Gynecological Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 12.08 Billion |

| Market Size (2031) | USD 17.62 Billion |

| Growth Rate (2026 - 2031) | 7.86% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Gynecological Devices Market Analysis by Mordor Intelligence

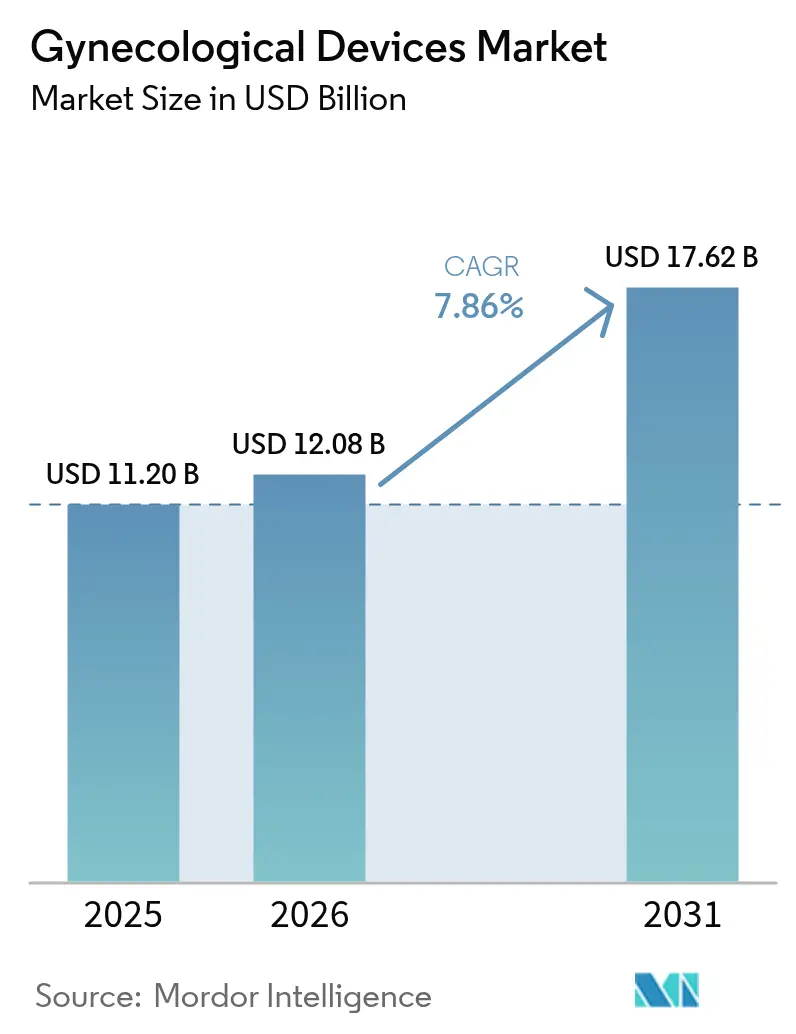

The gynecological devices market size is expected to grow from USD 11.20 billion in 2025 to USD 12.08 billion in 2026 and is forecast to reach USD 17.62 billion by 2031 at 7.86% CAGR over 2026-2031. Rising demand for minimally invasive therapies, rapid technology convergence in endoscopy and imaging, and supportive reimbursement for outpatient procedures are combining to accelerate replacement cycles and spur fresh capital spending by providers. Adoption of artificial-intelligence-enabled diagnostics, next-generation robotic systems with force feedback, and smart contraceptive platforms is reshaping competitive dynamics and intensifying the focus on integrated care pathways. Heightened patient awareness, a growing elderly female population, and value-based payment structures that reward shorter hospital stays are expanding addressable volumes for office-based therapies while simultaneously raising the bar for usability and safety validation. Established brands are leveraging acquisitions to access niche intellectual property, whereas younger entrants are racing to commercialize connected devices that deliver data-driven insights to clinicians.

Key Report Takeaways

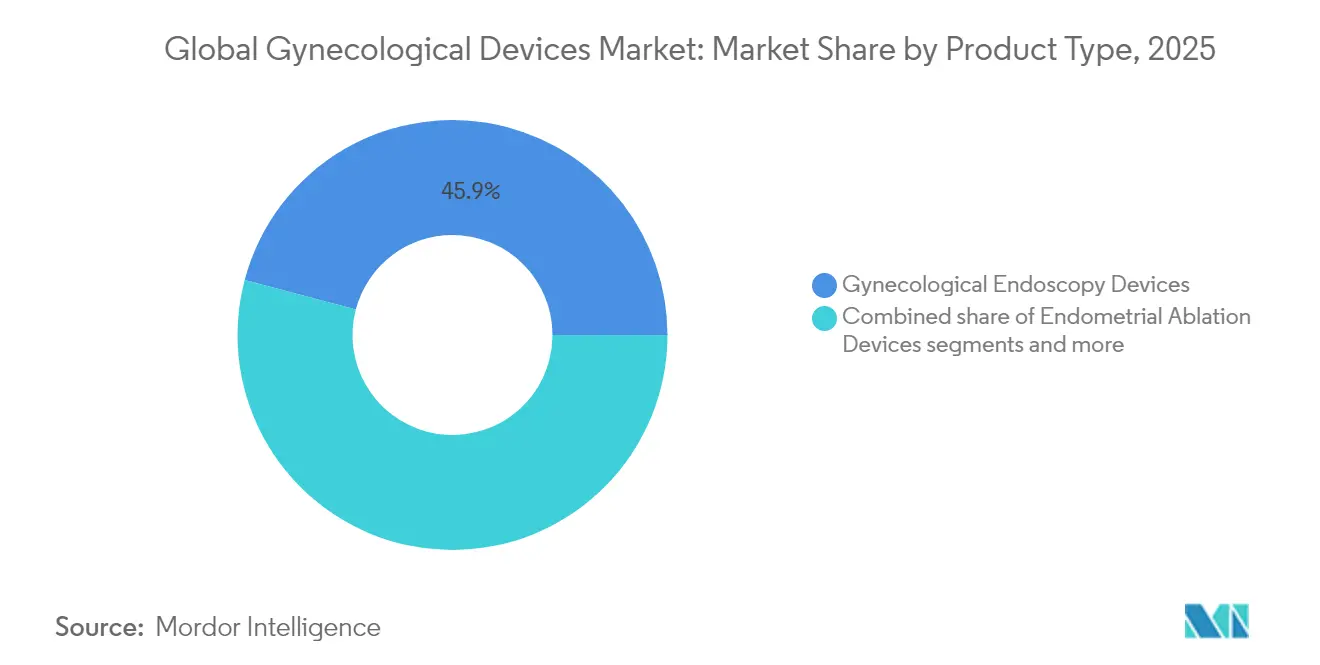

- By product type, gynecological endoscopy devices led with 45.88% revenue share in 2025; endometrial ablation devices are forecast to expand at an 8.54% CAGR to 2031.

- By application, laparoscopy accounted for 37.65% of the gynecological devices market share in 2025 and is advancing at a 9.25% CAGR through 2031.

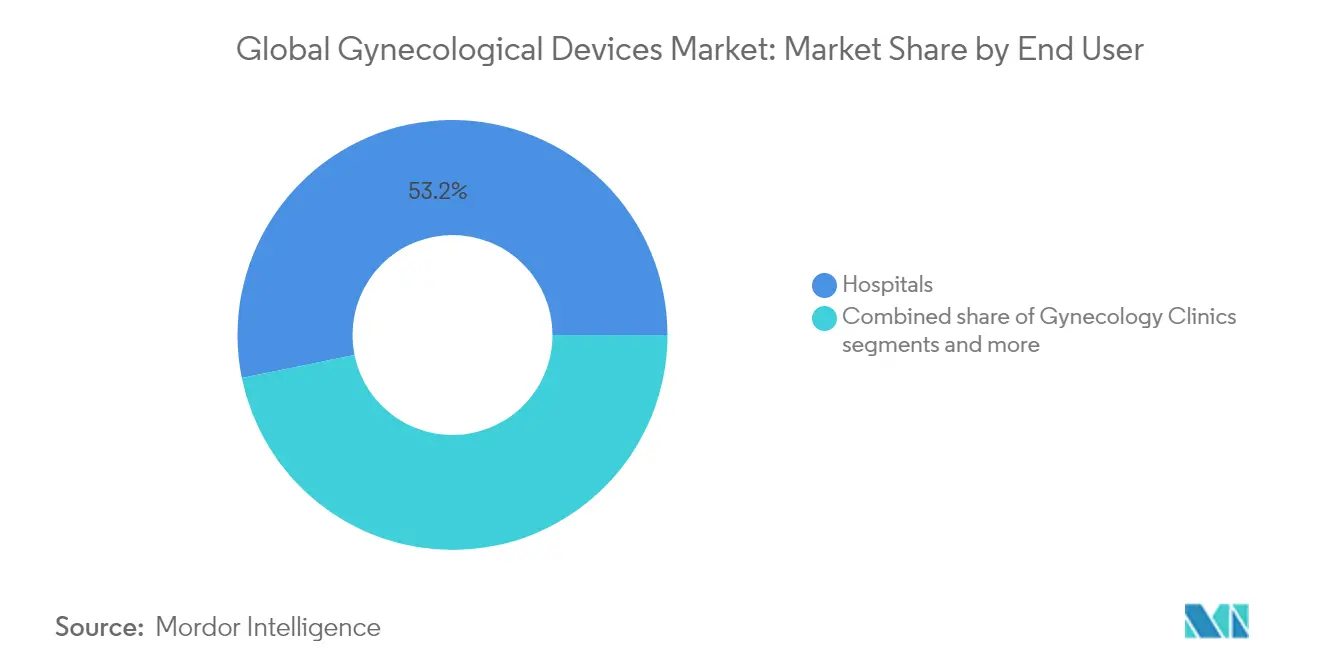

- By end user, hospitals held 53.20% share of the gynecological devices market size in 2025, while gynecological centers record the highest projected CAGR at 9.98% through 2031.

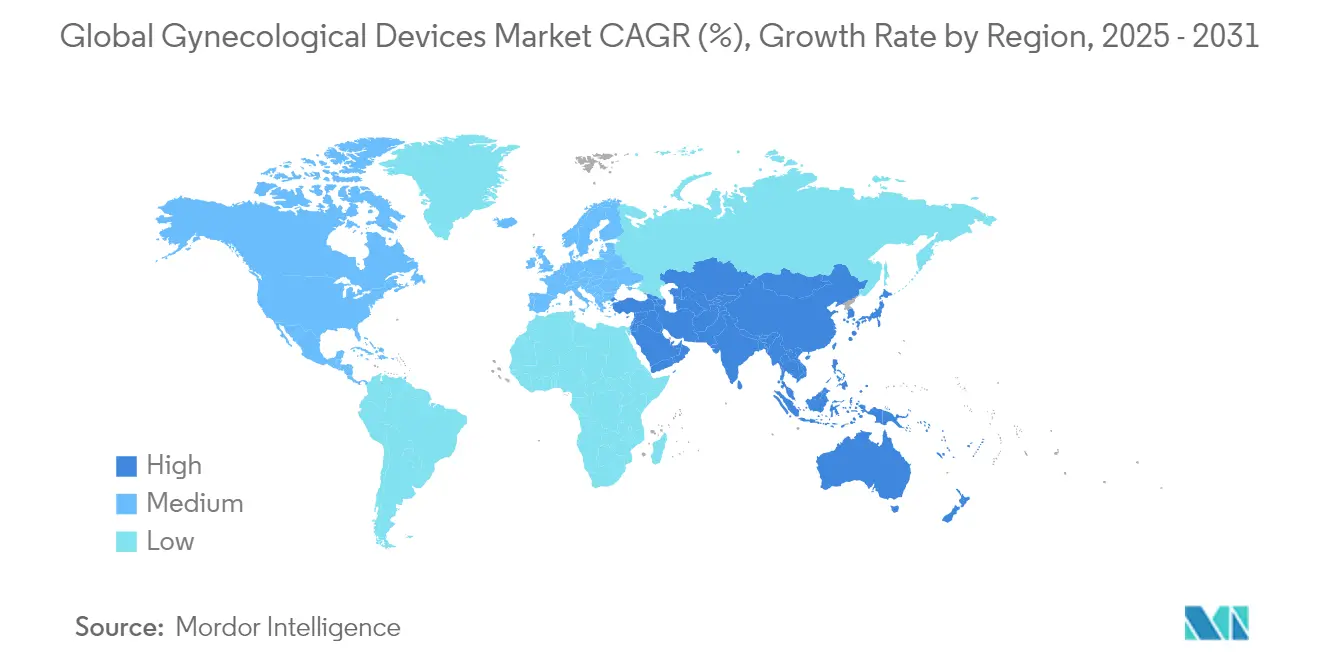

- By geography, North America captured 41.86% share of the gynecological devices market in 2025; Asia-Pacific is set to grow at 10.74% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Gynecological Devices Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Gynecological Disorders | +2.1% | Global with higher impact in North America and Europe | Long term (≥ 4 years) |

| Growing Adoption of Minimally Invasive Surgeries | +1.8% | Global led by North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Technological Advances in OB-GYN Endoscopy and Imaging | +1.5% | North America and Europe core with spill-over to Asia-Pacific | Medium term (2-4 years) |

| Aging Female Population and Higher Healthcare Spend | +1.3% | Global concentrated in developed markets | Long term (≥ 4 years) |

| Outpatient Hysteroscopy Reimbursement Bundling Surge | +0.9% | North America and Europe | Short term (≤ 2 years) |

| FemTech-enabled Smart OB-GYN Instruments | +0.4% | Global with early adoption in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Gynecological Disorders

Chronic and malignant gynecological conditions are increasing in incidence, raising the need for frequent screenings and intervention devices. Cervical and uterine cancers continue to post high mortality in parts of Asia, while incidence in North America remains stable but still drives significant demand for early detection tools. Providers are upgrading colposcopes and biopsy systems that integrate optical enhancements to detect premalignant lesions during first-line exams. Growth momentum is strongest in urban settings where organized screening programs and public awareness campaigns capture patients earlier in disease progression. Parallel investments in home-based diagnostics aim to improve participation rates and relieve hospital capacity constraints. Collectively, these trends increase the installed base of precision instruments and consumables, reinforcing recurring revenue streams for manufacturers.

Aging Female Population and Higher Healthcare Spend

Women older than 50 constitute a steadily rising share of the global population, bringing elevated risk for prolapse, incontinence, and malignant gynecological diseases. In the United States, the annual pelvic organ prolapse surgery cost hit USD 1.523 billion in 2018[1]St Martin, "Estimated National Cost of Pelvic Organ Prolapse Surgery in the United States," Obstetrics & Gynecology, journals.lww.com, with 82.5% of cases managed outpatients. Similar trajectories are emerging in Western Europe, prompting hospitals to adopt cost-efficient, minimally invasive approaches. Higher disposable incomes in developed nations further support elective treatments such as uterine fibroid ablation and long-acting contraception, expanding demand for premium devices with patient-friendly features. On the payer side, improved health coverage in emerging markets unlocks new volumes, though at lower average selling prices.

Growing Adoption of Minimally-Invasive Surgeries

Robotic platforms dedicated to transvaginal and abdominal gynecologic surgery now integrate force feedback and three-dimensional visualization to raise precision. The Hominis system, the first robot cleared for transvaginal hysterectomy[2]SAGES, "Hominis", sages.org, utilizes flexible arms that mimic natural wrist motion, thereby minimizing access trauma. Companion software overlays real-time analytics on surgical fields, guiding less experienced surgeons and reducing learning curves. Parallel improvements in imaging sensors and artificial intelligence-driven tissue recognition allow earlier lesion identification during diagnostic hysteroscopy. Upstream suppliers are investing in chip-on-tip cameras and advanced illumination, stimulating a rapid upgrade wave across provider fleets.

Technological Advances in OB-GYN Endoscopy & Imaging

Procedural migration from open surgery toward laparoscopic and hysteroscopic techniques is well underway, delivering shorter recovery times and lower complication rates. Clinical data show that vNOTES hysterectomy reduces operating time to 80 minutes, compared with 100 minutes for single-port laparoscopy[3]Wenhan Yuan, "Perioperative outcomes of transvaginal natural orifice transluminal endoscopic surgery and transumbilical laparoendoscopic single-site surgery in hysterectomy: A comparative study," International Journal of Gynecology & Obstetrics, pubmed.ncbi.nlm.nih.gov, while maintaining comparable safety. These performance gains spur demand for slimmer scopes, ergonomic hand instruments, and energy systems optimized for ambulatory settings. Enhanced recovery after surgery protocols enable same-day discharge, allowing facilities to increase throughput without the need to build new inpatient beds. The shift also broadens the eligible patient pool to older women with comorbidities, reinforcing procedure volumes and supporting sustained device replacement cycles

Restraints Impact Analysis of Gynecological Devices Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Device Recalls & Litigation | -1.80% | Global, with heightened scrutiny in North America & EU | Long term (≥ 4 years) |

| Heightened FDA/EU MDR Re-classification Hurdles | -1.50% | North America & EU, spill-over to APAC | Medium term (2-4 years) |

| Shortage of Trained Gynecologic Surgeons | -1.20% | Global, with acute shortages in emerging markets | Long term (≥ 4 years) |

| Price Erosion from Generic Laparoscopic Instruments | -1.00% | Global, with competitive pressure intensifying in APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Device Recalls and Litigation

High-profile transvaginal mesh lawsuits and subsequent product withdrawals continue to exert a chilling effect on innovation and procurement. For instance, Johnson & Johnson’s Ethicon division faced a USD 302 million fine for deceptive marketing after the Supreme Court ruled in favor of the State of California in February 2023. Hospitals scrutinize vendor track records more closely, lengthening evaluation cycles and increasing demand for exhaustive post-market surveillance data. Manufacturers redirect R&D budgets toward regulatory compliance, slowing the cadence of new product introductions. At the same time, insurers impose stricter coverage criteria, particularly for implantable devices, dampening near-term procedure growth.

Heightened FDA / EU MDR Re-classification Hurdles

The FDA Quality System Regulation amendments taking effect in February 2026[4]US FDA, "Quality Management System Regulation: Final Rule," fda.gov align US rules with international standards but raise documentation requirements for clinical evidence and manufacturing control. The EU MDR similarly demands expanded technical files and periodic safety updates. Smaller innovators without dedicated regulatory departments face higher costs and longer timelines, deterring entry into high-risk categories. Established players possess the resources to navigate the complexity, cementing their market positions but potentially narrowing the pipeline of disruptive solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Gynecological Devices Market Segment Analysis

By Product Type:

Endoscopy Dominance Faces Ablation DisruptionIn 2025, gynecological endoscopy platforms commanded 45.88% of the gynecological devices market size thanks to their versatility in diagnosing and treating diverse conditions. Continuous improvements in chip-on-tip optics and disposable sheath options simplify office workflows and reduce cross-contamination risks. However, endometrial ablation devices are projected to post an 8.54% CAGR through 2031, outpacing every other product class. Second-generation balloon and radiofrequency systems deliver higher amenorrhea rates and fit within reimbursement bundles that reward same-day discharge. Their rapid uptake is steering capital budgets away from legacy resectoscopes. Contraceptive devices remain a resilient revenue base, highlighted by the 2025 approval of Miudella, which uses half the copper of earlier IUDs yet maintains 99% efficacy.

Miniaturized hysteroscopes, such as the 3.1 mm Olympus HYF-XP, facilitate dilation-free access, opening hysteroscopy to smaller clinics with limited anesthesia capabilities. Diagnostic imaging systems are converging toward unified towers that integrate fluorescence, ultrasound, and AI analysis to streamline operating-room footprints. Fluid management remains mission-critical as new pumps with real-time pressure monitoring aim to curb fluid overload complications. Overall, product choice is tilting toward multi-modality platforms that compress procedure times and minimize inventory while embedding software hooks for future analytics upgrades.

By Application:

Laparoscopy Leadership Challenged by Ablation GrowthLaparoscopy held 37.65% of the gynecological devices market share in 2025, underpinned by its broad indications across benign and oncologic surgeries. Robotic assistance, extended reality guidance, and articulating instrumentation continue to enhance laparoscopy outcomes, keeping the technique at the forefront of complex pelvic procedures. Nonetheless, endometrial ablation applications are forecast to expand at a 9.25% CAGR to 2031 as providers pivot to minimally invasive solutions for abnormal uterine bleeding. Radiofrequency-induced ablation shows promise in postpartum hemorrhage management, offering rapid hemostasis with lower morbidity than hysterectomy.

Hysteroscopy volumes are rising in parallel, driven by office-based adoption and improved patient tolerance achieved through smaller scopes and localized anesthesia. Dilation and curettage usage is in gradual decline as suction-based evacuation and ablation gain preference for miscarriage and heavy bleeding cases. Colposcopy benefits from AI-assisted lesion mapping that elevates diagnostic yield, while demand for female sterilization is resilient in markets emphasizing permanent contraception. Emerging applications, including fertility-preservation cryotherapies and in-uterus drug delivery, hint at future revenue streams tied to regenerative and precision medicine paradigms.

By End User:

Hospital Dominance Meets Specialized Center GrowthHospitals controlled 53.20% of overall 2025 revenues due to their capacity to conduct high-acuity surgeries and host advanced imaging suites. They remain the primary purchasers of integrated robotic platforms and multi-tower visualization systems. However, gynecological specialty centers are projected to grow at 9.98% CAGR through 2031, propelled by payer incentives for lower-cost outpatient settings and patient preference for streamlined care experiences. These centers optimize throughput by standardizing procedure protocols and investing in single-use instruments that eliminate reprocessing overhead.

Ambulatory surgery centers benefit from relaxed regulatory frameworks in North America that permit a broader range of gynecological procedures outside hospitals. Fertility clinics, fueled by delayed childbearing trends, are scaling laboratories and cryostorage facilities, boosting demand for precision aspiration needles and hormone monitoring kits. Research institutes continue to act as early adopters of experimental devices, piloting novel energy modalities and data-driven diagnostic tools before commercial rollout. This diversified end-user mix stabilizes demand across economic cycles and cushions suppliers from reimbursement volatility in any single channel.

Geography Analysis

North America Gynecological Devices Market

North America retained 41.86% share of the gynecological devices market in 2025, supported by robust reimbursement, widespread robotic surgery adoption, and continuous refresh of imaging infrastructure. Providers prioritize capital projects that shorten procedure times and enable outpatient migration, creating steady pull for AI-enabled visualization and ergonomically optimized instrumentation. Strategic acquisitions, such as Boston Scientific’s USD 3.7 billion purchase of Axonics, underscore the region’s appetite for neuromodulation and other high-growth adjacencies that complement core surgical franchises.

Europe Gynecological Devices Market

Europe remains a key market, though growth is tempered by the resource demands of MDR compliance. Health systems encourage reuse and sustainability initiatives, steering procurement toward devices with validated reprocessing protocols or recyclable components. Investment in office-based hysteroscopy has accelerated, aided by bundled payments that incentivize day-case care. European research hubs foster collaborations between hospitals and technology firms, driving pilot programs for AI-guided colposcopy and smart tampon diagnostics.

APAC Gynecological Devices Market

Asia-Pacific is projected to deliver the fastest 2026-2031 expansion at a 10.74% CAGR as governments pour resources into maternal health and cancer screening programs. Rising disposable incomes and urbanization improve access to private care, where demand skews toward minimally invasive and fertility services. Local manufacturers are scaling up to compete globally, aided by harmonized regulatory pathways and export-oriented policies. Telemedicine is extending specialist reach into rural settings, lifting adoption of portable ultrasound and at-home monitoring kits.

Regulatory Landscape

Regulation in the gynecological devices market is shaped by risk-based device rules alongside oversight for drug-device combinations. In the United States, many gynecological devices fall under 21 CFR Part 884, while combination products follow a Primary Mode of Action (PMOA) determination that assigns a lead FDA center (CDRH, CDER, or CBER) and sets the premarket pathway and postmarket obligations.

A key compliance inflection is the FDA Quality Management System Regulation (QMSR) transition taking effect in February 2026, which updates quality-system expectations by incorporating ISO 13485:2016 by reference. For combination products, FDA activity also includes the June 2025 draft guidance on Unique Device Identifier (UDI) requirements for combination products, raising implementation expectations for device constituent parts. In Europe, EU MDR requirements and Article 117 workflows for integral drug-device combinations increase the focus on technical documentation, General Safety and Performance Requirements (GSPR) evidence for device components, and coordination with Notified Bodies and the EMA for marketing authorization submissions.

Value Chain Analysis

The value chain covers component and material inputs (optics, electronics, and surgical-grade metals for endoscopy and energy systems, medical-grade polymers for catheters and disposable accessories), then moves through precision manufacturing, assembly, and validation. For drug-device combination segments such as hormonal implants and certain intrauterine systems, upstream activities add API production and polymer compounding, followed by controlled dosing or assembly steps and sterile packaging. In both the US (PMOA) and Europe (EU MDR plus Article 117 expectations for integral combinations), classification affects process controls, documentation, and how deeply suppliers are qualified.

Downstream, distribution runs through hospital and outpatient procurement channels, with service, training, and consumables logistics (single-use accessories, fluid management disposables, and device kitting) contributing to lifetime economics. Bottlenecks typically include sterile manufacturing capacity, sterilization validation, and re-qualification timelines when critical suppliers change, as well as the need for CDMO support for cleanroom assembly and documentation in combination-product programs. These requirements drive dual-sourcing strategies for sensitive inputs (selected polymers, electronics, and APIs where applicable) and favor earlier engagement with regulators and Notified Bodies to reduce rework during submission cycles.

Competitive Landscape

The gynecological devices market displays moderate consolidation as incumbents leverage acquisitions to secure differentiated intellectual property and expand geographical coverage. Hologic’s USD 350 million takeover of Gynesonics broadens its fibroid treatment suite and locks in future recurring revenue from single-use RF applicators. Karl Storz’s purchase of Asensus Surgical grants access to the LUNA next-generation robotic platform, adding a digital interface and performance analytics to its endoscopy core.

Technology rivalry centers on robotics and AI. Johnson & Johnson’s OTTAVA system, now in US clinical trials, employs four low-profile arms that integrate seamlessly with existing OR layouts, signaling competitive pressure on Intuitive Surgical’s da Vinci franchise. Force feedback modules and automated camera alignment seek to shorten learning curves and democratize advanced laparoscopy across mid-volume hospitals. Meanwhile, start-ups in FemTech are carving space with connected contraceptive platforms and remote pelvic-floor therapy, enticing strategic investors with data monetization opportunities.

Pricing remains under scrutiny as payers tie reimbursement to proven outcomes. Vendors that bundle devices with analytics software and training demonstrate higher retention and resistance to commoditization. Supply-chain resilience, highlighted during recent semiconductor shortages, is now a purchase criterion, prompting manufacturers to dual-source critical components and invest in regional assembly facilities. Competition is poised to intensify as Chinese and South Korean firms scale exports, backed by cost advantages and improving design capabilities.

Gynecological Devices Industry Leaders

-

Boston Scientific Corporation

-

Hologic, Inc.

-

Medtronic PLC

-

Olympus Corporation

-

Stryker Corporation

- *Disclaimer: Major Players sorted in no particular order

Gynecological Devices Market Companies Covered in this Report

- Hologic

- Boston Scientific

- Johnson & Johnson

- Medtronic

- The Cooper Companies

- Karl Storz

- Olympus

- Stryker

- Cook Group

- Richard Wolf

- Intuitive Surgical

- B. Braun

- Coloplast

- Beckton Dickinson

- Conmed

- Teleflex

- Minerva Surgical

- Lumenis

Market Opportunities and Future Outlook

White-space opportunities are most visible where outpatient migration and tighter safety expectations intersect with workflow pain points. Fluid management and containment solutions stand out, since office and ambulatory hysteroscopy growth increases demand for integrated pumps, pressure monitoring, and simpler setup, while hospitals look for validated systems that reduce procedural variability and cross-contamination burden. Portfolio strengthening is also continuing, including Boston Scientific receiving FDA 510(k) clearance for the Asurys Fluid Management System in March 2026, which reinforces investment in procedure-enabling infrastructure that supports higher-throughput gynecology settings.

Drug-device combination and long-acting contraception platforms offer additional opportunity through durability, adherence, and differentiated materials science. In January 2026, Organon secured FDA approval for a supplemental NDA extending NEXPLANON use from three to five years, illustrating how lifecycle extensions can reshape replacement cycles and counseling pathways in contraceptive care. The same direction is showing up in minimally invasive and robotic gynecologic surgery, where instruments and digital layers that shorten learning curves and standardize outcomes create space for differentiation; Medtronic submitting FDA 510(k) filings in June 2026 to expand Hugo robotic-assisted surgery into gynecologic indications reflects active competitive investment in this direction. Regulatory complexity remains a gate, so programs that align quality-system readiness (including the FDA QMSR transition) with submission planning and combination-product evidence generation can improve the pace of commercialization across regions.

Recent Industry Developments in Gynecological Devices Market

- June 2026: Medtronic announced it submitted 510(k) filings to the US FDA to expand the indications for its Hugo robotic-assisted surgery system into gynecologic and general surgery procedures. The update also noted completion of enrollment in the Embrace Gynecology IDE clinical study, supporting broader clinical and regulatory positioning for robotic-assisted gynecology workflows.

- January 2025: Hologic completed its acquisition of Gynesonics for about USD 350 million, adding the Sonata system for transcervical treatment of symptomatic uterine fibroids. The deal deepened Hologic's minimally invasive therapy footprint in womens health and strengthened its offering beyond diagnostics into procedure-based care.

- November 2024: Boston Scientific closed its USD 3.7 billion acquisition of Axonics, expanding into implantable neuromodulation used in conditions including overactive bladder. The move broadened Boston Scientific's pelvic health portfolio and added a durable implant franchise adjacent to gynecology and urology pathways.

Gynecological Devices Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers medical devices used to diagnose, monitor, or treat conditions related to the female reproductive system, across hospital and outpatient care settings, and across the full care pathway from screening to procedure and follow-up.

Scope exclusions: We exclude pharmaceuticals and hormones, general surgical consumables, and standalone obstetric devices that are not primarily used for gynecologic diagnosis or procedures.

Segments Covered in This Report

-

By Product Type (Value)

-

Gynecological Endoscopy Devices

- Hysteroscope

- Resectoscope

- Colposcope

- Laparoscope

- Endoscopic Imaging Systems

-

Endometrial Ablation Devices

- Balloon Ablation Devices

- Hydrothermal Ablation Devices

- Radiofrequency Ablation Devices

- Other Endometrial Ablation Devices

-

Contraceptive Devices

- Temporary Birth Control

- Permanent Birth Control

- Diagnostic Imaging Systems

- Fluid Management Systems

- Other Product Types

-

Gynecological Endoscopy Devices

-

By Application (Value)

- Laparoscopy

- Hysteroscopy

- Dilation & Curettage

- Colposcopy

- Endometrial Ablation

- Female Sterilization

- Others

-

By End User (Value)

- Hospitals

- Gynecology Clinics

- Ambulatory Surgery Centers

- Fertility Centers

- Research & Academic Institutes

-

By Geography (Value)

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by grounding the demand pool and procedure environment using public sources such as the World Health Organization (WHO), the US Centers for Disease Control and Prevention (US CDC), and national health ministries that publish women's health and screening statistics. We also refer to sources such as the Organisation for Economic Co-operation and Development (OECD), the World Bank, and customs or trade statistics portals to understand healthcare spending direction, import-export flows, and region-level access trends.

Next, we build supply and adoption context using company annual reports and filings, investor presentations, product literature, and recall or safety updates published by regulators such as the US FDA. To support consistency checks, we also use paid subscriptions for company financials and intelligence, patent databases, and tender tracking where available to sense product rollouts and replacement activity. The sources listed here are illustrative, and many other public documents and datasets were also reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure test what we saw in desk research, especially around procedure mix changes, device replacement cycles, and how pricing moves across hospital systems and clinics. We speak with a mix of manufacturers, distributors, clinicians, procurement teams, and service providers across APAC, EMEA, and the Americas so assumptions get challenged from both the supply and care delivery sides.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 17% | APAC: 47% |

| Mid tier: 53% | Functional/Unit leaders: 23% | EMEA: 30% |

| Smaller Players: 20% | Managers: 60% | Americas: 23% |

Market-Sizing & Forecasting

The sizing model is built using top-down logic where procedure volumes and diagnosed or treated cohorts are reconstructed by major geographies, and then mapped to typical device use per procedure and expected pricing. Once the demand pool is formed, we apply adjustment factors for access to minimally invasive care, care setting shifts, and replacement-driven purchases, which is often where the totals move the most.

To keep the outputs practical, the model uses a small set of trackable inputs such as laparoscopy and hysteroscopy procedure activity, screening and diagnostic imaging utilization, prevalence of conditions such as fibroids and abnormal uterine bleeding that drive interventions, hospital versus clinic share, and average selling price bands by device group (endoscopy, ablation, contraception, fluid management, and related tools). Where local data is thin, assumptions are filled using proxy indicators like healthcare spending direction and peer-country procedure intensity, and then refined through channel checks and interview feedback.

For forecasting, scenario analysis is used so the base case can be stress-tested against faster adoption of minimally invasive techniques, slower capital budgets, and pricing pressure from procurement. The forecast trajectory is then sanity checked using selective bottom-up approximations, such as sampled average selling prices (ASPs) times implied unit demand, and supplier and distributor roll-ups in a few anchor countries to confirm the order of magnitude.

Data Validation & Update Cycle

Validation happens in layers, starting with cross-checks between procedure-linked demand signals, device category totals, and regional healthcare spending patterns, before numbers are finalized. Outliers are flagged and reviewed in an analyst pass that looks for breaks in logic, unusual year-to-year jumps, and currency effects that can distort the picture.

If a variance cannot be explained through published data, we re-contact relevant interviewees and re-check the assumption that created the gap, and then the model is re-run with the updated input. Reports are refreshed annually, and interim updates are made when material events occur that can shift volumes or pricing, such as major guideline changes, recall activity, or large reimbursement moves. Before delivery, a fresh review is completed so clients receive the latest updated view.

Mordor Intelligence's Gynecological Devices Market Sizing Compared With Other Published Estimates

Published market sizes for gynecological devices can look different even when the topic name is similar, because each publisher draws the boundary in its own way and applies different pricing and geography treatments. Differences also come from how procedure-linked demand is translated into device value, and how often the underlying assumptions are revisited.

Key gaps usually show up in what gets counted as a gynecological device (for example, whether broad diagnostic imaging systems are fully included or only the gynecology-specific use case), which year is treated as the base, and how pricing is projected during the forecast window. Currency conversion timing, the share split between hospitals and clinics, and the approach to minimally invasive procedure growth can also change the final number in a meaningful way.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 12.08 B (2026) | |

| Global Consultancy A | USD 11.38 B (2025) | Uses an earlier base year and a longer forecast window, and its product buckets appear to emphasize surgical and imaging groupings that can shift what is counted under gynecology versus general care equipment. |

| Research Publisher B | USD 10.09 B (2024) | Anchors the market in 2024 and reports a broader 10-year outlook, which can embed different pricing progression and adoption assumptions for minimally invasive procedures across regions. |

Procedure activity signals and category-level consistency checks are what keep Mordor Intelligence tied to a clear treated demand pool for endoscopy, ablation, contraception, diagnostic imaging, and fluid management, which then reduces over-counting from adjacent device categories. Taken together, the spread across the table is mainly explained by base-year choice, scope boundaries around imaging and tools, and how pricing and adoption are carried forward into the forecast.

Key Questions Answered in the Report

What is the current size of the gynecological devices market?

The gynecological devices market size reached USD 12.08 billion in 2026 and is projected to grow to USD 17.62 billion by 2031.

Which product category holds the largest share?

Gynecological endoscopy devices led with 45.88% revenue share in 2025.

Which region is expanding the fastest?

Asia-Pacific is forecast to post a 10.74% CAGR from 2026 to 2031, the quickest among all regions.

What technology trends are reshaping competition?

Adoption of robotics with force feedback, AI-assisted imaging, and connected FemTech devices are driving vendor differentiation.

Page last updated on: