Differentiated Thyroid Cancer Therapeutics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

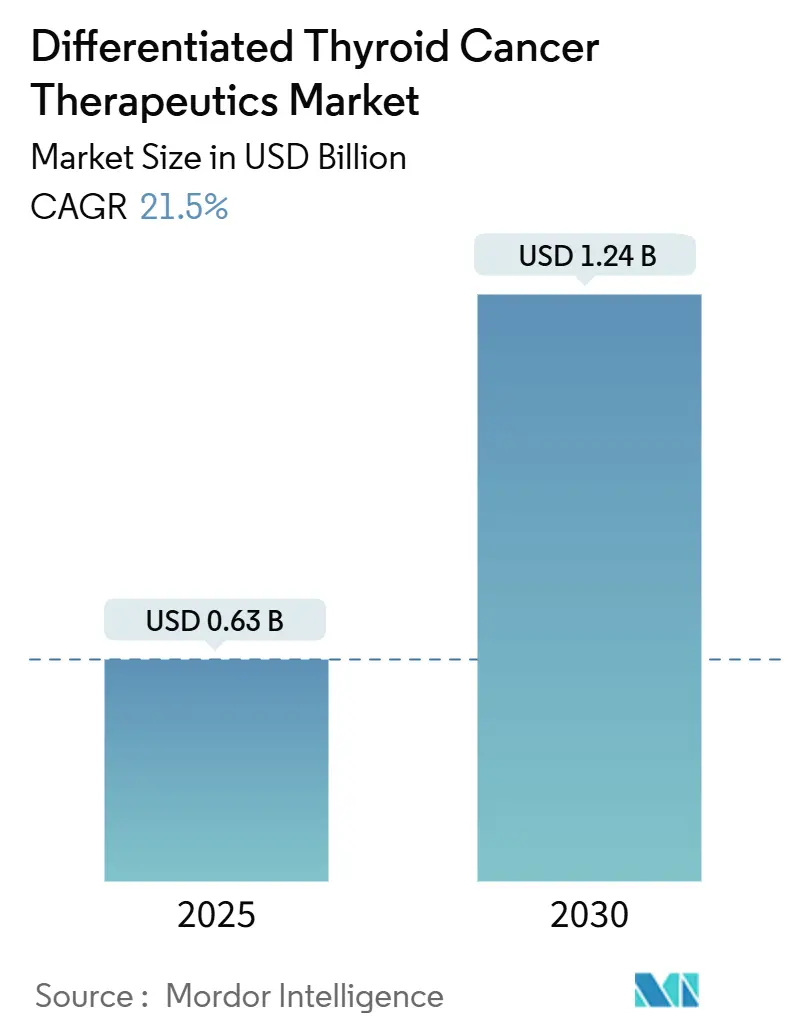

| Market Size (2025) | USD 0.63 Billion |

| Market Size (2030) | USD 1.24 Billion |

| Growth Rate (2025 - 2030) | 21.50% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Differentiated Thyroid Cancer Therapeutics Market Analysis by Mordor Intelligence

The differentiated thyroid cancer therapeutics size market reached USD 0.63 billion in 2025 and is forecast to climb to USD 1.24 billion by 2030, advancing at a 15.1% CAGR. Rapid growth follows twin forces: a steady rise in newly diagnosed cases and a surge of targeted agents that move care beyond exclusive reliance on radioactive iodine (RAI)[1]U.S. Food and Drug Administration, “FDA Approves Selpercatinib for Pediatric RET-Mutated Thyroid Cancer,” fda.gov. Breakthrough approvals such as selpercatinib for pediatric RET-mutated disease and repotrectinib for NTRK-positive tumors demonstrate the pace of innovation and broaden the eligible patient pool. As testing for key genetic alterations becomes routine, payers in major markets increasingly reimburse precision medicine regimens, reinforcing demand. At the same time, manufacturers build new radiopharmaceutical plants and sign isotope-supply agreements that ease historical bottlenecks and open fresh revenue streams. Patent cliffs for first-generation multi-kinase inhibitors add urgency for sponsors to file next-generation compounds while exclusivities remain intact.

Key Report Takeaways

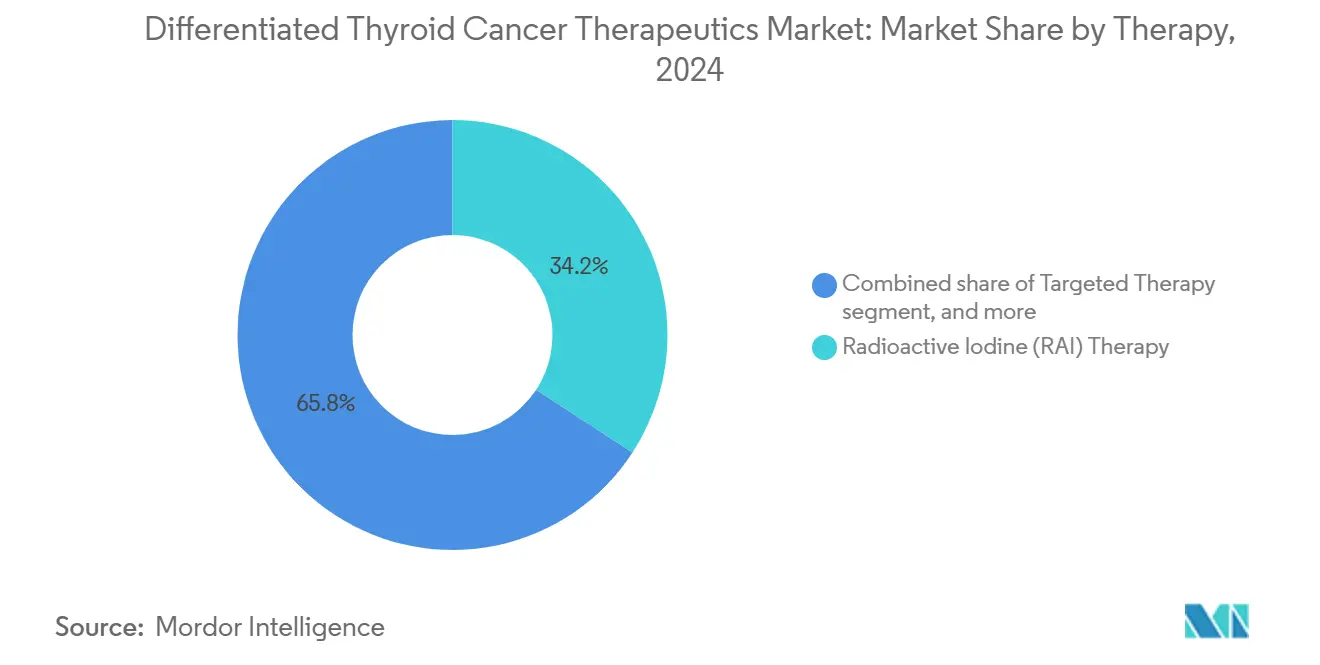

- By therapy, radioactive iodine maintained the lead with 34.23% of differentiated thyroid cancer therapeutics market share in 2024; targeted therapy is expanding fastest at a 17.26% CAGR through 2030.

- By stage, localized disease held 46.64% revenue in 2024, whereas metastatic/RAI-refractory cases are projected to grow at 16.84% CAGR.

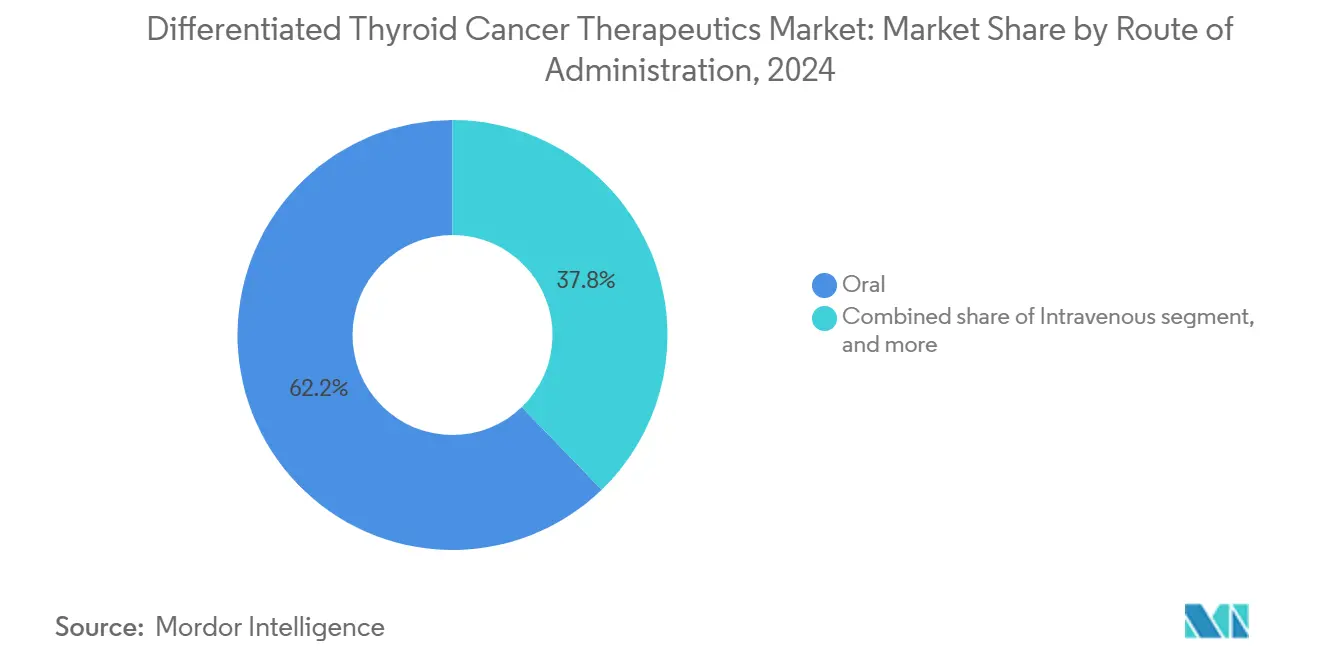

- By route of administration, oral products captured 62.65% of the differentiated thyroid cancer therapeutics market size in 2024; intravenous options are pacing at a 15.89% CAGR to 2030.

- By end user, hospitals accounted for 43.76% share of the differentiated thyroid cancer therapeutics market size in 2024, while ambulatory surgical centers post the quickest trajectory at 16.34% CAGR.

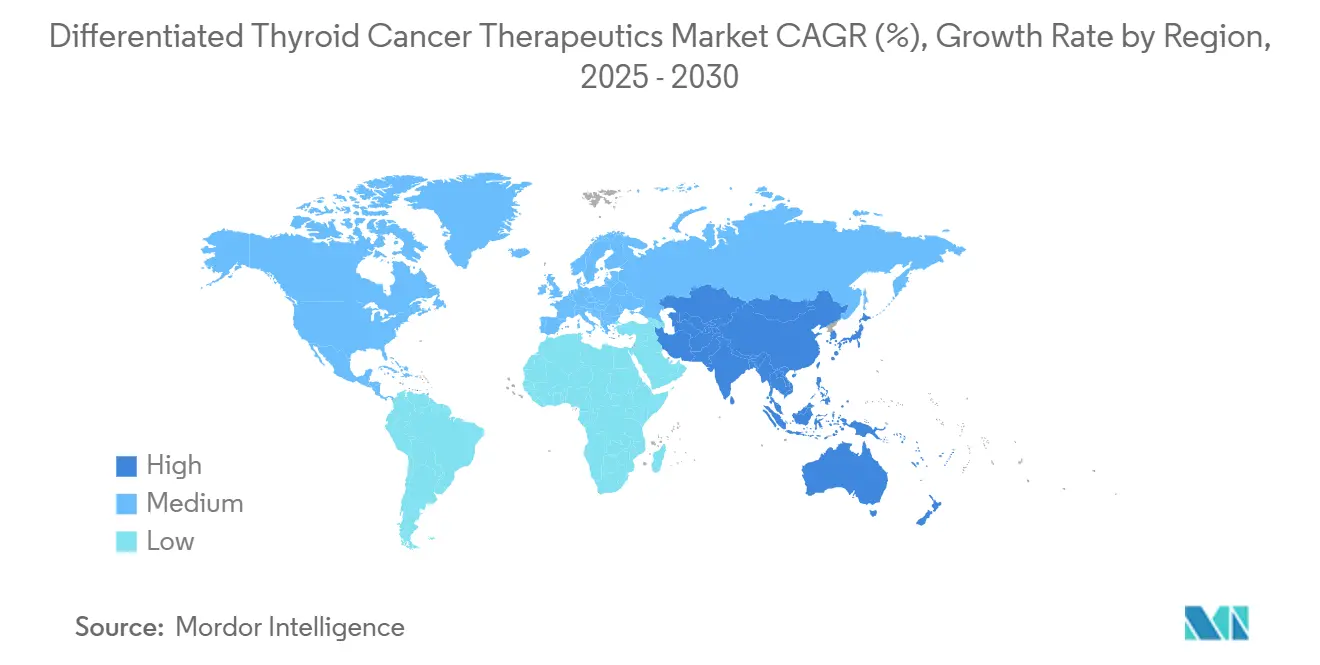

- By geography, North America led with 42.32% revenue in 2024; Asia-Pacific is on course for the highest 16.43% CAGR to 2030.

Global Differentiated Thyroid Cancer Therapeutics Market Trends and Insights

Driver Impact Analysis*

| Drivers Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global incidence and earlier detection | +2.8% | Asia-Pacific, North America | Medium term (2-4 years) |

| Expansion of approved targeted therapies and label extensions | +3.2% | North America, Europe | Short term (≤2 years) |

| Favourable reimbursement and inclusion in national cancer-care guidelines | +1.9% | North America & EU, expanding APAC | Medium term (2-4 years) |

| Increasing adoption of radioisotope-based theranostics | +2.1% | North America, Europe | Long term (≥4 years) |

| Growing demand for minimally invasive, orally administered alternatives to surgery | +1.6% | Developed markets worldwide | Medium term (2-4 years) |

| Intensifying R&D investment and clinical-trial pipeline depth worldwide | +2.4% | North America, Europe, select APAC | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Global Incidence and Earlier Detection

Global thyroid cancer cases rose from 87,583 in 1990 to 233,847 in 2019, with the greatest spike among people aged 10–24 years. Better imaging, artificial-intelligence-assisted pathology, and wider screening in high-income countries reveal tumors at smaller sizes, pushing more patients into the differentiated thyroid cancer therapeutics market earlier in their disease journey. Earlier diagnosis prevents many cases from progressing to RAI-refractory status yet still elevates the absolute number eligible for adjuvant systemic therapy. Continuation of national ultrasound programs in South Korea and growing adoption of fine-needle aspiration with AI image analysis worldwide sustain this driver.

Expansion Of Approved Targeted Therapies and Label Extensions

In 2024 the FDA lowered the age cut-off for selpercatinib to 2 years, and repotrectinib secured an accelerated nod for NTRK-positive tumors after showing a 58% objective response rate in treatment-naïve patients. Updated 2025 NCCN guidelines now recommend broad next-generation sequencing before systemic therapy, cementing genomic profiling as standard practice. The combined effect sharply enlarges the differentiated thyroid cancer therapeutics market by moving pediatric and refractory cohorts into the treatable population.

Favourable Reimbursement and Inclusion in National Cancer-Care Guidelines

Private insurers in the United States use the NCCN Compendium as a binding reference, and Canada’s Time-Limited Recommendation pathway trimmed provincial listing timelines for oncology drugs starting in 2023[2]National Comprehensive Cancer Network, “NCCN Drugs & Biologics Compendium,” nccn.org. Real-world cost-sharing studies show 75% of commercially insured lenvatinib users pay USD 100 or less per month despite list prices over USD 17,000, signalling adequate payer support[3]Erin Shank, “Real-World Costs of Lenvatinib,” American Journal of Managed Care, ajmc.com. Guideline inclusion of pembrolizumab-lenvatinib combinations widens coverage and encourages earlier therapy initiation.

Increasing Adoption of Radioisotope-Based Theranostics in Oncology Centers

Big-pharma investments in isotope manufacturing—Novartis committed more than USD 200 million to an Indianapolis site—reduce historical shortages that slowed uptake. Orano Med is building a EUR 250 million thorium-228 plant that will raise lead-212 output tenfold, opening the door for targeted alpha therapy production. FDA stability-testing standards for PET drugs, although adding cost, unify quality expectations and foster hospital adoption. These factors support sustained demand for intravenous radiopharmaceuticals.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patent expiries and rapid generic erosion compressing branded-drug prices | -2.1% | Developed markets globally | Short term (≤2 years) |

| High treatment costs and limited access in low- and middle-income countries | -1.8% | Sub-Saharan Africa, South Asia | Long term (≥4 years) |

| Safety concerns and adverse-event burden of multikinase inhibitors | -1.5% | Global, higher impact in developed markets | Short term (≤2 years) |

| Fragile global radioisotope supply chain affecting RAI availability | -1.3% | North America, Europe, APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Patent Expiries and Rapid Generic Erosion Compressing Branded-Drug Prices

Sorafenib has already lost exclusivity, and a settlement enables generic cabozantinib from 2031, setting up sequential price pressure. Historical data show oncology brands can lose 52% of annual sales within 2 years after generic entry. While innovators race to launch next-generation assets, shrinking margins may dampen overall revenue growth for the differentiated thyroid cancer therapeutics market.

High Treatment Costs and Limited Access in Low- And Middle-Income Countries

In Morocco 22 of 39 innovative oncology drugs lack reimbursement, with market entry lagging FDA approval by up to 7 years. Similar patterns across South Asia lead to under-treatment and elevated mortality despite rising incidence. Unless parallel import programs and tiered-pricing agreements accelerate, emerging markets will contribute fewer therapy units than their disease burden suggests.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy: Targeted Agents Disrupt RAI Leadership

The differentiated thyroid cancer therapeutics market size for therapy choices remained dominated by RAI at 34.23% revenue in 2024. Yet targeted therapy is projected to post 17.26% CAGR, reflecting expanding indications and higher per-patient spending. Multi-kinase inhibitors such as lenvatinib delivered median progression-free survival of 18.3 months in the SELECT study, far outstripping placebo and driving physician confidence. Oral TKIs also align with growing outpatient care models. Immunotherapy combinations now under study could take share from chemotherapy, which retains limited use because of modest response rates in differentiated tumors. Genetic testing adoption highlights mutations like BRAF V600E that correlate with better outcomes on kinase inhibitors, reinforcing the precision‐medicine mind-set. Resistance mutations in NTRK genes are already shaping sequential therapy choices and will continue to influence regimen design.

Surgery remains first-line for localized disease, but systemic agents play a larger role in metastatic management and in neoadjuvant settings that allow tumor shrinkage ahead of resection. Emerging alpha-emitting radiopharmaceuticals offer another high-margin category, potentially enlarging the differentiated thyroid cancer therapeutics market. Sponsors also explore lower-dose TKI regimens that preserve efficacy while improving tolerability and adherence. As more oral agents qualify for first-line RAI-refractory use, the hierarchy of therapies is likely to invert, with targeted agents surpassing RAI revenue by the end of the forecast horizon.

By Stage: Advanced Disease Commands Premium Pricing

Localized tumors generated 46.64% of 2024 revenue, a reflection of sheer patient numbers and standard postoperative RAI use. However metastatic or RAI-refractory disease will expand fastest at 16.84% CAGR, absorbing the lion’s share of high-priced targeted therapies. The new WHO classification that separates minimally invasive from widely invasive forms refines risk profiles and better predicts progression, guiding clinicians to escalate systemic therapy earlier. Active surveillance for microcarcinoma keeps low-risk patients on observation, holding down overtreatment rates. Conversely, neoadjuvant BRAF/MEK inhibition has produced surgical downsizing in locally advanced tumors, enlarging the candidate pool for curative operations.

Long-term survivor data show thyroid-cancer-specific mortality of only 0.6% at 20 years among low-risk cohorts, while cardiovascular disease now represents a bigger threat. These figures validate selective intervention strategies and free resources for aggressive treatment of advanced disease. As patients progress from regional to metastatic stages, prescription intensity and monitoring frequency rise, contributing disproportionate revenue gains even though patient counts remain smaller.

By Route Of Administration: Oral Convenience Meets IV Innovation

Oral drugs dominated with 62.65% revenue in 2024 thanks to the popularity of lenvatinib, sorafenib, and newer TKIs. The differentiated thyroid cancer therapeutics market size for intravenous formats is poised for 15.89% CAGR, buoyed by radioligand therapy launches and checkpoint-inhibitor combinations. Intramuscular thyrotropin alfa remains a niche diagnostic aid, while subcutaneous options under study may challenge current paradigms.

IV products require hospital or specialized outpatient center infrastructure, reinforcing the relevance of central pharmacies and nuclear-medicine suites. Oral therapies, in contrast, enable dispensing at ambulatory sites, easing patient burden. Manufacturers are optimizing capsule strengths and exploring once-daily schedules to further tilt prescribing toward the outpatient setting. Parallel growth in radiopharmaceutical capacity, notably at Novartis facilities under construction, will underpin the IV segment’s momentum.

By End User: Hospitals Remain Core While Ambulatory Sites Surge

Hospitals captured 43.76% revenue in 2024, reflecting their control of surgery, nuclear medicine, and IV infusion. Ambulatory surgical centers (ASCs) will experience a 16.34% CAGR to 2030 as more oral regimens and minimally invasive procedures migrate outside hospital walls. Specialty cancer centers offer genomic testing, clinical trials, and multidisciplinary tumor boards that steer patients into targeted or combination regimens, sustaining high-value care episodes.

Radiofrequency ablation for recurrent lesions, often performed in ASCs, provides an example of shifting site-of-service economics. Hospitals nonetheless remain pivotal for radiopharmaceutical administration, adverse-event management, and complex neck surgeries. Digital pathology and AI imaging that span both settings support continuity of care and shared decision-making.

Geography Analysis

North America generated 42.32% of 2024 revenue, supported by comprehensive insurance coverage, experienced surgical centers, and large clinical-trial networks. Real-world databases show lenvatinib as the predominant first-line systemic agent in the United States and Canada, underscoring first-mover advantage for oral TKIs. The region also benefits from early radiopharmaceutical adoption, with a growing number of centers participating in theranostic research programs.

Asia-Pacific will grow at 16.43% CAGR through 2030, anchored by rising incidence in South Korea, Japan, and China. Opportunistic ultrasound screening contributed to a reported “epidemic” in South Korea, but subsequent studies confirm that a genuine increase, not just detection bias, is occurring across several Asian countries. High-income Asia-Pacific economies post the largest disability-adjusted life-year burden, pointing to tangible unmet needs that new therapies can address. As reimbursement frameworks mature in Japan and China, patient access to targeted drugs is accelerating.

Europe sustains mid-single-digit growth on the back of unified EMA processes and broad adoption of NCCN-aligned treatment pathways. Uptake of radioisotope therapies is high in Germany and France, where nuclear-medicine infrastructure is well-established. In contrast, Middle East & Africa and South America contribute smaller shares today but register above-average growth as governments modernize cancer-care systems and private insurers enter the market. Partnerships that bundle diagnostics with therapeutics may help overcome resource limitations in these regions.

Competitive Landscape

The differentiated thyroid cancer therapeutics market is moderately consolidated. Exelixis, Eisai, and Bayer together control a significant revenue pool through multi-kinase inhibitors with broad labels. Their depth in clinical development, manufacturing, and market access creates formidable entry barriers for smaller contenders. Yet precision oncology’s shift toward genotype-targeted drugs invites nimble biotech entrants that license or co-develop narrow-spectrum inhibitors.

Strategic plays concentrate on supply-chain security and pipeline diversification. Novartis is spending over USD 200 million to scale radiopharmaceutical production, assuring dose availability for current agents and future ligands. Orano Med’s thorium-228 project addresses alpha-particle therapy feedstock, giving partners a hedge against isotope shortages. Exelixis’s CABINET success in neuroendocrine tumors showcases lifecycle management that extends cabozantinib into new indications.

Generic erosion is imminent for older TKIs; sorafenib has already lost exclusivity, and cabozantinib faces generic launch in 2031. Manufacturers respond by advancing next-generation inhibitors such as zanzalintinib, which targets VEGF, HGF, and AXL kinases in a single molecule. M&A activity remains brisk: Eli Lilly’s USD 2.5 billion purchase of Scorpion Therapeutics and GSK’s USD 1 billion acquisition of IDRx highlight the premium placed on early-stage precision assets. The overall competitive narrative points to coexistence of large pharma with broad portfolios and specialty firms focused on genomic niches.

Differentiated Thyroid Cancer Therapeutics Industry Leaders

Bayer AG

Eisai Co Ltd

Exelixis Inc.

Sanofi (Genzyme)

Curium Pharma

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Exelixis obtained FDA approval for CABOMETYX (cabozantinib) to treat previously treated advanced neuroendocrine tumors in patients aged ≥12 years, the first systemic option irrespective of primary site or somatostatin receptor status.

- February 2025: GSK purchased IDRx for more than USD 1 billion, gaining access to IDRX-42, a selective TKI designed to address resistance mutations in solid tumors.

- January 2025: Eli Lilly announced acquisition of Scorpion Therapeutics for up to USD 2.5 billion, adding precision oncology candidates that could extend into thyroid cancer indications.

- January 2025: Lantheus Holdings completed its USD 250 million acquisition of Evergreen Theragnostics, with milestones up to USD 752.5 million, to strengthen radiopharmaceutical supply.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the differentiated thyroid cancer (DTC) therapeutics market as the total manufacturer-level revenues generated by prescription drugs and radio-iodine doses used to treat papillary, follicular, and Hurthle cell carcinomas. The scope spans kinase inhibitors, thyroid hormone suppressants, chemotherapy agents, and therapeutic radioisotopes employed after diagnosis or relapse.

Revenues from surgery, diagnostic imaging, and therapies for medullary or anaplastic thyroid cancers are excluded.

Segmentation Overview

- By Therapy

- Chemotherapy

- Targeted Therapy

- Thyroid Stimulating Hormone Suppression (THS)

- Radioactive Iodine (RAI) Therapy

- Other Therapies

- By Stage

- Localized

- Regional

- Metastatic/RAI-Refractory

- By Route of Administration

- Oral

- Intravenous

- Other Route of Administrations

- By End User

- Hospitals

- Specialty Cancer Centers

- Ambulatory Surgical Centers

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We hold semi-structured interviews with endocrinologists, nuclear-medicine physicians, payor pharmacists, and procurement managers in North America, Europe, and key Asia-Pacific markets to validate dosing norms, RAI retreatment rates, and effective therapy costs. Brief online surveys gauge patient-support uptake.

Desk Research

Mordor analysts collect incidence and prevalence statistics from SEER, GLOBOCAN, and Eurostat cancer registries, scan FDA and EMA approval dossiers for label populations, and monitor prescription volumes through IQVIA country dashboards. Insights are enriched with SEC 10-Ks, peer-reviewed articles in Thyroid and JCO, hospital formulary price lists, and news retrieved via Dow Jones Factiva and D&B Hoovers. The sources named are illustrative; numerous other open and proprietary datasets inform our desk work.

Market-Sizing & Forecasting

The model starts with a top-down reconstruction. Country-level DTC incidence multiplied by treatment-eligible share and average annual therapy cost delivers 2024 consumption. Selective bottom-up checks using distributor sell-out data and manufacturer disclosures refine totals. Variables such as rising RET/BRAF test penetration, guideline shifts favoring adjuvant lenvatinib, generic TKI entry, RAI reimbursement caps, and exchange-rate movements are explicitly forecast. A multivariate regression, supported by scenario analysis, projects demand through 2030.

Data Validation & Update Cycle

Outputs undergo variance checks against historic spend curves, external benchmarks, and peer estimates before senior review. We refresh each file annually and issue interim updates when launches, price controls, or safety alerts materially change assumptions.

Why Mordor's Differentiated Thyroid Cancer Therapeutics Baseline Commands Reliability

Published estimates diverge because firms widen disease scope, embed surgical costs, or apply frozen pricing.

Mordor selects a therapy-only lens, layers real-world dosing, and refreshes inputs yearly, giving planners a balanced reference.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.63 B (2025) | Mordor Intelligence | |

| USD 0.48 B (2023) | Regional Consultancy A | Historic base year and limited pipeline adjustment |

| USD 2.30 B (2024) | Global Consultancy B | Bundles surgery and hospital services inflating totals |

| USD 0.45 B (2024) | Industry Association C | Excludes targeted TKIs and assumes single-course RAI only |

The comparison shows that, once differing scopes and cost bases are stripped away, Mordor's incidence-anchored model offers the most transparent, repeatable baseline for strategic decision-making.

Key Questions Answered in the Report

What is the current size of the differentiated thyroid cancer therapeutics market?

It stands at USD 0.63 billion in 2025 and is projected to reach USD 1.24 billion by 2030, growing at a 15.1% CAGR.

Which therapy segment is expanding fastest?

Targeted therapy leads with a 17.26% CAGR through 2030, reflecting approvals for drugs such as selpercatinib and repotrectinib.

Why is Asia-Pacific the most attractive growth region?

Rising incidence, broader insurance coverage, and growing access to precision drugs drive a 16.43% CAGR for the region.

How soon will generic competition affect leading TKIs?

Sorafenib generics are already available, and cabozantinib generics may enter from 2031, pressuring branded prices.

What role do radiopharmaceuticals play in future growth?

New isotope manufacturing capacity and alpha-particle therapies underpin a 15.89% CAGR for intravenous products, broadening treatment choices.

Are ambulatory surgical centers gaining share?

Yes. ASCs will grow at 16.34% CAGR thanks to the shift of oral TKIs and minimally invasive procedures away from hospitals.

Page last updated on: