-Gates, and facial recognition under single-vendor contracts, compressing deployment timelines.

Europe sustains mid-single-digit growth as the EU Digital Identity Wallet initiative urges member states to harmonize chip standards, while the UK plows GBP 195 million into its next-gen border platform. Schengen reforms push agencies to install readers capable of handling multiple biometric modalities, ensuring future compliance. In the Middle East and Africa, Dubai’s one-second passport control benchmark and Ghana’s fee-cut e-passport campaign highlight the region’s leapfrog potential. Collectively, these programs broaden the geographic base for the passport reader market and mitigate reliance on any single corridor.

Competitive Landscape

Competition remains moderately concentrated, with the top five vendors holding an estimated 55% revenue share, a level that rewards scale but leaves headroom for niche innovators. Thales increased its Digital Identity and Security sales 15.7% to EUR 2.914 billion in 2024, underscoring how diversified defense-plus-identity portfolios insulate against cyclical public-sector orders. ASSA ABLOY folded IXLA’s laser-engraving technology into HID Global’s line, giving it end-to-end coverage of personalization, issuance, and reader hardware.

IDEMIA leads biometric accuracy contests, topping the U.S. DHS RIVTD test in January 2025, which bolsters its bids for large-scale reader contracts that hinge on liveness detection. Patent filings show emergent players targeting blockchain-anchored audit trails and quantum-safe firmware, signaling future differentiation points. Component shortages, notably in NFC-tag lines, still pose tactical risks; vendors with in-house chip sourcing, such as Thales and IDEMIA, can cushion margins better than pure-play scanner firms.

Regional specialists thrive by tailoring firmware to local scripts and visa regulations, proving that even in a consolidated passport reader industry, service proximity and compliance expertise open doors. As private-sector opportunities scale, subscription models featuring remote device management and over-the-air security patches could tilt revenue mixes away from one-off hardware sales toward recurring platforms.

Passport Reader Industry Leaders

Thales Group

HID Global Corporation

Vision-Box – Soluções de Visão Por Computador SA

IDEMIA Group

Regula Forensics Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: IDEMIA Public Security topped DHS RIVTD biometric accuracy rankings, cementing leadership in liveness detection.

- January 2025: Dominican Republic awarded a 5 million biometric-passport contract using a supplier-financed model to start issuance in August 2025.

- January 2025: Malaysia extended Datasonic’s biometric passport supply deal by MYR 104.78 million (USD 23.86 million).

- December 2024: IDEMIA Smart Identity unveiled laser-engraved IDQR codes that allow remote smartphone verification.

Global Passport Reader Market Report Scope

| RFID |

| Barcode |

| OCR |

| Swipe Readers |

| Self-Service Kiosk |

| Compact Full-Page Reader |

| Other Types |

| Airport Security |

| Border Control |

| Other Applications |

| Public |

| Private |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Technology | RFID | ||

| Barcode | |||

| OCR | |||

| By Type | Swipe Readers | ||

| Self-Service Kiosk | |||

| Compact Full-Page Reader | |||

| Other Types | |||

| By Application | Airport Security | ||

| Border Control | |||

| Other Applications | |||

| By Sector | Public | ||

| Private | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What dollar value will automated passport readers generate by 2030?

The passport reader market size is projected to reach USD 696.59 million by 2030.

Which technology is advancing fastest inside passport checkpoints?

OCR-powered readers grow at 12.16% CAGR as AI boosts character-recognition accuracy for legacy documents.

Why are self-service kiosks attracting airports?

Kiosks merge passport scanning, facial match, and database queries, letting airports cut queues and staffing costs while maintaining security compliance.

Which region is gaining share the quickest?

Asia-Pacific posts the highest 12.46% CAGR thanks to major biometric border upgrades in Malaysia, Indonesia, and China.

How are privacy rules shaping future deployments?

EU and North American regulations mandate stronger encryption, shielding, and zero-knowledge proofs, pushing vendors to embed advanced on-device cryptography without sacrificing throughput.

What level of market concentration exists among suppliers?

The passport reader market earns a score of 6 on a 10-point scale, indicating that while the top five vendors control more than half of sales, meaningful opportunities remain for regional specialists.

Page last updated on: