Market Overview

| Study Period | 2020 - 2031 |

|---|---|

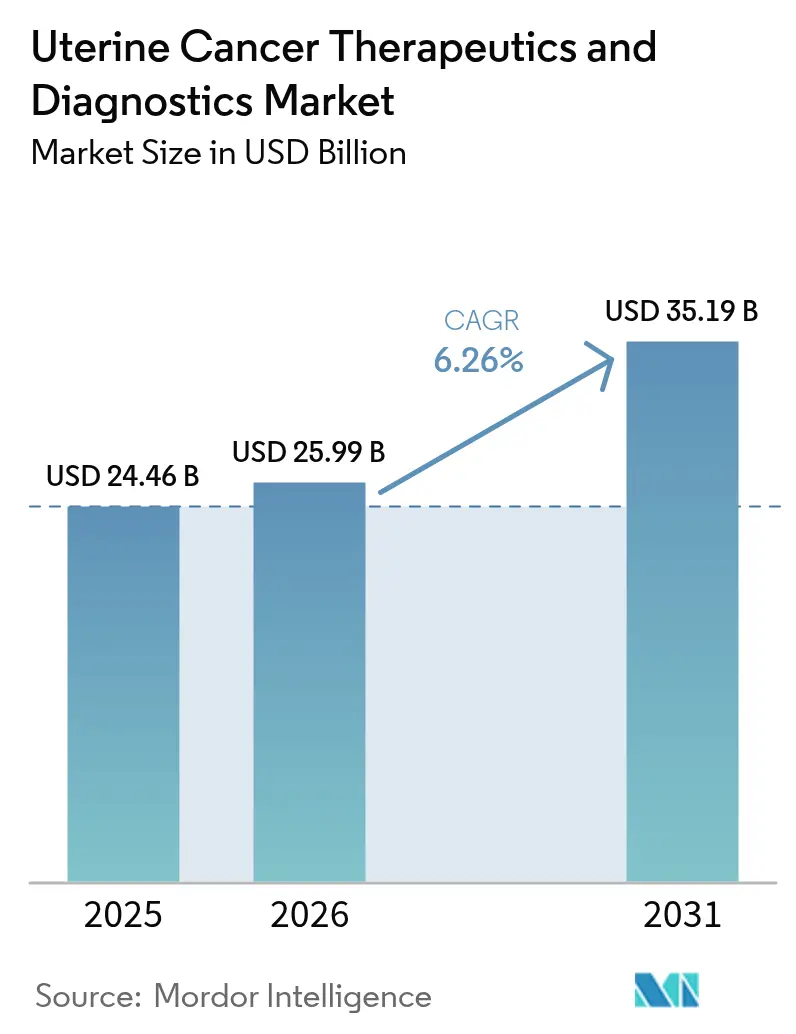

| Market Size (2026) | USD 25.99 Billion |

| Market Size (2031) | USD 35.19 Billion |

| Growth Rate (2026 - 2031) | 6.26% CAGR |

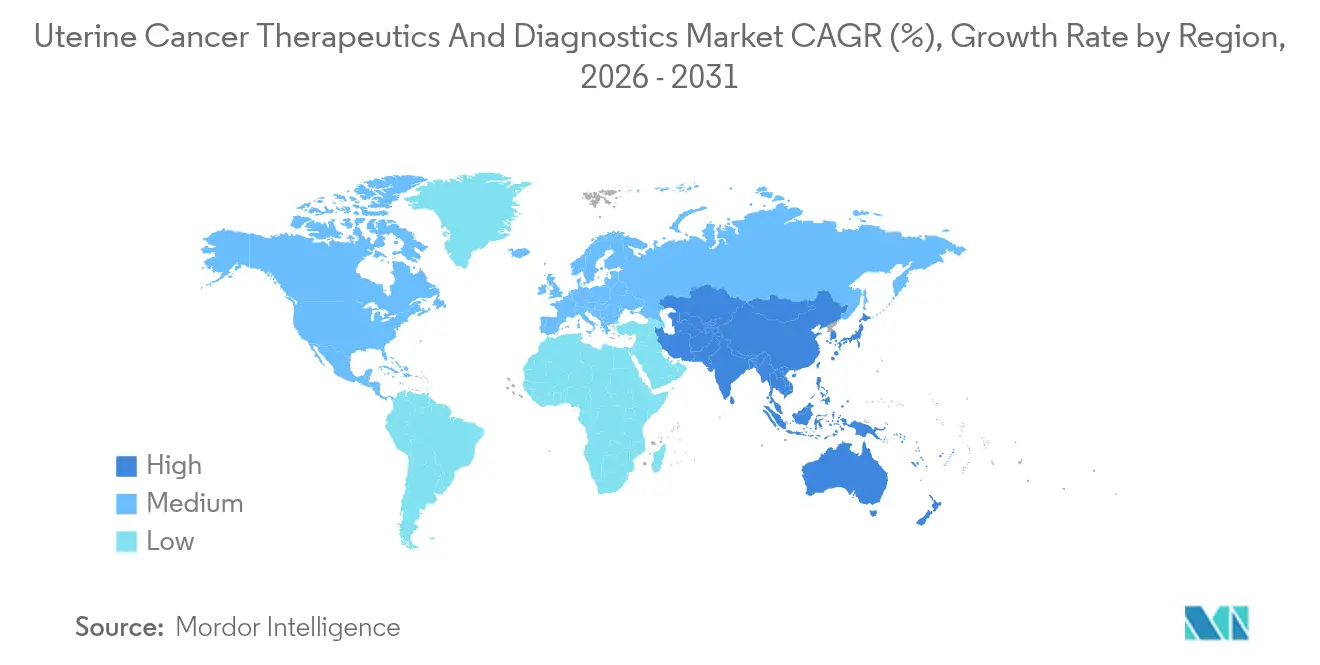

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Uterine Cancer Therapeutics And Diagnostics Market Analysis by Mordor Intelligence

The uterine cancer therapeutics & diagnostics market size in 2026 is estimated at USD 25.99 billion, growing from 2025 value of USD 24.46 billion with 2031 projections showing USD 35.19 billion, growing at 6.26% CAGR over 2026-2031. Growing obesity-linked endometrial adenocarcinoma prevalence, swift immunotherapy adoption, and roll-outs of artificial-intelligence diagnostic platforms are redefining care pathways and sustaining demand. Regulatory support—illustrated by the 2024 U.S. approval of pembrolizumab plus chemotherapy for primary advanced disease—continues to shorten bench-to-bedside timelines. Segment momentum remains strongest in therapeutics, yet double-digit growth in next-generation diagnostics signals a structural shift toward precision medicine. Regional leadership rests with North America, while Asia-Pacific delivers the fastest incremental revenue as cancer centers proliferate and screening programs broaden. Competitive activity is moderate; leading multinationals defend share with immuno-oncology portfolios as start-ups commercialize micro-injectors, liquid biopsies, and machine-learning algorithms.

Key Report Takeaways

- By cancer type, endometrial adenocarcinoma commanded 54.02% of the uterine cancer therapeutics & diagnostics market share in 2025, whereas uterine sarcoma is forecast to deliver a 9.11% CAGR through 2031.

- By product, the therapeutics segment accounted for 62.93% of the uterine cancer therapeutics & diagnostics market size in 2025, while diagnostics are projected to grow at a 10.02% CAGR to 2031.

- By geography, North America led with a 44.85% revenue share in 2025; Asia-Pacific is poised to accelerate at a 10.42% CAGR during the forecast period.

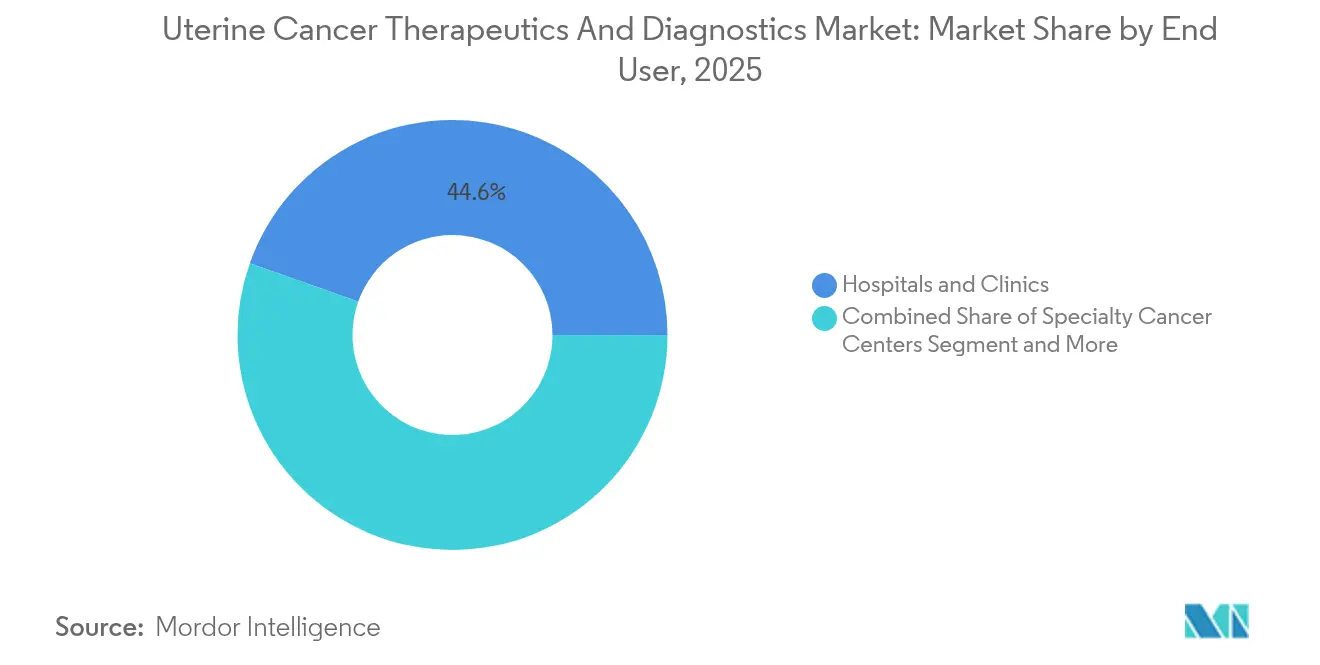

- By end user, hospitals & clinics held 44.58% of the uterine cancer therapeutics & diagnostics market size in 2025 and specialty cancer centers will post a 9.58% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Uterine Cancer Therapeutics And Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of obesity-linked endometrial adenocarcinoma | +1.2% | Global; highest in North America & Europe | Long term (≥ 4 years) |

| Growing adoption of immunotherapy as first-line or maintenance therapy | +1.8% | North America & EU lead; APAC catching up | Medium term (2-4 years) |

| Increasing awareness & screening initiatives in high-risk populations | +0.9% | Global; targeted programs in developed markets | Medium term (2-4 years) |

| Launch of AI-enabled diagnostic imaging platforms | +0.7% | Early uptake in North America & EU; APAC expansion | Short term (≤ 2 years) |

| Commercialisation of ctDNA-based minimal-residual-disease tests | +0.6% | Global premium markets first | Medium term (2-4 years) |

| Novel intratumoral micro-injectors improving local drug delivery | +0.4% | North America & EU research hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Obesity-Linked Endometrial Adenocarcinoma

Body-mass-index data reveal that every 5 kg/m² increase raises endometrial cancer risk through estrogen-driven pathways[1]Takahiko Sakaue et al., “Obesity-induced extracellular vesicles proteins drive the endometrial cancer pathogenesis,” Nature, nature.com. Non-alcoholic fatty-liver disease further multiplies risk among women aged 20-39, intensifying disease onset in younger cohorts. Tumor-promoting extracellular vesicle proteins such as TMEM205 and STAT5 have emerged as dual biomarkers and therapeutic targets, steering pharmaceutical pipelines toward metabolic-oncology combinations. The trend reframes adenocarcinoma as a metabolic disorder, prompting integrated treatment regimens that tackle insulin resistance alongside tumor suppression. Consequently, the uterine cancer therapeutics & diagnostics market benefits from higher diagnosis volumes and extended treatment durations.

Growing Adoption of Immunotherapy as First-Line or Maintenance Therapy

Dostarlimab’s 2024 U.S. label expansion validated immune checkpoint blockade for biomarker-agnostic populations and established durable survival benchmarks. Median overall survival of 44.6 months in the RUBY trial outperformed historical controls, accelerating payer acceptance for premium-priced regimens. Pembrolizumab plus carboplatin-paclitaxel secured approval weeks later, underscoring a regulator-endorsed shift to first-line immunotherapy. Maintenance protocols extend dosing cycles, expanding lifetime revenue per patient and reinforcing the competitive moat for PD-1/PD-L1 innovators. As emerging markets relax import barriers, global uptake is set to scale rapidly.

Increasing Awareness & Screening Initiatives in High-Risk Populations

Campaigns such as CDC’s Inside Knowledge and the International Gynecologic Cancer Society’s Uterine Cancer Awareness Month have brought symptom education to underserved communities[2]Centers for Disease Control and Prevention, “About the Inside Knowledge Campaign,” cdc.gov. Molecular screening tests like DOvEEgene, which leverages routine Pap samples, promise population-level early detection. Targeted initiatives—GSK’s “Red Dab? Red Flag” for Black women—highlight both ethical imperatives and untapped diagnostic volumes. Minimally invasive tampon sampling under the DETECT study may democratize access by enabling at-home collection kits. Rising positivity rates at earlier stages enlarge the treatable pool and funnel more patients into the downstream therapeutics market.

Launch of AI-Enabled Diagnostic Imaging Platforms

Deep-learning algorithms now classify endometrial tumors with 99.26% accuracy, eclipsing conventional automated rates near 80%. AI-based histopathology discerns p53abn-like NSMP subtypes that routine staining misses, aligning patients with precise regimens. The University of British Columbia’s model stratifies risk using 2,300+ tissue images, a boon for rural oncology networks. MRI-integrated platforms pair imaging with genomics, delivering a one-stop workflow that lowers repeat visits. Capital expenditure on these systems creates multi-year software-licensing streams for vendors in the uterine cancer therapeutics & diagnostics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of combination ICI + targeted-therapy regimens | −0.8% | Global; most acute in LMICs | Short term (≤ 2 years) |

| Low historical clinical-trial success rates in uterine sarcoma | −0.6% | Global research centers | Long term (≥ 4 years) |

| Limited reimbursement for advanced molecular diagnostics in LMICs | −0.4% | Primarily LMIC markets | Medium term (2-4 years) |

| Supply-chain bottlenecks for radioisotopes used in brachytherapy | −0.3% | Global; acute in Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Combination ICI + Targeted-Therapy Regimens

Cost-effectiveness analyses report incremental ratios above USD 150,000 per quality-adjusted life-year for durvalumab combinations, breaching conventional payer thresholds. Affordability gaps widen in low-middle-income countries, where immunotherapy penetration lags despite rising incidence. Global oncology spending reached USD 223 billion in 2023 and is forecast to jump to USD 409 billion by 2028, prompting insurers to demand value-based contracts. Biosimilar pipelines worth USD 25 billion by 2029 could ease access but compress margins. Manufacturers are testing tiered pricing and risk-sharing agreements to safeguard uptake in cost-sensitive regions.

Low Historical Clinical-Trial Success Rates in Uterine Sarcoma

Uterine sarcoma trials have long suffered from small sample sizes and heterogeneous histologies, leading to high attrition and limited drug approvals. Novel selinexor–eribulin regimens demonstrated promise at the Medical College of Wisconsin but remain early-phase. Biomarker-driven designs using TP53, ATRX, and RB1 mutations may reverse the trend, yet timeline risks persist. Extended development cycles dampen near-term revenue contributions and weigh on the uterine cancer therapeutics & diagnostics market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cancer Type: Adenocarcinoma Dominance Faces Sarcoma Innovation

Endometrial adenocarcinoma generated 54.02% of 2025 revenue in the uterine cancer therapeutics & diagnostics market, reflecting its high incidence and reliance on multimodal therapy. Combination regimens pairing immunotherapy with targeted agents have become front-line standards, prolonging treatment courses and sustaining double-digit prescription volumes. Obesity and metabolic syndrome continue to enlarge the patient pool, reinforcing adenocarcinoma’s share dominance. AI-assisted histopathology now detects p53abn-like NSMP adenocarcinomas, enabling more aggressive adjuvant strategies that lengthen survival windows. Genomic classifiers integrated into electronic health records accelerate personalized protocol selection, trimming diagnostic turnaround times from weeks to days.

Uterine sarcoma, while representing a smaller cohort, leads segment growth at a 9.11% CAGR through 2031. Breakthroughs such as selinexor–eribulin combinations have revitalized drug pipelines for leiomyosarcoma, and multi-omics biomarker panels identify actionable TP53 or ATRX mutations. The FIGO 2023 staging overhaul improves prognostic accuracy for carcinosarcomas, sharpening patient stratification. Precision-therapy roll-outs broaden clinical-trial enrollment, which in turn accelerates regulatory pathways. Consequently, venture funding is shifting toward sarcoma-specific biologics and drug-device hybrids that can penetrate historically refractory tumors.

By Product: Therapeutics Leadership Challenged by Diagnostics Innovation

Therapeutics retained 62.93% of 2025 revenue, anchored by surgery, radiotherapy, chemotherapy, and the surging immuno-oncology class. First-line pembrolizumab-based combinations and maintenance dostarlimab drive continuing-patient fractions higher, inflating annual per-patient spend. Pipeline agents targeting PI3K, mTOR, and FGFR pathways diversify mechanisms of action, while micro-injector technologies promise site-specific drug delivery that may reduce systemic adverse events. Cost-containment pressures persist, yet outcomes data justify premium pricing in most developed markets, sustaining top-line growth.

Diagnostics, however, will post a 10.02% CAGR to 2031 as precision medicine becomes standard. Liquid biopsy using cfDNA fragmentomics achieves 99% sensitivity for stage I disease, positioning it as a screening adjunct where imaging access is limited. AI-enabled transvaginal ultrasound now matches MRI staging accuracy at lower cost, broadening availability across secondary hospitals. Ethnically validated assays such as WID-qEC improve detection in Black women, addressing disparity-driven unmet need. These innovations expand recurring test revenues, compress time to diagnosis, and ultimately funnel patients into therapeutic pipelines, reinforcing the overall uterine cancer therapeutics & diagnostics market growth.

By End User: Specialty Centers Gain Ground on Hospital Dominance

Hospitals & clinics delivered 44.58% of 2025 turnover owing to comprehensive infrastructure and the ability to perform complex surgeries, radiation, and inpatient chemotherapy. Integrated multidisciplinary teams drive high referral capture, and bundled reimbursement models protect margin integrity. Yet specialty cancer centers will log a 9.58% CAGR by 2031, capitalizing on concentrated expertise, robotic-surgery programs, and embedded clinical-trial units. Outcomes data linking higher procedural volumes to lower mortality bolster their case mix, attracting insurers and patients alike.

Diagnostic laboratories gain share as liquid-biopsy menus expand and AI-driven histopathology offloads interpretation from over-burdened pathologists. Research institutes remain pivotal; collaborations such as ImmunityBio’s vaccine plus N-803 cytokine study leverage academic networks to accelerate recruitment. Ambulatory surgical centers exploit minimally invasive hysterectomy techniques to shift early-stage cases to outpatient settings, offering shorter stays and lower infection risk. Collectively, these shifts fragment traditional hospital volumes, compelling network partnerships and technology investments.

Geography Analysis

North America led the uterine cancer therapeutics & diagnostics market with 44.85% revenue in 2025, underpinned by sophisticated insurance coverage, robust clinical-trial infrastructure, and rapid adoption of checkpoint inhibitors. Rising incidence—projected to spike by 2050—has prompted public health responses such as the Cancer Moonshot, which funds screening programs for underserved communities. Black women’s mortality remains nearly three times that of white women, steering industry initiatives toward disparity mitigation, including GSK’s awareness campaign and community-based trial sites. Academic centers deploy AI-powered pathology and liquid-biopsy tools to shorten diagnostic timelines. Despite premium pricing, reimbursement remains favorable, and biosimilar entrants are yet to exert downward pressure.

Asia-Pacific is forecast to advance at a 10.42% CAGR, driven by expanding middle-class populations, improved insurance penetration, and healthcare-infrastructure upgrades. China’s gynecologic cancer burden now mirrors that of developed economies, presenting a sizable addressable cohort. Private-equity investment in “core-plus” cancer assets accelerates construction of tertiary-level centers equipped with linear accelerators and immunotherapy infusion suites. Telehealth and hospital-at-home programs widen access to specialist care across Indonesia, Thailand, and India. In parallel, local regulators are aligning with ICH guidelines, expediting multinational trial approvals and enhancing time-to-market for novel agents.

Europe remains a mature yet evolving market that balances innovation with cost containment. Value-based procurement shapes formulary inclusion, pushing manufacturers to link price with outcome metrics. A continental shortage of medical radioisotopes disrupted brachytherapy schedules in 2024, instigating projects such as a proposed USD 400 million actinium-225 facility in Wales to secure domestic supply. Precision-medicine mandates propel uptake of molecular diagnostics, with German and Scandinavian payers reimbursing ctDNA-based minimal-residual-disease tests. Eastern European nations follow a catch-up curve, leveraging EU structural funds to modernize oncology centers.

The Middle East, Africa, and South America collectively offer long-run upside but face reimbursement and infrastructure hurdles. Gulf Cooperation Council states procure leading-edge radiotherapy and robotic-surgery systems, aiming to reverse outbound medical tourism. South African insurers pilot bundled-payment programs for endometrial cancer, whereas Brazilian hospital networks integrate AI-ultrasound platforms to alleviate radiologist shortages. The regions’ adoption trajectory depends on macroeconomic stability and expansion of universal health-coverage schemes.

Competitive Landscape

Competition in the uterine cancer therapeutics & diagnostics market is moderate, with top multinationals leveraging broad immunotherapy repertoires to defend share. Merck’s pembrolizumab backbone underpins multiple combination studies; Roche builds differentiation via atezolizumab plus bevacizumab for biomarker-selected subsets; GSK advances dostarlimab into frontline settings. Mid-cap innovators concentrate on delivery-platform patents, such as ultra-long-acting depot injectors and biomimetic nanoparticles that cloak payloads from immune clearance. Diagnostic disruptors monetize AI-software licenses and disposables for liquid-biopsy sample prep, forging razor-razorblade revenue structures.

Strategic alliances are trending toward mechanism-of-action complementarities rather than geographic co-marketing. Generate:Biomedicines applies generative-AI protein design to engineer CAR-T constructs tailored for solid-tumor microenvironments, partnering with Roswell Park to initiate first-in-human trials[3]Generate:Biomedicines, “Generate:Biomedicines and Roswell Park Comprehensive Cancer Center…,” generatebiomedicines.com. Merck KGaA’s USD 3.9 billion acquisition of SpringWorks Therapeutics underscores appetite for niche tumor assets that can plug into existing commercial infrastructures. Intellectual-property filings on intratumoral micro-injectors climbed 40% year on year, signaling an arms race for local-delivery exclusivity.

Diagnostic entrants wield AI as a competitive wedge. Early-stage companies providing cloud-based histopathology platforms close capital rounds within months, buoyed by 99% sensitivity data. Liquid-biopsy developers secure laboratory-developed-test status ahead of FDA review to build real-world evidence at scale. Larger IVD manufacturers respond by acquiring algorithm start-ups to bundle software with scanners, locking customers into ecosystem contracts that include service, reagents, and analytics.

Uterine Cancer Therapeutics And Diagnostics Industry Leaders

Abbott Laboratories

Becton Dickinson and Company

Merck & Co., Inc.

F. Hoffmann-La Roche AG

GSK plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Therapeutic whitespace is expanding beyond PD-1 plus chemotherapy into biomarker-driven combinations and next-wave modalities, including antibody-drug conjugates (ADCs) that link target selection with cytotoxic payload delivery. In 2024, multiple first-line endometrial cancer regimens received US FDA approvals, including pembrolizumab plus carboplatin and paclitaxel, durvalumab plus chemotherapy for dMMR disease, and dostarlimab-gxly plus chemotherapy. These approvals support routine molecular characterization, such as mismatch repair status, as a gating step for regimen selection and add to testing demand within the same care pathway. In April 2026, BioNTech and DualityBio reported positive Phase 2 data for trastuzumab pamirtecan in HER2-expressing recurrent endometrial cancer and communicated plans to file a BLA in 2026, keeping HER2 testing and ADC supply-chain readiness as near-term priorities for advanced disease.

Diagnostics opportunities focus on moving uterine cancer workups toward minimally invasive, scalable collection and algorithm-assisted interpretation earlier in the patient journey. New evidence around AI-enabled, noninvasive sampling approaches (including vaginal swab-based testing with high reported discriminative performance) and protein-based uterine fluid assays supports a wider menu of pre-biopsy triage tools. This can expand testing volumes across hospitals, specialty centers, and independent laboratories while easing access constraints in settings with limited imaging or pathology capacity. Interoperability and workflow integration also offer a monetizable gap, since linking molecular and screening assays into oncology electronic medical record ordering and results pathways can reduce friction for repeat testing and longitudinal monitoring, which aligns with longer treatment courses and precision protocols.

Recent Industry Developments

- May 2026: Merck announced that its Phase 3 TroFuse-005 trial of sacituzumab tirumotecan (sac-TMT) in certain patients with advanced or recurrent endometrial cancer met the dual primary endpoints of overall survival and progression-free survival. The readout reinforces competitive intensity around TROP2-directed antibody-drug conjugates and broadens therapeutic options beyond checkpoint inhibitor backbones in later-line settings.

- March 2025: Health Canada approved Keytruda (pembrolizumab) in combination with chemotherapy for adult patients with primary advanced or recurrent endometrial carcinoma. The decision extends first-line immunotherapy access beyond the United States and supports more standardized adoption of biomarker-informed treatment pathways across North American practice.

- June 2024: The US FDA approved pembrolizumab with carboplatin and paclitaxel for adult patients with primary advanced or recurrent endometrial carcinoma. This approval moved immunotherapy further into frontline treatment and increased the need for coordinated diagnostic workups and infusion-capable care settings to manage combination regimens.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the uterine cancer therapeutics and diagnostics market includes revenues from products and services used to detect, confirm, and treat uterine cancers across key care settings. Values are reported in USD and counted at the point of sale to the healthcare system.

Scope exclusions: We exclude general womens health tests or procedures not ordered for suspected or confirmed uterine cancer, and we also exclude non-medical wellness services.

Segmentation Overview

- By Cancer Type

- Endometrial Adenocarcinoma

- Adenosquamous Carcinoma

- Papillary Serous Carcinoma

- Uterine Sarcoma

- Clear Cell Carcinoma

- Others

- By Product

- Therapeutics

- Surgery

- Radiation Therapy

- Chemotherapy

- Immunotherapy

- Targeted Therapy

- Hormone Therapy

- Others

- Diagnostics

- Imaging (Ultrasound, CT, MRI, PET)

- Biopsy (Aspiration, Core Needle, D&C)

- Hysteroscopy

- Liquid Biopsy (ctDNA)

- Genomic & Molecular Tests

- Pap Smear / Cytology

- Others

- Therapeutics

- By End User

- Hospitals & Clinics

- Specialty Cancer Centers

- Diagnostic Laboratories

- Research Institutes

- Ambulatory Surgical Centers

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with public disease and care pathway signals, so the model reflects a realistic demand pool before any pricing or share assumptions were applied. We used sources such as the World Health Organization and IARC (GLOBOCAN), US CDC and NCHS mortality tables, SEER program releases for incidence and stage mix, and peer-reviewed clinical guidelines and journal articles for test and treatment sequencing.

To translate that demand pool into market value, we cross-checked treatment patterns and diagnostics intensity using sources such as government health ministry publications, reimbursement and coding references where available, hospital and cancer center clinical pathway notes, company annual reports and investor presentations, and reputed press coverage of approvals and label changes. In a few places, a paid subscription covering company financials, patents, and shipment-level trade signals was used to confirm pricing direction and supply availability. The desk sources listed here are illustrative only, since many additional public references were reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on confirming what gets used in routine care, and what is still limited to selected centers, because that difference can shift the diagnostics and therapy mix materially. We spoke with clinicians, pathology and lab leaders, procurement and reimbursement informed contacts, and industry participants across APAC, EMEA, and the Americas to pressure test incidence linked demand, regimen adoption, testing rates, and typical price corridors used in the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 17% | APAC: 51% |

| Mid tier: 46% | Functional/Unit leaders: 33% | EMEA: 31% |

| Smaller Players: 19% | Managers: 50% | Americas: 18% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand pool assessment, where incidence and diagnosed case counts were converted into treated cohorts and tested cohorts based on stage mix and typical care pathways, then translated into value through expected utilization and price bands. To keep totals realistic, we also ran selective bottom-up checks using sampled country rollups, channel discussions, and a few supplier revenue anchors, then used the results to adjust any over- or under-shoot.

Inputs that mattered most included uterine cancer incidence and mortality trendlines, proportion diagnosed by stage, rates of surgery and systemic therapy use, adoption of immunotherapy and targeted regimens following approvals, diagnostic workup intensity (biopsy, imaging, and molecular or pathology testing where applicable), and typical repeat testing or monitoring frequency. Where country data were missing, we used proxy markets with similar screening access and treatment guidelines, followed by an adjustment step after interview feedback.

For the forecast, we used scenario analysis supported by regression-style sensitivity checks. Growth was driven by changes in treated patient counts, regimen mix shift, and price evolution tied to reimbursement and generic entry expectations. Assumptions were finalized only after the expert feedback converged on what is likely to be used in routine practice over the next cycle.

Data Validation & Update Cycle

Outputs were checked against independent signals such as cancer burden trends, reported procedure and test activity where available, and therapy adoption signals that show up soon after major label updates. Any sharp step changes were reviewed, and when the reason was not clear, we went back to the source set and re-contacted experts to confirm whether it reflected a real market move or a modeling artifact.

Before sign-off, the file goes through a multi-step analyst review so assumptions, conversions, and currency timing are consistent across countries and segments. Reports are refreshed annually, and we also do interim updates when a material approval, reimbursement change, or guideline shift can move the demand pool or pricing. Right before delivery, we perform a final pass so clients receive the most current view possible.

Mordor Intelligence's Uterine Cancer Therapeutics Diagnostics Market Size Measured Against Other Published Estimates

Published market values for this space can differ because the care pathway is not uniform across countries. Some studies count only drug therapy, while others also add diagnostics and follow-on testing. Variations also come from what is treated as in-scope value, such as whether hospital procedures are counted, how combination regimens are priced, and how quickly numbers are refreshed after major label updates.

Incidence-by-stage checks and observed shifts in regimen adoption after key approvals are used to keep Mordor Intelligence tied to a clearly defined treated and tested cohort rather than a broad oncology spend proxy. When other estimates diverge, the common drivers are mixing adjacent gynecologic cancers, using aggressive price escalation, or relying on global averages that smooth out low-access markets where testing and treatment intensity remain limited.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 25.99 B (2026) | |

| Industry Research House A | USD 23.21 B (2025) | Uses a different base year and often applies broader therapy and procedure inclusions by cancer type, which can shift totals when 2026 uptake and pricing assumptions are not revalidated country by country. |

| Publisher B | USD 20.60 B (2025) | Typically reflects a more conservative growth path and may undercount diagnostics intensity or newer regimen penetration, especially when global averages are used instead of stage-linked treated cohort build-ups. |

Taken together, the spread is mostly explained by base-year choice, what is counted inside diagnostics versus treatment value, and how fast adoption and pricing are allowed to move in the early forecast years. By keeping the model traceable to patient counts, stage mix, testing frequency, and regimen mix, the estimate stays repeatable and easier to audit when new clinical or reimbursement changes occur.

Key Questions Answered in the Report

What is the current size of the uterine cancer therapeutics & diagnostics market?

The market is valued at USD 25.99 billion in 2026 and is on track to reach USD 35.19 billion by 2031.

Which segment of the uterine cancer therapeutics & diagnostics market is growing fastest?

Diagnostics is expanding at a 10.02% CAGR thanks to AI-driven imaging and liquid-biopsy adoption.

Why is uterine sarcoma considered a high-growth opportunity?

Breakthrough combinations such as selinexor with eribulin and multi-omics biomarker panels are propelling a 9.11% CAGR for sarcoma treatments.

How significant is North America’s role in this market?

North America contributed 44.85% of 2025 revenue due to early immunotherapy uptake, dense clinical-trial networks, and favorable reimbursement.

What are the main barriers to market growth?

High combination-therapy costs, limited reimbursement for advanced diagnostics in emerging markets, and radioisotope supply shortages constrain short-term expansion.

Page last updated on: