Healthcare Gamification Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

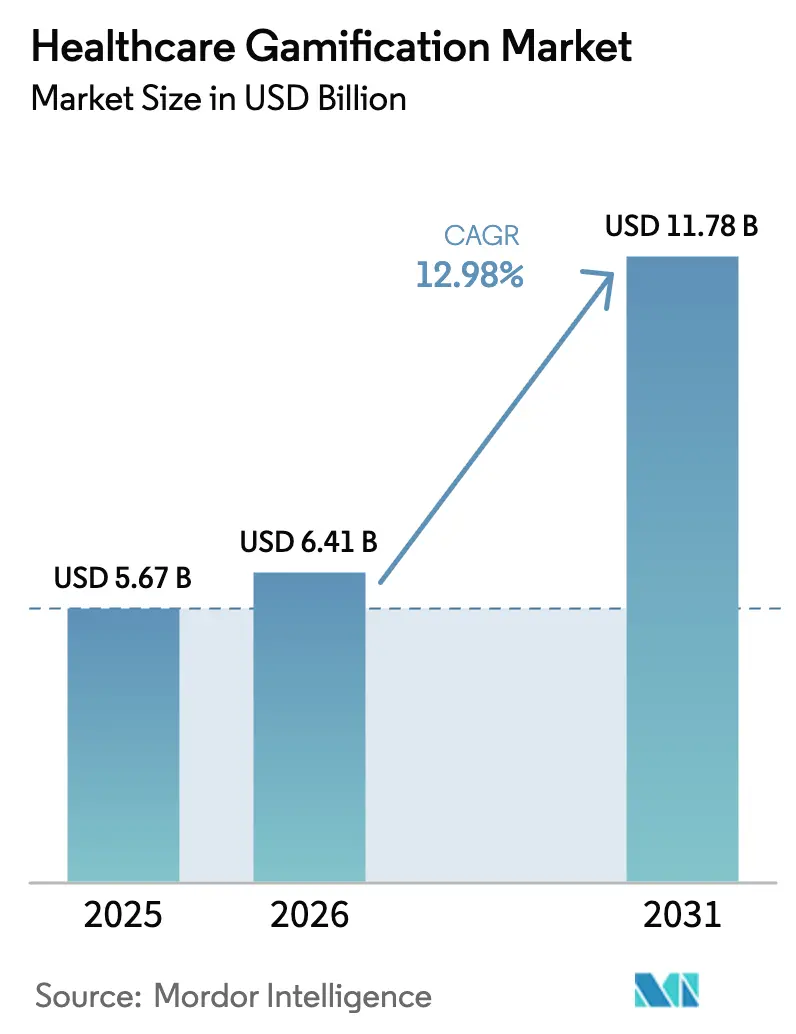

| Market Size (2026) | USD 6.41 Billion |

| Market Size (2031) | USD 11.78 Billion |

| Growth Rate (2026 - 2031) | 12.98% CAGR |

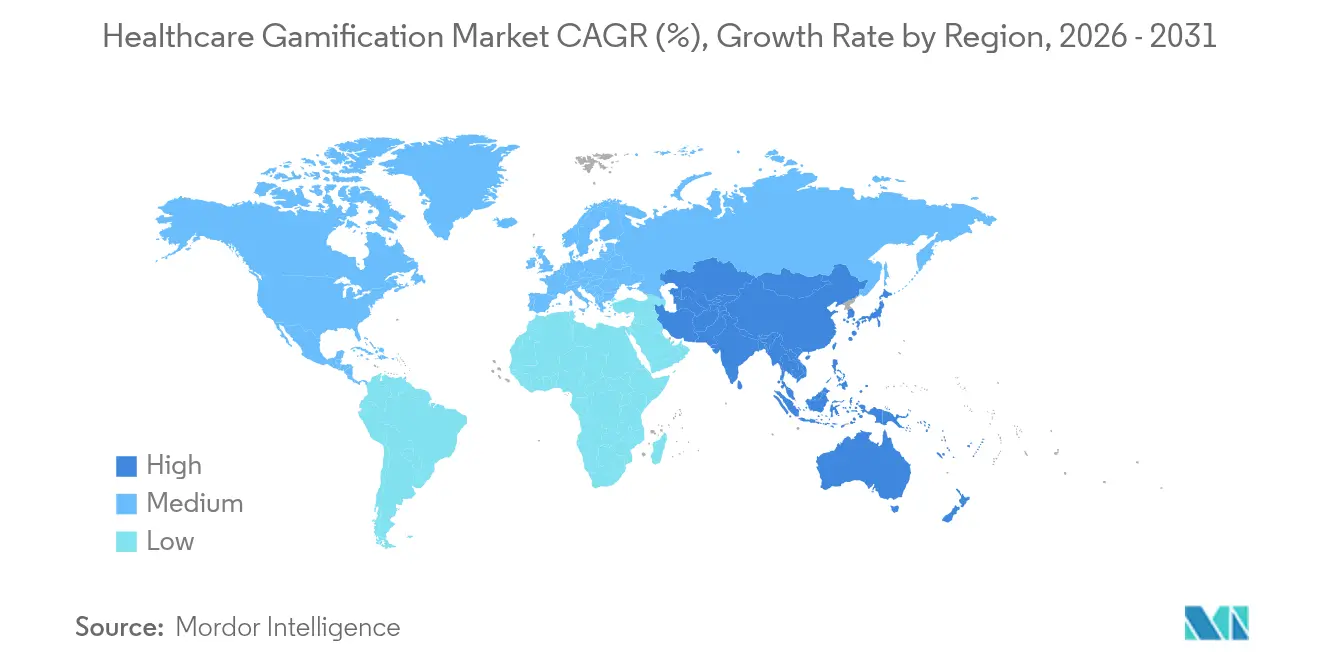

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Gamification Market Analysis by Mordor Intelligence

Healthcare gamification market size in 2026 is estimated at USD 6.41 billion, growing from 2025 value of USD 5.67 billion with 2031 projections showing USD 11.78 billion, growing at 12.98% CAGR over 2026-2031. This expansion reflects the shift from simple fitness trackers to FDA-cleared prescription digital therapeutics that treat conditions such as ADHD and migraine. Enterprise demand for measurable outcomes, advancing reimbursement codes for software-based care, and growing evidence that gamified tools improve adherence all reinforce momentum. Wider smartphone and wearable ownership, cloud interoperability, and AI-driven personalization remove historical technical hurdles, while collaboration between game studios and life-science firms accelerates product pipelines. Competitive intensity remains high because regulatory approval, clinical validation, and engaging design each require specialized capabilities that few single companies possess.

Key Report Takeaways

- By end user, enterprise solutions held 54.83% of the healthcare gamification market share in 2025.

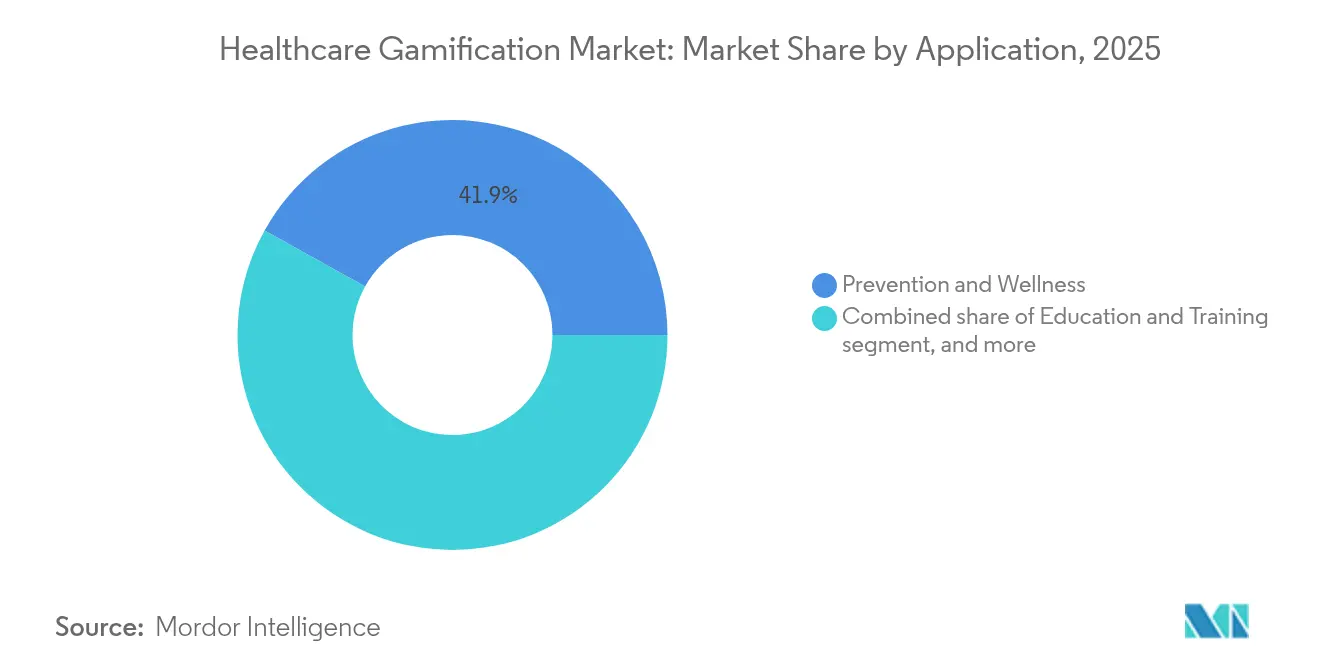

- By application, prevention and wellness accounted for 41.92% share of the healthcare gamification market size in 2025, while therapeutics and rehabilitation is forecast to expand at a 16.42% CAGR through 2031.

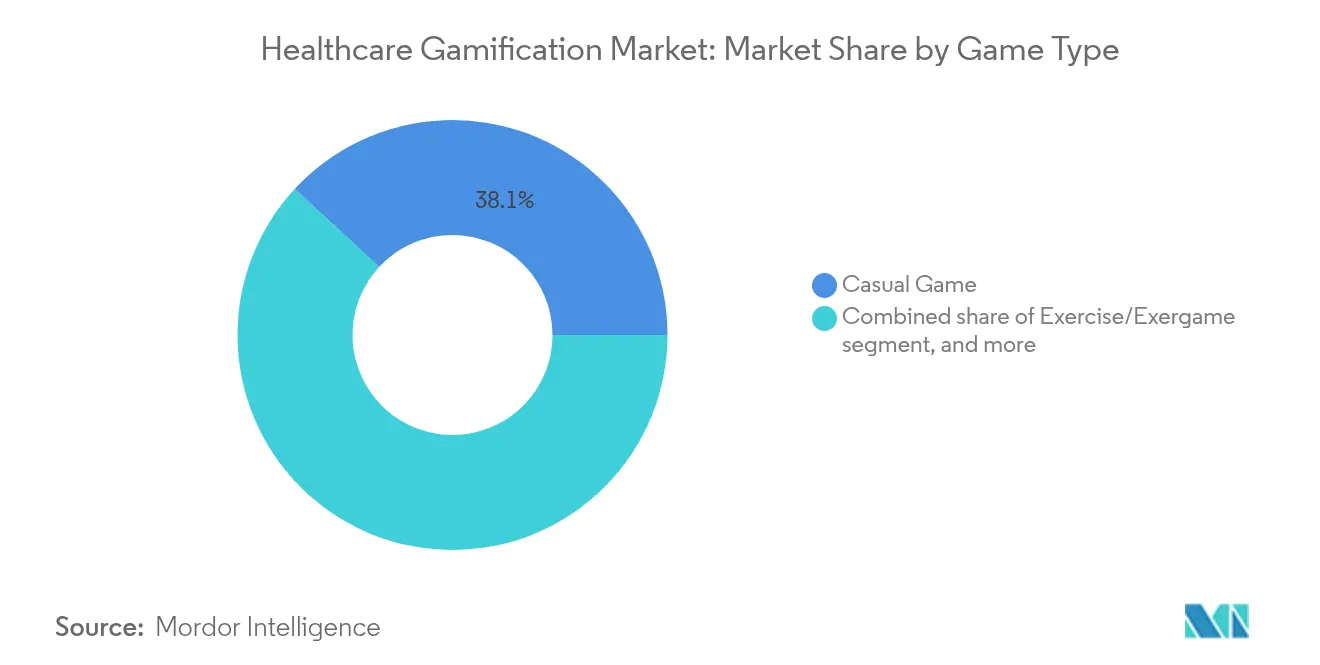

- By game type, casual games captured 38.12% of the healthcare gamification market share in 2025, whereas serious games are projected to grow at a 14.87% CAGR during 2026–2031.

- By region, North America led with 42.11% revenue share in 2025; Asia-Pacific is anticipated to record the fastest CAGR at 14.21% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Healthcare Gamification Market Trends and Insights

Driver Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing burden of chronic diseases | +2.8% | Global; highest in North America and Europe | Long term (≥ 4 years) |

| Proliferation of smartphones and wearable devices | +2.1% | Global; accelerated adoption in APAC | Medium term (2–4 years) |

| Regulatory endorsement of digital therapeutics | +1.9% | North America and Europe leading; APAC following | Medium term (2–4 years) |

| Rising demand for patient engagement solutions | +1.7% | Global; particularly developed markets | Short term (≤ 2 years) |

| Value-based insurance incentives for gamified adherence | +1.4% | North America and select European markets | Medium term (2–4 years) |

| Integration of digital twin technology into health games | +1.2% | Global; early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Chronic Diseases

Chronic illnesses drive sustained demand for healthcare gamification market offerings because traditional episodic care fails to meet daily self-management needs. The Centers for Disease Control and Prevention reports that 76.4% of U.S. adults now live with at least one chronic condition, while multi-morbidity among adults aged 20–44 rose to 27.1% between 2013 and 2023[1]Centers for Disease Control and Prevention, “National Center for Chronic Disease Prevention and Health Promotion Statistics,” cdc.gov. Payers face more than USD 4 trillion in annual treatment costs and therefore invest in platforms that raise adherence and prevent complications. Randomized studies show gamified tuberculosis protocols delivering 90.87% medication compliance versus the 80% standard, proving utility across diverse therapeutic areas. As chronic disease prevalence grows worldwide, digital tools that reward incremental behavior change secure budgets in payer, provider, and employer settings.

Proliferation of Smartphones and Wearable Devices

More than 85% of adults in developed economies carry smartphones, while global shipments of connected wearables surpassed 400 million units in 2024. Embedded sensors stream heart rate, activity, and sleep data that power real-time feedback loops central to the healthcare gamification market. The BE ACTIVE randomized trial combined gamification with financial incentives and raised daily step counts by 868 compared with controls, with benefits persisting six months post-intervention[2]American Heart Association, “Financial Incentives and Gamification in Physical Activity: BE ACTIVE Trial Results,” ahajournals.org. Device manufacturers now pre-install SDKs that support game mechanics such as leaderboards, streaks, and avatar progression, accelerating developer adoption. AI personalization engines fine-tune difficulty, targets, and rewards, keeping users engaged as baseline fitness or disease severity shifts.

Regulatory Endorsement of Digital Therapeutics

Regulators increasingly treat gamified software as evidence-based medical devices. The U.S. Food and Drug Administration cleared Akili’s EndeavorOTC for adult ADHD in June 2024 after studies showed 83% of users improved attention control. CMS followed with proposed Digital Mental Health Treatment billing codes effective 2025, giving providers a route to reimbursement and lifting a long-standing barrier. Europe’s Medical Device Regulation now references real-world evidence from digital therapeutics, aligning with U.S. precedents and shortening future review times. Companies that master clinical trials and post-market surveillance gain durable advantages because the process is capital-intensive and time-consuming.

Rising Demand for Patient Engagement Solutions

Value-based care ties hospital revenue to outcomes, forcing providers to track patient activity between visits. Gamified dashboards, missions, and point systems improve activation and adherence at scale, with virtual incentives costing less than live coaching. A multi-site deployment of an engagement platform for nurses and physicians cut self-reported burnout by 32% while boosting satisfaction scores. Pediatric clinics that combined chatbot education with game rewards achieved a Cohen’s d of 2.50 for parental nutrition knowledge gains. Such results support broader rollouts as health systems seek low-cost tools to meet quality benchmarks.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustaining long-term user engagement challenges | −1.8% | Global; affects consumer-based solutions | Short term (≤ 2 years) |

| Data privacy and security concerns | −1.3% | Global; stricter impact in Europe and other developed markets | Medium term (2–4 years) |

| Algorithmic bias in reward mechanics | −1.2% | Global; heightened scrutiny in regulated markets | Medium term (2–4 years) |

| Uncertain reimbursement pathways for prescription games | −1.5% | North America, Europe, emerging APAC markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sustaining Long-Term User Engagement Challenges

Health apps struggle to retain users after the novelty fades. Industry audits find that 80% of programs are abandoned within six months. A depression-focused serious game retained only 30% of eligible participants for the minimum therapeutic dose, underscoring the gap between initial curiosity and lasting adherence. Because clinical benefit depends on consistent play, developers must refresh content, add social competitions, and personalize pacing to avoid plateau-driven drop-offs. Early attrition especially hampers consumer-direct products that lack employer or provider reinforcement mechanisms.

Data Privacy and Security Concerns

Healthcare gamification platforms process biometric, behavioral, and psychological data subject to HIPAA in the U.S. and GDPR in Europe. Encryption, audit trails, and consent management raise development costs, while breaches invite fines as high as USD 1.5 million per violation. The American Health Information Management Association cautions that AI models trained on narrow populations risk bias and regulatory scrutiny[3]Journal of AHIMA Staff, “AI, Privacy, and Bias in Health Data,” journal.ahima.org. Privacy-preserving analytics such as federated learning address some concerns but slow performance and complicate onboarding. Organizations with limited cybersecurity budgets may delay adoption until vendor assurances improve.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Game Type: Clinical Evidence Elevates Serious Games

Serious games posted a 14.87% CAGR outlook from 2026 to 2031, outpacing casual titles that nonetheless held 38.12% revenue in 2025. FDA-cleared toolkits now help media studios embed validated biofeedback loops, merging entertainment reach with therapeutic rigor. Surgical simulators and VR-based anatomy modules show retention rates above 90% in continuing-education studies. Fitness-oriented exergames remain popular in employer wellness programs, but stringent reimbursement rules steer medical centers toward products backed by controlled trials.

The healthcare gamification market size for serious games addressing ADHD, post-stroke motor recovery, and chronic pain is projected to grow quickly as providers link software to electronic health records for outcome tracking. Hybrid casual-serious formats add mini-quests with clinical targets, broadening appeal among younger users. Companies that certify content under both entertainment ratings and medical device regulations access diversified revenue streams and reduce dependence on payer contracting cycles.

By Application: Therapeutics Gain Ground on Wellness

Prevention and wellness kept 41.92% revenue in 2025, yet prescription therapeutics and rehabilitation widen at a 16.42% CAGR. FDA authorization of CT-132 for episodic migraine in April 2025 positions prescription gaming as a mainstream treatment option. Tuberculosis adherence pilots that integrate biometric verification and reward streak calendars reached 90.87% compliance, supporting further investment in infectious-disease modules. Digital twin engines now simulate cardiac outputs to fine-tune exercise prescriptions, enhancing rehabilitation efficacy.

The healthcare gamification market share of therapeutic modules will accelerate as insurers reimburse software-only interventions that cost less than drugs and reduce readmissions. Pharmacovigilance dashboards embedded in apps flag side-effect patterns, enabling real-time clinician intervention. Education and training segments continue steady adoption in medical schools, which cite improved exam scores and reduced faculty demonstration hours after VR labs replaced mannequin-based setups.

By End User: Enterprises Anchor Commercial Adoption

Employers, payers, and provider networks captured 54.83% of spending in 2025 because they possess budgets tied directly to health outcomes and productivity. UnitedHealthcare’s UHC Rewards lets plan members earn up to USD 1,000 per year for sustained activity logging, driving 170% higher registration among self-insured groups. Chevron reports annual premium reductions of USD 750 for employees who complete streak-based wellness milestones. Retention rates are higher than in consumer-direct channels because participation is embedded in benefits portals and sometimes incentivized with lower copayments.

Consumer subscriptions grow at 16.05% CAGR as app stores roll out medical-grade categories that surface clinically validated titles. Families managing pediatric ADHD or autism spectrum disorders adopt paid plans that bundle coaching calls with in-game analytics. Pharmaceutical firms partner with platform providers to link coupon codes to medication adherence streaks, reinforcing brand loyalty while generating real-world evidence for regulators.

Geography Analysis

North America retained 42.11% revenue in 2025, propelled by FDA precedents, payer reimbursement clarity, and employer wellness budgets. CMS billing codes rolling out in 2025 will allow physicians to bill for digital mental health treatments, positioning the region for steady volume growth. The healthcare gamification market size registered robust spending in U.S. Medicaid populations where software addresses therapy shortages in rural areas.

Europe’s GDPR leadership demands strict consent flows, but successful compliance builds patient trust and distinguishes certified vendors. Germany’s DiGA framework fast-tracks software prescriptions reimbursed by statutory insurers, catalyzing launches that mirror U.S. FDA approvals. Nordic health systems deploy gamified platforms for remote physical therapy to tackle clinician shortages, citing 25% faster discharge timelines.

Asia-Pacific is the fastest-growing territory at 14.21% CAGR. Japan’s SB TEMPUS joint venture channels SoftBank capital into precision-medicine analytics combined with game-based engagement to personalize oncology care. Government-funded digital infrastructure in India and Indonesia bundles chronic-care pathways with low-cost smartphones, widening reach among under-served populations. Chinese municipal health bureaus pilot exergame-based fall-prevention curricula for seniors, aligning with national healthy-aging policy goals.

South America and the Middle East are nascent but promising. Brazil’s Unified Health System examines gamified smoking-cessation apps to curb rising noncommunicable disease costs, while Saudi Arabia’s Vision 2030 allocates subsidies for remote cardiac rehabilitation that leverages VR and point-scoring progress maps.

Competitive Landscape

The healthcare gamification market exhibits low concentration because capabilities span biotech, software, and entertainment. Akili Interactive secured first-mover advantage with FDA-cleared ADHD therapy and now adapts its engine for autism and executive-function disorders. DeepWell DTx offers an FDA-cleared biofeedback SDK that multiplies reach by licensing to independent studios, compressing time-to-clinic for partners while taking a revenue share.

Pharmaceutical alliances accelerate scale: Click Therapeutics collaborates with Otsuka to combine digital and pharmacologic treatments for depression. Relevate Health’s acquisition of Level Ex Games’ pharma division merges medical-education credibility with game-design talent to serve clinicians. Tech giants enter selectively; Apple bundles fitness quests with watch-based vitals, but regulatory burden deters them from prescription categories.

Differentiation hinges on AI-driven personalization, validated outcome measures, and payer integration rather than entertainment metrics. Niche opportunities persist in pediatric oncology, women’s health, and rare diseases where few competitors have collected sufficient clinical data. Vendors that overlay digital twin modeling on rehabilitation scenarios deliver quantifiable improvements that strengthen reimbursement negotiations.

Healthcare Gamification Industry Leaders

Nike Inc.

Fitbit Inc.

Microsoft Corp.

Apple Inc.

Akili Interactive Labs Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Click Therapeutics received FDA clearance for CT-132, the first prescription digital therapeutic for episodic migraine.

- March 2025: April Health and Wysa merged to broaden behavioral health access with AI-driven, game-inspired modules.

- February 2025: XRHealth acquired RealizedCare to expand immersive rehabilitation content that tracks motion and issues points for correct form.

- January 2025: Avel eCare purchased Amwell Psychiatric Care, adding gamified adherence touchpoints to its telepsychiatry network.

- June 2024: Akili Interactive earned FDA authorization for EndeavorOTC, the first over-the-counter ADHD treatment delivered via video game.

Global Healthcare Gamification Market Report Scope

Healthcare gamification can be defined as applying gaming principles, game design techniques, and game mechanics to non-game applications in order to improve clinical outcomes.

The healthcare gamification market is segmented by type, application, end-user, and geography. By type, the market is segmented into exercise game, serious game, and casual game. By application, the market is segmented into education, therapeutics, and prevention. By end user, the market is segmented into enterprises and consumers. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Exercise / Exergame |

| Serious Game |

| Casual Game |

| Simulation & VR/AR-based Game |

| Education & Training |

| Therapeutics & Rehabilitation |

| Prevention & Wellness |

| Medication & Adherence Management |

| Enterprise-based (Providers, Payers, Employers) |

| Consumer-based |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Game Type | Exercise / Exergame | |

| Serious Game | ||

| Casual Game | ||

| Simulation & VR/AR-based Game | ||

| By Application | Education & Training | |

| Therapeutics & Rehabilitation | ||

| Prevention & Wellness | ||

| Medication & Adherence Management | ||

| By End User | Enterprise-based (Providers, Payers, Employers) | |

| Consumer-based | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the healthcare gamification market?

The sector is worth USD 6.41 billion in 2026 and is forecast to reach USD 11.78 billion by 2031.

Which application area is growing the fastest?

Therapeutics and rehabilitation are expanding at a 16.42% CAGR as FDA-approved digital treatments gain reimbursement.

Why are enterprises leading adoption?

Employers and insurers capture ROI from reduced claims and higher productivity, giving enterprise solutions 54.83% market share in 2025.

Which region offers the highest growth potential?

Asia-Pacific shows the fastest trajectory with a 14.21% CAGR thanks to smartphone penetration and national digital-health initiatives.

What main challenge threatens long-term growth?

Sustaining user engagement is critical, as 80% of health apps are abandoned within six months without fresh content and social reinforcement.

How are regulators influencing market momentum?

FDA and CMS approvals create defined reimbursement codes, shifting gamified software from wellness tools to recognized medical devices.

Page last updated on: