Virtual Reality In Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.51 Billion |

| Market Size (2031) | USD 20.99 Billion |

| Growth Rate (2026 - 2031) | 26.39% CAGR |

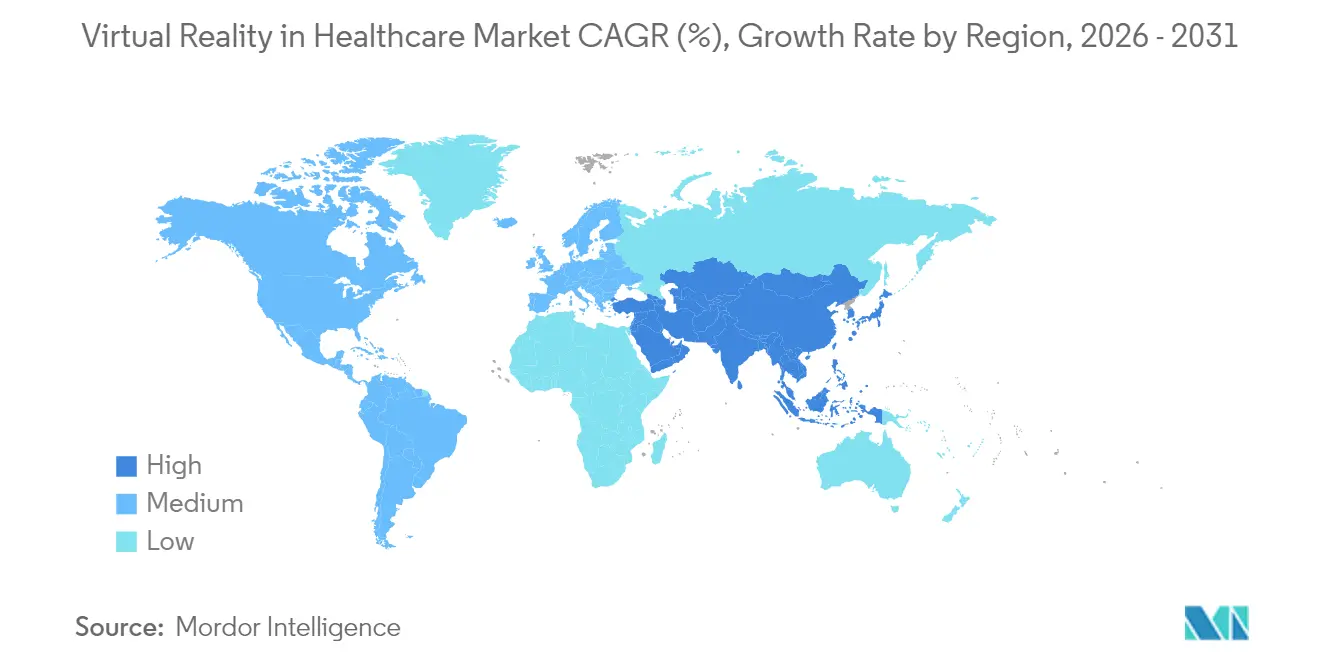

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

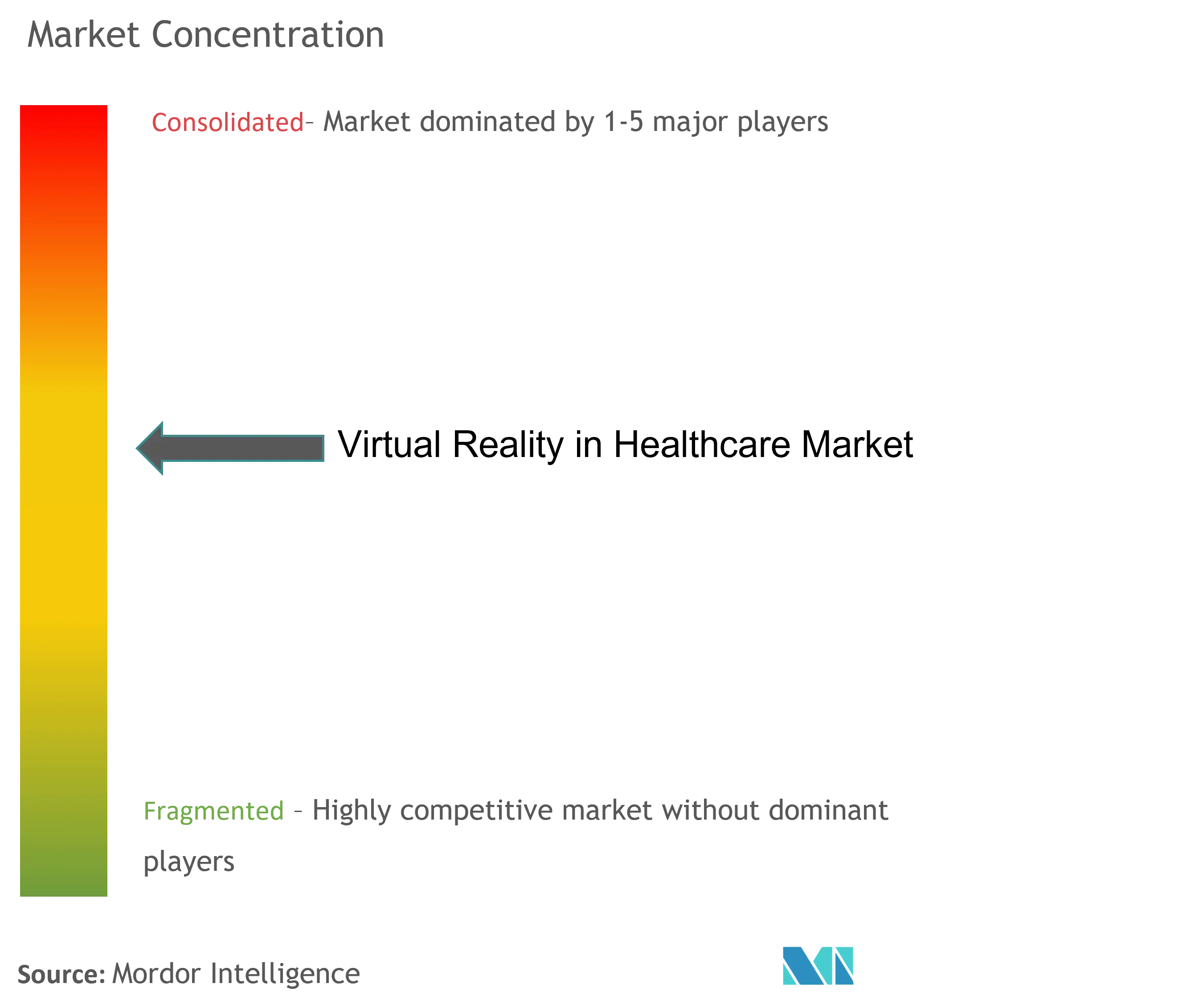

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Virtual Reality In Healthcare Market Analysis by Mordor Intelligence

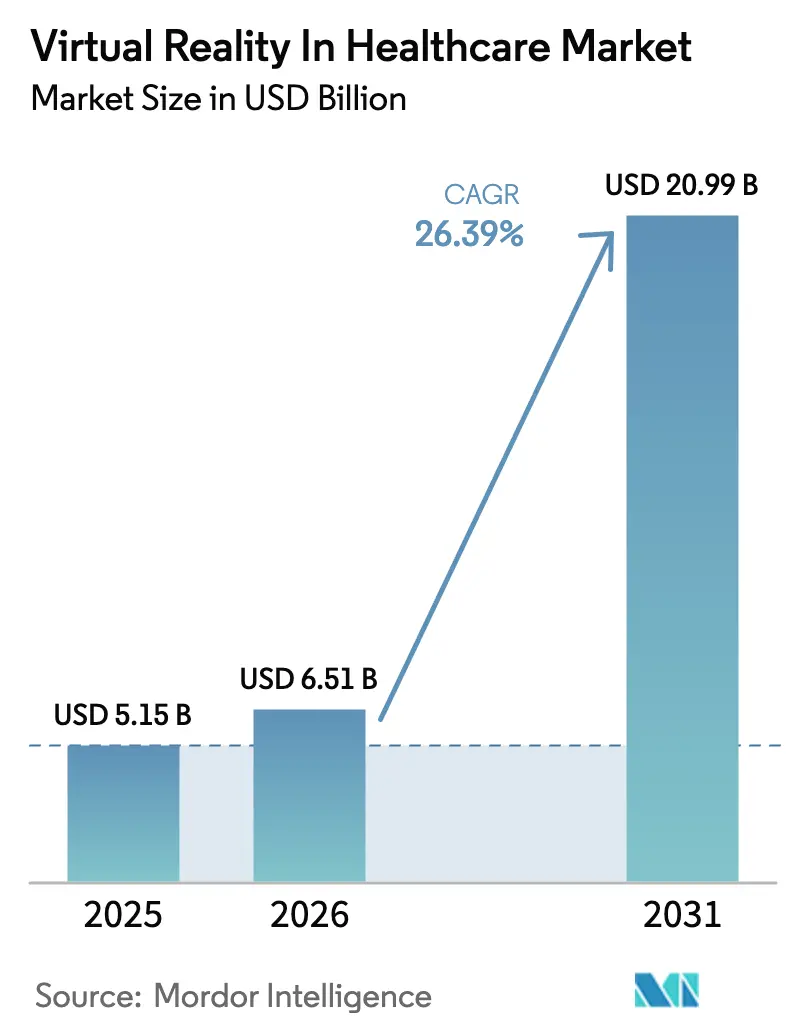

The Virtual Reality in Healthcare market size is expected to grow from USD 5.15 billion in 2025 to USD 6.51 billion in 2026 and is forecast to reach USD 20.99 billion by 2031 at 26.39% CAGR over 2026-2031. Growing institutional confidence, clearer reimbursement pathways, and falling hardware costs are converging to accelerate adoption. Hardware continues to anchor most revenues, yet content-rich software platforms are scaling faster as clinical validation and AI integration expand therapeutic scope. Early reimbursement decisions for FDA-authorized devices are already reshaping purchaser economics, and immersive delivery modes are proving especially effective for pain management, mental health, and rehabilitation. While cybersickness and privacy risks persist, targeted engineering improvements, risk-management frameworks, and stronger data-security standards are steadily mitigating these barriers.

Key Report Takeaways

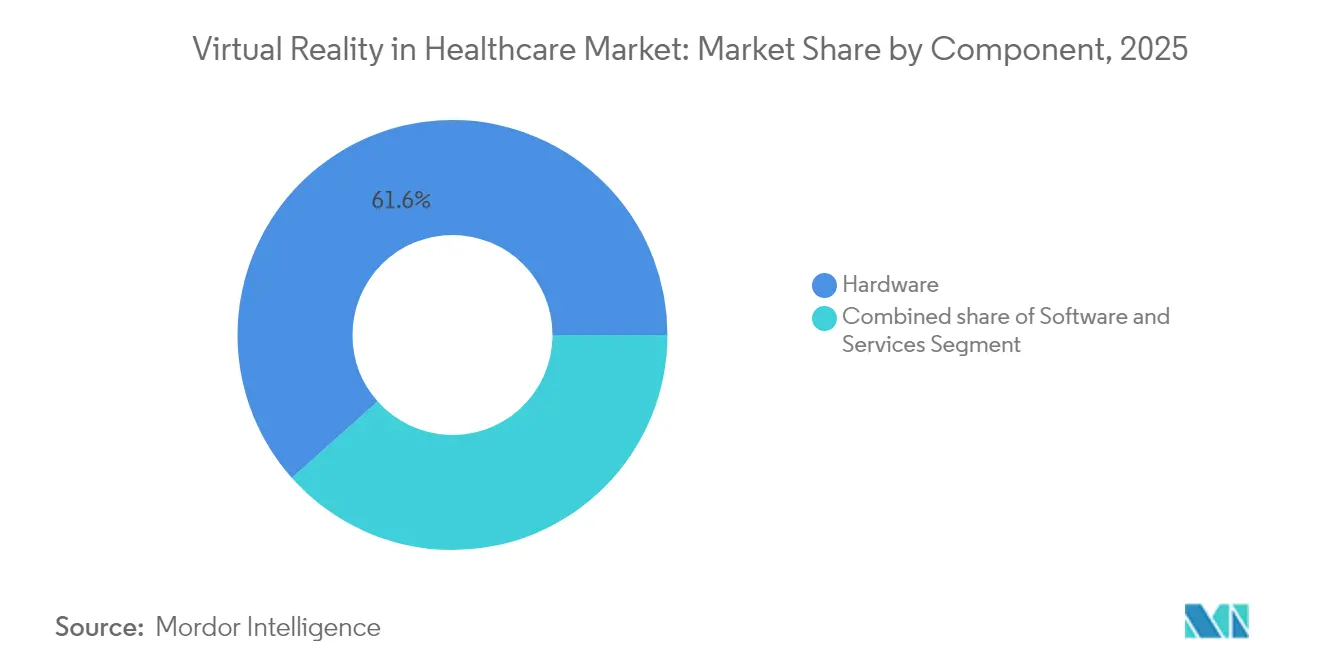

- By component, hardware held 61.58% of the Virtual Reality in Healthcare market share in 2025, while software is advancing at a 28.48% CAGR through 2031.

- By application, surgery simulation and training led with 32.10% revenue share in 2025; rehabilitation and physical therapy is forecast to expand at a 28.96% CAGR to 2031.

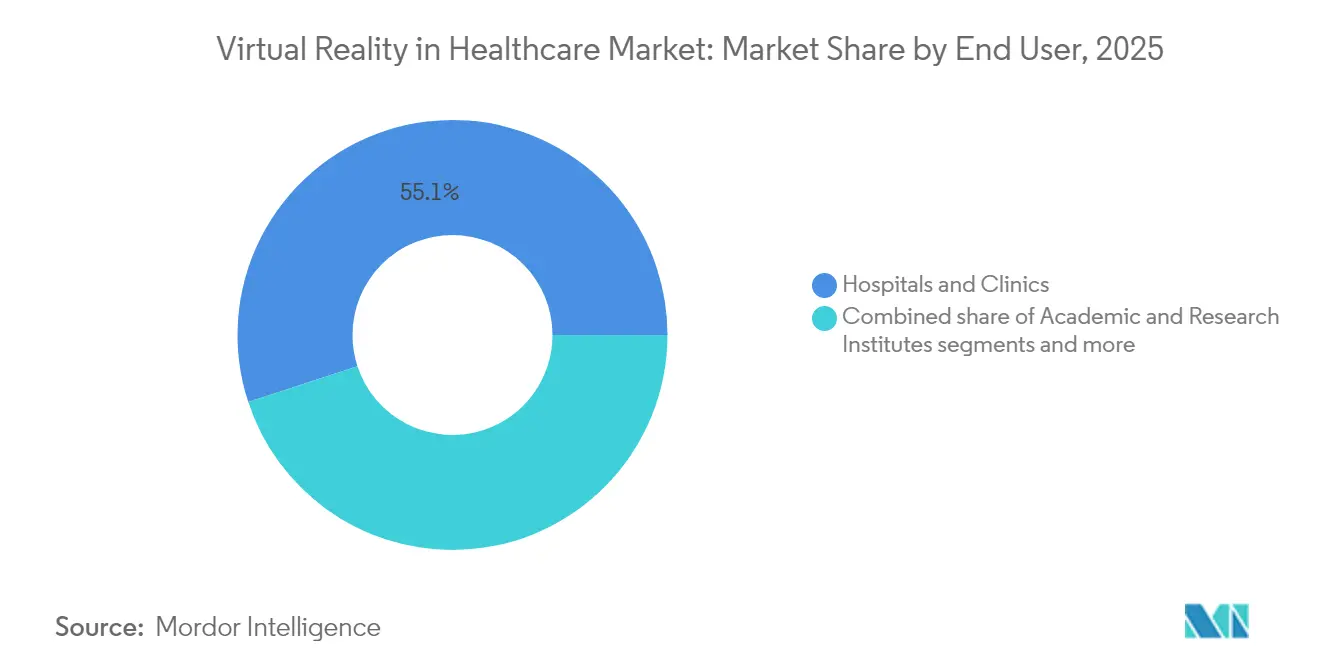

- By end user, hospitals and clinics commanded 55.05% of the Virtual Reality in Healthcare market size in 2025, and rehabilitation centers record the fastest projected CAGR at 29.35% through 2031.

- By delivery mode, immersive VR captured 68.10% share of the Virtual Reality in Healthcare market in 2025 and is growing at a 29.70% CAGR toward 2031.

- By geography, North America dominated with 42.85% share in 2025, while Asia-Pacific is poised for the highest CAGR at 30.05% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Virtual Reality In Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of VR for surgical training & simulation | +6.8% | Global, with early adoption in North America & Europe | Medium term (2-4 years) |

| Growing demand for pain management & mental-health therapies | +7.2% | Global, particularly strong in North America | Short term (≤ 2 years) |

| Technology cost reductions and improved hardware | +5.4% | Global, with manufacturing benefits in APAC | Long term (≥ 4 years) |

| Expansion of telemedicine integrating VR | +4.1% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Government reimbursement pilots for VR digital therapeutics | +5.9% | North America & EU, with CMS leading adoption | Short term (≤ 2 years) |

| Spatial-AI analytics enabling outcome-based rehabilitation | +3.8% | Global, with advanced healthcare systems leading | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of VR for Surgical Training & Simulation

Surgical education is shifting from observation to experiential skill building. Randomized trials in 2024 confirmed that virtual procedures improved accuracy and shortened learning curves at leading U.S. teaching hospitals. Several surgical teams successfully deployed Apple Vision Pro headsets during live cases, proving intraoperative viability and sparking demand for device-agnostic, sterile-field-ready apps. Platform vendors now bundle haptic controllers and AI-guided assessment dashboards that score performance and feed data into credentialing systems. Pharmaceutical firms are joining the ecosystem by commissioning custom extended-reality modules that teach drug administration protocols alongside operative steps. Hospital networks that form “spatial computing centers of excellence” report faster staff onboarding and lower per-resident training costs, underscoring a business case that is forcing laggard institutions to reassess investment priorities[1]Source: U.S. Department of Veterans Affairs, “Immersive Virtual Reality in Health Care Literature Compendium,” va.gov .

Growing Demand for Pain Management & Mental-Health Therapies

A sharp policy pivot toward non-pharmacological pain relief, driven by the opioid crisis, has lifted virtual analgesia into mainstream care. FDA-authorized systems such as RelieVRx demonstrated durable pain reduction in almost 70% of patients 18 months after therapy, prompting the Centers for Medicare & Medicaid Services to activate three HCPCS codes that reimburse digital mental-health devices from January 2025. Academic medical centers now pair VR mindfulness modules with biofeedback sensors, and early real-world evidence indicates improved adherence compared with mobile-app counterparts. AI-powered therapy companions analyze gaze, voice, and physiologic data to adjust scene intensity in real time, broadening access for diverse socioeconomic groups and minimizing clinician workload.

Technology Cost Reductions and Improved Hardware

Component standardization, mass-market optics, and spatial-computing chipsets are compressing headset price points. Hospitals that once paid five-figure sums for specialized rigs now pilot consumer-grade devices for bedside education and remote consultations. Research shows smartphone-based VR kits deliver comparable pain-reduction scores to premium systems in low-acuity settings, offering budget-constrained facilities a workable entry path. Advances in lens design and motion-prediction algorithms are cutting cybersickness incidence, while modular hygiene sleeves and rapid-wipe materials simplify infection control. Haptic gloves with micro-pneumatic feedback are reaching FDA-listed status, opening new therapeutic modalities for fine-motor rehabilitation.

Expansion of Telemedicine Integrating VR

Immersive tele-presence is extending specialist expertise to rural patients without expensive brick-and-mortar expansion. Large U.S. health systems report that virtual nursing pilots reduce average discharge times by 15% and lift patient-satisfaction scores. Tele-rehabilitation suites combine motion-capture analytics with remote physical-therapist oversight, letting stroke survivors complete gamified exercise regimens at home. Regulatory bodies now treat many VR sessions as parity equivalents to in-person visits, provided data flow remains HIPAA-compliant. As 35% of global telehealth platforms embed AI decision support, demand for add-on VR modules that visualize anatomy or simulate exposure therapy is accelerating[2]Source: HealthManagement.org, “The Future of Telehealth,” healthmanagement.org .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront hardware & integration costs | -3.2% | Global, particularly impacting smaller healthcare facilities | Short term (≤ 2 years) |

| Data-privacy & cybersecurity concerns | -2.8% | Global, with stricter regulations in EU and North America | Medium term (2-4 years) |

| Clinician cyber-sickness & ergonomic fatigue | -2.1% | Global, affecting healthcare worker adoption | Short term (≤ 2 years) |

| Fragmented device-certification pathways | -1.9% | Global, with varying regulatory frameworks by region | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Hardware & Integration Costs

Smaller providers struggle to fund capital purchases, staff training, and EHR integration simultaneously. Although baseline headset prices are falling, medical-grade add-ons such as sterilizable face cushions, 3D tracking cameras, and FDA-cleared haptic controllers keep bills elevated. Software licensing typically follows annual per-seat models that can rival the hardware cost within three years. Many administrators still lack clear return-on-investment templates, especially for non-reimbursed use cases like staff wellness or patient distraction during phlebotomy. Grants and pilot subsidies help, but sustained scaling often hinges on value-based contracts that share savings from reduced readmissions or opioid prescriptions.

Data-Privacy & Cybersecurity Concerns

Immersive systems capture biometric telemetry, gaze vectors, and contextual audio, adding new dimensions to protected health information. Regulators require granular consent and strong encryption, yet many off-the-shelf apps default to consumer-grade data handling. Recent threat assessments highlight risks of man-in-the-room attacks where unauthorized avatars impersonate clinicians during remote sessions. Hospitals are responding with zero-trust architectures, air-gapped VR networks, and real-time anomaly detection, but solution complexity raises deployment costs and slows procurement cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Momentum Builds on a Solid Hardware Base

Hardware accounted for 61.58% of 2025 revenue, underscoring its foundational role in the Virtual Reality in Healthcare market. Global headset shipments to hospitals rose sharply after vendors optimized optical stacks for prolonged clinical wear and rolled out plug-and-play sterilization kits. Gesture tracking and force-feedback peripherals are spreading from orthopedics into cardiology and endoscopy training programs. The Virtual Reality in Healthcare market size for software, while smaller today, is compounding at 28.48% annually as hospitals pivot to content subscriptions, AI-driven progress dashboards, and cloud-rendered multi-user scenarios. Regulatory-grade software development kits now ship with pre-filled documentation templates that speed FDA submissions, shortening time-to-revenue for independent developers.

Service revenues lag the two core segments yet remain vital. Health systems increasingly outsource design of VR skills-labs, endpoint provisioning, and cross-platform content curation. Consultants bundle change-management workshops that teach clinicians how to embed VR protocols in existing care pathways, strengthening long-term customer lock-in and boosting recurring revenues as software refresh cycles accelerate.

By Application: Rehabilitation Accelerates Past Training Growth Rates

Surgery simulation retained 32.10% share in 2025, with deployments in orthopedics, neurosurgery, and minimally invasive specialties continuing to expand. The Department of Veterans Affairs highlighted strong evidence for VR rehearsal boosting procedural confidence in novice surgeons. Meanwhile, rehabilitation and physical therapy captured payer attention after studies showed 20% faster gait-speed recovery for stroke survivors who engaged in immersive balance tasks. The Virtual Reality in Healthcare market size tied to rehabilitation is therefore scaling swiftly in absolute dollars despite its smaller base. FDA-authorized pain treatment modules further blur boundaries between rehab and chronic-pain care.

Medical education apps are diversifying into nursing, pharmacy, and emergency medicine, signaling broader curricular adoption. Patient-care-management tools, including exposure therapy and perioperative anxiety reduction modules, are winning grants aimed at lowering sedative use. Application developers who combine evidence generation with robust analytics dashboards gain an edge, because hospitals must demonstrate measurable functional gains to secure ongoing reimbursement.

By End User: Rehabilitation Centers Close the Gap

Hospitals and clinics still generate 55.05% of market revenue, reflecting their multi-modality focus on training, therapy, and patient education. Yet dedicated rehabilitation centers are posting a 29.35% CAGR as immersive platforms prove especially effective for neuro and ortho recovery. Home-based programs supplied by rehabilitation providers further expand the addressable pool of patients.

Academic and research institutes remain key influencers, leveraging grant funding to validate new protocols and publish outcome data that underpins reimbursement bids. Diagnostic centers are experimenting with VR to ease patient anxiety during procedures such as MRI or colonoscopy, reporting improved throughput and reduced need for sedatives. The Virtual Reality in Healthcare market share from these smaller segments is modest but strategically important, because positive patient experience scores help persuade insurers to authorize broader rollouts.

By Delivery Mode: Immersive VR Sets the Pace

Immersive systems delivered 68.10% of 2025 revenue and will sustain a 29.70% CAGR through 2031. Clinical trials consistently show that full sensory immersion boosts pain-distraction efficacy and movement learning by creating presence and focus. Semi-immersive setups, often displayed on wrap-around monitors, support group rehabilitation or patient education classes where clinician oversight is essential.

Non-immersive desktop or tablet solutions remain relevant for low-risk instruction but cannot match clinical outcomes demonstrated by head-worn devices. Developers consequently front-load R&D into immersive pipelines, and component suppliers chase higher-resolution micro-OLED panels, lighter counter-balanced frames, and longer battery life.

Geography Analysis

North America controlled 42.85% of 2025 revenue, supported by a proactive FDA that issued a dedicated 21 CFR code for VR behavioral-therapy devices and a Transitional Coverage for Emerging Technologies rule that accelerates Medicare payments. Large integrated-delivery networks budget for immersive technology labs and continually feed outcome data to payers, reinforcing virtuous adoption cycles. Insurers in the region now review VR claims under durable-medical-equipment criteria, giving providers a clearer cost-recovery path.

Europe follows with steady uptake driven by public-sector pilots and cross-border research consortia. Compliance with the EU’s General Data Protection Regulation shapes system design, fostering robust security architectures that are becoming global blueprints. Germany’s hospital-funding reforms in 2025 earmarked capital for digital therapeutics, and France’s national health authority published clinical-practice guidelines that recommend VR analgesia for certain chronic-pain cohorts.

Asia-Pacific is the fastest-growing region, posting a 30.05% CAGR. Local electronics supply chains trim headset bills, while government grants encourage rural tele-rehabilitation. Japan’s aging population fuels demand for fall-prevention programs, and Australia’s national insurance scheme has begun reimbursing VR chronic-pain modules for eligible patients. The Virtual Reality in Healthcare market size across APAC is therefore projected to surpass European totals earlier than once anticipated.

South America and the Middle East & Africa are smaller today but gaining momentum. Brazilian private hospitals deploy VR for pediatric oncology distraction, and Gulf states include immersive simulation centers in new medical-city master plans. Partnerships with global OEMs and university research hubs are accelerating technology transfer, bypassing legacy barriers that once slowed digital-health adoption.

Competitive Landscape

The Virtual Reality in Healthcare market remains moderately fragmented, with no single firm exceeding a one-quarter share. AppliedVR set a regulatory benchmark by obtaining FDA authorization for RelieVRx and then secured the first commercial-payer coverage with Highmark, catalyzing confidence among hospital buyers. Technology majors such as Apple and Meta supply high-volume headsets but rely on healthcare specialists for clinical content and regulatory dossiers. Osso VR, XRHealth, and Fundamental Surgery differentiate through evidence-backed libraries and cloud analytics that track performance at scale.

Strategic alliances are prolific. GE Healthcare and MediView co-develop augmented-reality guidance for interventional radiology, while pharmaceutical sponsors underwrite procedure-specific training modules bundled with drug launches. Venture capital continues to flow, focusing on start-ups with strong clinical-trial pipelines and reimbursement strategies. Intellectual-property portfolios increasingly combine device patents with health-economic data packages, an emerging requirement as payers demand proof of cost offsets.

Virtual Reality In Healthcare Industry Leaders

Koninklijke Philips N.V.

Samsung Electronics Co. Ltd.

HTC Corporation

Sony Corporation

Siemens Healthineers

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: XRHealth launched an AI clinician assistant at HIMSS25 to enhance patient instruction and adherence

- March 2025: Endo unveiled a spatial-computing injection simulator on Apple Vision Pro for hands-on drug-administration training

Global Virtual Reality In Healthcare Market Report Scope

As per the scope, virtual reality (VR) is a computer-generated environment with scenes and objects that appear real, making the user feel immersed in their surroundings. Virtual reality in healthcare has proven to be a boon to hospitals and healthcare practitioners. This technology is used to plan, treat, and diagnose people with autism, phobias, depression, and addiction. Many healthcare providers have recognized virtual reality's benefits and begun to incorporate it into operation.

The virtual reality in healthcare market is segmented by component (hardware, software, and services), application (pain management, education and training, surgery, patient care management, rehabilitation and therapy procedures, and others), end user (hospitals and clinics, research organizations and pharma companies, and others), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Hardware | Devices | Head-Mounted Displays |

| Gesture-Tracking Devices | ||

| Projectors & Display Walls | ||

| Other Devices | ||

| Accessories | ||

| Software | ||

| Services |

| Surgery Simulation & Training |

| Pain Management & PTSD |

| Rehabilitation & Physical Therapy |

| Medical Education & Training |

| Patient Care Management |

| Other Applications |

| Hospitals & Clinics |

| Academic & Research Institutes |

| Rehabilitation Centers |

| Diagnostic Centers |

| Other End-Users |

| Immersive VR |

| Semi-Immersive VR |

| Non-Immersive VR |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Component (Value, USD bn) | Hardware | Devices | Head-Mounted Displays |

| Gesture-Tracking Devices | |||

| Projectors & Display Walls | |||

| Other Devices | |||

| Accessories | |||

| Software | |||

| Services | |||

| By Application (Value, USD bn) | Surgery Simulation & Training | ||

| Pain Management & PTSD | |||

| Rehabilitation & Physical Therapy | |||

| Medical Education & Training | |||

| Patient Care Management | |||

| Other Applications | |||

| By End-User (Value, USD bn) | Hospitals & Clinics | ||

| Academic & Research Institutes | |||

| Rehabilitation Centers | |||

| Diagnostic Centers | |||

| Other End-Users | |||

| By Delivery Mode (Value, USD bn) | Immersive VR | ||

| Semi-Immersive VR | |||

| Non-Immersive VR | |||

| By Geography (Value, USD bn) | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

Key Questions Answered in the Report

How large will spending on immersive therapeutic VR become by 2031?

Expenditure is expected to reach USD 20.99 billion, reflecting the projected growth trajectory of the Virtual Reality in Healthcare market.

Which segment is expanding fastest across virtual reality health applications?

Rehabilitation and physical therapy is advancing at a 28.96% CAGR, making it the fastest-growing use case.

Why are insurers beginning to reimburse VR treatments?

FDA authorization and new CMS HCPCS codes have established clinical legitimacy and billing pathways, lowering financial risk for payers.

What is driving Asia-Pacific´s rapid uptake of medical VR?

Regional electronics manufacturing, government funding for digital health, and large aging populations combine to push a 30.05% CAGR.

Which delivery mode shows the best clinical outcomes?

Immersive VR leads in both market share and documented therapeutic efficacy for pain, mental health, and motor-skill rehabilitation.

How are hospitals addressing VR-related data-privacy risks?

Health systems deploy zero-trust networks, dedicated VR subnets, and real-time anomaly detection to protect biometric and behavioral data.

Page last updated on: