Health And Wellness Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

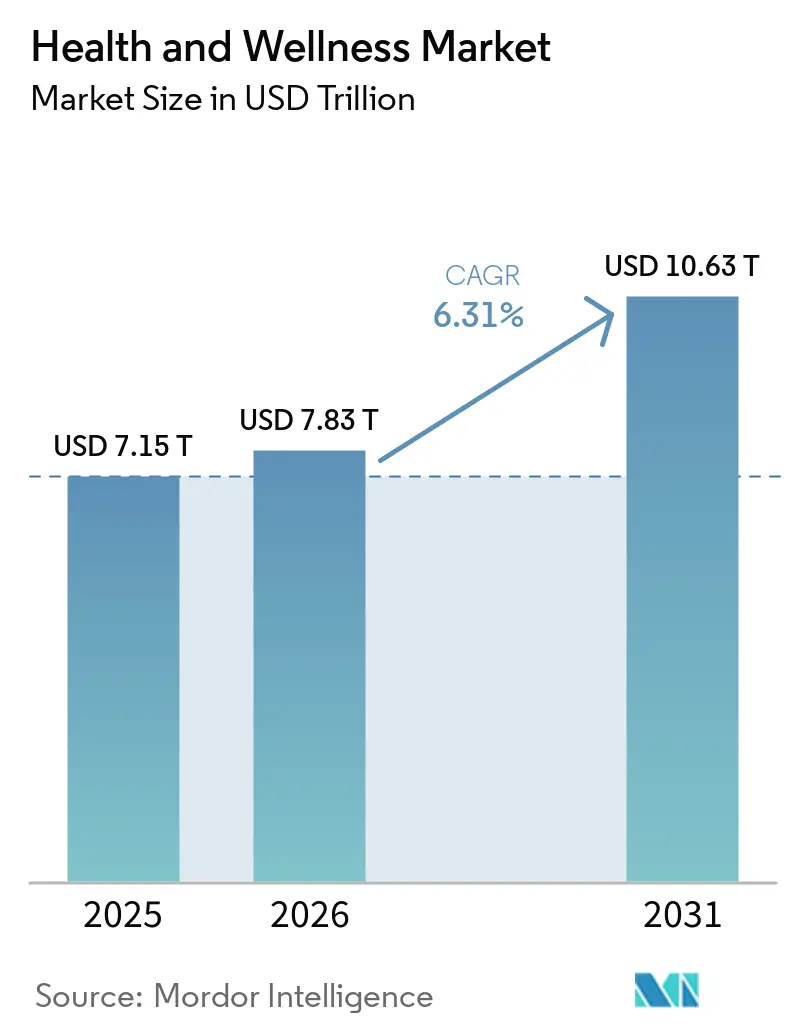

| Market Size (2026) | USD 7.83 Trillion |

| Market Size (2031) | USD 10.63 Trillion |

| Growth Rate (2026 - 2031) | 6.31% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

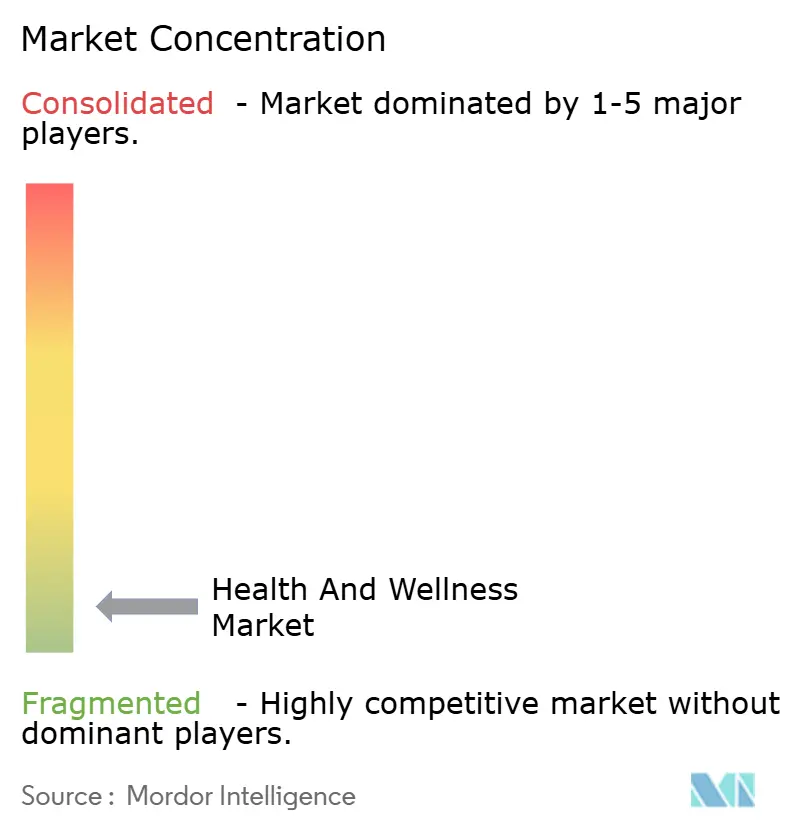

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Health And Wellness Market Analysis by Mordor Intelligence

The health and wellness market size is expected to grow from USD 7.15 trillion in 2025 to USD 7.83 trillion in 2026 and is forecast to reach USD 10.63 trillion by 2031 at a 6.31% CAGR over 2026-2031. The global health and wellness market is driven by a significant shift in consumer lifestyles toward preventive healthcare, balanced nutrition, fitness, and mental well-being. Growing awareness of chronic diseases, stress-related disorders, obesity, and immunity has prompted consumers to adopt healthier habits, such as using functional foods, dietary supplements, clean-label products, fitness programs, and wellness-oriented personal care items. The increasing adoption of digital health platforms, wearable fitness technologies, and wellness applications has enhanced access to personalized health monitoring and lifestyle management. Additionally, the rising demand for natural, organic, and sustainable products is influencing purchasing behavior across food, beauty, and healthcare categories. The expansion of corporate wellness programs, greater participation in recreational fitness activities, and the influence of social media and health-focused online communities are further driving market growth in both developed and emerging economies.

Key Report Takeaways

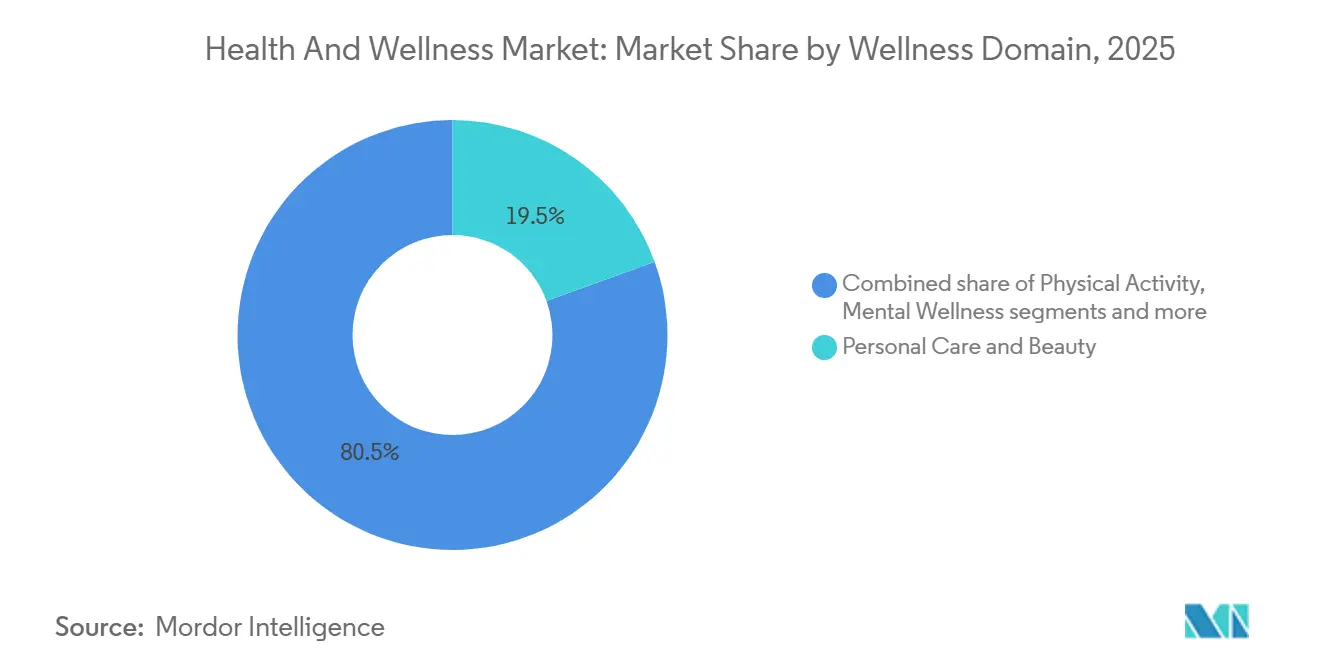

- By wellness domain, personal care & beauty held 19.46% share in 2025, while wellness real estate is forecast to expand at 6.93% CAGR during 2026-2031.

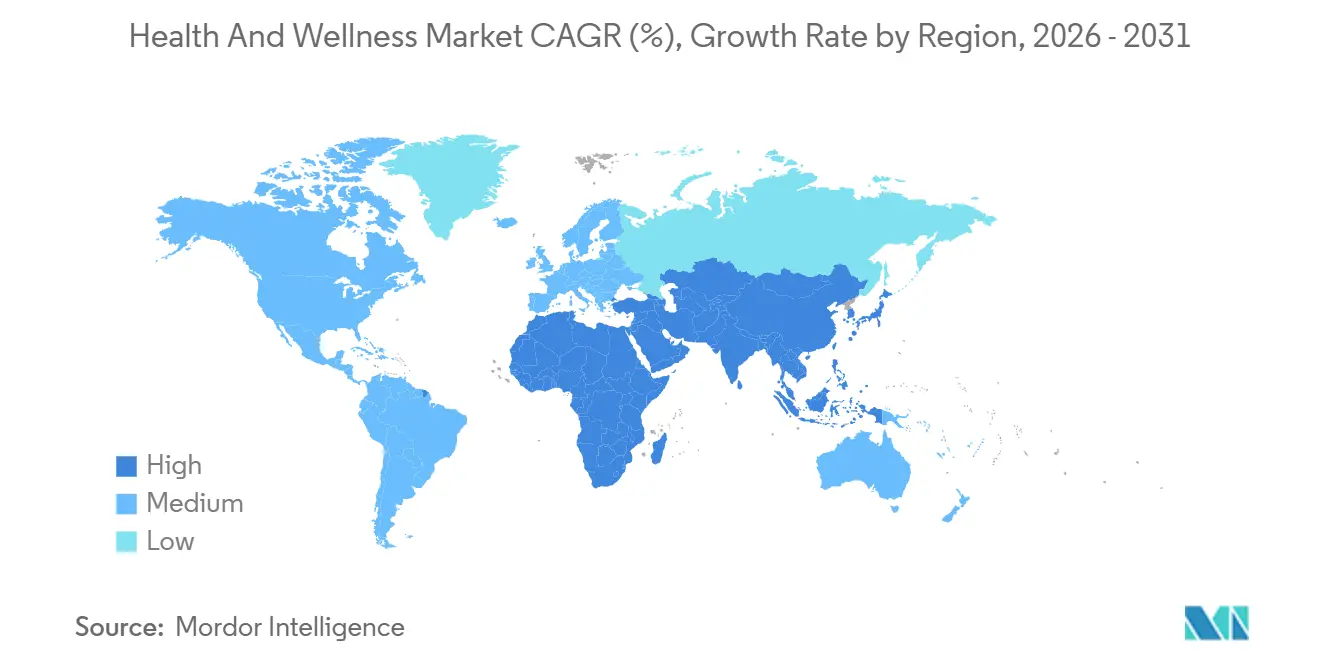

- By geography, North America held 37.64% share in 2025, while Asia-Pacific is forecast to expand at 7.13% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Health And Wellness Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer focus on preventive healthcare | +1.5% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Growing awareness of mental health and emotional wellness | +1.1% | Global, most acute in North America and Asia-Pacific | Medium term (2-4 years) |

| Increasing adoption of fitness-oriented lifestyles | +0.9% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Influence of social media, influencers, and wellness communities | +0.6% | North America and Asia-Pacific | Short term (≤ 2 years) |

| Innovation in functional foods and beverages | +0.7% | Global, Asia-Pacific and North America | Medium term (2-4 years) |

| Growing demand for clean-label and natural products | +0.5% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising consumer focus on preventive healthcare

The increasing consumer emphasis on preventive healthcare is a key driver of growth in the global health and wellness market. Individuals are prioritizing long-term health management over reactive treatment, focusing on physical fitness, immunity enhancement, mental well-being, and reducing the risk of chronic diseases. This shift is reflected in the adoption of healthier lifestyle choices, including balanced nutrition, dietary supplements, functional foods, and regular exercise. The rising prevalence of lifestyle-related diseases, such as diabetes, has further accelerated this trend. According to the International Diabetes Federation (IDF), in 2024, diabetes prevalence among adults in the United States reached 13.7%, equating to approximately 38.5 million cases[1]Source: International Diabetes Federation, "United States," idf.org. The growing incidence of such chronic conditions is driving consumers to invest in wellness products, fitness programs, personalized nutrition, and digital health monitoring solutions. These efforts aim to enhance the overall quality of life and prevent future medical complications, thereby contributing to the sustained growth of the global health and wellness market.

Growing awareness of mental health and emotional wellness

The growing awareness of mental health and emotional wellness is driving the expansion of the global health and wellness market. Consumers are increasingly recognizing the importance of psychological well-being alongside physical health. Rising stress levels, anxiety, depression, sleep disorders, and work-related burnout have prompted individuals to adopt wellness-focused lifestyles that support emotional balance and mental resilience. This trend has increased demand for products and services such as mindfulness applications, meditation programs, stress-relief supplements, aromatherapy products, wellness retreats, sleep-support solutions, and fitness activities aimed at mental relaxation. Additionally, greater social acceptance of mental health discussions, educational campaigns, and improved access to digital mental wellness platforms have encouraged proactive investment in self-care and emotional health management. Employers are also introducing workplace wellness initiatives and mental health support programs to enhance employee productivity and well-being. As consumers continue to seek holistic approaches integrating mental, emotional, and physical wellness, the global demand for health and wellness products and services is expected to grow steadily.

Increasing adoption of fitness-oriented lifestyles

The increasing adoption of fitness-oriented lifestyles is a key factor driving the growth of the global health and wellness market. Consumers are incorporating regular physical activity and wellness routines into their daily lives to enhance overall health, energy levels, and long-term well-being. Growing awareness of issues such as obesity, cardiovascular diseases, stress management, and physical fitness has led to higher participation in gym memberships, sports activities, yoga, strength training, and personalized fitness programs. This shift has fueled demand for fitness-related products and services, including active nutrition, wearable fitness devices, wellness applications, athleisure products, and health supplements. The rapid growth of the fitness industry underscores this consumer trend toward healthier lifestyles. According to the Health & Fitness Association, the U.S. fitness industry reached record levels in 2024, with gyms, studios, and fitness facilities attracting 77 million members. Membership further increased to 81 million Americans in 2025, marking a 5.2% rise compared to the previous year[2]Source: Health & Fitness Association, "81 Million Americans Were Members of a Fitness Facility in 2025, New HFA Report Finds," healthandfitness.org. This growing participation in fitness activities is driving consumer spending on wellness-focused products and services, thereby supporting the ongoing expansion of the global health and wellness market.

Innovation in functional foods and beverages

Innovation in functional foods and beverages is significantly contributing to the growth of the global health and wellness market, as consumers increasingly demand products offering nutritional benefits beyond basic dietary needs. Manufacturers are focusing on developing fortified foods and beverages enriched with proteins, probiotics, vitamins, minerals, adaptogens, botanicals, and immune-supporting ingredients to address specific health concerns, including digestive health, energy management, cognitive performance, weight control, and immunity enhancement. The rising demand for clean-label, plant-based, low-sugar, and natural formulations is driving innovation across categories such as functional beverages, nutritional snacks, dairy alternatives, sports nutrition products, and wellness supplements. Furthermore, advancements in food technology and ingredient science are enabling the creation of personalized and targeted nutrition solutions that align with evolving consumer health objectives. The growing availability of convenient, ready-to-consume functional products through retail stores and online platforms is enhancing consumer accessibility. As health-conscious individuals continue to prioritize preventive nutrition and holistic wellness, innovation in functional foods and beverages is anticipated to remain a key driver of growth in the global health and wellness market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory fragmentation on claims and formulations | -0.9% | Global, most acute in Europe, Asia-Pacific, and North America | Long term (≥ 4 years) |

| Risk of counterfeit and low-quality wellness products | -0.7% | Global, concentrated in Asia-Pacific and online channels | Short term (≤ 2 years) |

| Data privacy concerns in digital health ecosystems | -0.4% | North America and Europe | Medium term (2-4 years) |

| Prevalence of misleading health claims and misinformation | -0.3% | Global, strongest through social media in North America and Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory fragmentation on claims and formulations

Regulatory fragmentation regarding claims and formulations is a significant restraint on the growth of the global health and wellness market. Varying regulatory standards across countries pose challenges for manufacturers and brands operating internationally. Different regions enforce distinct rules on ingredient approvals, permissible health claims, labeling requirements, nutritional disclosures, and product safety standards. This makes it challenging for companies to maintain consistent product formulations and marketing strategies across global markets. Health and wellness products, including dietary supplements, functional foods, nutraceuticals, and wellness beverages, often require extensive scientific validation and regulatory approvals before claims related to immunity, weight management, digestive health, or cognitive benefits can be communicated to consumers. These requirements increase compliance costs, extend product development timelines, and create barriers for smaller companies with limited regulatory resources. Additionally, frequent regulatory updates and stricter scrutiny of misleading health claims can lead to product recalls, reformulations, legal penalties, and reputational risks for brands. The lack of global regulatory harmonization limits innovation flexibility, delays market entry, and constrains the overall growth of the global health and wellness market.

Risk of counterfeit and low-quality wellness products

The prevalence of counterfeit and low-quality wellness products poses a significant challenge to the global health and wellness market. The circulation of fake, adulterated, and substandard products undermines consumer trust and raises critical health and safety concerns. The rising demand for dietary supplements, personal care products, wellness beverages, and pharmaceutical wellness solutions has created opportunities for unauthorized manufacturers and counterfeit suppliers to introduce imitation products. These products often feature misleading labels, unsafe ingredients, or unverified health claims, which can harm consumer health, erode confidence in established brands, and create reputational risks for legitimate manufacturers. This issue is particularly pronounced in online retail channels, where unregulated marketplaces facilitate the distribution of counterfeit products. According to the U.S. Customs and Border Protection, personal care products valued at approximately USD 8 million and pharmaceuticals worth nearly USD 130 million were among the top commodities seized in 2024. Additionally, authorities confiscated around 3.7 million counterfeit pharmaceutical products and over 501,000 personal care products by quantity during the same year[3]Source: U.S. Customs and Border Protection, "The Truth Behind Counterfeits," cbp.gov. The increasing incidence of counterfeit wellness products has led to heightened regulatory scrutiny, complicated supply chain management, and hindered the overall growth potential of the global health and wellness market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Wellness Domain: Personal Care Leads While Built Environments Redefine Upside

The personal care & beauty segment maintained its position as the largest domain in the health and wellness market, holding a 19.46% share in 2025. This growth is driven by increasing consumer preference for products that enhance both aesthetic appeal and overall well-being. Consumers are showing a rising demand for clean-label, natural, organic, vegan, and dermatologically tested beauty products that align with healthier lifestyles and heightened awareness of skin health, aging, and personal hygiene. Concerns about pollution, UV exposure, stress, and chemical-based formulations are further fueling the demand for wellness-oriented skincare, haircare, cosmetics, and personal care products enriched with botanical extracts, vitamins, probiotics, and functional ingredients. Additionally, the influence of social media, beauty influencers, and digital marketing has significantly heightened consumer awareness of self-care and beauty wellness routines. Technological advancements, such as personalized beauty solutions, AI-based skin analysis tools, and wellness-focused product innovations, are also contributing to market growth. The increasing popularity of gender-neutral beauty products, premium wellness cosmetics, and sustainable packaging solutions is further driving the expansion of the personal care and beauty segment within the global health and wellness market.

The wellness real estate segment is expected to grow at a compound annual growth rate (CAGR) of 6.93% through 2031, driven by rising consumer demand for healthier living environments that support physical, mental, and emotional well-being. Factors such as increasing urbanization, stressful lifestyles, and greater awareness of the impact of built environments on health are encouraging developers to incorporate wellness-focused features into residential, commercial, and mixed-use properties. Consumers are prioritizing properties that offer enhanced air and water quality, natural lighting, green spaces, fitness facilities, meditation areas, biophilic designs, thermal comfort, and smart wellness technologies. The adoption of remote and hybrid work models has further increased demand for homes and workplaces that promote productivity, relaxation, and holistic wellness. Additionally, rising investments in sustainable infrastructure, eco-friendly construction materials, and energy-efficient buildings are supporting the development of wellness-oriented real estate projects globally. Hospitality operators, corporate offices, and residential developers are increasingly integrating wellness amenities to attract health-conscious consumers, thereby driving sustained growth in the wellness real estate segment of the global health and wellness market.

Geography Analysis

In 2025, North America accounted for 37.64% of the global wellness market, driven by high consumer awareness of preventive healthcare, fitness, mental well-being, and healthy lifestyle management. The rising prevalence of chronic diseases such as obesity, diabetes, and cardiovascular disorders has prompted consumers to adopt wellness-focused routines, including nutritional supplements, functional foods, fitness programs, and clean-label personal care products. The region benefits from a robust digital health infrastructure, widespread adoption of wearable fitness technologies, and growing demand for personalized nutrition and telehealth services. Additionally, increasing participation in gym memberships, wellness tourism, and mindfulness practices supports market growth. The presence of established wellness brands, continuous product innovation, and growing consumer preference for organic, plant-based, and sustainable products further drive the health and wellness market in North America.

Asia-Pacific is projected to grow at a 7.13% CAGR through 2031, making it the fastest-growing region in the health and wellness market. This growth is fueled by rapid urbanization, rising health consciousness, an expanding middle class, and increasing adoption of preventive healthcare practices. Consumers in countries such as China, India, Japan, South Korea, and Australia are increasingly investing in functional foods, herbal supplements, traditional wellness therapies, fitness activities, and natural personal care products to enhance overall well-being. The growing influence of digital commerce and social media platforms has improved access to wellness products and health-related information across the region. Additionally, increasing stress levels, sedentary lifestyles, and changing dietary habits are driving demand for nutritional supplements, mental wellness solutions, and fitness-oriented services. Strong cultural acceptance of traditional medicine systems, including Ayurveda, Traditional Chinese Medicine, and herbal wellness practices, further supports market growth. Rising investments in wellness tourism, smart healthcare technologies, and health-focused infrastructure are accelerating the expansion of the health and wellness market in the Asia-Pacific.

The health and wellness market in Europe, South America, and the Middle East & Africa is driven by growing awareness of healthy lifestyles, preventive healthcare, and holistic well-being. In Europe, strong consumer demand for organic foods, sustainable beauty products, clean-label nutrition, and environmentally conscious wellness solutions supports market growth, alongside increasing interest in fitness, mental wellness, and healthy aging. In South America, urbanization, improved access to wellness products, and the rising popularity of natural and plant-based nutrition are encouraging consumer spending on health-focused products and services. Meanwhile, in the Middle East & Africa, rising healthcare awareness, increased investments in wellness tourism, luxury wellness facilities, fitness centers, and premium wellness real estate projects contribute to market expansion. The growing influence of digital health platforms, concerns over lifestyle-related diseases, and government initiatives promoting healthier living collectively drive demand for wellness products, preventive healthcare services, and fitness-oriented lifestyles in these regions.

Competitive Landscape

The global health and wellness market remains highly fragmented, with no single dominant player across all wellness categories. Competitive dynamics are increasingly influenced by portfolio consolidation, as major consumer goods and nutrition-focused companies restructure their operations to prioritize beauty, well-being, personal care, preventive health, and functional nutrition. Large-scale mergers and internal business integrations are enabling companies to streamline operations, expand premium wellness offerings, enhance supply chain efficiency, and create unified product ecosystems. These ecosystems integrate nutritional supplements, clinical nutrition, and wellness-oriented consumer products under cohesive business structures.

Technology-driven differentiation has become a significant competitive factor in the market. Companies are investing in artificial intelligence, personalized nutrition platforms, digital wellness ecosystems, wearable health technologies, and data-driven consumer engagement strategies to enhance customer retention and product personalization. The rapid growth of connected fitness devices, health-monitoring wearables, and AI-enabled wellness solutions is intensifying competition between traditional consumer goods companies and technology-focused wellness brands. Increasing consumer demand for customized wellness experiences, preventive healthcare tracking, and digitally integrated health management is driving market participants to develop advanced platforms that deliver personalized recommendations, nutritional guidance, and real-time health insights. Additionally, rising investment activity and public market interest in digital wellness platforms underscore growing investor confidence in technology-enabled health and wellness business models.

Competitive opportunities are increasingly concentrated in mid-market wellness categories and high-growth emerging regions where premium wellness infrastructure and organized distribution channels are still developing. Smaller direct-to-consumer brands are gaining traction by utilizing social commerce platforms, influencer marketing, rapid product innovation cycles, and transparent ingredient-focused branding strategies to compete with larger incumbents. Fast-growing online wellness communities and short-form digital commerce platforms are enabling emerging brands to quickly commercialize trending ingredients, functional formulations, and niche wellness products. Concurrently, rising patent activity and increased investment in advanced formulation science, computational product development, and ingredient innovation are accelerating competition. Large-scale acquisitions in personal care, skin health, oral wellness, and preventive healthcare categories are reshaping the competitive landscape, as companies aim to achieve stronger category diversification, broader wellness portfolios, and operational synergies to solidify their long-term position in the global health and wellness market.

Health And Wellness Industry Leaders

-

Nestlé

-

Unilever PLC

-

Danone S.A.

-

Haleon plc

-

The Procter & Gamble Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Technogym partnered with Google Cloud to integrate generative AI into its wellness ecosystem, deploying an AI Coach for consumers and an AI Assistant for facility operators.

- April 2026: ŌURA announced the acquisition of technology and talent from the AI health startup Galen AI to enhance its connected health and artificial intelligence capabilities. This strategic initiative aims to advance the development of AI-driven personalized health solutions by integrating medical records, laboratory data, medications, and wearable health insights into a single platform.

- March 2026: Herbalife announced the acquisition of specific assets of Bioniq, a UK-based personalized supplements company. This acquisition is intended to strengthen Herbalife's position in the personalized nutrition and wellness market by utilizing AI-driven supplement personalization, which incorporates biomarker analysis and individual health data to provide customized wellness solutions.

Global Health And Wellness Market Report Scope

| Personal Care & Beauty |

| Healthy Eating, Nutrition, & Weight Loss |

| Physical Activity |

| Public Health, Prevention, & Personalized Medicine |

| Mental Wellness |

| Wellness Tourism |

| Traditional & Complementary Medicine |

| Spa Economy |

| Thermal/Mineral Springs |

| Workplace Wellness |

| Wellness Real Estate |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Wellness Domain | Personal Care & Beauty | |

| Healthy Eating, Nutrition, & Weight Loss | ||

| Physical Activity | ||

| Public Health, Prevention, & Personalized Medicine | ||

| Mental Wellness | ||

| Wellness Tourism | ||

| Traditional & Complementary Medicine | ||

| Spa Economy | ||

| Thermal/Mineral Springs | ||

| Workplace Wellness | ||

| Wellness Real Estate | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the global health and wellness market?

The global health and wellness market is valued at USD 7.83 trillion in 2026 and is projected to reach USD 10.63 trillion by 2031 at a 6.31% CAGR.

Which wellness domain leads global revenue?

Personal care & beauty led the global health and wellness market with a 19.46% share in 2025, supported by dermocosmetics, preventive aesthetics, and ingestible beauty products.

Which wellness domain is growing the fastest through 2031?

Wellness real estate is forecast to expand at a 6.93% CAGR through 2031.

Which region contributes the most revenue today?

North America held 37.64% of the global health and wellness market in 2025.

Page last updated on: