Exoskeleton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

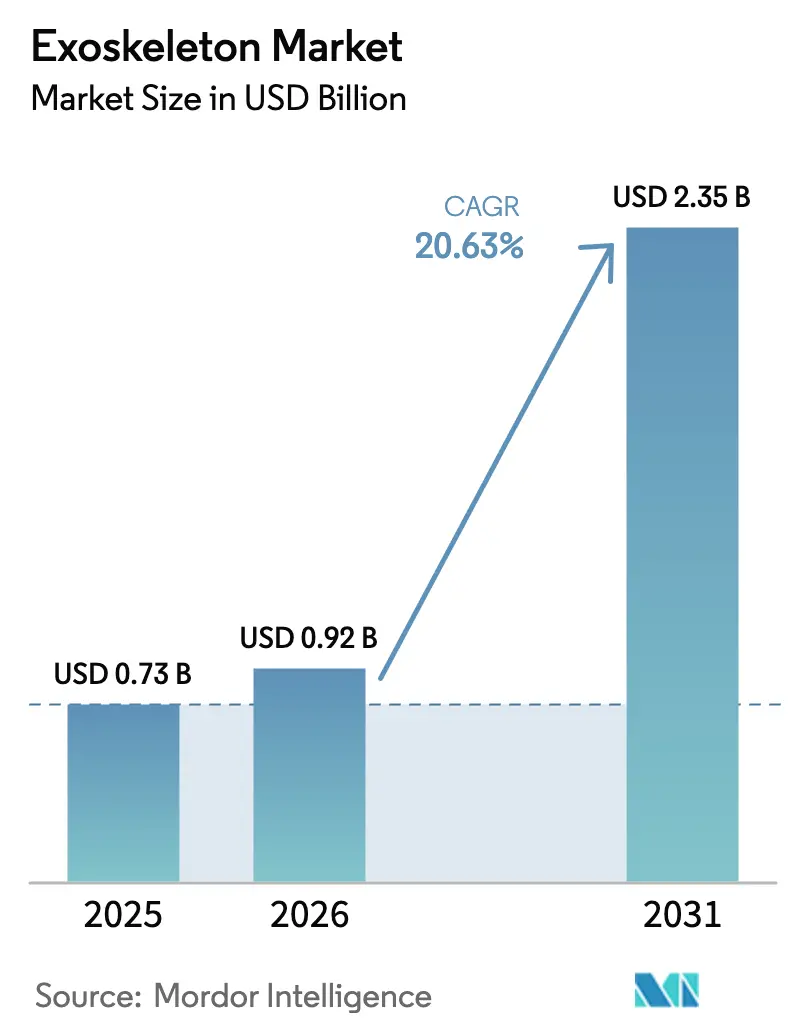

| Market Size (2026) | USD 0.92 Billion |

| Market Size (2031) | USD 2.35 Billion |

| Growth Rate (2026 - 2031) | 20.63% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Exoskeleton Market Analysis by Mordor Intelligence

The Exoskeleton Market size was valued at USD 0.73 billion in 2025 and is estimated to grow from USD 0.92 billion in 2026 to reach USD 2.35 billion by 2031, at a CAGR of 20.63% during the forecast period (2026-2031).

Uptake is broadening from hospital-based gait rehabilitation suites into factory production lines, soldier augmentation programs, and mid-priced consumer wellness gear. Subscription “Exoskeleton-as-a-Service” contracts are removing capital-expenditure barriers for small- and medium-sized manufacturers, while cloud-linked outcome analytics are paving the way for value-based reimbursement that compresses U.S. Medicare approval cycles from months to weeks. In the Asia Pacific, sovereign industrial-policy grants in China, Japan, and South Korea are localizing actuator supply chains and accelerating time-to-market for domestic brands. North American and European factories, meanwhile, adopt upper-body rigs that reduce deltoid muscle activity by 30–40%, lowering workers' compensation claims and supporting lean-manufacturing targets. Defense orders, such as the USD 6.9 million U.S. Army contract for ONYX, underscore a high-margin niche that also drives component ruggedization standards.

Key Report Takeaways

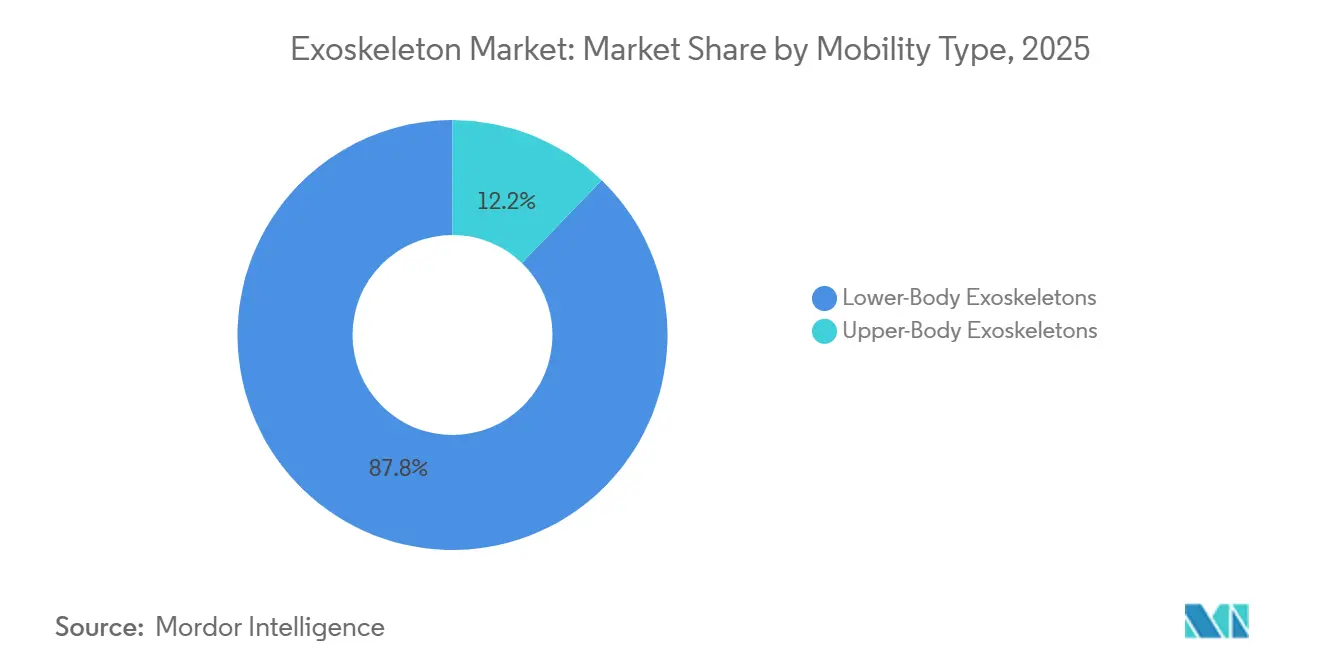

- By mobility type, lower-body systems led the exoskeleton market, accounting for 87.81% of the market share in 2025. Meanwhile, upper-body solutions are forecast to log a 24.06% CAGR through 2031.

- By power source, powered designs accounted for 82.83% of the exoskeleton market size in 2025; hybrid architectures are the fastest-growing segment at a 27.77% CAGR through 2031.

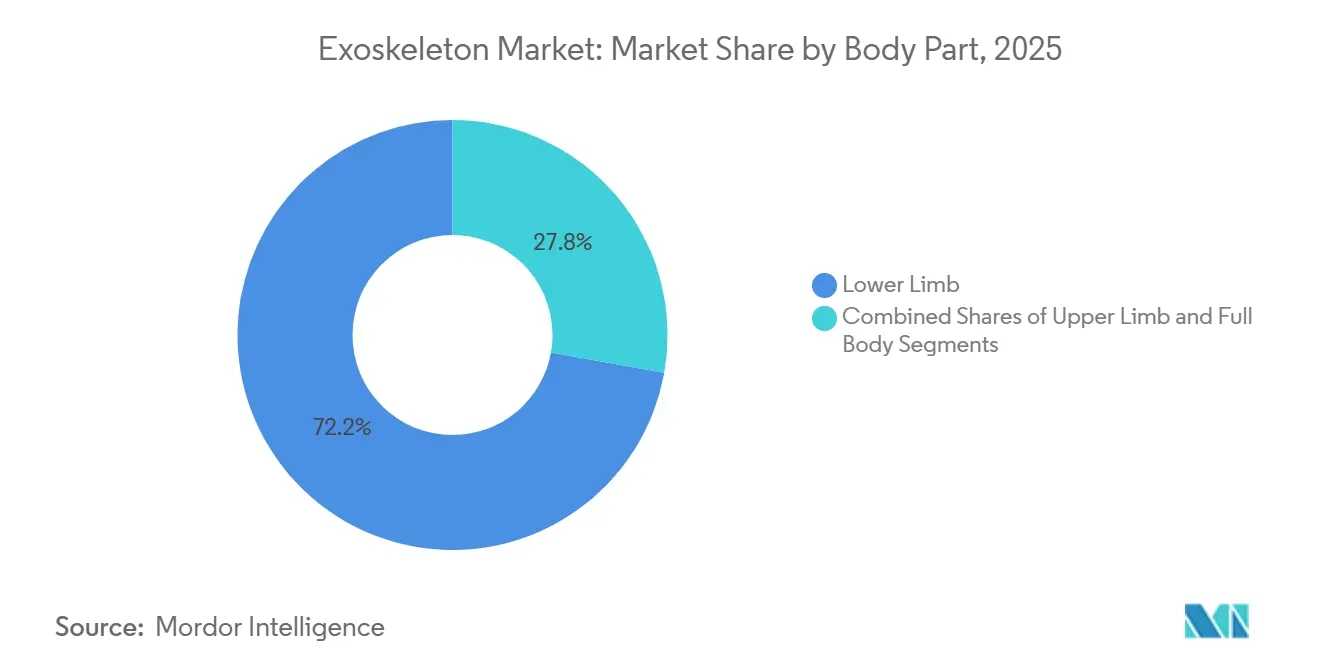

- By body part, lower-limb devices captured a 72.18% share of the exoskeleton market size in 2025, whereas upper-limb rigs are expected to advance at a 22.78% CAGR through 2031.

- By end user, hospitals and rehabilitation centers held 47.36% of the exoskeleton market share in 2025; personal and home-care buyers represent the fastest-growing segment, with a 28.87% CAGR up to 2031.

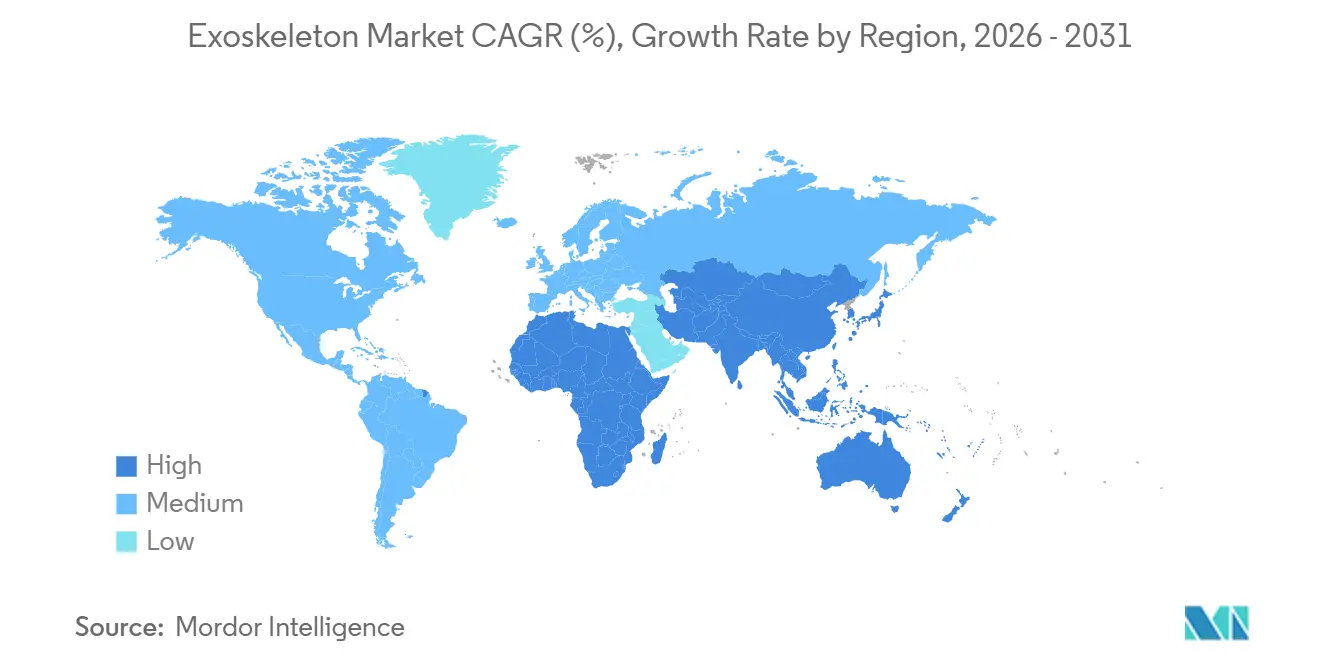

- By geography, North America dominated with 40.65% exoskeleton market share in 2025, while Asia Pacific is poised for a 26.87% CAGR during the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Exoskeleton Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population & Neurological-Disorder Prevalence Boosting Rehab Demand | +4.2% | Global, concentrated in Japan, South Korea, EU | Long term (≥ 4 years) |

| Work-Safety Regulations Spurring Industrial Adoption | +3.8% | North America, Germany, France | Medium term (2–4 years) |

| Defense Budgets Accelerating Soldier-Augmentation R&D | +2.1% | United States, South Korea, Australia | Medium term (2–4 years) |

| Emergence of Mid-Priced Consumer/Outdoor Exosuits Enlarges TAM | +3.5% | North America, China, urban Asia Pacific | Short term (≤ 2 years) |

| Subscription "Exoskeleton-As-A-Service" Lowers SME Entry Barriers | +2.9% | Global, early traction in North America, Germany | Medium term (2–4 years) |

| Cloud-Based Outcome Analytics Enabling Value-Based Rehab Payments | +2.4% | United States, pilot programs in UK, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Population & Neurological-Disorder Prevalence Boosting Rehab Demand

Worldwide, the cohort aged 60 and above will double to 2.1 billion by 2050, intensifying the incidence of stroke, Parkinson’s disease, and spinal-cord injury.[1]World Health Organization, “Ageing and Health,” who.int Japanese policymakers widened coverage for Cyberdyne’s HAL in 2024 after data showed that robotic gait therapy shortened the average post-stroke hospital stay by 14 days.[2]Ministry of Health, Labour and Welfare Japan, “Reimbursement Coverage for Assistive Devices,” mhlw.go.jp Similar evidence is informing European payer pilots, signaling that outcome-based contracts will become the default procurement method for rehabilitation devices. FDA 510(k) clearances and ISO 13482 compliance now serve as baseline requirements for clinic adoption in the United States and the European Union. Together, these trends highlight the enduring demand for lower-limb systems that restore upright mobility, mitigate pressure ulcer risk, and maintain bone density.

Work-Safety Regulations Spurring Industrial Adoption

Revised OSHA guidelines, effective in 2024, oblige U.S. employers to audit overhead tasks and loads above 10 kg, creating a regulatory incentive for shoulder-support rigs. Germany’s Federal Institute for Occupational Safety and Health reported 30–40% reductions in deltoid EMG when workers used passive exoskeletons, prompting automakers to extend deployments across weld, paint, and assembly shops.[3]Federal Institute for Occupational Safety and Health Germany, “Exoskeletons in Occupational Use,” baua.de As insurance premiums fall alongside musculoskeletal disorder claims, factories capitalize on double-digit internal rate of return metrics for upper-body wearables.

Defense Budgets Accelerating Soldier-Augmentation R&D

The FY 2026 U.S. National Defense Authorization Act earmarks multi-year funds for human augmentation systems, moving programs from prototypes into production. Lockheed Martin’s ONYX reduces the metabolic cost of carrying a 60 kg load by 30%, earning a USD 6.9 million contract that validates the use case for infantry patrols. South Korea’s DAPA is co-funding similar designs for surveillance along the Demilitarized Zone, reflecting allied interest in extended-range missions. Compliance with MIL-STD-810 and NATO STANAGs is driving suppliers to invest in ruggedized actuators and sealed electronics that later spill over into industrial SKUs. Hybrid powertrains, which combine passive springs with intermittent motor assist, increasingly satisfy both endurance and torque demands.

Emergence of Mid-Priced Consumer/Outdoor Exosuits Enlarges TAM

A new tranche of sub-USD 5,000 devices is expanding the total addressable population by 40%, offering aging hikers and recreational athletes powered assistance without the complexity of hospital-grade equipment. Hypershell’s Omega sells at USD 799 and delivers 30 W of hip support for six-hour trail treks. Samsung’s GEMS Hip was cleared by South Korean regulators for over-the-counter sale in 2024 at USD 3,750–7,500, providing a daily-use mobility aid without a prescription. These products sit outside stringent medical-device rules, yet vendors pursue voluntary IEC 60601 conformity to reassure retail buyers. Early adopters highlight lower perceived exertion and longer activity times, signaling a consumer-wellness channel that could rival therapeutic volumes by the end of the decade.

Restraints Impact Analysis of Exoskeleton Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost & Limited Reimbursement | -3.1% | Global, acute in United States, Southern Europe | Medium term (2–4 years) |

| Battery-Energy Density Limits Field Endurance | -2.4% | Industrial and defense segments globally | Long term (≥ 4 years) |

| Absence of Ergonomic Test Standards Creates Liability Concerns | -1.8% | North America, Europe | Medium term (2–4 years) |

| Tariff-Driven Actuator-Component Cost Volatility Squeezes Margins | -2.2% | Global supply chains, acute in United States | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost & Limited Reimbursement

Clinic-grade exoskeletons list at USD 80,000–150,000, restricting purchases to academic medical centers or flagship rehabilitation chains. U.S. Medicare requires documented failure of conventional physiotherapy and physician attestation of 30-minute upright tolerance, disqualifying nearly half of potential candidates. Private insurers label take-home models “investigational,” compelling many patients to self-fund despite FDA clearance. Germany reimburses hospital sessions under DRG codes, but refuses to reimburse personal devices, while Italy and France have yet to establish payment pathways. The mismatch depresses adoption in the high-growth home-care segment and reinforces calls for bundled-payment pilots tied to real-world outcome data.

Battery-Energy Density Limits Field Endurance

Today’s lithium-ion packs deliver 150–250 Wh/kg, capping active-mode runtime at 4–8 hours and forcing industrial and military users to schedule disruptive battery swaps. Sarcos’ Guardian XO requires replacement packs every four hours while lifting 90 kg loads, eroding uptime benefits. Solid-state chemistries promise 400 Wh/kg by 2027, but prototypes face thermal-runaway risks that necessitate heavier thermal management systems. Designers face a mass-benefit trade-off: packs exceeding 1.5 kg raise limb inertia, negating metabolic gains. UN 38.3 transport testing and IEC 62133 safety hurdles further delay commercialization timelines and investors’ break-even projections.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Exoskeleton Market Segment Analysis

By Mobility Type:

Industrial Traction Fuels Upper-Body GrowthLower-body rigs held an 87.81% exoskeleton market share in 2025, reflecting their entrenched use in stroke and spinal cord injury rehabilitation, where gait training protocols depend on programmable knee and hip assistance. These units generate steady replacement demand from rehabilitation centers and veterans’ hospitals. In contrast, upper-body systems experienced faster adoption in assembly lines, with a 24.06% CAGR, as automakers and aerospace primes addressed shoulder-injury costs that previously exceeded USD 1 billion annually in lost productivity and compensation claims. Factory pilots validate throughput gains of 15–20% in tasks such as windshield fastening and wing drilling, confirming immediate payback periods. The dual-track dynamic positions lower-limb rigs to dominate clinical revenues while upper-body devices expand industrial revenues and diversify supplier order books.

Upper-body progress aligns with ergonomic mandates now commonly found in U.S. and EU certification audits. Light passive braces weighing under 3 kg win favor for their drop-in compatibility with shift changes, whereas powered shoulder units combine high-peak torque with predictive-maintenance telemetry that reinforces service-contract annuity streams. Full-body exoskeletons remain a niche market for heavy-industry users with handling demands of 90 kg, and joint-specific waist supports are gaining traction in e-commerce distribution centers that face record parcel volumes.

By Power Source / Mode:

Hybrid Designs Extend Shift RuntimePowered architectures commanded 82.83% of the exoskeleton market size in 2025, necessary for therapeutic gait modulation and soldier-load reduction. Clinics rely on brushless DC motors paired with harmonic drives to deliver 40 Nm of knee torque with sub-50 ms latency, which is vital for neuroplastic rehabilitation. Passive frames, built on springs and cams, excel in overhead factory tasks due to their zero recharge requirements and minimal maintenance. Hybrids integrate passive load-sharing with bright motor bursts, lifting runtime to 8–10 hours and aligning with OSHA-defined shift blocks. Consequently, hybrids are growing at 27.77% CAGR and already dominate new proposal requests from automotive ergonomists.

Battery-intensive powered models still bear regulatory burdens under IEC 60601, while passive frames fall outside many medical device regimes. Vendors now tout firmware that tunes assist curves to user gait data, positioning hybrid exoskeletons as software-defined assets whose performance improves via over-the-air updates. The strategy focuses on recurring-revenue bundles and underpins the subscription leap beyond traditional sales. Suppliers that master torque-to-watt optimization will differentiate themselves as energy density increases, consolidating their share in an increasingly data-rich value chain.

By Body Part:

Shoulder-Support Leads Upper-Limb WaveLower-limb platforms captured 72.18% exoskeleton market share in 2025, given their decade-long head start in clinical research and regulatory clearances. Nevertheless, the 22.78% CAGR logged by upper-limb systems underscores unsatisfied demand across aerospace, shipbuilding, and logistics verticals. Myomo’s FDA-cleared MyoPro orthosis demonstrates that powered elbow-wrist assistance can be effectively integrated into daily living contexts, thereby expanding payers’ assessment of functional outcome gains.

Full-body rigs, typified by Sarcos Guardian XO, address heavy-load contexts but remain limited to specialized yards because device mass approaches 50 kg and list prices top USD 500,000. Joint-specific braces for lumbar support are being introduced in fulfillment centers, where Amazon is piloting soft textile suits to reduce lift-and-twist strain during parcel sortation surges. As AI-driven sensor fusion informs real-time load distribution, body-part segmentation may become blurred; however, device certification will still follow limb-specific risk profiles under ISO 13482.

By End User:

Home-Care Demand Rises with Aging-in-PlaceHospitals and rehabilitation centers held a 47.36% share in 2025, reflecting bundled DRG reimbursement and capital allocations for robotic therapy wings. Rapid throughput helps justify purchases, with outcome dashboards showing 25% therapist-time savings per gait-training day. Personal and home-care users, however, represent the fastest-growing segment at 28.87% CAGR, as seniors prefer mobility aids that minimize inpatient stays. ReWalk Personal-6.0 demonstrates that wheelchair users can navigate residential layouts and perform standing transfers, thereby reducing the demand for at-home nursing visits and strengthening payers’ shared-savings logic.

Industrial and military buyers fill a third bucket whose volumes swell amid workforce-shortage pressures and defense planning cycles. Subscription leasing at EUR 199 per user per month demonstrates that even tier-three suppliers to automotive OEMs can deploy exoskeletons without engaging in capital budget fights. Compliance in the home environment requires adherence to IEC 60601-1-11 for patient-moving equipment, which raises the bar for user-friendly interfaces and washable upholstery covers. Vendors that fulfill both hospital and home-care checklists will capture lifetime-value streams as therapy transitions from clinic to living room.

Geography Analysis

North America Exoskeleton Market

North America accounted for 40.65% of the exoskeleton market share in 2025, driven by FDA-cleared product portfolios and a robust distribution network of durable medical equipment suppliers. The United States leads clinical deployments at centers such as Kessler and Shepherd, where real-world evidence informs payer rule-making. OSHA’s 2024 ergonomic assessment directive is catalyzing factory pilots from Detroit to Seattle, converting EHS compliance budgets into exoskeleton leases. Canada lags due to provincial budget ceilings, whereas Mexico’s nascent market awaits revisions to its social security code to spur reimbursement.

APAC Exoskeleton Market

Asia Pacific registers the fastest growth at a 26.87% CAGR through 2031, propelled by China’s 297 million citizens aged 60+ and Japan’s super-aged demographic, where 29% of residents exceed 65 years. Mainland hospitals tap Healthy China 2030 subsidies to order gait-therapy robots, while Japan’s national insurance now reimburses HAL for eight neuromuscular indications. South Korea’s KRW 50 billion robotics fund is nurturing domestic actuator plants that lower bill-of-materials costs. Australia leverages its National Disability Insurance Scheme for pilot grants, and India courts FDI to assemble budget devices for a vast stroke population.

EMEA and South America Exoskeleton Market

Europe remains bifurcated. Germany, France, and the United Kingdom undertake large-scale industrial pilots under fresh ergonomic directives and secure CE-marked rehab units through DRG codes. Southern Europe lags because fragmented reimbursement hinders capital expenditure planning, and MDR transition timelines strain importer resources. Scandinavia experiments with soft-suit subsidies for rural eldercare, while Eastern Europe focuses EU cohesion funds on stroke rehab capacity. Middle East healthcare hubs in the UAE and Saudi Arabia procure flagship units for showcase hospitals. Still, Africa and South America exhibit limited uptake beyond Brazil’s pilot projects in São Paulo and Rio, which are constrained by tariff regimes and currency fluctuations.

Regulatory Landscape

Regulation in the exoskeleton market typically splits between medical-intended devices and occupational or consumer assist systems. In the United States, powered lower extremity exoskeletons are regulated by the FDA as Class II medical devices under 21 CFR 890.3480 (product code PHL), generally requiring 510(k) clearance along with risk management aligned to ISO 14971, plus electrical and home-use safety expectations commonly mapped to IEC 60601-1 and IEC 60601-1-11 for devices used outside acute-care settings.

In Europe, manufacturers often route therapeutic or rehabilitation claims through the EU Medical Device Regulation (MDR 2017/745), while mechanical and general safety obligations can also trigger the Machinery Directive (2006/42/EC) for actuated systems and components, especially for worker-assist configurations. This dual-regime setup increases documentation and testing loads for companies selling similar platforms into hospitals, industrial EHS programs, and personal or home environments, reinforcing quality-system expectations (for example, ISO 13485) and raising the compliance bar for software updates and connected analytics features.

Value Chain Analysis

The exoskeleton value chain starts with upstream components such as high-torque motors, gearsets, sensors, embedded compute, and lithium-ion battery packs, followed by midstream design, clinical and ergonomic validation, and regulated manufacturing under medical-grade quality systems for healthcare SKUs. Supplier concentration around specialized actuators and battery subsystems, together with long lead times for validated electronics and constrained EU MDR notified-body capacity, can create bottlenecks that affect delivery schedules for hospital tenders and fleet rollouts.

Downstream routes diverge by end user. Hospitals and rehabilitation centers often buy via direct sales and clinical channel partners, while industrial deployments more frequently use subscription or fleet-style contracting tied to EHS and productivity metrics. In 2026, distribution-oriented channel buildout stood out, including Wandercraft naming National Seating and Mobility as the exclusive U.S. complex rehabilitation technology distribution partner for the Eve personal exoskeleton, and Lifeward working with Shirley Ryan AbilityLab to schedule dedicated evaluation clinic days for ReWalk Personal, both of which strengthen the last-mile path from manufacturer to patient adoption and ongoing service support.

Competitive Landscape

Sector concentration is moderate: the five most prominent vendors, Ekso Bionics, ReWalk Robotics, Cyberdyne, Parker Hannifin, and Ottobock, hold significant revenue share, while dozens of smaller players focus on niche limbs, textile suits, or regional markets. Rehabilitation-centric firms court payers by publishing peer-reviewed outcomes and embedding cloud analytics that validate functional gains. Industrial-sector specialists promote subscription economics and telemetry that predict actuator overhaul windows, reducing downtime for SMEs. Defense contractors such as Lockheed Martin exploit classified supply chains and vendor-qualified lists to win sole-source awards for rugged soldier-assist kits.

Start-ups inject innovation: Bioservo’s tendon-driven Carbonhand glove secured EUR 10 million in Series B funding and achieved CE marking in 2024, extending grip-assist capabilities to industrial and clinical workflows. Fourier Intelligence scaled its X2 lower-limb model to 500 units annually by localizing gearboxes in Shanghai, under-pricing Western equivalents by 30–40% and signaling a credible cost-disruption threat. M&A reshapes the map; Ekso Bionics’ 2024 merger with Lifeward united industrial and rehab portfolios, and ReWalk’s partnership with AlterG bundles anti-gravity treadmills with exoskeleton therapy. Regulatory rigor remains a moat: full FDA 510(k) and MDR certification can exceed USD 10 million in trial and audit expenses, throttling undercapitalized aspirants.

Strategic roadmaps now pivot to AI-enabled gait adaptation, edge-compute-powered collision avoidance, and energy-recuperation brakes. Vendors able to fuse these technologies with flexible payment models and ISO-compliant quality systems will capture disproportionate share as volume scales beyond early adopters. Meanwhile, insurers are beginning to reward suppliers that guarantee outcome milestones, cementing data analytics capability as a competitive differentiator in the next five-year horizon.

Exoskeleton Industry Leaders

CYBERDYNE Inc.

Ekso Bionics Holdings Inc.

Ottobock SE & Co. KGaA

Parker Hannifin Corporation

Sarcos Technology & Robotics Corporation

- *Disclaimer: Major Players sorted in no particular order

Exoskeleton Market Companies Covered in this Report

- B-Temia

- BIONIK Laboratories Corp.

- Bioness Inc. (Bioventus)

- Bioservo Technologies

- CYBERDYNE Inc.

- Ekso Bionics

- Fourier Intelligence

- Gogoa Mobility Robots

- Lockheed Martin Corporation

- Myomo Inc.

- Ottobock

- Panasonic Corporation

- Parker Hannifin

- RB3D SAS

- ReWalk Robotics

- Rehab-Robotics Co. Ltd.

- Sarcos Technology & Robotics Corporation

- Seismic Powered Clothing

- Wearable Robotics SRL

Market Opportunities and Future Outlook

One opportunity is scaling home and community use without relying only on hospital purchasing cycles, by using established durable medical equipment (DME) and complex rehabilitation technology (CRT) channels. The June 2026 move naming National Seating and Mobility as the exclusive U.S. CRT distributor for Wandercraft's Eve personal exoskeleton (pending FDA clearance referenced for summer 2026) signals that vendors are formalizing distribution, fitting, and service pathways needed for take-home mobility, which also supports subscription and outcomes-linked contracting models.

Clinical evidence packages and safety datasets remain central to expanding reimbursement and clinician confidence, particularly for spinal cord injury and neurorehabilitation pathways that carry high device prices and frequent payer scrutiny. In May 2026, Lifeward shared longitudinal safety data for ReWalk users (2013 to 2025), emphasizing low reported lower extremity fracture incidence, which complements the report context on cloud-linked outcome analytics. On the technology side, integration efforts such as MicroPort NeuroTech's strategic agreement with OYMotion to combine brain-computer interface technology with exoskeleton systems point to a roadmap connecting neural and biopotential signals with adaptive control, creating whitespace for differentiated rehabilitation protocols and data-driven therapy services rather than hardware-only competition.

Recent Industry Developments in Exoskeleton Market

- June 2026: Wandercraft named National Seating and Mobility as the exclusive complex rehabilitation technology distribution partner in the United States for the Eve personal exoskeleton. The move links a home-use personal mobility product with an established CRT channel for fitting, service, and reimbursement navigation, tightening the go-to-market path as FDA clearance is pursued.

- December 2025: Ekso Bionics entered into an agreement with MediTouch to become the exclusive authorized U.S. distributor of the BalanceTutor rehabilitation system. Adding a complementary rehab platform broadens Ekso's clinic-facing portfolio and can deepen relationships with rehabilitation providers that already evaluate robotic therapy solutions.

- March 2024: Innophys began sales of its Muscle Suit exoskeleton models in Slovakia and the Czech Republic. The expansion shows continued geographic diversification for industrial-assist exoskeleton suppliers, using adjacent European markets to extend distribution and build an installed base outside core home geographies.

Exoskeleton Market Report Scope and Research Methodology

Market Definition and Coverage

This market is defined as the revenue earned from exoskeleton systems that are worn on the body to support, assist, or augment human movement and strength across medical, industrial, and defense use cases.

Scope exclusions: We exclude general fitness wearables, standalone prosthetics, and non-exoskeleton mobility aids that do not provide powered or mechanical assistance to the user.

Segments Covered in This Report

- By Mobility Type

- Lower-Body Exoskeletons

- Upper-Body Exoskeletons

- Full-Body Exoskeletons

- Joint-Specific / Waist Systems

- By Power Source / Mode

- Powered / Active

- Passive

- Hybrid

- Soft Exosuits

- By Body Part

- Upper Limb

- Lower Limb

- Full Body

- By End User

- Hospitals & Rehab Centers

- Personal / Home-care Users

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by building a clean view of the demand and supply environment for exoskeletons, using public and official data where it is available. Typical inputs include sources such as the US FDA device databases for approved and cleared systems, the US Bureau of Labor Statistics for injury rates and occupational exposure, and National Institutes of Health publications for rehabilitation outcomes and therapy trends.

We also check sources such as the International Trade Administration and customs trade statistics to understand cross border movement of relevant robotic and assistive equipment categories, along with patent databases to track technology focus areas and filing momentum. Company annual reports, investor decks, and reputable press coverage are used to map product launches and price positioning, and a paid company financials and intelligence subscription helps verify business line disclosures when they are reported at a usable level. The sources cited above are illustrative, and many other public references were reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to validate what is really being adopted in hospitals, rehab centers, and industrial sites, and to pressure test the assumptions taken from public information. We speak with a mix of device manufacturers, distributors, integrators, and clinical and workplace users across APAC, EMEA, and the Americas so that regional adoption patterns and procurement cycles can be compared in a consistent way.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 15% | APAC: 41% |

| Mid tier: 48% | Functional/Unit leaders: 42% | EMEA: 33% |

| Smaller Players: 20% | Managers: 43% | Americas: 26% |

Market-Sizing & Forecasting

Sizing is built using a top-down and bottom-up approach, where the main model reconstructs the revenue pool by linking addressable installations to average selling prices in the most common buying channels. For exoskeletons, the top-down path relies on a demand pool view tied to rehabilitation activity levels, workplace ergonomics adoption, and defense modernization emphasis, and then the totals are allocated across regions based on observed rollout intensity.

Selective bottom-up checks are then used to keep the output realistic, which includes sampled ASP x unit volumes for key device types, channel feedback on typical order sizes, and supplier roll ups where revenue disclosure is clear enough to use. Inputs that are commonly tracked include the split between powered and passive systems, the pace of new clinical site additions, budget cycles for workplace safety programs, utilization rates in therapy settings, and pricing shifts linked to feature upgrades and service bundles. Forecasts are derived using scenario analysis supported by expert views on adoption speed, reimbursement direction, and industrial automation spending, and then the scenarios are converted into a single base case after review. When data gaps exist, conservative penetration bands are applied and rechecked with interview feedback so the final numbers remain traceable to simple drivers.

Data Validation & Update Cycle

Validation is done through triangulation across model outputs, interview feedback, and external signals that should move in the same direction as sales, like therapy demand indicators and workplace injury focus areas. Outliers are flagged, assumptions are revisited, and the calculations are reviewed in more than one step before sign-off.

The dataset is refreshed at least once a year, and interim updates are made when there are material shifts such as regulatory approvals, major procurement programs, or meaningful pricing resets. Before delivery, a final review pass is completed so clients receive the most current view that can be supported by the latest checks.

Mordor Intelligence's Exoskeleton Market Estimate Compared With Other Published Estimates

Published market sizes for exoskeletons often vary because the product boundary is not treated the same way, and because pricing and adoption timing assumptions are not always refreshed on the same schedule. The year used as the base, whether values are reported in current dollars or adjusted terms, and how medical versus industrial demand is weighted can all move the total.

By tracking device type splits and refreshing pricing and adoption inputs through interviews, Mordor Intelligence keeps the model tied to shipped system demand and avoids counting adjacent wearable robotics categories that are sometimes bundled into broader totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.92 B (2026) | |

| Industry Research Group A | USD 0.59 B (2025) | Uses a different base year and a slower growth window, and the scope appears to be narrower on enterprise deployments, which can understate industrial adoption and near term program scale-ups. |

| Industry Publisher B | USD 0.93 B (2024) | Starts from an earlier base year and applies a longer horizon with higher expansion assumptions, which can amplify the impact of future healthcare and industrial penetration before it is visible in near term procurement activity. |

The spread mainly comes from year selection, how closely pricing is updated, and whether broader wearable robotics are grouped into the same bucket as exoskeletons. Our approach stays transparent because the totals can be walked back to clear drivers like adoption rates, site activity, and realistic ASP ranges, and then checked again with practitioner feedback before finalizing.

Key Questions Answered in the Report

How large is the exoskeleton market in 2026 and what is the expected growth?

The exoskeleton market size is USD 0.92 billion in 2026 and is set to reach USD 2.35 billion by 2031, reflecting a 20.63% CAGR.

Which mobility type currently dominates revenues?

Lower-body models account for 87.81% of 2025 revenue, as they are deeply entrenched in clinical gait-rehabilitation programs.

Which segment is expanding fastest?

Upper-body systems used in automotive and aerospace assembly are projected to grow at 24.06% CAGR through 2031.

Why is Asia Pacific the fastest growing region?

Aging demographics and government grants in China, Japan and South Korea underpin a 26.87% CAGR through 2031.

What is the main barrier to home-care adoption?

High unit costs of USD 80,000–150,000 and fragmented reimbursement keep personal users from wider uptake.

Page last updated on: