Astaxanthin Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

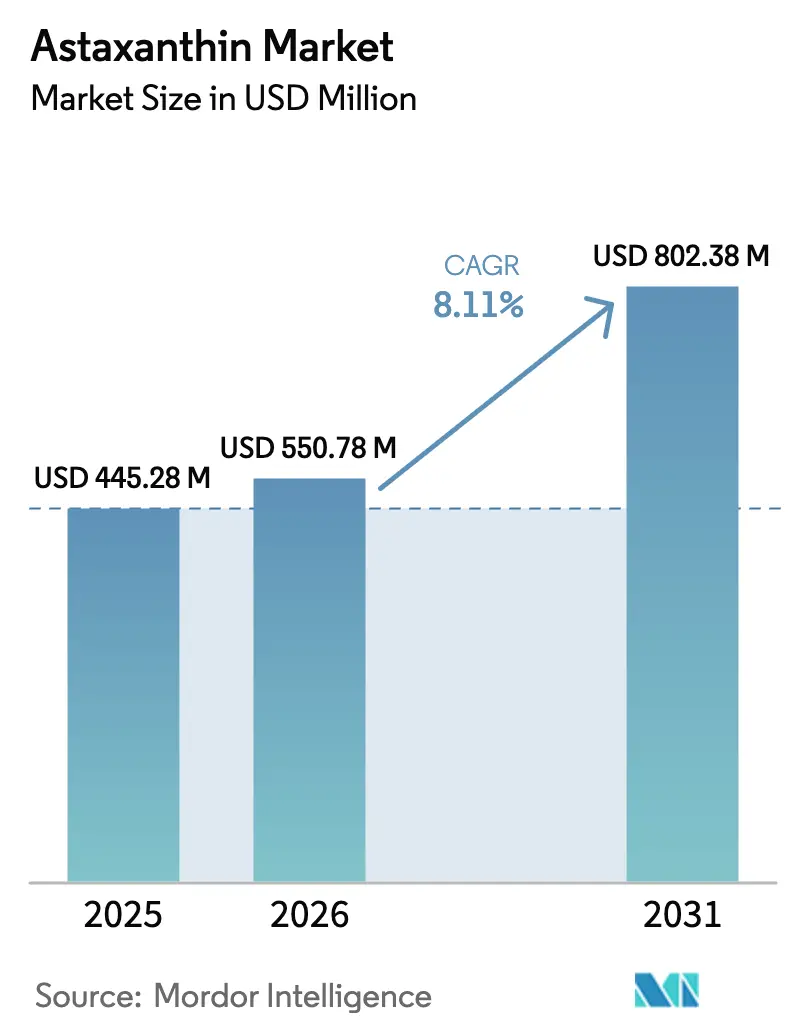

| Market Size (2026) | USD 550.78 Million |

| Market Size (2031) | USD 802.38 Million |

| Growth Rate (2026 - 2031) | 8.11% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Astaxanthin Market Analysis by Mordor Intelligence

The astaxanthin market size is valued at USD 550.78 million in 2026, growing from the 2025 value of USD 445.28 million, and is forecast to climb to USD 802.38 million by 2031, advancing at a 8.11% CAGR. Demand momentum is anchored in a global consumer shift toward microalgae-derived carotenoids, regulatory bans on synthetic variants in foods, and continuous clinical validation that favorably compares natural stereoisomers with synthetic counterparts. Price premiums for natural grades remain resilient despite a seven-fold cost differential, as formulators rely on documented bioavailability advantages. Meanwhile, production innovations such as two-stage cultivation protocols deliver yield gains that temper the cost pressure. Competitive strategies revolve around supercritical CO₂ extraction, beadlet and liposomal delivery systems, and multi-ingredient synergies that allow finished-product differentiation across supplements, cosmetics, and functional foods. Geographically, Europe retains leadership through stringent Novel Food approvals, Asia-Pacific delivers the fastest incremental revenue, and North America capitalizes on early Generally Recognized As Safe (GRAS) status.

Key Report Takeaways

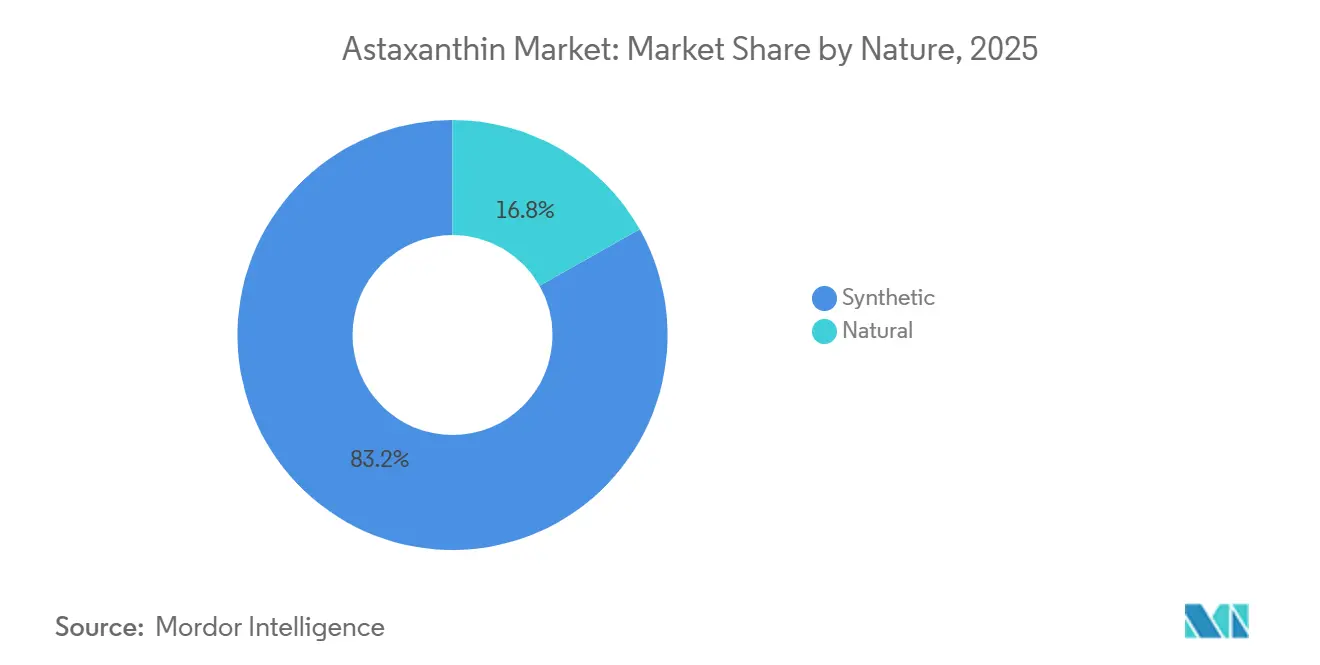

- By nature, synthetic held 83.18% of the astaxanthin market share in 2025, whereas natural grades are forecast to expand at a 9.24% CAGR to 2031.

- By form, powders captured 72.34% of the astaxanthin market size in 2025, while liquid formats are projected to grow at 9.55% CAGR through 2031.

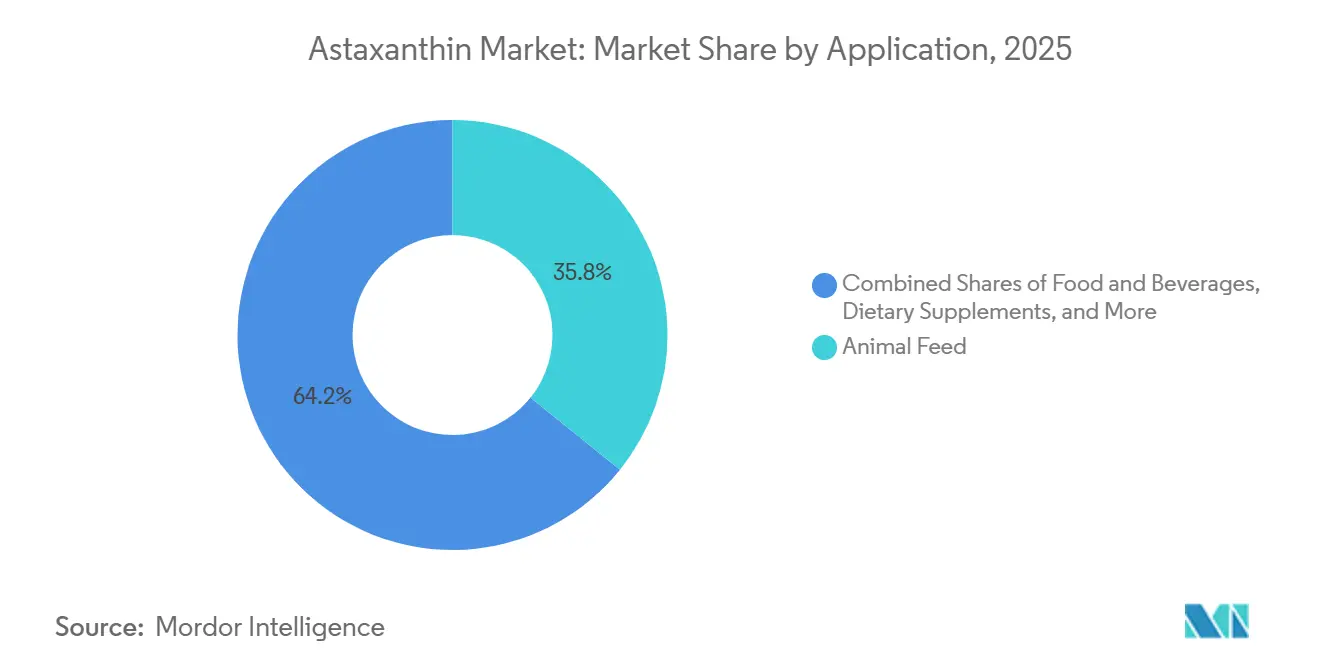

- By application, animal feed accounted for 35.78% of the astaxanthin market size in 2025, and dietary supplements are advancing at a 10.05% CAGR to 2031.

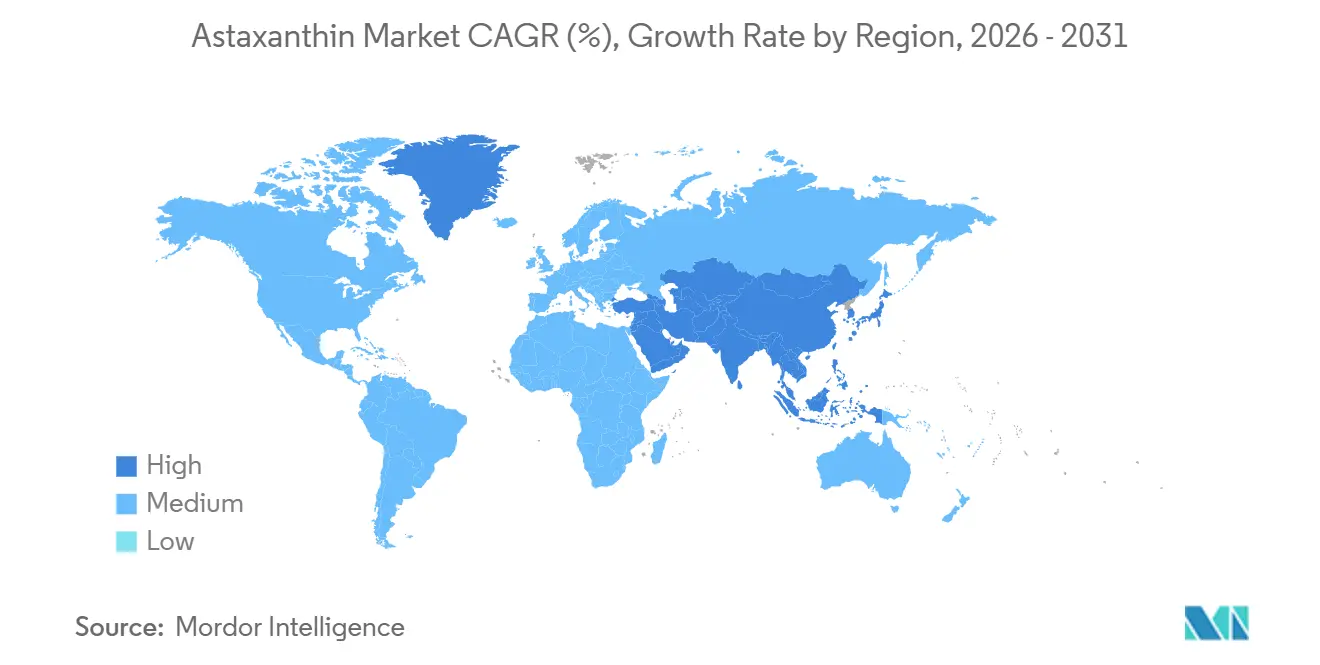

- By geography, Europe commanded 35.24% revenue share in 2025, whereas Asia-Pacific is poised for the quickest expansion at 9.78% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Astaxanthin Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Preventive Healthcare and Increasing Demand for Anti-Aging Products | +1.8% | Global, with concentration in North America, Europe, and urban Asia-Pacific markets | Medium term (2-4 years) |

| Rising Consumer Awareness of Astaxanthin's Antioxidant Benefits for Skin, Eye, and Heart Health | +1.5% | Global, particularly Japan, North America, and Western Europe with aging populations | Long term (≥ 4 years) |

| Preference for Natural Microalgae-Derived Astaxanthin Over Synthetics | +1.2% | Europe (regulatory-driven), North America, and premium segments in Asia-Pacific | Long term (≥ 4 years) |

| Technological Advances in Extraction Improving Bioavailability and Yields | +0.9% | Global, led by innovation hubs in Europe, North America, and Japan | Medium term (2-4 years) |

| Rising Sports Nutrition Use for Recovery and Inflammation Reduction | +1.0% | North America, Europe, and urban centers in China and India | Short term (≤ 2 years) |

| Consumer Shift Towards Clean-Label, Non-GMO Ingredients | +0.8% | North America and Europe; emerging in Asia-Pacific premium segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Preventive Healthcare and Increasing Demand for Anti-Aging Products

With aging demographics and growing health awareness, consumers are increasingly adopting astaxanthin as a preventive solution rather than a reactive supplement. A randomized controlled trial conducted in February 2025 revealed that consuming 4 milligrams of natural astaxanthin daily for 9 weeks significantly reduced UV-induced skin damage and prolonged time-to-sunburn, establishing the compound as an "internal sunscreen" that complements topical products. This clinical evidence is driving advancements in beauty-from-within formulations. Astaxanthin's ability to penetrate cellular membranes provides oxidative protection at the mitochondrial level, distinguishing it from surface-acting antioxidants. Additionally, the anti-aging market benefits from research showing that a 12-week intake of 12 milligrams daily improved cognitive performance in middle-aged and elderly individuals experiencing age-related memory decline, broadening its applications beyond dermatology. Regulatory support includes the FDA's 1999 approval of astaxanthin as a dietary supplement and its 2010 GRAS designation for Haematococcus pluvialis-derived astaxanthin, which has facilitated its adoption in functional foods and beverages targeting preventive health.

Rising Consumer Awareness of Astaxanthin's Antioxidant Benefits for Skin, Eye, and Heart Health

Consumer education campaigns are showcasing astaxanthin's multi-system benefits, fueling demand across cosmetics, nutraceuticals, and functional foods. A double-blind, placebo-controlled trial involving 64 schoolchildren aged 10 to 14, each with over 4 hours of daily screen time, administered 4 milligrams of AstaReal astaxanthin daily for 84 days. The study revealed a 20 percent improvement in computer vision syndrome scores and a 27 percent reduction in visual fatigue compared to the placebo group. Additionally, significant improvements were observed in stereopsis and pupillary light reflex. With the global increase in digital device usage, this pediatric efficacy data highlights a valuable new demographic segment. Cardiovascular benefits are supported by meta-analyses: 12 milligrams daily for 24 weeks reduced fibrinogen levels in prediabetic and high-cholesterol individuals. Moreover, an 8-week supplementation at the same dosage lowered blood pressure and improved vascular markers in postmenopausal women. Astaxanthin's antioxidant potency, reported to be over 100 times that of alpha-tocopherol in specific assays, along with its unique ability to cross lipid bilayers and protect both hydrophilic and lipophilic cellular compartments, distinguishes it from conventional antioxidants. This differentiation not only emphasizes its effectiveness but also validates its premium pricing among health-conscious consumers.

Preference for Natural Microalgae-Derived Astaxanthin Over Synthetics

Regulatory and bioavailability differences are driving a shift in preference toward natural sources, even with a cost premium that can exceed sevenfold. Synthetic astaxanthin contains stereoisomers absent in nature and demonstrates lower bioavailability and stability. The European Union's Regulation No. 1925/2006 prohibits synthetic astaxanthin in food applications, and in the United States, it does not have GRAS status for direct human consumption. Natural astaxanthin, primarily the all-E-3S,3′S stereoisomer derived from Haematococcus pluvialis, is often esterified with fatty acids. This enhances intracellular stability and may improve absorption, enabling a price premium in nutraceutical and cosmetic formulations. Certification trends support this preference: In May 2025, Algatech's AstaPure brand announced Non-GMO Project verification, USDA Organic, Kosher, and Halal certifications. Similarly, Algalif and Nutrex Hawaii's BioAstin have comparable third-party validations that align with clean-label consumer demands. While Europe and North America lead in prioritizing natural-source claims, this trend is expanding into premium segments in China and India, driven by rising disposable incomes and increasing health awareness.

Technological Advances in Extraction Improving Bioavailability and Yields

Innovations in extraction and formulation are overcoming the challenges of astaxanthin, such as its poor water solubility, sensitivity to light and oxygen, and low oral bioavailability. Techniques like supercritical CO2 extraction, enzymatic methods, and advanced encapsulation platforms are driving these advancements. Supercritical CO2 extraction, particularly with ethanol as an entrainer, has emerged as the preferred method for natural astaxanthin. This approach avoids organic solvent residues, retains the all-E stereoisomer configuration, and selectively extracts esterified forms known for their improved stability. According to the International Journal of Pharmaceutics, downstream encapsulation techniques, such as liposomes, PLGA nanoparticles, chitosan complexes, and cyclodextrin inclusion compounds, have enhanced bioavailability by 40 to 70% in comparative studies[1]Source: ScienceDirect, "Delivery systems for astaxanthin: A review on approaches for in situ dosage in the treatment of inflammation associated diseases", sciencedirect.com. Additionally, lipid-based formulations have shown 1.7 to 3.7 times higher absorption compared to reference preparations. In November 2024, Divi's Laboratories and Algalif launched AstaBead, a highly concentrated astaxanthin beadlet available in 5% and 2.5% concentrations, designed to improve stability and simplify formulation in tablets and capsules. Furthermore, two-stage cultivation protocols have revolutionized astaxanthin production. By separating green vegetative growth from the red, stress-induced phase, Haematococcus pluvialis has achieved astaxanthin contents of up to 38% of its dry cell weight. This represents a significant improvement over the typical range of 1.9 to 7.0%, reducing downstream extraction costs per kilogram of active ingredient.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Chain Vulnerabilities in Algal Cultivation Due to Climate Factors | -0.7% | Global, with acute exposure in outdoor cultivation regions (China, Hawaii, Israel) | Short term (≤ 2 years) |

| Stringent Regulations on Purity, Labeling, and Novel Food Approvals | -0.5% | Europe (Novel Food), China (regulatory approvals), emerging markets with evolving frameworks | Long term (≥ 4 years) |

| High Production Costs of Natural Astaxanthin | -0.9% | Global, affecting all natural-source producers; most acute in high-cost regions (Europe, North America) | Medium term (2-4 years) |

| Raw Material Price Fluctuations for Algae Feedstocks | -0.6% | Global, with exposure to energy, water, and nutrient input costs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Supply Chain Vulnerabilities in Algal Cultivation Due to Climate Factors

Haematococcus pluvialis cultivation is sensitive to temperature, light intensity, and water quality, making it vulnerable to climate variability that can disrupt production schedules and yield consistency. A European Union report on algae cultivation noted that outdoor open-pond systems are at risk of contamination from competing microorganisms. In contrast, photobioreactor systems, while more controlled, demand substantial energy for temperature regulation and mixing. Depending on the scale and system type, production costs for these systems can range from approximately USD 38 to USD 111 per kilogram of dry biomass, according to the European Commission[2]Source: European Commission, “Algae Cultivation and Production in Europe,” op.europa.eu. Climate-related disruptions to algal cultivation are manifold: extreme temperatures can stifle algal growth, regions like Israel's Arava desert and China's Yunnan province face water scarcity, and unseasonably warm periods see a spike in contamination events. The cultivation process, which involves a two-stage protocol first, green vegetative growth, followed by nutrient deprivation and high-light stress to boost astaxanthin accumulation, extends production cycles over several weeks. This prolonged cycle heightens vulnerability to weather variability and increases the risk of batch failures. The concentration of supply further amplifies this vulnerability. BGG World's facility in Yunnan, which doubled its capacity in May 2025, has now become the world's largest site for natural astaxanthin production. This centralization poses a significant risk, as it stands as a single point of failure for a large portion of the global supply. To counter these challenges, industry players are exploring several mitigation strategies. These include diversifying production geographically, transitioning to closed photobioreactor systems equipped with climate control, and pioneering heterotrophic cultivation methods that rely on organic carbon sources instead of traditional photosynthesis. However, it's worth noting that while heterotrophic methods show promise, they remain in the pilot stage and have yet to reach commercial cost-competitiveness.

Stringent Regulations on Purity, Labeling, and Novel Food Approvals

Regulatory pathways for natural astaxanthin vary widely across jurisdictions, creating challenges such as market entry barriers and compliance costs. These issues primarily benefit established players with robust regulatory dossiers, while delaying new entrants. In the European Union, astaxanthin derived from Haematococcus pluvialis requires Novel Food authorization. BGG World is notably the only brand with two EU Novel Food approvals for different extraction methods, providing a regulatory advantage that restricts competition in European markets. In China, Novel Food status was granted to Haematococcus pluvialis astaxanthin in 2010. However, the approval process for new suppliers and extraction methods remains unclear and lengthy, causing uncertainty for international entrants. Additional complexity arises from purity standards and labeling requirements, as products must disclose stereoisomer composition, esterification status, and the source organism. Health claims also require clinical trial validation, with costs ranging from USD 500,000 to USD 2 million per indication. In the United States, the FDA granted GRAS status to Haematococcus pluvialis-derived astaxanthin in 2010. This status applies exclusively to natural sources, excluding synthetic astaxanthin, resulting in a segmented market. While natural producers benefit from regulatory protections, they face higher production costs. Emerging markets, including India, Brazil, and Southeast Asian countries, are establishing their own regulatory frameworks for microalgae-derived ingredients. However, the lack of harmonization across jurisdictions increases compliance costs and slows the global expansion of producers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Nature: Natural Gains Ground Despite Synthetic Dominance

In 2025, synthetic grades held 83.18% of the astaxanthin market share, driven by the aquaculture feed industry's demand for cost-efficient pigments in bulk quantities. However, natural grades are expected to surpass the overall category with a projected 9.24% CAGR through 2031, as dietary supplements, cosmetics, and premium functional foods increasingly adopt microalgae sourcing. Natural batches are priced between USD 1,650 and 7,220 per kilogram, compared to USD 950 for synthetic materials. Nonetheless, regulatory bans on synthetic use in European foods and the absence of GRAS status in the U.S. provide a competitive edge for natural producers. Clean-label trends are accelerating the shift toward natural products in the Asia-Pacific's premium segments. At the same time, yeast-derived and genetically engineered microbial methods remain technically viable but are still in the early stages commercially, limited by low yields and regulatory concerns regarding GMOs in human nutrition.

A feedback loop between clinical research and consumer perception is driving the adoption of natural products. Brands emphasize the all-E-3S,3'S configuration, which aligns with human plasma studies, to support claims of superior bioavailability and oxidative stability. Retailers are allocating more shelf space to natural SKUs, particularly in e-commerce platforms where algorithms prioritize products with high conversion rates. Consequently, the astaxanthin market is transitioning toward natural sources, even as synthetic variants retain their role in aquaculture pigmentation.

By Form: Liquid Formulations Accelerate on Bioavailability Gains

Powders captured 72.34% of the astaxanthin market in 2025 due to compatibility with tablets, capsules, and feed premixes that require bulk density and long shelf life. Liquids are forecast to climb at 9.55% CAGR through 2031 as nanoemulsions, liposomes, and oil suspensions demonstrate 1.7-3.7-fold higher uptake in pharmacokinetic studies. Liquid softgels allow precise pediatric and geriatric dosing, evidenced by school-age studies employing liquid formats to reduce computer vision strain. Beadlet innovation within the powder sub-segment, Divi’s/Algalif’s AstaBead, delivers enhanced flowability and oxidative protection while preserving manufacturability.

Form-factor choice increasingly aligns with channel strategy. Sports nutrition brands favor single-serve liquid shots for post-workout convenience, whereas mass-market multivitamins rely on powder-based blends for cost optimization. Given rising evidence linking delivery technology to efficacy, formulators prioritize absorption-enhanced formats, a consideration that tips incremental share toward liquid solutions even if powders remain dominant.

By Application: Dietary Supplements Surge as Aquaculture Plateaus

Animal feed represented 35.78% of the astaxanthin market size in 2025, anchored by more than 1 million tonnes of Atlantic salmon production annually that requires pigmentation for consumer acceptance. Yet dietary supplements are projected to deliver the fastest growth at a 10.05% CAGR through 2031, propelled by expanding clinical dossiers, aging populations, and influencer-led adoption. Cosmetic uses rise on evidence of skin moisture retention and elasticity gains, and functional beverages experiment with low-dose inclusions for eye-health or recovery claims.

Pharmaceuticals remain exploratory, focusing on inflammatory bowel disease and neuroprotection, but regulatory pathways and dosage economics temper near-term revenue contribution. Supplement acceleration reflects converging trends: self-directed wellness, wearable health data, and retail migration to e-commerce. AstaReal’s pediatric vision study exemplifies how targeted trials create entirely new addressable cohorts. Meanwhile, multi-ingredient stacks blending astaxanthin with tocotrienols, lutein, or collagen unlock formulation synergies that sustain price premiums and support repeat purchases.

Geography Analysis

Europe secured 35.24% of global revenue in 2025, benefiting from a regulatory environment that bans synthetic astaxanthin in food and enforces Novel Food approval for natural variants. High health literacy and robust supplement channels in Germany, the United Kingdom, France, and the Netherlands strengthen volume growth, while premium pricing prevails due to certification stacking. Regulatory hurdles create defensive moats for incumbents that have secured dual extraction-method approvals.

Asia-Pacific is projected to record a 9.78% CAGR between 2026 and 2031, outpacing all other regions. China drives supply, with BGG’s May 2025 doubling of its Yunnan photobioreactor farm cementing its status as the largest natural producer globally. Japan remains a consumption pioneer, while India posts rapid demand gains aligned with rising disposable income and growing preventive-health awareness. Although synthetic grades dominate aquaculture in Southeast Asia, premium supplement uptake signals future migration toward natural inputs.

North America leverages early GRAS status to broaden application breadth across supplements, beverages, and cosmetics. Cyanotech’s Hawaiian operation supplies BioAstin, which contributed 65% of its USD 24.215 million net sales in fiscal 2025, underscoring single-product revenue reliance[3]Source: Cyanotech Corporation, “Fiscal Year 2025 Financial Results,” cyanotech.com. Regulatory clarity and widespread retail distribution support consistent demand, albeit tempered by cost sensitivity in mass channels. South America and Middle East and Africa remain nascent but promising as regulatory frameworks mature and urban middle-class populations seek clean-label nutraceuticals.

Competitive Landscape

The astaxanthin market is characterized by moderate fragmentation, with competition intensifying between well-established companies and emerging biotechnology firms. Leading players such as Cyanotech Corporation, Beijing Ginko Group, ENEOS Holdings, Inc., and BASF SE maintain their dominance by leveraging advanced production capabilities and extensive distribution networks, ensuring a strong foothold in the market.

Global players utilize their significant resources and international presence to dominate the market, while regional companies capitalize on their in-depth local expertise and tailored product offerings to secure competitive advantages. These key players are instrumental in driving the industry's growth through their specialized capabilities and well-crafted market strategies. On the other hand, smaller firms focus on carving out niches by offering natural variants and targeting specialized applications, enabling them to establish unique market positions despite the presence of larger competitors. Many companies are increasingly adopting vertical integration strategies, investing heavily in microalgae cultivation and formulation processes to gain better control over their supply chains and enhance operational efficiency.

Market participants are actively pursuing growth through various initiatives, including facility expansions, mergers and acquisitions, and innovative product development. Additionally, they are prioritizing strategic investments, market consolidation, and portfolio optimization to strengthen their competitive positions. A growing emphasis on sustainability is evident across the industry, as companies increasingly align their operations and strategies with environmentally responsible practices, as highlighted by recent developments.

Astaxanthin Industry Leaders

-

Cyanotech Corporation

-

Beijing Ginko Group

-

ENEOS Holdings, Inc.

-

BASF SE

-

dsm-firmenich

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Algalif, an Icelandic producer of natural astaxanthin from microalgae, has introduced Astalíf™ 15, the world's first 15% natural astaxanthin oleoresin. The ingredient is suitable for functional foods, gummies, beverages, and skincare due to its potent antioxidant properties.

- June 2025: BGG, the global leader in natural astaxanthin from Haematococcus pluvialis microalgae, has expanded its manufacturing facility in Yunnan Province, China. The plant claims to have a full value chain from farming, extraction, drying, packaging, and research and development.

- May 2024: US-based Divi's Nutraceuticals launched AstaBead, a product of sustainable natural astaxanthin beadlets, at Vitafoods 2024 in Switzerland. AstaBead is a collaboration between Divi’s and Algalif and uses Algalif's Iceland-based production process that uses 100% renewable energy.

- February 2024: AstaReal, a Swedish astaxanthin company, announced that it had rebranded its Astaxin Original product and plans to launch a vegan version in Europe in the near future. AstaReal also gave nutraceutical companies a first look at the rebranded product at Fi Europe in Frankfurt at the end of 2023.

Global Astaxanthin Market Report Scope

Astaxanthin is a blood-red pigment and is produced naturally in the freshwater microalgae Haematococcus pluvialis and the yeast fungus Xanthophyllomyces dendrorhous, among others. When algae are stressed by a lack of nutrients, increased salinity, or excessive sunshine, it creates astaxanthin. The global astaxanthin market is segmented by type into natural and synthetic. By form, the market is segmented into liquid and power. By application, the market is segmented into food and beverage, dietary supplements, animal feed, cosmetics, and other applications. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The market sizing has been done in value terms (USD) for all the abovementioned segments.

| Natural |

| Synthetic |

| Powder |

| Liquid |

| Food and Beverages |

| Dietary Supplements |

| Animal Feed |

| Personal Care and Cosmetics |

| Pharmaceuticals |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| Rest of Middle East and Africa |

| Nature | Natural | |

| Synthetic | ||

| Form | Powder | |

| Liquid | ||

| Application | Food and Beverages | |

| Dietary Supplements | ||

| Animal Feed | ||

| Personal Care and Cosmetics | ||

| Pharmaceuticals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast value of the astaxanthin market by 2031?

The astaxanthin market is projected to reach USD 802.38 million by 2031, reflecting an 8.11% CAGR over 2026-2031.

Which region leads global consumption?

Europe held 35.24% of global revenue in 2025, driven by regulatory bans on synthetics and strong supplement uptake.

Why are liquid astaxanthin formats gaining traction?

Nanoemulsions, liposomes, and oil suspensions deliver 1.7-3.7-fold higher bioavailability than powder, justifying premium pricing and accelerating adoption.

Which application segment is growing fastest?

Dietary supplements are expanding at a 10.05% CAGR through 2031 as clinical evidence broadens consumer demographics and supports higher daily dosages.

Page last updated on: