Multivitamin Gummies Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 16.55 Billion |

| Market Size (2031) | USD 22.91 Billion |

| Growth Rate (2026 - 2031) | 6.72% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Multivitamin Gummies Market Analysis by Mordor Intelligence

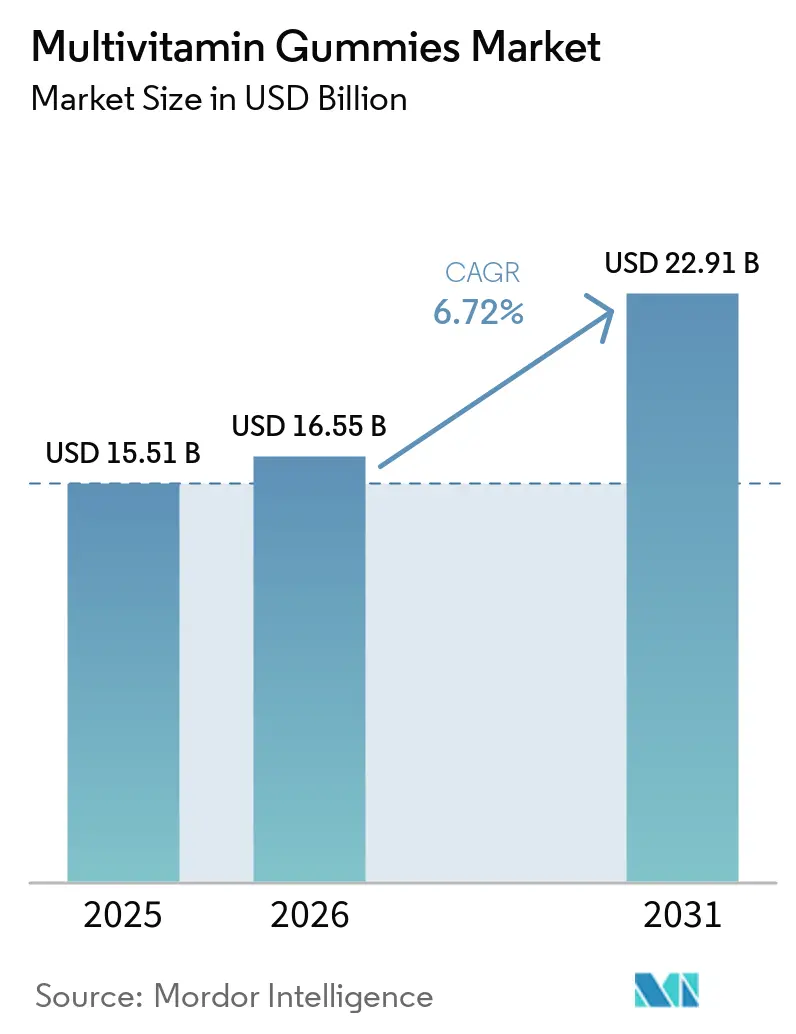

The multivitamin gummies market is expected to grow significantly, increasing from USD 15.51 billion in 2025 and USD 16.55 billion in 2026 to USD 22.91 billion by 2031. This growth represents a compound annual growth rate (CAGR) of 6.72% during the period from 2026 to 2031. The market's expansion is driven by the convenience of gummy formats, rising awareness about preventive healthcare, and consumer preference for chewable products that feel more like candy than traditional medicine. Online platforms, including e-commerce websites and social media-based storefronts, are making it easier for consumers to access high-quality multivitamin gummies. These products often offer a simple way to meet daily nutritional needs with minimal effort. At the same time, regulatory bodies worldwide are introducing stricter rules on sugar content and additives in such products. In response, manufacturers are shifting to healthier alternatives like pectin and stevia to maintain flavor while reducing calorie content. The market is moderately consolidated, with a mix of well-established players and smaller, competitive brands contributing to its dynamic nature.

Key Report Takeaways

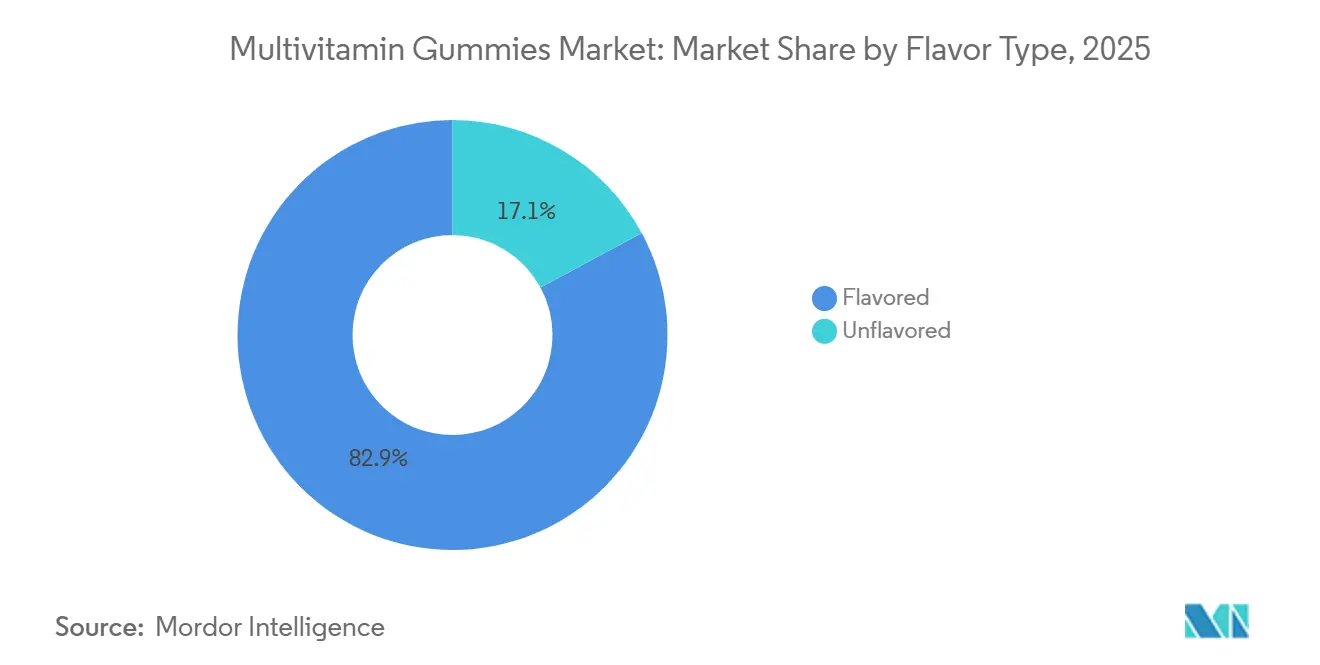

- By flavor type, flavored gummies led with 82.87% revenue share in 2025. Unflavored variants are forecast to expand at an 8.25% CAGR through 2031.

- By end user, women held 37.22% in 2025. Children’s gummies are advancing at a 7.27% CAGR to 2031.

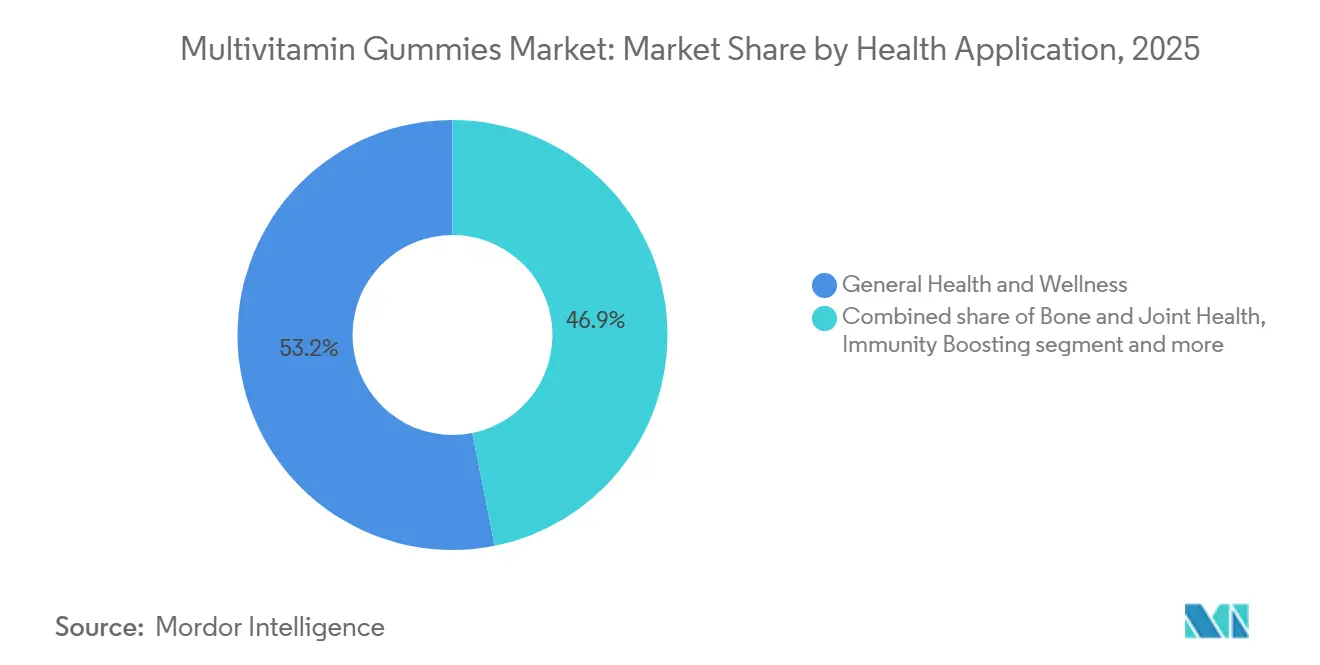

- By health application, general wellness commanded 53.15% in 2025. Energy and metabolism products are projected to grow at a 7.14% CAGR through 2031.

- By distribution channel, drug stores and pharmacies captured 43.27% in 2025. Online retail is growing at a 8.02% CAGR through 2031.

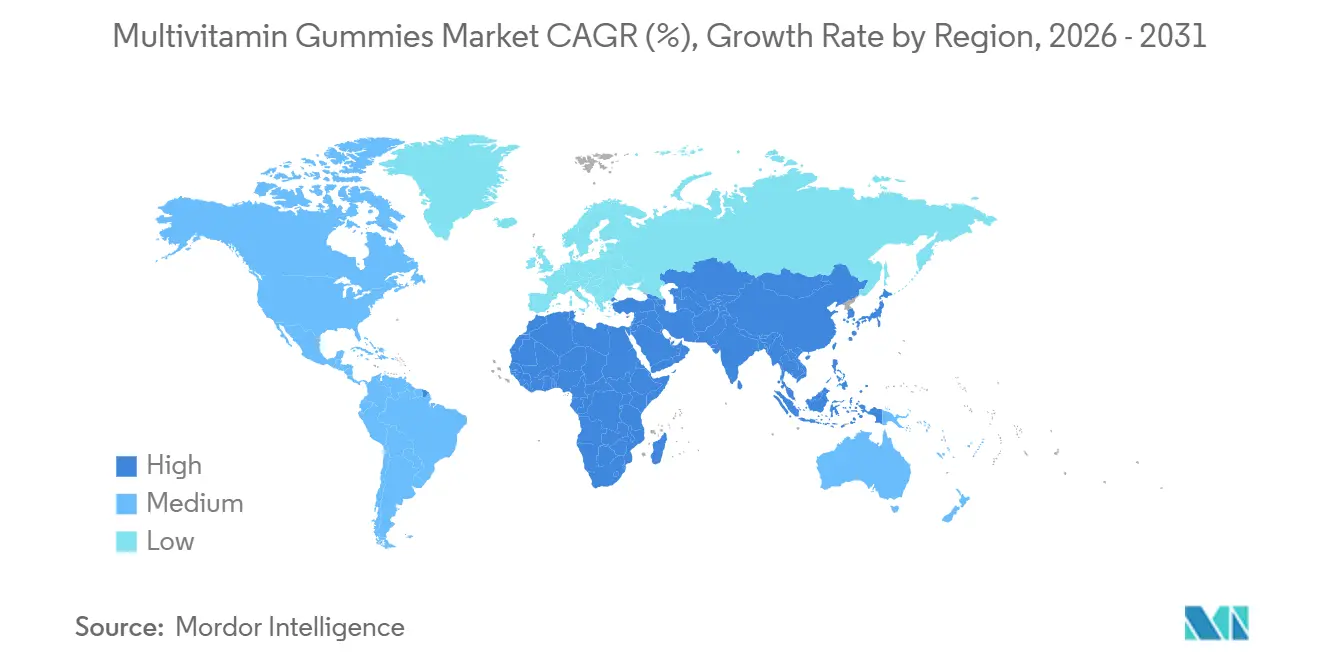

- By geography, North America held 45.63% in 2025. Asia-Pacific is predicted to record a 7.23% CAGR between 2026 and 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Multivitamin Gummies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer focus on preventive healthcare and daily wellness | +1.2% | Global, with strongest adoption in North America and Western Europe | Medium term (2-4 years) |

| Growing prevalence of vitamin deficiencies due to poor dietary habits and sedentary lifestyles | +0.9% | Global, particularly acute in Asia-Pacific and Middle East and Africa | Long term (≥ 4 years) |

| Continuous product innovation, including functional benefits such as immunity, beauty, and sleep support | +1.5% | North America, Europe, and urban centers in Asia-Pacific | Short term (≤ 2 years) |

| Increasing preference for convenient, easy-to-consume formats | +0.8% | Global, with rapid uptake in emerging markets | Medium term (2-4 years) |

| Enhanced taste and sensory appeal of gummies is improving consumer compliance | +0.7% | Global, especially impactful in children's and women's segments | Short term (≤ 2 years) |

| Strong influence of social media and wellness trends | +1.0% | North America, Europe, and digitally connected Asia-Pacific markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising consumer focus on preventive healthcare and daily wellness

Consumers are increasingly focusing on preventive healthcare and daily wellness, driving growth in the global multivitamin gummies market. People are now prioritizing a regular intake of nutrients to stay healthy rather than waiting to treat illnesses. The Global Wellness Institute reported that the U.S. wellness economy reached approximately USD 2.1 trillion as of April 2026, underscoring the trend's significance[1]Source: Global Wellness Institute, "US Wellness Economy Surges to $2.1 Trillion, Cementing Global Leadership", globalwellnessinstitute.org. Multivitamin gummies fit well with this shift because they offer a simple, tasty alternative to traditional pills, making it easier for people to stick to their daily health routines. For example, Bayer AG launched a children’s gummy containing added iron to help address nutritional deficiencies often caused by picky eating. This trend is especially strong in developed countries, where rising healthcare costs and aging populations are pushing people to invest more in self-care and long-term health solutions.

Growing prevalence of vitamin deficiencies due to poor dietary habits and sedentary lifestyles

More people are experiencing vitamin deficiencies due to unhealthy eating habits and less active lifestyles, which is driving the growth of the global multivitamin gummies market. Although programs like food fortification aim to address this issue, many individuals still lack essential nutrients. For instance, the Centers for Disease Control and Prevention (CDC) has identified certain groups at higher risk of vitamin D deficiency. Similarly, the World Health Organization (WHO) has reported widespread deficiencies in key nutrients, such as iron, iodine, and vitamin A, particularly in developing countries. A 2025 study published in ScienceDirect found that up to 84.1% of people in Northern India suffer from vitamin D deficiency, highlighting the severity of the problem in rapidly urbanizing areas[2]. This issue is worsened by factors such as increased consumption of processed foods, changing dietary patterns, and reduced exposure to sunlight.

Strong influence of social media and wellness trends

Social media and digital wellness trends are driving the growth of the global multivitamin gummies market. Online platforms are now a key way for consumers to discover and buy these products. In 2025, about 74% of the global population used the internet, according to the World Bank, significantly increasing the reach of health and wellness content online[3]Source: World Bank, "Individuals Using the Internet (% of Population)", data.worldbank.org. Platforms like TikTok are especially effective at promoting gummy supplements because they highlight their appealing appearance and easy-to-use format. Influencers and user-generated content are helping new brands, such as I Wanna Gummies, quickly gain customer trust and grow their business without relying on traditional retail stores. This trend is particularly noticeable among Millennials and Gen Z consumers, who spend more on wellness products and are heavily influenced by online interactions with brands. These younger generations prefer engaging with brands through digital platforms, making social media a critical tool for market growth.

Continuous product innovation, including functional benefits such as immunity, beauty, and sleep support

Product innovation, especially the addition of benefits such as boosting immunity, enhancing beauty, and improving sleep, is a major driver of the global multivitamin gummies market. Companies are focusing on creating formulations tailored to specific health needs, making these products more appealing to consumers and allowing brands to position them as premium offerings. For example, SmartyPants introduced a prenatal gummy enriched with advanced nutrients, while Nature Made and Swisse expanded their product lines to include gummies targeting probiotics and beauty benefits. Similarly, in September 2025, DaVinci Laboratories launched its first ADK gummy multivitamin, which combines three key nutrients to support bone, heart, and immune health. This reflects a growing trend toward multifunctional and clean-label products that meet diverse consumer demands. The rise of digital platforms and increasing interest in personalized wellness solutions are further fueling this innovation.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High sugar content in many gummy formulations | -0.5% | Global, with regulatory pressure intensifying in North America and Europe | Short term (≤ 2 years) |

| Presence of artificial additives, colors, and flavors | -0.3% | Europe and North America, where clean-label demand is strongest | Medium term (2-4 years) |

| Increasing competition from alternative supplement formats such as powders, effervescent tablets, and functional foods | -0.6% | Global, particularly in fitness and sports nutrition channels | Medium term (2-4 years) |

| Consumer skepticism around actual health benefits and efficacy of gummies | -0.4% | Global, with heightened scrutiny in mature markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High sugar content in many gummy formulations

One of the major challenges in the global multivitamin gummies market is the high sugar content found in many products, especially those targeted at children. Parents are becoming more cautious about the sugar levels in these supplements due to concerns about their impact on dental health, obesity, and long-term metabolic issues when consumed daily. Traditional gummy formulations often include significant amounts of added sugars, which have drawn attention from regulatory bodies like the U.S. Food and Drug Administration (FDA) and the European Food Safety Authority (EFSA). These organizations are working on stricter guidelines for sugar labeling and are considering more rigorous standards for supplements aimed at children. To address these concerns, manufacturers are increasingly developing sugar-free alternatives by using sweeteners such as stevia and erythritol. However, creating sugar-free gummies comes with its own set of challenges, including maintaining the desired taste, texture, and cost-effectiveness. Companies like Tate & Lyle are exploring innovative solutions, such as pectin-based formulations, to overcome these issues.

Presence of artificial additives, colors, and flavors

The use of artificial additives, colors, and flavors is a significant challenge in the global multivitamin gummies market, as consumers increasingly prefer clean-label products made with natural ingredients. Synthetic additives like Red 40 and Yellow 5, although approved by the U.S. Food and Drug Administration, are often viewed negatively by health-conscious consumers. This has pushed manufacturers to replace these synthetic components with plant-based alternatives for coloring and flavoring. However, using natural ingredients comes with its own set of difficulties. These ingredients are more sensitive to factors like heat and light, which can affect the stability and shelf life of the products. As a result, creating formulations with natural components becomes more complex and costly. For example, Vegums uses natural colors in its products but requires stricter storage and transportation conditions to preserve quality, which increases logistical expenses. This issue is even more pronounced in Europe, where stricter regulations by the European Food Safety Authority require companies to reformulate their products to comply with additive restrictions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Flavor Type: Clean-Label Pivot Accelerates Unflavored Growth

The flavored segment was the largest in the global multivitamin gummies market in 2025, accounting for 82.87% of market share. Flavored gummies are widely preferred because they are enjoyable to eat and easy to include in daily routines, especially for children and young adults. These gummies make taking vitamins more appealing by masking the unpleasant taste of certain nutrients. The availability of a variety of flavors and innovative combinations further attracts consumers, making flavored gummies the top choice in the market. Their convenience and taste continue to drive their popularity.

The unflavored segment, while smaller, is expected to grow at a steady CAGR of 8.25% through 2031. This growth is fueled by increasing demand for products with simple, clean ingredients that avoid artificial flavors, colors, or sweeteners. Many health-conscious adults prefer unflavored gummies because they value transparency and minimal ingredient lists. Concerns about sugar intake and dietary restrictions are pushing more consumers toward unflavored options. Although this segment has a smaller share, its growth reflects a shift toward healthier and more natural choices in the market.

By End User: Children’s Segment Leads Growth on Iron Fortification

The women's segment held a notable 37.22% share of the multivitamin gummies market in 2025, driven by growing health awareness and the need for targeted nutrition. Women are turning to multivitamin gummies for benefits like improved immunity, better skin health, stronger bones, and hormonal balance. The availability of products designed specifically for women, along with attractive flavors, has further boosted their popularity. Additionally, as more women join the workforce and focus on preventive healthcare, demand for convenient, effective supplements like gummies continues to rise, making this segment a key contributor to market revenue.

The children’s segment is expected to grow at a CAGR of 7.27% through 2031, driven by increasing parental concern about child nutrition and immunity. Multivitamin gummies are a popular choice for children because they are easy to consume and taste better than traditional tablets or syrups. Parents are also turning to these products to address issues such as nutritional deficiencies and picky eating. Companies are continuously innovating with new shapes, flavors, and added nutrients to make these gummies more appealing to kids. As a result, this segment is expected to grow steadily over the forecast period.

By Health Application: Energy and Metabolism Surge on Functional Positioning

The general wellness segment was the largest in the multivitamin gummies market in 2025, accounting for 53.15% of market share. This segment became popular as more people focused on improving their overall health, including strengthening their immunity, meeting daily nutritional needs, and preventing common illnesses. These gummies are easy to consume and fit well into everyday routines, making them a practical choice for consumers. Additionally, the availability of different flavors and formulations has made them appealing to a wide range of people, helping this segment maintain its leading position in the market.

The energy and metabolism segment is expected to grow steadily at a 7.14% CAGR through 2031. This growth is driven by the increasing demand for products that help boost energy, support metabolism, and assist with weight management. These gummies are particularly popular among working professionals and fitness enthusiasts who need convenient solutions to stay active and energized. The inclusion of ingredients such as B vitamins and adaptogens has driven innovation, leading to new and improved products in this category. As a result, this segment is expected to see consistent growth during the forecast period.

By Distribution Channel: Online Retail Disrupts Pharmacy Dominance

Drug stores and pharmacies made up 43.27% of the multivitamin gummies market in 2025, mainly because they are trusted by consumers and easy to access. People prefer buying from these outlets as they can get advice from pharmacists and choose from a variety of well-known brands. Pharmacies are often seen as reliable sources of health products, which adds to their popularity. Additionally, their convenient locations and customers' tendency to make impulse purchases further boost sales in this segment, making them a key distribution channel in the market.

On the other hand, online retail is expected to grow at a CAGR of 8.02% through 2031, driven by the increasing use of e-commerce and rising awareness about digital health. Many consumers are turning to online platforms because they offer convenience, better prices, and a wider range of products. Features like detailed product descriptions, customer reviews, and subscription options make online shopping more appealing. Additionally, the growth of direct-to-consumer brands and the use of digital marketing are driving online sales. As a result, online retail is set to grow significantly during the forecast period.

Geography Analysis

North America was the largest market for multivitamin gummies in 2025, accounting for about 45.63% of the total revenue. This strong position is due to the availability of a wide network of retail stores and pharmacies, along with consumers' preference for high-quality, premium products. The region is also known for leading in the development of innovative products, such as clean-label and functional options. While the market continues to grow, the pace has slowed as it matures. In the coming years, growth in North America is expected to come from unique and premium products that address specific consumer needs, such as targeted health benefits.

The Asia-Pacific region is expected to grow the fastest, with a CAGR of 7.23% through 2031. This growth is mainly driven by rising incomes and an increasing focus on preventive healthcare among consumers. Urbanization and the expansion of online shopping platforms are making these products more accessible in key markets like China and India. Companies are also introducing products that cater to local tastes and are adapting to changing regulations, which is helping them grow in the region. As a result, Asia-Pacific is expected to gain a larger share of the global market in the years ahead, supported by growing consumer awareness and demand.

Europe is a stable and steadily growing market for multivitamin gummies, supported by strict regulations that ensure high product quality and build trust among consumers. Major markets in the region include Germany, France, the United Kingdom, and Italy, which contribute significantly to the overall market performance. Growth in Europe is expected to remain moderate, driven by demand for scientifically backed and premium products that meet consumer expectations. Meanwhile, South America and the Middle East & Africa currently hold smaller shares of the market but are expected to grow faster due to improving healthcare systems, rising disposable incomes, and increasing awareness about the benefits of multivitamin gummies.

Competitive Landscape

The global multivitamin gummies market is led by well-known companies such as Bayer AG, Church & Dwight Co., Inc., Otsuka Pharmaceutical Co., Ltd., Unilever PLC, and Nestlé S.A. These companies have built strong brands and leverage their wide distribution networks to make their products readily available in stores and online. They regularly update their products with new formulations and packaging to meet changing consumer preferences. Their ability to innovate and maintain a strong market presence helps them stay ahead of competitors.

At the same time, newer brands that focus on online sales are becoming more popular. Companies like Hiya Health and MaryRuth's are targeting specific consumer groups, such as those who prefer clean-label or health-focused products. These brands use social media to connect with customers and often offer subscription services, which help them build loyal customer bases. This growing competition has encouraged traditional companies to improve their online presence and find new ways to engage consumers, making the market more dynamic.

Private-label brands and contract manufacturers are also playing an important role in the market's growth. Companies like TopGum Industries Ltd. are expanding their production capabilities and investing in advanced technologies to meet the rising demand for multivitamin gummies. Retailers are introducing their own private-label products to provide affordable yet high-quality options for consumers. Additionally, advancements in nutrient delivery systems and innovative formulations are driving the growth of premium products, where effectiveness and innovation are key factors in attracting customers.

Multivitamin Gummies Industry Leaders

-

Bayer AG

-

Church & Dwight Co. Inc.

-

Otsuka Pharmaceutical Co., Ltd.

-

Unilever PLC

-

Nestlé S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: TopGum introduced a new women’s health gummy range featuring shatavari and targeted botanicals, designed to support needs such as PMS, menopause, and prenatal health across different life stages. The portfolio includes condition-specific, plant-based formulations with added nutrients like vitamin D and B6.

- July 2025: One A Day introduced One A Day Kids Multi with Iron. This gummy multivitamin provides 12mg of iron per serving, more than any other leading kids' gummy multivitamin, helping address common nutrient gaps in children.

- June 2025: Vitafusion, in partnership with viral chef and former “Bon Appétit” host Brad Leone, launched the new Power Plus Multivitamin. According to the brand, these gummies come in strawberry and watermelon flavors, deliver 100% daily value of ten vital nutrients, including vitamin D3, E, biotin, and folate, and feature softer bite formulas for easier consumption.

- May 2025: Pharmavite, the maker of Nature Made vitamins, has opened a USD 250 million production facility in New Albany, Ohio, marking a major step in its Central Ohio expansion. According to the company, the new site focuses on increasing the production of Nature Made vitamin gummies and includes a Gummies Innovation Center of Excellence dedicated to enhancing R&D capabilities.

Global Multivitamin Gummies Market Report Scope

Multivitamin gummies are chewable supplements that deliver essential vitamins and minerals in a tasty, easy-to-eat form. The global multivitamin gummies market is classified into flavor type, end user, health application, distribution channel, and geography. Based on flavor type, the market is classified into flavored and unflavored. Based on end user, the market is classified into men, women, and children. Based on health applications, the market is classified into general health and wellness, bone and joint health, immunity boosting, digestive health, energy and metabolism, hair, skin, and nail health, and others. Based on distribution channel, the market is classified into supermarkets/hypermarkets, drug stores and pharmacies, online retail stores, and other channels. Based on geography, the market is classified into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market forecasts are provided in terms of value (USD).

| Flavored |

| Unflavored |

| Men |

| Women |

| Children |

| General Health and Wellness |

| Bone and Joint Health |

| Immunity Boosting |

| Digestive Health |

| Energy and Metabolism |

| Hair, Skin, and Nail Health |

| Others |

| Supermarkets/Hypermarkets |

| Drug Stores and Pharmacies |

| Online Retail Stores |

| Other Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Flavor Type | Flavored | |

| Unflavored | ||

| By End User | Men | |

| Women | ||

| Children | ||

| By Health Application | General Health and Wellness | |

| Bone and Joint Health | ||

| Immunity Boosting | ||

| Digestive Health | ||

| Energy and Metabolism | ||

| Hair, Skin, and Nail Health | ||

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Drug Stores and Pharmacies | ||

| Online Retail Stores | ||

| Other Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the global multivitamin gummies market in 2031?

The multivitamin gummies market size is expected to reach USD 22.91 billion by 2031.

Which region is forecast to grow fastest through 2031?

Asia-Pacific is projected to record a 7.23% CAGR, driven by rising incomes, e-commerce adoption, and regulatory harmonization.

Which flavor type is gaining momentum despite a smaller base?

Unflavored gummies are set to grow at an 8.25% CAGR as clean-label shoppers opt for minimal-ingredient products.

Why are children’s gummies considered a high-opportunity segment?

Iron-fortified and sugar-reduced formulations are anticipated to drive market growth at a CAGR of 7.27%, supported by 92% daily compliance rates observed in pediatric trials.

Page last updated on: