Market Overview

| Study Period | 2021 - 2031 |

|---|---|

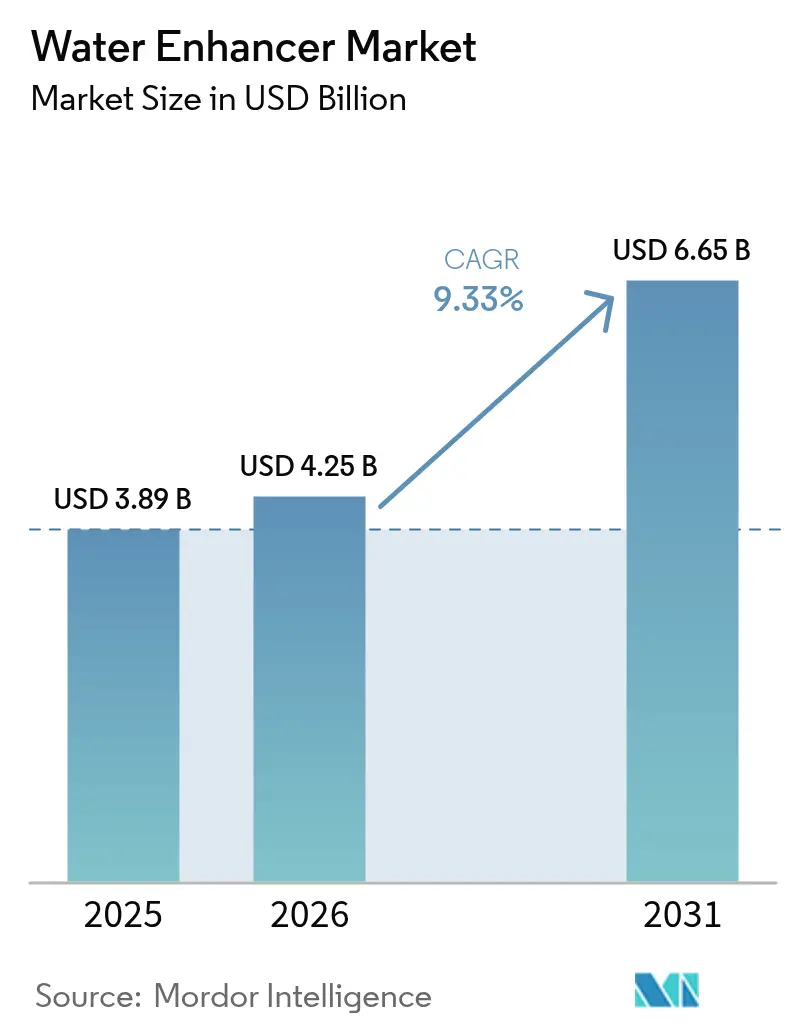

| Market Size (2026) | USD 4.25 Billion |

| Market Size (2031) | USD 6.65 Billion |

| Growth Rate (2026 - 2031) | 9.33% CAGR |

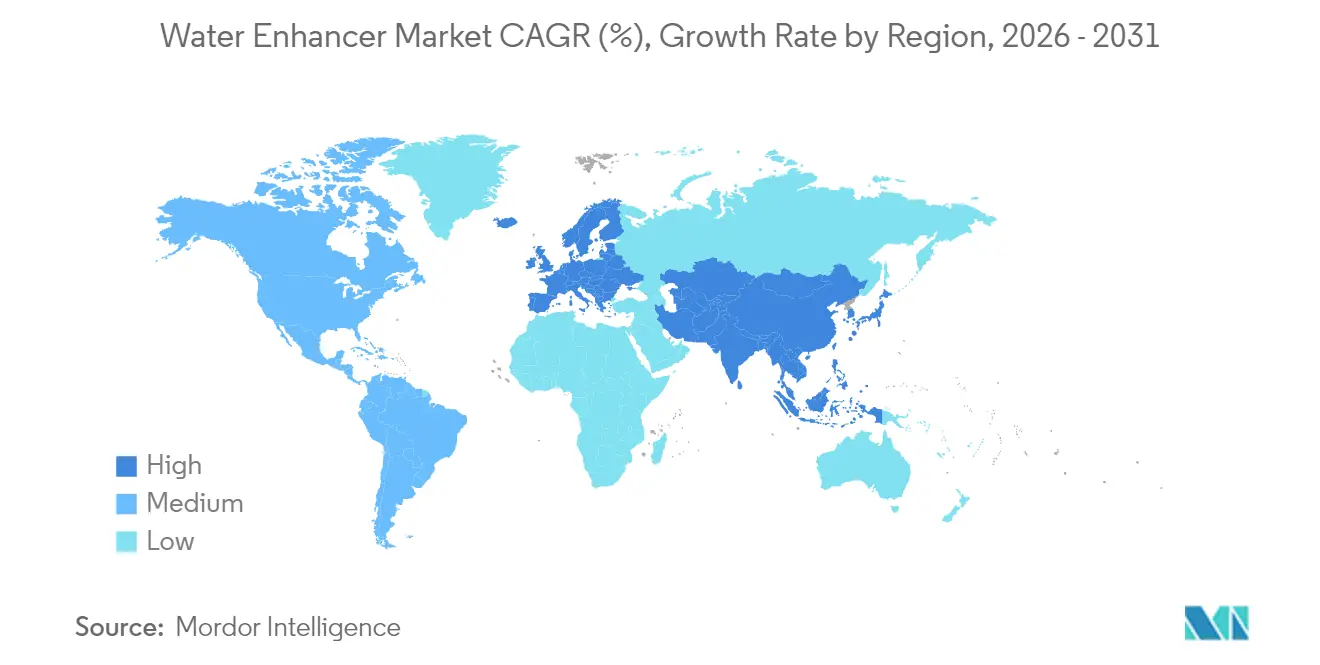

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Water Enhancer Market Analysis by Mordor Intelligence

The water enhancer market size was valued at USD 3.89 billion in 2025 and estimated to grow from USD 4.25 billion in 2026 to reach USD 6.65 billion by 2031, at a CAGR of 9.33% during the forecast period (2026-2031). Consumers are moving away from sugar-laden sodas toward customizable, low-calorie hydration solutions, and this behavioral shift is opening sustained headroom for brands that deliver functional benefits with minimal calories. Major beverage companies that once protected carbonated soft drinks are now investing in drop-based, powder, and liquid formats that give users control over flavor intensity, nutrient delivery, and portion size. The water enhancer market is also benefiting from the rise of wearable fitness devices that track hydration, encouraging users to reach daily water goals with electrolyte-fortified add-ins. Rapid distribution gains through e-commerce, quick-commerce, and subscription services further reduce purchase friction, creating a virtuous cycle of trial and repeat.

Key Report Takeaways

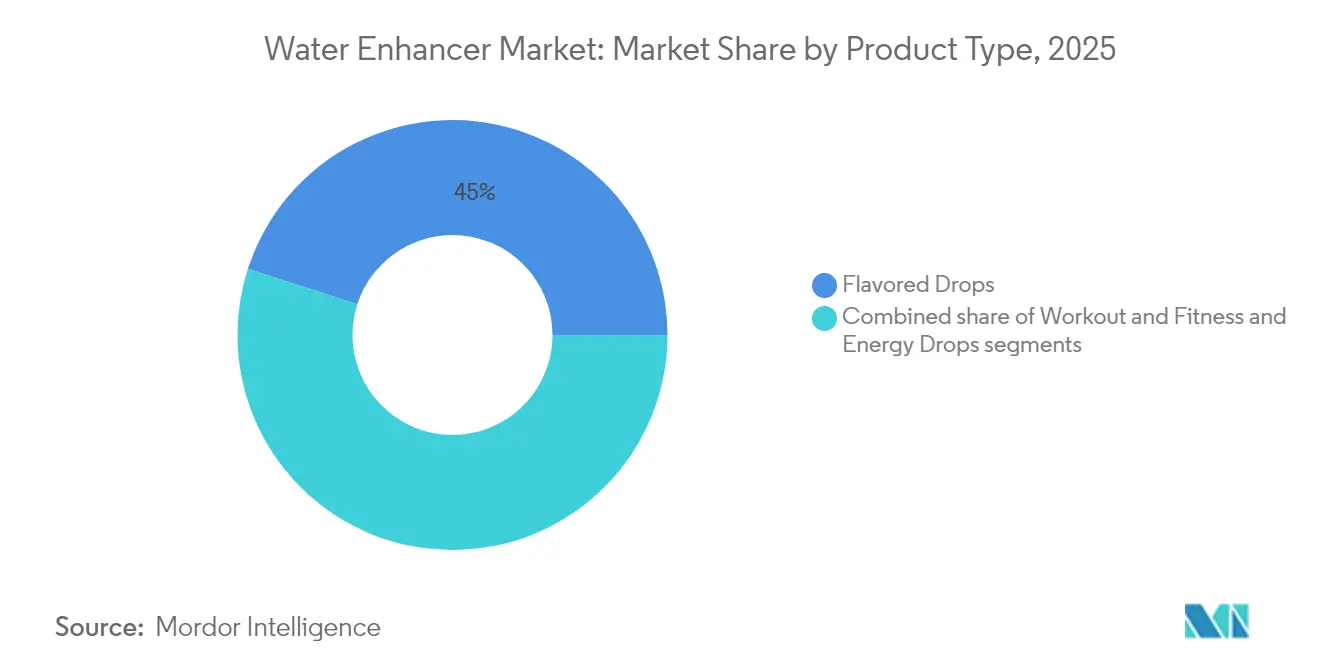

- By product type, Flavored Drops led with 45.02% revenue share in 2025; Workout and Fitness formulations are expanding at 10.12% CAGR through 2031.

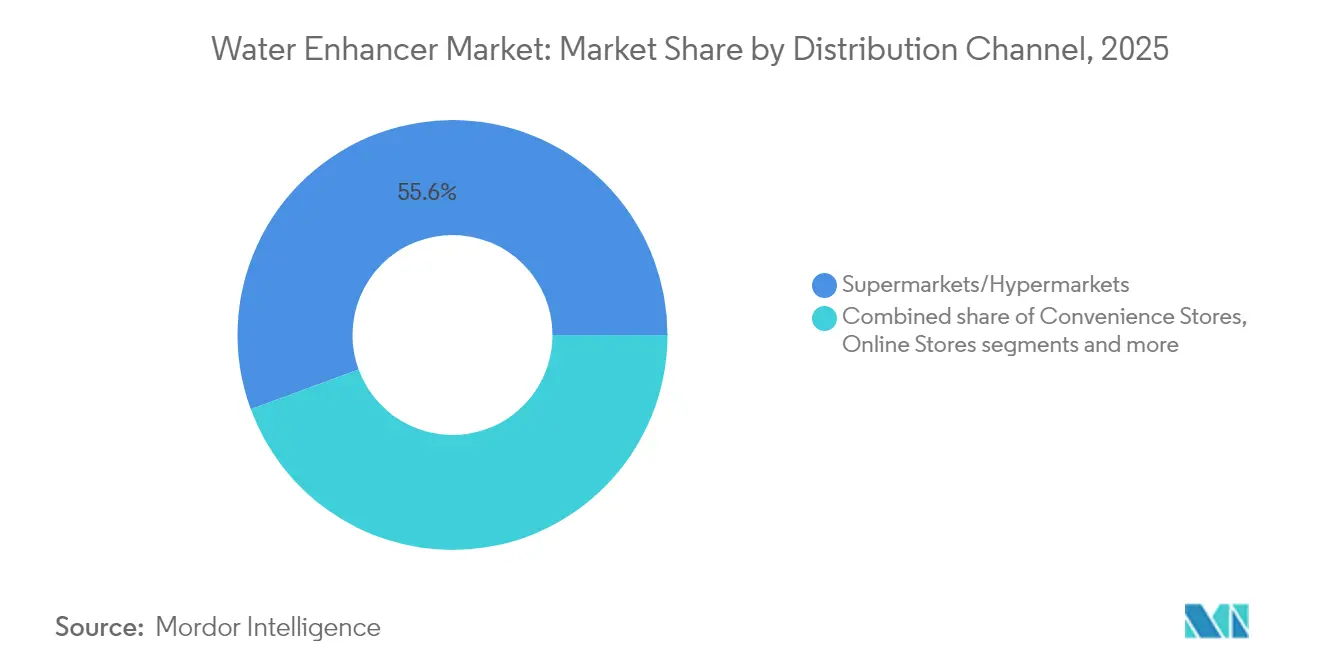

- By distribution channel, Supermarkets and Hypermarkets accounted for 55.62% share of the water enhancer market size in 2025, while Online Retail Stores are projected to grow at 11.24% CAGR to 2031.

- By geography, North America held 34.78% of the water enhancer market share in 2025 and South America is advancing at a 5.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Water Enhancer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health consciousness and demand for low-calorie hydration alternatives | +2.3% | Global, with strongest uptake in North America and Western Europe | Medium term (2-4 years) |

| Increasing preference for flavored water over sugary beverages | +1.8% | Global, particularly urban centers in Asia-Pacific and South America | Long term (≥ 4 years) |

| Major beverage firms' marketing and innovation fuel consumer engagement | +1.5% | North America, Europe, with spillover to Asia-Pacific | Short term (≤ 2 years) |

| Innovation in natural, organic, and functional ingredient formulations | +1.2% | Global, led by North America and Europe regulatory frameworks | Medium term (2-4 years) |

| Growing convenience for on-the-go consumers and busy lifestyles | +1.0% | Global, strongest in urban metros across all regions | Short term (≤ 2 years) |

| Collaborations of beverage brands with fitness influencers boosting market presence | +0.9% | North America, Europe, emerging in South America and Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising health consciousness and demand for low-calorie hydration alternatives

Rising health consciousness is a key driver for the water enhancer market, as consumers increasingly move away from sugary carbonated drinks and juices toward low‑calorie hydration options that still deliver flavor and variety. Growing focus on weight management, diabetes prevention, and overall metabolic health makes reduced‑sugar or zero‑calorie enhancers particularly attractive. At the same time, the expansion of the fitness culture is enlarging the addressable base: according to the Health & Fitness Association, professional fitness establishments in the United States now serve 77 million members, equivalent to roughly a quarter of the population aged six and above in 2024 [1]Source: Health & Fitness Association (HFA), "US Health Club and Studio Memberships Increase to Record 77 Million", healthandfitness.org. This large, exercise‑oriented cohort actively seeks convenient ways to support hydration before, during, and after workouts without adding unnecessary calories. Water enhancers fit naturally into gym bags and daily routines, allowing users to customize taste intensity while keeping total energy intake under control.

Increasing preference for flavored water over sugary beverages

Growing consumer preference for flavored water over sugary beverages is a major driver for the water enhancer market, as many people now seek refreshing options that deliver taste without the high sugar and calorie load associated with sodas and juices. This shift is reinforced by rising awareness of obesity, diabetes, and dental health concerns, prompting households to reduce soft drink consumption and look for lighter alternatives. Water enhancers allow consumers to transform plain water into a flavorful drink on demand, giving them control over sweetness and intensity while keeping overall calorie intake low. The wide range of fruit, botanical, and exotic flavors helps maintain interest and encourages higher daily hydration, especially among younger demographics. Manufacturers are also launching naturally flavored, zero‑sugar and vitamin‑fortified variants that closely align with clean‑label and functional beverage trends. Convenient formats such as squeezable drops and stick packs make it easy to flavor water at home, work, or on the go, further supporting adoption.

Major beverage firms' marketing and innovation fuel consumer engagement

Major beverage firms act as powerful growth engines for the water enhancer market by combining heavy marketing investments with rapid product innovation. Leading players such as PepsiCo, Kraft Heinz, Nestlé, and Coca‑Cola leverage established brands, celebrity endorsements, and digital campaigns to build awareness and trial among mainstream and fitness‑oriented consumers. Their large R&D budgets support continuous launches of new flavors, zero‑sugar lines, and functional variants with vitamins, electrolytes, or energy ingredients, keeping the category fresh and engaging. Frequent limited‑edition releases and co‑branding initiatives create a sense of novelty that encourages repeat purchases and experimentation. These companies also optimize packaging formats, from squeezable concentrates to single‑serve sticks, to fit on‑the‑go lifestyles and expand usage occasions. Strong trade relationships secure premium shelf space in supermarkets and visibility on leading e‑commerce platforms, further amplifying consumer reach.

Innovation in natural, organic, and functional ingredient formulations

Innovation in natural, organic, and functional ingredient formulations is a pivotal driver of the water enhancer market, as consumers increasingly favor clean-label products made with recognizable, plant-based components and minimal artificial additives. Brands are reformulating concentrates with botanical extracts, fruit essences, and natural sweeteners to deliver authentic taste alongside perceived health and sustainability benefits. Data from the German Organic Food Industry Association (BÖLW) indicating that German consumers spent around EUR 16.99 billion on organic products in 2024 underscores the strength of demand for natural offerings and signals similar expectations in beverages [2]Source: German Organic Food Industry Association (BÖLW), "Industry Report", boelw.de . At the same time, companies are integrating functional ingredients such as electrolytes, vitamins, probiotics, and adaptogens to position enhancers as tools for energy, immunity, focus, and recovery rather than simple flavor boosters. This supports the broader shift toward preventive wellness, where shoppers want hydration solutions that contribute to overall physical and mental well-being.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer skepticism toward artificial sweeteners and flavors | -1.4% | Global, most pronounced in North America and Western Europe | Medium term (2-4 years) |

| Stringent regulatory requirements for food additives and health claims | -1.1% | Europe and North America, with spillover to Asia-Pacific markets adopting similar standards | Long term (≥ 4 years) |

| Fluctuating raw material costs for flavors and extracts | -0.8% | Global, with acute impact on smaller brands lacking hedging capacity | Short term (≤ 2 years) |

| Limited consumer awareness in developing regions | -0.6% | Asia-Pacific (excluding Japan, Australia), Middle East and Africa, and rural South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Consumer skepticism toward artificial sweeteners and flavors

Growing consumer skepticism toward artificial sweeteners and flavors acts as a notable restraint for the water enhancer market, as many shoppers question the long-term safety of synthetic ingredients such as aspartame, saccharin, and acesulfame-K. Media coverage of scientific studies linking certain high-intensity sweeteners to potential health risks has amplified concerns and reduced willingness to try new artificially sweetened products. Clean-label trends mean consumers increasingly scrutinize ingredient lists and avoid products with unfamiliar chemical names or “artificial flavor” declarations. This skepticism is particularly strong among health-conscious buyers who are switching back to sugar in moderation or seeking perceived safer, plant-based alternatives like stevia and monk fruit. As a result, water enhancers that rely heavily on synthetic sweeteners can face slower adoption, weaker repeat purchase rates, and greater pressure to reformulate.

Stringent regulatory requirements for food additives and health claims

Stringent regulatory requirements for food additives and health claims act as a significant restraint on the water enhancer market, as manufacturers must navigate complex approval processes, safety evaluations, and labeling rules before launching new formulations. Authorities closely scrutinize permitted sweeteners, colors, preservatives, and functional ingredients, which can delay innovation cycles and increase research and development and compliance costs. Claims related to hydration, energy, immunity, or cognitive support must be supported by robust scientific evidence, limiting the ability of brands to use bold marketing messages. Smaller companies and start-ups are particularly affected, as they often lack the resources to manage dossier preparation, clinical testing, and ongoing regulatory monitoring. Differences in standards across regions, such as between North America and the European Union, further complicate global rollouts and require separate reformulations or labels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Functional Formats Drive Premiumization

Flavored Drops held the largest share in the water enhancer market in 2025, commanding 45.02% of total revenue. This segment's popularity is driven by its appeal to mainstream consumers who prioritize taste enhancement in their hydration. The convenience of portable squeeze bottles, which fit easily into purses and gym bags, further boosts consumer preference. These products successfully address the common challenge of plain water’s blandness, encouraging higher water intake. Brands continue to innovate in flavor variety and sugar-free options to cater to diverse taste profiles and health-conscious trends. The widespread accessibility across retail and online channels solidifies the segment’s market dominance.

Workout and Fitness formulations are the fastest-growing segment, projected to expand at a CAGR of 10.12% through 2031. This growth surpasses the overall market average, driven by athletes and fitness enthusiasts seeking targeted recovery and hydration solutions. These formulations often include electrolyte blends and branched-chain amino acids (BCAAs), offering functional benefits beyond traditional sports drinks. Increasing health awareness and the desire for specialized nutrition during and after workouts contribute significantly to this surge. The segment capitalizes on a shift towards more personalized and performance-driven hydration products. This dynamic growth indicates a changing consumer landscape that favors scientifically formulated enhancers for active lifestyles.

By Distribution Channel: E-Commerce Disrupts Traditional Retail Dominance

Supermarkets and hypermarkets commanded the largest share of the water enhancer market in 2025, accounting for 55.62% of total revenue. This dominance is fueled by their widespread physical presence, high foot traffic, and ability to offer consumers an in-store experience including product sampling. These retail channels capitalize on the tactile shopping experience, which helps convert skeptical or first-time buyers into regular users. Their extensive product assortments and promotional activities further reinforce customer loyalty and drive repeat purchases. Additionally, supermarkets and hypermarkets benefit from their role as convenient one-stop destinations, where consumers can purchase water enhancers alongside other grocery items. This channel remains the backbone of water enhancer distribution due to its broad accessibility and brand variety.

Online retail stores are the fastest growing segment in the water enhancer market, projected to grow at a CAGR of 11.24% through 2031. This rapid growth is driven by innovative subscription models that secure recurring revenue streams and direct-to-consumer platforms that eliminate retailer margin costs. By bypassing traditional retail intermediaries, brands can reinvest savings into product development, marketing, and customer acquisition, fueling further expansion. The convenience and personalization offered by digital-first discovery and e-commerce channels appeal to younger, tech-savvy consumers who prefer shopping on mobile devices. Moreover, online platforms enable greater product variety and access to niche or premium formulations not always available in physical stores.

Geography Analysis

In 2025, North America dominated the global water enhancer market, securing 34.78% of total revenue. This leadership is largely attributed to heightened consumer demand for convenient hydration solutions in the United States and Canada. The region's prominence is bolstered by a strong health consciousness, a pervasive fitness culture, and a sophisticated retail infrastructure that champions premium flavored and functional enhancers. Major players, including PepsiCo and Nestlé, leverage this market maturity, ensuring their products are widely available in supermarkets and online platforms. Additionally, the increasing preference for on-the-go hydration options and the growing trend of personalized nutrition further contribute to the region's dominance.

South America, though smaller in scale, is on an upward trajectory, boasting a robust 5.52% CAGR through 2031. This growth is primarily driven by urbanization in Brazil and a surge in disposable incomes. As the middle class expands, there's a noticeable shift towards affordable, portable water enhancers, seen as healthier alternatives to sugary drinks. This trend underscores a broader movement towards healthier hydration choices amidst economic growth. Furthermore, the rising awareness of lifestyle diseases, such as diabetes and obesity, is encouraging consumers to opt for low-calorie and functional hydration products, further fueling market growth in the region. In 2024, Brazil reported approximately 16.6 million adults lived with diabetes, marking a prevalence rate of 10.6% among its adult population of 155.4 million, as per the International Diabetes Federation .

Europe stands as a significant player in the water enhancer market, with Germany accounting for about 25% of regional sales, thanks to its robust retail networks and a growing wellness trend. Other nations, including the United Kingdom, France, Italy, and Spain, are witnessing a surge in the adoption of flavored drops and fitness-oriented formulations, a trend further amplified by the rise of e-commerce. The increasing focus on fitness and wellness, coupled with the availability of innovative product offerings, is driving demand across the region. Meanwhile, the Middle East and Africa showcase steady growth potential. In Saudi Arabia, affluent urbanites are gravitating towards imported premium enhancers, a choice driven by the region's arid climate and hydration needs. Additionally, a regulatory push for low-sugar products is facilitating market penetration, even as distribution channels remain heavily skewed towards modern trade. The growing influence of international brands and the introduction of region-specific flavors are also contributing to the market's gradual expansion in this region.

Regulatory Landscape

Water enhancers are regulated mainly through ingredient-level frameworks for food additives, flavorings, colors, and claims, rather than through a dedicated product-category approval. In the United States, 21 CFR Part 170 sets the basis for whether substances added to food must be covered by a food additive regulation or are Generally Recognized as Safe (GRAS), so manufacturers need to align formulations and labeling with FDA expectations for ingredient safety and with permissible claims for functional variants (for example, electrolyte, energy, or vitamin positioning).

In the European Union, compliance is anchored in list-based authorizations and labeling rules for additives and flavorings, including Regulation (EC) No 1333/2008 (additives, including functional class declaration) and the common authorization procedure under Regulation (EC) No 1331/2008. In January 2026, the European Commission updated the Union flavorings lists via Commission Regulation (EU) 2026/175 (adding hesperetin dihydrochalcone) and Commission Regulation (EU) 2026/172 (adding 3-[3-(2-isopropyl-5-methyl-cyclohexyl)-ureido]-butyric acid ethyl ester), which reinforces that water enhancer brands need to verify each flavoring component against current Union listings when launching or reformulating in Europe.

Value Chain Analysis

The water enhancer value chain starts with suppliers of sweeteners (including high-intensity and plant-derived options), flavors and botanical extracts, acids, colors, preservatives, and functional actives such as electrolytes, vitamins, and amino-acid blends used in workout and fitness formulations. These inputs then move to formulators and contract manufacturers that blend and stabilize concentrates (drops) and dry mixes (stick packs and powders), followed by packaging converters that provide small-format squeeze bottles, droppers, and single-serve sachets designed for portability and dosing accuracy.

Brand owners route finished goods through distributors and modern trade, with supermarkets and hypermarkets remaining an important volume channel, while direct-to-consumer and online marketplaces support assortment depth and subscription replenishment. Value capture centers on flavor system development, clean-label reformulation capability, and regulatory and claims substantiation, particularly for functional SKUs. Recurring bottlenecks include additive and claim compliance complexity, ingredient cost volatility for flavors and extracts, and packaging scrutiny tied to plastics and on-the-go formats. In January 2026, the EU updated flavorings lists via Commission Regulation (EU) 2026/175 and 2026/172, affecting flavor-system development across the supply chain.

Competitive Landscape

The water enhancer market exhibits moderate fragmentation, where global giants such as PepsiCo Inc., Nestlé S.A., The Coca-Cola Company, and The Kraft Heinz Company command significant shelf space and marketing budgets through established brand strength and extensive distribution networks. These incumbents leverage scale to dominate hypermarkets, supermarkets, and online platforms, capturing substantial shares via iconic products like MiO from Kraft Heinz and Propel from PepsiCo. Their competitive advantages include robust research and development for flavor innovation and partnerships with retailers for prime visibility. However, no single player holds outright dominance, allowing a diverse ecosystem of mid-sized firms and regional specialists to thrive. This structure fosters healthy rivalry while enabling market expansion through varied consumer touchpoints.

Incumbents deploy a dual strategy of portfolio breadth and innovation velocity to maintain leadership amid fragmentation. PepsiCo and Coca-Cola expand offerings across flavored drops, fitness blends, and zero-sugar variants to cover mainstream and niche demands. Nestlé emphasizes functional enhancers with vitamins and electrolytes, aligning with health trends through targeted campaigns. Kraft Heinz focuses on convenience formats like portable squeezes, bolstered by subscription models on e-commerce sites. These firms invest heavily in digital marketing and influencer partnerships to accelerate product launches and consumer trials.

Smaller entrants carve profitable niches by targeting underserved segments such as organic, plant-based, or adaptogen-infused formulations that appeal to wellness-focused consumers. Startups differentiate through sustainable packaging and transparent sourcing, gaining traction in online retail where agility trumps scale. Regional brands in Asia-Pacific and emerging markets exploit local tastes with culturally resonant flavors unavailable from giants. Private labels from discounters further fragment the space by offering affordable alternatives. This dynamic rewards innovation in high-growth areas like natural ingredients, which grow faster than synthetics.

Water Enhancer Industry Leaders

-

The Coca-Cola Company

-

The Kraft Heinz Company

-

PepsiCo, Inc.

-

Eau Exquise

-

Nestlé S.A.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Functional hydration is extending into adjacent use-cases between classic water enhancers and sports nutrition, creating room for electrolyte powders, vitaminized hydration, and higher-utility formats that travel well. In July 2026, AMASS Brands Group launched AMASS Electrolyte Powder Mixers in 16-count stick packs with low-calorie positioning and B-vitamins, showing continued product development around portable powders that compete for the same occasions as liquid drops while widening the addressable base beyond at-home use.

The opportunity set also includes more differentiated flavor profiles and crossovers with other functional beverage concepts, along with ongoing efforts by large brand owners to renovate legacy brands with functional claims and cleaner labels. In the EU, continued list-based updates for flavorings (Commission Regulation (EU) 2026/175 and 2026/172) and ongoing additive scrutiny support reformulation roadmaps that emphasize approved ingredients, transparent labeling, and tighter claim discipline, which can benefit players with regulatory capability and faster commercialization across multiple regions.

Recent Industry Developments

- May 2026: The Kraft Heinz Company launched Kool-Aid Hydration, single-serve electrolyte powder sticks positioned with zero sugar and no artificial dyes in three flavors. This extends a legacy flavor brand into a format and functional space that directly overlaps with water enhancers and stick-pack hydration mixes, increasing competitive intensity in retail aisles where portability and clean-label cues support trial.

- October 2025: The Coca-Cola Company launched Power Water, a functional flavored water with defined electrolyte content (520 mg sodium and 150 mg potassium) offered in multiple bottle sizes. The launch strengthens Coca-Cola's participation in functional hydration occasions that also bring users into enhancer-led routines, and planned wider distribution including Amazon adds pressure on brands that rely heavily on online discovery.

- December 2024: Ocean Spray Cranberries, Inc. partnered with Dyla Brands to launch powdered-format water enhancers. This collaboration broadened Ocean Spray's presence beyond ready-to-drink into customizable hydration, and it reinforced powder as a scalable format for brands seeking shelf-stable distribution and wider flavor-driven line extensions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers consumer water enhancers sold as concentrated drops or similar formats that are added to plain water to deliver flavor or functional benefits (such as energy, fitness support, or hydration).

Scope exclusions: It excludes ready-to-drink flavored or functional beverages that do not require the user to mix the product into water.

Segmentation Overview

-

By Product Type

- Energy Drops

- Workout and Fitness (Electrolyte/BCAA)

- Flavored Drops

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail Stores

- Other Distribution Channels

-

By Region

-

Noth America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Rest of Middle East and Africa

-

Noth America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the category boundaries, build the initial demand story, and anchor the model to real-world indicators that are available publicly. We leaned on sources such as the US Department of Agriculture for food category context, the US Food and Drug Administration for labeling and ingredient compliance cues, and trade statistics portals such as UN Comtrade to understand packaging and ingredient trade flows that can correlate with concentrate formats.

To keep the sizing logic practical, we also reviewed company annual reports, investor decks, and earnings call notes where category growth, channel focus, and pricing actions were discussed. Patent databases were scanned to understand the pace of formulation activity (sweeteners, electrolytes, vitamins), and a news and financials subscription was used to track launches and distribution expansion signals across regions. The sources listed here are illustrative, and many other public references were also used for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary inputs were used to pressure test the market definition, confirm which products buyers treat as water enhancers, and verify how pricing typically changes by pack size and channel. We spoke with a mix of brand-side teams, ingredient and contract manufacturing participants, and distribution-facing stakeholders, and then compared views across APAC, EMEA, and the Americas so regional adoption and channel mix could be checked against what respondents described in-market.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 17% | APAC: 44% |

| Mid tier: 40% | Functional/Unit leaders: 28% | EMEA: 29% |

| Smaller Players: 22% | Managers: 55% | Americas: 27% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where the flavored and functional concentrate demand pool is reconstructed using region-level retail channel splits and the expected penetration of enhancer usage in at-home and on-the-go hydration routines, and then expressed in value terms through typical price ladders. We then corroborate totals with selective bottom-up checks, such as sampled SKU price points across key channels and supplier-side sense checks on volumes, which helps adjust for gaps in distribution coverage.

A few inputs matter most in this market, and we used them as recurring checks during modeling. These include channel mix shifts (especially online retail versus supermarkets), average selling price movement by pack size, the sweetener and functional ingredient mix that influences cost and shelf pricing, the share of flavored drops versus energy and workout formats, and region-level adoption differences linked to low sugar preferences. Forecasts were run using scenario analysis, where base case assumptions on channel growth, pricing progression, and mix shift were aligned to what primary respondents described as the most likely path, and then stress tested for faster or slower premiumization.

Data Validation & Update Cycle

Outputs were validated through multiple passes that compare model results with independent signals such as channel growth patterns, observed price ranges, and mix shifts across product types. When a region or channel result looked off, the assumptions were revisited, outliers were inspected, and clarifying questions were sent back to selected interviewees before sign-off.

Reports are refreshed annually, and interim updates are made when material events change demand or pricing direction. Before delivery, we conduct a final review pass so the numbers reflect the latest available inputs and any newly confirmed market signals.

Mordor Intelligence's Water Enhancer Market Size Compared Against Other Published Estimates

Published market sizes for water enhancers can look different even when they are describing the same consumer behavior, because the product boundary and the base year do not always match. Differences also show up when some studies mix in adjacent ready-to-drink beverages, or when pricing is projected using a straight CAGR without checking channel-level price ladders.

The main gap drivers here are scope and timing, since some estimates anchor on 2024 revenue while others use 2025, and currency conversion timing can also shift the reported value for markets with volatile exchange rates. Another practical difference is how e-commerce is treated, because some models apply an aggressive online growth curve across all regions, while others keep it closer to observed channel share change. This is the basis for how the approach was kept tied to channel mix checks and product-type splits in the view attributed to Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.25 B (2026) | |

| Global Consultancy A | USD 3.80 B (2025) | Uses an earlier base year and a slightly different scope emphasis around ingredient groupings, which can shift what is counted as an enhancer versus an adjacent functional drink mix. |

| Industry Publisher B | USD 2.90 B (2024) | Anchors on 2024 and uses broader product-type buckets, where some formulations and forms may be counted differently, and exchange-rate timing is not always clear across regions. |

The table shows that a one to two year base-year shift explains a meaningful part of the spread, and the rest mainly comes from what gets included as a water enhancer and how channel mix is carried forward. By keeping the model traceable to product-type splits, channel shares, and realistic price ladders, the final view stays repeatable and easier to reconcile when new data points arrive.

Key Questions Answered in the Report

What is the projected value of the water enhancer market in 2031?

The market is forecast to reach USD 6.65 billion by 2031.

How fast is the water enhancer market expected to grow?

The market is expanding at a 9.33% CAGR over the 2026-2031 period.

Which product type currently leads sales?

Flavored Drops hold 45.02% of 2025 revenue.

Which distribution channel is growing the fastest?

Online Retail Stores are advancing at 11.24% CAGR through 2031.

Page last updated on: