Gummy Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

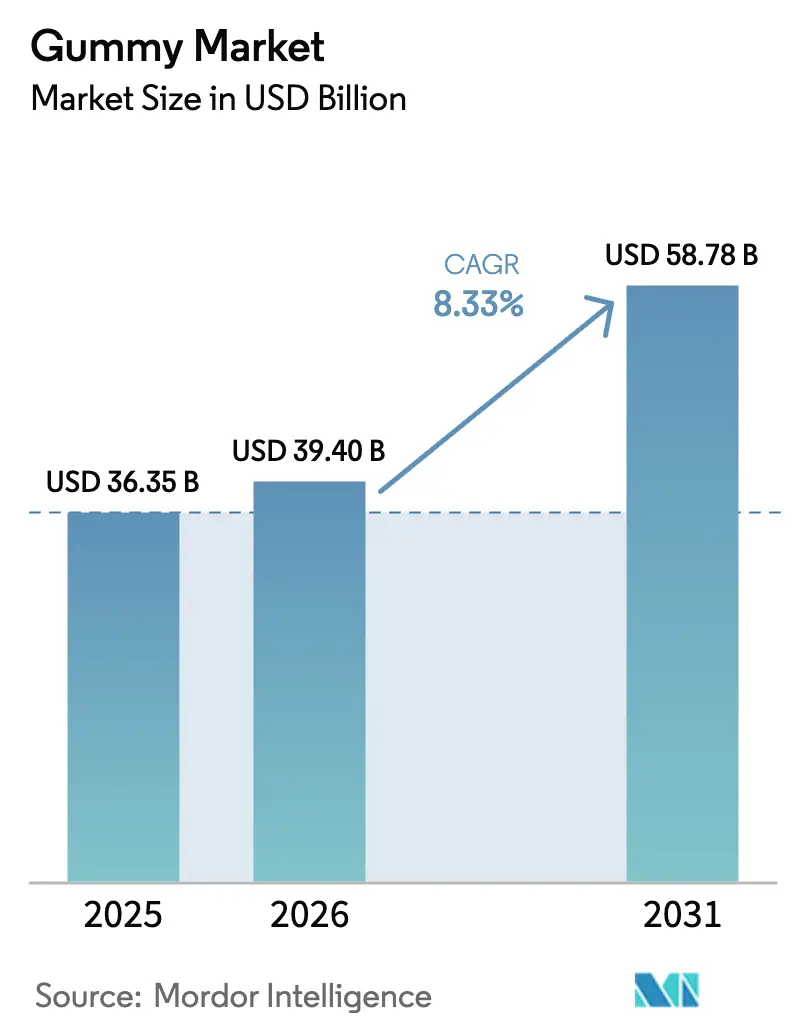

| Market Size (2026) | USD 39.40 Billion |

| Market Size (2031) | USD 58.78 Billion |

| Growth Rate (2026 - 2031) | 8.33% CAGR |

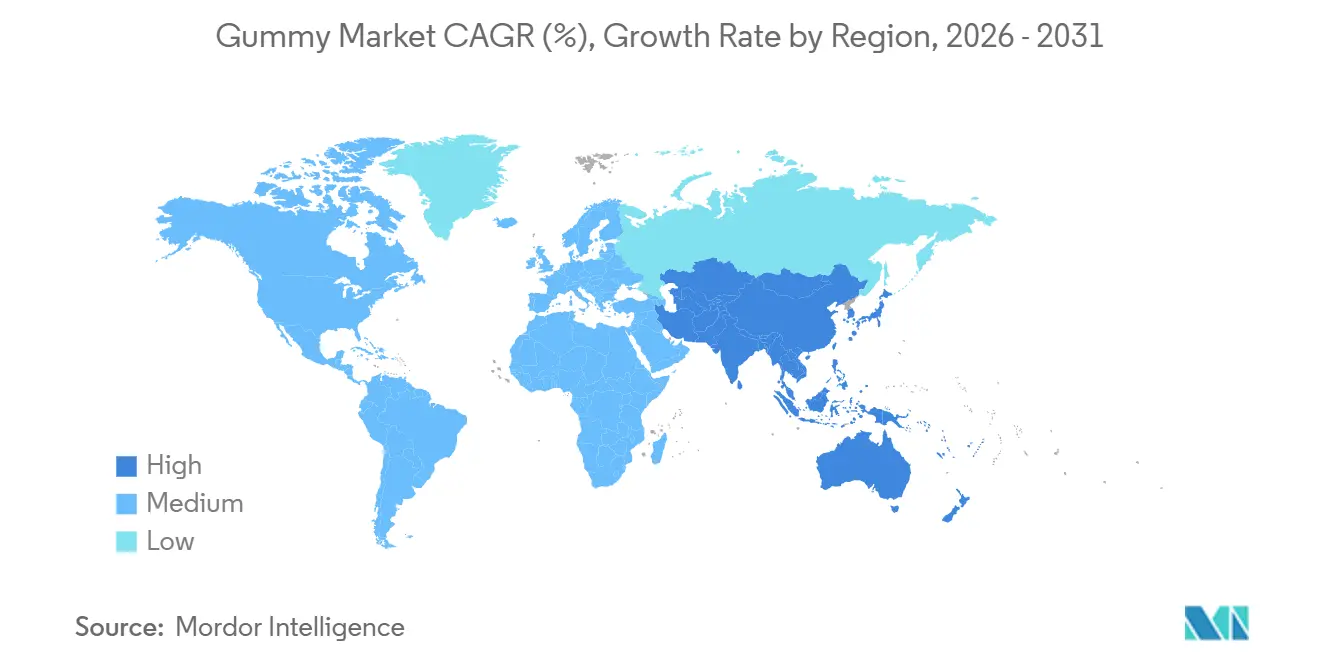

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Gummy Market Analysis by Mordor Intelligence

The Gummy Market size is expected to increase from USD 36.35 billion in 2025 to USD 39.40 billion in 2026 and reach USD 58.78 billion by 2031, growing at a CAGR of 8.33% over 2026-2031. Initially limited to traditional confections, the gummy market has transformed to meet the needs of health-conscious consumers who prefer supplements in more convenient and palatable formats. This shift highlights a growing preference for gummies over conventional pills and capsules due to their taste and ease of consumption. Manufacturers have responded by creating innovative formulations that combine nutritional benefits with appealing flavors. As a result, gummies have become the dominant format in the vitamin and supplement market. Additionally, cannabis and hemp-infused gummies are anticipated to grow at an annual rate of 8.96%, supported by federal clarifications in November 2026 that limit THC content to 0.4 milligrams per container. Regulatory advancements, such as Sweegen’s 2025 GRAS approval for brazzein and California’s AB 899 transparency law, are further driving the development of clean-label, sugar-reduced products.

Key Report Takeaways

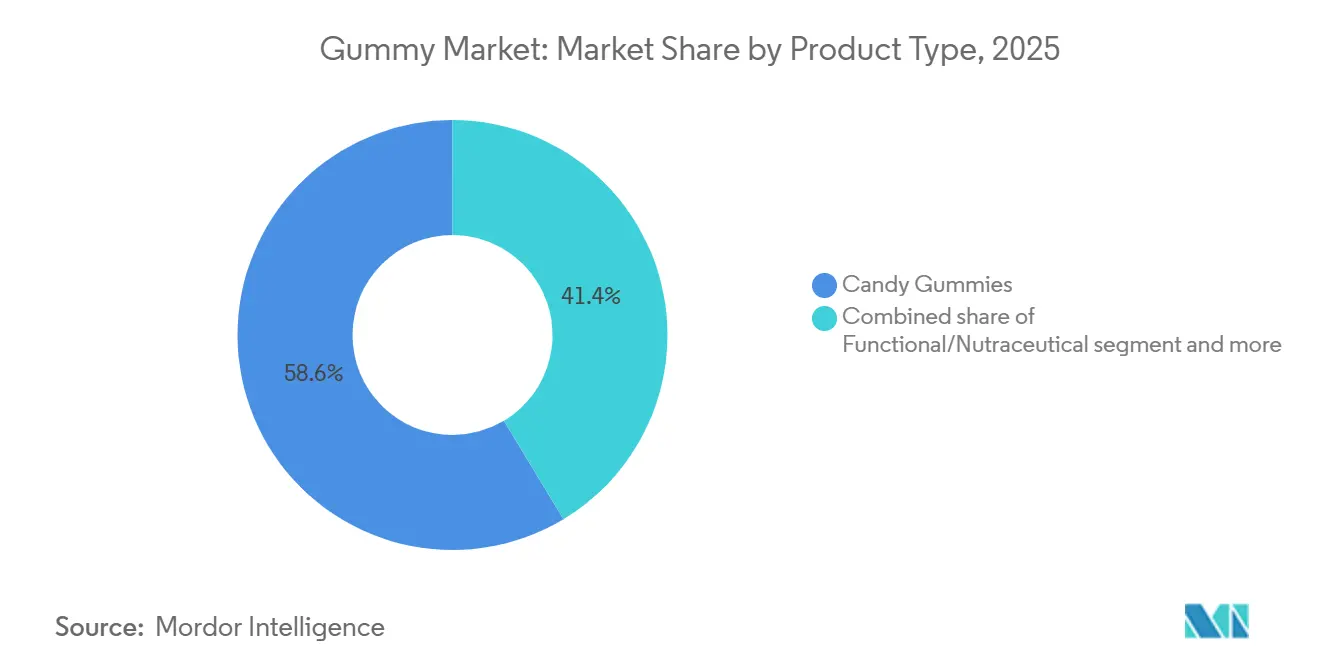

- By product type, candy gummies commanded 58.63% of the gummy market share in 2025, whereas cannabis and hemp-infused gummies are projected to post the highest 8.96% CAGR through 2031.

- By ingredient, gelatin held 60.38% of the gummy market size in 2025, and pectin formulations are advancing at a 9.15% CAGR to 2031.

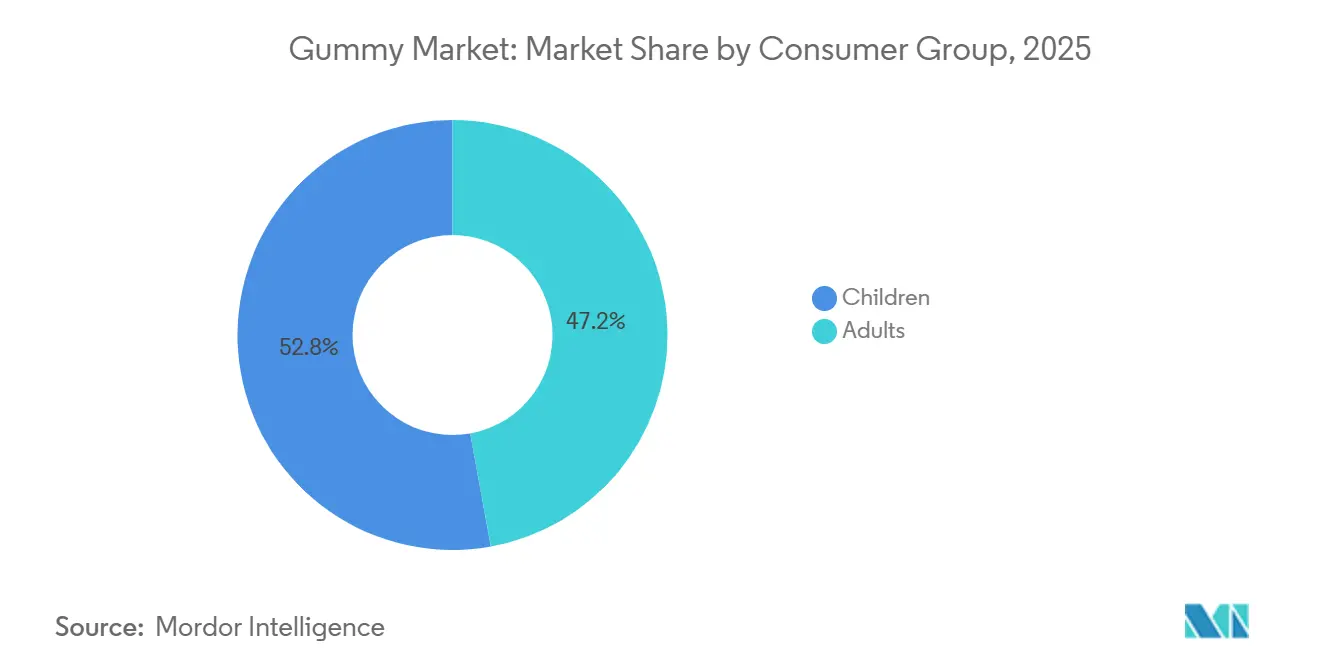

- By consumer group, children led with 52.84% revenue share in 2025, while the adult segment is progressing at a 9.57% CAGR up to 2031.

- By distribution channel, supermarkets and hypermarkets contributed 45.36% of 2025 sales, yet online retail is the fastest-growing avenue at 9.47% CAGR to 2031.

- By geography, North America represented 29.64% of the 2025 value; Asia-Pacific is expanding at a leading 9.68% CAGR during the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Gummy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer appetite for functional supplement gummies | +2.2% | Global (North America and Europe lead) | Medium term (2-4 years) |

| Growing demand for sugar-reduced gummies | +1.5% | North America and European Union; expanding in Asia-Pacific | Short term (≤ 2 years) |

| Product innovation and flavor variety | +1.3% | Global (premium markets) | Medium term (2-4 years) |

| Shift toward vegan and plant-based formulations | +1.0% | Europe and North America; spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Clean-label and natural ingredients | +0.8% | Global (regulation-driven in European Union) | Medium term (2-4 years) |

| Technological advances in manufacturing | +0.7% | Global (developed markets) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising consumer appetite for functional supplement gummies

The combination of confectionery appeal and nutritional benefits has transformed supplement consumption patterns. Consumers are increasingly avoiding traditional pills due to difficulty in swallowing and daily consumption fatigue, instead preferring gummy formats that make their health routines more enjoyable and sustainable. The U.S. Food and Drug Administration's March 2024 update to New Dietary Ingredient Notification Procedures has simplified the approval process for new gummy formulations, reducing regulatory timelines and enabling manufacturers to bring functional ingredients to market more quickly[1]Source: U.S. Food and Drug Administration, “New Dietary Ingredient Notification Procedures Guidance,” fda.gov. Manufacturing innovations, particularly starch-free production methods, have enhanced operational efficiency, improved hygiene standards, and reduced production cycles for custom formulations. The market has evolved significantly beyond children's vitamins to encompass adult wellness products, with older adults emerging as a key consumer segment due to their preference for easier-to-consume supplement formats and increasing focus on preventive health measures.

Growing demand for sugar-reduced and sugar-free confectionery gummies

Regulatory pressure and health consciousness have catalyzed the development of sugar-reduced gummy formulations that maintain taste appeal while addressing nutritional concerns. The European Commission's updated specifications for food additives, including sorbic acid and potassium sorbate, reflect the regulatory environment's evolution toward healthier formulations[2]Source: EUR-Lex, "COMMISSION REGULATION (EU) 2024/2597," eur-lex.europa.eu. Research demonstrates that fruit juice concentrates can successfully substitute glucose syrup in gummy formulations, achieving pH values between 2.22-3.08 and water activity levels of 0.46-0.52, while enhancing nutritional profiles. The challenge lies in maintaining texture and stability characteristics that consumers expect from traditional gummies. Stevia and natural antioxidants have emerged as preferred alternatives, though formulation complexity increases with sugar reduction levels. The trend extends beyond health-conscious consumers to include parents seeking better-for-you options for children, driving innovation in natural sweetening systems.

Product innovation and flavor variety

The gummy market's flavor innovation has transcended traditional fruit profiles to encompass sophisticated adult-oriented tastes and functional flavor masking for nutraceutical applications. Playful texture combinations, featuring firmer exteriors with soft centers, represent the latest innovation frontier, appealing to the growing "kidults" demographic seeking nostalgic yet premium experiences. Red and orange colors dominate consumer preferences, linked to familiar flavors and the demand for natural coloring agents. The blurring line between traditional confectionery and vitamin-infused gummies has created opportunities for hybrid products that deliver both indulgence and health benefits. The trend toward premium ingredients and exotic flavor profiles has enabled price point elevation, particularly in the adult supplement segment, where consumers demonstrate a willingness to pay for quality and efficacy.

Shift toward vegan and plant-based formulations

The gummy market is experiencing a significant shift toward plant-based ingredients, driven by sustainability concerns and clean-label demands. Pectin has emerged as a preferred ingredient, accounting for over 55% of new gummy formulations in 2023, while gelatin-based alternatives represented 32%. Cargill data shows a 7% increase in pectin-containing product launches across Europe from 2022 to 2023, with 50% of European consumers now recognizing pectin as an ingredient. Companies are also implementing sustainable packaging solutions to meet environmental requirements. The rising vegan population continues to drive demand for plant-based gummies, with the 2024 IFIC Food & Health Survey indicating that 2% of U.S. consumers follow a vegan diet[3]Source: International Food Information Council, "2024 IFIC Food & Health Survey," ific.org.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening global regulations on sugar and health-claims | -1.0% | Global, with strictest enforcement in European Union and North America | Short term (≤ 2 years) |

| Raw-material supply volatility for gelatin and pectin | -0.8% | Global, with acute impact in Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| High Cost of premium ingredients and manufacturing | -0.6% | Global, with premium market concentration in developed economies | Medium term (2-4 years) |

| Product shelf life and stability | -0.4% | Global, with tropical climate challenges in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening global regulations on sugar and health-claims

Regulatory frameworks worldwide are imposing stricter controls on sugar content and health claim substantiation, creating compliance challenges for gummy manufacturers. The FDA and FTC's joint enforcement actions against delta-8 THC gummy products in July 2024 demonstrate regulatory agencies' heightened scrutiny of the sector, with over 300 adverse event reports received between January 2021 and December 2023. European Union regulations on food additives and contaminants continue to evolve, with Commission Regulation 2023/915 establishing maximum contaminant levels that particularly affect products targeting children. The challenge extends beyond formulation to marketing claims, where substantiation requirements for functional benefits have become increasingly stringent. Companies must navigate complex approval processes for new ingredients while maintaining product efficacy and consumer appeal. The regulatory landscape's fragmentation across jurisdictions creates additional complexity for global manufacturers seeking standardized formulations.

Raw-material supply volatility for gelatin and pectin

Supply chain disruptions and raw material price volatility pose significant challenges to gummy manufacturers' cost structures and production planning. Gelatin pricing is influenced by multiple factors, including quality grades, raw material costs, supply chain stability, and shipping logistics, with food-grade gelatin commanding premium prices due to strict safety standards. The pectin market faces supply shortages, with domestic markets heavily reliant on imports, creating vulnerability to international trade disruptions. Bovine gelatin remains the most common but faces periodic supply constraints, while fish gelatin commands higher prices due to limited sourcing options. The shift toward plant-based alternatives has intensified competition for pectin and other hydrocolloids, with manufacturers requiring careful formulation expertise to achieve desired texture properties. Volume discounts and minimum order quantities create additional challenges for smaller manufacturers seeking to compete with established players who benefit from economies of scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Functional Gummies Drive Volume, Cannabis Variants Lead Growth

In 2025, candy gummies dominated the market with a 58.63% share, bolstered by Haribo's expansive global presence and Ferrara's diverse portfolio, which includes Brach's, Jelly Belly, and Trolli. However, this segment's growth has lagged behind the more rapidly expanding nutraceutical and cannabis categories, signaling its maturity. Functional and nutraceutical gummies, holding the second-largest market share, are reaping benefits from the U.S. supplement market's increasing gummy adoption. This momentum was further amplified by Charlotte's Web's December 2025 introduction of a Medicare-Medicaid pilot, which allows CBD product reimbursements, broadening the potential market to 67 million beneficiaries. While still in their infancy, pharmaceutical gummies are drawing significant investment. A case in point is TopGum's February 2026 purchase of a U.S. pharma-grade facility for USD 25 million, underscoring its ambition to cater to clinical trials and prescriptions, areas where compliance with cGMP and accurate dosing are paramount. In the realm of pet supplement gummies, though they command a smaller market share, their presence is rapidly growing. Noteworthy launches include GumPaws' March 2025 debut as the "world's first" dog gummy touting dental plaque removal, DotDotPet's June 2024 Multifit Gummies aimed at joint and gut health, and NaturVet's May 2025 All-In-One Daily Care line, catering to puppies, adults, and seniors, and featuring PlaqueOff for oral care.

Among various product types, cannabis and hemp-infused gummies are leading the pack, expanding at a robust 8.96% CAGR through 2031. This growth is fueled by clearer regulations, such as the November 2026 federal cap of 0.4 milligrams THC per container and the March 2026 CMS guidance. The latter defines eligible hemp products for Beneficiary Engagement Incentive programs as those containing up to 3 milligrams THC per serving. Highlighting the segment's shift from mere recreational edibles to precise wellness solutions, Charlotte's Web rolled out its Brightside line in May 2025, boasting formulations like Rest & Relax and Focus & Flow, and featuring its proprietary TiME INFUSION for a swift 5-to-15-minute onset. Additionally, their October 2025 introduction of the Knockout sleep gummy, infused with hemp THC and CBN, underscores this evolution. Yet, challenges loom: the FDA's drug-exclusion rule still bars CBD from foods and supplements, posing enforcement risks. This limitation curtails mainstream retail distribution, nudging brands towards specialty channels and direct-to-consumer avenues. In a bid to innovate, confectionery candy gummies are experimenting with textures. Sweet Venture Group's March 2026 Gummi Popz, retailing at USD 2.49, melds chewy gummies with popping candy, while Ferrara's May 2025 SweeTARTS Gummy Halos, featuring airy-fluffy bases, seek to captivate the teen and tween demographic through novel experiences. Meanwhile, functional gummies are broadening their horizons. No longer limited to multivitamins, they're venturing into specific areas like sleep, immunity, and cognitive focus. This evolution not only masks the bitterness of active ingredients but also enhances user adherence, solidifying the gummy format's role as a bridge between traditional supplements and pharmaceuticals.

By Ingredient: Gelatin Dominates, Pectin Gains on Vegan Demand

In 2025, gelatin-based gummies led the market with a 60.38% share. Gelatin's benefits in texture, clarity, and cost significantly contributed to this dominance. Being 20 to 40% cheaper than pectin per kilogram and offering superior elasticity, gelatin remains a preferred choice for confectionery applications. However, regulatory concerns over bovine sourcing in Europe and the Asia-Pacific, due to sporadic disease outbreaks, and religious dietary restrictions in the Middle East and halal markets, are tightening supply. This has driven manufacturers to explore porcine gelatin and plant-based alternatives. Agar and other hydrocolloids, such as tapioca and modified potato starches, cater to niche applications, particularly in the Asia-Pacific, where seaweed cultivation supports agar production. However, these alternatives require precise temperature control and longer setting times, which reduce throughput and limit their use to premium or specialty SKUs.

Pectin-based gummies are experiencing rapid growth, with a 9.15% CAGR projected through 2031, the highest among ingredient types. This growth is driven by European vegan mandates, Asia-Pacific dietary preferences, and North American clean-label trends. Reflecting these trends, Charlotte's Web launched its Brightside and Knockout gummies in May and October 2025, respectively. These products, marketed as vegan and gluten-free, align with the company's Certified B Corporation values and target health-conscious consumers. However, the pectin supply chain remains volatile. Spot prices dropped in June 2025 due to an oversupply from citrus peel processors but rebounded in October 2025 as pharmaceutical and nutraceutical buyers tightened availability. This fluctuation created margin pressures for smaller manufacturers without long-term contracts. Additionally, specialty starches, particularly Thai tapioca, saw an 18% year-over-year price increase in 2025. This was caused by drought-reduced cassava yields and rising demand from the biodegradable packaging sector, which increased formulation costs for vegan gummies. As pectin-based formulations gain market share, procurement risks are shifting from a tactical issue to a strategic bottleneck. This could hinder capacity expansions and raise entry barriers, especially for mid-tier brands lacking vertical integration or hedging capabilities.

By Consumer Group: Children Lead Share, Adults Drive Premium Growth

In 2025, children accounted for 52.84% of the market, supported by well-established multivitamin brands such as Bayer's Flintstones, Church & Dwight's L'il Critters, and Hero Nutritionals, which introduced gummy vitamins in the late 1990s. Bayer's July 22, 2025, launch of One-A-Day Kids Multi with Iron gummies, providing 12 milligrams of iron in a child-friendly format, addresses a nutrient gap that ferrous sulfate tablets fail to meet due to their metallic taste. This highlights Bayer's ongoing innovation in pediatric formulations. However, these advancements face increasing regulatory scrutiny. California's AB 899, effective in 2024, requires transparency regarding synthetic dyes in children's products. Additionally, the European Food Safety Authority's updated sweetener ADI thresholds are driving reformulations.

Adults are experiencing the fastest growth among consumer groups, with a 9.57% CAGR projected through 2031. This growth is driven by demand for targeted health benefits—such as sleep, immunity, cognitive focus, and joint health- and a shift toward premium products. A December 2025 pilot program announced by Medicare and Medicaid, which allows reimbursements for Charlotte's Web CBD products, reflects this trend. This institutional support could expand the market to 67 million Medicare beneficiaries, approximately 20% of whom already use cannabidiol for pain and age-related conditions. In 2025, gummies accounted for 24.6% of the U.S. supplement market, up from around 18% in 2020, reflecting a growing preference among adults, particularly those aged 35 to 54, for the convenience and taste of gummies over traditional tablets and capsules. Online retail, which represented 24.3% of supplement sales and is expected to lead by 2028, is enabling direct-to-consumer brands to utilize subscription models and personalized quizzes to guide adult consumers toward premium gummy formulations, priced 30 to 50% higher than standard multivitamins. As functional gummies transition from general wellness products to targeted health interventions, illustrated by Charlotte's Web establishing a Scientific Advisory Board in September 2025 to support R&D and medical education, adult consumers are shifting from generic multivitamins to clinically validated, condition-specific formulations.

By Distribution Channel: Supermarkets Anchor Sales, Online Retail Accelerates

In 2025, supermarkets and hypermarkets accounted for 45.36% of the market, highlighting their stronghold in confectionery impulse purchases and family-pack multivitamins. Key players such as Walmart, Albertsons, and Safeway, along with European retailers like Tesco and Carrefour, served as primary distribution channels for brands like Haribo, Ferrara, and various mass-market supplements. Convenience and specialty stores, including GNC and Vitamin Shoppe, cater to niche and premium segments but face challenges from online competitors and direct-to-consumer models, which exert pressure on margins. Pharmacies and drugstores, which also held a significant market share in 2025, have traditionally prioritized tablets and capsules due to their higher margins and longer shelf life. However, pharmacists are increasingly recommending gummies for pediatric and geriatric patients to address swallowing difficulties. Sweet Venture Group's March 2026 launch of Gummi Popz, priced at a suggested retail of USD 2.49 and distributed through major outlets like Walmart, Albertsons, Circle K, H-E-B, and Amazon, exemplifies the multi-channel approach needed to capture both impulse and planned purchases.

Online retail is experiencing rapid growth, with a 9.47% CAGR projected through 2031, making it the fastest-growing distribution channel. This growth is driven by direct-to-consumer subscription models, personalized wellness quizzes, and the rise of social-commerce platforms. In 2025, e-commerce represented 24.3% of U.S. supplement sales and is expected to become the leading channel by 2028. TikTok Shop, for instance, generated approximately USD 1 billion in supplement sales in 2025, accounting for 3% of the market and achieving 71% year-over-year growth. Charlotte's Web's December 2025 Medicare-Medicaid pilot program, which includes a secure online healthcare portal, demonstrates the integration of e-commerce with advanced data security. This platform enables reimbursement for CBD products, showcasing the convergence of digital health platforms and supplement distribution. Amazon continues to dominate the online space, utilizing Prime-eligible fulfillment and algorithm-driven product recommendations that favor items with high review counts. This creates challenges for emerging brands that lack the resources for advertising and promotional discounts. Specialty stores, such as health-food chains and boutique wellness retailers, are focusing on experiential retail strategies, including in-store consultations, product sampling, and curated assortments. However, they face structural challenges as consumers increasingly prioritize convenience and price transparency over personalized service. As online penetration grows, brands are investing in first-party data strategies—such as loyalty programs, email capture, and quiz funnels—to reduce reliance on Amazon and enhance customer lifetime value, despite the higher fulfillment and customer-acquisition costs compared to wholesale channels.

Geography Analysis

By 2025, North America's gummy market experienced significant growth, reaching nearly USD 12 billion and securing a notable 29.64% share of the global market. This growth was largely driven by the U.S.'s mature and well-established supplement industry, coupled with Canada's strong consumer preference for confectionery products. The introduction of federal THC caps in the U.S. in 2026 played a pivotal role in reducing compliance uncertainties, which encouraged mainstream retailers to reconsider the inclusion of hemp gummies in their product portfolios. While Mexico's gummy market remains in its nascent stages, it benefits from cross-border brand recognition, which has helped to establish a foothold in the market. However, Mexico's per-capita gummy consumption continues to trail significantly behind that of its northern counterparts, highlighting room for growth.

In Europe, the growing consumer inclination to pay a premium for vegan and clean-label products has driven annual gummy sales growth of over 10% within the region's EUR 20 billion supplement market. Germany remains the market leader, supported by the extensive presence of drugstore chains such as dm and Rossmann, which cater to a wide consumer base. Meanwhile, the U.K. and France are prioritizing sugar reduction in gummy products to align with public health mandates and address rising health concerns. Eastern Europe presents a promising growth opportunity, driven by increasing disposable incomes and evolving consumer preferences. However, the fragmented nature of retail distribution in the region continues to pose challenges, limiting the potential for immediate large-scale expansion.

The Asia-Pacific region is witnessing rapid growth, with a compound annual growth rate (CAGR) of 9.68%, driven by strong performances in key markets such as China, Japan, South Korea, and India. India's gummy market is forecast to reach USD 1.59 billion by 2033, fueled by a growing preference for vegan products and the rapid expansion of the e-pharmacy sector, which has made gummies more accessible to consumers. Singapore has emerged as a premium market within the region, supported by its high per-capita income levels and demand for high-quality products. In contrast, South America and the Middle East & Africa collectively account for a smaller share of the global gummy market. However, these regions are increasingly attracting multinational companies due to the expanding middle-class population and the growing penetration of modern retail formats, which are creating new opportunities for market players.

Competitive Landscape

The gummy market's moderate fragmentation level of 4 out of 10 reflects a competitive landscape where established confectionery giants compete with specialized nutraceutical companies and emerging cannabis-focused brands. Traditional players like Mars, Haribo, and Ferrara leverage manufacturing scale and distribution networks, while supplement specialists such as Pharmavite and Church & Dwight capitalize on health-focused positioning and direct-to-consumer capabilities.

The market's fragmentation creates opportunities for innovative companies to establish niche positions through specialized formulations, unique ingredients, or targeted demographic approaches. Strategic patterns reveal a bifurcated approach where confectionery companies expand into functional segments while supplement manufacturers enhance palatability and consumer appeal. Mars's USD 70 million R&D facility investment in New Jersey demonstrates the commitment to innovation and sustainability that characterizes leading players.

Technology adoption focuses on manufacturing efficiency, ingredient innovation, and supply chain optimization, with companies investing in starch-free production methods and advanced quality control systems. White-space opportunities exist in personalized nutrition, therapeutic applications, and sustainable packaging solutions that address evolving consumer preferences and regulatory requirements.

Gummy Industry Leaders

-

Haribo GmbH & Co. KG

-

Ferrara Candy Co. (Ferrero)

-

Church & Dwight (Vitafusion)

-

Mars, Incorporated

-

Bayer AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: PIM Brands, Inc. introduced Juicefuls Fusions under its Welch’s Fruit Snacks brand. The juice-filled gummy snacks are available in three dual-flavored varieties: green apple and peach, watermelon and lemon, and blueberry and raspberry. The gluten- and peanut-free snacks are formulated with natural flavors, colors from natural sources and contain vitamins C, A, and E.

- June 2025: Tom Brady collaborated with Gopuff to introduce GOAT Gummies, an organic and vegan gummy product manufactured in France. The gummies contain no artificial sweeteners, dyes, or flavors and are made with real fruit. Gopuff, an instant delivery platform, is distributing the product exclusively in the United States.

- May 2025: Pharmavite opened a new facility in Ohio dedicated to gummy supplements manufacturing, featuring a 'Gummies Innovation Center of Excellence' for R&D of new products. The facility aims to create 225 local jobs and enhance production capabilities as gummy supplements became the number one form of vitamins and supplements in 2024.

- November 2024: Organigram Holdings Inc., a licensed cannabis producer, has launched Edison Sonics gummies, featuring the company's FAST nanoemulsion technology. The FAST technology enables up to 50% faster onset and improved bioavailability, delivering approximately double the cannabinoids at peak effect compared to traditional edible products.

Global Gummy Market Report Scope

| Candy Gummies |

| Functional/Nutraceutical Gummies |

| Cannabis and Hemp-Infused Gummies |

| Pharmaceutical Gummies |

| Pet Supplement Gummies |

| Gelatin-Based |

| Pectin-Based |

| Agar and Other Hydrocolloids |

| Children |

| Adults |

| Seniors |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialty Stores |

| Pharmacy/Drug Stores |

| Online Retail Stores |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Candy Gummies | |

| Functional/Nutraceutical Gummies | ||

| Cannabis and Hemp-Infused Gummies | ||

| Pharmaceutical Gummies | ||

| Pet Supplement Gummies | ||

| By Ingredient | Gelatin-Based | |

| Pectin-Based | ||

| Agar and Other Hydrocolloids | ||

| By Consumer Group | Children | |

| Adults | ||

| Seniors | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Specialty Stores | ||

| Pharmacy/Drug Stores | ||

| Online Retail Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the global gummy market size in 2025?

The gummy market size is valued at USD 36.35 billion in 2025.

How fast is the gummy market expected to grow?

The market is forecast to expand at an 8.38% CAGR between 2025-2030.

Which product segment is growing the quickest?

Cannabis and hemp-infused gummies are projected to record the fastest 10.34% CAGR through 2030.

Why are pectin-based gummies gaining traction?

Pectin satisfies vegan, kosher, and sustainability preferences and fuels a forecast 10.06% CAGR for plant-based formulations.

Page last updated on: