Mental Health And EAP Technology Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.96 Billion |

| Market Size (2031) | USD 4.01 Billion |

| Growth Rate (2026 - 2031) | 15.39% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mental Health And EAP Technology Platform Market Analysis by Mordor Intelligence

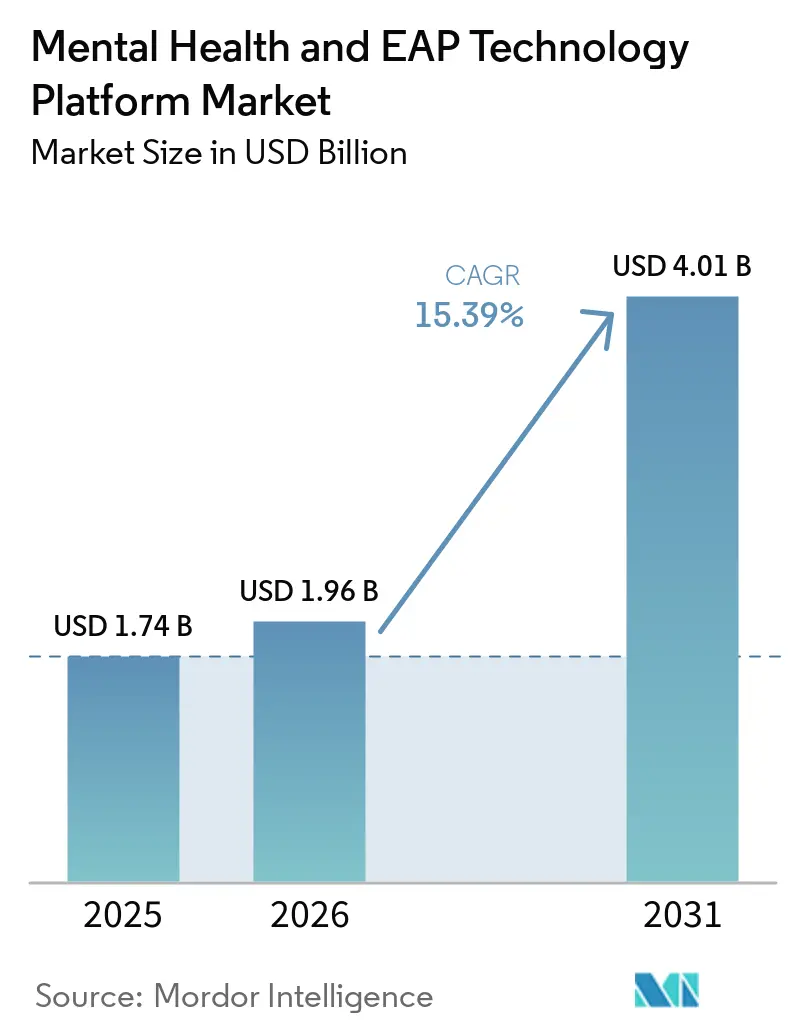

The mental health and EAP technology platform market was valued at USD 1.74 billion in 2025, USD 1.96 billion in 2026, and is forecast to reach USD 4.01 billion by 2031, growing at a CAGR of 15.39% from 2026 to 2031. Employer demand has strengthened as workforce mental health moved into the core benefits agenda, with 84% of U.S. employers in 2025 identifying employee mental wellbeing as a key objective, up from 71% in 2020. That shift has made these platforms more relevant to productivity, retention, and healthcare cost management, rather than positioning them as optional welfare tools. The mental health and EAP technology platform market is also moving beyond simple access, with buyers placing more value on clinical outcomes, AI-enabled care navigation, and the ability to support employees across borders. Competitive activity now favors vendors that can combine provider network depth with outcome reporting and integrated service delivery. At the same time, provider shortages, cybersecurity exposure, licensure complexity, and tighter oversight of AI-led interventions continue to shape adoption patterns across the mental health and EAP technology platform market.

Key Report Takeaways

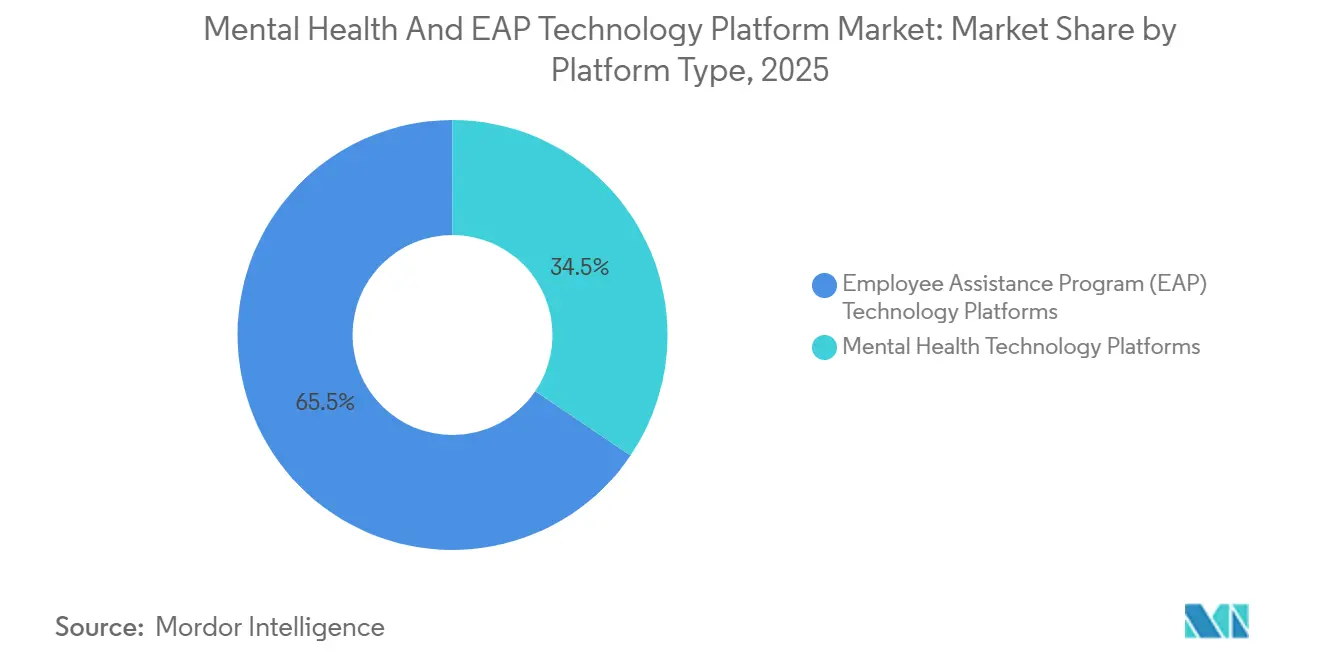

- By platform type, Mental Health Technology Platforms led with 34.47% share in 2025, while EAP Technology Platforms are projected to expand at a 16.94% CAGR through 2031 in the mental health and EAP technology platform market.

- By deployment model, cloud-based solutions held 46.23% share of the mental health and EAP technology platform market in 2025, while on-premises deployments are projected to grow at a 17.86% CAGR through 2031.

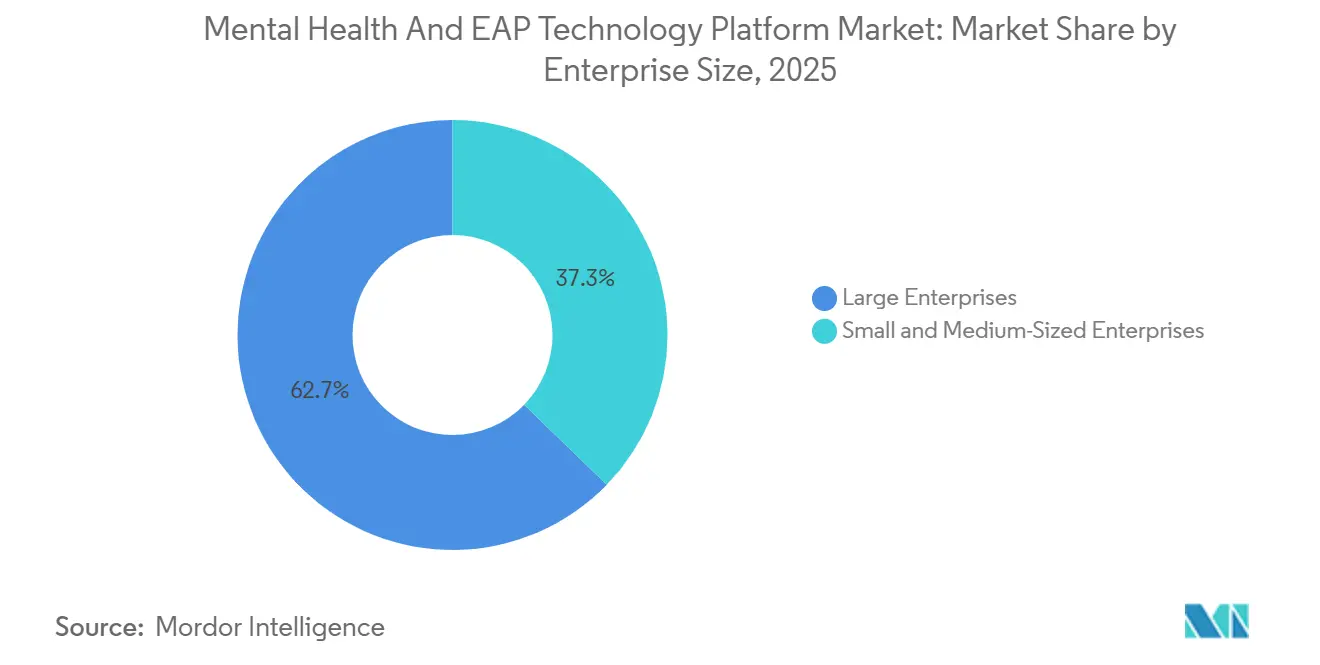

- By enterprise size, large enterprises accounted for 62.73% of the market in 2025, while SMEs are projected to expand at a 18.73% CAGR through 2031 in the mental health and EAP technology platform market.

- By end user industry, Healthcare and Life Sciences captured 22.43% share of the mental health and EAP technology platform market in 2025, while Information Technology and Telecom are projected to advance at a 19.62% CAGR through 2031.

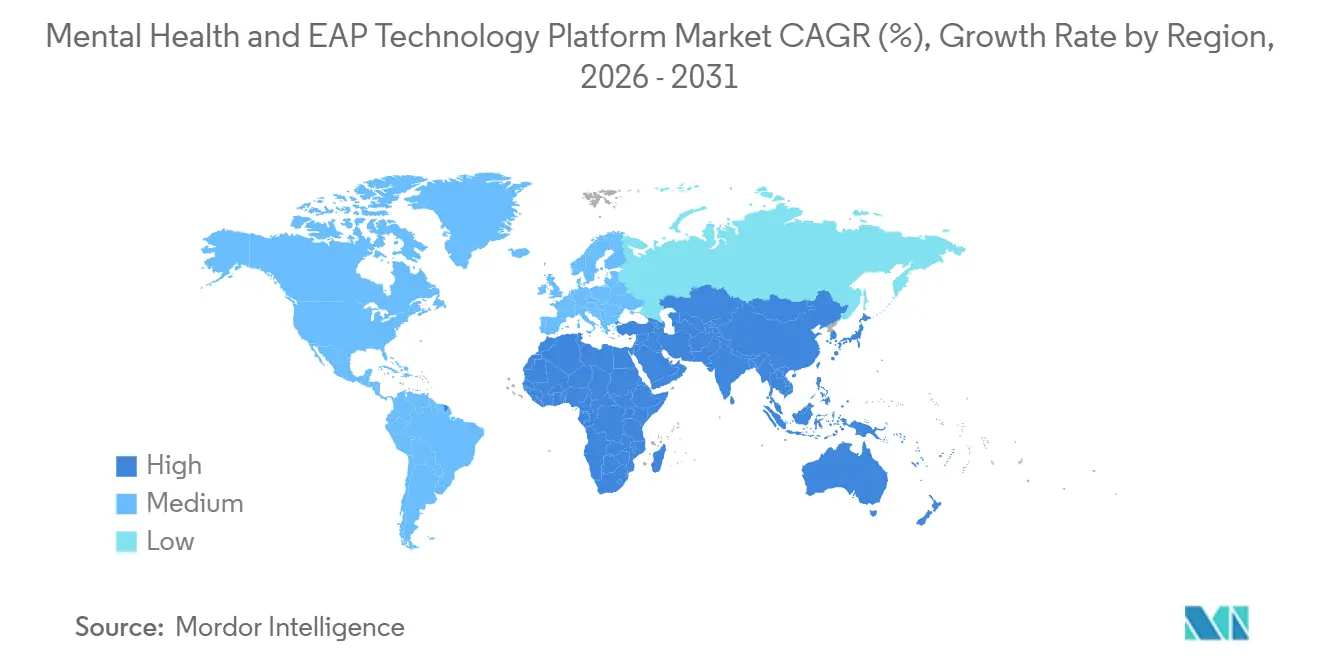

- By geography, North America held 39.83% share of teh mental health and EAP technology platform market in 2025, while the Asia-Pacific is projected to grow at a 15.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mental Health And EAP Technology Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Employer Spend on Workforce Mental Health and Retention | +3.2% | Global, with early-mover intensity in North America and Europe | Short term (= 2 years) |

| AI-Powered Navigation and Stepped-Care Routing | +2.8% | Global, with fastest adoption in North America and Asia-Pacific tech corridors | Medium term (2-4 years) |

| Expansion of Digital-First and Hybrid Care Delivery | +2.2% | Global, adoption led by North America, with spillover to Asia-Pacific and Europe | Short term (= 2 years) |

| Demand for Measurable ROI and Reduced Productivity Loss | +1.8% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Tightening Workplace Mental Health and Parity Requirements | +1.2% | North America and EU-core, with state and national spillover to Asia-Pacific | Medium term (2-4 years) |

| Global Workforce Localization and Multilingual Care Requirements | +0.8% | Asia-Pacific core, Middle East, South America, with spillover to Africa | Long term (= 4 years) |

| Source: Mordor Intelligence | |||

Rising Employer Spend on Workforce Mental Health and Retention

Employers have moved from optional wellness budgets to structured spending on behavioral health, and that shift is giving the mental health and EAP technology platform market a firmer demand base. A 2025 meta-analysis of 19 employer cohort studies found a pooled return of USD 2.30 for every USD 1 invested in enhanced behavioral health services, with net savings of USD 159 per member per month, and all 19 employers showed positive ROI.[1]Matt Hawrilenko, Casey Smolka, Emily Ward, RuthAnne Kavelaars, Millard Brown, and Adam M. Chekroud, “The Impact of Enhanced Behavioral Health Services on Total Healthcare Costs Among US Employers: A Site-Level Analysis of 19 Cohort Studies,” Journal of Health Economics and Outcomes Research, jheor.org That level of proof supports contract renewals and wider deployment across enterprise workforces. It also changes the buying process, because outcome-backed mental health spending is moving beyond HR teams and receiving closer attention from finance and strategy leaders. As a result, vendors in the mental health and EAP technology platform market that can deliver auditable results are better placed to win larger, longer contracts.

AI-Powered Navigation and Stepped-Care Routing That Raises Utilization

Traditional EAP models have long suffered from low engagement, with global utilization typically sitting at 2-3%, leaving a large portion of employer demand unrealized. Spring Health reported that intelligent care navigation lifted utilization from 2% to 16% within 11 months at one health system, while enrollment rose by another 37% after session limits were expanded.[2]Syed Afroz Keramat, Tracy Comans, Alison Pearce, et al., “Psychological Distress and Productivity Loss: A Longitudinal Analysis of Australian Working Adults,” The European Journal of Health Economics, link.springer.com A 2025 randomized controlled trial in NEJM AI found that Therabot produced statistically significant symptom reductions in major depressive disorder and generalized anxiety disorder, with effect sizes comparable to outpatient psychotherapy and average engagement above 6 hours. The practical effect is that AI routing now serves as a clinical bridge, identifying employees who would otherwise remain outside the care pathway. This supports the mental health and EAP technology platform market by rewarding platforms that improve both access and meaningful use, rather than just increasing digital sign-ups.

Expansion of Digital-First and Hybrid Care Delivery

The care mix has shifted in a lasting way, and the mental health and EAP technology platform market now depends on platforms that can coordinate video, in-person, digital, and self-guided support within a single workflow. AllOne Health reported that video counseling accounted for 47% of modality use in 2025, compared with 43% for in-person care, reversing the pattern seen in 2024. A randomized controlled trial published in Communications Medicine in January 2026 found that a generative AI-enabled CBT app increased engagement frequency 2.4 times and duration 3.8 times compared with static digital workbooks, though it did not show a statistically significant overall symptom advantage.[3]Jessica McFadyen, Johanna Habicht, Larisa-Maria Dina, Ross Harper, Tobias U. Hauser, and Max Rollwage, “Increasing Engagement With Cognitive-Behavioral Therapy Using Generative AI: A Randomized Controlled Trial,” Communications Medicine, doi.org The Society for Digital Mental Health also found that EHR integration remained one of the most difficult implementation tasks for digital mental health deployments across U.S. healthcare organizations. That makes flexible care orchestration and enterprise workflow integration more important for growth across the mental health and EAP technology platform market.

Demand for Measurable ROI and Reduced Productivity Loss

Employers increasingly want hard evidence that mental health benefits improve workforce performance, and that is reshaping vendor selection across the mental health and EAP technology platform market. A 2025 longitudinal study covering 70,973 person-years of Australian workers found that high psychological distress was associated with presenteeism costs of AUD 3,656.05 (USD 2,611.35) per worker annually. Spring Health stated in February 2025 that a JAMA Network Open study across seven employers showed a 1.9x ROI, with nearly USD 2 saved in health plan costs for every dollar invested and net savings of USD 1,070 per participant in the first year. This is separating vendors that can document clinical and financial outcomes from those that still rely mostly on engagement dashboards. In practice, the mental health and EAP technology platform market is shifting toward premium pricing and longer contracts for providers that can connect care delivery with absenteeism, presenteeism, retention, and claims reduction.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Confidentiality, Data Privacy, and Cybersecurity Concerns | -1.6% | Global, with highest intensity in North America, Europe, and regulated Asia-Pacific markets | Short term (= 2 years) |

| Shortage of Licensed Behavioral Health Professionals | -1.2% | Global, most acute in non-metropolitan United States, Southeast Asia, and Sub-Saharan Africa | Long term (= 4 years) |

| Cross-Border Data Transfer and Clinical Licensure Friction | -0.8% | Asia-Pacific, Middle East, and South America, with secondary effects in Europe | Medium term (2-4 years) |

| Evidence Scrutiny for AI-Enabled and Self-Guided Interventions | -0.6% | North America and Europe, with growing attention in Asia-Pacific regulatory systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Confidentiality, Data Privacy, and Cybersecurity Concerns

Mental health information falls into one of the most sensitive categories of health data, making security and privacy a direct commercial issue for the mental health and EAP technology platform market. In September 2025, a ransomware attack on Richmond Behavioral Health Authority exposed records for 113,232 individuals, including Social Security numbers and mental health treatment data. Healthcare organizations handling behavioral health information must manage HIPAA obligations alongside stricter protections for substance use and related behavioral health records, which increases implementation complexity. The burden becomes heavier in multinational deployments, where GDPR treats mental health data as a special category and where certain healthcare AI use cases face extra review under the EU AI Act. This means that vendors in the mental health and EAP technology platform market increasingly need a strong security posture, governance controls, and compliance readiness to qualify for enterprise procurement.

Shortage of Licensed Behavioral Health Professionals

Provider scarcity remains a structural brake on the mental health and EAP technology platform market because demand is rising faster than clinical capacity. HRSA data showed 6,807 Mental Health Professional Shortage Areas in the United States as of December 31, 2025, up from 6,418 in 2024, leaving 137 million Americans in underserved areas. A 2026 projection study in the Journal of Psychiatric Research estimated that the U.S. adult psychiatrist supply will fall from 37,470 in 2026 to 36,550 by 2038, while annual demand will rise from 52,100 to 73,330, cutting workforce adequacy from 71.9% to 49.8%.[4]Jason Silvestre, Sydney Seeger, Charles A. Reitman, and Benoit Dubé, “Supply, Demand, and Adequacy of the Adult Psychiatry Workforce in the United States: Projecting a Shortage to 2038,” Journal of Psychiatric Research, sciencedirect.com These shortages raise network costs and pressure margins for vendors that price employer contracts on a per-employee-per-month basis. Interstate licensure efforts, such as PSYPACT and the Counseling Compact, expand geographic reach, but they do not address the underlying pipeline deficit.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform Type: EAP Technology Platforms Drive Integration-Led Purchasing

Mental Health Technology Platforms held 34.47% of the mental health and EAP technology platform market in 2025, maintaining its lead due to its stronger clinical infrastructure, employer awareness, and established measurement-based care models. The segment has benefited from years of investment in therapy workflows, provider quality controls, and outcome tracking that employers can use in renewal discussions. A retrospective cohort study published in October 2025 examined 52,929 participants across 589 employers and found that 92.3% showed reliable symptom improvement in depression or anxiety, while depression effect sizes of 1.61 exceeded meta-analytic benchmarks. That kind of performance data explains why the mental health and EAP technology platform market still assigns premium value to clinical depth. It also reinforces the position of vendors that can show measurable symptom improvement rather than just offering broad content libraries.

EAP Technology Platforms are the fastest-growing platform type, with a 16.94% CAGR from 2026-2031, as employers move away from older counseling hotline contracts and toward integrated digital systems. In 2025, 77% of EAP referrals tracked by AllOne Health were for mental health counseling, showing that clinical demand now sits at the center of many EAP frameworks. This is pushing convergence across the mental health and EAP technology platform industry, because leading mental health vendors are adding work-life and guidance modules, while legacy EAP operators are licensing AI triage and digital therapeutic tools. Vendors that can move utilization above the historical 2-3% benchmark and into the 10% range or higher are in a stronger position to win multiyear contracts.

By Deployment Model: On-Premises Gains Traction in Regulated Enterprise Segments

Cloud deployment accounted for 46.23% of the market in 2025, reflecting the default preference for scalability, faster implementation, and subscription-led commercial models across the mental health and EAP technology platform market. The segment also benefits from the availability of HIPAA-eligible cloud environments that support analytics, content delivery, and care coordination at enterprise scale. Lyra Health stated that its Lyra Empower platform supports more than 21.5 million users globally on cloud infrastructure, enabling the company to run predictive tools and connected workflows in real time. Cloud, therefore, remains the most practical option for employers that want rapid deployment across distributed workforces. It is especially well-suited to organizations that value central administration and lower upfront infrastructure burden.

On-premises deployments are projected to grow at a 17.86% CAGR through 2031, reflecting demand from regulated industries that require data residency, air-gapped environments, or local infrastructure control. This pattern may seem counterintuitive at first, but it aligns with the purchasing behavior of defense, government, and financial services buyers who face stricter governance requirements. The hybrid model is also gaining traction as multinational employers try to balance local compliance with a centralized user experience across the mental health and EAP technology platforms. A 2025 study available through PMC described an AI-driven platform built with federated learning and zero-trust architecture, showing how privacy-preserving design, GDPR alignment, ISO/IEC 27001, and HL7 FHIR are moving into the core architecture rather than being treated as later add-ons.

By Enterprise Size: SME Adoption Bridges the Longstanding Access Gap

Large enterprises accounted for 62.73% of the market in 2025, reflecting their long-standing use of EAP contracts, stronger HR resources, and greater ability to negotiate pricing at scale across the mental health and EAP technology platform markets. This advantage was built over time because traditional EAP administration required dedicated internal support and steady employee communication. As a result, smaller organizations often faced commercial and operational barriers that limited adoption. Large employers also tend to demand integrated reporting, broader provider networks, and layered support options, which favor larger platform contracts. That legacy base helps explain why large enterprises still contribute the greatest volume today.

SMEs are projected to expand at an 18.73% CAGR through 2031 as digital-native vendors reduce minimum contract sizes and simplify onboarding, support, and reporting. Research cited in the input showed that only 21% of SMEs in the United Kingdom currently offer EAP access, indicating significant room for growth among underserved employer groups. A September 2025 study found that Canadian SMEs running sustained mental health programs for 3 years or more generated a median annual ROI of CAD 2.18 (USD 1.58) per dollar invested, compared with CAD 1.62 (USD 1.17) for shorter-term programs. OpenUp has been supporting clients in more than 35 languages across Europe, while Kyan Health has positioned first appointments within 3 working days as part of its SME-ready operating model. Public-sector tools, including a free workplace mental health toolkit launched for small businesses in New Zealand in 2025, are also helping normalize adoption in markets where commercial penetration has been low.

By End User Industry: IT and Telecom Accelerates Past Healthcare in Growth Rate

Healthcare and Life Sciences accounted for 22.43% of the mental health and EAP technology platform market share in 2025, reflecting the significant burnout burden among physicians, nurses, and other clinical staff. In this vertical, mental health support is directly tied to absenteeism, turnover, patient care continuity, and staffing costs, making the business case unusually direct. That gives the segment a durable base within the mental health and EAP technology platform market. Healthcare employers also tend to place more value on evidence-based models, workflow integration, and outcome reporting because mental health support affects both employees and broader care operations. This keeps demand steady for vendors that can combine clinical rigor with enterprise deployment discipline.

Information Technology and Telecom is projected to grow at a 19.62% CAGR through 2031, making it the fastest-growing end-user vertical as younger workforces and high-pressure work cultures lift digital engagement. The segment is more willing to use app-led interventions, AI triage, and blended care pathways, which makes adoption faster once benefits are offered. BFSI remains important because well-funded HR teams and ESG-linked disclosures are driving greater formal mental health support, while manufacturing is expanding EAPs as part of wider psychosocial risk management. Retail and e-commerce are also increasing adoption where seasonal labor volatility and turnover make absenteeism reduction easier to measure, and government buyers are gradually widening the addressable base through evidence-led digital health procurement requirements.

Geography Analysis

North America accounted for 39.83% of the mental health and EAP technology platform market in 2025, reflecting mature EAP infrastructure, stronger digital health funding conditions, and a more developed regulatory environment. The United States remains the largest contributor in the region because employer-sponsored benefits are more established, and enterprise buyers have shown greater willingness to pay for clinical outcome reporting and AI-enabled navigation. The MHPAEA 2024 Final Rule strengthened nonquantitative treatment limitation requirements and called for more formal data evaluation of access differences, which kept compliance and reporting high on employer agendas even after a May 2025 nonenforcement policy created temporary uncertainty around some newer provisions. Canada continues to act as a secondary growth node, and GreenShield’s February 2026 acquisition of Kii Health’s mental health services segment showed how regional players are using acquisitions to deepen clinician capacity and digital therapy reach. Together, these conditions keep North America at the center of current revenue generation in the mental health and EAP technology platform market.

Europe ranked second in 2025, with Germany, the United Kingdom, and the Netherlands serving as the main volume centers for the mental health and EAP technology platform market. The United Kingdom combines broad EAP access with utilization that still lags behind underlying coverage, leaving room for platforms to raise engagement through better navigation and simpler care journeys. Germany’s workplace health framework and the EU Occupational Safety and Health Strategy have helped formalize psychosocial risk management, while France’s 2025 EAP acquisition activity showed that operators are scaling to meet cross-market employer demand. The EU AI Act will add another layer of compliance work for AI-enabled vendors that want to scale across Europe from 2026 onward.

Asia-Pacific is the fastest-growing region, with the mental health and EAP technology platform market projected to rise at a 15.86% CAGR from 2026 to 2031 as it expands from a lower penetration base. A January 2025 cross-sectional study covering 15,302 employed adults across 6 Southeast Asian countries found that only 29.04% of employees reported access to employer-provided EAP services, with access ranging from 62.84% in the Philippines to 17.96% in Thailand. India, China, Japan, South Korea, and Australia and New Zealand remain the core growth markets, while Singapore and the Philippines are emerging as regional hubs for multinational deployments. Outside Asia-Pacific, the Middle East is advancing through workplace wellness programs in Saudi Arabia and the UAE; Africa is building around mobile-first models led by South Africa and Nigeria; and South America is seeing stronger demand from multinational employers, even though licensure and multilingual requirements still slow rollout.

Competitive Landscape

The mental health and EAP technology platform market is moderately fragmented, but consolidation is accelerating at the top as scale becomes increasingly important in enterprise procurement. Spring Health’s combination with Alma in May 2026 created an integrated platform serving more than 170 million lives across employer and health plan channels, which raised the bar for network depth and lifetime care coverage. Talkspace reported FY2025 revenue of USD 228.9 million, up 22% year over year, and said payor revenue accounted for nearly 75% of total revenue, underscoring how quickly institutional channels are becoming the main path to scale. Lyra Health added to that competitive pressure with the April 2025 launch of Lyra Empower and then secured USD 75 million in new financing in May 2026 to expand platform capabilities and its global provider network. These moves have made AI navigation, provider reach, and auditable ROI more decisive than simple content breadth across the mental health and EAP technology platform market.

Strategy is now converging around 3 levers: higher utilization, stronger proof of outcomes, and wider multilingual coverage. Vendors that can push engagement above 10-15% are gaining an advantage over legacy EAP models that historically struggled to move far beyond 1-3% usage. Kyan Health positioned its EAP 4.0 model around reported utilization rates of 10-40% and outcome-linked ROI reporting, reflecting how newer entrants are competing on measurable performance rather than access alone. Wysa has also used clinical publications and patents tied to its AI conversational framework to strengthen credibility in more regulated markets, while Talkspace’s TalkAI beta signaled that supervised AI tools are becoming a central area of differentiation.

White-space opportunity remains strongest in SMEs and in multilingual emerging markets where culturally adapted support is still limited. Unmind moved to address that gap with growth funding in 2025 and with the wider rollout of its AI mental health agent Nova, targeting the enterprise mid-market and global employers that need scalable support across countries. Security certifications have also become a baseline requirement, because large employers are less willing to shortlist vendors that cannot demonstrate mature governance and data protection practices. As a result, the mental health and EAP technology platform market remains open to new entrants, but the path to leadership now depends on clinical credibility, compliance-readiness, and the ability to serve global workforces at scale.

Mental Health And EAP Technology Platform Industry Leaders

Lyra Health, Inc.

Headspace Health

Spring Care, Inc.

Modern Life, Inc.

Talkspace, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Lyra Health secured USD 75 million in new financing to expand its platform technology and global provider network, bringing cumulative funding to over USD 175 million. The company currently serves over 21.5 million users globally with clinical-grade AI mental health tools.

- May 2026: Spring Health and Alma completed their combination, creating what the companies describe as the first lifelong mental health platform, covering over 170 million lives globally across employer and health plan channels, with Dr. Harry Ritter continuing as CEO of Alma within Spring Health.

- April 2026: Voya Financial announced a collaboration with TELUS Health to integrate TELUS Health's EAP services with Voya's group insurance benefits, providing mental and emotional wellbeing support including digital services, work-life assistance, and financial guidance to employer clients.

- February 2026: GreenShield acquired Kii Health's Canadian mental health services segment, including its EFAP business, Student Assistance Program, and the MindBeacon digital therapy platform, adding 700 clinicians to GreenShield's network and strengthening its position in Western Canada and Quebec.

Global Mental Health And EAP Technology Platform Market Report Scope

The mental health and employee assistance program (EAP) technology platform market comprises digital solutions that support employee well-being, resilience, and workplace productivity through accessible mental health services and structured assistance programs. These platforms provide tools for counseling, stress management, crisis intervention, and holistic wellness, while also integrating with HR systems to deliver scalable support across diverse workforce needs.

The mental health and EAP technology platform market is segmented by Platform Type (Mental Health Technology Platforms, and Employee Assistance Program Technology Platforms), Deployment Model (Cloud, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-user Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, and Government and Public Sector), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Mental Health Technology Platforms |

| Employee Assistance Program (EAP) Technology Platforms |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| BFSI |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Platform Type | Mental Health Technology Platforms | |

| Employee Assistance Program (EAP) Technology Platforms | ||

| By Deployment Model | Cloud | |

| On-Premises | ||

| Hybrid | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By End User Industry | BFSI | |

| Healthcare and Life Sciences | ||

| Information Technology and Telecom | ||

| Retail and E-commerce | ||

| Industrial Manufacturing | ||

| Government and Public Sector | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the mental health and EAP technology platform market?

The mental health and EAP technology platform market was valued at USD 1.74 billion in 2025 and is forecast to reach USD 4.01 billion by 2031, growing at a 15.39% CAGR from 2026-2031.

Which platform type leads revenue generation in this space?

Mental Health Technology Platforms led in 2025 with 34.47% share, supported by established clinical infrastructure, outcome tracking, and stronger employer familiarity.

Which segment is expanding the fastest through 2031?

EAP Technology Platforms are the fastest-growing platform type at a 16.94% CAGR, while Information Technology and Telecom is the fastest-growing end-user vertical at a 19.62% CAGR.

Why are employers investing more in these platforms?

Employers are linking mental health support with retention, productivity, and claims management, and studies cited in the report showed positive ROI, including pooled returns of USD 2.30 for every USD 1 invested in enhanced behavioral health services.

Which region contributes the most revenue today, and which one is growing the fastest?

North America held 39.83% share in 2025 because of stronger EAP maturity and regulatory activity, while Asia-Pacific is projected to grow the fastest at a 15.86% CAGR through 2031.

What are the main risks affecting vendor growth and adoption?

The biggest constraints are provider shortages, cybersecurity and privacy exposure, cross-border compliance friction, and closer scrutiny of AI-led self-help tools and digital therapeutics.

Page last updated on: