Assisted Reproductive Technology (ART) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

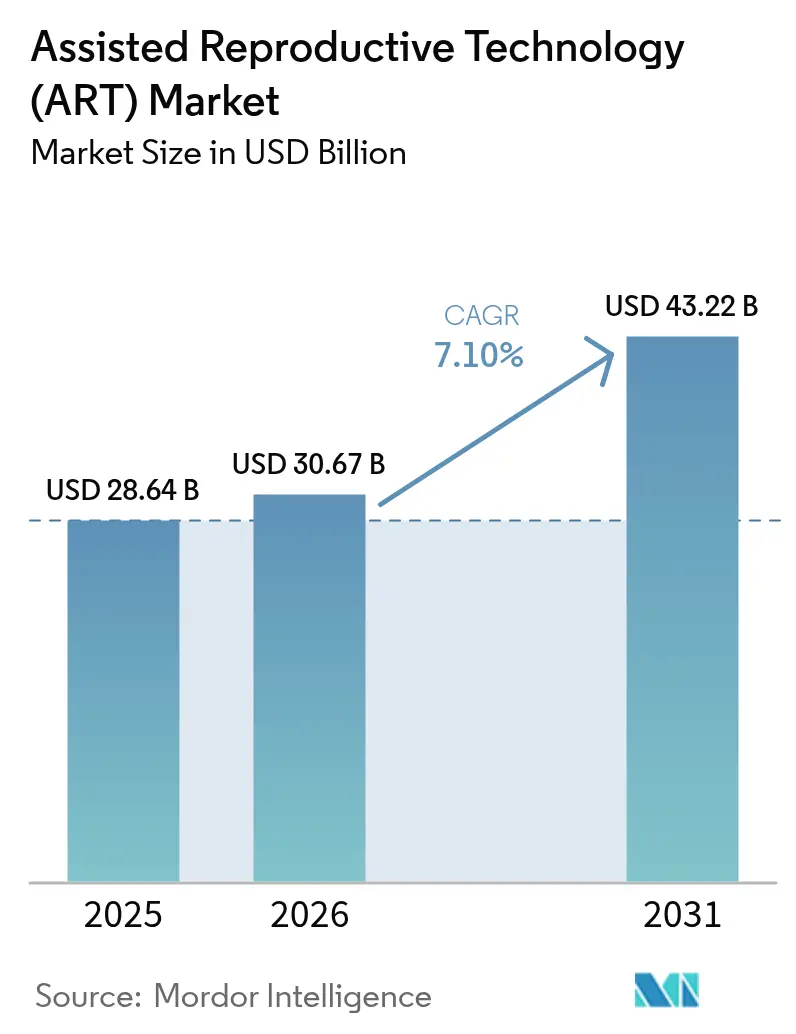

| Market Size (2026) | USD 30.67 Billion |

| Market Size (2031) | USD 43.22 Billion |

| Growth Rate (2026 - 2031) | 7.10% CAGR |

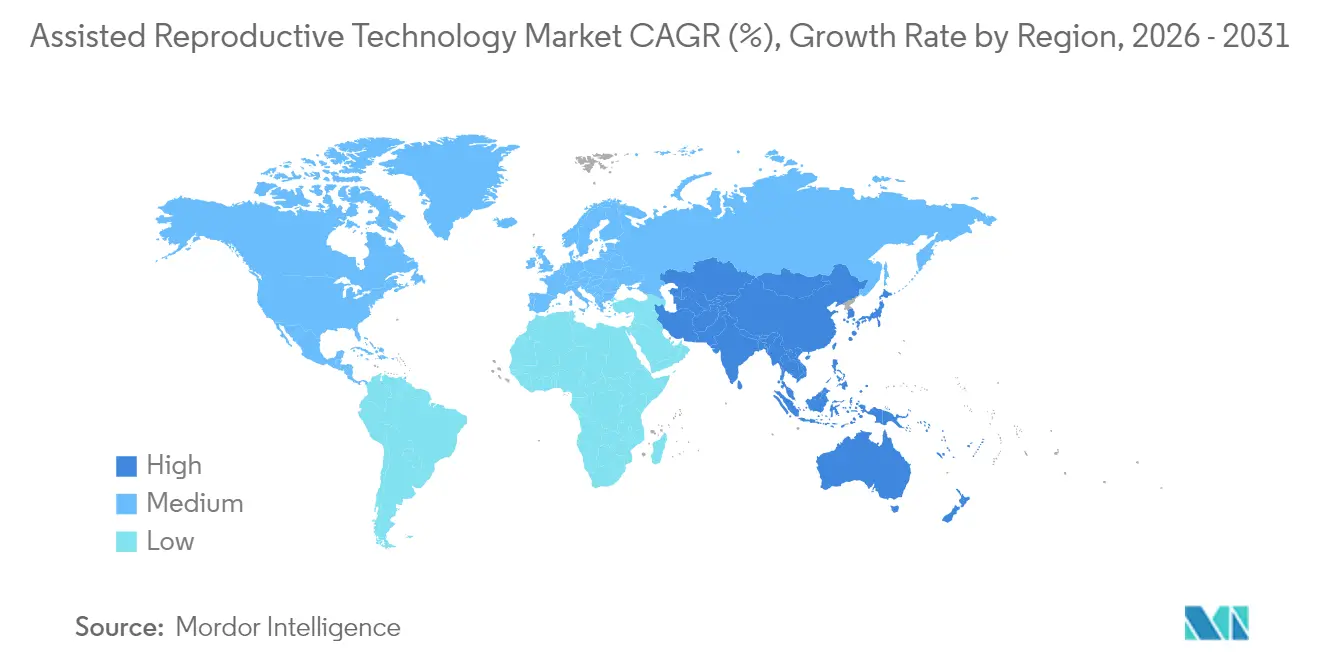

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

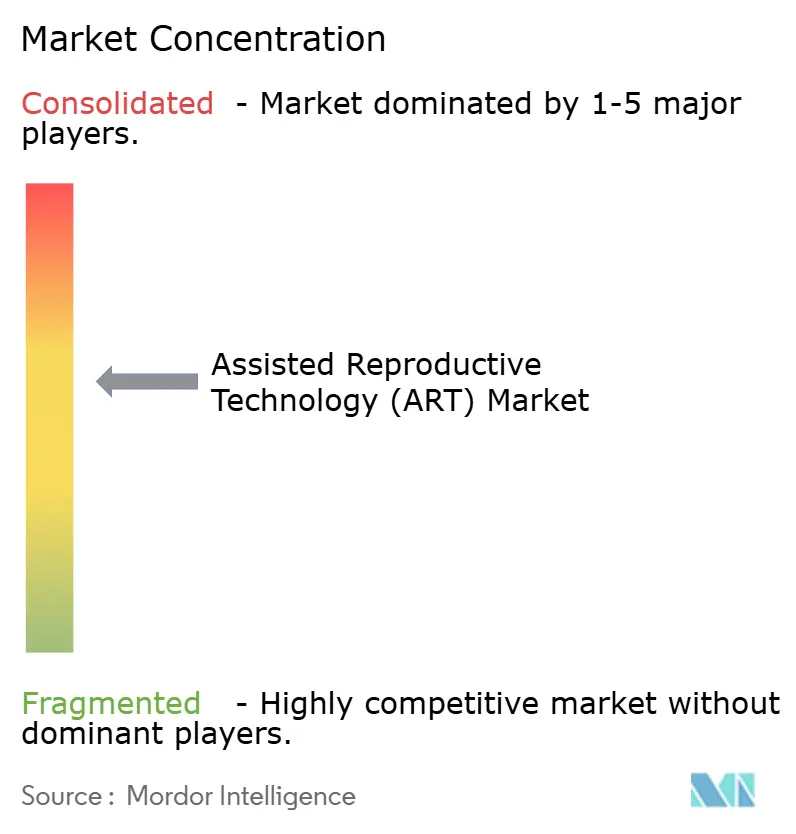

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Assisted Reproductive Technology (ART) Market Analysis by Mordor Intelligence

The assisted reproductive technology market size is expected to grow from USD 28.64 billion in 2025 to USD 30.67 billion in 2026 and is forecast to reach USD 43.22 billion by 2031 at 7.1% CAGR over 2026-2031. Adoption accelerates as artificial intelligence (AI) reaches 70–97% accuracy in embryo selection, improving clinical decisions while cutting laboratory workload. Private-equity capital flows underscore sector resilience, exemplified by Astorg’s agreement to buy Hamilton Thorne at a 54% premium, signalling confidence in mission-critical laboratory platforms. Employer-sponsored fertility benefits now cover 40–42% of United States workers, broadening the paying patient pool and stabilising revenues for the assisted reproductive technology market[1]SHRM Staff, “Employer-Provided Fertility Benefits Continue to Grow,” shrm.org. Regionally, Asia-Pacific’s rapid clinic roll-out and China’s fertility policy support drive the fastest growth, while Europe readies for the 2027 Regulation on Substances of Human Origin that will harmonise quality standards across borders.

Key Report Takeaways

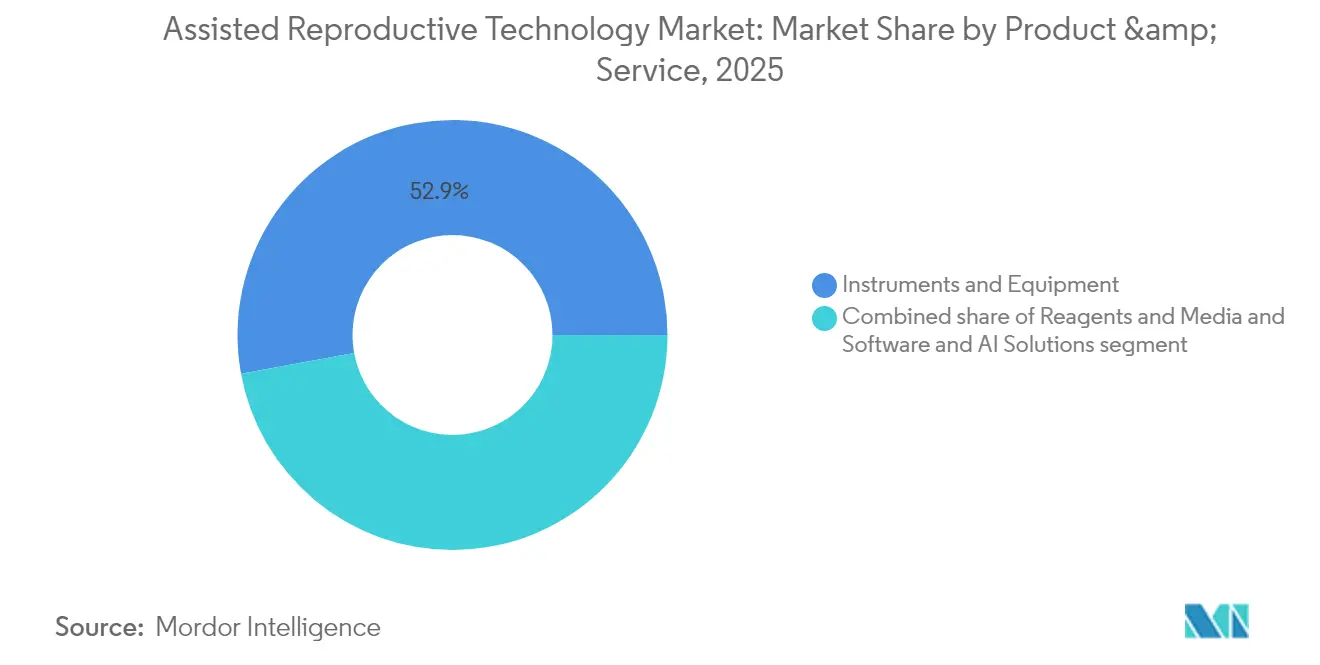

- By product & service, Instruments & Equipment led with 52.88% revenue share in 2025; Software & AI Solutions are set to climb at a 9.25% CAGR to 2031.

- By technology, in-vitro fertilisation held 63.72% of assisted reproductive technology market share in 2025, while Frozen Embryo Replacement is forecast to expand at a 9.18% CAGR through 2031.

- By procedure, Fresh Non-Donor cycles accounted for 44.12% of the assisted reproductive technology market size in 2025; Frozen Donor cycles are advancing at an 8.31% CAGR to 2031.

- By end user, Fertility Clinics captured 78.02% of revenue in 2025; Hospitals & Surgical Centres are growing fastest at 10.05% CAGR as integrated women’s-health hubs.

- By geography, North America commanded 45.01% of the assisted reproductive technology market size in 2025, whereas Asia-Pacific is projected to post an 8.38% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Assisted Reproductive Technology (ART) Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global infertility prevalence | +1.2% | Asia-Pacific, Middle East, Global spillover | Long term (≥ 4 years) |

| Increasing acceptance of assisted reproductive procedures | +0.9% | North America, Europe → Asia-Pacific | Medium term (2-4 years) |

| Rapid technological innovations in reproductive medicine | +1.8% | North America & Europe lead, Global reach | Short term (≤ 2 years) |

| Growth of cross-border fertility services | +0.7% | Europe & Asia-Pacific hubs, Middle East inflows | Medium term (2-4 years) |

| Integration of artificial intelligence in embryo selection | +1.1% | North America, Europe, select Asia-Pacific | Short term (≤ 2 years) |

| Expansion of employer-sponsored fertility benefits | +0.8% | North America, early adoption in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global Infertility Prevalence

Female infertility in Asia-Pacific rose markedly, with polycystic ovary syndrome (PCOS) cited as a major driver. Demographic infertility in some Middle-Eastern countries stands at 38.5%, far above the 3.8% clinical infertility rate, indicating large latent demand. Lifestyle shifts—urban stress, dietary change, occupational toxins—further erode reproductive health across age groups. Policymakers increasingly frame infertility as a public-health issue requiring systematic intervention. Together, these factors sustain long-run volume growth for the assisted reproductive technology market.

Increasing Acceptance of Assisted Reproductive Procedures

Organised Indian clinic chains now capture 35–40% of national IVF cycles—up from zero 10 years ago—showing stigma decline and brand-led consolidation. All EU members fund IVF after Poland reinstated reimbursement in 2025, signalling pan-European support. U.S. companies promote fertility benefits to attract talent; 66% of employees weigh reproductive-health perks in job decisions. Visibility rises as LGBTQIA+ populations, single parents and celebrity advocates normalise usage. Societal openness drives patient inflows and stabilises payer mix for the assisted reproductive technology market.

Rapid Technological Innovations in Reproductive Medicine

The world’s first fully automated intracytoplasmic sperm injection (ICSI) birth occurred in 2025, validating robotised precision. AI models such as BELA predict embryo ploidy with 70–80% accuracy, reducing reliance on invasive tests. Time-lapse incubators safeguard culture consistency despite mixed live-birth evidence. Gameto’s iPSC-based Fertilo, now in Phase 3 trials, aims to cut hormone injections by 80%. These innovations increase success rates and lower per-cycle costs, deepening technology-driven competitive moats.

Growth of Cross-Border Fertility Services

An estimated 25,000 couples now travel each year for reproductive care, chasing legal, price and quality advantages. Spain, Denmark and Belgium attract Europeans under liberal laws and high lab standards. India offers IVF for USD 2,700 versus USD 10,200 in Singapore, drawing medical tourists keen on lower bills. Harmonised EU safety rules may further smooth patient flows by 2027. However, disparities in patient-rights protection spur calls for global accreditation frameworks to shield outcomes and data.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High treatment costs and limited insurance coverage | −1.4% | Emerging markets & United States | Long term (≥ 4 years) |

| Stringent and evolving regulatory frameworks | −0.8% | Europe, Asia-Pacific → Global effects | Medium term (2-4 years) |

| Ethical and religious concerns regarding embryo manipulation | −0.6% | Middle East, Latin America, parts of Asia | Long term (≥ 4 years) |

| Clinical variability and uncertain success rates | −0.5% | Global, accentuated in new or smaller clinics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Treatment Costs and Limited Insurance Coverage

United States IVF averages USD 12,000–25,000 per cycle, with 2.5 cycles typically needed, thrusting many households above USD 30,000 in expenses. Only 21 U.S. states mandate partial infertility coverage, leaving sizeable gaps. Nearly 28% of employees entering treatment incur debt, disproportionately burdening marginalized groups. Internationally, cycle costs vary from EUR 4,000 in many EU states to higher levels in developed Asia, spurring outbound medical tourism that can fragment follow-up care. Without broader reimbursement, cost remains the steepest barrier to assisted reproductive technology market participation.

Stringent and Evolving Regulatory Frameworks

The U.S. Food and Drug Administration is phasing in supervision of laboratory-developed tests, raising compliance investment for PGx and embryo-screening labs[2]Federal Register, “Laboratory Developed Test Proposed Rule,” federalregister.gov. Alabama’s 2024 ruling deeming frozen embryos “children” forced clinic suspensions amid liability concerns. Europe’s new SoHO regulation sets continent-wide traceability rules due 2027, demanding extensive documentation upgrades. Divergent embryo-research laws in Asia create export licensing snags. Heightened oversight lifts costs and can slow the commercial rollout of breakthrough platforms inside the assisted reproductive technology market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product & Service: Software Integration Drives Equipment Evolution

Instruments & Equipment generated 52.88% of 2025 revenue, underscoring laboratories’ dependence on high-value capital assets for incubating, imaging and micromanipulating gametes. Software & AI Solutions will grow at 9.25% CAGR to 2031 as clinics chase predictive analytics that boost implantation odds. Vendors increasingly bundle microscopes with AI algorithms-such as EmbryoScope+ paired with iDAScore-to offer an integrated decision-support workflow. Automation pioneers including Conceivable Life Sciences deploy AURA, the first fully robotic IVF lab, processing 2,000 cycles a year while slashing headcount.

Recurring consumables remain crucial. Culture media sales track cycle volume because every retrieval triggers new batches, stabilising revenue even during downturns. Meanwhile, the assisted reproductive technology market size linked to laboratory service contracts is expanding as manufacturers introduce subscription models for continuous software updates and remote calibration. These hybrid hardware-software offerings deepen switching costs and create stickier cash flows, attracting private-equity capital.

Digitalisation also fosters data-sharing networks that feed machine-learning models, widening performance gaps between adopters and laggards. Clinics using AI allocation protocols have reported 13.6% higher success rates after chain acquisition due to standardised best practices. Over 2026-2031, product roadmaps show a clear pivot from stand-alone instruments toward cloud-enabled ecosystems that monetise both disposables and proprietary datasets.

By Technology: Cryopreservation Advances Enable Procedure Flexibility

In-Vitro Fertilisation preserved technological primacy with 63.72% 2025 share, benefiting from decades of know-how and broad reimbursements. Yet elective freeze-all strategies fuel a 9.18% CAGR for Frozen Embryo Replacement cycles, which allow chromosomal screening and flexible scheduling without hormone-related endometrial stress. Clinics report fewer multiple pregnancies after vitrification plus single-embryo transfer protocols-an increasingly mandated quality metric.

Emerging science reshapes the technology stack. Induced-pluripotent-stem-cell methods, exemplified by Fertilo, could lower ovarian stimulation exposure by 80% while compressing treatment duration to three days. Research into in-vitro gametogenesis hints at lab-grown gametes that may open new parenthood routes for severe male-factor or same-sex couples. For now, artificial insemination persists as a lower-complexity option but surrenders share to IVF variants as payers recognise higher overall success per investment.

Clinicians increasingly tailor technology bundles-combining vitrified embryos, PGT-A genetic testing and AI scoring-to patient-specific prognostics, reducing miscarriage risk while optimising cost per live birth. That personalisation further enlarges the assisted reproductive technology market as older patients consider treatment viable.

By Procedure: Genetic Testing Integration Reshapes Treatment Protocols

Fresh Non-Donor cycles held 44.12% revenue in 2025 because many patients still attempt immediate transfer. Yet Frozen Donor procedures, rising 8.31% CAGR, address diminished ovarian reserve and hereditary-disease avoidance via donor gametes alongside vitrification. Widespread pre-implantation genetic testing sparks a move toward freeze-all, letting labs perform chromosomal assays before selecting embryos.

Policy developments broaden eligibility. The U.S. Department of Veterans Affairs now funds IVF for unmarried veterans and authorises donor gametes, enlarging the candidate pool. AI-boosted decision models predict patient-specific live-birth probability, helping clinics choose among procedure types. Some chains report >50% pregnancy rates when algorithms guide embryo selection.

Ethical oversight intensifies, yet demand for bespoke donor banks grows, particularly among cross-border patients seeking specific phenotype matches. Sophisticated cryobank logistics integrate radio-frequency tracing to maintain chain-of-custody compliance across borders, strengthening trust in the assisted reproductive technology market.

By End User: Hospital Integration Accelerates Service Expansion

Fertility Clinics generated 78.02% of 2025 revenue, thanks to specialised staff and purpose-built labs. Hospitals & Surgical Centres, however, will log 10.05% CAGR through 2031 as integrated health systems bundle reproductive care with obstetrics, oncology and endocrinology, capturing lifetime patient value. Large networks install dedicated IVF suites, leveraging established electronic-health-record infrastructure to streamline referrals.

Chain ownership enhances performance: acquired clinics have shown 27.2% cycle-volume gains post-integration. Hospitals emulate this scale, negotiating bulk reagent contracts and embedding fertility dashboards in enterprise analytics platforms. Cryobanks and research institutes continue niche roles-long-term storage and advanced genome editing research-but also become data nodes feeding AI algorithms.

Patient expectations for one-stop women’s-health journeys advance hospital participation. Insurance carriers increasingly direct patients to in-network hospitals that meet quality metrics, creating managed-care pull-through. These shifts diversify the assisted reproductive technology industry’s revenue channels and mitigate standalone clinic concentration risk.

Geography Analysis

North America controlled 45.01% of 2025 revenue, buoyed by premium pricing and rising employer benefits that absorb high cycle costs. The assisted reproductive technology market size in this region also reflects ongoing automation pilots and an ecosystem of software vendors clustered around biomedical corridors. U.S. reimbursement expansion through corporate plans continues to offset uneven state mandates, whereas Canada’s single-payer system covers limited cycles, prompting some patients to seek private U.S. services and sustaining cross-border flows.

Asia-Pacific is projected to exhibit an 8.38% CAGR to 2031, the fastest among regions. India opens 60-70 new IVF facilities annually, with organised chains steadily capturing share through branded quality guarantees that appeal to price-sensitive urban couples. China’s government promotes fertility following birth-rate declines, offering provincial subsidies and approving more clinic licences. The assisted reproductive technology market size for Asia-Pacific is forecast to reach USD 13.74 billion by 2028, supported by cost arbitrage that attracts foreign patients seeking both affordability and competent care.

Europe presents a mature yet evolving picture. Universal public funding after Poland’s policy reversal in 2025 eliminates national gaps, yet waiting lists vary widely. Demographically, Europe’s fertility rate of 1.46 births per woman remains below replacement, prolonging demand. The 2027 SoHO regulation will standardise quality metrics and traceability, potentially smoothing intra-EU patient redirection to high-capacity centers. Spain, Denmark and Belgium already host large volumes of foreign cycles, and shared EU data registries could enhance transparency and outcomes, reinforcing Europe’s role in the assisted reproductive technology market.

Competitive Landscape

Private-equity transactions signal growing consolidation. Astorg’s USD 228 million buyout of Hamilton Thorne—alongside Cook Medical’s ART division purchase—builds a vertically integrated lab-hardware platform controlling microscopes, pipettes and media consumables. Post-deal, the combined entity can cross-sell service contracts and negotiate distributor margins, sharpening scale economies. Similarly, Conceivable Life Sciences launched AURA, the first fully automated lab, attaining 51% success rates at lower staffing costs, demonstrating disruptive cost curves.

Technology is the key competitive differentiator. Vendors race to secure regulatory approvals for AI modules that convert raw lab imagery into ranked implantation lists. Clinics adopting these solutions highlight 13–15% gains in clinical-pregnancy rates within a year, fuelling a virtuous data loop. Barriers rise since AI engines require millions of labelled images and ongoing cloud training pipelines, assets difficult for new entrants to replicate quickly.

Regional chains leverage acquisition financing to roll out unified electronic health records, share embryologist expertise and market brand trust. Hospital systems eye similar synergies, acquiring stand-alone clinics to create hub-and-spoke networks. Meanwhile, pharma innovators like Gameto and Repronovo attract venture funding to develop adjunctive therapies addressing ovarian-reserve or male-factor constraints, expanding the definition of product competition beyond pure procedures. Overall, the assisted reproductive technology market tilts toward players combining equipment, data and therapeutic pipelines within diversified service platforms.

Assisted Reproductive Technology (ART) Industry Leaders

CooperSurgical Inc.

Vitrolife AB

FUJIFILM Irvine Scientific Inc.

Ferring B.V.

Merck KGaA (EMD Serono)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Repronovo raised USD 65 million Series A to progress infertility drug candidates.

- May 2025: AutoIVF secured investment led by Vitrolife to advance OvaReady egg-collection automation.

- April 2025: Overture Life completed a USD 20.6 million funding round, bringing total to USD 57 million for IVF automation.

- April 2025: Thermo Fisher Scientific committed USD 2 billion over four years to expand U.S. life-science manufacturing, including ART tools.

- February 2025: Femasys obtained Israeli approvals for FemaSeed, FemVue and FemCerv fertility devices.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the assisted reproductive technology market as the total value generated when eggs, sperm, or embryos are handled outside the human body to enable pregnancy; it therefore spans IVF, intra-cytoplasmic sperm injection, donor and frozen embryo programs, clinic fees, and supportive lab equipment, media, and emerging AI software. According to Mordor Intelligence analysts, this integrated view mirrors how fertility providers bill patients and pay suppliers.

Scope exclusion: Fertility-enhancing pharmaceuticals sold separately from ART cycles are not counted.

Segmentation Overview

- By Product & Service

- Instruments & Equipment

- Reagents & Media

- Software & AI Solutions

- By Technology

- In-Vitro Fertilisation (IVF)

- Artificial Insemination (AI-IUI)

- Frozen Embryo Replacement (FER)

- Other Technology

- By Procedure

- Fresh Non-Donor

- Fresh Donor

- Frozen Donor

- Frozen Non-Donor

- By End User

- Fertility Clinics

- Hospitals & Surgical Centres

- Cryobanks & Research Institutes

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor's team interviewed reproductive endocrinologists, embryology lab directors, and procurement heads across North America, Europe, and fast-growing Asian hubs. These conversations clarified average cycles per clinic, acceptance of add-on genetic tests, pricing dispersion, and pipeline expansions, which were then matched against the desk findings to tighten assumptions.

Desk Research

We began with authoritative public datasets such as WHO's infertility prevalence tables, CDC and ESHRE cycle-success registries, OECD health-expenditure series, and UN population projections, which collectively anchor incidence, treatment volume, and spending power. Trade association fact sheets (SART, European Society of Human Reproduction, Asia Pacific Initiative on Reproduction) provided cycle pricing ranges and clinic capacity updates, while 10-K filings and investor decks from leading clinic chains helped validate service revenues. To profile equipment turnover and supplier share, we mined shipment traces in customs aggregates and drew company financials from D&B Hoovers and news flows via Dow Jones Factiva. Many other secondary repositories were also reviewed to complete and cross-check the evidence base.

Market-Sizing & Forecasting

A top-down model converts treated-patient volumes sourced from national registries and adjusted for self-reported cycles into revenue using region-specific average spend per cycle, which is subsequently filtered through currency and payer-mix weights. Supplier roll-ups of incubators, micromanipulators, and culture media offer a selective bottom-up lens that flags any over- or under-estimation. Five market fingerprints underpin the forecast: 1) cycles per 1,000 women aged 20-44, 2) clinic bed additions, 3) average procedure tariff shifts, 4) success-rate-linked demand elasticity, and 5) government-funded cycle quotas. Multivariate regression, supplemented by scenario analysis for policy shocks, projects each driver through 2030, and gaps in bottom-up estimates are bridged with weighted regional proxies.

Data Validation & Update Cycle

Outputs pass three gates: variable anomaly scans, senior analyst peer review, and model reruns against newly released registry data. Reports refresh annually; interim updates trigger when policy, reimbursement, or major M&A events materially move a key variable, ensuring clients receive an up-to-date view.

Why Mordor's Assisted Reproductive Technology (ART) Baseline Commands Confidence

Published estimates often differ because firms slice the market by unlike scopes, price decks, and refresh cadences.

Key gap drivers include product-only scopes that omit clinic revenues, aggressive uniform pricing, or dated currency bases, which can skew totals upward or downward relative to our balanced clinical plus equipment lens and yearly refresh.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 28.6 B (2025) | Mordor Intelligence | |

| USD 27.6 B (2023) | Global Consultancy A | Emerging-market clinic revenues partially excluded; 2023 FX locked |

| USD 4.3 B (2025) | Trade Journal B | Counts only lab instruments and media, omitting service fees |

| USD 31.6 B (2024) | Industry Research C | Applies premium add-on pricing globally and assumes universal uptake |

The comparison shows how scope width, pricing assumptions, and update cadence can swing values by tens of billions. By grounding our baseline in full treatment economics, region-specific cost structures, and a disciplined annual refresh, Mordor Intelligence delivers a dependable reference point for strategic decisions.

Key Questions Answered in the Report

What is the current size of the assisted reproductive technology market?

The assisted reproductive technology market generated USD 30.67 billion in 2026 and is forecast to rise to USD 43.22 billion by 2031 at a 7.1% CAGR.

Which region is growing fastest?

In 2026, the Assisted Reproductive Technology Market size is expected to reach USD 30.67 billion.

Who are the key players in Assisted Reproductive Technology Market?

Asia-Pacific is expected to lead growth with an 8.38% CAGR between 2026 and 2031 due to rapid clinic expansion in India and pro-fertility policies in China.

How important is AI in fertility treatment today?

AI now supports embryo selection with 70-97% accuracy, helping clinics lift success rates and reduce per-cycle costs, and its adoption is accelerating in leading markets.

Why are treatment costs a major restraint?

U.S. IVF cycles cost USD 12,000-25,000 each, and limited insurance coverage forces many patients to pay out-of-pocket, delaying treatment and increasing financial stress.

What product segment is expanding quickest?

Software & AI Solutions are projected to grow at a 9.25% CAGR to 2031 as clinics integrate predictive analytics and automated lab systems.

How is private equity influencing the industry?

Investors such as Astorg are consolidating equipment makers and clinic networks, chasing defensive growth and the recurring revenue profile of fertility services.

Page last updated on: