Physiotherapy Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 23.89 Billion |

| Market Size (2031) | USD 33.26 Billion |

| Growth Rate (2026 - 2031) | 6.85% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

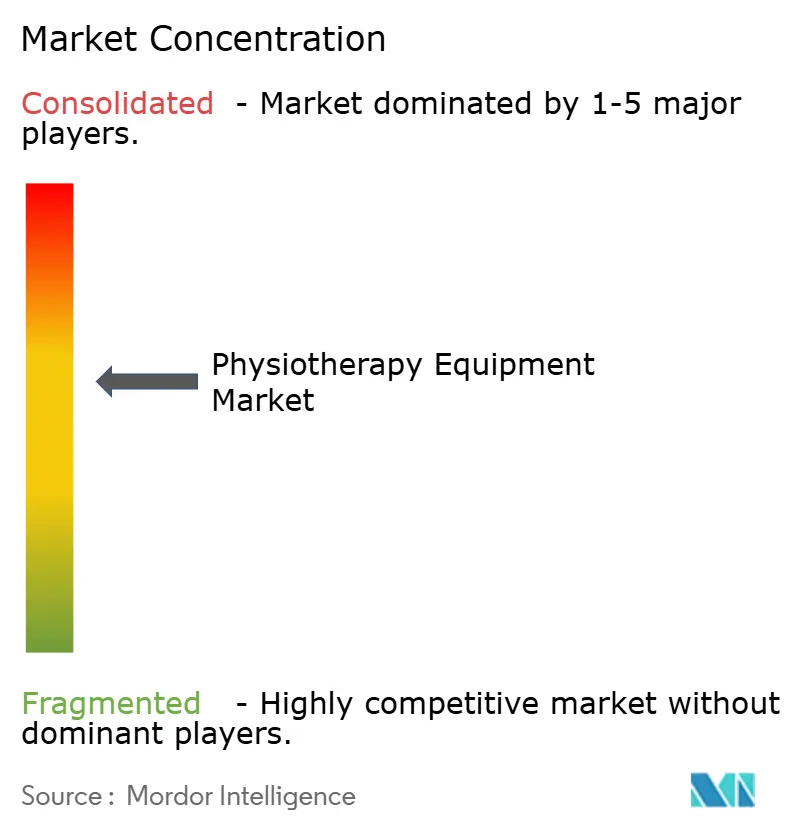

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Physiotherapy Equipment Market Analysis by Mordor Intelligence

The Physiotherapy Equipment Market size is expected to grow from USD 22.37 billion in 2025 to USD 23.89 billion in 2026 and is forecast to reach USD 33.26 billion by 2031 at 6.85% CAGR over 2026-2031.

The solid outlook stems from health-system budgets pivoting toward prevention and functional recovery, an aging population that is driving rehabilitation demand, and widening insurance coverage for connected devices. The World Health Organization reports that 2.41 billion people require rehabilitation yet fewer than half receive it, highlighting a persistent access gap that fuels the physiotherapy equipment market. A growing preference for home-based care, rising sports participation, and broader reimbursement for AI-enabled tele-rehabilitation are increasing the installed base of portable and connected systems. Competitive pressure is intensifying as low-cost Asian suppliers challenge Western incumbents, while robotics and SaaS platforms are opening new profit pools. Together, these forces underpin robust demand across hospitals, rehabilitation centers, and home-care channels.

Key Report Takeaways

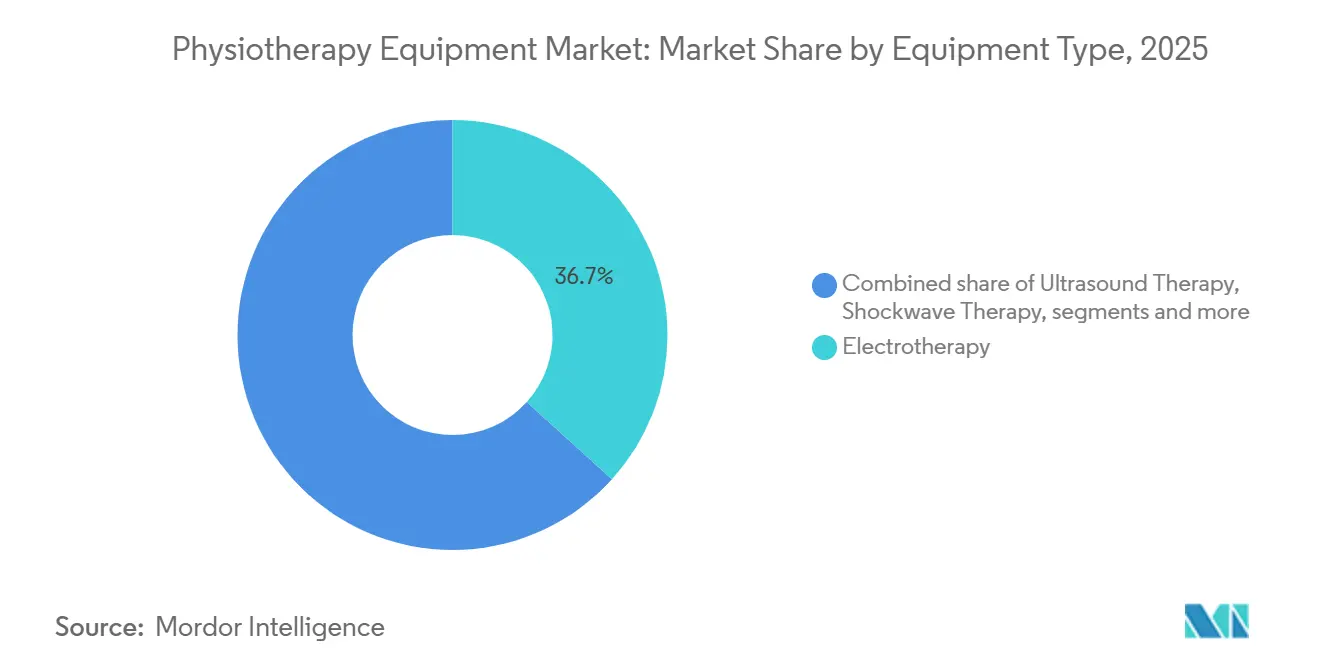

- By equipment type, electrotherapy commanded 36.7% of the physiotherapy equipment market share in 2025, while wearable and assistive rehabilitation devices are forecast to expand at a 7.12% CAGR through 2031.

- By application, musculoskeletal conditions accounted for 51.6% of the physiotherapy equipment market size in 2025, and sports & orthopedic injuries are projected to post a 7.45% CAGR to 2031.

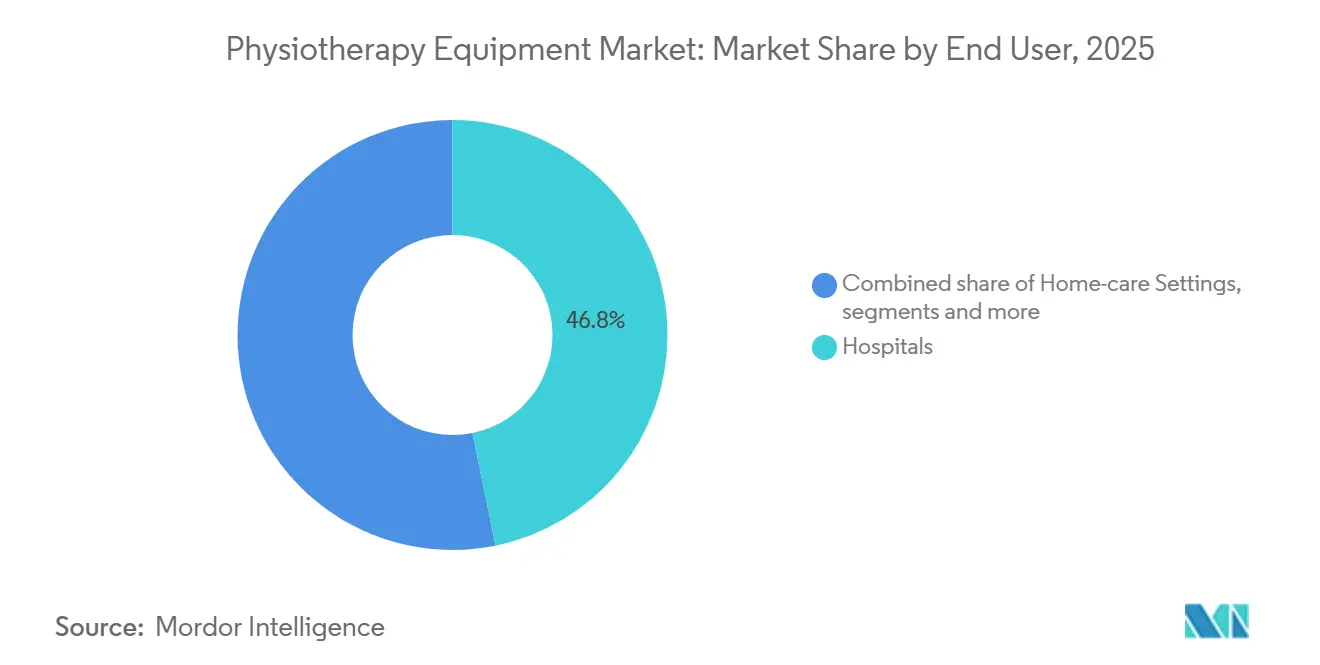

- By end user, hospitals held 46.8% revenue share in 2025; rehabilitation centers are advancing at a 6.98% CAGR through 2031.

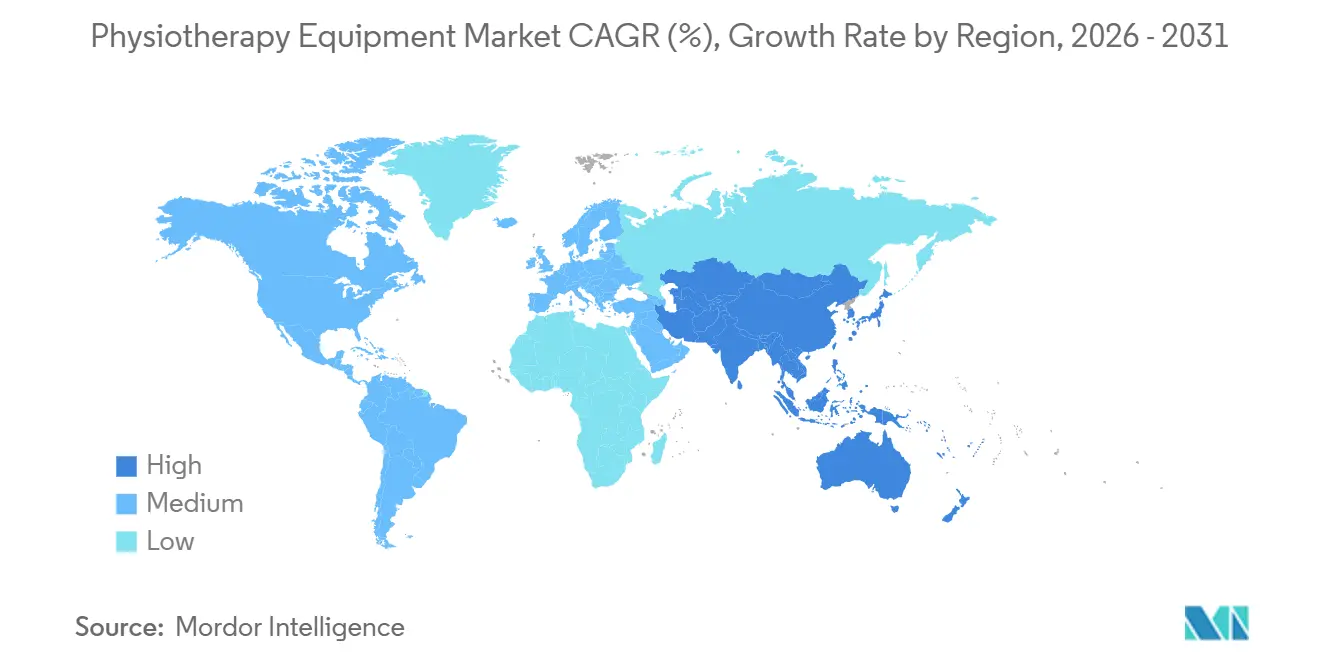

- By geography, North America led with 39.4% of revenue in 2025, whereas Asia-Pacific is set to grow at 7.62% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Physiotherapy Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising geriatric population & chronic disease burden | +1.2% | Global, notably Asia-Pacific and Europe | Long term (≥ 4 years) |

| Rapid adoption of connected & portable physiotherapy devices | +1.1% | North America, Europe, accelerating in Asia-Pacific | Medium term (2-4 years) |

| AI-driven tele-rehabilitation platforms gaining reimbursement | +1.3% | United States, Germany, Netherlands | Short term (≤ 2 years) |

| Exoskeleton & robotics integration in physiotherapy suites | +0.9% | Japan, South Korea, United States | Medium term (2-4 years) |

| Expanding post-surgical & oncology rehabilitation demand | +0.6% | North America, Europe | Medium term (2-4 years) |

| Growing investments in outpatient & sports medicine facilities | +0.4% | North America, Western Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Geriatric Population & Chronic Disease Burden

According to the World Health Organization, the proportion of the geriatric population is expected to nearly double from 12% to 22% of the global population[1]World Health Organization "Ageing and health" who.int. Older demographics experience higher rates of osteoarthritis, stroke, and chronic pain, pushing demand for automated gait trainers, electrotherapy units, and balance systems. WHO’s Rehabilitation 2030 agenda highlights a 40% therapist shortfall in lower-income regions, prompting suppliers to build devices that lower clinician-to-patient ratios [2]World Health Organization, “Rehabilitation,” who.int. As chronic disease prevalence rises, the physiotherapy equipment market is positioned for sustained volume growth.

Rapid Adoption of Connected & Portable Physiotherapy Devices

Payers are encouraging home-based care to reduce inpatient costs, and portable electrotherapy units priced at USD 300-500 are reshaping purchasing patterns. Medicare removed prior authorization for physician-prescribed DME in 2024, helping Zynex Medical shift the majority of revenue to direct-to-consumer channels. Embedded inertial measurement sensors stream compliance data that insurers use to validate therapy adherence. New FDA cybersecurity guidance obliges suppliers to disclose software bills of materials, raising technical barriers but standardizing data protocols. Collectively, these dynamics are enlarging the connected-device share of the physiotherapy equipment market.

AI-Driven Tele-Rehabilitation Platforms Gaining Reimbursement

Remote Therapeutic Monitoring (RTM) codes launched by CMS in 2024 permit clinicians to bill USD 200-300 per patient per month for asynchronous data review, establishing a USD 1.2 billion reimbursement pool. AI algorithms that analyze smartphone-captured gait parameters now alert therapists to re-injury risks, cutting readmissions significantly among orthopedic cases. Germany’s Digital Health Applications pathway forces suppliers to prove clinical equivalence to in-person therapy, opening doors for SaaS platforms with rigorous evidence bases. Hardware-only manufacturers risk commoditization, while integrated software ecosystems gain recurring margins.

Exoskeleton & Robotics Integration in Physiotherapy Suites

Costs of robotic gait trainers historically limited uptake, but new insurance mechanisms are unlocking demand. A 2024 meta-analysis reported 30% faster time-to-independent walking for stroke patients using robotic assistance. South Korea declared rehabilitation robotics a strategic industry and earmarked USD 400 million in subsidies, incentivizing joint ventures between electronics giants and med-tech specialists. Robotics is progressing from niche to mainstream within the physiotherapy equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of skilled physiotherapists worldwide | -1.0% | Sub-Saharan Africa, South Asia, rural North America | Long term (≥ 4 years) |

| High upfront cost of advanced electro-mechanical systems | -0.8% | India, Southeast Asia, Latin America | Medium term (2-4 years) |

| Unfavorable or patchy reimbursement in developing markets | -0.5% | Sub-Saharan Africa, South Asia, parts of Latin America | Long term (≥ 4 years) |

| Cyber-security & data-compliance risk in connected devices | -0.3% | North America, EU, select Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Physiotherapists Worldwide

Low-income nations average only 0.1 therapists per 10,000 people versus 15-20 in Scandinavia, creating a 50-fold disparity. India's mental health professional-to-population ratio is critically low, with only about 0.7 mental health professionals per 100,000 people, well below the recommended three per 100,000. Equipment utilization suffers when staffing is inadequate, limiting the physiotherapy equipment market in high-need regions. Manufacturers are adding automated feedback and multi-patient stations, yet professional bodies caution against diluting individualized care.

Unfavorable or Patchy Reimbursement in Developing Markets

In Latin America and Africa, few public insurers reimburse outpatient physiotherapy, forcing patients to self-pay. Clinics then hesitate to invest in premium hardware, focusing instead on low-cost modalities. This reimbursement patchwork keeps the physiotherapy equipment market under-penetrated outside high-income geographies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Electrotherapy Dominance Faces Wearable Disruption

Electrotherapy accounted for a 36.7% physiotherapy equipment market share in 2025, buoyed by decades of evidence for pain control and neuromuscular re-education [3]National Institutes of Health, “Electrotherapy for Pain Management,” nih.gov. Ultrasound and laser modalities added close to 20% combined share as sports clinics adopted tissue-healing technologies. Despite entrenched demand, the physiotherapy equipment market size for electrotherapy is moderating, while the wearable sub-segment is accelerating.

Wearable and assistive devices are projected to grow at a 7.12% annual rate through 2031. The costs of inertial sensors have dropped below USD 5, allowing for 6-axis motion tracking in braces and straps that retail at consumer-friendly price points. These devices collect adherence data that feed payer dashboards, a capability traditional clinic-bound systems lack. Multi-exercise stations are losing ground in home settings, whereas hydrotherapy remains confined to hospitals where space and maintenance budgets are available.

By Application: Musculoskeletal Volume, Sports Injury Momentum

Musculoskeletal conditions represented 51.6% of the physiotherapy equipment market size in 2025, reflecting the pervasive burden of low back pain and osteoarthritis. Robotics adoption is highest in neurology, but volume still trails musculoskeletal demand. Cardiopulmonary rehabilitation claims a stable 10-12% slice, sustained by post-COVID-19 programs.

Sports and orthopedic injuries are forecast to deliver the fastest expansion at 7.45% CAGR. Leagues and amateur athletes alike view technology as a performance differentiator, spurring procurement of force-plate platforms and anti-gravity treadmills. Pediatric and women’s health segments remain niche yet present upside as clinical evidence strengthens and reimbursement frameworks evolve.

By End User: Hospitals Hold, Rehabilitation Centers Rise

Hospitals contributed 46.8% revenue in 2025, maintaining the largest footprint due to high-acuity caseloads. Procurement committees favor multi-modal systems to maximize usage across departments. The physiotherapy equipment market share of rehabilitation centers is, however, rising rapidly as insurers steer patients toward lower-cost outpatient pathways.

Home-care settings promise the highest margins. Direct-to-consumer channels sidestep group-purchasing discounts, and patients value convenience. Ambulatory surgical centers and sports medicine facilities demand smaller form-factor equipment that supports same-day discharge and fast return-to-play targets, respectively.

Geography Analysis

North America generated 39.4% of 2025 revenue, supported by Medicare coverage of tele-rehabilitation and a vast outpatient clinic network. The physiotherapy equipment market size in the United States benefits from new RTM codes that reward connected devices. Canada’s private clinics charge USD 60-90 per session, prompting investments in wearables to enhance service differentiation.

Asia-Pacific is the fastest-growing region at a 7.62% CAGR, propelled by China’s Healthy China 2030 mandate requiring rehabilitation departments in all tertiary hospitals. India’s Ayushman Bharat extended coverage to 500 million citizens, encouraging private providers to expand rehabilitation capacity. Japan’s super-aging society funneled USD 2.1 billion into robotic mobility aids in 2024-2025, elevating physiotherapy equipment market penetration.

Europe contributes roughly one-quarter of global value. Stringent EU MDR rules have raised compliance costs, favoring well-resourced manufacturers. The Middle East and Africa remain nascent, though the United Arab Emirates and Saudi Arabia are investing under Vision 2030. South America, led by Brazil, is advancing steadily at 5-6%, but currency volatility tempers capital spending.

Competitive Landscape

Global supply is moderately fragmented. The top five vendors, Enovis, BTL Industries, Zimmer MedizinSysteme, EMS Physio, and Patterson Medical, collectively contribute a significant share of the physiotherapy equipment market revenue. Enovis integrated DJO Global in 2025, leveraging group-purchasing contracts to cross-sell bracing, cold therapy, and electrotherapy systems. BTL’s subscription model shifts capital outlay to monthly fees, broadening its reach among mid-tier clinics.

Cost-advantaged Chinese suppliers such as Guangzhou Longest capture a significant share in emerging markets by pricing below Western peers, although perceptions of after-sales support cap penetration in regulated regions. High-margin whitespace lies in AI-enabled SaaS platforms from Lifeward and Hocoma, which yield 60-70% gross margins compared with 30-40% for hardware lifts. Robotics firms are moving to rental models aligned with Japan’s reimbursement shift, smoothing adoption curves.

Start-ups focused on tele-rehabilitation analytics are attracting venture funding, but FDA cybersecurity rules complicate entry for smaller players. Overall, the physiotherapy equipment market exhibits healthy rivalry across price bands and technology tiers, fueling consistent innovation.

Physiotherapy Equipment Industry Leaders

-

EMS Physio

-

BTL industries

-

Enovis

-

Zimmer MedizinSysteme GmbH

-

Patterson Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: BTL Industries officially launched a new suite of robotic physiotherapy systems, marking a significant expansion of their "BTL Robotics" portfolio into high-end rehabilitation technology.

- February 2025: DJO Global received U.S. FDA approval in February 2025 for its Aircast Pneumatic Series, a new range of portable, air-pressure-based recovery products.

- January 2025: Resolve360 announced the development of India's first Artificial Intelligence (AI) and Augmented Reality (AR) application for active physiotherapy.

Global Physiotherapy Equipment Market Report Scope

As per the scope of the report, Physiotherapy equipment encompasses a broad range of medical devices and tools designed to alleviate pain, restore mobility, and support rehabilitation after injury, surgery, or illness.

The physiotherapy equipment market is segmented by equipment type, application, end user, and geography. By equipment type, the market is categorized into electrotherapy, ultrasound therapy, laser & light therapy, shockwave therapy, magnetic & PEMF therapy, heat & cryotherapy systems, hydrotherapy systems, multi-exercise & rehabilitation stations, and wearable & assistive rehabilitation devices. By application, it is segmented into musculoskeletal, neurology, cardiovascular & pulmonary, sports & orthopedic injuries, pediatrics, women’s health & OB/GYN, and pain management & chronic care. By end user, the segmentation includes hospitals, rehabilitation centers/specialty clinics, home-care settings, ambulatory surgical centers, and sports medicine centers. Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Electrotherapy |

| Ultrasound Therapy |

| Laser & Light Therapy |

| Shockwave Therapy |

| Magnetic & PEMF Therapy |

| Heat & Cryotherapy Systems |

| Hydrotherapy Systems |

| Multi-exercise & Rehabilitation Stations |

| Wearable & Assistive Rehabilitation Devices |

| Musculoskeletal |

| Neurology |

| Cardiovascular & Pulmonary |

| Sports & Orthopedic Injuries |

| Pediatrics |

| Women’s Health & OB/GYN |

| Pain Management & Chronic Care |

| Hospitals |

| Rehabilitation Centers / Specialty Clinics |

| Home-care Settings |

| Ambulatory Surgical Centers |

| Sports Medicine Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of APAC | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Equipment Type | Electrotherapy | |

| Ultrasound Therapy | ||

| Laser & Light Therapy | ||

| Shockwave Therapy | ||

| Magnetic & PEMF Therapy | ||

| Heat & Cryotherapy Systems | ||

| Hydrotherapy Systems | ||

| Multi-exercise & Rehabilitation Stations | ||

| Wearable & Assistive Rehabilitation Devices | ||

| By Application | Musculoskeletal | |

| Neurology | ||

| Cardiovascular & Pulmonary | ||

| Sports & Orthopedic Injuries | ||

| Pediatrics | ||

| Women’s Health & OB/GYN | ||

| Pain Management & Chronic Care | ||

| By End User | Hospitals | |

| Rehabilitation Centers / Specialty Clinics | ||

| Home-care Settings | ||

| Ambulatory Surgical Centers | ||

| Sports Medicine Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of APAC | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

Estimated market size of the physiotherapy equipment market in 2026?

The physiotherapy equipment market size is estimated at USD 23.89 billion in 2026 and is forecast to grow at a 6.85% CAGR through 2031.

Which equipment segment leads global sales?

Electrotherapy systems led with 36.7% physiotherapy equipment market share in 2025, supported by established reimbursement in North America and Europe.

What is the fastest-growing application area?

Sports and orthopedic injuries are projected to register a 7.45% CAGR through 2031 as professional and amateur athletes increase preventive spending.

Which region will expand most rapidly?

Asia-Pacific is expected to post a 7.62% CAGR thanks to initiatives such as Healthy China 2030 and Japan’s investment in robotics.

How are insurers influencing purchasing trends?

New Remote Therapeutic Monitoring codes allow providers to bill USD 200-300 per patient monthly, incentivizing the shift toward connected and AI-enabled devices.

Page last updated on: