Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 29.1 Billion |

| Market Size (2031) | USD 37.19 Billion |

| Growth Rate (2026 - 2031) | 5.04% CAGR |

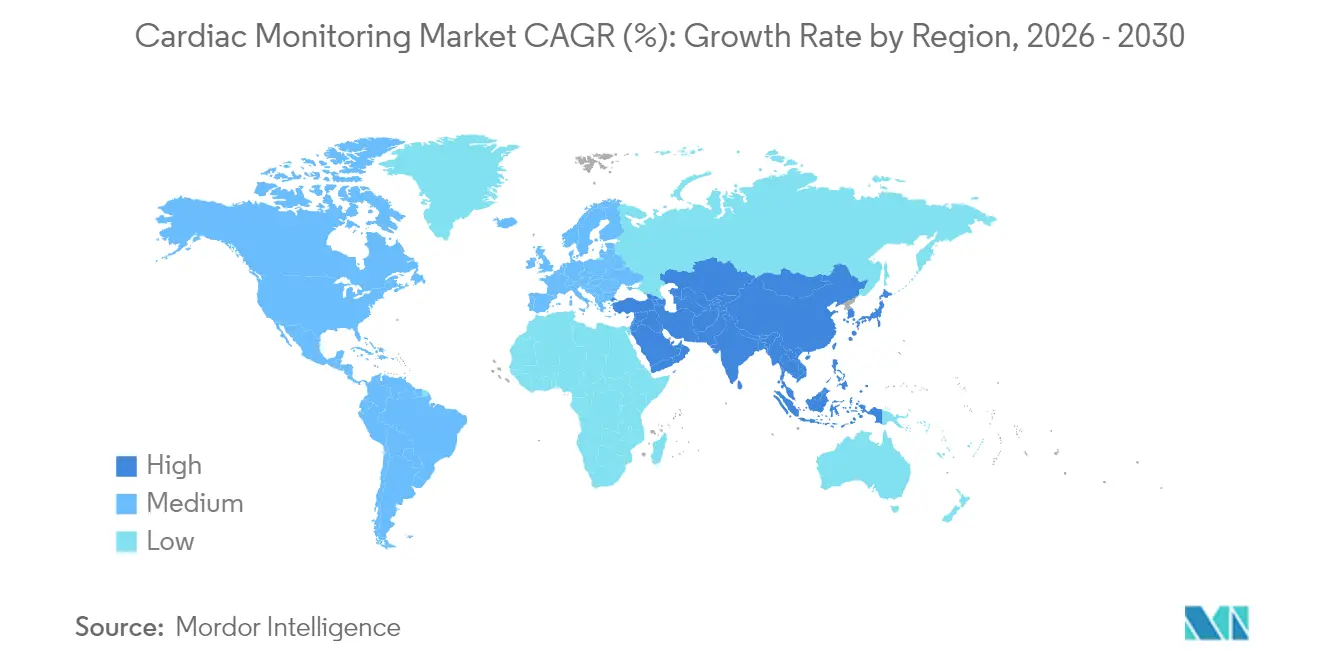

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cardiac Monitoring Market Analysis by Mordor Intelligence

The cardiac monitoring market size in 2026 is estimated at USD 29.1 billion, growing from 2025 value of USD 27.70 billion with 2031 projections showing USD 37.19 billion, growing at 5.04% CAGR over 2026-2031. The rising prevalence of cardiovascular disease, an aging population that favors non-invasive technology, and expanding reimbursement for ambulatory care underpin this momentum. Demand is shifting from episodic hospital monitoring toward continuous, AI-enhanced home-based solutions that lower readmissions and reduce long-term care costs. Regional growth centers on Asia-Pacific, where infrastructure upgrades intersect with demographic shifts, while North America maintains scale leadership through early technology adoption. Competition remains moderate as incumbents integrate artificial intelligence, cybersecurity protections, and remote connectivity to defend their share against nimble wearable specialists.

Key Report Takeaways

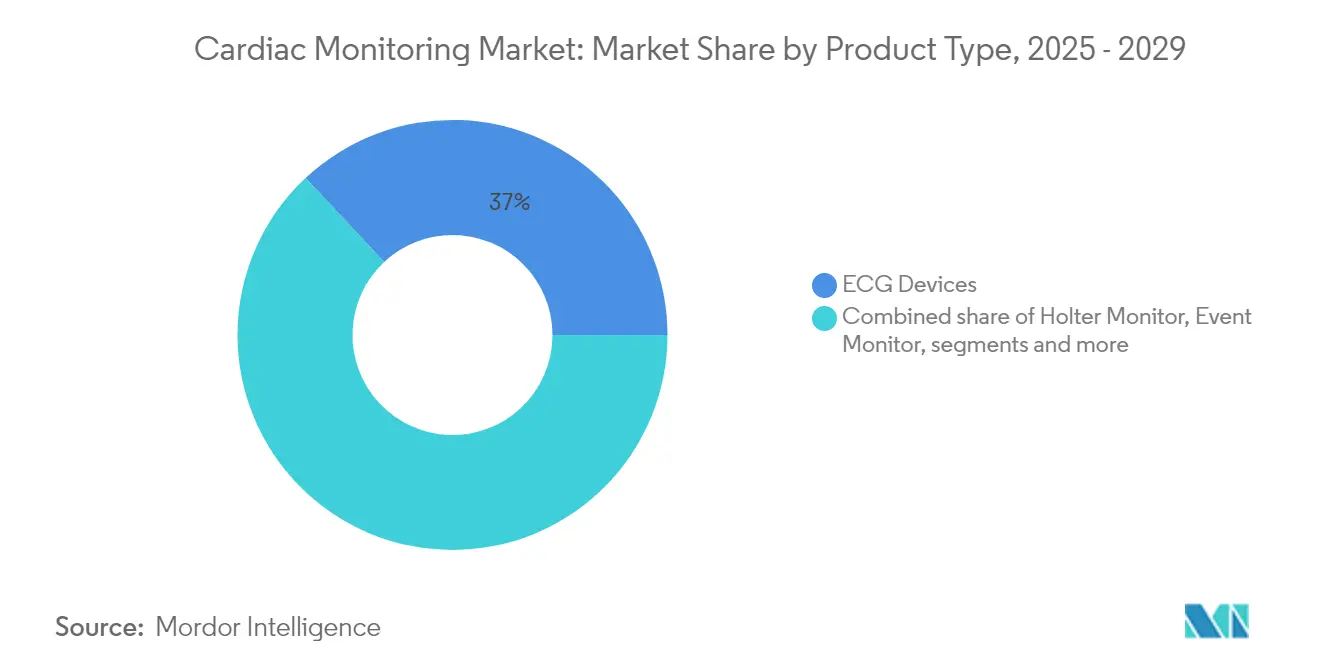

- By product type, ECG devices led with 36.98% of the cardiac monitoring market share in 2025, whereas wearable patch monitors are projected to post a 6.35% CAGR through 2031.

- By technology, conventional wired systems accounted for 59.12% revenue in 2025, but AI-enabled platforms are growing at a 6.63% CAGR to 2031.

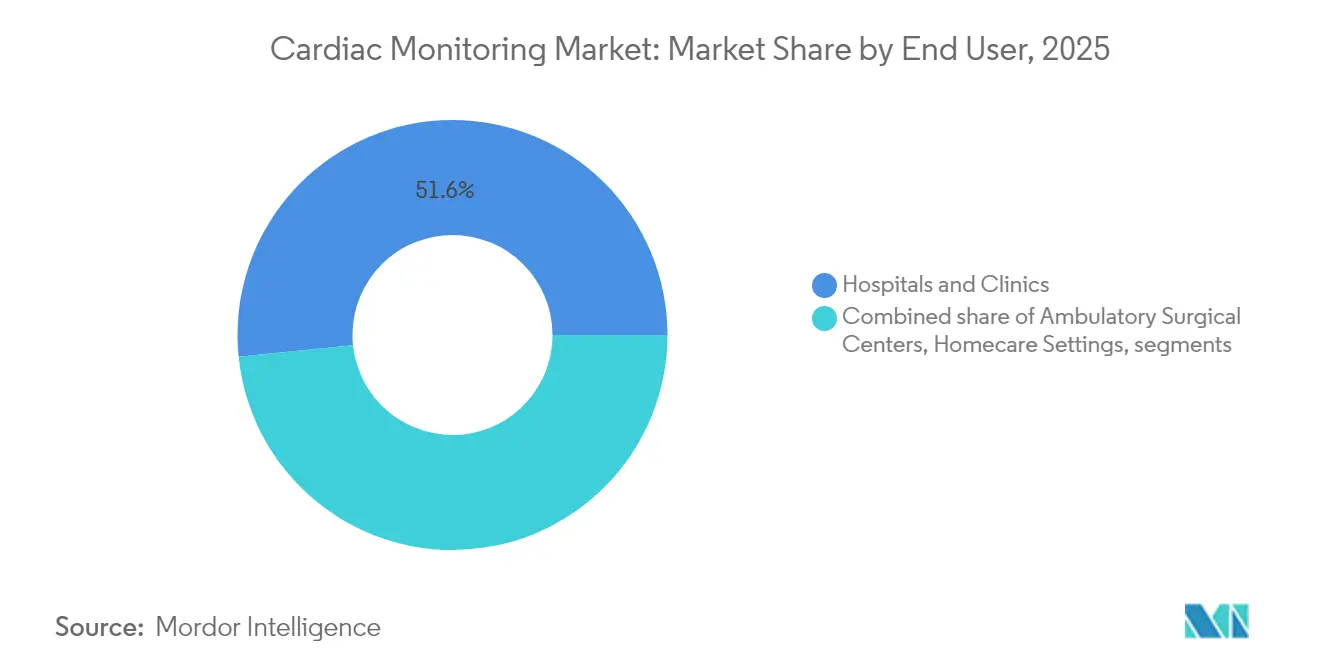

- By end user, hospitals and clinics held 51.62% of the cardiac monitoring market size in 2025; home-care settings deliver the fastest 6.78% CAGR through 2031.

- By geography, North America contributed 40.71% revenue in 2025; Asia-Pacific is expected to expand at a 6.98% CAGR during the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cardiac Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of cardiovascular diseases | +1.6% | Global, with higher concentration in North America and Europe due to lifestyle factors | Long term (≥ 4 years) |

| Growing geriatric population | +1.1% | Global, particularly pronounced in developed markets of North America, Europe, and Asia-Pacific (Japan) | Long term (≥ 4 years) |

| Technological advances in wireless & wearable devices | +0.8% | Global, led by North America and Europe, with rapid adoption in Asia-Pacific core markets | Medium term (2-4 years) |

| Expansion of AI-enabled predictive analytics | +0.6% | North America & Europe initially, with spillover to Asia-Pacific developed markets | Medium term (2-4 years) |

| Reimbursement shift to ambulatory continuous monitoring | +0.7% | North America & Europe primarily, driven by established healthcare reimbursement systems | Medium term (2-4 years) |

| Increasing Awareness and Screening Programs for Heart Health | +0.5% | Global, with early gains in developed markets and government-led initiatives in emerging Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of cardiovascular diseases

Cardiovascular disease affects 127.9 million US adults and is projected to impact 61% of the population by 2050, driving health systems toward continuous monitoring that mitigates USD 422.3 billion in annual treatment costs[1]Source: American Heart Association, “Heart Disease and Stroke Statistics—2025 Update,” ahajournals.org. Age-standardized prevalence continues to climb in middle- and low-income nations, pressuring providers to adopt scalable tele-cardiology programs. Population-specific disparities—such as diabetes rates ranging from 6.3% among Vietnamese Americans to 15.2% among Filipino Americans—further underscore the need for personalized monitoring protocols. Evidence shows early intervention via continuous ECG analytics lowers emergency admissions and improves survival.

Growing geriatric population

Stroke cases are forecast to double to 20 million older adults by 2050, amplifying chronic monitoring demand. Two-thirds of Americans already track heart data using smartwatches or blood-pressure devices, yet only 25% share the information with clinicians; integrating these data streams into care pathways remains a growth opportunity. Remote patient monitoring programs are on track to serve 70.6 million US patients by 2025, with cardiac indications comprising 21% of enrollments.

Technological advances in wireless & wearable devices

Next-generation wearables such as the Jewel Patch cardioverter-defibrillator achieve 23.5 hours median daily wear time with only 2.3% adverse events, meeting clinical-grade standards without intrusive leads. AI chips developed at the University of Mississippi detect myocardial infarction in real time with 92.4% accuracy, doubling detection speed compared with legacy alert systems. Patch-based rhythm monitoring delivers 95% analyzable data versus 85% for multi-electrode Holters, broadening adoption among primary-care networks.

Expansion of AI-enabled predictive analytics

Large-language-model ECG interpretation at Tsinghua University increased early-stage heart-disease detection accuracy, validating the fusion of signal data with demographic context. AI-enhanced ECGs achieve up to 99.9% accuracy for heart-failure diagnosis, and asymmetric architectures outperform classical networks on rare arrhythmias. FDA designation of Apple Watch as a medical-device development tool legitimizes consumer wearables for clinical endpoints.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced implantable monitors | -0.8% | Global, with highest impact in emerging markets | Medium term (2-4 years) |

| Stringent regulatory approval timelines | -0.6% | North America and Europe primarily | Short term (≤ 2 years) |

| Cyber-security & data-privacy concerns | -0.5% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Semiconductor supply-chain vulnerabilities | -0.4% | Global manufacturing and supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High cost of advanced implantable monitors

Cost-effectiveness studies in Europe show ePatch solutions offer 3.4-6.0× savings versus implantable loop recorders when detecting atrial fibrillation. In the US, mobile cardiac telemetry reduced 18-month care costs by USD 27,429 compared with implantables while lowering readmissions to 30.2%. With heart-failure expenditure projected above USD 70 billion in 2030, payers prioritize lower-cost external devices that still deliver predictive insight.

Stringent regulatory approval timelines

Actual FDA 510(k) clearance averages 154-201 days despite 90-day targets, and software-based devices undergo additional cybersecurity reviews under 2023 guidance. New Quality System Regulation amendments taking effect in February 2026 will require harmonization with ISO 13485, adding compliance complexity during transition

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Wearable Patches Drive Innovation

ECG devices accounted for 36.98% of the revenue in the cardiac monitoring market in 2025, reflecting broad clinical familiarity and near-universal reimbursement. Holter and event monitors continue to address episodic diagnostics; however, extended-wear patches now deliver 95% analyzable time and patient comfort, allowing for sustained 21-day monitoring windows. This performance, paired with a 6.35% CAGR, positions patches as the primary disruptor within the cardiac monitoring market. Investor interest is high: VitalConnect has secured USD 100 million to commercialize the VitalPatch platform, anticipating the development of hospital discharge kits paired with telehealth dashboards.

Extended monitoring also closes diagnostic gaps in paroxysmal arrhythmia detection, driving guideline revisions that recommend up to 14 days of continuous ECG monitoring for the evaluation of cryptogenic stroke. Implantable loop recorders capture long-term, asymptomatic events but face adoption barriers when the costs and surgical risks are weighed against external alternatives. Still, high-risk cohorts benefit from six-year devices such as Abbott’s Assert-IQ, which adds Bluetooth telemetry, reducing clinic visits while enhancing data fidelity. Collectively, the product mix demonstrates a continuum where non-invasive, AI-enhanced patches occupy mass-market tiers, while implantables serve specialized cases in the cardiac monitoring market.

By Technology: AI Integration Accelerates Growth

Conventional wired systems retained 59.12% of 2025 revenue, supported by established ICU and telemetry ward protocols. Yet AI-enabled platforms register the highest 6.63% CAGR, signifying a pivot toward predictive insights. Researchers validated smartwatch-derived inter-beat interval analytics, which achieved 90% accuracy in distinguishing patients with congestive heart failure. Such advancements elevate consumer devices to clinical utility, feeding algorithm pipelines that learn from billions of annotated heartbeats collected by leaders like iRhythm Technologies.

Wireless telemetry further removes friction in care transitions. Edge-compute patches enable on-device arrhythmia classification, reducing bandwidth requirements and mitigating cybersecurity exposure while meeting latency thresholds for automated alerts. Interoperability standards such as IEEE 11073 accelerate integration with electronic health records, enabling seamless clinician workflows. As AI matures, cloud-based dashboards synthesize multivariate data—such as blood pressure, SpO2, and activity—to inform the titration of medications and triage interventions, reinforcing the long-term value proposition of the cardiac monitoring market size attributed to intelligent analytics solutions.

By End User: Homecare Settings Transform Delivery

Hospitals and clinics controlled 51.62% of the cardiac monitoring market share in 2025; however, payers are increasingly reimbursing remote models that show a 30% lower cost per admission avoided. Homecare monitoring benefits from the 2025 RPM code revisions, enabling practices to bill for care management and device 30-day bundles simultaneously. The cardiac monitoring market size for home settings is projected to record the fastest CAGR of 6.78% through 2031.

Hospital-at-home programs harness wearable sensors, weight scales, and connected BP cuffs to replicate telemetry wards virtually. Initial evidence suggests a reduced risk of nosocomial infections and improved patient satisfaction scores. Ambulatory surgical centers are adopting single-use patches for post-procedure discharge, thereby freeing catheter lab capacity. Telehealth platforms overlay AI-triaged alerts, enabling cardiologists to review arrhythmia summaries rather than raw waveforms, optimizing clinical productivity. The convergence of policy shifts, technology readiness, and patient preference underscores why home care environments will remain the growth engine of the cardiac monitoring market.

Geography Analysis

North America commanded 40.71% of 2025 global revenue, supported by FDA device pipelines and Medicare reimbursement that recognize remote monitoring as standard of care. New CPT codes for cardiovascular risk stratification promise additional billing avenues, while private-equity ownership of cardiology groups—now 3.9% of US practices—streamlines large-scale device deployment strategies. Semiconductor tariff proposals could elevate device manufacturing costs, yet suppliers diversify sourcing to shield availability.

Asia-Pacific delivers the swiftest 6.98% CAGR on the back of urbanization and rising hypertension prevalence. China’s volume-based procurement schemes encourage cost-effective patch devices, while India’s Ayushman Bharat Digital Mission integrates mobile ECG data into national health records. Japan’s super-aging society accelerates adoption of continuous rhythm surveillance in community clinics. Venture financing slowed 22% from 2021 highs, yet strategic investors maintain commitments to AI-enabled diagnostics that localize languages and waveform signatures.

Europe remains a mature cluster emphasizing preventive cardiology. Germany expands Disease Management Programs to include prescribed mobile telemetry, boosting hardware uptake. The United Kingdom’s NHS Long Term Plan endorses virtual wards, targeting 40-50 patients per 100,000 population equipped with cardiac monitors for post-discharge surveillance. Economic headwinds elevate value-analysis scrutiny, steering tenders toward single-use patches with lower total cost of ownership. South America and the Middle East & Africa witness incremental progress as local distributors partner with multinational vendors to pilot low-cost wearable ECGs in hypertension screening campaigns.

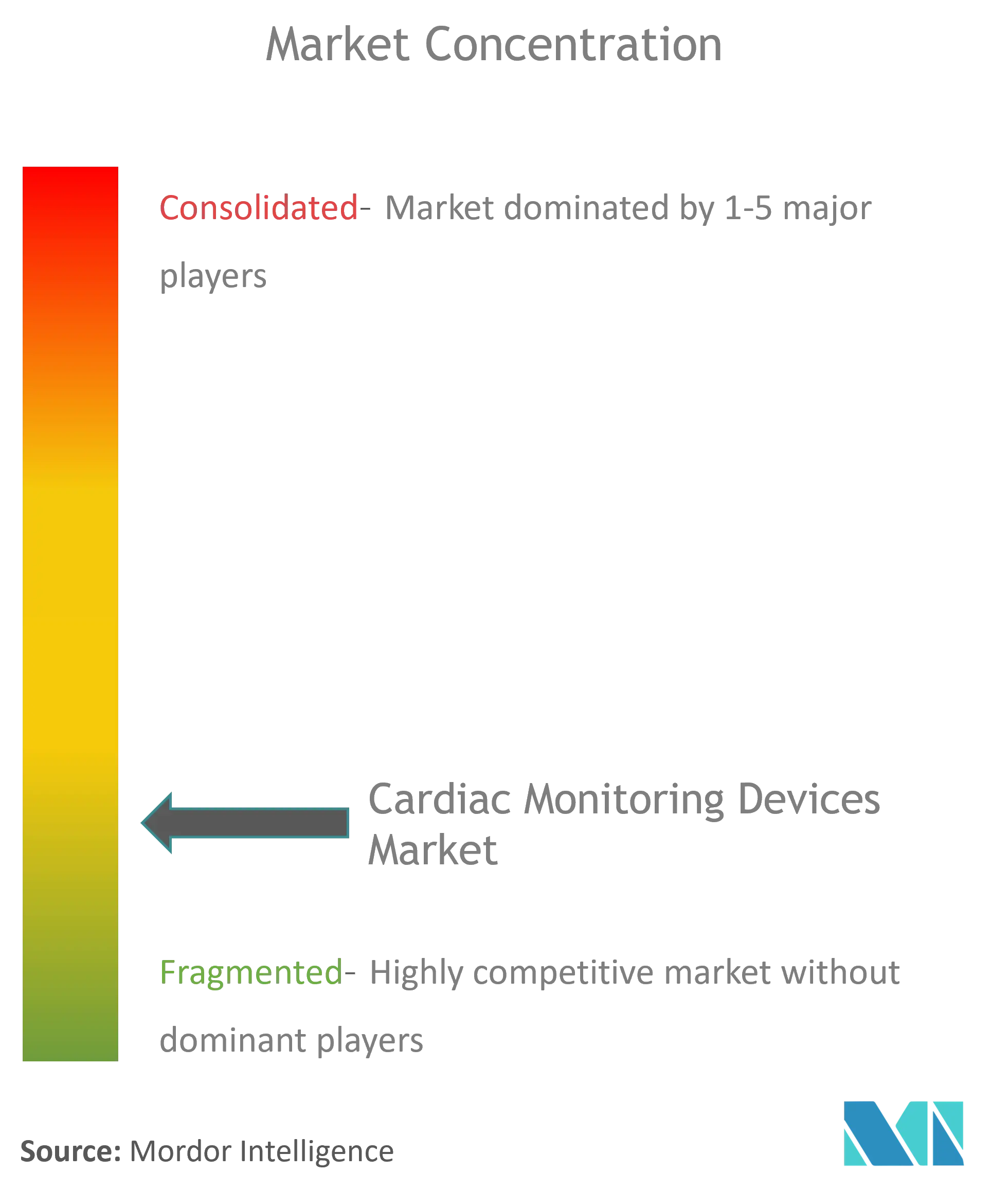

Competitive Landscape

Incumbent medtech firms pursue acquisitions and R&D investments totaling USD 62.68 billion to secure AI competencies and remote connectivity. Abbott’s USD 27 billion allocation includes the Assert-IQ six-year implantable monitor and AVEIR dual-chamber leadless pacemaker, both pivotal in extending ecosystem lock-in. Medtronic’s OmniaSecure 4.7 French defibrillation lead gained FDA clearance after achieving 100% defibrillation success rates, underscoring miniaturization leadership.

Mid-size disruptors leverage data advantages. iRhythm has processed 1.8 billion hours of heartbeat recordings, training deep-learning models that feed cardiologist dashboards with auto-classified arrhythmia episodes. Element Science entered commercialization with the Jewel Patch wearable defibrillator, bypassing vest discomfort to enhance adherence.[3]Source: Journal of the American College of Cardiology, “Wearable Patch Cardioverter-Defibrillator Clinical Performance,” jacc.org Start-ups such as HeartBeam integrate 12-lead equivalent smartwatch ECGs with cloud-AI triage, highlighting the converging consumer and clinical device lines.

Strategic collaborations multiply. Payers partner with device vendors to offer value-based contracts that reimburse per avoided hospital day. Cloud hyperscalers supply secure data lakes that enable algorithm retraining while meeting HIPAA and GDPR mandates. Cybersecurity firms embed zero-trust architectures, satisfying the FDA’s 2023 pre-market guidance and differentiating products on regulatory readiness. The competitive hierarchy increasingly favors platforms that pair predictive analytics with end-to-end care pathways rather than standalone hardware.

Cardiac Monitoring Industry Leaders

Abbott Laboratories

Boston Scientific Corporation

iRhythm Technologies Inc

Biotronik

Medtronic PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Element Science received FDA approval for the Jewel Patch wearable cardioverter-defibrillator, the first AI-enabled patch defibrillator clearance.

- April 2025: Medtronic gained FDA approval for the OmniaSecure 4.7 French defibrillation lead, achieving 100% defibrillation success in trials.

- April 2025: EBR Systems obtained FDA approval for the WiSE CRT system, a wireless biventricular pacing option for lead-intolerant heart-failure patients.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study values the global cardiac monitoring market as all professional-grade devices, including resting or stress ECG, Holter, event and mobile telemetry recorders, implantable loop recorders, pacemakers, defibrillators, cardiac resynchronization systems, and smart diagnostic wearables, that capture, display, or transmit rhythm or hemodynamic data for clinical use. Revenues are factory-gate, expressed in 2024 United States dollars, and cover demand across 17 countries grouped into five regions.

Scope Exclusions: Fitness trackers that only trend heart rate, standalone analytics sold without hardware, and single-use interventional catheters are excluded.

Segmentation Overview

- By Product Type

- Electrocardiograph (Resting ECG)

- Holter Monitor

- Event Monitor

- Mobile Cardiac Telemetry (MCT)

- Implantable Loop Recorder

- Wearable Patch Monitors

- Others

- By Technology

- Conventional (Wired)

- Wireless & Wearable

- AI-enabled Analytics Platforms

- By End User

- Hospitals & Clinics

- Ambulatory Surgical Centers

- Homecare Settings

- Cardiac Centers

- Telehealth Providers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with cardiologists, electrophysiology nurses, biomedical engineers, and hospital buyers in the United States, Germany, Japan, China, India, and the Gulf validated installed-base churn, ambulatory uptake, and discount ladders, letting us fine-tune every assumption.

Desk Research

Public repositories such as the WHO CVD dashboard, CDC and Eurostat health statistics, and customs shipment logs supplied incidence curves, procedure counts, and trade flows that anchor demand. Specialty bodies (Heart Rhythm Society, Japanese Circulation Society, and peers) added device-usage surveys, while regulatory portals and company 10-Ks enriched product pipelines and ASP clues.

Mordor analysts layered these inputs with D&B Hoovers financials, Dow Jones Factiva deal screens, and Questel patent alerts to gauge technology diffusion. The sources named are illustrative; many additional datasets underpinned verification.

Market-Sizing & Forecasting

A top-down build starts with regional CVD prevalence and procedure volumes, which are then multiplied by monitoring penetration and blended ASPs to derive 2024 value. Supplier roll-ups, distributor checks, and sampled price-volume pairs provide a bottom-up cross-check held within a six percent guardrail. Key levers such as new CVD incidence, outpatient telemetry prescriptions, device replacement cycles, regulatory approvals, and AI-wearable adoption feed a multivariate regression that projects through 2030, while scenario analysis addresses reimbursement shocks.

Data Validation & Update Cycle

Outputs pass variance screens against prior editions, import-export tallies, and quarterly earnings commentary before senior reviewer sign-off. The database refreshes annually, with interim updates for recalls, policy shifts, or landmark trials.

Why Mordor's Cardiac Monitoring Baseline Deserves Trust

Published values differ because firms mix device types differently, stretch limited country data, or model aggressive wearable growth.

Mordor's broad scope, dual-path validation, and yearly refresh temper such swings.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 26.28 B (2024) | Mordor Intelligence | - |

| USD 21.84 B (2024) | Global Consultancy A | Omits implantable CRM devices, keeps flat ASPs |

| USD 9.23 B (2024) | Regional Consultancy B | Scales global value from five nations |

| USD 8.24 B (2024) | Trade Journal C | Focuses only on diagnostic monitors |

These contrasts show that, by counting the full clinical device universe and validating every step with frontline experts, Mordor offers a balanced, transparent baseline decision-makers can rely on.

Key Questions Answered in the Report

How big is the Global Cardiac Monitoring Market?

The Global Cardiac Monitoring Market size is expected to reach USD 29.1 billion in 2026 and grow at a CAGR of 5.04% to reach USD 37.19 billion by 2031.

What is the current Global Cardiac Monitoring Market size?

In 2026, the Global Cardiac Monitoring Market size is expected to reach USD 29.1 billion.

Who are the key players in Global Cardiac Monitoring Market?

Abbott Laboratories, Boston Scientific Corporation, iRhythm Technologies Inc, Biotronik and Medtronic PLC are the major companies operating in the Global Cardiac Monitoring Market.

Which is the fastest growing region in Global Cardiac Monitoring Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Global Cardiac Monitoring Market?

In 2025, the North America accounts for the largest market share in Global Cardiac Monitoring Market.

What years does this Global Cardiac Monitoring Market cover, and what was the market size in 2025?

In 2025, the Global Cardiac Monitoring Market size was estimated at USD 29.1 billion. The report covers the Global Cardiac Monitoring Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Global Cardiac Monitoring Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: