Cardiology Information System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

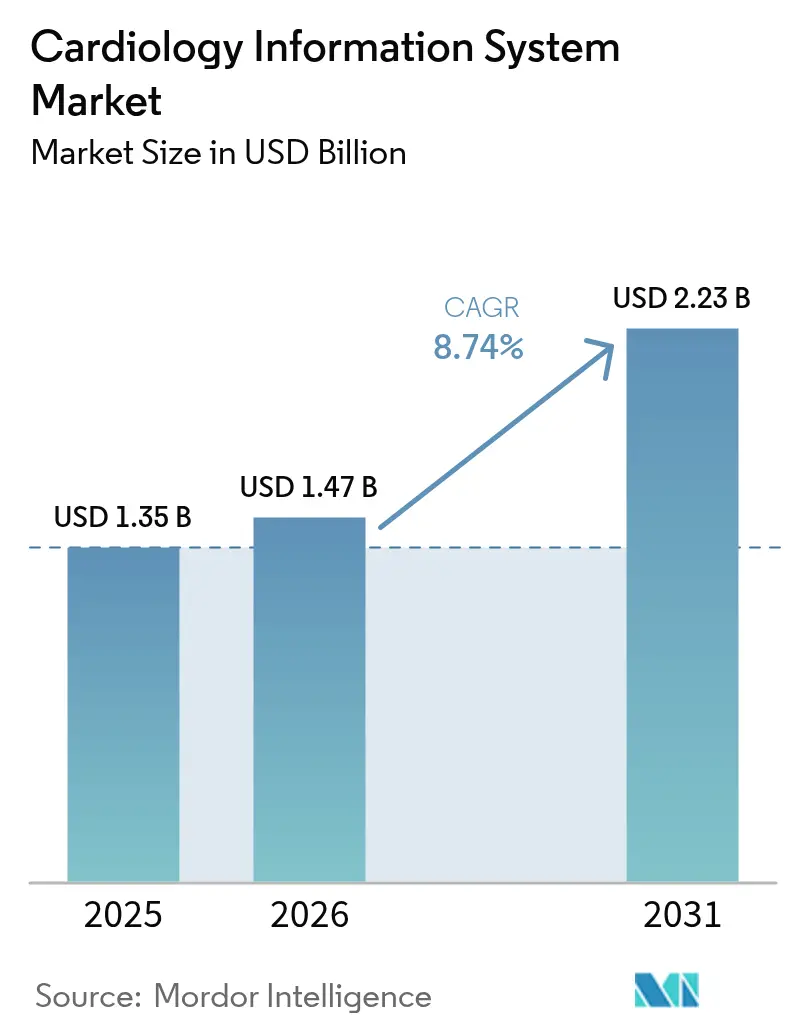

| Market Size (2026) | USD 1.47 Billion |

| Market Size (2031) | USD 2.23 Billion |

| Growth Rate (2026 - 2031) | 8.74% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players/cardiovascular-information-system-market---growth,-trends,-and-forecast-(2020---2025)_CVIS_-_MP.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cardiology Information System Market Analysis by Mordor Intelligence

The Cardiology Information System Market size was valued at USD 1.35 billion in 2025 and estimated to grow from USD 1.47 billion in 2026 to reach USD 2.23 billion by 2031, at a CAGR of 8.74% during the forecast period (2026-2031). Growing cardiovascular disease prevalence, the push for national digital-health mandates, and faster FDA clearances for artificial intelligence tools are creating a large addressable base for modern cardiac IT solutions. Industry leaders are moving quickly to embed structured reporting, predictive analytics, and automated image interpretation so that over-worked cardiologists can manage higher procedure volumes without compromising care quality. Vendor neutrality, native interoperability with mainstream electronic health record suites, and modular architectures that allow phased migrations are emerging as standard bid requirements. At the same time, hospitals are reassessing long-standing radiology-centric platform decisions because bundled-payment models tie reimbursement directly to cardiac outcomes. As a result, the cardiology information system market is witnessing intensified competition across cloud, edge, and hybrid deployment formats that balance cybersecurity with workflow gains.

Key Report Takeaways

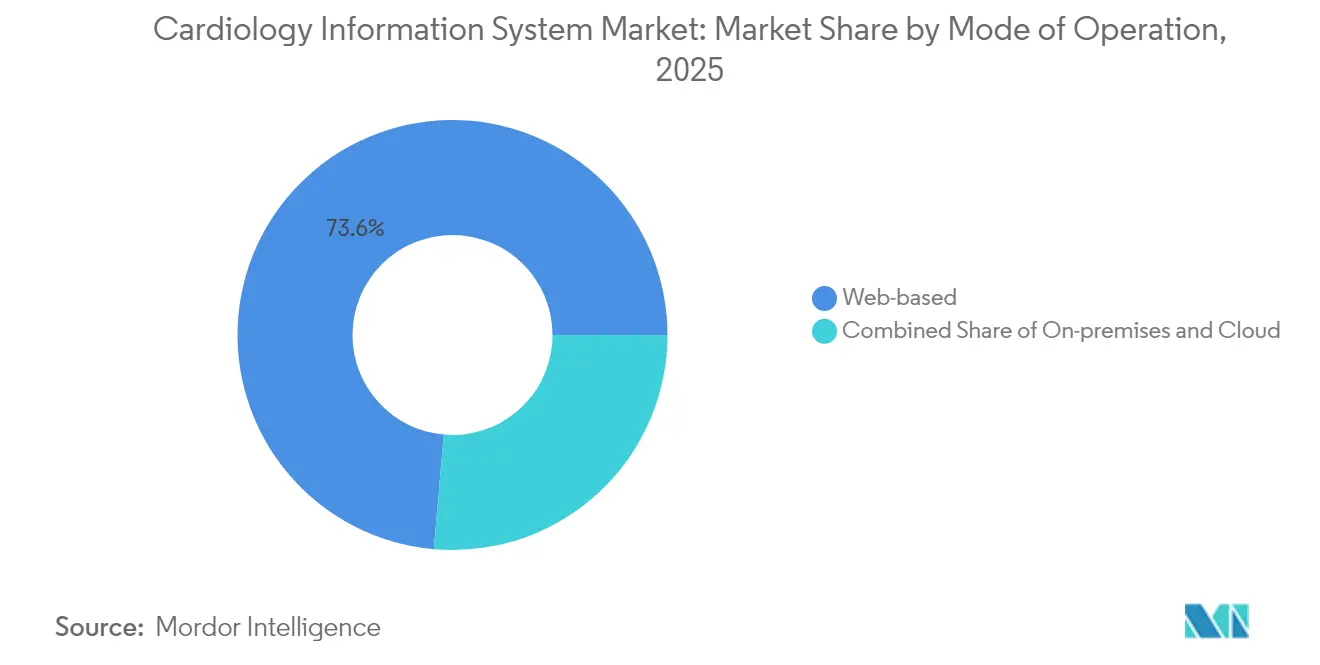

- By deployment model, web-based systems led with 73.62% revenue share in 2025; cloud/SaaS platforms are projected to expand at a 10.21% CAGR through 2031.

- By component, software secured 50.88% revenue share in 2025, while the services segment is forecast to grow at 9.97% CAGR to 2031.

- By system type, cardiovascular information systems captured 55.02% revenue share in 2025; cardiology PACS is expected to post a 9.56% CAGR through 2031.

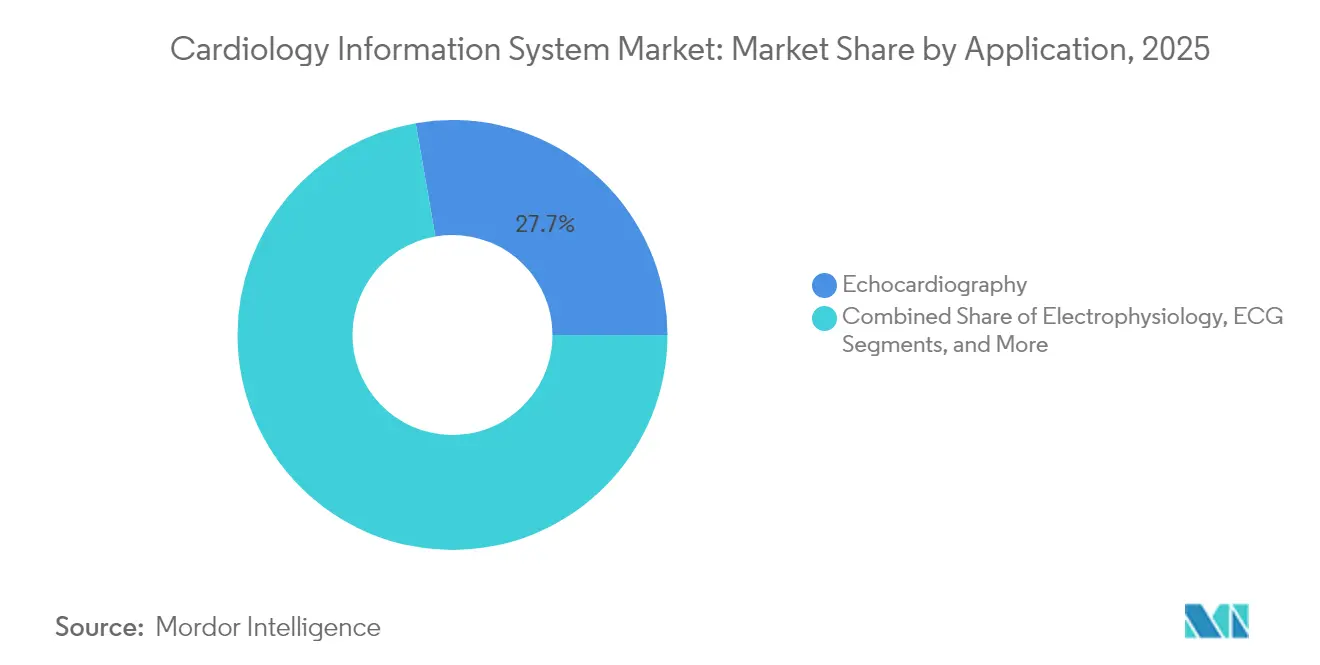

- By application, echocardiography accounted for 27.74% revenue share in 2025; ECG & stress testing is on track for a 9.74% CAGR to 2031.

- By end-user, hospitals dominated with 64.71% revenue share in 2025; ambulatory surgical centers are set to grow at a 9.41% CAGR through 2031.

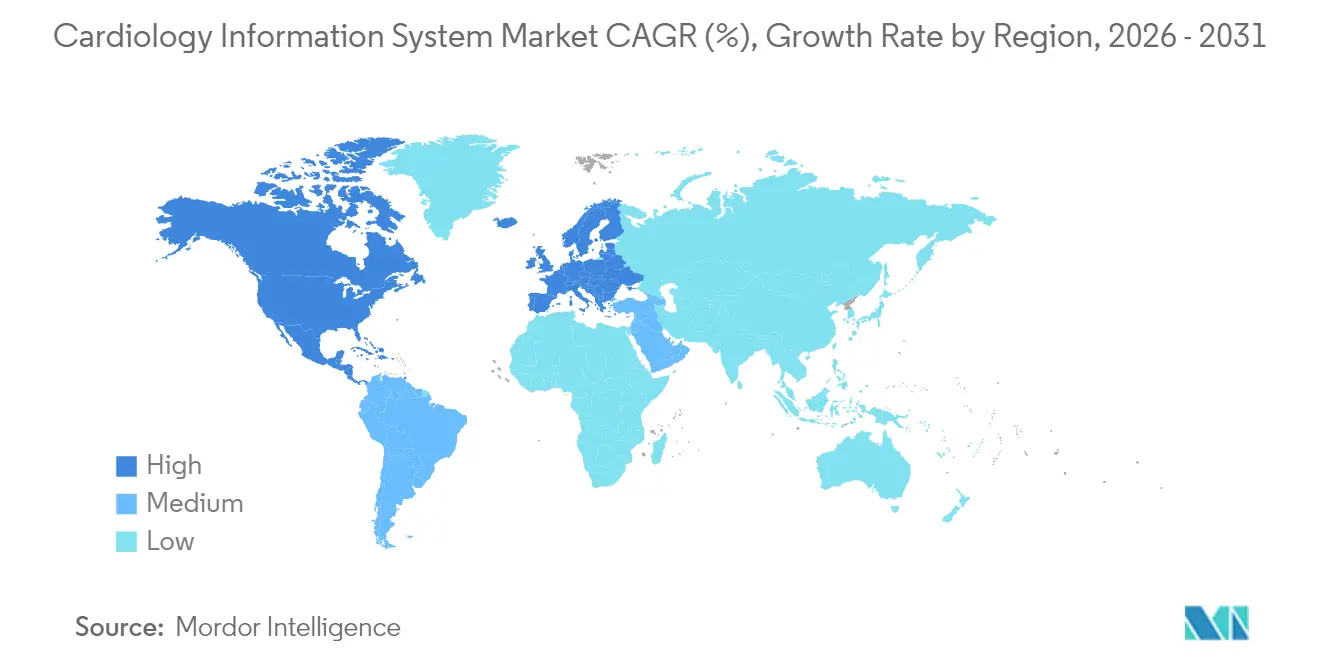

- By region, North America held 42.31% revenue share in 2025, whereas Asia-Pacific is positioned for a 10.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cardiology Information System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in global prevalence of cardiac diseases & stroke | +2.1% | Global, with highest impact in APAC and MEA | Long term (≥ 4 years) |

| Government funding for digital cardiology & EHR mandates | +1.8% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Shift to value-based care & demand for enterprise imaging | +1.5% | North America core, spill-over to EU | Medium term (2-4 years) |

| Expansion of ambulatory & ASC cardiac procedures | +1.2% | North America & Australia, emerging in EU | Short term (≤ 2 years) |

| AI-powered decision support improving cardiologist workflow | +1.7% | Global, led by North America and developed APAC | Short term (≤ 2 years) |

| Cloud-native CVIS platforms enabling mid-tier hospital adoption | +0.9% | Global, particularly mid-tier markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise in Global Prevalence of Cardiac Diseases & Stroke

Cardiovascular disease cases almost doubled between 1990 and 2024, reaching 523 million and underscoring the structural need for scalable informatics platforms in both mature and emerging health systems [1]Gregory A. Roth, “Global Burden of Cardiovascular Diseases and Risk Factors, 2024,” Journal of the American College of Cardiology, jacc.org. Low- and middle-income regions now represent 80% of global cardiovascular deaths, yet diagnostic infrastructure remains limited, prompting ministries to mandate cost-efficient cloud access to imaging, hemodynamics, and structured reporting modules. Ischemic heart disease and stroke together contribute more than one-third of total mortality, amplifying the urgency for predictive analytics that identify high-risk cohorts before costly acute events occur. Payers in Asia-Pacific and the Middle East have begun financing population-level screening that feeds directly into national cardiology information system market deployments. Health systems are also directing stimulus funds toward vendor-neutral archives that support life-long longitudinal records, providing the clinical backbone for disease-management programs. These moves signal durable demand for interoperable, AI-enabled cardiology information system market platforms able to manage escalating caseloads with constrained specialist supply.

Government Funding for Digital Cardiology & EHR Mandates

In the United States the Centers for Medicare & Medicaid Services tie reimbursement bonuses to certified EHR interoperability, and recent Local Coverage Determinations now pay for AI-enabled coronary CT analysis that feeds output directly into cardiology information system market workflows [2]CMS Staff, “Promoting Interoperability Programs,” Centers for Medicare & Medicaid Services, cms.gov. The 21st Century Cures Act imposes stiff penalties for information blocking, forcing mid-tier hospitals that previously postponed investments to adopt standards-based interfaces for cardiovascular images and structured reports. Europe is following with the European Health Data Space, which compels cross-border data exchange, favoring comprehensive over point solutions. Asia-Pacific governments, led by Singapore and South Korea, offer matching grants that offset initial subscription costs for cloud platforms. Collectively these policies lower total cost of ownership and accelerate budget approvals, lifting adoption curves in markets that were formerly restrained by cap-ex constraints.

Shift to Value-Based Care & Demand for Enterprise Imaging

Bundled payments and accountable-care targets place direct financial accountability on hospitals for 30-day and 90-day cardiac outcomes, driving immediate interest in enterprise imaging strategies that integrate radiology, cardiology, and vascular data silos. Two-thirds of US provider networks now plan to fold cardiology into cross-departmental image strategies so that clinicians share common viewers, archives, and analytics dashboards. Purchase committees increasingly score vendors not only on modality support but also on evidence that their cardiology information system market platforms can reduce length-of-stay and readmission penalties. Cloud-based enterprise repositories further allow rural spoke sites to upload catheterization studies for specialist over-read, a capability that directly supports value-based contracts where geographically dispersed care teams must coordinate seamlessly.

AI-Powered Decision Support Improving Cardiologist Workflow

The US FDA has cleared more than 160 AI solutions specifically for cardiology, making it the second most AI-adopted specialty after radiology. Approved algorithms now automate wall-motion scoring, coronary plaque quantification, and arrhythmia detection, reducing interpretation times by up to 50% in peer-reviewed trials. These gains matter because national workforce studies predict a shortage of up to 15,800 cardiologists by 2030, while almost half of US counties currently have no practicing cardiologist on site. Structured reporting modules that auto-populate measurements and annotate key findings are therefore attracting premium pricing among health systems striving to improve throughput without hiring. Vendors that seamlessly embed FDA-cleared AI into the cardiology information system market user interface are differentiating on measurable time savings, not just algorithm accuracy, and thus secure multiyear enterprise contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront investment & integration costs | -1.4% | Global, particularly acute in emerging markets | Short term (≤ 2 years) |

| Reluctance to change existing PACS/EMR workflows | -0.8% | North America & EU, legacy system prevalence | Medium term (2-4 years) |

| Cyber-security & data-sovereignty concerns in multi-cloud | -0.7% | Global, heightened in regulated industries | Long term (≥ 4 years) |

| Shortage of CVIS-literate cardiology IT talent | -0.6% | Global, most severe in rural and emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Investment & Integration Costs

Full-scope cardiology information system market deployments often exceed USD 1 million when hardware, interfaces, and change-management services are included, a figure that deters medium-sized hospitals despite proven clinical returns. Legacy radiology archives and closed hemodynamic modules complicate integration, stretching project timelines well beyond twelve months and locking scarce informatics staff into prolonged test cycles. Even where cloud-subscription pricing eliminates servers, data-migration fees and workflow redesign expenses remain material. Leading children’s hospitals cut almost USD 3 million over five years by pivoting to vendor-neutral archives, showing savings are possible but require scale and negotiating clout. Newer subscription models that bundle implementation services are gaining traction, yet take-up is slow because boards still prioritize physician recruitment and facility expansion over back-office IT upgrades.

Cyber-Security & Data-Sovereignty Concerns in Multi-Cloud

A spike in ransomware attacks on US hospitals has raised the bar for due-diligence audits, with procurement teams now demanding detailed encryption roadmaps, cyber-liability coverage, and in-region data-replication for every cardiology information system market proposal. European buyers invoke GDPR rules that prohibit patient data from leaving the bloc unless equivalent safeguards exist, compelling vendors to build geo-fenced tenants that inflate operating costs. Australia and Canada impose additional health-data residency mandates, further fragmenting deployment options. While distributed ledger and confidential compute techniques promise stronger controls, most IT departments lack the headcount to manage these advanced architectures, delaying go-lives or steering buyers back toward on-premises appliances.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Operation: Cloud Platforms Drive Digital Transformation

Cloud & SaaS models are growing at a 10.21% CAGR and are visibly eroding the once unassailable dominance of browser-hosted systems that still account for 73.62% of 2025 revenue. Subscription pricing appeals to budget-constrained regional hospitals because outlays shift from capital to operating budgets, and vendors now guarantee 99.9% uptime that rivals internal datacenters. The cardiology information system market size for cloud deployments is projected to rise faster than any other mode, especially inside multi-site ambulatory networks created by private-equity roll-ups. On-premises clusters persist in jurisdictions with strict data-sovereignty rules or military-health installations where air-gap policies remain. Yet even those buyers are experimenting with hybrid stacks that sync anonymized datasets to analytic workspaces in the public cloud during off-peak hours.

Cloud adoption triggers new evaluation criteria, including availability of modern RESTful APIs, single-sign-on workflows, and serverless analytics pipelines that crunch hemodynamic waveforms in near real time. Cardiologists value the ability to launch advanced 3-D visualizations on lightweight laptops without loading client software, and health-system CFOs prefer the predictable per-study fees that align cost with procedure growth. A second accelerant is the cardiology information system market demand from ambulatory surgical centers, which reached 0.87 PCI procedures per 10,000 Medicare beneficiaries in 2022 and requires instant image exchange with referral hospitals. Vendors that pre-integrate cardiovascular modules into leading EHRs therefore secure rapid cycle wins in markets where in-house IT skills remain thin.

By Components: Services Growth Reflects Implementation Complexity

Software still commands 50.88% of 2025 revenue, yet services are advancing at a faster 9.97% CAGR because boards realize technology alone cannot deliver operational gains. Comprehensive go-lives demand interface scripting, workflow mapping, physician onboarding, and multi-site change management that few hospital IT teams can absorb. The cardiology information system market size generated by services is thus expected to approach parity with licenses by decade-end as buyers bundle three- to five-year optimization retainers into master agreements. Hardware growth is tapering because hyper-converged appliances consolidate compute and storage footprints, but demand remains solid in high-throughput cath labs that require deterministic processing for hemodynamic acquisition.

Integration services are the fastest-growing sub-segment because Epic, Oracle, and Meditech clients seek real-time triggers that push structured echocardiography findings directly into clinical notes. Vendors that maintain catalogues of pre-built connectors for Abbott, GE, and Philips modalities shorten time-to-value and thus capture larger service envelopes. Education programs are equally pivotal: health systems invest in week-long boot camps so that nursing staff can configure templates and minimize dependence on vendor help desks. As a result, analysts expect the cardiology information system market to place comparable strategic weight on professional-services depth and software feature breadth during 2025-2030 RFP cycles.

By System Type: CVIS Platforms Maintain Leadership Despite PACS Growth

Comprehensive cardiovascular information systems held 55.02% revenue share in 2025 because they merge imaging, waveforms, inventory, and billing into a single database that supports enterprise dashboards. The cardiology information system market share for these platforms remains solid even as specialized cardiology PACS logs a 9.56% CAGR; standalone imaging archives appeal to dedicated heart centers that already run enterprise EMRs and need only lightweight image management. Integrated CVIS-PACS suites are emerging so that health systems can phase migrations, replacing PACS first and layering full workflow modules later.

Vendor roadmaps increasingly highlight micro-service architectures that allow customers to activate discrete modules—stress reporting, nuclear cardiology, or structured ECG—without a time-consuming big-bang replacement. This modularity keeps incumbent vendors defensible yet creates openings for cloud-native challengers that ship continuous feature updates under FDA-approved change-control plans. Major players such as Siemens Healthineers pitch Sensis Vibe as a documentation hub that can dock into older archives, demonstrating an awareness that mature hospitals favor incremental modernization paths. The cardiology information system market therefore rewards suppliers who respect existing investments while offering clear migration ladders to full workflow convergence.

By Application: Echocardiography Leadership Faces ECG Innovation Pressure

Echocardiography generated 27.74% of 2025 revenue and remains the clinical mainstay because ultrasound is non-invasive, portable, and relatively affordable. Nevertheless, ECG & stress-testing now posts the fastest 9.74% CAGR thanks to cloud-connected patches and AI tools that flag silent arrhythmias during routine activity monitoring. Catheterization-lab modules gain momentum as outpatient PCI volumes rise, and electrophysiology suites demand high-resolution image fusion to guide ablation procedures. The cardiology information system market size attached to nuclear cardiology remains niche yet steady, particularly in Latin America, where adoption lifts as supply-chain bottlenecks ease.

Artificial intelligence is reshaping modality rankings: Philips validated an algorithm that scores regional wall-motion abnormalities at expert-level precision, trimming physician read times by half . Start-ups offer cloud APIs that analyze 12-lead ECGs in near real time and funnel results into structured CVIS notes, making rhythm data as searchable as imaging metadata. As reimbursement expands for remote cardiac monitoring, vendors that harmonize imaging, waveform, and wearable feeds inside one viewer will gain a lasting edge. This shift keeps the cardiology information system market in flux as buyers rethink application priorities to match multidisciplinary care pathways.

By End-User: ASC Growth Challenges Hospital Dominance

Hospitals still produce 64.71% of 2025 revenue because they host full cardiac service lines, run continuous ICU monitoring, and employ the specialists who approve capital purchases. Yet ambulatory surgical centers record a compelling 9.41% CAGR now that Medicare pays for elective PCI outside hospital walls. Private-equity groups have acquired more than 342 clinic sites since 2013, standardizing workflows on cloud Saas platforms to ensure uniform quality metrics. Specialty cardiology clinics also add incremental demand, though budgets remain tighter and emphasis lies on interoperability with hospital portals for smooth referral cycles.

The cardiology information system market responds with lighter subscription tiers that fit ASC capital profiles while still offering cath-lab image management, stress testing, and outcomes dashboards. Rural ASCs often lack full-time cardiologists, so cloud tools that route images to city-based readers help maintain procedure throughput without on-site staffing. Hospitals counter by deploying enterprise platforms that cover employed and affiliated sites, creating a network-wide data spine that discourages piecemeal vendor encroachment. In this tug-of-war vendors must prove they can span a heterogeneous estate of surgical centers, outreach clinics, and flagship tertiary hospitals under a single license framework.

Geography Analysis

North America, responsible for 42.31% of 2025 revenue, benefits from deep EHR penetration, well-defined Medicare add-on payments, and an FDA pipeline that clears cardiology AI faster than any other region. However, 46% of US counties have no resident cardiologist, forcing health systems to rely on tele-interpretation and workload triage dashboards that the cardiology information system market increasingly embeds as core features. Private-equity capital flows toward cardiology ASCs intensify the push for cloud-first deployments that scale across multi-state footprints without on-premises servers. Cyber-security remains a board-level worry, and the White House ransomware task-force advisories place additional compliance obligations on multi-cloud architectures.

Asia-Pacific delivers the fastest 10.32% CAGR, fueled by national digitization strategies that earmark cardiac imaging as a first-wave use case. Indonesia executed its inaugural robotic-assisted cardiac bypass in 2024 and partnered with foreign vendors to install cloud CVIS nodes in provincial referral centers . China expanded its volume-based procurement program to include ultrasound machines, driving local manufacturers to integrate native CVIS software as a bundled differentiator. Japan’s super-aged society invests in AI risk stratification to curb mounting heart-failure admissions, and Australia’s My Health Record mandate accelerates adoption of DICOMweb endpoints that plug directly into CVIS archives.

Europe occupies a solid mid-growth trajectory where GDPR and the European Health Data Space steer procurements toward open-standards architectures. Nordic nations pioneer cross-border image sharing, and vendors that gain conformance lab certification enjoy earlier shortlist placement. Middle-Eastern governments, flush with oil-diversification budgets, commission greenfield cardiology centers outfitted with hybrid ORs and real-time analytics towers. South America shows uneven progress: Brazil’s private hospital chains invest in next-generation hemodynamic systems, while public institutions still battle budget restrictions, favoring phased rollouts that start with cloud PACS and add structured reporting later. Collectively, geography trends ensure the cardiology information system market maintains regional diversity, preventing any single vendor from dominating on a global scale.

Regulatory Landscape

Regulation for cardiology information systems spans health IT interoperability rules and, where functions cross into diagnosis or treatment recommendations, medical-device software oversight. In the United States, the FDA re-issued final guidance on Clinical Decision Support Software in January 2026, clarifying how CDS functions fit under section 520(o)(1)(E) of the FD&C Act, and in February 2026 finalized guidance on Computer Software Assurance for production and quality system software. The FDA also finalized its Cybersecurity in Medical Devices guidance in February 2026, raising the bar for secure-by-design development and lifecycle vulnerability management for software used in clinical workflows, including CVIS modules that incorporate AI decision support.

In Europe, market access and classification for software functions used in cardiology workflows are shaped by the EU Medical Device Regulation (Regulation (EU) 2017/745), with MDCG guidance (including the June 2025 update on qualification and classification of software) commonly used to distinguish monitoring, decision support, and decision-making functions under Rule 11. Internationally, the International Medical Device Regulators Forum (IMDRF) continues to align expectations for software risk and change control, including its SaMD work on predetermined change control plans and its April 2026 draft technical framework for AI lifecycle management (N93). These updates reinforce governance expectations for AI-enabled modules embedded into cardiology information system deployments.

Value Chain Analysis

The cardiology information system value chain starts with enabling inputs and infrastructure layers, including clinical interoperability standards (DICOM/DICOMweb, HL7), security and identity controls, and compute infrastructure from on-premises appliances to hyperscale cloud. Platform vendors develop CVIS, cardiology PACS, and integrated CVIS-PACS suites, then assemble ecosystem connectors to imaging modalities (ultrasound, CT, cath lab systems) and EHRs. Downstream value is realized through systems integration, workflow design, data migration, and training, and is reinforced by ongoing managed services for uptime, cybersecurity, and optimization, reflecting the implementation complexity typically seen in enterprise CVIS projects.

Partner ecosystems increasingly shape differentiation and speed to deployment. Philips and MediReport (January 2026) integrating Philips Ultrasound Workspace (TomTec) with CardioReport 360 is an example of a tighter cardiovascular imaging and reporting workflow, while clinical network partnerships such as AISAP with Cardiology Consultants of Philadelphia (March 2026) aim to integrate AI-powered diagnostics across a larger cardiology group. Algorithm and device adjacencies also feed into the chain, including Viz.ai and Alnylam (March 2026) deploying a cardiac amyloidosis care pathway using Us2.ai echocardiography algorithms, and AccurKardia and Wellysis (July 2026) combining wearable monitoring with ECG analysis software. Quality and postmarket processes remain a gating layer for enterprise buyers, highlighted by the February 2025 Class II recall for Philips IntelliSpace Cardiovascular software related to archiving/export functionality. This, in turn, reinforces the importance of validation, audit trails, and export reliability in CVIS procurement and renewals.

Competitive Landscape

The cardiology information system market is moderately fragmented. GE HealthCare, Philips, and Siemens Healthineers anchor the high end with end-to-end ecosystems that bundle ultrasound, CT, and cath-lab hardware into tightly integrated informatics stacks. They defend share by providing full catheterization lab analytics, inventory tracking, and AI decision support. Intelerad’s 2024 purchase of LUMEDX added mature cardiology dashboards to its cloud PACS portfolio, signaling that imaging vendors cannot compete without unified cardiovascular offerings. Epic Systems enlarged its EHR footprint to 39.1% of US hospitals, leveraging native Cupid modules to make cardiology workflows a seamless extension of inpatient documentation.

Cloud-born challengers position themselves on faster release cycles and consumption pricing. Examples include vendors that orchestrate serverless image rendering, allowing browser-based viewers to load 2-GB cath studies in under three seconds on standard bandwidth. AI start-ups such as iCardio.ai supply FDA-cleared algorithms via REST APIs that vendors embed straight into structured reports, blurring lines between core platform and best-of-breed add-ons. Alliances with hyperscale providers give incumbents access to GPU clusters for real-time inference; GE HealthCare’s collaboration with NVIDIA demonstrates how hardware and software ecosystems converge to accelerate autonomous imaging.

Buyer power is rising as health systems form regional purchasing coalitions that demand outcome-based payment terms. Vendors are countering with managed-service contracts that guarantee uptime, cybersecurity audits, and periodic algorithm upgrades under fixed monthly fees. The cardiology information system market therefore evolves toward subscription bundles where software, AI, and service quality metrics are inseparable. Players that fail to front-load professional-services talent risk churn because customers judge platform performance by achieved productivity gains rather than feature checklists.

Cardiology Information System Industry Leaders

Koninklijke Philips N V

Esaote SpA

INFINITT Healthcare Co Ltd

Central Data Networks PTY Ltd

CREALIFE Medical Technology

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Interoperability-driven replacement and add-on cycles create near-term whitespace for CVIS and cardiology PACS vendors that can align to evolving certification and data-exchange expectations without costly custom interfaces. In the United States, the ONC Standards Version Advancement Process (SVAP) 2026 cycle formalizes voluntary use of newer standards, including updated HL7 FHIR US Core implementation guides starting August 29, 2026, which raises demand for modern APIs, structured data capture, and consistent mapping of cardiology observations into enterprise records. Work on HL7 International CardX implementation guides, including CardX CIED v2.0.0 at Trial-use Active status, supports more uniform ingestion of device-related data into longitudinal cardiology records and creates opportunities for vendors that can normalize remote and implantable-device feeds alongside imaging and hemodynamics.

AI-enabled workflow layers are also moving from pilots into commercial pathways where they can be acquired and operated as modular components. HeartSciences receiving Epic Toolbox designation for its MyoVista Insights platform in March 2026 points to an integration-led commercialization path for EHR-centric customers, while its subsequent mainstream SaaS agreement with St. Vincent Health in May 2026 and its June 2026 release adding an AI-ECG algorithm marketplace illustrate a procurement model that separates the core platform from swappable algorithms. On the invasive imaging side, Abbott receiving FDA clearance and CE Mark for its Ultreon 3.0 AI-powered coronary imaging platform in April 2026 supports tighter interventional-to-CVIS data flows, as cath lab imaging outputs increasingly need to be archived, structured, and shared across care teams. In Europe, projects such as DataTools4Heart deploying a secure federated network across seven sites (v3.0 milestone) reinforce an opportunity for federated analytics and cross-site governance models that fit data-protection constraints while still enabling multi-center cardiology insights.

Recent Industry Developments

- March 2026: Philips launched IntraSight Plus, an interventional guidance platform for coronary interventions, with FDA 510(k) clearance and CE Mark coverage. By extending connected guidance across imaging and physiology, the platform increases the volume and complexity of cath lab data that must be captured, structured, and routed into cardiology information system workflows. The launch reinforces vendor strategies to link procedure-room decision support with downstream reporting and longitudinal archives.

- December 2025: Philips agreed to acquire SpectraWAVE Inc. to expand coronary intravascular imaging and physiologic assessment capabilities that incorporate AI. The deal strengthens Philipp shared interventional portfolio and supports tighter integration between imaging acquisition and CVIS documentation and analytics. Consolidation of advanced imaging assets can also influence enterprise buyers that prefer fewer vendors across cath lab hardware and associated software ecosystems.

- August 2024: INFINITT North America partnered with Hunterdon Health to implement radiology and cardiology PACS solutions. The deployment highlights continued demand for enterprise imaging platforms that support both cross-departmental imaging strategies and specialty cardiology workflows. Multi-department implementations also raise the importance of interoperability and shared viewers, shaping requirements for integrated CVIS-PACS roadmaps.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the cardiology information system market covers software and related services used to capture, store, manage, and share cardiology clinical data and images inside care settings, including cardiology PACS and integrated CVIS workflows.

Scope exclusions: We exclude general hospital EHR/EMR platforms, standalone diagnostic devices, and radiology-only archiving tools that are not sold or used as cardiology-focused information systems.

Segmentation Overview

- By Mode of Operation

- Web-based

- On-premises

- Cloud / SaaS

- By Components

- Hardware

- Software

- Services

- By System Type

- Cardiovascular Information System (CVIS)

- Cardiology PACS (C-PACS)

- Integrated CVIS-PACS Platform

- By Application

- Catheterization Lab

- Echocardiography

- Electrophysiology

- ECG & Stress

- Nuclear Cardiology

- Others

- By End-user

- Hospitals

- Ambulatory Surgical Centers

- Specialty Cardiology Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- GCC

- South Africa

- Rest of Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a clean demand and supply context for cardiology IT before any numbers are modeled. We refer to public health statistics and adoption signals such as CDC heart disease burden updates, WHO cardiovascular disease fact sheets, OECD health system indicators, and CMS or equivalent national payer publications for procedure and care-setting trends. To anchor the digital side, we also review sources such as FDA device and software listings where relevant, NLM-hosted peer-reviewed journals for workflow patterns, and standards bodies material (such as DICOM and HL7) to understand interoperability requirements.

We then cross-check supplier positioning using annual reports, 10-K style filings, investor presentations, reputable press coverage, and health system procurement notes where publicly available. In a few cases, paid subscriptions for company financials and news intelligence, plus patent databases, help validate ownership changes, product roadmap direction, and the timing of commercial launches. These examples are not exhaustive, and many other public sources are also used for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary work is used to test whether desk assumptions reflect real buying and usage patterns, especially around cloud migration, integration effort, and pricing that is often bundled with imaging and workflow tools. We speak with a mix of hospital IT leaders, cardiology department users, system integrators, and solution-side executives across major regions so gaps in utilization, replacement cycles, and service attach rates can be closed before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 14% | APAC: 42% |

| Mid tier: 48% | Functional/Unit leaders: 37% | EMEA: 35% |

| Smaller Players: 14% | Managers: 49% | Americas: 23% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where procedure volumes, cardiology imaging workload, and the count of active care sites are translated into an addressable deployment pool, then filtered by CIS adoption levels and average annual spending. The model is then corroborated using selective bottom-up approximations, such as a supplier roll-up for a sample set, channel checks on typical contract values, and ASP multiplied by estimated deployments for key modes of operation.

A few practical inputs that shape the totals include hospital share versus ambulatory settings, web-based versus cloud versus on-premise mix, average contract duration and renewal timing, and the service portion tied to implementation and support. Where public data is thin, gaps are handled through bounded ranges, then tightened using what interviewees say about replacement cycles, integration effort, and pricing shifts from one-time license to subscription. For forecasting, we rely on scenario analysis supported by simple regression checks on drivers like cardiovascular disease burden, digitization budgets, and cloud adoption rates, with assumptions reviewed against what users and solution-side experts expect in the next cycle.

Data Validation & Update Cycle

Validation is done by triangulating the modeled market value against independent signals, such as regional hospital IT spending direction, procedure and imaging activity trends, and observed migration to web and cloud deployments. Outliers are investigated through variance checks at the region and end-user level, and numbers are reviewed in multiple analyst passes so definition drift and double counting are avoided.

If a material event changes demand or pricing, such as a major regulatory shift, a large acquisition, or a sudden budget tightening, the team re-contacts sources and re-tests the assumptions that moved. Reports are refreshed annually, and before delivery a fresh scan is done so the final output reflects the most current information available at the time.

Mordor Intelligence's Cardiology Information System Market Estimate Compared With Other Published Estimates

Published figures for this market do not always line up, even when the topic sounds identical, because analysts make different calls on what products count and which year is treated as the starting point. The table helps make this visible by putting the current-year number next to other estimates that use different base years and forecasting windows.

The benchmark table shows a spread that is mainly driven by scope and year alignment, because in Mordor Intelligence's model the value is limited to cardiology-focused information systems and related services, with general EHR platforms and non-cardiology archiving excluded, and the current sizing year set to 2026 instead of 2024 or 2025. Some published totals also pull in hardware or broader imaging infrastructure, or they apply faster cloud ASP escalation without matching it to observed contract structures, which can lift the headline number.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.47 B (2026) | |

| Industry Publisher A | USD 1.48 B (2025) | Uses a different base year and a longer horizon, and it also includes hardware as a formal component, which can increase totals versus software and services only. |

| Research Group B | USD 1.32 B (2024) | Starts from an earlier year and applies a broader CIS definition that is not always separated from adjacent clinical IT, and the base-year framing listed separately can make comparisons less direct. |

When these differences are normalized, the gap becomes easier to explain, because the sizing step is driven by what is counted, how contracts are treated, and how the base year is chosen. By tying totals back to observable deployment pools, adoption levels, and realistic spend patterns, the estimate stays traceable and repeatable for planning discussions.

Key Questions Answered in the Report

What is the current Cardiology Information System Market size?

The cardiology information system market size equals USD 1.47 billion in 2026 and is projected to reach USD 2.23 billion by 2031 at a 8.74% CAGR.

Who are the key players in Cardiology Information System Market?

Koninklijke Philips N V, Esaote SpA, INFINITT Healthcare Co Ltd, Central Data Networks PTY Ltd and CREALIFE Medical Technology are the major companies operating in the Cardiology Information System Market.

Which is the fastest growing region in Cardiology Information System Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Cardiology Information System Market?

In 2025, the North America accounts for the largest market share in Cardiology Information System Market.

What segments have the strongest growth outlook?

Services, cardiology PACS, and ECG & stress-testing applications each exceed 9% CAGR as buyers prioritize workflow consulting and AI-enhanced diagnostics.

Page last updated on: