Healthcare Data Monetization Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.71 Billion |

| Market Size (2031) | USD 1.35 Billion |

| Growth Rate (2026 - 2031) | 13.87% CAGR |

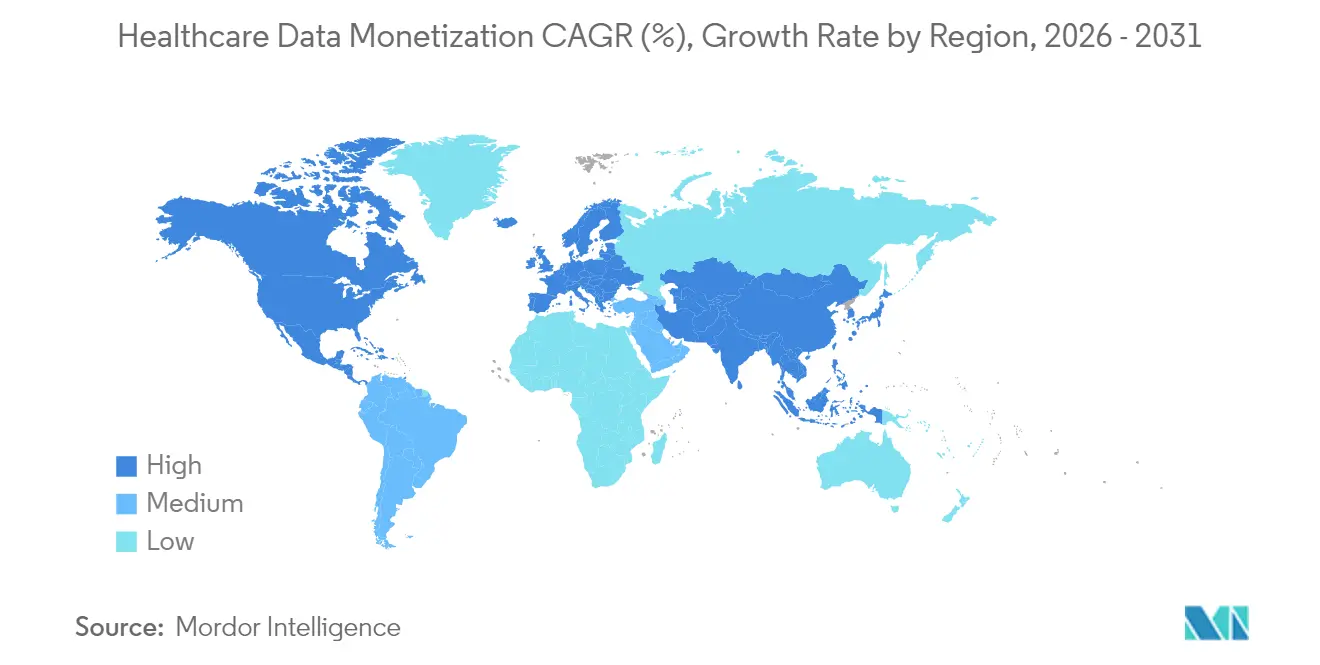

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

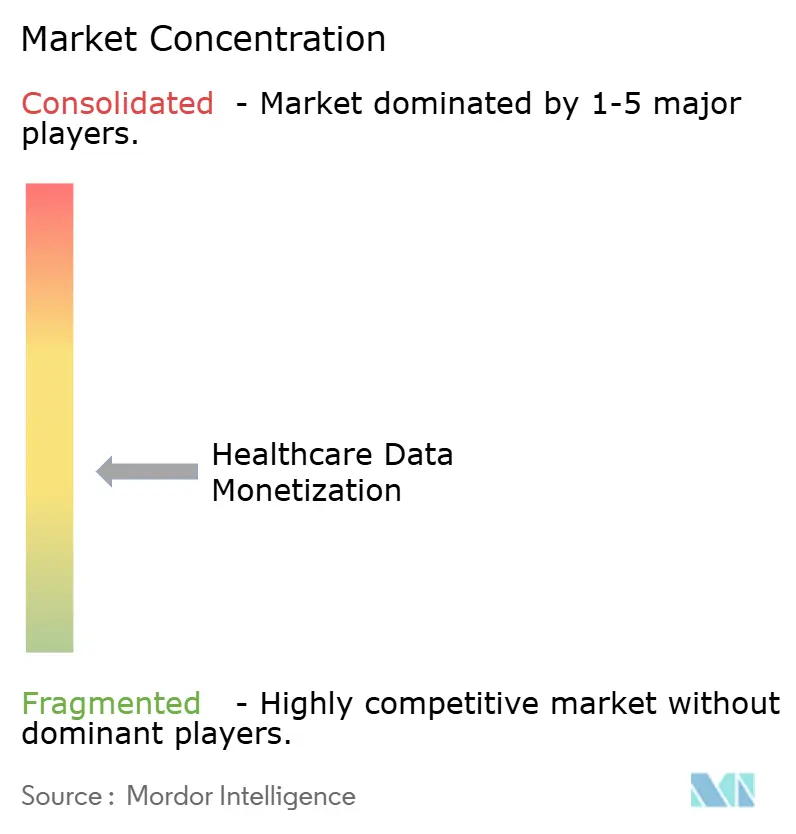

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Data Monetization Market Analysis by Mordor Intelligence

The healthcare data monetization market size is expected to grow from USD 0.62 billion in 2025 to USD 0.71 billion in 2026 and is forecast to reach USD 1.35 billion by 2031 at 13.87% CAGR over 2026-2031. The expansion reflects tighter interoperability rules, maturing analytics platforms, and the global shift toward value-based reimbursement, all of which elevate the economic return on clinical information assets. Growing electronic health record (EHR) penetration, multi-year cloud alliances, and significant genomic acquisitions are broadening the routes through which providers, payers, and life-science firms exploit data. North America sets adoption velocity through Medicare’s mandate that all fee-for-service beneficiaries move into value-based models by 2030, while the European Health Data Space supplies fresh capital and regulatory certainty for cross-border secondary use. Pharmaceutical demand for real-world evidence, combined with federated learning that protects privacy, is pulling new buyers into the healthcare data monetization market. Parallel advances in AI assistants such as Microsoft’s DAX Copilot, now live across 400-plus systems, illustrate how workflow savings translate into monetizable insights.

Key Report Takeaways

- By monetization type, direct data deals led with 50.18% of the healthcare data monetization market share in 2025, while indirect models are projected to expand at an 18.28% CAGR to 2031.

- By deployment, cloud captured 67.55% revenue share in 2025; on-premise is shrinking as cloud grows 14.32% CAGR through 2031.

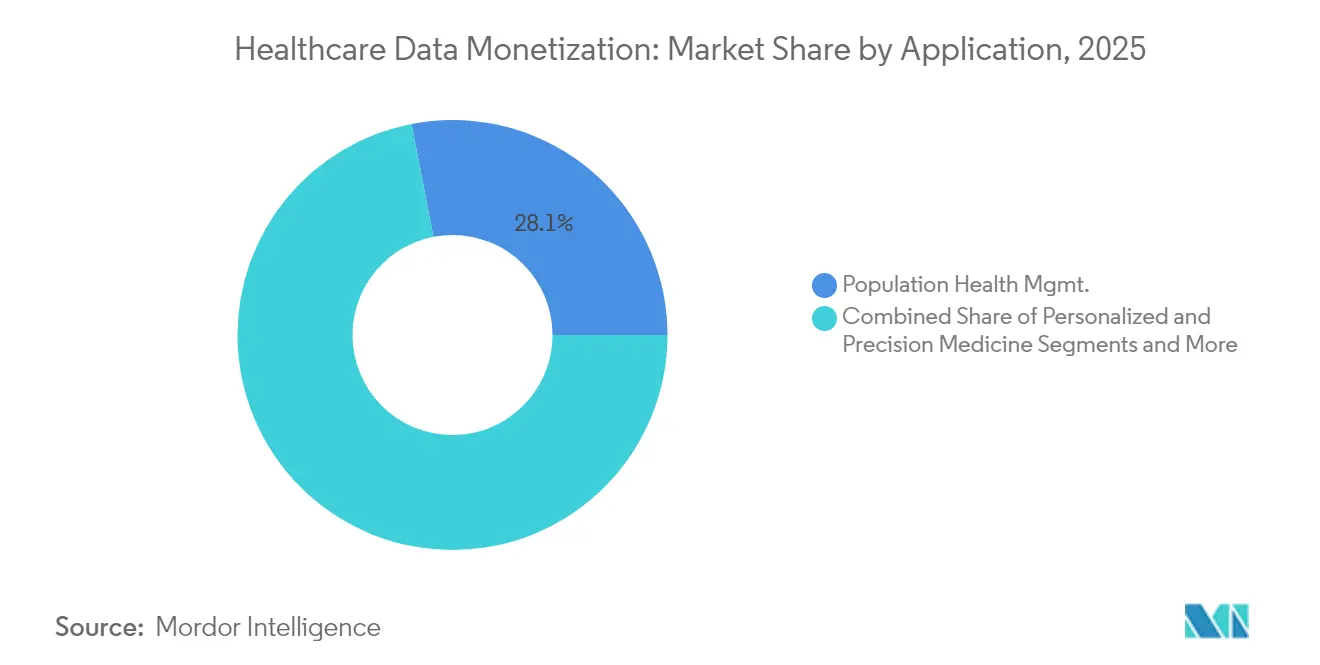

- By application, population health management held 28.05% of the healthcare data monetization market size in 2025, whereas personalized medicine advances at an 18.24% CAGR to 2031.

- By end user, pharmaceutical and biotechnology companies controlled a 34.02% share in 2025, yet digital health platforms recorded the fastest 16.89% CAGR to 2031.

- By pricing, subscription, and licensing models delivered 54.68% of 2025 revenue; revenue-sharing structures log the highest 17.12% CAGR through 2031.

- By geography, North America led with 39.92% revenue share in 2025; Asia-Pacific is projected to post the fastest 17.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Healthcare Data Monetization Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Electronic Health Records (EHRs) | +3.20% | Global, with North America leading | Medium term (2-4 years) |

| Rising Public & Private Investments in Advanced Analytics Platforms | +2.80% | North America & Europe, expanding to APAC | Short term (≤ 2 years) |

| Shift Toward Value-Based Care Reimbursement Models | +2.50% | North America core, spill-over to Europe | Long term (≥ 4 years) |

| Emergence of Federated Learning Frameworks for Cross-Institutional Data Collaboration | +2.10% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Monetization Potential of Multi-Omics Data in Precision Medicine | +1.80% | North America & Europe, selective APAC markets | Long term (≥ 4 years) |

| Expansion of Patient-Mediated Data Marketplaces Enabled by Tokenization | +1.60% | Global, with regulatory variations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Electronic Health Records (EHRs)

Hospitals that raise EHR maturity by one unit lift operating margins 5.34%, which is evidence that digitization directly improves financial performance.[1]Saleh AlGhamdi et al., “EHR Adoption and Hospital Operating Margins,” jmir.org Oracle’s next-generation EHR, launched 2025, embeds AI to merge clinical and claims data, repositioning EHRs from passive stores to revenue engines. Microsoft’s DAX Copilot frees 5 minutes per visit for 400+ providers, quantifying workflow gains that can be sold as aggregated insight. Interoperability rules in the HTI-2 Final Rule standardize exchange pathways, lowering the transaction cost of data licensing. Health systems integrating monetization into the core EHR stack are set to capture outsized value as the healthcare data monetization market matures

Rising Public & Private Investments in Advanced Analytics Platforms

Funding for consumer health tech reached USD 6.3 billion in 2024, up 37% year-on-year, spotlighting investor confidence. The USD 500 billion Stargate program, fronted by Oracle, OpenAI, and SoftBank, earmarks USD 100 billion for cancer-focused AI infrastructure. GE HealthCare joined AWS to convert unstructured imaging into decision support, signaling equipment vendors’ shift toward data-centric revenue. With each analytics upgrade, providers unlock richer datasets, driving fresh demand in the healthcare data monetization market.

Shift Toward Value-Based Care Reimbursement Models

CMS will move every traditional Medicare member into value-based contracts by 2030, opening a USD 500 billion-to-USD 1 trillion incentive pool that hinges on data-verified outcomes. Indiana’s Innovative Healthcare Collaborative cut costs materially once integrated data dashboards pinpointed avoidable admissions. Orthopedic supplier Zimmer Biomet and RevelAi Health struck a revenue-sharing pact that links implant success metrics to joint analytics delivery. These moves confirm that monetization strategies that reward outcome improvements will outpace flat data sales.

Emergence of Federated Learning Frameworks for Cross-Institutional Data Collaboration

Federated models collectively outperform single-site AI while keeping raw records behind the firewall.[2]Marinka Zitnik, “Federated learning in medicine: facilitating multi-institutional collaborations without data exchange,” Nature Digital Medicine, nature.comDatavant and AWS apply clean-room services so collaborators swap model weights, not patient files. Federated Timeline Synthesis scales that logic to time-series EHRs, enabling synthetic trial design without breaching HIPAA.[3]Zachary C. Lipton, “Federated Timeline Synthesis: Generating Privacy-Preserving Longitudinal EHR Data,” arxiv.org As privacy norms tighten, federated learning multiplies the addressable volume for the healthcare data monetization market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Patient Privacy Regulations (HIPAA, GDPR) | -2.40% | Global, with varying enforcement intensity | Short term (≤ 2 years) |

| Lack of Data Standardization & Interoperability | -1.80% | Global, with fragmentation in emerging markets | Medium term (2-4 years) |

| Rising Cyber-Insurance Premiums for Data Breaches Impacting Monetization ROI | -1.20% | North America & Europe primarily | Short term (≤ 2 years) |

| Ethical Concerns Around Secondary Use of AI-Generated Synthetic Health Data | -0.90% | Global, with higher sensitivity in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Patient Privacy Regulations (HIPAA, GDPR)

Two-thirds of US providers are not ready for the the more demanding HIPAA security criteria arriving in 2025. The HTI-3 rule adds new information-blocking exceptions for reproductive care, layering fresh legal checks on data exchange. Europe’s Health Data Space obliges holders to log assets in national catalogues, and non-compliance stalls license workflows. The 23andMe breach that preceded its USD 256 million asset sale to Regeneron demonstrates reputational exposure in genomic datasets. Compliance costs and legal uncertainty temporarily temper growth in the healthcare data monetization market.

Lack of Data Standardization & Interoperability

The HTI-1 rule forces certified IT to disclose 31 attributes behind predictive algorithms, but harmonizing inputs across radiology, genomics, and remote monitoring remains costly. European pilots report gaps in FHIR implementation that slow HealthData@EU roll-out. Without cleaner ontologies, data buyers pay premiums only for curated stores, depressing monetization ratios in fragmented systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Monetization Type: Direct Models Drive Immediate Cash-Flow

Direct transactions accounted for 50.18% of the healthcare data monetization market share in 2025, demonstrating that straightforward licensing continues to pull the most extensive checks from pharmaceutical and technology buyers. The segment’s appeal stems from the clarity of pricing and short payback cycles, especially for providers holding high-fidelity longitudinal datasets. Microsoft’s DAX Copilot yields indirect gains, yet Regeneron’s USD 256 million purchase of 23andMe’s 15 million-record biobank shows investors still reward outright ownership.

Indirect monetization is scaling faster at 18.28% CAGR as organizations embed analytics into clinical workflows that boost outcome-based revenue. These models turn clinical improvements into shared savings, reshaping perceptions of data value. As interoperability rules lower transaction friction, indirect pathways are set to chip away at direct dominance, supporting long-run expansion of the healthcare data monetization market size.

By Deployment: Cloud Infrastructure Takes the Lead

Cloud services captured 67.55% of 2025 revenue, underscoring confidence in hyperscale security frameworks that satisfy HIPAA and GDPR. Multi-year SCA agreements such as Datavant-AWS exemplify how clean-room functions de-risk sharing while delivering elasticity critical for AI model training. On-premise estates persist in regions with data-sovereignty rules but are losing ground as compliance attestation from cloud vendors strengthens.

The healthcare data monetization market size associated with cloud deployments is forecast to widen because federated learning, synthetic data, and multi-omics analytics demand compute bursts unaffordable in traditional data centers. National EU investments into HealthData@EU, backed by EUR 810 million, further accelerate cloud migration across public-sector networks.

By Application: Personalized Medicine Accelerates

Population health management retained 28.05% of 2025 revenue by enabling payers and systems to pinpoint risk clusters and allocate preventive resources. Yet personalized medicine is advancing at 18.24% CAGR as multi-omics integration becomes viable at scale. Sweden’s PROMISE project and the Truveta Genome Program both point to genomic depth becoming a premium monetization lever.

Applications marrying AI with molecular data attract higher price-per-record premiums, lifting the relative contribution of precision-centric datasets to overall healthcare data monetization market size. Drug-discovery, fraud analytics, and marketing intelligence segments follow with steady gains as life-science firms demand post-market surveillance evidence.

By End User: Digital Health Platforms Surge

Pharmaceutical and biotech buyers absorbed 34.02% of 2025 spending because of regulatory reliance on real-world evidence. Digital health platforms, however, are outpaced at 16.89% CAGR by controlling both data origination and consumer engagement. Deals such as NeuroFlow’s integration of Intermountain Health’s behavioral algorithm illustrate how platforms package proprietary risk scores for payer clients.

As consumer apps gather continuous streams, they create longitudinal dossiers prized by research sponsors, pushing the healthcare data monetization market toward patient-mediated licensing and tokenized exchanges that reward individual contributors.

By Pricing Model: Revenue-Sharing Gains Momentum

Subscription and licensing still deliver 54.68% of receipts, preferred for budgeting stability. Revenue-sharing is climbing 17.12% CAGR because it aligns with value-based reimbursement. RevelAi Health and Zimmer Biomet split orthopedic savings as AI tools lower revision surgery rates, a template likely to replicate across service lines. Pay-per-use remains niche, serving ad-hoc academic queries where full licenses are uneconomic, but overall, dynamic pricing frameworks will increase the stickiness of the healthcare data monetization market.

Geography Analysis

North America leads the healthcare data monetization market with the most significant installed EHR base, robust payer incentives, and deep capital pools. Medicare’s compulsory value-based enrollment channels billions into analytics that certify outcome improvement. The USD 500 billion Stargate investment and Oracle’s AI-enabled EHR illustrate unmatched infrastructure build-out. High-profile transactions such as Regeneron-23andMe confirm investor appetite for genetic troves.

Europe is the fastest regulatory mover. The European Health Data Space earmarks EUR 810 million (USD 849 million) to harmonize secondary-use rules, targeting EUR 5.5 billion (USD 6.4 billion) in system savings within a decade. Germany’s Digital Act plus Sweden’s PROMISE raise data liquidity, while Promptly Health’s Datavant alliance seeds commercial clean rooms across Iberia and beyond. Buyers pay premiums for high-quality, interoperable EU datasets, pushing regional healthcare data monetization market share upward.

Asia Pacific posts the highest volume growth as tech giants roll out AI-driven consumer apps. Ant Group’s AQ service links 1 million doctors and 5,000 hospitals, wrapping clinical chat into a monetizable data layer. Indian collaborations such as Apollo-Monash extend research-grade de-identified records to 200 million patients. Southeast Asian digital health revenue nears USD 6.1 billion, setting a foundation for future data licensing.

Middle East & Africa, plus South America, are emergent. Gulf governments bankroll AI hospital pilots, and Latin America’s telehealth uptake produces new longitudinal datasets. While market weight is modest today, improved infrastructure and harmonized privacy codes could unlock latent healthcare data monetization market opportunities.

Competitive Landscape

Competition is moderate—enterprise software majors—Microsoft, Oracle, Salesforce—bundle analytics engines into existing clinical suites. Microsoft’s DAX Copilot proves scale with 400+ deployments, saving minutes per clinical note. Oracle’s 2025 EHR embeds AI natively, targeting nation-scale roll-outs with partners like the UAE’s G42—Salesforce and IQVIA co-develop Life Sciences Cloud, fusing CRM and orchestration data.

Specialists such as Datavant and Truveta serve as connective tissue. Datavant’s AWS clean-room pact underpins privacy-preserving exchange. Truveta’s genome project, funded at USD 119.5 million, shows buyers will finance next-generation datasets. Emerging disruptors build tokenized marketplaces and synthetic data engines, challenging license-only incumbents.

Strategic moves signal consolidation. Regeneron’s 23andMe asset buy, Zimmer Biomet’s AI orthopedic tie-up, and GE HealthCare’s AWS imaging venture illustrate acquisitive and partnership-driven growth. Vendors that combine data quality, compliance automation, and AI toolkits are best positioned to enlarge their healthcare data monetization market share.

Healthcare Data Monetization Industry Leaders

Informatica Inc.

Infosys Limited

Innovaccer, Inc.

Accenture

Microsoft

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Ant Group unveiled AQ, an AI medical consultation app slated for global reach.

- May 2025: Regeneron finalized the USD 256 million purchase of 23andMe’s genetic database.

- May 2025: Oracle Health, Cleveland Clinic, and G42 launched an AI platform for large-scale data analytics.

- February 2025: Promptly Health partnered with Datavant to improve European data accessibility, beginning in Iberia.

Global Healthcare Data Monetization Market Report Scope

As per the scope of the report, healthcare data monetization involves leveraging patient information, medical records, and clinical insights to generate revenue or create value for healthcare organizations. The healthcare data monetization market is segmented into type, deployment, end-user, and geography. By type, the market is segmented into direct data monetization and indirect data monetization. By deployment, the market is segmented into on-premise and cloud. By end user, the market is segmented into pharmaceutical and biotechnology companies, pharmaceutical and biotechnology companies, healthcare providers, healthcare payers, and medical technologies companies. By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World. The report also covers the market size and forecasts for the wooden decking market in 11 countries across major regions. The report offers the value (USD) for the above segments.

| Direct Data Monetization |

| Indirect Data Monetization |

| On-Premise |

| Cloud |

| Population Health Management |

| Drug Discovery & Development |

| Real-World Evidence / Outcomes Research |

| Personalized & Precision Medicine |

| Risk Modeling & Fraud Analytics for Payers |

| Marketing & Commercial Intelligence |

| Pharmaceutical & Biotechnology Companies |

| Healthcare Providers |

| Healthcare Payers |

| Medical Technology Companies |

| Academic & Research Institutes |

| Digital Health Platforms |

| Subscription / Licensing |

| Revenue-Sharing Partnerships |

| Pay-Per-Use / On-Demand |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Direct Data Monetization | |

| Indirect Data Monetization | ||

| By Deployment | On-Premise | |

| Cloud | ||

| By Application | Population Health Management | |

| Drug Discovery & Development | ||

| Real-World Evidence / Outcomes Research | ||

| Personalized & Precision Medicine | ||

| Risk Modeling & Fraud Analytics for Payers | ||

| Marketing & Commercial Intelligence | ||

| By End User | Pharmaceutical & Biotechnology Companies | |

| Healthcare Providers | ||

| Healthcare Payers | ||

| Medical Technology Companies | ||

| Academic & Research Institutes | ||

| Digital Health Platforms | ||

| By Pricing Model | Subscription / Licensing | |

| Revenue-Sharing Partnerships | ||

| Pay-Per-Use / On-Demand | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Healthcare Data Monetization Market?

The Healthcare Data Monetization Market size is expected to reach USD 0.71 billion in 2026 and grow at a CAGR of 13.87% to reach USD 1.35 billion by 2031.

What is the current Healthcare Data Monetization Market size?

In 2026, the Healthcare Data Monetization Market size is expected to reach USD 0.71 billion.

Who are the key players in Healthcare Data Monetization Market?

Informatica Inc., Infosys Limited, Innovaccer, Inc., Accenture and Microsoft are the major companies operating in the Healthcare Data Monetization Market.

Which is the fastest growing region in Healthcare Data Monetization Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Healthcare Data Monetization Market?

In 2025, the North America accounts for the largest market share in Healthcare Data Monetization Market.

What years does this Healthcare Data Monetization Market cover, and what was the market size in 2025?

In 2025, the Healthcare Data Monetization Market size was estimated at USD 0.71 billion. The report covers the Healthcare Data Monetization Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Healthcare Data Monetization Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: