Behavioral And Mental Health Software Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

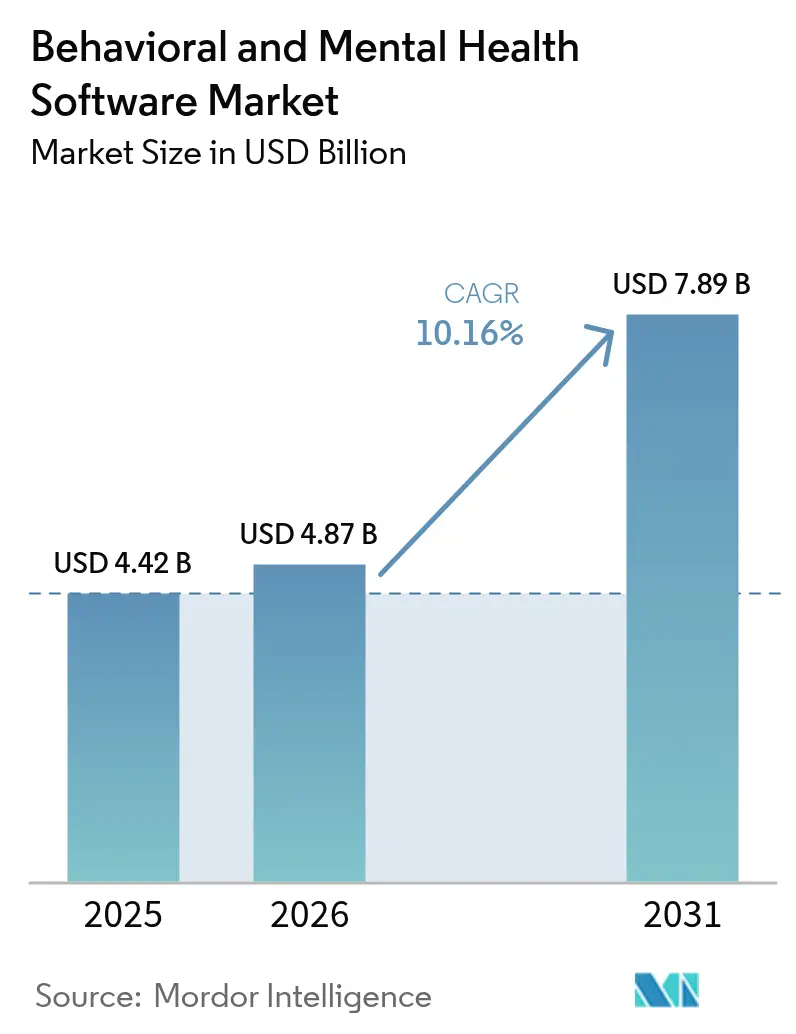

| Market Size (2026) | USD 4.87 Billion |

| Market Size (2031) | USD 7.89 Billion |

| Growth Rate (2026 - 2031) | 10.16% CAGR |

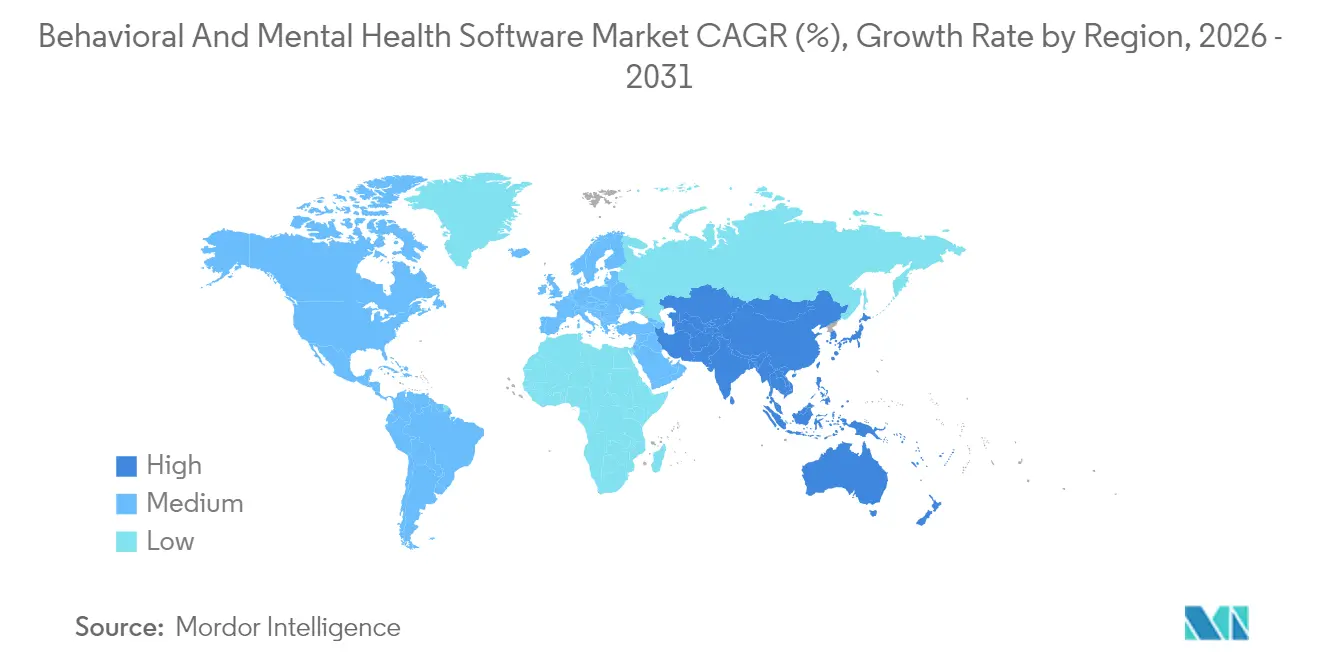

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Behavioral And Mental Health Software Market Analysis by Mordor Intelligence

The behavioral and mental health software market size is expected to grow from USD 4.42 billion in 2025 to USD 4.87 billion in 2026 and is forecast to reach USD 7.89 billion by 2031 at 10.16% CAGR over 2026-2031. Across every delivery setting, payers, providers, and employers are re-platforming legacy workflows onto purpose-built behavioral tools as AI-driven triage, measurement-based care, and automated documentation prove they can compress clinician workload and lift outcomes. Key lift factors include permanent tele-mental-health reimbursement codes, cloud cost efficiencies that remove capital barriers for small practices, and federal incentives that finally put behavioral providers on parity with acute-care peers for EHR subsidies. In parallel, growing public concern over climate anxiety and workplace burnout is redirecting self-care traffic toward evidence-based apps, expanding total addressable demand for software vendors that embed validated assessments and CBT-based micro-interventions. Accelerating consolidation among vendors and sustained funding flows from private equity and strategics further reinforce the medium-term expansion thesis for the behavioral and mental health software market.

Key Report Takeaways

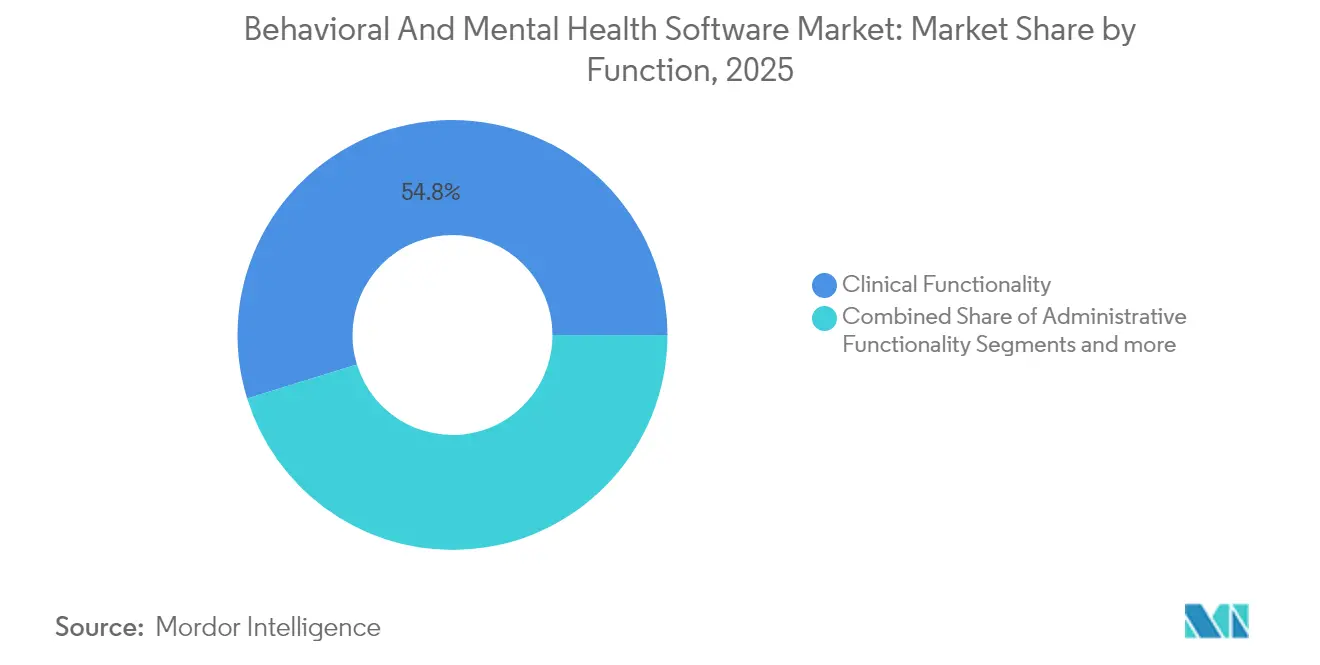

- By function, Clinical Functionality led with 54.78% revenue share of the behavioral and mental health software market in 2025, while Administrative Functionality is projected to expand at an 11.02% CAGR to 2031.

- By solution, Software accounted for 63.08% of the behavioral and mental health software market size in 2025; the Services segment is growing fastest at an 10.88% CAGR through 2031.

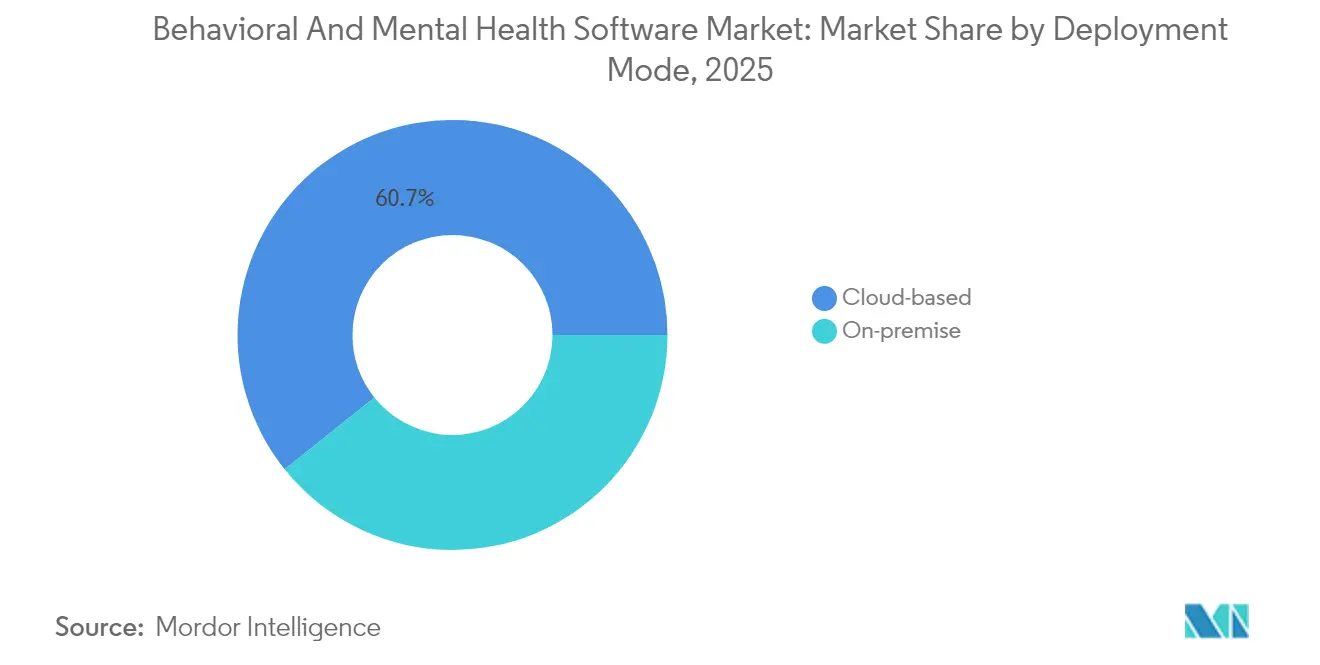

- By deployment mode, Cloud solutions held 60.74% of the behavioral and mental health software market share in 2025, yet On-premise is forecast to increase at an 11.05% CAGR on sovereignty concerns.

- By end-user, Hospitals captured 42.71% of the behavioral and mental health software market size in 2025, while Private Practices are advancing at an 11.06% CAGR to 2031.

- By geography, North America dominated with 41.86% share in 2025; Asia-Pacific is expected to register the highest 11.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Behavioral And Mental Health Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing stress-related mental-health conditions | +2.8% | Global, strongest in North America & Europe | Medium term (2-4 years) |

| Government funding & EHR incentives for behavioral health | +2.1% | North America primary, expanding to APAC | Short term (≤ 2 years) |

| Payer acceptance & reimbursement for tele-mental-health | +1.9% | North America, Europe, selected APAC | Medium term (2-4 years) |

| AI-powered clinical decision support improves outcomes | +1.7% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Climate-anxiety boosts demand for digital self-help tools | +1.2% | Global, eco-conscious regions | Medium term (2-4 years) |

| Employer-sponsored mental-health platforms surge | +1.5% | North America & Europe, emerging in APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Stress-Related Mental-Health Conditions

More than 26% of U.S. adults report a diagnosable mental condition each year, a prevalence now mirrored across several European countries, pushing providers toward scalable digital screening and care-navigation tools [1]Office of the National Coordinator for Health IT, “2025 Behavioral Health Funding Opportunities,” healthit.gov. Software vendors are packaging over 400 standardized assessments and real-time analytics that flag risk for climate anxiety, workplace burnout, and social-media-induced stress. In Asia, disability-adjusted life years tied to mental disorders jumped from 43.9 million to 69 million between 1990 and 2019, steering demand for multilingual mobile apps that can triage large rural populations. Intermountain Health’s deployment of NeuroFlow’s AI risk models illustrates how predictive scoring cuts time to intervention by identifying suicidal ideation within routine primary-care encounters. As these modules integrate seamlessly with core EHR workflows, adoption accelerates across both enterprise health systems and solo practices. Together, these epidemiologic and technology trends enlarge the addressable behavioral and mental health software market.

Government Funding & EHR Incentives for Behavioral Health

The U.S. Improving Access to Behavioral Health Information Technology Act cleared the path for CMS to reimburse psychologists, psychiatric hospitals, and community mental-health centers for certified EHR adoption. Separate ONC programs earmarked USD 20 million for behavioral workflows, while SAMHSA funds extend state Medicaid matches for software that supports crisis response and tele-behavioral capabilities. Collectively, these initiatives shrink the historic digital divide where only 6% of specialty behavioral facilities used EHRs versus 97% of hospitals. Smaller practices now access targeted grants plus technical-assistance hubs that streamline vendor evaluation and change management [2]Centers for Medicare & Medicaid Services, "Accessing Enhanced Federal Medicaid Matching Rates for State Information Technology Expenditures to Improve Access to Mental Health and Substance Use Disorder Treatment and Care Coordination," medicaid.gov. As dollars flow, vendors see record inbound RFP volume, fueling growth in the behavioral and mental health software market.

Payer Acceptance & Reimbursement for Tele-Mental-Health

UnitedHealthcare’s 2025 fee schedule codifies permanent tele-behavioral codes for clinical psychologists, including remote physiologic monitoring CPTs that software must auto-populate. Medicare added new behavioral health modifiers, and most U.S. states moved closer to parity on synchronous tele-visit reimbursement. In Europe, insurers in Germany and France introduced bundled payments tied to symptom-score improvement, nudging platforms toward outcome documentation. Vendors therefore embed automated coding engines, prior-authorization prompts, and claim-scrubbing to trim denials. This reimbursement clarity accelerates revenue capture, enhancing ROI narratives that expand the behavioral and mental health software market.

AI-Powered Clinical Decision Support Improves Outcomes

Oracle Health’s 2025 cloud EHR layers voice commands, ambient scribe, and predictive medication alerts that reduce documentation time by 40%. Peer-reviewed trials show Therabot achieving 51% symptom reduction in depression and 31% in anxiety within four weeks, while WiseMind’s multi-agent framework reached 84.2% diagnostic accuracy versus human experts. NeuroPal’s multimodal LLM registered an 89.1% adherence rate in a 513-patient RCT, outperforming therapist-guided CBT on sleep-quality metrics. Vendors integrating evidence-backed CDS tools gain competitive lift, particularly where payers tie bonuses to validated improvement scales. These data points reinforce investor confidence and stimulate M&A, deepening capabilities across the behavioral and mental health software market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy & cybersecurity gaps | -1.8% | Global, strongest in regulated markets | Short term (≤ 2 years) |

| Continued use of paper workflows among small providers | -1.4% | Rural & underserved areas worldwide | Medium term (2-4 years) |

| Interoperability gaps between general & BH-specific EHRs | -1.1% | North America & Europe | Medium term (2-4 years) |

| Uncertain parity laws for digital therapeutics reimbursement | -0.9% | North America, emerging Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy & Cybersecurity Gaps

Behavioral data carry heightened stigma risk, so breaches prompt outsized regulatory and reputational penalties. The FTC’s enforcement against Cerebral spotlighted tracking-pixel misuse, pushing vendors to adopt on-device analytics, geofenced consent, and zero-trust architectures. EU GDPR rules further complicate cross-border deployments, forcing granular data-minimization and “right to be forgotten” workflows. Many small practices lack cyber budgets for 24/7 monitoring, making them hesitant to migrate sensitive charts to cloud stacks. As a result, near-term behavioral and mental health software market expansion slows where privacy doubts remain unresolved.

Continued Use of Paper Workflows Among Small Providers

Only 30% of behavioral clinicians use an EHR, versus 74% of office-based physicians, with rural clinics lagging most. Barriers span up-front license fees, training fatigue, and fear of productivity dips during cut-over. Studies show low computer literacy, alert fatigue, and cumbersome templates derail adoption unless vendors tailor interfaces and fund hands-on onboarding. Until cost-down versions and micro-grant subsidies reach this cohort, the behavioral and mental health software market will under-penetrate thousands of small practices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function: Clinical Functionality Drives Core Adoption

Clinical modules captured 54.78% of 2025 revenue, underpinning every modern deployment decision. This dominance stems from electronic charting, order sets, and integrated care plans that clinicians rely on daily. Oracle Health’s ambient documentation reduces note time by 40%, illustrating why providers anchor platform selection on clinical depth. Administrative add-ons are heating fastest with an 11.02% CAGR as practices seek automated intake, referral routing, and prior-auth checks. Revenue-cycle widgets further entice buyers chasing clean-claim rates. Because comprehensive suites now marry progress notes with intake questionnaires and billing edits, cross-sell uplift remains strong across the behavioral and mental health software market.

Inline analytics and AI triage heighten clinical value further. NeuroFlow’s risk engines synthesize PHQ-9, vital signs, and social determinants to flag suicidality, letting care teams intervene earlier. Population-health dashboards map depression prevalence by zip code, guiding grant applications. As precision measurement becomes reimbursement-linked, clinical functionality’s share will hold above half of the behavioral and mental health software market size through 2031. Administrative automation meanwhile pulls new dollars from underserved solo practices transitioning away from spreadsheets.

By Solution: Integrated Software Leads, Services Accelerate

Software sustained 63.08% of 2025 spend as health systems standardized on unified tech stacks. Buyers favor single-vendor suites that collapse point solutions and eliminate API maintenance. Still, professional services revenue is trending at an 10.88% CAGR, fueled by workflow redesign demands and regulatory reporting setup. Vendors monetize advisory engagements that map DSM-5 templates to FHIR resources, train staff, and secure cloud configurations.

Mobile apps add stickiness by extending care outside clinic walls. Condition-specific tools push daily CBT nudges, whereas measurement diaries feed directly into clinician dashboards for just-in-time interventions. As customer success teams optimize engagement telemetry, subscription renewals climb, enlarging total contract value. Consequently, blended software-plus-services bundles now dominate RFP scoring, deepening wallet share throughout the behavioral and mental health software industry.

By Deployment Mode: Cloud Prevails but On-Premise Finds Niche

Cloud accounted for 60.74% of 2025 installations, buoyed by elastic compute, auto-scaling, and simplified patching. Seventy percent of provider IT leaders already run at least one mission-critical workload in the cloud, and 94% would recommend migration to peers. Oracle’s Autonomous Shield eases hospital lift-and-shifts, giving over 1,000 EHR clients active breach-analytics and continuous compliance hardening .

Yet on-premise grows 11.05% annually where data-sovereignty or Part 2 concerns trump cloud benefits. Substance-abuse centers often prefer local vaults with air-gapped backups. Hybrid offerings emerge-compute stays local while analytics run in hardened clouds-providing regulatory compromise. This bifurcation means vendors must maintain dual deployment road-maps, sustaining choice within the behavioral and mental health software market.

By End-User: Hospitals Hold Lead, Private Practices Surge

Hospitals retained 42.71% of spend in 2025 thanks to enterprise EHR refresh cycles and psychiatric-unit rollouts. They prize robust inter-departmental interoperability and enterprise analytics. Conversely, private practices-often 5-clinician groups-show the sharpest 11.06% CAGR. Subscription plans under USD 200 per clinician and turnkey cloud provisioning slash barriers. Grants in the Behavioral Health Information Technology Coordination Act funnel USD 20 million annually toward this strata, catalyzing first-time buyers.

Community clinics also gain from SAMHSA funding, layering telepsychiatry modules atop primary-care EHRs to broaden access. As solutions become template-driven and mobile-friendly, even solo counselors adopt digital note-taking and outcomes dashboards, diffusing technology deeper into the behavioral and mental health software industry.

Geography Analysis

North America commanded 41.86% of 2025 revenue, anchored by federal reimbursement clarity and sustained grant pipelines. CMS’s 2025 Physician Fee Schedule unlocked new care-coordination modifiers that software platforms automate for billing compliance. States tapping enhanced Medicaid match rates deploy crisis-line triage tools and real-time bed registries, embedding software across public networks. Oracle’s 1.2 million-sq-ft Nashville campus signals tech giants’ long-term bet on regional digital-health demand.

Asia-Pacific is the fastest-expanding territory at 11.18% CAGR through 2031. Mental-disorder DALYs surged 57% since 1990, and GDP drag from untreated conditions could top USD 9 trillion in India and China by 2030. Governments respond with mobile-first frameworks; the APEC Digital Hub promotes FHIR-based primary-care integration to spread screening protocols. Eight categories of mental-health mobile apps dominate regional download charts, reflecting linguistic and cultural tailoring needs. COVID-19 accelerated tele-health normalization, yet access inequities persist, requiring offline-capable apps and SMS check-ins for low-bandwidth zones. Vendors that localize UX and partner with telecoms capture share as the behavioral and mental health software market deepens regionally.

Europe exhibits steady but moderate uptake. GDPR mandates privacy-by-design, elevating consent orchestration complexity but also establishing trust among end users. Several national health services fund stepped-care digital therapeutics, spurring vendors to publish peer-reviewed evidence. Multi-language build-outs and stringent CE-marking processes elongate launch timelines, yet once approved, reimbursement clears in bulk, yielding durable revenue. The Middle East and Africa see rising mental-health budgets in Gulf states, whereas South America leverages cloud platforms to leapfrog capital infrastructure gaps. Collectively, geographic diversification cushions currency and policy risk across the behavioral and mental health software market.

Competitive Landscape

The market remains moderately fragmented, though consolidation accelerates. Oracle’s USD 28.3 billion Cerner buy created scale but also integration hurdles that saw some clients pivot to Epic, which added 176 hospitals and 29,399 beds during 2024. Teladoc’s UpLift purchase extends BetterHelp into higher-acuity therapy, reflecting a trend where telehealth majors bolt on specialized behavioral capabilities. NeuroFlow’s acquisition of Owl forged a measurement-based care platform now covering 17 million lives.

AI features differentiate next-generation offerings. Oracle embeds ambient scribe and predictive flagging, while smaller entrants launch chatbot triage that escalates seamlessly into clinician dashboards. Mentaily’s USD 3 million seed round for the LIV assessment bot underscores investor appetite for early-stage diagnostic AI. Vendors also race to solve 42 CFR Part 2 segregation through fine-grained consent engines and patient-controlled data vaults.

White-space innovation focuses on climate-anxiety modules, employer ROI analytics, and culturally adaptive CBT content. Channel partnerships with payers and employers reshape go-to-market economics, favoring vendors that can demonstrate claim cost offsets. Consequently, the behavioral and mental health software market rewards clinically validated, interoperable, and compliance-centric platforms over legacy feature checklists.

Behavioral And Mental Health Software Industry Leaders

-

BestNotes

-

WELLIGENT, INC.

-

Accumedic Computer Systems Inc.

-

Credible a part of Qualifacts Systems, LLC.

-

TELUS Health

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Interoperability and data standardization are enabling vendors to build FHIR-first integrations and consent segmentation across care settings. In February 2026, ONC and SAMHSA selected nine pilot programs under the USD 20 million Behavioral Health Information Technology Initiative to test the USCDI+ Behavioral Health dataset and FHIR Behavioral Health Profiles Implementation Guide through 2026, raising the bar for vendors that need to connect behavioral specialty platforms with general medical records and public health workflows.

Go-to-market expansion is shifting toward payer, employer, and group-purchasing channels that reduce friction for private practices while tightening documentation and compliance requirements. In April 2026, Osmind entered an exclusive partnership with CareNet GPO aimed at independent psychiatry practices, combining purchasing leverage for specialty medications with integrated REMS compliance automation and interventional-focused workflows, signaling demand for platforms that bundle clinical, medication-safety, and administrative value. In March 2026, Pyramid Healthcare expanded its collaboration with Netsmart to deploy myAvatar EHR and the AI-powered Bells documentation suite across a multistate behavioral health and addiction treatment system, reinforcing near-term opportunity for AI documentation and standardized clinical pathways that can scale across multi-site networks. Data partnerships also expand addressable use cases beyond care delivery, as shown by the June 2026 partnership between Behavioral Health Insights and HealthVerity to link behavioral clinical data with broader datasets via privacy-protected exchange for real-world evidence generation.

Recent Industry Developments

- June 2026: Behavioral Health Insights and HealthVerity announce a data linkage partnership to enable privacy-protected exchange of behavioral health data with broader datasets for real-world evidence generation. The collaboration expands addressable use cases beyond care delivery and enhances validation pathways for outcome-focused programs.

- April 2026: Osmind enters an exclusive partnership with CareNet GPO to bundle purchasing leverage for specialty medications with integrated REMS compliance automation and interventional-focused workflows across independent psychiatry practices, signaling demand for platforms that combine clinical, medication-safety, and administrative value.

- March 2026: Pyramid Healthcare expands its collaboration with Netsmart to deploy myAvatar EHR and the AI-powered Bells documentation suite across a multistate behavioral health and addiction treatment system, reinforcing near-term opportunities for AI-assisted documentation and standardized clinical pathways across multi-site networks.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers software and related services used to document, coordinate, and run behavioral and mental health care, including clinical workflows, administrative workflows, and financial workflows across provider settings.

Scope exclusions: Pure general-purpose medical EHR platforms with no behavioral health specific functionality are excluded from this scope.

Segmentation Overview

-

By Function

-

Clinical Functionality

- Electronic Health Records

- Clinical Decision Support

- Care Plans / Population Health

- Other Clinical Functions

-

Administrative Functionality

- Patient Scheduling

- Case Management

- Other Administrative Functions

-

Financial Functionality

- Revenue Cycle Management

- Accounts Payable / General Ledger

- Other Financial Functions

-

Clinical Functionality

-

By Solution

-

Software

- Integrated Suites

- Stand-alone Modules

- Mobile Apps

- Services

-

Software

-

By Deployment Mode

- Cloud-based

- On-premise

-

By End-user

- Community Clinics

- Hospitals

- Private Practices

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary and to build the first set of assumptions that can be checked in interviews. We referenced public health statistics and policy signals (such as the CDC, SAMHSA, CMS, and the WHO) to understand treated populations, provider settings, and the pace of care digitization.

We also reviewed standards and evidence sources, such as ONC interoperability resources, peer-reviewed journals indexed in PubMed, and payer or provider association publications to map typical workflows and the spread of cloud adoption. For commercial context, we used company filings, investor presentations, product literature, and reputable press coverage, and we supplemented with paid subscriptions for company financials and intelligence, news and financials, and patent databases. These materials were used to confirm product direction and integration activity, and to tighten the link between buyer needs and the features covered in the market scope. These desk sources are illustrative, and many other public and paid references were also used to collect data, confirm numbers, and clarify open questions.

Primary Interviews and Surveys

Primary work focused on verifying what is actually purchased and deployed in behavioral health settings, then pressure-testing the pricing and adoption assumptions using practical adoption language from buyers. We spoke with a mix of provider-side users (community clinics, hospitals, and private practices) and solution-side roles (product, sales, implementation, and partnerships). Coverage was balanced across APAC, EMEA, and the Americas so regional reimbursement and care delivery differences were not missed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 12% | APAC: 51% |

| Mid tier: 54% | Functional/Unit leaders: 43% | EMEA: 29% |

| Smaller Players: 15% | Managers: 45% | Americas: 20% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the addressable spend from behavioral health delivery volumes and the software penetration seen across care settings, and then converts that demand pool into revenue using typical subscription and services attach assumptions. In practice, the model is anchored on indicators such as the number of behavioral health providers and facilities, share of visits documented digitally, mix of tele-mental-health usage, reimbursement and funding signals, and the split between cloud and on-premise deployments.

Once the first totals are formed, they are corroborated through selective bottom-up checks, such as sampled vendor pricing per user or per site multiplied by estimated active customers in key countries, and cross-checked against publicly visible revenue disclosures where available. When a bottom-up view is incomplete, gaps are handled using conservative adoption ranges and services attach rates that were validated in interviews, before totals are rebalanced back to the broader demand indicators.

Forecasting uses scenario analysis supported by variable-by-variable expectations gathered from experts, since policy, reimbursement, and provider staffing constraints can shift adoption faster than simple trend lines. Growth rates are then applied by region and setting using the same input drivers, so the forecast stays traceable to observable changes in care delivery and software procurement.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, including provider counts, usage intensity proxies, and the implied revenue per site or per clinician versus what buyers report paying. Outliers are flagged and reworked, and when a variance cannot be explained by scope or unit differences, the assumptions are revisited and the related interview questions are repeated with fresh respondents.

Before sign-off, the model goes through multi-step analyst review, where inputs, conversions, and regional splits are checked for consistency and the math is re-run from scratch to catch avoidable errors. Reports are refreshed annually, and interim updates are made when major regulatory changes, reimbursement moves, or notable shifts in care delivery patterns occur, followed by a final pre-delivery pass so clients receive the latest updated view.

Mordor Intelligence's Behavioral Mental Health Software Market Size Compared With Other Published Estimates

Published market sizes for behavioral and mental health software often do not match because each publisher draws the line differently on what counts as revenue and which care settings are included. Differences also come from how fast pricing is assumed to change, whether services are bundled into the total, and which year is treated as the starting point for the forecast.

The biggest gaps usually show up around adjacent categories and packaging, such as whether broad digital wellness apps are counted, whether implementation and support services are fully included, and how hybrid care delivery (in-person plus tele-mental-health) is translated into software spend. Digital wellness and self-help apps sold directly to consumers sit outside Mordor Intelligence's scope, which keeps the total tied to provider-grade behavioral health workflows and their recurring software and services spend.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.42 B (2025) | |

| Industry Research Publisher A | USD 7.49 B (2025) | This figure appears to use a broader definition that can pull in consumer mental wellness apps and wider digital health tooling, and it also uses a different growth window that can lift the starting-year total. |

| Healthcare Research Publisher B | USD 4.66 B (2025) | This estimate is framed as software plus services for behavioral health care, which can differ from software-only views depending on how implementation, support, and workflow services are allocated across years and regions. |

Taken together, the spread is mainly explained by what is counted as behavioral health specific software versus adjacent wellness tools, plus whether services are treated as a full revenue line item. Using clear inclusions, observable demand indicators, and repeatable cross-checks helps keep the market total consistent year to year, even when adoption and pricing move at different speeds across regions.

Key Questions Answered in the Report

What is the current size of the behavioral and mental health software market?

The behavioral and mental health software market size reached USD 4.87 billion in 2026 and is projected to climb to USD 7.89 billion by 2031.

Which functional segment holds the largest share of spending?

Clinical Functionality commands the largest 54.78% share, driven by core electronic health records, care plans, and decision-support tools.

How fast is the Asia-Pacific market growing?

Asia-Pacific is forecast to expand at an 11.18% CAGR through 2031 as governments scale digital mental-health infrastructure and mobile app adoption.

Why are private practices adopting software more quickly now?

Targeted federal grants, cloud subscription models under USD 200 per clinician, and simplified user interfaces are reducing barriers for small clinics, fueling an 11.06% CAGR in this segment.

What role does artificial intelligence play in new behavioral health platforms?

AI now powers ambient documentation, risk stratification, and chatbot triage, producing documented symptom reductions of 30–50% in controlled trials and cutting clinician paperwork by up to 40%.

Are data-privacy concerns slowing market growth?

Yes, high-profile breaches and stringent regulations like GDPR create adoption hesitancy, subtracting an estimated 1.8 percentage points from the market’s overall CAGR until more robust security frameworks become standard.

Page last updated on: