Nutraceutical Gummies Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

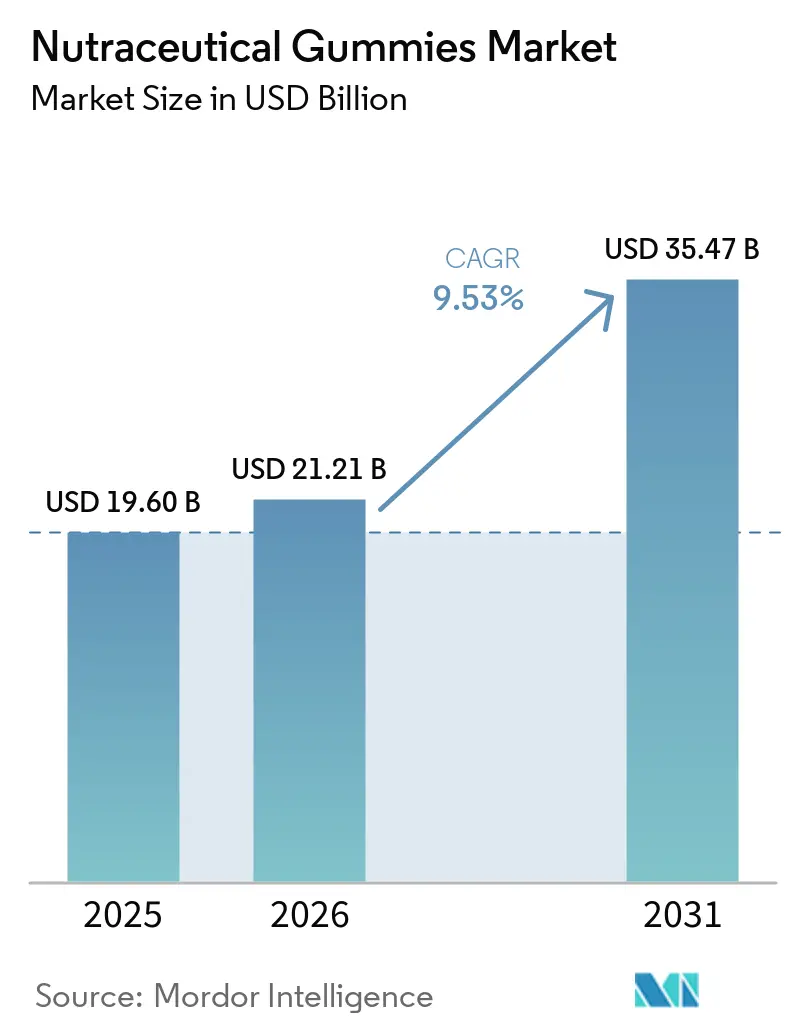

| Market Size (2026) | USD 21.21 Billion |

| Market Size (2031) | USD 35.47 Billion |

| Growth Rate (2026 - 2031) | 9.53% CAGR |

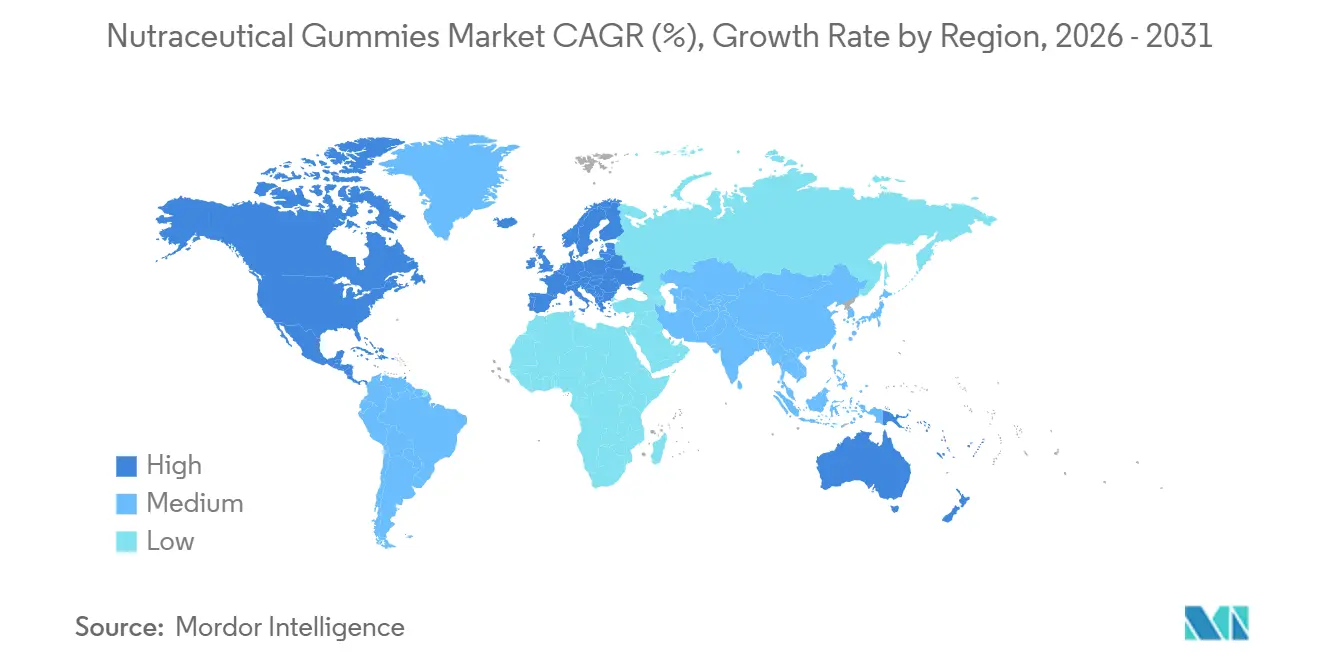

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nutraceutical Gummies Market Analysis by Mordor Intelligence

The nutraceutical gummies market size is projected to expand from USD 19.60 billion in 2025 and USD 21.21 billion in 2026 to USD 35.47 billion by 2031, registering a CAGR of 9.53% between 2026 to 2031. Continuous format-driven demand, growing gut-health awareness, and premiumization around clean-label claims are widening the category’s consumer base. Digestive formulations lead sales, while bone and joint health variants are rising fastest as collagen science gains clinical backing. Adults remain the dominant users, yet pediatric penetration is accelerating as parents favor sugar-reduced, kid-friendly dosage forms. In channel terms, supermarkets preserve impulse-buy leadership, though direct-to-consumer (DTC) subscription models strengthen margins and data capture. Competitive intensity is moderate, with mid-tier brands still able to win shelf space despite consolidation moves by multinational consumer-health conglomerates.

Key Report Takeaways

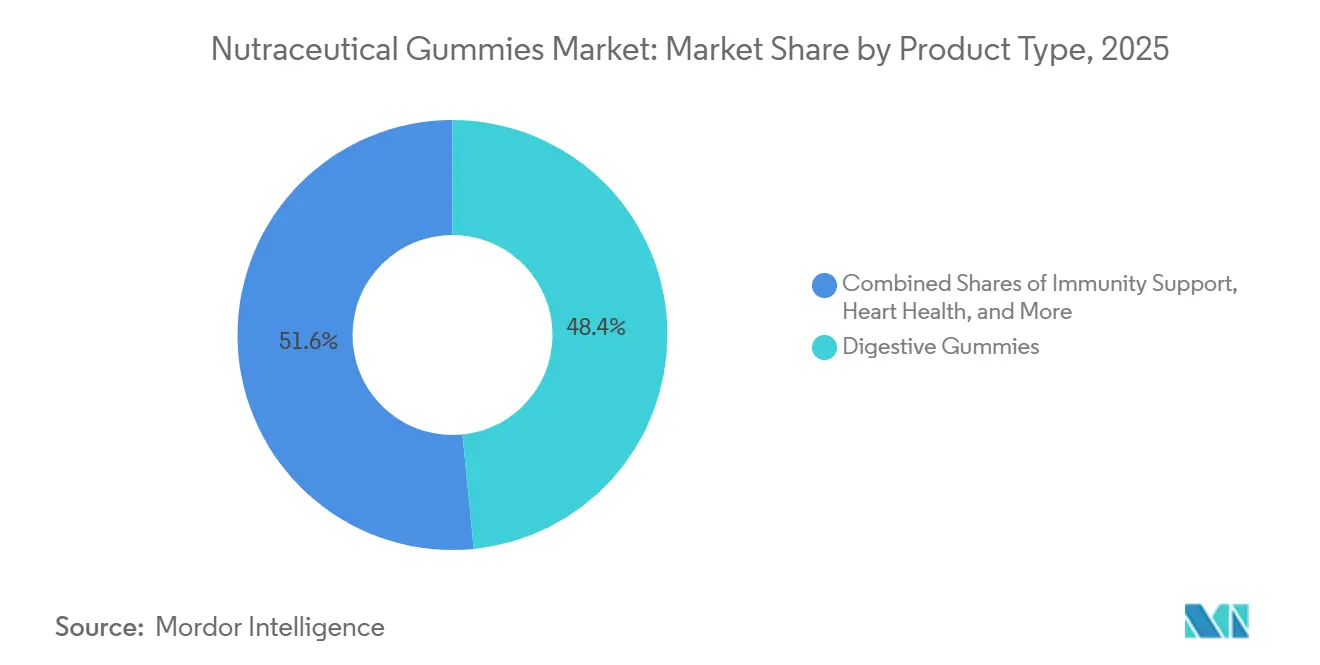

- By product type, digestive gummies commanded 48.42% of the nutraceutical gummies market share in 2025, while bone and joint health gummies are advancing at an 11.48% CAGR through 2031

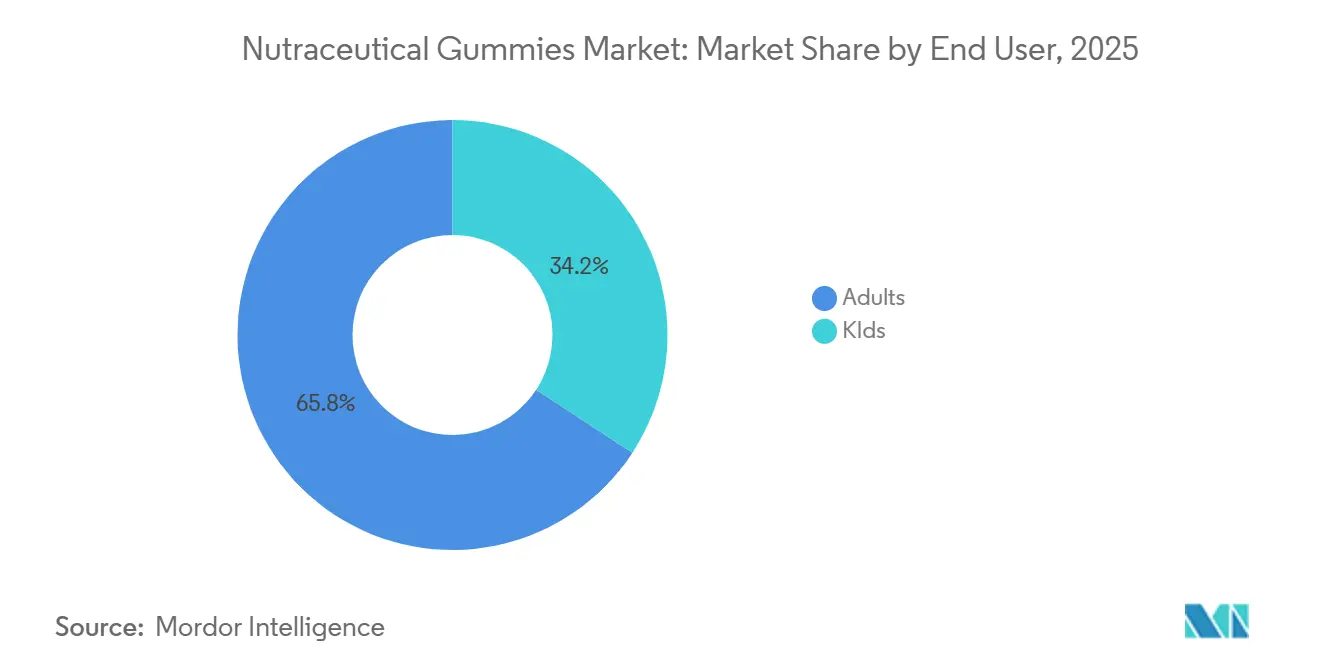

- By end user, adults accounted for 65.78% of consumption in 2025, whereas the kids segment is projected to expand at an 11.05% CAGR over 2026-2031.

- By distribution channel, supermarkets and hypermarkets held a 41.29% share of the nutraceutical gummies market in 2025, while online retail is the fastest-growing channel at an 11.27% CAGR to 2031.

- By geography, North America retained 43.21% of the nutraceutical gummies market share in 2025, while Asia-Pacific exhibits the fastest 10.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Nutraceutical Gummies Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing interest in functional nutrition | +2.1% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Convenient and palatable supplement format | +1.8% | Global, particularly strong in North America and Asia Pacific | Short term (≤ 2 years) |

| Rising consumer awareness of probiotics and gut health | +1.5% | Global, with early adoption in China, India, and United States | Medium term (2-4 years) |

| Product innovation: sugar-free, organic, vegan | +1.3% | North America and Europe core, expanding to Asia Pacific | Long term (≥ 4 years) |

| Increasing focus on immunity post-pandemic | +1.0% | Global, with sustained demand in Asia Pacific and South America | Short term (≤ 2 years) |

| Health and wellness focus | +0.9% | Global, with premium positioning in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Interest in Functional Nutrition

Functional nutrition has shifted from niche wellness circles to mainstream consumer behavior, with gummy formats emerging as a key avenue for ingredient experimentation. A 2025 study published in the Journal of Functional Foods indicated that 62% of consumers in the U.S. and Germany now prioritize bioactive compounds, such as omega-3 fatty acids, adaptogens, and nootropics, over basic vitamins. This represents a significant 19 percentage-point increase compared to 2020. Social media influencers have further driven this change by presenting supplementation as a proactive lifestyle choice rather than a reactive health measure. Gummy supplements leverage this trend by incorporating functional ingredients into a format that minimizes the cognitive resistance associated with pill-swallowing. This approach reduces barriers to both initial trials and repeat purchases. The takeaway is clear: brands that can credibly highlight ingredient origins and clinical validation are well-positioned to capture a larger share of health-conscious consumers.

Convenient and Palatable Supplement Format

Palatability remains the decisive competitive advantage for gummy supplements, particularly as taste preferences diverge across age groups and geographies. Kerry Group's 2026 Taste Charts revealed that gummy formats accounted for 23.4% of the global supplement market, up from 18.1% in 2023, with flavor innovation, such as elderberry, turmeric-ginger blends, and tropical fruit combinations, driving trial among skeptical consumers. Convenience extends beyond taste; single-serving packaging and shelf-stable formulations align with on-the-go consumption patterns, especially among working professionals and parents managing pediatric nutrition. This format advantage is particularly pronounced in the Asia Pacific, where traditional supplement forms like powders and tonics face cultural resistance among younger urban populations. The strategic takeaway is that convenience is not merely a feature but a category-defining attribute that justifies premium pricing and enables cross-category expansion into beauty, sleep, and cognitive health.

Rising Consumer Awareness of Probiotics and Gut Health

Gut health narratives have achieved mainstream penetration, with probiotics serving as the anchor ingredient for digestive gummy formulations. A 2025 cross-sectional study conducted across India, Saudi Arabia, and China found that 71% of respondents could correctly identify probiotics as beneficial bacteria, compared to 48% in 2020, indicating rapid knowledge diffusion facilitated by digital health platforms and physician endorsements. This awareness is translating into purchasing behavior; digestive gummies commanded 48.42% market share in 2025, with formulations combining Lactobacillus and Bifidobacterium strains alongside prebiotic fibers to enhance gut microbiome diversity. The National Institutes of Health (NIH) reported in 2024 that probiotic supplement use among U.S. adults increased by 34% between 2019 and 2023, with gummy formats capturing 41% of incremental volume due to perceived ease of use[1]Source: NIH Office of Dietary Supplements, “Probiotics Fact Sheet,” ods.od.nih.gov. Brands that can substantiate strain-specific health claims through peer-reviewed clinical trials will command pricing power and shelf priority in pharmacy channels.

Product Innovation: Sugar-Free, Organic, Vegan

Industry product development roadmaps are evolving to prioritize sugar-free, organic, and vegan profiles. In 2024, the World Health Organization issued guidelines on non-sugar sweeteners (NSS), recommending against artificial sweeteners for weight control. This has driven manufacturers to focus on natural alternatives such as stevia, monk fruit, and allulose[2]Source: WHO, “Guideline on Use of Non-Sugar Sweeteners,” who.int. By 2025, Israeli startup TopGum launched honey-based gummy supplements free of refined sugars, achieving distribution in 1,200 European pharmacies within six months. Organic certification, regulated by the USDA National Organic Program in the U.S. and the EU Organic Regulation 2018/848 in Europe, has become a critical requirement for premium market positioning. This is particularly significant for millennial and Gen Z consumers, who closely examine ingredient labels. Vegan formulations, which use pectin or agar instead of gelatin, represented an estimated 28% of new product launches in 2025, up from 19% in 2023. This growth highlights the increasing importance of ethical consumerism and allergen avoidance strategies.

Sugar Content Concerns

Gummy supplements, particularly those designed for children, are under increased scrutiny due to their sugar content. In 2024, Germany's Federal Institute for Risk Assessment (BfR) highlighted concerns by reporting that some children's gummy vitamins contain up to 3 grams of sugar per serving. This amount represents 12% of the World Health Organization's (WHO) recommended daily sugar limit for children aged 4 to 6, raising alarms about potential dental and metabolic health risks. At the same time, the European Union is considering revisions to Regulation 1924/2006, which oversees nutrition and health claims. The proposed changes would require front-of-pack labeling for added sugars in supplements, a measure that could reduce impulse purchases and necessitate reformulation. To address these challenges, manufacturers are adopting sugar alcohols such as erythritol and xylitol, along with natural sweeteners. However, these alternatives come with a 15-25% cost increase and may cause gastrointestinal discomfort when consumed in large amounts. The key challenge lies in striking a balance between maintaining palatability, which is crucial for compliance and repeat purchases, and meeting clean-label demands. This dynamic tends to benefit vertically integrated companies with proprietary sweetening technologies.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sugar content concerns | -1.2% | Europe and North America core, expanding to Asia Pacific | Short term (≤ 2 years) |

| Competition from alternative formats | -0.9% | Global, with traditional format preference in South America and MEA | Medium term (2-4 years) |

| Stability and shelf-life issues | -0.7% | Global, particularly acute in tropical climates (Southeast Asia, MEA) | Long term (≥ 4 years) |

| Allergen and ingredient restrictions | -0.5% | Europe and North America, with emerging regulatory frameworks in Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from Alternative Formats

Gummy supplements face persistent competition from capsules, tablets, powders, and liquid formats, each offering distinct advantages in bioavailability, dosing precision, or cost efficiency. Capsules and tablets dominate in clinical and pharmacy settings due to standardized dosing and longer shelf life, while powders appeal to fitness enthusiasts seeking customizable serving sizes and rapid absorption. The Council for Responsible Nutrition (CRN) reported in 2025 that capsules and tablets still accounted for 54% of the U.S. dietary supplement market by volume, with gummies capturing 23%, indicating that format preference remains fragmented[3]. Liquid supplements, particularly in single-serve sachets, are gaining traction in Asia Pacific markets where on-the-go consumption patterns favor portability over palatability. The competitive implication is that gummy manufacturers must continuously innovate on texture, flavor, and functional ingredient loading to justify price premiums, while also defending against private-label encroachment in mass retail channels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Digestive Dominance Meets Bone Health Surge

In 2025, digestive gummies secured a dominant 48.42% share of the nutraceutical gummies market, establishing their leadership with clinically validated multi-strain probiotic blends. This growth reflects increasing consumer awareness of the microbiome's critical role in immunity and mental health. As retailers prioritize gut-health products with prime shelf placement and physicians recommend probiotic gummies for patients who avoid capsules, the market for digestive nutraceutical gummies is expected to expand further. Manufacturers are differentiating their offerings by focusing on strain specificity, ensuring CFU transparency, and adding prebiotic fibers, thereby increasing switching costs for brand-loyal consumers.

Bone and joint health gummies are projected to grow at a faster rate than the overall category, with an anticipated 11.48% CAGR. These formulations, enriched with collagen peptides, vitamin D3, and calcium, appeal to aging populations aiming to preserve mobility. A 2024 randomized trial demonstrated a 4.2% improvement in bone mineral density after 12 months of collagen supplementation. Brands are highlighting clean-label collagen sources, with premium claims such as grass-fed or marine origins. Retailers are integrating bone-health gummies into active-aging displays, driving larger shopper basket sizes.

By End User: Adult Stability, Pediatric Acceleration

In 2025, adults represented a substantial 65.78% share of the nutraceutical gummies market. This dominance is attributed to the growing demand for functional stackers that address stress management, cognitive enhancement, and cardiovascular health, particularly among wellness-oriented professionals who prioritize convenience. The segment's growth is further supported by direct-to-consumer (DTC) programs, which not only provide monthly supply packs but also integrate lifestyle-focused content. These programs play a crucial role in fostering routine consumption, improving adherence rates, and significantly reducing customer churn.

Kids’ gummies, though smaller, are expanding at an 11.05% CAGR on the back of parental focus on nutrient gaps. Formulations minimize sugar and artificial colors while maximizing flavor acceptance, often leveraging mascot branding to encourage daily compliance. Regulatory mandates for age-specific dosing and allergen notice, updated by the FDA in 2024, enhance trust and legitimize brand claims. Classroom wellness campaigns and pediatrician endorsements further normalize gummy supplementation among school-age children.

By Distribution Channel: Shelf Space Versus Digital Agility

In 2025, supermarkets and hypermarkets represented 41.29% of the nutraceutical gummies market share, primarily driven by impulse purchases at checkout counters and the presence of dedicated health aisles. These retail formats enhance product visibility through promotional end-caps and bundled discounts, which are particularly effective during high-demand periods such as the cold-and-flu season or back-to-school shopping. The allocation of shelf space is often influenced by trade-promotion budgets, providing a competitive advantage to established players with substantial resources.

Online retail, expanding at a CAGR of 11.27%, has significantly lowered entry barriers for emerging brands by leveraging social proof and advanced algorithmic targeting. For instance, Care/of utilizes personalized quiz funnels to engage consumers, while Goli Nutrition capitalizes on influencer partnerships to transform product discovery into long-term subscriptions. Direct-to-consumer (DTC) channels offer margins that are typically 10-12 percentage points higher than those of traditional brick-and-mortar stores, enabling brands to reinvest in aggressive research and branding efforts. Successful omnichannel strategies incorporate features like QR codes on physical packaging, which redirect consumers to loyalty portals. This approach not only enhances customer engagement but also facilitates the collection of cross-channel behavioral data, providing valuable insights for future marketing and product development initiatives.

Geography Analysis

North America held 43.21% nutraceutical gummies market share in 2025, anchored by stringent FDA cGMP oversight, which elevates perceived quality. U.S. brands like Vitafusion and L’il Critters generated USD 637 million in revenue in 2024, underlining continued household penetration. Canadian consumption rises alongside government nutrition campaigns, while Mexico benefits from cross-border e-commerce imports. Market maturity slows unit growth but lifts premiumization, as consumers trade up to vegan or organic lines.

Asia Pacific is forecast to register a 10.46% CAGR during 2026-2031, the fastest globally. Rising disposable incomes in China and India intersect with broader preventive-health narratives. Chinese SAMR labeling reforms enacted in 2024 have increased compliance expense yet boosted consumer confidence. Japan’s aging society values bone-health and cognitive gummies, while Australia’s well-established pharmacy networks stock immunity and beauty SKUs. Southeast Asian climates magnify stability hurdles, spurring demand for microencapsulated formulas.

Europe ranks third by value, driven by Germany, the United Kingdom, and France, where organic and vegan designations sway purchase decisions. The Netherlands and Sweden show above-average growth as e-pharmacies gain traction. The EU’s mooted sugar labeling regulation could trigger regional reformulations, elevating R&D costs but differentiating low-sugar pioneers. South America’s expansion clusters around Brazil and Argentina, though currency volatility remains a risk. The Middle East and Africa offer nascent but high-potential opportunities in the United Arab Emirates, Saudi Arabia, and South Africa; fragmented regulations and supply-chain constraints require local partnerships.

Competitive Landscape

The nutraceutical gummies market, with a moderate concentration, demonstrates that mid-tier players continue to hold pricing power and distribution leverage. This remains the case even as multinational consumer health corporations expand through acquisitions and organic innovations. Leading brands such as Church & Dwight's Vitafusion, Unilever's OLLY, and Bayer's One A Day dominate shelf space in mass retail and pharmacy channels. They achieve this by utilizing substantial marketing budgets and fostering strong retailer relationships to secure premium placements. At the same time, digitally native brands like Goli Nutrition and Care/of are disrupting traditional distribution models. By implementing direct-to-consumer subscription strategies, they ensure steady revenue streams and gain critical first-party consumer data.

Bayer's 2024 acquisition of Care/of highlights a strategic shift, recognizing that subscription-based models and personalized recommendations are shaping the future of supplement retail. Opportunities remain in therapeutic-dose formulations, condition-specific products, and geographic expansion into the rapidly growing Asia Pacific markets, where local flavor preferences and ingredient demands create entry barriers for Western brands. Emerging disruptors are utilizing technology to gain a competitive advantage. For example, vertically integrated manufacturers are adopting microencapsulation techniques that extend shelf life by 40%. This innovation addresses persistent challenges such as moisture sensitivity and active ingredient degradation, as documented in peer-reviewed research from 2025.

As transparency and quality assurance become increasingly important to both retailers and consumers, compliance with FDA cGMP standards and third-party certifications like NSF International and USP Verified is transitioning from a competitive differentiator to a baseline requirement. Consequently, competition is expected to intensify across three key areas: ingredient innovation supported by clinical trials, omnichannel distribution strategies that balance physical shelf presence with digital adaptability, and operational excellence in manufacturing to ensure product stability and regulatory compliance.

Nutraceutical Gummies Industry Leaders

Church & Dwight Co. Inc.

Unilever plc

The Clorox Company

Nestle S.A.

Bayer AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Gummi World launched a line of stock formulas aimed at accelerating market entry for nutraceutical brands. These formulas provide customizable, compliant gummy bases that reduce the time and complexity of developing unique gummy supplements.

- March 2025: Sirio launched its XtraGummies range, highlighting breakthrough gummy supplements that combine high nutritional impact with superior sensory experience. The portfolio’s six key formulas include omega-3, creatine, iron, magnesium citrate, biotin, and selenium gummies, all designed for efficacy, stability, and taste.

- January 2025: Sirio introduced XtraGummies, an innovative high-strength gummy technology designed to deliver potent doses of challenging functional ingredients in a convenient, enjoyable format. The range includes six concepts addressing common supplement needs, including Xtra Omega-3: Provides 125 mg DHA per gummy from fish oil, Xtra Creatine: Offers 1,800 mg per gummy for muscle strength and recovery, and Xtra Iron: Contains 14 mg iron along with a triple-ingredient blend to maximize absorption.

- September 2024: TopGum Industries advanced its range of specialized gummy supplements targeting diverse groups including children, adults, seniors, and athletes. With tailored formulations incorporating premium organic, functional, and sports nutrition ingredients, their products were asserted to exemplify the broader market trend toward segmentation and personalization in gummy supplements.

Global Nutraceutical Gummies Market Report Scope

| Digestive Gummies |

| Immunity Support Gummies |

| Beauty and Skin Health Gummies |

| Brain and Cognitive Health Gummies |

| Sleep and Stress Management Gummies |

| Weight Management Gummies |

| Bone and Joint Health Gummies |

| Heart Health Gummies |

| Others |

| Kids |

| Adults |

| Supermarkets And Hypermarkets |

| Pharmacies and Health Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Digestive Gummies | |

| Immunity Support Gummies | ||

| Beauty and Skin Health Gummies | ||

| Brain and Cognitive Health Gummies | ||

| Sleep and Stress Management Gummies | ||

| Weight Management Gummies | ||

| Bone and Joint Health Gummies | ||

| Heart Health Gummies | ||

| Others | ||

| By End User | Kids | |

| Adults | ||

| By Distribution Channel | Supermarkets And Hypermarkets | |

| Pharmacies and Health Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the nutraceutical gummies market in 2031?

It is forecast to reach USD 35.47 billion by 2031, expanding at a 9.53% CAGR from 2026-2031.

Which product type currently leads sales?

Digestive gummies lead with 48.42% nutraceutical gummies market share in 2025.

Which region is expected to grow fastest through 2031?

Asia Pacific is poised for the quickest expansion at a projected 10.46% CAGR over the forecast period.

Why are sugar-free gummies gaining traction?

Regulatory scrutiny of added sugars and consumer demand for cleaner labels push brands toward stevia, monk fruit, and allulose sweetening systems.

Page last updated on: