Mental Health Apps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

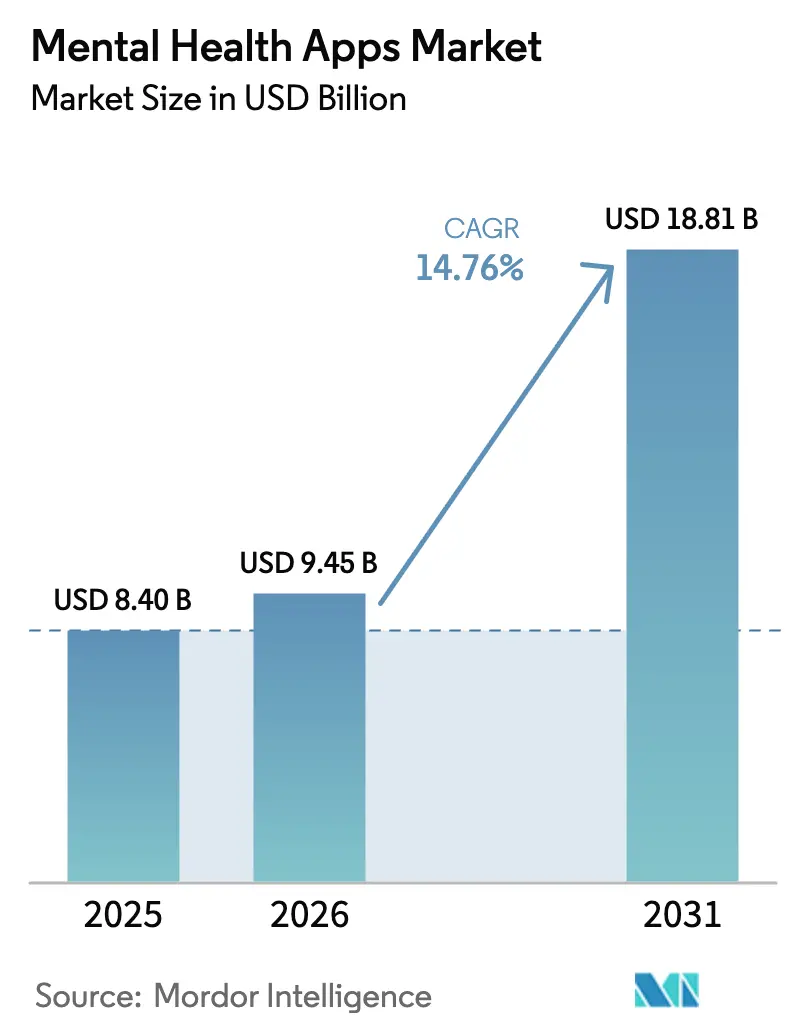

| Market Size (2026) | USD 9.45 Billion |

| Market Size (2031) | USD 18.81 Billion |

| Growth Rate (2026 - 2031) | 14.76% CAGR |

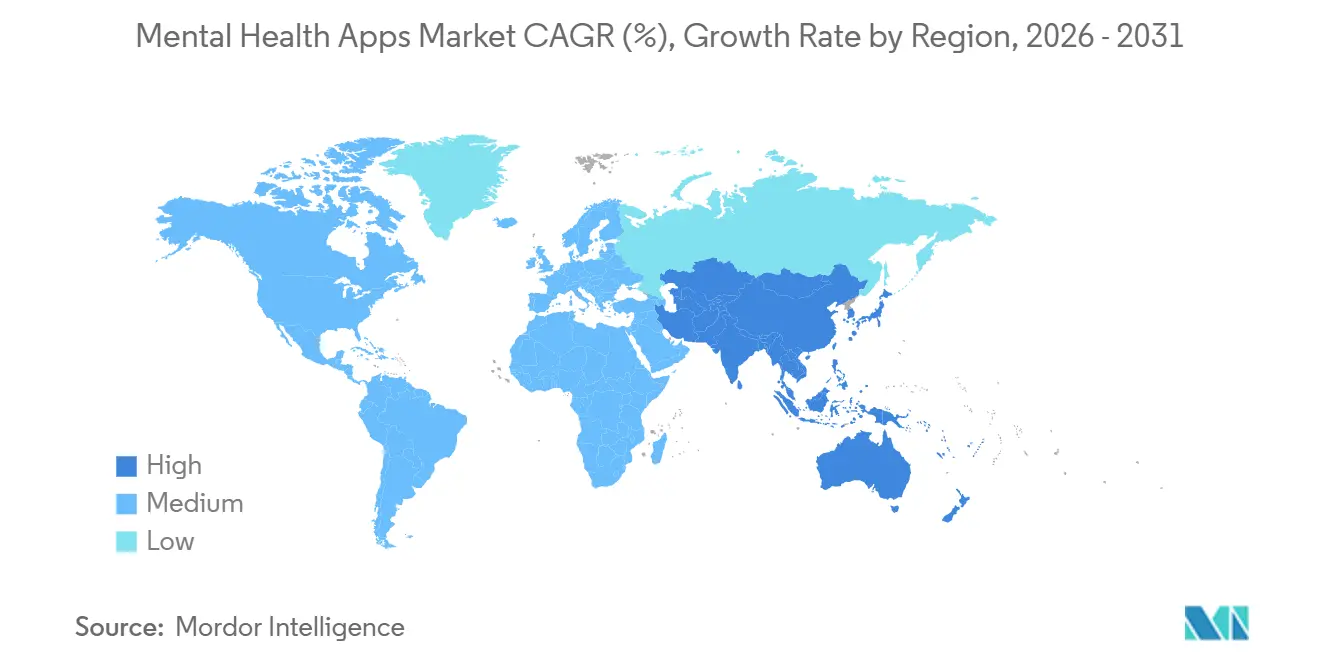

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

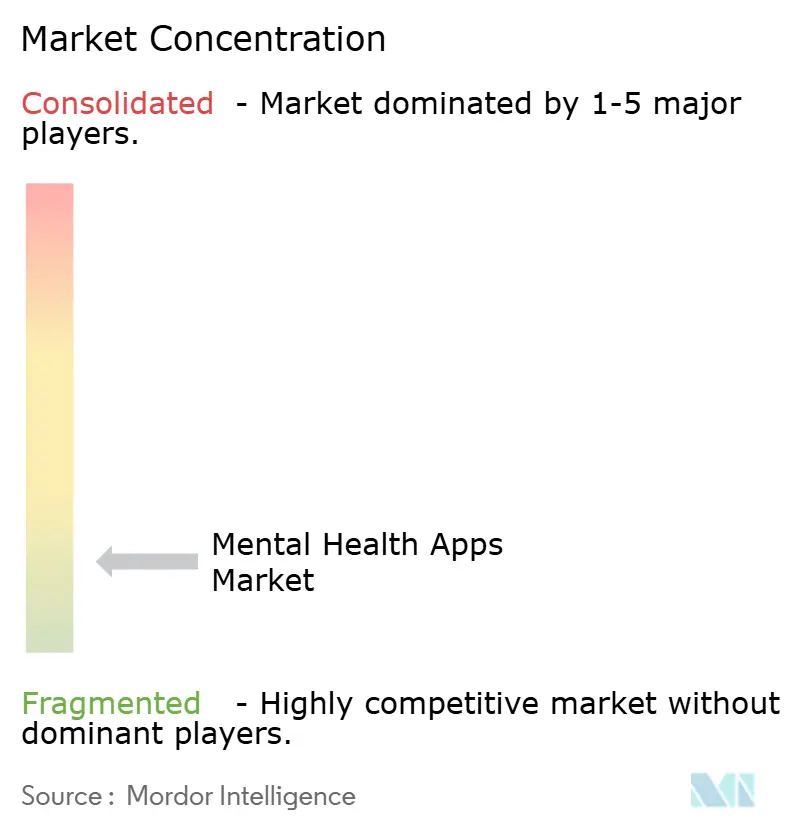

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mental Health Apps Market Analysis by Mordor Intelligence

The Mental Health Apps Market size was valued at USD 8.40 billion in 2025 and is estimated to grow from USD 9.45 billion in 2026 to reach USD 18.81 billion by 2031, at a CAGR of 14.76% during the forecast period (2026-2031).

Strong clinical evidence for app-based cognitive behavioral therapy, newly activated U.S. reimbursement codes, and Apple’s on-device State of Mind logging each widen the addressable mental health apps market. The shift from direct-to-consumer cash payments to employer and payer funding reshapes revenue mix, drives higher engagement, and cuts acquisition costs. Rapid smartphone adoption in India and Indonesia is expanding the mental health apps market beyond mature economies, while AI chatbots are personalizing content and enhancing adherence. Consolidation quickens as buyers seek FDA-cleared assets, yet more than 10,000 titles continue to maintain competitive intensity. Privacy-first operating system features alleviate data concerns and enable employer deployment at scale.

Key Report Takeaways

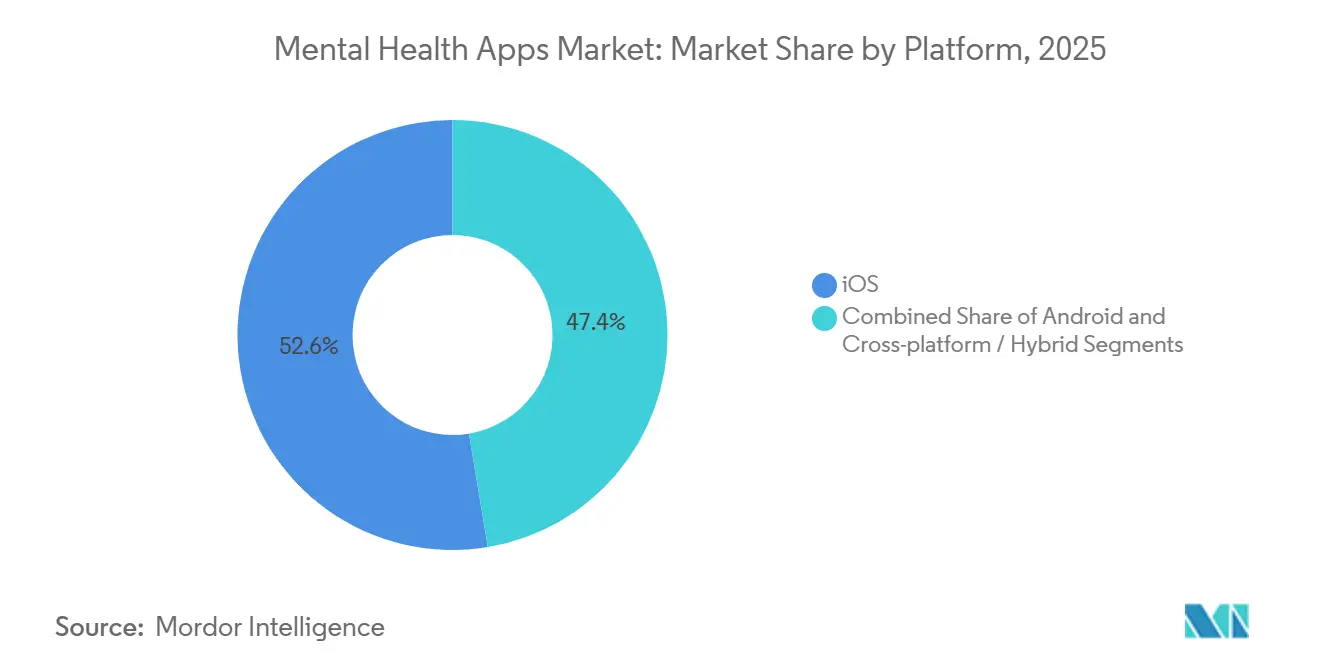

- By platform, iOS led with 52.63% of mental health apps market share in 2025 while Android is forecast to expand at a 17.45% CAGR through 2031.

- By application, depression and anxiety tools captured 30.13% of the mental health apps market share in 2025 and stress management apps are set to grow at a 16.34% CAGR to 2031.

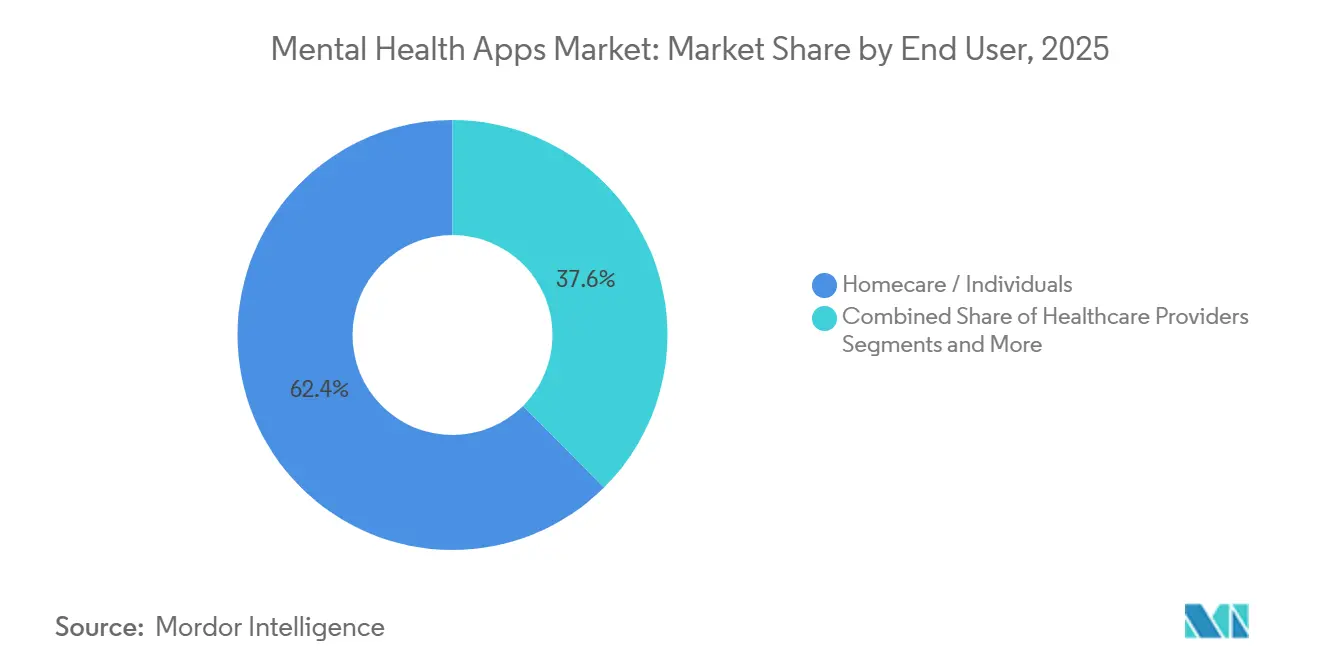

- By end user, homecare and individuals held 62.44% of the mental health apps market share in 2025 whereas employer programs are projected to advance at a 17.02% CAGR during the forecast period.

- By age group, adults accounted for 68.78% of the mental health apps market share in 2025 and the children and adolescent segment is poised for a 16.07% CAGR to 2031.

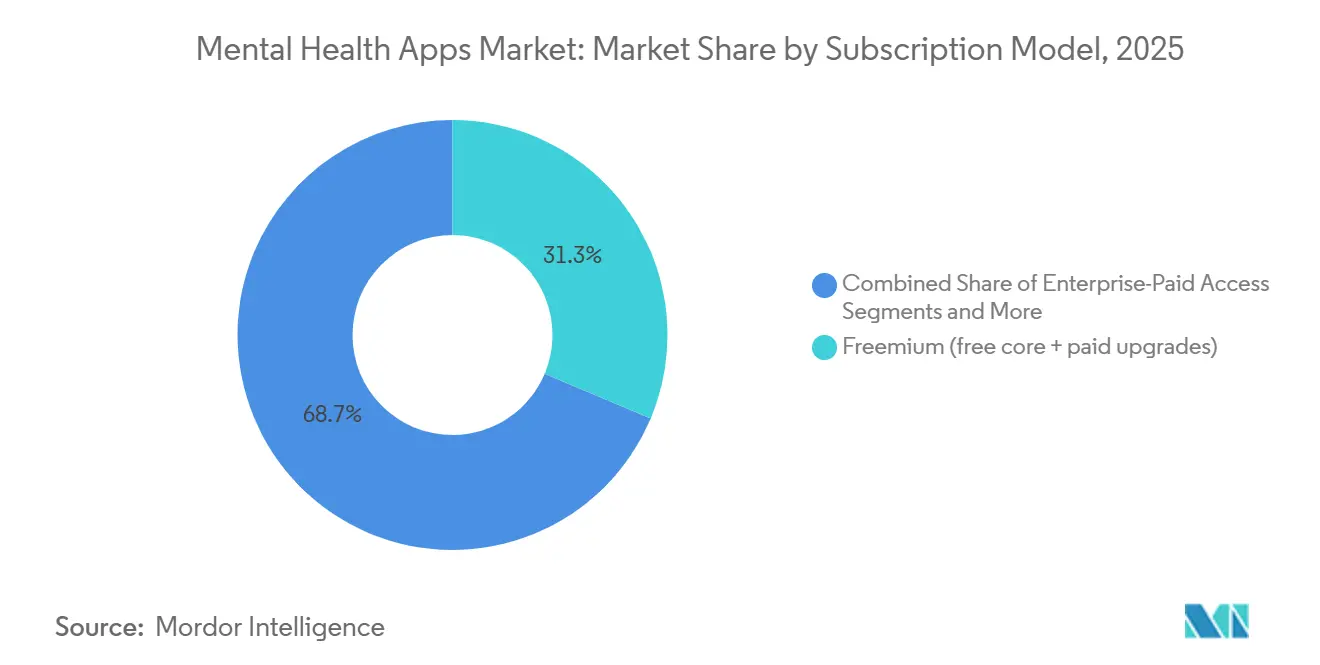

- By subscription model, freemium plans commanded 31.34% of the mental health apps market share in 2025 while paid plans are expected to rise at a 15.77% CAGR through 2031.

- By geography, North America generated 37.56% revenue in 2025 and Asia-Pacific is estimated to post a 17.55% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Mental Health Apps Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of anxiety and depression globally | 3.2% | Global, with acute pressure in North America and Europe | Long term (≥ 4 years) |

| Smartphone penetration and app-store distribution scale | 2.8% | APAC core (India, Indonesia, Vietnam), spill-over to MEA | Medium term (2-4 years) |

| Employer and payer adoption of digital mental health benefits | 2.5% | North America and Western Europe, early pilots in Australia | Medium term (2-4 years) |

| AI chatbots and CBT personalization improving access and outcomes | 2.3% | Global, with faster uptake in English-speaking markets | Short term (≤ 2 years) |

| Shift from D2C cash-pay to insurance-billed hybrid models | 1.9% | North America, Germany, France, Netherlands | Medium term (2-4 years) |

| OS-level mental health features and on-device AI enable privacy-first adoption | 1.7% | Global, concentrated in iOS ecosystem initially | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Burden Of Anxiety And Depression Globally

More than 1 billion people live with a mental disorder, and treatment gaps stay wide.[1]World Health Organization, “Over a Billion People Living With Mental Health Conditions: Services Require Urgent Scale-Up,” WHO News, who.int U.S. surveys in 2024 showed 19% of adults reported depression and anxiety, while 42% of high-school students felt persistently sad.[2]Centers for Disease Control and Prevention, “Mental Health Numbers,” CDC Healthy Youth, cdc.gov Eight thousand U.S. regions lacked enough professionals, leaving 167 million residents underserved. Evidence now places app-based CBT on par with face-to-face therapy for mild cases. Validated results move apps onto payer formularies, converting unmet need into the expanding mental health apps market.

Smartphone Penetration And App-Store Distribution Scale

Smartphone ownership reached 52% in India and 68% in Indonesia by 2024. App stores let developers reach new users at minimal marginal cost and update weekly, speeding feature iteration. Wysa gained 5 million users and embedded its chatbot in leading Indian hospital systems.[3]Sarah Baldry, “Wysa To Develop Hindi Version of World's Most Popular Mental Health App,” Wysa Blog, wysa.io Japanese public campaigns raised demand for Awarefy and Emol. Fast feedback loops cut the attrition that plagues stand-alone digital content and enlarge the global mental health apps market.

Employer And Payer Adoption Of Digital Mental Health Benefits

Seventy-four percent of U.S. employers offered meditation or mindfulness apps in 2024, up from 52% in 2020. Spring Health now covers more than 10 million lives through per-employee contracts, and Lyra Health reached a USD 5.58 billion valuation in 2022. Medicare Advantage began reimbursing app sessions in 2025 at USD 15-45 each. Payers direct members to lower-cost digital channels first, trimming claims by up to 30% and growing the mental health apps market.

AI Chatbots And CBT Personalization Improving Access And Outcomes

Woebot’s 2024 trial showed a 22% drop in PHQ-9 scores within four weeks and 83% adherence. Wysa achieved a 30% reduction in GAD-7 scores across India and the U.K. Youper deployed large language models in 2025 to produce empathetic exchanges, which increased session time. Personalized sequencing increases engagement and widens the mental health apps market footprint.

Restraints Impact Analysis of Mental Health Apps Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory classification ambiguity and evidence thresholds | -1.2% | Global, acute in EU and post-Brexit UK | Long term (≥ 4 years) |

| Data privacy and cybersecurity risks erode trust and add compliance cost | -1.0% | Global, with GDPR/HIPAA enforcement concentrated in EU and North America | Medium term (2-4 years) |

| Subscription fatigue and high churn depress LTV of paid apps | -0.9% | Global, most visible in mature D2C markets (North America, Western Europe) | Short term (≤ 2 years) |

| App store privacy changes and paid acquisition costs raise CAC | -0.8% | Global, concentrated in iOS ecosystem | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Classification Ambiguity And Evidence Thresholds

The FDA cleared only two prescription digital therapeutics for mental health, and both left the market after Pear Therapeutics’ bankruptcy. Germany’s DiGA directory contained 53 reimbursable apps by late 2024, each needing randomized trial proof within a year. Fragmented rules force multi-country filings that can cost up to USD 1 million. Small developers struggle with these demands, slowing new evidence-grade launches and tempering growth in the mental health apps market.

Data Privacy And Cybersecurity Risks Erode Trust

The U.S. Office for Civil Rights issued 14 penalties in 2024 for unauthorized data sharing, reaching USD 5.1 million per case. The Irish regulator fined a developer EUR 2.3 million under GDPR. Mozilla’s 2024 audit found 37% of iOS mental health apps sent identifiers to Facebook. HIPAA-grade infrastructure adds as much as USD 300,000 in yearly overhead, squeezing margins across the mental health apps industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Mental Health Apps Market Segment Analysis

By Platform:

iOS Dominance Faces Android Volume SurgeiOS held 52.63% of mental health apps market share in 2025 due to higher average revenue per user and strong privacy controls. Android is set to grow at a 17.45% CAGR because India, Indonesia, and China now supply most new smartphone users. Cross-platform frameworks cut build costs yet miss native features that deepen engagement. Wearables-first designs stay niche but validate passive tracking. Together these trends diversify the mental health apps market.

Apple’s on-device AI encrypts data and satisfies employer risk teams, boosting adoption in corporate programs. Google’s Health Connect mirrors this privacy stance for Android. Paid conversion remains stronger on iOS, yet enterprise sponsorship is bridging the gap on Android. Platform strategies will determine monetization pathways across the mental health apps market.

By Application:

Stress Management Gains As Employers Prioritize PreventionDepression and anxiety tools captured 30.13% of the mental health apps market share in 2025 on the back of FDA 510(k) clearances for Sleepio and Daylight. Stress management apps are projected to rise at a 16.34% CAGR as employers bundle mindfulness to curb absenteeism. Meditation apps face free-content competition, while sleep solutions benefit from wearable data. Substance use and PTSD apps remain underserved, leaving white space within the mental health apps market.

Employer demand for preventive tools helps stress apps outpace legacy meditation catalogs. Integration with Apple Watch and Fitbit sleep scores anchors engagement. The limited pipeline for substance use care after Pear’s exit signals an acquisition opportunity for validated newcomers. Niches such as eating disorder support need careful design to avoid triggering behaviors, yet they remain part of the broader mental health apps industry.

By End User:

Enterprise-Paid Access Reshapes EconomicsHomecare users controlled 62.44% of mental health apps market share in 2025, yet churn and low lifetime value cap revenue potential. Employer programs are forecast to grow at a 17.02% CAGR as per-employee fees remove cost barriers. Healthcare providers use dashboards to scale therapist reach, while payers now reimburse digital sessions. These channels distribute risk and sustain the mental health apps market size.

Spring Health and Lyra Health show that enterprise contracts cut acquisition cost and triple engagement relative to direct-to-consumer models. CMS reimbursement aligns digital therapy payments with stepped-care models, moving apps into the covered benefits mix. Interoperability demands raise engineering spend but deepen integration into clinical ecosystems, fortifying the mental health apps market.

By Age Group:

Youth Crisis Drives Adolescent Segment GrowthAdults represented 68.78% of users in 2025, reflecting smartphone fluency and diagnosis rates. Children and adolescents are projected to rise at a 16.07% CAGR after U.S. pediatric bodies declared a youth mental health emergency. School programs embed kid-friendly apps under parental consent workflows, enlarging the mental health apps market.

Design limits curb addictive game loops and protect privacy for minors, while compliance with COPPA remains mandatory. Geriatric adoption lags because of usability challenges, yet age-friendly interfaces from firms such as SilverCloud suggest latent demand. Broad demographic reach underpins the long-term expansion of the mental health apps market.

By Subscription Model:

Enterprise Sponsorship Outpaces FreemiumFreemium tiers held 31.34% of mental health apps market share in 2025 but convert poorly to paid plans. Paid subscriptions are forecast to climb at a 15.77% CAGR as employers and payers absorb fees. In-app microtransactions offer high-margin add-ons for reluctant subscribers. Reimbursement codes price sessions above enterprise per-member fees, opening blended models that bolster the mental health apps market size.

Spotify and YouTube crowd the meditation niche, pressing Calm and Headspace to diversify revenue. Enterprise sponsorship shapes higher engagement and reduces churn. Hybrid billing that mixes insurance rates with employer coverage hedges volatility and stabilizes cash flow across the mental health apps industry.

Geography Analysis

North America Mental Health Apps Market

North America produced 37.56% of global revenue in 2025, fueled by wide employer adoption and the 2025 CMS codes that reimburse digital therapy sessions. The United States alone delivered 85% of the region’s value as self-insured firms adopted Spring Health and Lyra Health to curb claims. Canada and Mexico trail because fragmented payor systems complicate reimbursement, though Dialogue Health Technologies expanded mental health offerings for Canadian employers in 2024. CAC inflation from Apple privacy policies squeezed direct-to-consumer margins, yet enterprise channels kept the mental health apps market growing.

APAC Mental Health Apps Market

Asia-Pacific is projected to post the fastest regional expansion at a 17.55% CAGR through 2031. Smartphone ownership and destigmatization campaigns push adoption in India, Indonesia, and China. Wysa’s partnerships with Apollo and Manipal hospitals integrate chatbots into clinical care, while Japanese government initiatives boosted use of Awarefy and Emol. South Korea piloted reimbursement through the National Health Insurance Service. Anonymity addresses cultural stigma, lifting participation and enlarging the mental health apps market.

Europe Mental Health Apps Market

Europe is led by Germany’s DiGA pathway with 53 reimbursable apps. France’s Forfait Innovation approves tools but lacks fixed pricing, slowing roll-out. The U.K. NHS Apps Library sets safety and privacy standards, yet post-Brexit divergence adds duplication. Northern Europe’s high digital literacy speeds adoption, while the Mediterranean and Eastern regions advance slowly. Outside Europe, emerging programs in Brazil and select Middle East markets signal early interest, but infrastructure gaps limit near-term contribution to the mental health apps market.

Competitive Landscape

More than 10,000 titles populate app stores, yet 2024 saw faster consolidation when Headspace bought Big Health’s FDA-cleared Sleepio and Daylight. Customer acquisition costs, rather than clinical features, now set the competitive bar. Apple’s privacy rules inflated CAC by up to 50% and contributed to Calm’s valuation decline, while Headspace, Cerebral, and Noom enacted layoffs. Two strategy lanes dominate: mass-market subscriptions from Calm and Headspace versus enterprise contracts from Spring Health, Lyra Health, and Modern Health. These tracks segment the mental health apps market.

Regulatory gaps create openings. Pear Therapeutics’ bankruptcy removed the only cleared substance use solutions, inviting new entrants. Generative AI differentiates emerging players: Woebot, Wysa, and Youper implement large language models that improve adherence and user satisfaction. On-device encryption from Apple and similar measures from Google reassure employers and accelerate B2B uptake. Strategic buyers hunt for assets with real-world evidence, suggesting further mergers will shape the mental health apps market.

Sustained fragmentation keeps pricing power low, yet validated clinical outcomes help premium apps stand apart. Enterprise clients value analytics that identify at-risk populations, enhancing retention. As reimbursement expands, evidence and interoperability become acquisition triggers. This dynamic sets the stage for continued reinvention within the global mental health apps industry.

Mental Health Apps Industry Leaders

Teladoc Health

Calm

Cerebral

Talkspace

Headspace

- *Disclaimer: Major Players sorted in no particular order

Mental Health Apps Market Companies Covered in this Report

- Calm.com Inc.

- Headspace Health

- BetterHelp (Teladoc Health)

- Talkspace Inc.

- Sanvello Health Inc.

- Wysa Ltd.

- Happify Health

- MoodMission

- Youper

- K Health

- CVS Health (Aetna Inc.)

- Lyra Health

- Spring Health

- Big Health (Sleepio)

- Unmind Ltd.

- Inner Explorer Inc.

- Insight Timer

- MoodTools

- TimelyCare

- MindDoc Health GmbH

- Kintsugi

Recent Industry Developments in Mental Health Apps Market

- October 2025: Union Minister of Health and Family Welfare, India, launched the Tele MANAS App in ten regional languages with chatbot and emergency modules.

- October 2025: Australian startup Give Me 5 invested AUD 5 million to pilot its GM5 Beta App in Hyderabad.

- October 2025: Talkspace acquired Wisdo Health to integrate peer support and group coaching.

- July 2025: LISSUN bought U.S. startup Being Cares Inc. to enhance AI-driven child-focused mental health care in India.

Mental Health Apps Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the mental health apps market as all downloadable iOS, Android, and progressive-web applications whose core purpose is to screen, monitor, or ease clinically recognized mental health conditions such as anxiety, depression, stress, substance use disorder, and insomnia. Revenue is tracked at the point developers or distributors earn money; one-time fees, in-app purchases, or recurring subscriptions are expressed in U.S. dollars for 2025.

Scope exclusion: tools that only count steps, general fitness or diet trackers, and telepsychiatry platforms that require live clinician oversight are excluded.

Segments Covered in This Report

- By Platform Type

- iOS

- Android

- Web/Progressive Web Apps

- Others (Wearable-first, Voice-only)

- By Application

- Depression and Anxiety Management

- Stress Management

- Meditation and Mindfulness

- Sleep and Wellness Improvement

- Substance-Use Disorder Support

- Other Applications

- By End User

- Home-care Settings

- Employers and Corporate Wellness Programs

- Mental Hospitals and Clinics

- Schools and Universities

- Other End Users

- By Age Group

- Children and Adolescents (≤17 yrs)

- Adults (18-64 yrs)

- Geriatric (65+ yrs)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

To fill gaps, Mordor analysts interviewed digital health entrepreneurs, practicing psychiatrists, corporate benefits managers, and app store category specialists across North America, Europe, and Asia Pacific. These conversations validated usage cohorts, churn rates, and future reimbursement prospects that secondary sources only hinted at.

Desk Research

We began with structured searches across public sources such as the World Health Organization, the U.S. National Institute of Mental Health, the OECD Health Statistics portal, and app store download leaderboards, which helped us profile prevalence, user adoption, and spending patterns. Company filings, investor decks, and reputable trade associations, including the mHealth Regulatory Coalition, clarified average selling prices and regulatory shifts. Our analysts also referenced subscription and revenue data mined from paid databases like D&B Hoovers and Dow Jones Factiva to benchmark key players' financial footprints. This list is illustrative; numerous additional references informed the evidence base.

Market-Sizing & Forecasting

A combined top-down and bottom-up logic underpins the model. We start with smartphone populations by region and apply penetration rate build-ups that reflect diagnosed prevalence, download propensity, and conversion to paid tiers, which are then cross-checked against sampled developer revenues and channel checks. Key variables include smartphone penetration growth, median subscription price, clinically diagnosed anxiety and depression rates, employer mental wellness budget trends, and evolving privacy regulations. Multivariate regression, supported by ARIMA smoothing for short-term seasonality, projects each driver through 2030. Where bottom-up estimates under report emerging markets, adjustment factors derived from primary interviews close the gap.

Data Validation & Update Cycle

Outputs pass three filters: variance checks against historical series, peer review by a senior analyst, and a reconciliation against fresh news in Dow Jones Factiva. Reports refresh annually, and we issue interim revisions when material policy or funding events occur, ensuring clients receive an up-to-date baseline.

How Mordor Intelligence's Mental Health Apps Market Size Compares to Other Published Estimates

Published figures often vary because firms pick different revenue streams, user cohorts, or refresh cadences. Our disciplined scope selection and annual refresh mean decision makers can rely on a value that balances optimism with traceable evidence.

Key gap drivers include whether free downloads are monetized, how aggressively lifetime value is extrapolated, and the frequency with which new reimbursement codes are folded into models.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.5 B | Mordor Intelligence | - |

| USD 8.87 B | Global Consultancy A | Includes mindfulness and generic wellness apps; assumes uniform 3-year paid conversion |

| USD 7.48 B | Industry Data Firm B | Excludes employer bulk license revenues; uses 2023 ASP without inflation adjustment |

In short, Mordor's balanced scope, variable transparency, and twice validated model provide a dependable starting point for investors, developers, and policymakers who must act on trustworthy numbers.

Key Questions Answered in the Report

How large is the mental health apps market in 2026?

The mental health apps market size is USD 9.45 billion in 2026 with a 14.76% CAGR toward 2031.

Which platform leads adoption?

IOS holds 52.63% of mental health apps market share, though Android is growing faster at a 17.45% CAGR.

What segment is expanding the quickest?

Stress management applications are projected to rise at a 16.34% CAGR as employers prioritize preventive care.

How are employers influencing growth?

Per-employee contracts between USD 2 and USD 6 remove user payment friction and raise engagement threefold.

Which region will see the fastest growth?

Asia-Pacific is expected to deliver a 17.55% CAGR, supported by rising smartphone use and destigmatization programs.

What drives consolidation among app providers?

Higher customer acquisition costs and demand for validated clinical outcomes encourage mergers and strategic buyouts.

Page last updated on: