Gummy Vitamin Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 10.33 Billion |

| Market Size (2031) | USD 16.47 Billion |

| Growth Rate (2026 - 2031) | 9.78% CAGR |

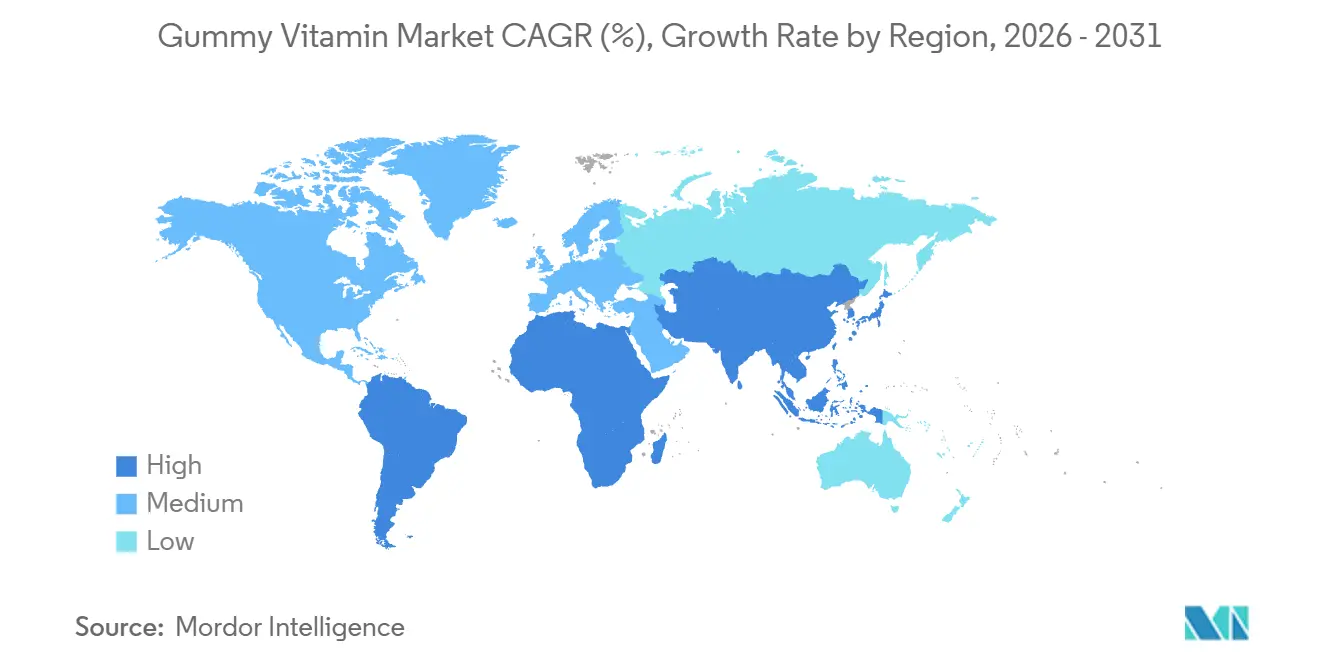

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

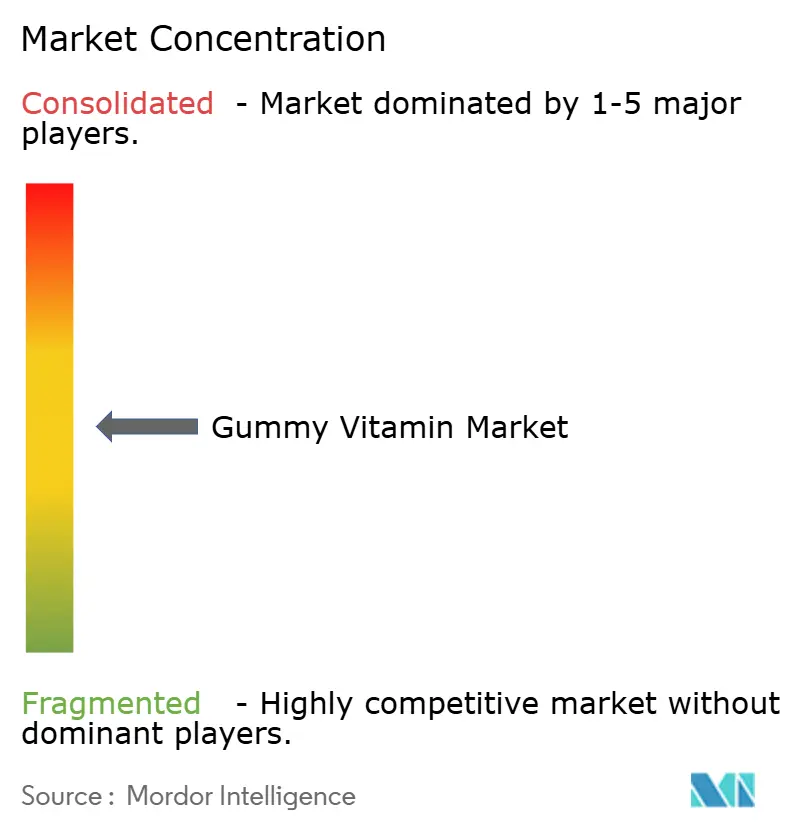

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gummy Vitamin Market Analysis by Mordor Intelligence

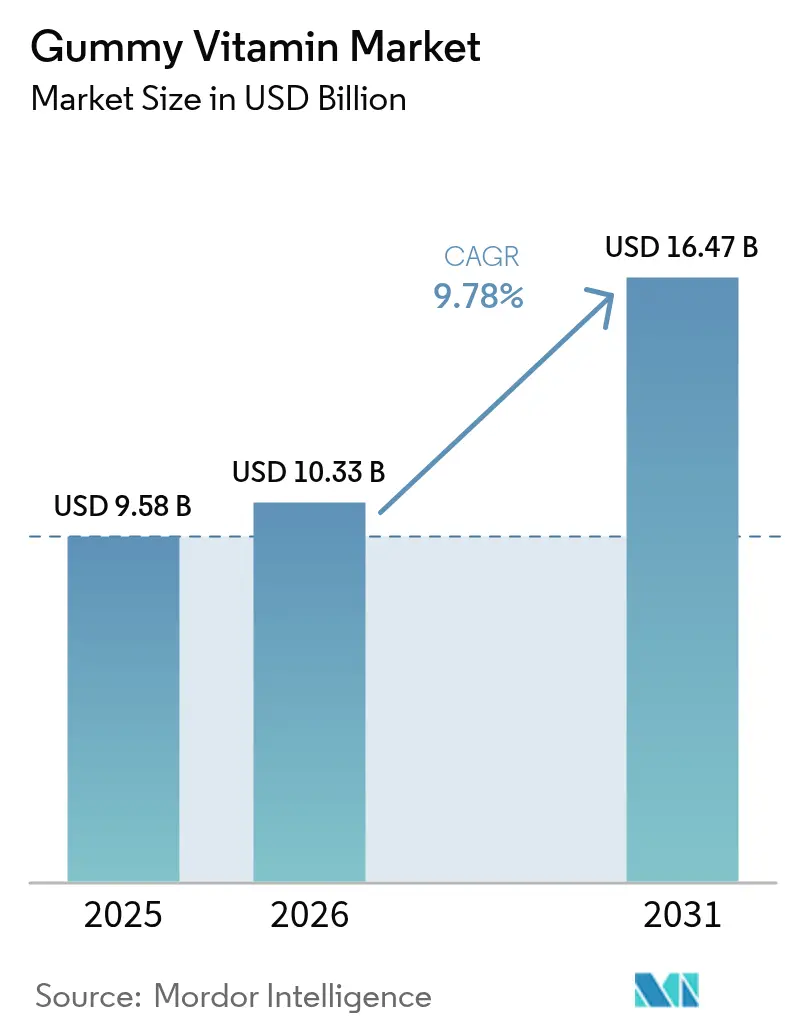

The gummy vitamin market size is projected to be USD 9.58 billion in 2025, USD 10.33 billion in 2026, and reach USD 16.47 billion by 2031, growing at a CAGR of 9.78% from 2026 to 2031. Multivitamin gummies continue to lead the market, while single-nutrient products are experiencing increased demand as consumers leverage diagnostics and wearable devices to optimize their micronutrient intake. This shift is driven by factors such as aging populations, a growing preference for vegan-friendly options like pectin instead of gelatin, and the introduction of sugar-free or organic formulations, which are expanding the potential consumer base. Stricter regulations in regions including the United States, the European Union, China, and India are increasing compliance costs, creating an advantage for larger, well-funded companies. Additionally, investments in supply chains, such as the establishment of large-scale gummy production facilities in the United States and e-commerce hubs in the Asia-Pacific region, reflect sustained confidence in the growth of the gummy vitamin market.

Key Report Takeaways

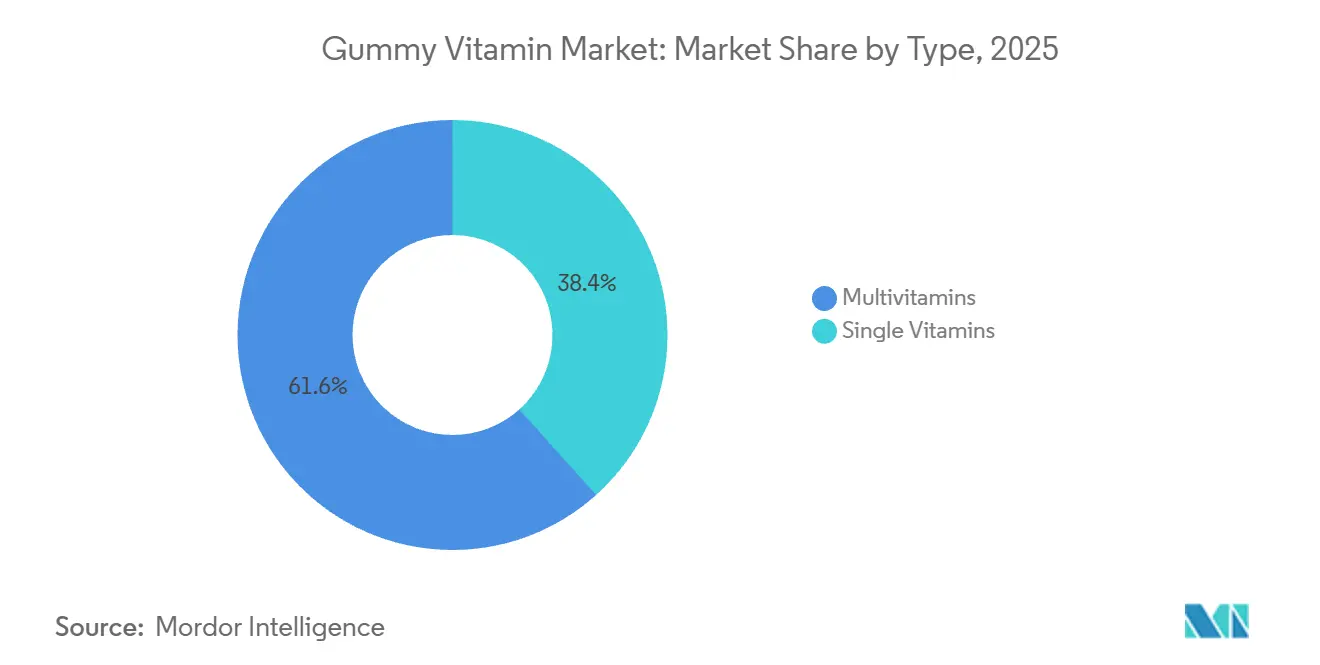

- By product type, multivitamins led with 61.64% of gummy vitamins market share in 2025, while single-vitamin products are forecasted to expand at a 10.54% CAGR through 2031.

- By category, adults accounted for 69.89% of the gummy vitamins market size in 2025, and seniors are poised to grow at a 10.81% CAGR.

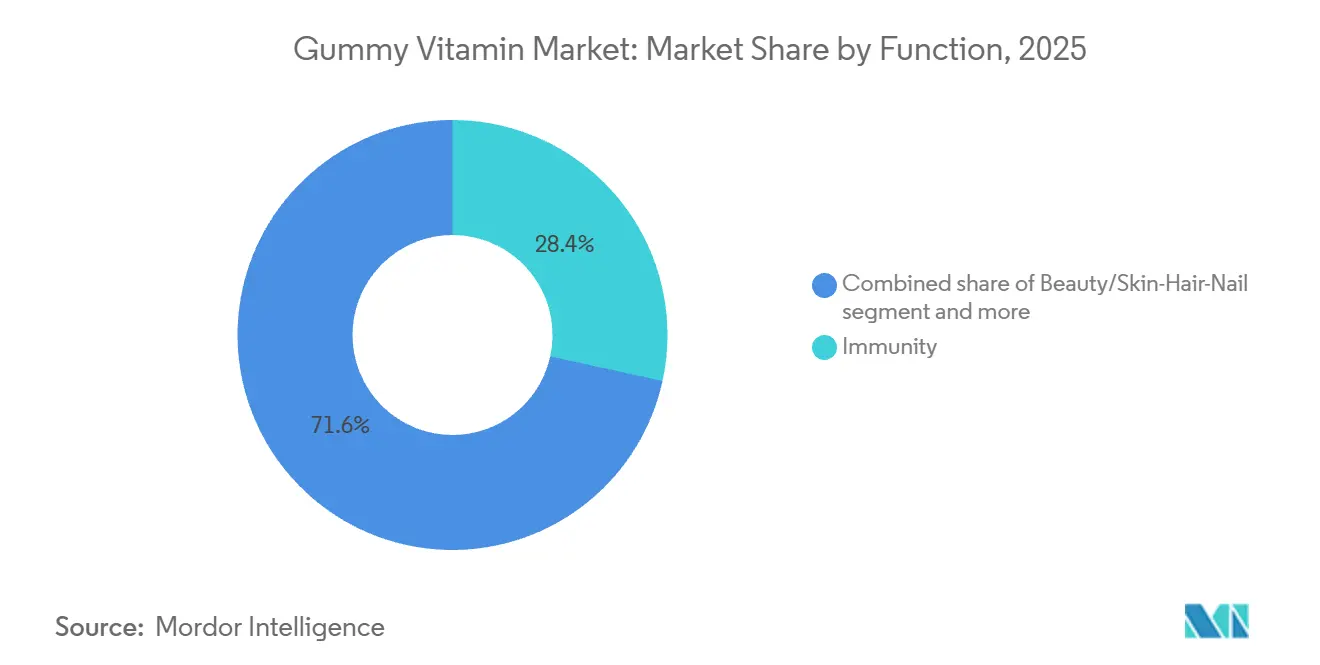

- By function, immunity products secured a 28.43% share of the gummy vitamins market size in 2025, and the beauty/skin-hair-nail segment is advancing at a 11.43% CAGR.

- By packaging, bottles commanded 62.43% of 2025 revenue, whereas stand-up pouches are projected to post a 10.43% CAGR.

- By distribution channel, supermarkets/hypermarkets held 62.31% share in 2025, and online retail shows the quickest 10.93% CAGR to 2031.

- By geography, North America held 34.22% share in 2025, and Asia-Pacific shows the quickest 10.82% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gummy Vitamin Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising focus on preventive healthcare and daily nutrition | +1.8% | Global, with pronounced uptake in North America and Europe | Medium term (2-4 years) |

| Increasing vegan population demanding plant-based options | +1.5% | North America and Europe core, expanding into Asia-Pacific urban centers | Medium term (2-4 years) |

| Growing geriatric population seeking easy-to-consume formats | +1.6% | Global, with accelerated impact in Asia-Pacific and Europe due to aging demographics | Long term (≥ 4 years) |

| Product innovations like sugar-free and organic variants | +1.4% | North America and Europe lead, with spillover to premium segments in Asia-Pacific | Short term (≤ 2 years) |

| Expansion in health-conscious millennials and fitness enthusiasts | +1.3% | Global, with urban concentration in Asia-Pacific, North America, and Middle East | Medium term (2-4 years) |

| Surge in immunity-boosting demands post-pandemic | +1.2% | Global, with sustained elevation in markets that experienced severe COVID-19 waves | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising focus on preventive healthcare and daily nutrition

Preventive healthcare has transitioned from a clinical focus to a consumer-driven habit, with a majority of Americans now using dietary supplements, as reported by the Council for Responsible Nutrition's 2024 survey [1]Source: Council for Responsible Nutrition, “2024 CRN Consumer Survey on Dietary Supplements,” crnusa.org. Gummy vitamins have gained popularity by addressing adherence challenges as chewable formats eliminate the need for water and mask the metallic or chalky aftertaste often associated with tablets. A consumer health report highlighted that household spending on wellness products increased by 12% annually between 2022 and 2025, with convenience-focused formats capturing a significant share of this growth. The United States supplement market is increasingly driven by consumers viewing supplementation as a proactive measure to address nutritional gaps rather than a reactive solution. This proactive approach is particularly evident in employer-sponsored wellness programs that subsidize vitamin subscriptions, integrating gummy formats into corporate health benefits. Additionally, the trend aligns with personalized nutrition platforms that recommend specific micronutrient combinations based on genetic testing or wearable device data, positioning gummies as customizable components in tailored regimens.

Increasing vegan population demanding plant-based options

The growing vegan population is driving increased demand for pectin-based gummy formulations as alternatives to traditional gelatin derived from animal collagen. Pectin, sourced from citrus peels or apple pomace, provides a similar texture and chewability while meeting plant-based certifications, such as the Vegan Society's Vegan Trademark. Unilever's acquisition of SmartyPants Vitamins in November 2020 highlighted the appeal of non-genetically modified organism (non-GMO), clean-label products, which resonate with flexitarian and vegan consumers who prioritize ingredient transparency. This consumer segment also contributes to premiumization, as plant-based gummies are priced significantly higher than gelatin-based counterparts due to elevated raw material costs and certification requirements. Retailers report that vegan gummy stock-keeping units (SKUs) experience faster inventory turnover in urban markets with significant millennial and Generation Z populations, who value ethical sourcing over price considerations. This trend extends beyond vitamins to include vegan collagen precursors such as amino acids and vitamin C blends, which support endogenous collagen synthesis without relying on animal-derived peptides.

Growing geriatric population seeking easy-to-consume formats

The United Nations estimates that the global population aged 65 and above will increase significantly by 2050, with the Asia-Pacific region contributing the majority of this growth. Difficulty swallowing, known as dysphagia, affects a notable portion of seniors, making gummy vitamins a practical necessity rather than a lifestyle choice. Vitamin D3 gummies fulfill an important need in this group, as aging skin produces substantially less cholecalciferol from sunlight compared to younger adults, requiring supplementation to support bone density and immune function [2]Source: National Institutes of Health, “Vitamin D,” ods.od.nih.gov. In the United States, a large percentage of Medicare beneficiaries use supplements, with gummy formats favored for their taste and ease of portioning. Japan's Ministry of Health, Labour and Welfare has endorsed Foods for Specified Health Uses, which include senior-friendly gummy formats enriched with calcium, magnesium, and B-complex vitamins to help address age-related cognitive decline. Furthermore, packaging innovations such as easy-open bottles with large-print labels and single-serve sachets reduce challenges for individuals with arthritis, thereby improving accessibility for this demographic.

Product innovations like sugar-free and organic variants

Pharmavite introduced its Nature Made Zero Sugar gummies in March 2024, utilizing allulose, a rare sugar with significantly fewer calories than sucrose, to address consumer concerns about added sugars conflicting with low-glycemic diets. Allulose is not metabolized by the body and does not raise blood glucose levels, making it suitable for diabetics and individuals following ketogenic diets who previously avoided gummy supplements. Additionally, stevia and monk fruit extracts are gaining popularity as natural sweeteners that meet Food and Drug Administration (FDA) Generally Recognized as Safe (GRAS) standards while avoiding the aftertaste associated with earlier sugar alcohols like sorbitol. Organic certifications, such as USDA Organic in the United States and EU Organic under Regulation (EU) 2018/848, provide premium shelf positioning and justify price increases by assuring consumers that ingredients are free from synthetic pesticides and genetically modified organisms (GMOs). Pharmavite's February 2024 launch of Advanced Multivitamin Gummies, which contain significantly more nutrients than previous formulations, highlights the competition among brands to enhance nutrient density while addressing the bioavailability constraints of gummy formats. These innovations also align with regulatory requirements as the FDA's mandate for added sugars labeling on Nutrition Facts panels has compelled brands to reformulate their products to avoid potential consumer rejection.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict regulatory compliance for labeling and claims | -0.6% | Global, with heightened enforcement in North America and Europe under FDA and EFSA oversight | Medium term (2-4 years) |

| Artificial additives raising safety and transparency concerns | -0.5% | North America and Europe lead consumer backlash, with spillover to urban Asia-Pacific markets | Short term (≤ 2 years) |

| Presence of added sugars conflicting with low-sugar diets | -0.4% | Global, with pronounced impact in North America and Europe where low-glycemic diets are prevalent | Short term (≤ 2 years) |

| Shelf-life and stability issues with natural ingredients | -0.4% | Global, with particular challenges in tropical climates and markets lacking cold-chain infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict regulatory compliance for labeling and claims

The United States Food and Drug Administration (FDA) increased its issuance of warning letters to dietary supplement manufacturers by 100% between 2017 and 2022. These warnings primarily focused on unapproved disease claims, contamination issues, and violations of current Good Manufacturing Practice (CGMP) standards. Gummy vitamin producers have been subjected to greater scrutiny because the candy-like appearance of these products makes them particularly appealing to children. This has led to the enforcement of mandates requiring child-resistant packaging and labeling instructions that clearly advise consumers to "keep out of reach of young children." The European Food Safety Authority (EFSA) introduced updated guidance in September 2024, which is scheduled to take effect in February 2025 [3]Source: European Food Safety Authority, “Administrative guidance for the preparation of applications on new nutrient sources,” efsa.onlinelibrary.wiley. This guidance mandates novel food authorization for new micronutrient sources and requires the inclusion of relative bioavailability data to substantiate absorption claims. The European Union (EU) Directive 2002/46/EC, consolidated in July 2024, outlines the permitted vitamins and minerals in Annexes I and II. However, it delegates the responsibility of setting maximum and minimum dosage levels to individual member states, resulting in a fragmented compliance framework that poses challenges for cross-border e-commerce operations. Furthermore, the EFSA's Health Claims Article 8 working group has identified 13 substances, including melatonin, curcumin, ashwagandha, and tryptophan, for potential restriction in dietary supplements due to safety concerns at high doses. This has compelled manufacturers to reformulate products and has caused delays in product launches.

Artificial additives raising safety and transparency concerns

Consumer advocacy groups have raised concerns about synthetic colors, such as Red 40 and Yellow 5, and artificial flavors in gummy vitamins, citing potential links to hyperactivity in children and calling for clean-label alternatives. The United States Food and Drug Administration's (FDA) labeling mandate for added sugars, implemented in 2020, revealed that many gummy vitamin formulations contain 2 to 4 grams of sugar per serving, accounting for 5% to 10% of the daily recommended limit. This has led to criticism from proponents of low-sugar diets. In response, brands are reformulating their products using natural colorants like beet juice, turmeric, and spirulina, as well as plant-based sweeteners. However, these alternatives often present challenges, such as reduced shelf stability. Natural colors tend to fade when exposed to ultraviolet (UV) light, and pectin-based gummies without synthetic preservatives are more susceptible to microbial contamination. The European Union's Chemicals Data Platform, established under Regulation (EU) 2025/2455, aims to collect ingredient data from supplement manufacturers by January 2029. Mandatory study notifications will begin in November 2027, enhancing transparency but also potentially exposing proprietary formulations to competitors. Additionally, counterfeit gummy vitamins sold on e-commerce platforms, particularly Amazon, which features over 10,000 supplement brands, undermine consumer trust. Third-party sellers often bypass quality control measures, listing products with unverified ingredient claims.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Single-Nutrient Precision Outpaces Broad-Spectrum Blends

Multivitamin gummies accounted for 61.64% of the projected 2025 revenue, highlighting their popularity as a convenient nutritional solution for time-constrained consumers who prioritize simplicity over targeted supplementation. In contrast, single-vitamin formats are expected to grow at a compound annual growth rate (CAGR) of 10.54% through 2031. This growth is driven by consumers seeking precise dosing to address specific deficiencies identified through blood tests or feedback from wearable devices. Within the single-vitamin category, Vitamin D3 gummies lead the market, addressing widespread deficiencies. According to the National Institutes of Health (NIH), 42% of adults in the United States are vitamin D deficient. This segment benefits from clinical evidence linking adequate vitamin D levels to improved bone health, immune function, and mood regulation. Vitamin C gummies, which gained popularity during the pandemic, have maintained their momentum as consumers associate ascorbic acid with immune support and collagen synthesis.

Biotin gummies, promoted for enhancing hair and nail strength, have gained traction among women aged 25-45. Influencer endorsements on platforms such as Instagram and TikTok have played a significant role in driving impulse purchases in this segment. Multivitamin formulations are increasingly focusing on nutrient density to differentiate themselves in the market. For instance, Pharmavite's February 2024 launch of Advanced Multivitamin Gummies introduced a product offering approximately 60% more nutrients than previous versions. This includes harder-to-stabilize compounds such as folic acid and iron, which enhance the overall nutritional value of the product.

By Category: Seniors Segment Accelerates as Aging Demographics Reshape Demand

Adults accounted for 69.89% of gummy vitamin consumption in 2025, driven by working-age populations aged 25 to 64 years who incorporate gummy vitamins into their daily wellness routines. This group treats gummy vitamins as an integral part of their morning habits. However, the seniors segment is projected to grow at a compound annual growth rate (CAGR) of 10.71% through 2031. This growth is supported by the United Nations' projection that the global population aged 65 years and above will reach 1.5 billion by 2050, with the Asia-Pacific region contributing 60% of this increase. Dysphagia, a condition that makes swallowing difficult and affects up to 15% of seniors, makes chewable formats a medically preferable option compared to tablets. Additionally, age-related taste bud atrophy enhances the appeal of gummies' fruit flavors over chalky alternatives. In the United States, more than 75% of Medicare beneficiaries use supplements, with calcium, vitamin D, and B-complex gummies addressing conditions such as osteoporosis, immune system decline, and cognitive impairment.

The children's segment, while smaller in overall consumption, benefits from parents' willingness to pay premiums for products that simplify the process of administering vitamins, avoiding daily struggles over pill-taking. Compliance costs are increased by child-resistant packaging requirements and "keep out of reach" labeling, but these measures also enhance safety and provide reassurance to parents. In Japan, the Food for Specified Health Uses (FOSHU) system has approved senior-specific gummy formulations fortified with calcium and magnesium to address bone density loss, establishing a regulatory framework for age-targeted health claims.

By Function: Beauty-from-Within Disrupts Immunity's Dominance

In 2025, immunity-focused products contributed 28.43% of revenue, driven by post-pandemic consumer demand for vitamin C, vitamin D, and zinc gummies, which are marketed for their immune resilience benefits. Meanwhile, the beauty and skin-hair-nail applications segment is projected to grow at a compound annual growth rate (CAGR) of 11.43% through 2031. This growth aligns with Unilever's report, which highlights significant expansion in the beauty-from-within category, expected to continue in the coming years. Biotin gummies, known for promoting keratin synthesis and enhancing hair strength, dominate this segment. Their popularity is bolstered by influencer-led campaigns on platforms like TikTok and Instagram, showcasing before-and-after transformations that drive impulse purchases. Collagen gummies, containing hydrolyzed peptides sourced from bovine or marine origins, are also projected to grow at a steady CAGR during the forecast period. These products primarily target women aged 30 to 50, addressing concerns such as skin elasticity and wrinkle prevention.

Bone and joint health gummies, fortified with calcium, magnesium, and vitamin K2 (menaquinone-2), cater to the senior demographic. However, they face competition from prescription osteoporosis medications, which offer higher efficacy. Digestive health gummies, formulated with probiotics like Lactobacillus and Bifidobacterium strains and prebiotics such as inulin and fructooligosaccharides, encounter challenges related to shelf stability. Live cultures often degrade in gummy matrices unless microencapsulated, a process that increases formulation complexity and costs. Other functional gummy categories include energy products with B-complex vitamins and coenzyme Q10 (CoQ10), sleep aids containing melatonin and L-theanine, and cognitive support products featuring omega-3 docosahexaenoic acid (DHA) and bacopa monnieri. These categories represent fragmented niches that brands use to differentiate themselves in competitive retail markets.

By Packaging Type: Stand-Up Pouches Challenge Bottle Hegemony

Bottles accounted for 62.43% of the packaging share in 2025, supported by established retail shelf standards, compatibility with child-resistant caps, and consumer familiarity. Stand-up pouches are projected to grow at a compound annual growth rate (CAGR) of 10.43% through 2031, driven by sustainability considerations. These pouches use 60% to 70% less plastic compared to rigid bottles and reduce shipping weight, thereby lowering carbon footprints. Brands such as SmartyPants and MaryRuth Organics have adopted pouches to emphasize eco-consciousness, appealing to millennial and Generation Z consumers who prioritize environmental impact in their purchasing decisions. Additionally, pouches offer features like resealable zippers and single-serve tear-off sachets, enhancing portability for travel and gym use.

Blister packs, commonly used in pharmaceutical applications, provide tamper-evidence and precise dosing but incur higher per-unit costs, making them less viable for high-volume consumer products. Other packaging formats, such as jars and tubes, cater to niche applications like gift sets or subscription boxes. Child-resistant packaging remains a requirement under the Poison Prevention Packaging Act in the United States and similar regulations in the European Union, adding 5% to 10% to packaging costs while reducing liability risks.

By Distribution Channel: E-Commerce Disrupts Traditional Retail Gatekeeping

Supermarkets and hypermarkets are projected to account for 62.31% of the distribution share in 2025. These channels benefit from high foot traffic, opportunities for impulse purchases, and the ability to cross-merchandise gummy vitamins with adjacent categories such as pharmacy and snacks. Online retail stores are expected to grow at a compound annual growth rate (CAGR) of 10.93% through 2031. This growth is supported by Amazon's disclosure of approximately USD 20 billion in supplement sales, which are increasing at a rate of 21% year-over-year. The growth of e-commerce has significantly outpaced that of brick-and-mortar channels. Over time, e-commerce has expanded at a much faster rate than physical retail, driven by factors such as subscription models, direct-to-consumer brands, and algorithmic product recommendations that increase basket sizes. Amazon, hosting a wide range of supplement brands, holds a significant share of online vitamin and mineral supplement sales, creating a competitive environment where top-ranked listings dominate click-through rates.

Convenience and grocery stores primarily cater to fill-in purchases and impulse buys but lack the assortment depth of supermarkets or the price competitiveness of e-commerce. Other distribution channels, including pharmacies, health food stores, and direct-selling networks such as Amway's Nutrilite, collectively serve niche segments that prioritize expert consultation or brand loyalty. Channel parity is becoming increasingly apparent, with the Nutrition Business Journal (NBJ) forecasting that e-commerce, mass market, and natural specialty channels will each hold approximately equal shares of the market in the coming years. This trend is encouraging brands to adopt omnichannel strategies that align pricing, promotions, and inventory across multiple touchpoints.

Geography Analysis

North America is projected to account for 34.22% of the 2025 revenue, led by the United States' supplement market. This dominance is supported by high per-capita supplement spending, a well-established retail infrastructure, and regulatory clarity provided by the Food and Drug Administration (FDA). However, growth in the region is slowing as market penetration approaches saturation in key demographics. Canada and Mexico contribute smaller shares but are growing rapidly due to the expansion of cross-border e-commerce and retail chains like Walmart and Costco, which have improved product availability. The FDA's Current Good Manufacturing Practice (CGMP) enforcement and added sugars labeling mandate have increased compliance costs, favoring larger manufacturers with dedicated regulatory teams over smaller entrants.

The Asia-Pacific region is expected to grow at a compound annual growth rate (CAGR) of 10.82% through 2031, driven by rising middle-class incomes, urbanization, and increasing e-commerce penetration in countries such as China, India, and Southeast Asia. In China, the National Medical Products Administration (NMPA) requires Blue Hat certification for health foods, a process that demands clinical trial data and takes 18 to 24 months. However, successful applicants gain access to a market where platforms like Alibaba and JD.com drive product discovery and conversion. In India, the Food Safety and Standards Authority of India (FSSAI) introduced nutraceutical regulations in 2022, capping vitamin dosages and prohibiting certain botanical extracts. While these regulations create compliance challenges, they also legitimize the category and reduce grey-market competition. Japan's Ministry of Health, Labour and Welfare oversees the Foods for Specified Health Uses (FOSHU) system, which allows approved gummy formulations to make health claims, setting them apart from general supplements.

Europe's growth is limited by the European Food Safety Authority's (EFSA) strict novel food authorization requirements and fragmented member-state regulations, which complicate cross-border e-commerce. In September 2024, the EFSA issued updated guidance, effective February 2025, requiring relative bioavailability data for new micronutrient sources. This has delayed product launches and increased research and development (R&D) costs. Germany, the United Kingdom, Italy, France, and Spain dominate European sales, with clean-label preferences and organic certifications (EU Organic under Regulation (EU) 2018/848) commanding premium positioning. Additionally, the Health Claims Article 8 working group identified 13 substances, including melatonin, curcumin, ashwagandha, and tryptophan, for potential restriction. This has forced reformulations and created uncertainty for brands with affected stock-keeping units.

Competitive Landscape

The gummy vitamin market exhibits moderate concentration, characterized by a competitive landscape where multinational companies such as Bayer, Nestlé, and Unilever operate alongside specialized supplement manufacturers like Pharmavite and Haleon, as well as direct-to-consumer brands such as Goli Nutrition and MaryRuth Organics. Nestlé's acquisition of The Bountiful Company for USD 5.75 billion, announced in January 2025, highlights the strategic importance of owning diversified product portfolios, including gummy, softgel, and tablet formats. This approach enables companies to facilitate cross-selling opportunities and secure dominance in shelf space within retail environments.

Vertical integration remains a significant competitive strategy in the market. Pharmavite's Project Sunrise, a 225,000-square-foot greenfield gummy manufacturing facility in New Albany, Ohio, completed in late 2024, demonstrates a focus on controlling formulation intellectual property, reducing reliance on third-party toll manufacturing, and accelerating time-to-market for new products. Similarly, Amway's expansion of its Ada, Michigan facility, which added 18,750 square feet for nutrition laboratories and pilot manufacturing with the support of a USD 2 million Michigan Strategic Fund grant, underscores the critical role of research and development infrastructure in maintaining product differentiation and innovation.

Opportunities for growth exist in functional gummies that combine vitamins with adaptogens such as ashwagandha and rhodiola or nootropics like L-theanine and bacopa monnieri. These products target stress management and cognitive performance, which are areas where established players have been slow to innovate. Direct-to-consumer brands are increasingly leveraging social commerce to bypass traditional retail channels. For example, MaryRuth Organics generated over USD 70 million in sales on TikTok Shop through influencer-driven short-form video content that emphasizes product efficacy and ingredient transparency. Amazon's dominance in the online vitamin and mineral supplement market, accounting for 70-80% of sales, creates a highly competitive environment. Top-ranked listings benefit from algorithmic amplification but face challenges such as counterfeit products from third-party sellers, which can undermine quality assurance and brand reputation.

Gummy Vitamin Industry Leaders

Church & Dwight Co. Inc.

Nestle S.A.

Bayer AG

Pharmavite LLC

Haleon plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: TopGum launched OMG3!, a new line of fish-free omega-3 gummies featuring a dual-color, bi-layer design that delivered 50mg of plant-based DHA, prenatal vitamins, and iron in a single chewable, with no fishy aftertaste due to the use of orange essential oil. Using proprietary microencapsulation technology, the gummies achieved high potency and stability while maintaining a pleasant, fruity flavor, according to the brand.

- May 2025: Pharmavite, the maker of Nature Made vitamins, opened a USD 250 million, 225,000-square-foot manufacturing and R&D facility in New Albany, Ohio, creating 225 jobs with future expansion potential. According to the brand, the facility, dedicated to producing vitamin gummies—a category that nearly doubled in size since 2019—expanded Pharmavite’s production capacity and strengthened its research and innovation through the Gummies Innovation Center of Excellence.

- September 2024: SmartyPants Vitamins launched Kids Triple Action Immunity, a science-backed gummy supplement for children featuring vitamin C, D, zinc, and clinically-tested elderberry extract to support immune health. According to the brand, the product contained 67% more nutrients than the leading kids’ immunity gummy, used bioavailable forms for better absorption, and was free from major allergens, GMOs, gluten, and synthetic colors.

- May 2024: Nature Made launched Zero Sugar‡ Gummies, expanding its vitamin and supplement lineup to help more consumers meet their wellness goals without added sugar. According to the brand, the new gummies catered to health-conscious individuals seeking effective, sugar-free supplement options that fit into modern wellness routines.

Global Gummy Vitamin Market Report Scope

Gummy vitamins are chewable dietary supplements designed to resemble gummy candies, available in various flavors, colors, and shapes. The gummy vitamin market is segmented by type, category, function, packaging type, distribution channel, and geography. By type, the market is divided into single vitamin and multivitamin. Single vitamin is further subsegmented into vitamin C, vitamin D3, biotin, and other single vitamins. By category, the market is segmented into kids, adults, and seniors. By function, the market includes immunity, bone and joint health, beauty/skin-hair-nail, digestive health, and other functions. By packaging type, the market is categorized into bottles, stand-up pouches, blister packs, and other packaging. By distribution channel, the market is segmented into supermarkets and hypermarkets, convenience and grocery stores, online retail stores, and other distribution channels. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Single Vitamin | Vitamin C |

| Vitamin D3 | |

| Biotin | |

| Other Single Vitamin | |

| Multivitamin |

| Kids |

| Adults |

| Seniors |

| Immunity |

| Bone and Joint |

| Beauty/Skin-Hair-Nail |

| Digestive Health |

| Other Functions |

| Bottles |

| Stand-up Pouches |

| Blister Packs |

| Other Packaging |

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type | Single Vitamin | Vitamin C |

| Vitamin D3 | ||

| Biotin | ||

| Other Single Vitamin | ||

| Multivitamin | ||

| By Category | Kids | |

| Adults | ||

| Seniors | ||

| By Function | Immunity | |

| Bone and Joint | ||

| Beauty/Skin-Hair-Nail | ||

| Digestive Health | ||

| Other Functions | ||

| By Packaging Type | Bottles | |

| Stand-up Pouches | ||

| Blister Packs | ||

| Other Packaging | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the gummy vitamin market?

The market was valued at USD 10.33 billion in 2026 and is projected to reach USD 16.47 billion by 2031.

Which segment is growing the fastest within gummies by function?

Beauty and skin-hair-nail formulations are forecast to expand at 11.43% CAGR through 2031.

Why are single-vitamin gummies gaining popularity?

Consumers use diagnostics to pinpoint deficiencies, and single-nutrient gummies allow precision dosing with improved shelf stability.

How big is online retail’s role in gummy vitamin sales?

Online channels are expected to post a 10.93% CAGR, with Amazon alone moving around USD 20 billion in supplements in 2025.

What regulatory hurdles do gummy vitamin brands face?

FDA CGMP rules, EFSA bioavailability mandates, and China’s Blue Hat certification extend approval cycles and raise compliance costs.

Page last updated on: